This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Yesterday, Mastercardunveiled two new clients for its Mastercard Track Business Payment Service. The New York-based payments giant announced that BMO and Moneris Solutions Corporation have joined Mastercard Track.

Mastercard launched the new service for Canadian businesses earlier this year. Mastercard Track creates efficiencies for business users by simplifying and automating the exchange of payments data between buyers and suppliers. The service seeks to modernize the $135 trillion B2B payments market.

“Current business payment processes often require manual reconciliation work that can be very labour intensive,” said Sasha Krstic, President of Mastercard in Canada. “The availability of Mastercard Track through our new partnerships with BMO and Moneris will help Canadian businesses gain freedom from an inefficient process by simplifying and automating the exchange of payments to make B2B payments work harder, faster and smarter.”

Using Mastercard Track will help BMO and Moneris modernize the business payments process for their customers. Ultimately, the service will free up working capital for businesses by offering them more control of their payments and helping them to optimize cash flow management.

Derek Vernon, Head of Payments Modernization of BMO’s North American Commercial Deposits and Corporate Card division said that the service “enhances the digital experience by offering a universal solution to simplify and automate B2B payments.” Specifically, Vernon noted that Mastercard Track will help reduce supplier friction and facilitate quicker speed-to-spend.

Mastercard is a public company listed on the New York Stock Exchange under the ticker MA. It has a market capitalization of $364 billion. Michael Miebach took the helm of the company as CEO in January of last year.

Latin American payments company EBANX is doubling down on its commitment to its business in Mexico, opening its first office in Mexico City and introducing a range of solutions designed to help Mexican companies offer new payment experiences for their customers in-country. These solutions include credit and debit cards, installments, OXXO and OXXOPay, SPEI, and digital wallets like Mercado Pago.

“The launch of these local solutions and the opening of the new office are part of our strategy for continuous growth in Mexico, a country where e-commerce is one of the most dynamic and relevant sectors,” EBANX co-founder and CEO João Del Valle said. “With these new initiatives, we became the ideal strategic ally to help e-merchants grow their operations in Mexico or other LatAm markets.”

For EBANX, bringing broader payment options to Mexican consumers is a way to better serve the country’s unbanked population. According to the Association of Mexican Banks, 53% of Mexican adults not have a bank account as of 2020. At the same time, the company’s own study on digital commerce in Mexico revealed that as much as 60% of the digital commerce in Mexico is conducted using payment methods ranging from digital wallets and cash vouchers to debit and credit cards. By enabling more merchants in Mexico to process both cash-based transactions as well as these methods preferred in digital commerce, EBANX believes it can help merchants in the country increase their reach and sales potential by 2x and increase their total addressable market faster.

Founded in 2012 and headquartered in Curitiba, Brazil, EBANX has been active in the Mexican market since 2015. Last year, the company grew the number of transactions processed in Mexico by 115%. Hibobi, SHEIN, Shopee, and Wish are among EBANX biggest customers in the country.

The acquisition is slated to take place in two parts. First, Itaú will acquire 50.1% of the share capital of Ideal, which was founded in 2019 and is one of the leaders in traded volume on the Brazilian stock exchange, B3. Second, the bank plans to execute its right to purchase the remaining 49.9% of the brokerage’s shares for approximately $117 million (R$651 million) securing control of the company. Stage two of the acquisition plan is reportedly not scheduled to take place for another five years.

“This investment materializes our mantra of client centrality because they are the ones who will get the most out of the transaction,” Itaú Unibanco president Milton Maluhy Filho said. “Ideal is going to help us expand and standardize the offer for different channels. Customers from various segments of the bank, such as iti, ion, or even Itaú Corretora, will be able to have access to the same products on whichever platform they prefer.”

The acquisition will add to the talent base for the 60-million customer financial institution, which bills itself as a digital bank with the convenience of physical banking. Ideal CEO Nilson Monteiro will continue to oversee operations at the company with Itaú serving essentially as one of Ideal’s financial institution clients. Itaú Unibanco’s Carlos Constantini, who runs Wealth Management and Services for the bank, underscored the importance of maintaining Ideal’s autonomy, citing the company’s market position and “well-defined strategy for its segment of activity.” Constantini added, “the company will play an important role in consolidating Itaú Unibanco’s investment ecosystem and maintaining our market leadership.”

Founded in 2008 via the merger of Banco Itaú and Unibanco, Itaú Unibanco is headquartered in São Paulo, Brazil. With total assets of more than $377 billion and 90,000 employees, Itaú Unibanco is the largest private sector bank in the country. The institution is publicly traded on the Brazilian stock exchange and has a market capitalization of $41 billion.

FinovateEurope 2022 is right around the corner. If you are an innovative fintech company with new technology to show, then there’s no better time than now and no better forum than FinovateEurope. To learn more about how to demo your latest innovation at FinovateEurope 2022 in London, March 22-23, visit our FinovateEurope hub today!

Here is our look at fintech innovation around the world.

A partnership between India-based private sector bank RBL Bank and Google will enhance the customer experience and potential for expansion for its digital platform Abacus 2.0.

FundThrough noted that the deal is designed to accelerate both its commitment to embedded finance as well as fuel expansion plans for the U.S. market. Specifically, FundThrough believes the acquisition of its American rival will enable it to increase its U.S. clientele by 2x, boosting the number of customers in the States who use its technology to turn unpaid invoices into access to working capital.

“We are committed to helping small businesses grow and thrive – especially those who sell to large customers where long payment terms and a lack of financing options stand in the way of growing a business,” FundThrough co-founder and CEO Steven Uster said. “BlueVine was one of our biggest competitors in the U.S. market, and through this acquisition we can fulfill our mission on a much larger scale.”

With growth of more than 10x since its founding in 2014 and 3x growth over the past year, FundThrough has scaled to process more than $120 million in funding each month. The company’s AI-powered funding platform, along with its partnerships with companies like Intuit and Enverus, has enabled it to cut the standard amount of time it takes for SMEs to get their invoices paid by as much as 97%.

Invoice factoring was BlueVine’s founding business – and the centerpiece of the company’s 2014 Finovate presentation. The company has grown significantly since then, adding a range of new financing solutions for small businesses and giving the Redwood City, California-based fintech the ability to choose which area of small business financing it will focus on going forward.

“Since launching BlueVine, we’ve been focused on the financial needs of small businesses and are very proud of what we’ve been able to accomplish,” BlueVine co-founder and CEO Eyal Lifshitz said. “As we evolve our products and services, we continuously examine how we can better serve our customers at scale. We determined that FundThrough is perfectly positioned to serve our factoring clients with the care and individual attention they need and deserve. Our factoring clients will be in great hands with FundThrough.”

As part of the acquisition, BlueVine’s invoice funding division employees will join the FundThrough team. The transaction will enable BlueVine to focus on other elements of its business including its BlueVine Business Checking, Payments, and Line of Credit offerings. Since inception in 2014, the Redwood City, California-based fintech has helped SMEs access more than $14 billion in financing.

Consumer credit reporting agency TransUnion is moving in the direction of Web3. The Illinois-based company announced this week it will bring off-chain consumer credit, identity, and compliance information to public blockchain networks.

The move is made possible via a partnership with Spring Labs, a company that offers decentralized infrastructure for credit and identity data. Spring Labs allows network participants, such as financial institutions, to share information about credit and identity data without needing to share the underlying data itself. Specifically, TransUnion will bring its VantageScore to Spring Labs’ ky0x Digital Passport, a tool that enables blockchain and smart contract applications to access off-chain data sources to create new, permission-controlled decentralized Web3 services and applications.

“We believe in the growth potential of DeFi,” said TransUnion President of U.S. Markets and Consumer Interactive Steve Chaouki. “Providing credit and identity data on-chain is a huge step towards improving the financial products available in the space. Working with Spring’s ky0x, we now have a solution for users to control and share their data on blockchain in a privacy-preserving way, enabling them to safely interact with a broader set of financial products.”

Transporting consumer credit data to the blockchain allows users to offer up information about themselves while maintaining privacy and anonymity of their identity. This secure data sharing allows users to access smart contract applications and helps DeFi and Web3 apps to scale.

Ultimately, the move should benefit both end users and lenders. By having their credit score available on-chain, users can receive better interest rates from DeFi lenders. Simultaneously, DeFi lenders can reduce their risk.

“Enabling access to an industry-standard, trusted credit risk score like VantageScore on-chain and in a consumer permissioned, anonymous way opens the door to greater growth and financial inclusion in the DeFi space,” said TransUnion SVP Consumer Lending Business Leader Liz Pagel. “Paired with ky0x’s AML and KYC capabilities, DeFi lenders can transact with confidence at lower rates, potentially paving the way for lending without the over-collateralization that is standard today.”

To be honest, there is a potential downside to this partnership. Traditional credit scores are prone to racial bias and have negative consequences for borrowers who have no established credit. By porting this imperfect risk underwriting model to the decentralized world, we may be doing ourselves a disservice.

Headquartered in New York City, Tern is a fintech as a service innovator dedicated to enabling startups and established financial institutions alike to launch embedded banking and payments services products. The company, founded in 2015 by CEO Brion Bonkowski, offers a multi-currency, multi-language prepaid and stored-value platform with embedded AML, KYC, CIP, and fraud mitigation solutions.

We caught up with Brion to discuss a variety of critical topics in fintech – from the power of embedded finance and the future of neobanks, to the rise of BNPL and the challenge from Big Tech and Big Retail. We also discussed how Tern enables more companies to fulfill the promise of the banking as a service (BaaS) phenomenon.

What problem does Tern solve and who does it solve it for?

Brion Bonkowski: Tern is a fintech infrastructure company that exists to help virtually any company launch fintech products. Launching fintech products is hard and expensive. Anyone who has done it before knows the pains of contracting with banks, processors, and networks. Combined with long project timelines, these obstacles sadly prevent many programs from ever launching.

The emergence of Banking as a Service (BaaS) was the market’s initial reaction to try and serve this need. It was a way to package program management, processing, and banking under one roof. But BaaS had a narrow mandate aimed at serving startups for the most part when, in reality, the number and type of companies interested in launching financial services offerings is much broader.

Tern is the next evolution of BaaS in that we’re building tools that allow virtually any type of company to launch fintech products. This could include an early stage fintech startup, a legacy fintech, or a big global brand that wants to provide value-added financial services products to their existing customer bases. By offering no code (white labeled UX), low code (embeddable widgets), u code (API) options, we are striving to be every company’s answer to launching fintech products quickly and compliantly.

The rise of embedded finance has been one of the biggest trends in fintech of late. How do you see this trend evolving in 2022?

Bonkowski: We see a definite trend with more traditional enterprise players launching embedded finance applications, aiming to add stickiness to their service offering and additional lines of revenue to increase ARPU (average revenue per unit). The problem is, it is really hard to prototype, A/B test, and launch pilot programs to test a particular thesis in the market. We find marketing and product teams attempting to prototype and launch products quickly, however the problem is the complex compliance and regulatory oversight required. In response to this growing demand, technology providers will need to make their tools easier to deploy (with compliance baked in) to keep up with ambitious project timelines. Tern, for example, launched low code widgets to enable companies to launch core fintech services, such as onboarding, account issuance, and payouts, quickly and inexpensively.

Looking ahead, the real uptick in embedded finance will come when enterprise legacy companies, with established customer bases, realize the ROI of launching fintech services across a broad range of industries, and have a deployable vehicle to bring them to market. So, really, I would say we’re still at the beginning of this trend, and that’s exciting.

Another major trend in fintech is the proliferation of neobanks – especially those serving specific communities and consumer segments. What is driving this and how sustainable is it?

Bonkowski: New neobanks are popping up all over the place, and for good reason. Consumers have decreasing loyalty to traditional banks, so when a new online bank with messaging targeting a specific demographic appears, that demographic will typically at least test the waters, especially if motivated to do so by their peers. This is especially true if the account is free and offers services traditional banks do not, like earned wage access (EWA). Challenger banks like Chime started the wave of EWA programs and we find this function to be a big driver for neobanks to differentiate themselves and add new customers. Unfortunately, outside of EWA offerings, many of these neobanks have little to no differentiation. Many rely on celebrities and influencers to get the word out which is definitely not sustainable. Coupled with a bullish fintech venture market, we are sure to see some major casualties in the coming years.

Neobanks with specific functionality catering to their audience, however, still have a fighting chance at disruption. These differentiators vary, but even something like lowering the friction of moving funds into or out of accounts, or adding a utility like crypto or remittance to a portfolio, can be very powerful.

We’ve seen a number of different types of industries – from Big Tech to Big Retail – move into the banking services space. What kind of challenge does this represent for both “traditional” fintech providers as well as for banks?

Bonkowski: One distinct advantage that Big Tech and Big Retail have over banks and “traditional” fintechs is data. They know who their customers are, how they spend their time, and what they buy, which gives them a significant leg up in offering financial services and credit products. Traditional banks and processors see transaction data and know if you have paid your bills on time, but they haven’t a clue as to who their customers are and what makes them tick. Big data is playing an increasing role in establishing very specific cohorts of users. Within this construct, they can facilitate the orchestration of a variety of financial services, offered in different formats with cohort specific messaging, to see which one works.

The one saving grace traditional banks have is regulation and oversight, two things Big Tech and Big Retail want to stay as far away from as possible. They are already under the federal microscope, and the thought for some is that adding banking regulatory obligations could stifle growth and innovation. This has moved Big Tech and Big Retail to partner with banks, rather than compete against them…at least for now.

The Buy Now Pay Later e-commerce phenomenon seems very much in a boom phase. Is regulatory scrutiny inevitable and how might it change the way BNPL services are offered?

Bonkowski: BNPL feels like it’s the wild west of payments right now with little to no oversight. These services are, in fact, credit products and we feel they will eventually be treated as such by the CFPB. We expect new regulations and standards for things like fees, disclosures, payment due dates, penalties, etc. Our fear is these new regulations may stifle the BNPL form factor by adding steps to the process or forcing consumers to accept multiple onerous disclosures. This may increase shopping cart abandonment, the very thing BNPL is looking to obfuscate. With many products and programs, we feel the best and cleanest end use experience will prevail. BNPL providers need to remain agile and incorporate these new regulations as they come up with the least amount of end user friction possible.

This fall Tern announced a partnership with TransferMex. How did this collaboration come about and how does it help fulfill Tern’s mission?

Bonkowski: TransferMex is a great case study on the power of partnership. In 2020, Tern was approached to help an institutional Mexican labor supplier issue bank accounts for H2 Visa workers. The driver for the program was to service the employers by eliminating paper checks and, in turn, the exorbitant cost for employers to track down workers that have to leave unexpectedly to deliver their final paycheck. Looking to add value to not just the employer, but the workers, Tern suggested adding simple and inexpensive remittance capabilities to the program and TransferMex was born. The TransferMex team had limited technical resources or fintech experience so they chose to use Tern’s No Code deployment option, essentially outsourcing the entire program to Tern.

Today, the TransferMex program is live and is seeing dramatic increases in the number of workers and employers using the service. The TransferMex team does all of the marketing, onboarding, and customer support, while Tern hosts and manages all of the technology, applications, and fintech components. Tern sees growing demand for this model of issuing prepaid cards with remittance capabilities to existing brands, and will be launching two telecom companies with similar functionality in early 2022.

Apple’s iPhone celebrated its 15th birthday this week (if that doesn’t make you feel old, I don’t know what will). Since its launch, the iPhone has been through 33 different models and Apple’s market capitalization has risen from $174 billion to $3 trillion.

In addition to making Apple shareholders much better off, the iPhone is also responsible for reinventing an entire industry– fintech. While fintech did indeed exist before smartphones and app stores, it was quite basic. As an example, check out Jim Bruene’s 2006 post titled, SMS Banking: Will it Work in the United States?.

Without the invention of the iPhone, smartphones would likely be around today– Blackberry and Palm Pilot would have gotten us here eventually. However, they probably wouldn’t have advanced as quickly as Apple did, and therefore wouldn’t have upended so many industries so quickly. So in celebration of the iPhone’s 15th birthday, here’s a look at how the big idea behind the small, rectangular device reinvented fintech to become what we know today.

Always on

Most people carry their phone on their person (or at least within arm’s reach) at all times. According to a 2021 study of smartphone usage statistics, 79% of users have their phone with them at least 22 hours each day, 22% of users check their phone every few minutes, and 51% of users look at it a few times per hour. These devices (and the information that they carry) have essentially become an extension of ourselves.

When your customers have their device nearby for all but two hours of each day, it not only gives them access to interact with your company and brand, it also offers you access to interact with them. Compare this to pre-iPhone era. Customers were only interacting with you when they were physically in a branch location, opening a piece of direct mail, or using their PC. Today, when a nagging thought comes up about their budget or investment information, they no longer have to jot it down to remember to look it up later. Instead, they can simply open an app on their phone to get their answer.

Push notifications

According to the study referenced above, the average smartphone user has 63 interactions with their phone each day. Some of those interactions are thanks to the user receiving alerts or push notifications, which Apple launched in 2009.

When used properly, push notifications can be a powerful tool to prompt users to take important action. Others are useful for simply promoting brand awareness. With the advent of the iPhone and push notifications, reminding customers that you still exist became much easier.

From SMS to GUI

Simply put, the iPhone helped take banks’ and fintechs’ digital customer interactions outside of strictly texting and email. The graphical user interface behind phone’s screen brought a new world to the user’s fingertips. Users were no longer limited to checking their balance or making simple transfers. Mobile apps opened up capabilities to do anything they could do online and (in many cases) in person in a bank branch.

Independent developers increasing competition

When you think of the expertise and capital required to start a bank vs. the requirements to launch a fintech, there are gaping differences. Thanks to an increasingly large talent pool of developers, anyone with a viable fintech product or service has the ability to compete with traditional banks by launching their own app in the app store.

Increased competition from fintechs has been overall healthy for the financial services industry and has made end consumers better off. When customers are unable to find a product they like or even when they have been rejected by a traditional bank, fintechs have consistently proven to meet their needs.

Authentication

Apple launched Touch ID in 2013 and in 2014 it was made available for third party apps to authenticate users. More recently, the company launched Face ID in 2017 to facilitate authentication. While fingerprint and facial recognition technology pre-dates the iPhone, it didn’t come on a pocket-sized device that consumers carry around with them.

Having biometric authentication technology available to verify the identity of users each of the 63 times they open their phone each day has made every day tasks safer for banks, fintechs, and users.

A fundraising round of $1 billion has given Checkout.com a valuation of $40 billion, more than 20x the valuation the company earned upon its first fundraising three years ago. The investment takes Checkout.com’s total capital raised to $1.8 billion, and the company said that it plans to use the funds to support growth in the U.S. market, launch its marketplaces solution, and strengthen its position in Web3.

“At our core, we help enterprise merchants to navigate the complexity of moving money around the world, whether in fiat currency or bridging the gap to Web3,” Checkout.com founder and CEO Guillaume Pousaz said. “By combining an elegant technology stack with industry expertise and an ‘extra-mile’ approach to service over the past decade, we’ve built deep partnerships with some of the world’s most innovative companies.” Pousaz added that while he considered this week’s investment to be a “validation” of the firm’s work to date, “we’re still in ‘chapter zero’ of our journey.”

Investors in the Series D included Altimeter, Dragoneer, Franklin Templeton, GIC, Insight Partners, the Qatar Investment Authority, Tiger Global, the Oxford Endowment Fund and “another large west coast mutual fund manager.”

With customers ranging from Netflix and Pizza Hut to fintechs like Klarna, Revolut, and Coinbase, Checkout.com offers a full-stack online platform that makes payments easier for global businesses. Enterprise merchants that face significant challenges in moving money around the world have partnered with Checkout.com for its flexible, cloud-based payment platform that offers improved authorization rates, feature parity, and direct connection to local networks in key geographies and for all major alternative payment methods.

Looking forward, Checkout.com plans to launch a solution to service both marketplaces and payment facilitators later in 2022. The new offering will combine identity verification, split payments, and treasury-as-a-service functionality with Checkout.com’s Payouts solution, which helps companies send funds to both cards and bank accounts worldwide by way of a single integration. Checkout.com reports that both TikTok and MoneyGram have taken advantage of the service, with “billions of dollars in payout transactions” processed.

Headquartered in London and founded in 2012, Checkout.com spent 2021 opening new offices in six countries across four continents and making numerous major C-suite additions. These include a new Chief Financial Officer, a new Chief Technology Officer, and a new Chief Product Officer. The company announced an extension of its strategic partnership with JCB in September, and led a $110 million funding round for Saudi Arabian-based fintech Tamara in April.

Founded in 2015, Tandem Bank used to be among the ranks of U.K. challenger banks Monzo and Starling. But Tandem Bank has remained relatively quiet for the past year-and-a-half– seemingly sidelined from the digital banking race taking place across the globe.

That’s changing today, however. Tandem Bank announced it has acquired lending platform Oplo. Financial details about the deal were undisclosed.

“I think this is a really exciting business combination,” said Tandem Bank Group CEO Susie Aliker. “We have a shared and common purpose to create a greener and fairer banking proposition. We want to build on our digital and technology capabilities to really create a really exciting but also profitable challenger bank.”

Oplo was founded in 2004 and has since lent over $1.2 billion (£900 million) to mainstream customers. The U.K.-based fintech offers car finance, personal loans, and secured loan products as alternatives to traditional bank loans. When it combines with Tandem, the digital bank will have $1.64 billion (£1.2 billion) in assets.

Tandem is very focused on the ESG initiative that has been sweeping the fintech industry; this includes digital banking players in particular. Tandem Bank currently holds $315 million (£230 million) in its Green Loans, a product that helps accountholders “save the planet whilst saving money.” Last year, the digital bank provided customers with loans for home improvements that contributed to over 12,000 tonnes of CO2 reductions.

The Green Loans product comes courtesy of Tandem Bank’s 2020 acquisition of Allium Money, an alternative lender that offers consumers financing to improve the energy efficiency of their homes.

“By joining forces, we will be able to offer a wider range of products and higher quality of service to more people than ever before,” Oplo said in a blog post announcing the change. “And together, as Tandem, we will build a fairer and greener bank for all.”

In a video, Aliker described the company’s recent shift to double-down on its ESG focus. “Our target market going forward will be what we call The New Mainstream.” We want to give them the choices so that they can also help contribute towards a fairer and greener future.”

CBANC, the biggest verified professional network for U.S. commercial banking institutions – and the professionals that run and work for them – announced the launch of its new platform this week. The CBANC Marketplace will host data and information on 1,000 products from more than 450 companies – all designed to meet the unique needs of small banks and credit unions.

“Over the past 10 years, CBANC has been a place for all financial professionals to connect and discover the information they need to succeed,” CBANC CEO Tom Ferries said. “Today, the speed of technological innovation is outpacing awareness, and community banks and credit unions need a place to discover what’s available for them and feel confident in their decisions.”

The CBANC Marketplace gives companies the ability to have their solutions accessed by a verified audience of community banking and credit union professionals. Both the CBANC Community and Marketplace are free for all employees of U.S. financial institutions, and there is no cost for fintechs and other companies that want to add their product or solution. For more information, and to request inclusion in the CBANC Marketplace, visit the network’s vendor hub.

Headquartered in Austin, Texas, and founded in 2009, CBANC benefits from the collective wisdom of more than 8,600 financial institutions with a combined total of more than $22 trillion in assets. The CBANC Community consists of 65,000 verified financial professionals representing more than 80% of all financial institutions in the United States. A unique opportunity to connect and collaborate with peers in the industry who are innovating in a wide range of technologies from AI to the blockchain to cryptocurrencies, the CBANC Network earned a spot on the 2020 Inc 5000 list of the fastest growing private companies in the U.S. Ferries, who took over at CEO days before the Inc 5000 announcement, credited CBANC’s three-year revenue growth of more than 6.5x for helping the organization secure the listing.

“Our strong revenue growth is a testament to the value we deliver to our Members and Partners,” Ferries said. “Look for new and exciting product launches later this year to continue our mission of helping our Members preserve the diversity of the American banking system.”

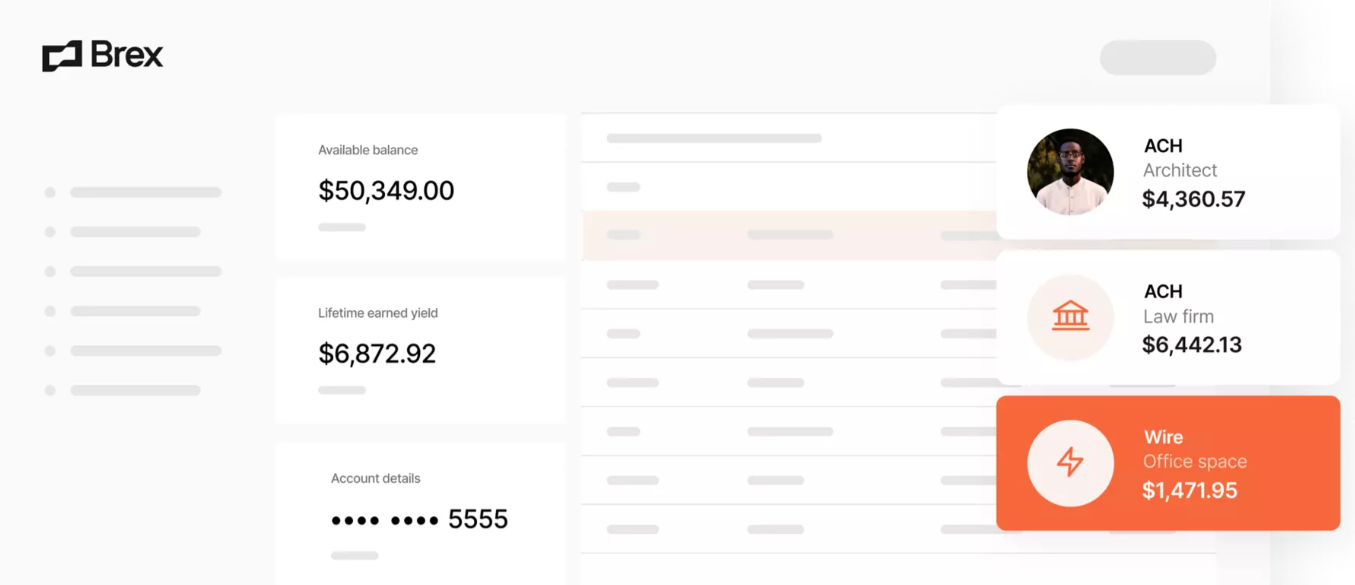

Credit card and cash management solutions company Brexclosed a $300 million D-2 round today. The round, which values the company at $12.3 billion, was led by Greenoaks Capital and Technology Crossover Ventures (TCV).

Brex will use the fresh capital to expand its product portfolio to serve more of companies’ financial needs. The California-based fintech’s funding now totals $1.2 billion.

“Brex is a market disruptor and the opportunity to create economic opportunity for millions of people and businesses globally through innovation in financial products is incredibly exciting,” said Brex Chief Product Officer Karandeep Anand. “The opportunity ahead for Brex is expansive, and I’m grateful for the opportunity to create products that will help our customers grow their businesses.”

Brex was founded in 2017 to create a digital-first business banking solution. The company offers business bank accounts with credit cards that have built-in rewards, spend controls, and expense tracking. The accounts give businesses early access to their online revenue, billpay tools, and integration with popular accounting tools– all with zero fees. The company serves “tens of thousands of businesses” ranging from small private companies to large public brands, including Airbnb and Classpass.

“Brex has always moved fast. But as the company has scaled, they’ve managed to get even faster, accelerating their growth since our last investment,” said Greenoaks Founder and Managing Partner Neil Mehta. “Brex is building a full financial operating system that keeps getting more comprehensive, all of which will delight existing customers and attract new ones.”

In addition to the funding announcement, Brex is also highlighting a noteworthy personnel change. The company appointed Karandeep Anand as Chief Product Officer. Anand comes to Brex from Meta, where he led the business products group, which served more than 200 million businesses globally. Before his start at Meta, Anand spent 15 years at Microsoft leading the product management strategy for Microsoft’s Azure cloud and developer platform.

With its acquisition of financial analysis as a service company FlashSpread, digital mortgage platform BeSmartee’s ability to deliver a complete, digital lending experience just got that much more complete.

“We are excited to welcome FlashSpread and Ariel Trybuch to the BeSmartee family,” CEO and co-founder of BeSmartee Tim Nguyen said in a statement. “This is an acquisition that not only brings new clients, technologies, and talents to BeSmartee, but one that also sparks further innovation into all lending verticals, including mortgages, consumer, and commercial.”

Founded in 2017 and headquartered in Glendale, California, FlashSpread specializes in instant tax spreading for commercial lenders and fintechs. The company’s proprietary algorithms enable lenders to convert scanned tax returns into customized and comprehensive financial reports with the click of a button. The technology brings significant efficiencies to the commercial loan process – from origination to servicing – and empowers lenders to make accurate, data-driven credit decisions quickly.

Via its acquisition of FlashSpread, BeSmartee will be able to accelerate its growth strategy, prioritizing increased automation as it expands into the commercial lending space. FlashSpread is integrated with some of the largest loan origination systems in the commercial lending industry, with more than 100 financial institutions relying on its technology to automate manual processes. Post-acquisition, FlashSpread will continue independently to serve customers as a “BeSmartee Company” with FlashSpread founder and CEO Ariel Trybuch taking on the role of General Manager.

“This partnership will provide the resources necessary to support the hyper-growth FlashSpread is currently experiencing, as well as allow us to provide our customers with an even higher level of customer support, rapidly introduce new features and functionality, and expand our ever-growing library of supported document types,” Trybuch said. The company will continue growing its document library to support a broader range of financial statements, as well as launch a no-code reporting module to offer instant custom reports, and unveil an ongoing credit monitoring tool.

BeSmartee’s acquisition announcement comes just days after the company reported a partnership with Freddie Mac. The Huntington Beach-based fintech will integrate Freddie Mac’s automated underwriting system, Loan Product Advisor, improving workflows for lenders by automating risk assessment, and both asset and income data review. The integration will also improve lenders’ ability to make smart business decisions, leveraging actionable insights from Loan Product Advisor’s rich data visualization features.

As we survey the damage from the pandemic and its multiple variants, technology services and consulting firm Accenture has some advice, “It is critical that every bank becomes a challenger.”

In a recent report, the firm uncovered that banking has moved from vulnerable to volatile on its Disruptability Index. Underlining this point, Accenture found that bank revenues declined in 2020, then rebounded last year. “Although COVID hasn’t been a solvency event for the banking industry, we have seen material profit compression that has reordered banks’ priorities,” the report states. “Leading institutions have witnessed double-digit net income declines of 7 percent in Asia-Pacific, 37 percent in North America, and 51 percent in Europe in 2020.”

This profit compression, along with an increased cost of risk and accelerated digital transformation, has resulted in what Accenture is calling a “neo-normal.” The more level playing field has resulted in a more crowded industry. Fortunately, Accenture leaves readers with four “imperatives for success” in this new, post-COVID arena.

Understand your market

While it has always been imperative for banks to understand their customer base, customers’ needs and wants have changed since the pandemic. For example, Global Banking Consumer Study found that when dealing with a bank, customers rank value as the number one priority. That’s up four slots from just two years ago when customers ranked it number five.

Also as a part of this, Accenture noted that banks must balance managing costs with customer acquisition. “Banks can no longer spend multiple years on complex integrations—they need to build a technical stack that can quickly onboard and migrate acquired portfolios and customers so the economic value of the acquisition can be realized swiftly,” the report said.

Future-proof your business

If this was important before the pandemic, it is even more so now. That’s because what we once thought was “the future” is here today. One of the best ways to do this may be cloud partnerships, Accenture explained, because the partnerships can accelerate digital transformation via partnerships.

Banks can’t take a blanket approach, however. There is no one-size-fits-all business model, especially for larger financial institutions. Instead, banks must adopt tailored models for each business sector in which they operate.

Focus on becoming digital

Accenture suggested that a mobile app is just a ticket to the game. Banks can’t rely on the app alone as their digital strategy. Instead of relying on their mobile app as their entire digital strategy, banks should shift their thinking outside of their budget. That is, digital tools shouldn’t be put in place just to decrease cost. Banks should also leverage digital to enhance differentiation, increase revenue, and boost customer acquisition.

Adopt technology

Simply put, “there is a high correlation between technology adoption and revenue growth.” That’s what Accenture found in two separate studies recently. Similar to the point above, banks shouldn’t just look to technology to decrease costs and increase efficiencies. Instead, in order to get ahead, banks need to consider how technology can enable growth, boost differentiation, and facilitate productive partnerships.

This is, of course, easier said than done, so Accenture suggests two jumping off points for banks. First, banks should improve their boards’ knowledge about technology. Second, banks need to align their IT strategy and their growth strategy.

These four tips are just highlights. There is a lot more to the full report, including graphs and many more stats. Check out Accenture’s brief and download the report.