This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

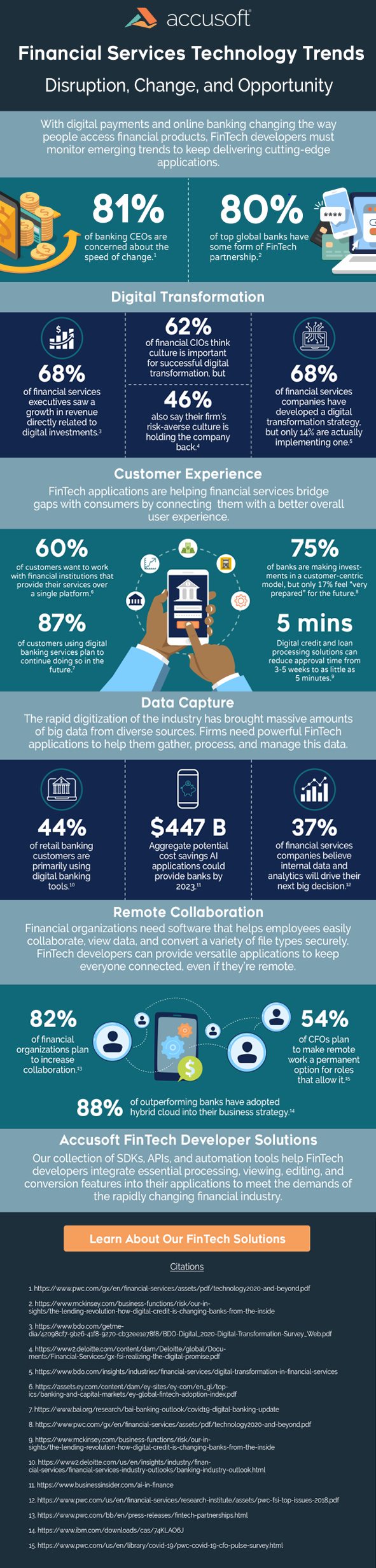

Accusoft researched several of the factors driving technology and innovation in the financial services industry to better understand the current and future role of FinTech in the marketplace. Find out what they learned, discover assets that can help you solve your content processing, conversion, and automation challenges, andlearn more about their FinTech solutions >>

AI marketing expert Micronotes recently launched a refinancing tool that will help consumers reorganize their debt, while enabling banks to lower their borrowing costs and boost customer retention.

The new tool builds on Micronotes’ ReFi solution it launched last June. The credit marketing automation suite enables banks to leverage AI to help their clients automatically identify refinancing opportunities for a range of consumer debt, including auto loans, personal loans, student loans, credit card debt, and mortgages.

With today’s advancement of ReFi, Micronotes is teaming up with Experian to leverage the firm’s database of consumer credit profiles. Experian will compare the bank’s current lending criteria to the consumer’s credit profile, and then synthetically refinance the customer’s existing debt held elsewhere while identifying other refinancing opportunities.

“We’re thrilled to partner with Experian to leverage artificial intelligence and data to help consumers lower their borrowing costs,” said Devon Kinkead, founder and CEO of Micronotes. “With an estimated $2 trillion in mispriced debt, during an era of persistently low interest rates, we help digital banking customers see where they’re overpaying interest that can be refinanced with a lender they know and trust — their primary financial institution.”

Micronotes’ personalization expertise comes in via the customer communication piece. The company will send the customer a message in the digital banking channel that informs them of the potential savings. Using Micronotes’ technology, the customer can respond to the message using preset, customizable quick-response buttons that range from “remind me later” to “chat with a banker.”

This quick-response messaging system is Micronotes’ bread and butter. The company was founded in 2008 to help financial institutions start conversations with their customers in a non-invasive way. At the company’s most recent Finovate appearance, FinovateSpring 2013, Micronotes showed off its cross-sell feature that uses predictive analytics to bring the branch sales process into the digital channel.

Headquartered in Boston, Massachusetts, Micronotes has raised $12.2 million.

One of the biggest impacts of COVID-19 in the financial services world has been to invigorate the relationship between banks and fintechs. This week’s news that Berkshire Bank has turned to cloud-based document management solution providerCirrus to help it manage financial relief efforts for small businesses is another example of this trend.

“Cirrus’ portal plays a key role in expediting the process of managing SBA loans, enabling Berkshire Bank to collaborate remotely, execute rapidly, and scale quickly to efficiently address the influx in loan requests and alleviate the document chaos associated with SBA lending,” Cirrus founder and CEO David Brooks explained.

Challenged with a massive inflow of SBA loan requests, including 942 Paycheck Protection Program loans on the program’s first day, Berkshire Bank will also benefit from real-time transparency into the progress of each loan. The combination of automation and greater visibility via the integration make the overall lending process faster and more efficient, for both the bank and the customer.

This capacity, Brooks noted in an article written last month, is important. But so is scalability and the ability of businesses and the solutions they depend on to react and adapt to new potential challenges. “With a new administration in place, it is uncertain what additional relief programs may be on the horizon,” Brooks wrote. “By taking time to evaluate existing technology and operational workflows to ensure they are configurable and scalable to support PPP, financial institutions will be better positioned to accommodate future programs.”

Headquartered in Evergreen, Colorado, Cirrus works with banks and other businesses to help them better manage the document processing needs of their commercial and small business accountholders during onboarding and when seeking financing. The company made its Finovate debut last year at our all-digital conference, demonstrating version six of its front-end document management solution.

Founded in 2018, Cirrus includes The FIS FinTech Accelerator in Partnership with The Venture Center and Queen City Fintech among its investors.

Berkshire Bank operates 130 branch offices in New England and New York, and has $12.9 billion in assets. The bank is owned by Berkshire Hills Bancorp, a Boston, Massachusetts-based bank holding company.

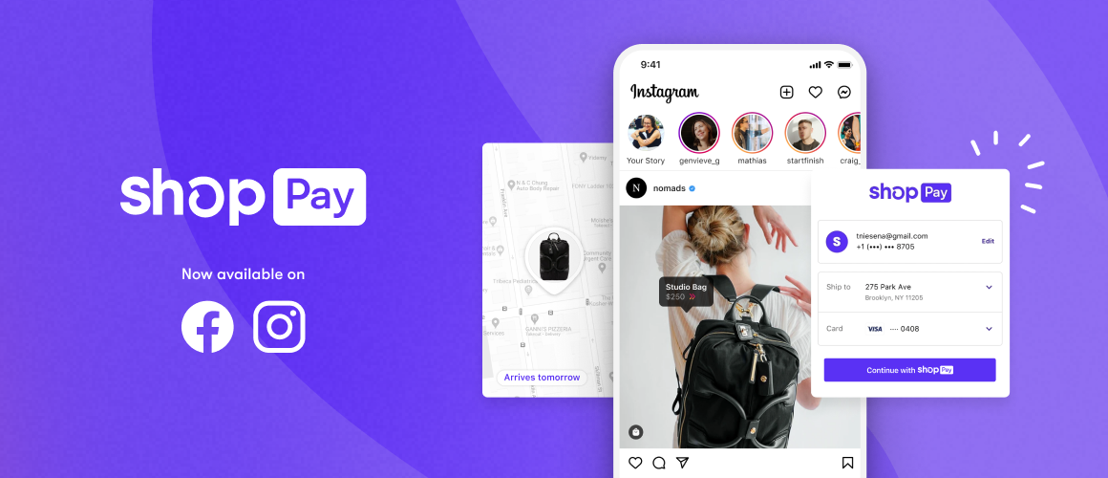

As social commerce rises, e-commerce platform Shopify is getting in on where the action is happening. The company announced today it is bringing its Shop Pay checkout and payment processing system to Instagram users and Facebook Shops.

This builds on the existing payment methods available to these Facebook-owned social platforms. Previously, shoppers had the option to either pay with PayPal or manually enter their payment card credentials.

Shop Pay, on the other hand, stores users’ payment card and shipping information to make the embedded payment experience as seamless as possible for the end customer. Prior to today, Shop Pay was only available to Shopify’s e-commerce store clients, including brands such as Allbirds, Kith, Beyond Yoga, and Jonathan Adler.

Shop Pay has 60 million users and last year helped buyers complete more than 137 million orders. This is small compared to PayPal’s 377 million active users. Shopify, however, is aiming to gain an edge by targeting the millennial customer base by offering carbon offset options that allow merchants and customers to offset the carbon emissions of their deliveries.

“People are embracing social platforms not only for connection, but for commerce,” said Carl Rivera, General Manager of Shop. “Making Shop Pay available outside of Shopify for the first time means even more shoppers can use the fastest and best checkout on the Internet.”

As for what’s next in the Shopify-Facebook tie-up, Rivera said to expect more collaboration in the future. He added, “…we’ll continue to work with Facebook to bring a number of Shopify services and products to these platforms to make social selling so much better”

The ecommerce tools are available for Instagram users today and will be available for U.S. Facebook Shops in the coming weeks.

The decentralized finance (DeFi) conversation started to pick up about a year ago. Today, we’re starting to see this once-fringe topic emerge as a mainstream conversation in fintech.

In fact, now that DeFi has become a reality, it’s not something that’s going away any time soon. The advent of cryptocurrencies enabled consumers to transfer money between parties without relying on a traditional bank. DeFi takes this power the next level.

These added capabilities are what have the potential to take cryptocurrencies from a speculative device to a useful tool. But while this is a reality for some, it is still a concept on paper for most. So why am I paying attention to DeFi now, while it’s still in its infancy?

It’s more than an idea

As mentioned above, DeFi has moved from the concept of “an interesting idea” into a concrete, value-added financial tool. Leveraging the power of smart contracts, DeFi allows users to lend, earn interest, and claim insurance. It can also be used to prove identity, assist with underwriting, AML and KYC compliance, and more.

Because of these capabilities, the use of DeFi is becoming more popular. The following graphic from DeFi Pulse shows the total U.S. dollar value locked in DeFi. The graph shows DeFi starting to take off in July of last year and rise exponentially. Today, the total locked value is more than $35.9 billion.

With this growth, we can expect to see more projects and use cases launch as DeFi emerges from an idea to a new reality.

DeFi will change banking as we know it

Today’s traditional banking system relies on centralized control. But one of the key aspects of DeFi is that it operates without an intermediary. That is, users can complete banking activities without a central governmental authority, a bank, or even a company setting rules, governing, and regulating activity.

Instead of this central control, DeFi leverages smart contracts that use “oracles,” or services that inform smart contracts of external data so that it can execute its purpose based on that data. As an example, a smart contract for flood insurance might rely on rain gauges to determine whether or not to pay out insurance claims to homeowners living in a certain area.

This key difference will change how consumers shop for financial services. Instead of hinging on trusting an institution, the consumer’s decision will rely on how smart they think the smart contract is, and whether or not they trust the oracles the smart contract uses.

It will transform the industry for the better

While DeFi is a little bit intimidating, it has the ability to change the financial world for the better. It is scalable and programmable, and is therefore well-suited for growth. In addition, it is immutable. That is, it is tamper-proof and cannot be changed or hacked. And transaction details are transparent; DeFi protocols are built with open source code and can be viewed by anyone.

The final, and perhaps most notable, aspect of DeFi is that it is permissionless. This means that anyone with a crypto wallet and an internet connection can participate in the DeFi economy. There is no minimum balance requirement and, because it doesn’t revolve around a central government, there are no geographic limitations.

Two weeks after announcing its purchase of Cardtronics, fintech hardware giant NCR is acquiringTerafina, a company known for its digital account opening and onboarding tools.

Financial terms of the agreement were not disclosed.

NCR will tap Terafina’s expertise to expand NCR’s sales and marketing capabilities in its Digital First Banking Platform. The offering, which can be tailored to fit institutions ranging in size from large banks to community banks and credit unions, provides an API-led approach to digital banking that can be hosted or deployed on-premise to help banks lower costs and speed up their innovation cycle.

Last year increased the urgency for financial services companies of all kinds to improve their digital customer experiences. Founded in 2014, Terafina suits this need. The company offers a software-as-a-service solution that offers digital onboarding tools and helps banks and credit unions synchronize their branch, call center, and digital operations to provide a consistent user experience across channels.

At FinovateSpring 2019, Terafina Founder and CEO Meheriar Hasan showcased the company’s digital sales platform that helps banks address the needs of their small business clients.

“Digital Banking is a key aspect of the NCR-as-a-Service strategy we laid out at Investor Day in December,” said NCR CEO Michael D. Hayford. “Terafina has been a partner of ours and is already up and running, integrated with our Digital Banking platform. We know this adds value for our clients by making digital account sales, marketing and onboarding easier, so they can provide a superior experience for customers.”

Today’s deal marks NCR’s 29th acquisition since it was founded in 1884. NCR’s purchase of Terafina fits with the company’s strategy to purchase early stage companies to boost its product capabilities and enhance its leadership.

NCR is headquartered in Atlanta, Georgia, and counts 36,000 employees across the globe. The company is listed on the New York Stock Exchange under the ticker NCR and has a market capitalization of $4.81 billion.

A just-announced partnership between two Finovate alums – Mambu and Signicat – will bring digitized identity management services to banks, fintechs, and financial service providers across Europe. The collaboration between the SaaS banking platform and the digital identity company is designed to help institutions in the region leverage innovations in identity management to boost customer acquisition, enhance the customer experience, and defend against identity fraud.

The single-API integration between Signicat’s identity platform and Mambu will enable users to apply a variety of digital identity verification solutions to a range of processes, including onboarding, identity authentication, and e-signatures. In their joint statement, both companies highlighted abandonment as one challenge the new integration will help companies meet. They noted that 63% of consumers in Europe quit at least one financial app in the last year, citing research conducted by Signicat.

At the same time, the integration also will help companies deal with the new environment for cybercrime, particularly identity fraud, which has flourished in the work-from-home, COVID-19 era. “Identity fraud continues to be a major threat to businesses across the globe and damages trust,” Mambu Managing Director for EMEA Eelco-Jan Boonstra said. “And with everyone working from home – the COVID-19 pandemic has only accelerated this. Therefore financial service providers are relying on customer trust and loyalty more than ever.”

Asger Hattel, who took over as Signicat’s CEO in January of last year, underscored the way the pandemic had accelerated pre-existing trends toward digitization. “Global lockdowns have turned a desire for digital services into an urgent need,” Hattel said. “Our research into consumer attitudes towards onboarding show that financial service providers are struggling to keep up with consumer’s digital demands – and it is costing them customers.”

Mambu’s partnership with Signicat comes in the wake of the Mambu’s $132+ million (€110 million) fundraising last month – which brought the company’s total valuation to more than $2 billion (€1.7 billion). Also last month, Mambu announced the addition of new Chief Financial Officer Langley Eide. Founded in 2011 and headquartered in Berlin, Germany, Mambu is an alum of both our Finovate conferences – debuting in 2013 at FinovateAsia – and our event for developers and engineers – FinDEVr New York, in 2016.

Based in Trondheim, Norway, Signicat specializes in providing identity assurance worldwide, enabling banks to leverage existing customer identity to accelerate onboarding, improve access to services, and connect users, devices, and more across channels and markets. A Finovate alum since 2017, Signicat has raised $8.8 million in funding from investors including Horizon 2020, Viking Venture, and Secure Identity Holding.

Upcoming webinar Title: Biometric authentication for SCA and beyond: the art of the possible Date: Wednesday, March 03, 2021 Time: 03:00 PM Central European Time Duration: 1 hour

The PSD2 requirement for Strong Customer Authentication, combined with Mastercard’s mandate on biometrics, has led to an increase in the deployment of biometrics as one of the 2 factors of authentication. A strong preference from consumers for its ease of use is also driving adoption.

Join this webinar, with BNPP Personal Finance, Mastercard, and Fabrick, as they share their experience of deploying ID Check Mobile (IDCM), MasterCard’s biometric authentication solution for online payments.

The expert panel will tackle the topics including how the solution can help issuers meet regulatory requirements and how biometrics can deliver additional value-added services to maximize return on investment. The speakers will take time during the discussion to answer questions from the audience – so use this time to get your queries and thoughts addressed.

Featuring:

Moderated by: Julie Muhn, Analyst, Finovate

Stephanie Chlala, Project Manager, Payments, BNPP Personal Finance, France

Digital corporate banking solutions company CoCoNet Softwareannounced a new CEO today. Mark Lohweber is now heading up the company, taking the reins from former CEO Björn Hassing, who will transition to serve as the company’s CTO.

Lohweber will head up CoCoNet’s board of directors, which also consists of Hassing and company CFO and COO Axel B. Wiethoff.

“In corporate banking, many banks have great potential for process and portfolio optimisation through digitalisation”, said Lohweber. “CoCoNet already offers outstanding solutions in this area. That is why I am very happy, together with Axel, Björn and the entire CoCoNet team, to be a strong partner in digitalisation for the banking sector.

Lohweber comes to CoCoNet after leading the banking business unit at IT service management company adesso for 13 years.

Founded in 1984, CoCoNet provides digital banking solutions to banks, with a customer lineup including Citi, GarantiBank, HSBC, ING, JPMorgan, KBC, and UniCredit.

At FinovateWest 2020, the company demonstrated its digital onboarding solution. The solution is tailored to corporate customers and is designed to suit the complex needs of this segment.

Can cryptocurrencies play a role in bringing the benefits of modern – or even post-modern – finance to underserved African American communities? Is it possible that bitcoin could be the key to enabling black Americans to close with wealth gap with their non-black fellow citizens?

Provocative as it sounds, this is the thesis of Isaiah Jackson, co-founder of KRBE Digital Assets Group. Jackson’s book Bitcoin & Black America makes the case that a cryptocurrency like Bitcoin has a number of features that make it an important ingredient in the kind of economic independence he believes would benefit black Americans. In an interview with Forbes’ Jason Brett last summer, Jackson noted that during the golden era of black-owned banking in the United States – the Reconstruction Period after the Civil War – the existence of multiple currencies played a significant part in supporting the development of community-based financial institutions. This, in turn, helped build the first black middle class in the U.S.

Jackson sees Bitcoin playing a similar role today. He approves of both Bitcoin’s deflationary nature, which he says encourages savings over spending, and its “circular economy” which – not unlike the economy of 19th century black banking – exists significantly outside of a traditional banking system Jackson decries as racist.

With a background as a computer scientist, as well as a Bitcoin consultant and trader, Jackson is nevertheless wary about a future in which Bitcoin and other cryptocurrencies are common. To the extent that human nature endures, discriminatory practices like redlining, in his opinion, are likely to follow us into our digital future – with the moral (or immoral) panic of the day incentivizing regulators to monitor and restrict certain digital currency transactions from certain people or communities. And if history is any guide, the negative impacts of these restrictions are most likely to fall on those least able to manage them.

Nevertheless, when it comes to the potential for Bitcoin to make a difference for black Americans, Washington is a believer. “For the first time in history,” Washington told CNBC in an interview last month, “we have a Plan B option to the current financial system which has seen years of redlining, racial discrimination, and other egregious acts by retail banks to the Black community.”

The second edition of Bitcoin and Black America is currently available via pre-order. The new edition features seven additional chapters including information on Bitcoin specifically for small business owners, as well as a roster of more than 200+ black professionals working in the Bitcoin industry.

The rise of insurtech – entrepreneurs and innovators looking to do for insurance what fintechs have done for financial services – is a global phenomenon. And one of the areas where insurtech is beginning to take hold is Vietnam. The country experienced a fintech mini-boom from 2017 to 2019 which, among other things, helped put the country’s nascent insurtech market on the map. This week’s Finovate Global Lists shares Fintech News Singapore’s roundup of insurtechs operating in the APAC market of Vietnam that are leveraging everything from mobile to machine learning to bring digital insurance to the more than 97 million citizens of the country.

INSO. Founded in 2018. Headquartered in Hanoi, INSO offers insurance products online as well as the ability to make claims online. The company was among the first in the country to offer flight delay insurance. Vũ Nguyễn Thuỳ Vân is CEO.

OPES. Founded in 2018. Headquartered in Hanoi, OPES Insurance Joint Stock Company is a pioneer in Vietnam’s digital insurance industry. OPES specializes in providing personalized insurance solutions to empower customers rather than brokers.

Papaya. Founded in 2018. Headquartered in Ho Chi Minh City, Papaya offers a one-stop shop for employee benefits to promote health and wellness. Hung Phan is co-founder and CEO.

Save Money. Founded in 2013. Headquartered in Ho Chi Minh City, Save Money is a B2B2C digital insurance platform for banks, hospitals, and telecommunication companies. Trần Quang Ninh is founder and CEO.

Wicare. Founded in 2018. Headquartered in Hanoi, Wicare is a lifestyle insurance company that leverage gamification to boost engagement and encourage customers to exercise. Quang Ngoc Nguyen is founder and CEO.

It’s been more than two years since Finovate launched its first conference on the African continent. In that time, we’ve seen a number of alums from FinovateAfrica in the fintech news headlines: Best of Show-winning digital wealth technology company Bambu raised $10 million, credit decisioning solution provider RISQ teamed up with Aion Digital, and this week, small business solution provider Yoco, headquartered in Cape Town, South Africa, reported that it has reached a major milestone: more than 120,000 small businesses served.

“Through our platform and the results of a recent merchant survey, we have seen up to a 90% decrease in in-person transactions since the lockdown began,” Yoco CEO told TechGist Africa last year when it launched a trio of new payment solutions to support online transactions for small businesses. “We knew that the best way to support our merchants was to develop products that would enable them to do business online and keep money coming in through this period.”

This week for Finovate Global Voices we present Bradley Wattrus, Yoco CFO and co-founder, and Clayton Brett, Capital Product Owner, demoing the Yoco Capital solution for SMEs at FinovateAfrica 2018.

Here is our look at fintech innovation around the world.

Asia-Pacific

South Korea’s Financial Services Commission (FSC) announced plans to expand its open banking ecosystem, which launched in December 2019. The goal initially is to support the use of contactless financial services, with the inclusion of financial investment companies to follow.

Banking-as-a-service company NymCard secured $7.6 million in Series A funding in a round led by Shorooq Partners. Based in Abu Dhabi, NymCard has raised a total of $12 million in capital.

A partnership between Mastercard and subscription-based payments firm Sokin will bring the company’s fixed-price currency exchange services to markets in India, Sri Lanka, Bangladesh, Nepal, and the Maldives.

Flink, Mexico City-based stock trading platform for retail traders, secures $12 million in funding courtesy of a Series A round led by Accel.

Latin American financial receivables marketplace Monkey raised $6 million in Series A funding. Quona Capital and Kinea Ventures co-led the round for the Sao Paulo-based startup, which was founded in 2016.

Investment platform Stashannounced a new round of financing today. The $125 million Series G round boosts the company’s total funding to over $427 million.

Eldridge led the round, which received additional funding from new and existing investors, including Owl Ventures, funds advised by T. Rowe Price Associates, Goodwater Capital, Entree Capital, and others.

The funding comes after a year of record growth for Stash, which was founded in 2015. Last year, the New York-based company saw a 100% increase in account openings. It now has five million customers and $2.5 billion in assets under management. Fueling this increase was the boost in automated deposits; Stash reported a 50% increase in the number of customers automating their investments last year.

Stash’s investment platform democratizes long-term investing by making the process easier and more affordable. “We believe in tried and tested principles of regular, long-term, and balanced investing as the key to building wealth. We therefore built Stash to make diversified investing easy, affordable and accessible, backed by personalized advice and accessible education—in order to avoid the pitfalls of short-term speculation and day-trading,” said Stash Co-Founder and CEO Brandon Krieg. “This new round of funding enables us to take this mission to millions more Americans.”

Stash’s newest upcoming product, Smart Portfolios, helps customers build long-term, diversified portfolios that are fully managed by Stash. The new offering is made for users who want to invest, but don’t know where to start. To keep things simple, Stash uses a subscription model instead of charging fees based on portfolio size. The Smart Portfolios product is included in Stash’s Growth and Plus subscription plans, which cost $3 per month and $9 per month, respectively.