This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

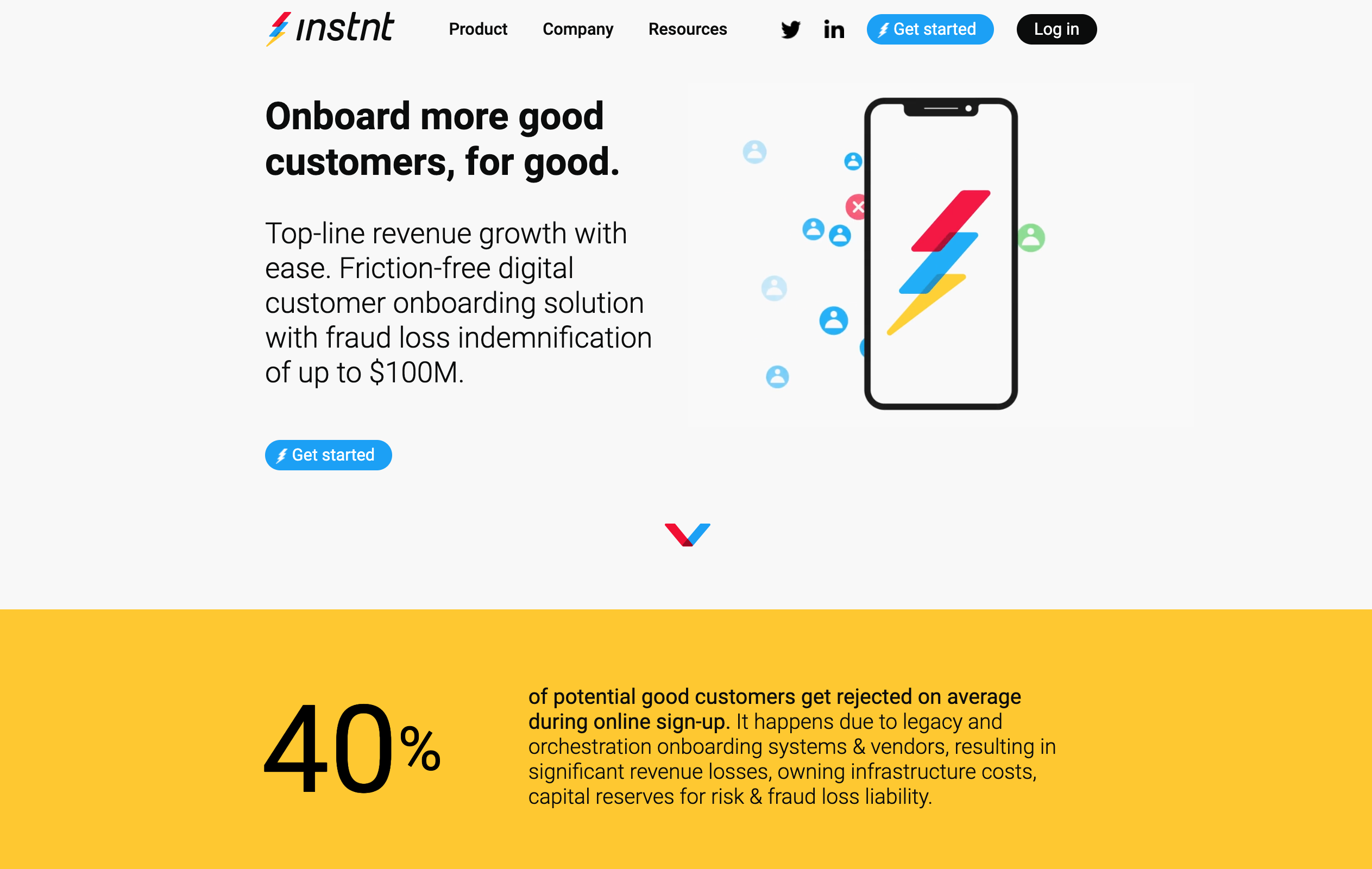

Instnt is a fully managed customer onboarding solution for with up to $100 million in fraud loss insurance. It helps businesses sign-up and onboard twice as many good customers without the fraud losses.

Features

AI-powered managed service that replaces vendor integration and human orchestrated waterfalls

No Code/Low code integration without giving up ownership of user journey

Fraud loss insured up to $100 million

Why it’s great Instnt is the first AI-powered managed onboarding service that replaces human-driven vendor integration and orchestration and is also the only offering in the market with fraud loss insurance.

Presenters

Sunil Madhu, CEO & Founder As the Founder and previous CEO of Socure and a leader in AI-driven fraud, Madhu has spent over 20 years innovating in the Identity & Access Management, Security, Governance, and Risk and Compliance markets. LinkedIn

Justin Kamerman, Chief Product Officer Kamerman has over 20 years experience designing and building high performance distributed systems in the telecommunications, IPTV, identity verification, social media analytics, and IIoT industries. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

Sequretek offers end-to-end security in the areas of enterprise threat monitoring, incident response, device security, identity, and access governance through its own AI-driven Percept Cloud Security Platform.

Features

Enterprise scale, easy to use, and cloud native

AI-driven threat detection, protection, remediation and response

Quick implementation and integration capabilities

Why it’s great Percept Cloud Security Platform offers end-to-end security through three products instead of implementing and managing 12 to 15 different cybersecurity products. It reduces the total cost of ownership while simplifying security.

Presenters

Pankit Desai, Co-CEO & Co-Founder Desai is a veteran of the corporate industry with over 25 years of experience in global sales, operations, and FP&A, with leadership stints at Rolta, NTT Data, IBM, and Wipro. LinkedIn

Anand Naik, Co-CEO & Co-Founder Naik has worked in the corporate industry for over 25 years with companies like Symantec, where he was the MD for South Asia. He was also previously with IBM and Sun Microsystems in technology roles. LinkedIn

From partnership to acquisition, the Buy Now Pay Later revolution shows few signs, if any, of abating any time soon.

Apple, one of the Big Tech companies that has been aggressive in its expansion into fintech and financial services, recently announced that it is teaming up with BNPL company Affirm Holdings to offer new, interest-free financing options for qualifying Apple customers in Canada. The new program enables consumers to finance iPhone purchases over a 24-month period and iPad and Mac purchases over a 12-month period, both with 0% APR.

The new initiative comes a month after Apple announced that it was teaming up with Goldman Sachs to help introduce its own Buy Now Pay Later service – ostensibly to rival companies like the aforementioned Affirm. The offering will reportedly be called Apple Pay Later.

And filed in the “if you can’t beat ’em, buy ’em” folder is the news from London, U.K.-based Buy Now Pay Later company Zilch. The firm agreed this week to acquire San Francisco, California-based debt funding platform Neptune Financial as part of setting up shop in the U.S. “We’ve been exploring growth options in the U.S. for some time and following the additional funding,” Zilch founder and CEO Philip Belamant said. “Now was the perfect time to take another meaningful step towards our U.S. launch.”

Zilch’s acquisition news comes less than a month after the company secured $110 million as part of an extension of its Series B round. One of the first Buy Now Pay Later firms in the U.K. (founded in 2018), Zilch enables consumers to pay for purchases using their virtual Zilch card by splitting their transaction into four, interest-free payments over a six week period. The company has raised more than $200 million and boasts 150,000 new sign-ups a month for its BNPL services.

One of the more interesting pivots in the BNPL space of late was an internal one as Canada’s Scotiabank announced that it will convert its credit card repayments into BNPL plans. The new arrangement will give cardholders the ability to pay off their debt balances in fixed installments over three-, six-, or 12-month periods.

“Our customers told us that they’re looking for more options to help them manage their finances,” Scotiabank SVP for Credit Cards and Lending Brett Mooney explained. “This new credit card feature offers our customers more flexibility in how they pay for purchases, in addition to the convenience, rewards and lifestyle benefits that our credit cards already provide.”

The new service is called Scotia SelectPay and can be accessed via the Scotia mobile banking app as well as online. Purchases of more than $100 are eligible for the new financing option, which requires no additional credit check or application.

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

unitQ’s product quality platform empowers fintechs and banks to take a data-driven approach to product quality so they can fix the right quality issues faster.

Features

Leverage a single source of truth for product quality

Determine what’s impacting your product right now

Identify, prioritize, and fix the right quality issues faster

Why it’s great Staying on top of product quality is hard. unitQ empowers your organization to take a data-driven approach to product quality.

Presenter

Anthony Heckman, Head of Business Development & Growth Prior to unitQ, Heckman was an EIR at XSeed Capital. He graduated from the University of Southern California and University of Pennsylvania Law School. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

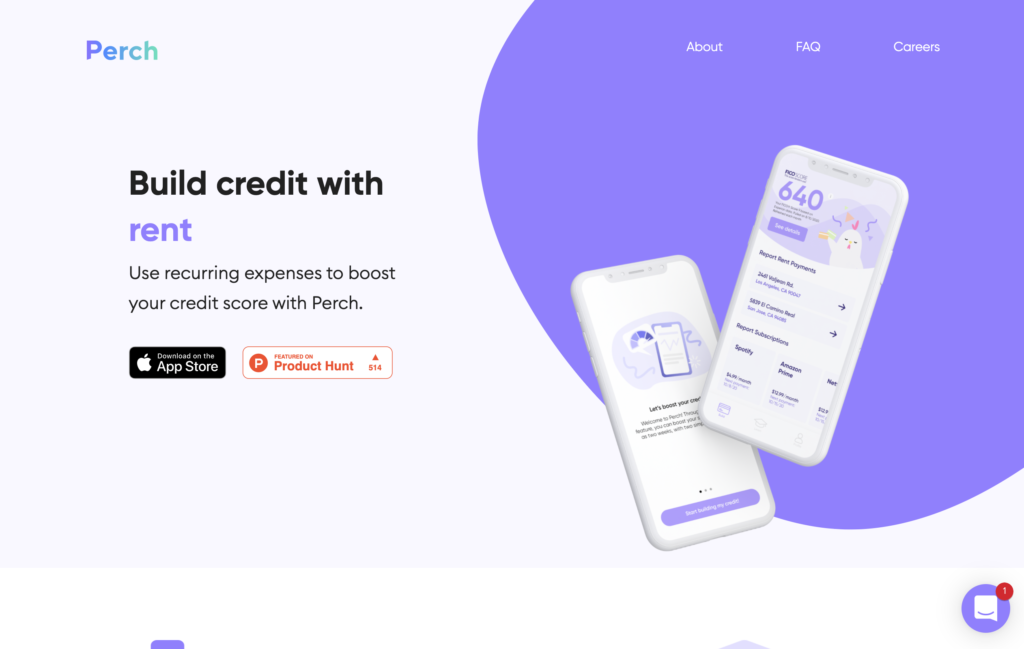

Perch helps you get and build your credit with everyday payments and subscriptions. It helps you earn credit by starting with the recurring payments you’re already making – your rent and subscriptions.

Features

Quick and easy setup: start credit building in as little as 5 minutes

Automated credit building: increase your credit score as you continue to pay

All your information is kept safe

Why it’s great Perch is on a mission to financially empower all.

Presenter

Michael Broughton, CEO & Co-Founder Broughton is a young entrepreneur who studied business at the University of Southern California. Coming from a military family, he grew up in the Far East, living in South Korea and Japan. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

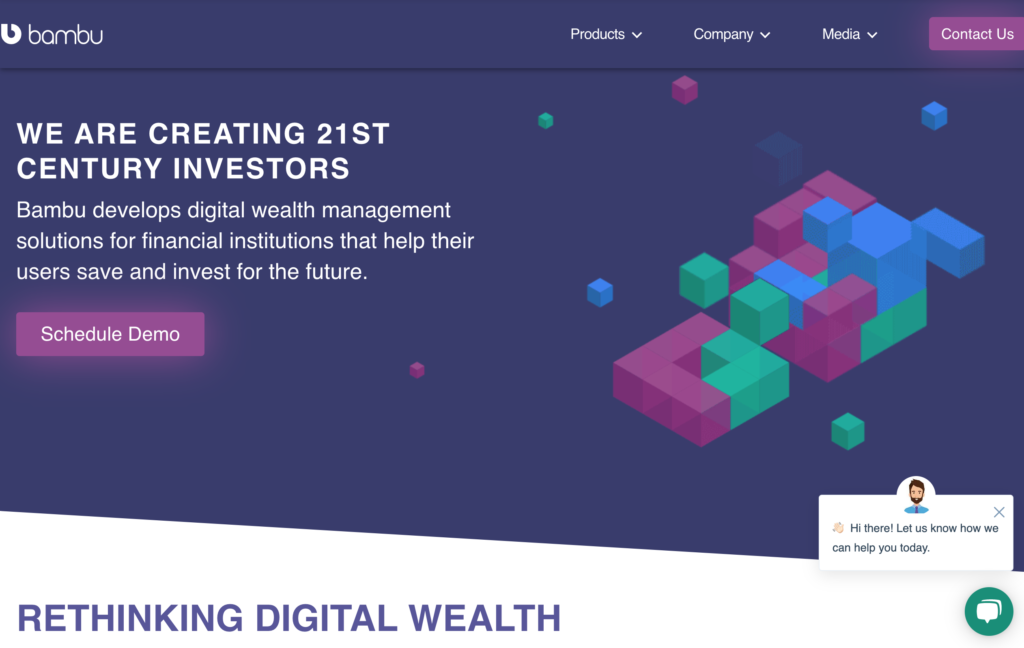

Bambu is the next-generation, B2B robo-advisory platform for financial and technology institutions, enabling companies to make saving and investing simple and intelligent for their clients.

Features

Enable and empower small and medium RIAs to scale up and increase AUM

Avoid complex technology that prevents RIAs from adopting the platform

Save on cost with no integration and developer cost

Why it’s great Bambu GO 2.0 is a turn-key digital investment platform.

Presenters

Ned Phillips, CEO Phillips has over 20 years of fintech experience. He is on a mission to improve the wealthtech industry with a robo-advisory platform. LinkedIn

Michael Larsen, Head of Sales, Americas Larsen is an experienced Head of Sales with a demonstrated history of working in the SaaS and financial services industries. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

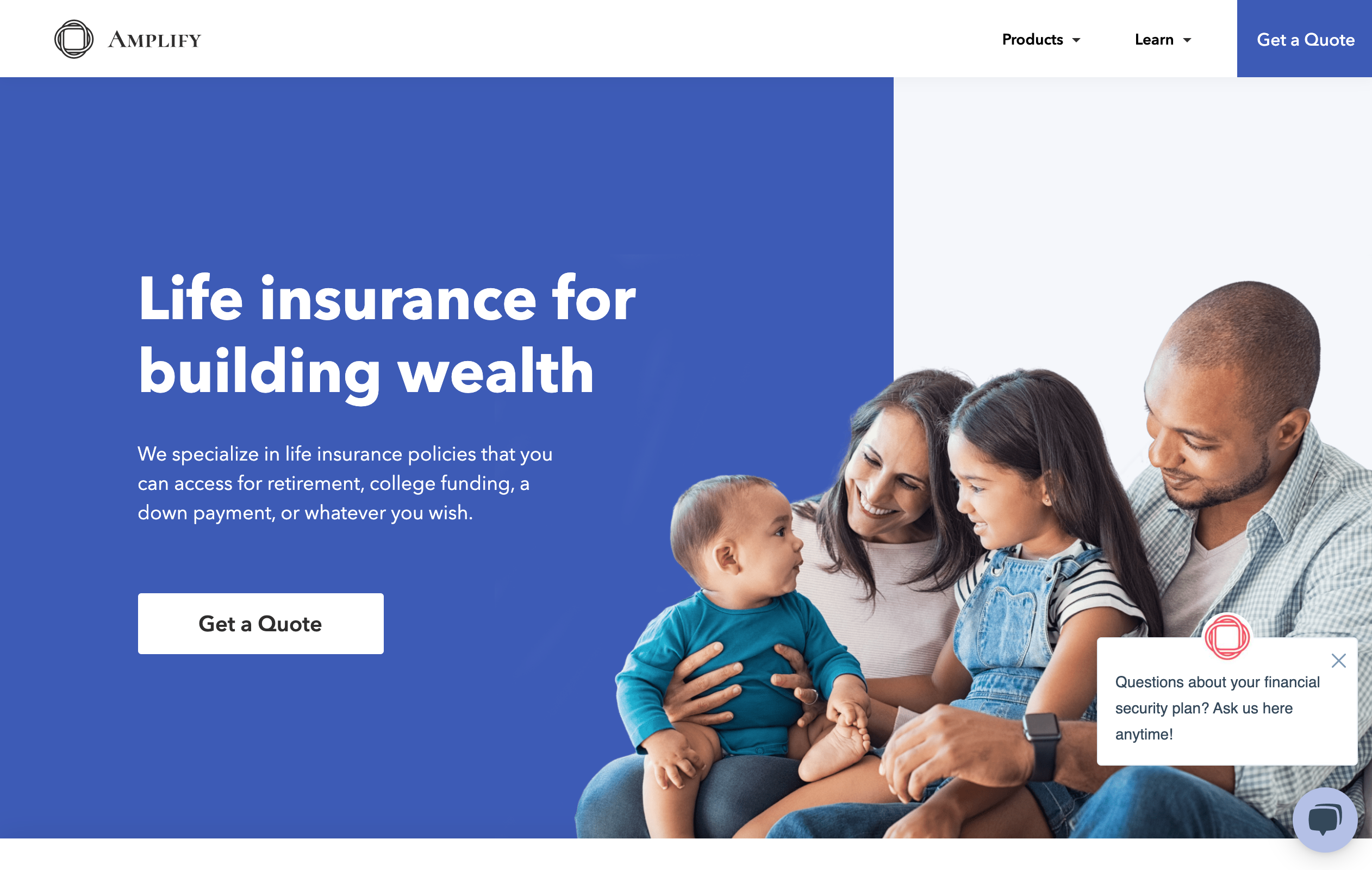

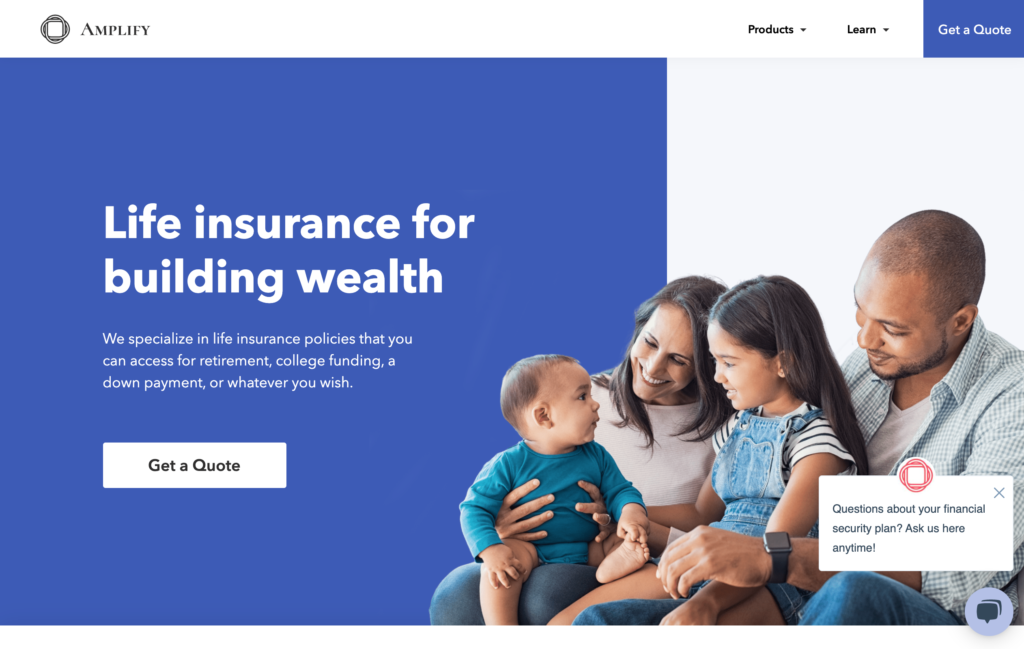

Amplify helps people build wealth through permanent life insurance. They’ve built an intelligent customer journey with frictionless policy customization, pre-underwriting, and in-force policy management.

Features

Delightful customer journey for life insurance investment products

Policy customization and pre-underwriting for accurate quoting and fast decisions

API infrastructure and ecosystem connectivity

Why it’s great Bespoke life insurance investment products can now be customized and purchased instantly D2C or through an advisor via Amplify’s platform.

Presenters

Hanna Wu, CEO & Co-Founder Wu’s family has been in life insurance for over 30 years. Prior to Amplify, she built a financial planning agency with three locations and placed over $2B in life insurance coverage over five years. LinkedIn

Qiyun Cai, President & Co-Founder Cai started her career in venture capital and found her passion in early stage software startups that make an impact on how we work and live. She is a graduate of Harvard Business School. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

AFS, a leading commercial lending solution provider, will demonstrate the ability to add and utilize new Custom Data Fields to the system in real-time, with no programming.

Features

Respond to market, product, and regulatory demands immediately

Define, label, and create data fields

Use the fields as soon as they are created

Why it’s great Commercial lending technology is behind in moving to digital. AFS will demonstrate that commercial lending solutions can be agile and responsive to technology innovation and customer/market demand.

Presenters

Brenda Alek, Director of Client Strategies Alek is responsible for working with financial institutions to evaluate workflows, review operations, and develop new business models/transformations. LinkedIn

Derrick Wise, Director Wise brings over 20 years of experience in the financial services industry. His expertise is with financial software design and implementation.

Jerry Cooper, AFSVision Solution Architect Cooper leads the design and development of new products and features in the AFSVision platform. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

txtsmarter is a communications surveillance service for messaging and social platforms to capture, encrypt, and archive previously inaccessible data for compliance requirements in the financial space.

Features

Archive iMessage, Android SMS/MMS, and WhatsApp

Comply with FINRA, SEC, FDIC, MiFID II, Dodd-Frank, and FCA regulations

Adhere to privacy regulations

Why it’s great txtsmarter is an API-driven Intelligent Communications Surveillance Service. Once activated, it requires no user interaction, is OS and device-agnostic with full compliance coverage, and directs data to an eDiscovery platform.

Presenters

Nuri Otus, CEO & President Otus drives the strategic direction for txtsmarter as the company establishes itself as a market leader in the communications surveillance and compliance space. LinkedIn

Sabine Zimmerhansl, Director of Compliance & Product Development Zimmerhansl is focused on developing txtsmarter’s line of products and services for customers while assuring compliance with global regulations and anticipating the impact on business. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

Berbix is an identity verification solution for building trusted relationships online by instantly and accurately validating a user’s identity.

Features

Increase new account signups

Reduce cost of acquisition

Reduce fraud

Why it’s great Berbix is the most accurate and reliable ID verification solution – 4x more accurate than legacy providers.

Presenter

Eric Levine, Co-Founder Co-Founder of Berbix, Levine currently leads the engineering, product and design efforts. Prior to Berbix, he led the Trust & Safety engineering team at Airbnb. LinkedIn

Financial planning software company RightCapital unveiled new dynamic retirement spending strategies on its platform this week. The new offering gives investors the ability to better plan their finances once their working days are done.

“The industry has been using a rather simple retirement expense approach in the financial planning process for many years,” RightCapital CEO Shuang Chen said. “The ability to offer multiple options for retirement spending within our comprehensive planning tool is a significant step forward.”

Traditionally, financial planners have relied on an inflation-adjusted retirement spending model which focuses on a single input – the rising cost of living – to anticipate an increase in retirement spending each year. One criticism of this approach is that it does not account for changes in an individual’s portfolio that might significantly affect how much they are able to spend in retirement. RightCapital’s new offering factors in changes in portfolio value, reducing retirement spending projections when the portfolio loses value and giving investors the option to spend more in retirement should their portfolio significantly increase in value. The two dynamic strategies – referred to as guardrail and floor and ceiling – enable retirement spending to adjust in sync with portfolio performance and investment strategy parameters rather than being limited to tracking the rate of inflation.

Dynamic strategies such as those now available on the RightCapital platform more accurately reflect how individuals respond to changes in their investments in the real world. As Michael Kitces, Chief Financial Planning Nerd for Kitces.com and Head of Planning Strategy for Buckingham Wealth Partners explained, “as advisors, we cannot eliminate the uncertainty of markets themselves, but tools like RightCapital’s dynamic spending can help eliminate the uncertainty for clients of what they’d have to do in response to those market events, facilitating better client conversations about how to keep their retirement on track.”

Other features of RightCapital’s dynamic retirement spending strategies include the ability to customize spending levels by age, anticipating a higher level of spending early in the investor’s retirement life and tapering off as the investor ages. The strategies can also incorporate changes in healthcare expenditures over the course of the investor’s retirement, as well.

Founded in 2015 and headquartered in Shelton, Connecticut, RightCapital demonstrated its technology most recently at FinovateSpring in 2019. At the conference, the RightCapital team demonstrated the company’s API/Enterprise solution, which gives financial advisors the ability to offer their clients access to custom applications ranging from PFM to account aggregation to secure document sharing. In June, RightCapital announced that it would “enhance (its) integration” with partner Riskalyze, a specialist in risk alignment and portfolio analytics. Also that month, RightCapital and a coalition of fintechs including fellow Finovate alum Bettermentlaunched the RIA Tech Suite to provide financial advisors with services and tools to automate back-office operations.

“Our mission has remained steadfast to help financial institutions of any size succeed with impactful, intentional innovation,” Nymbus CEO and Chairman Jeffery Kendall said. “OFG Ventures’ investment is an added vote-of-confidence to the value our strategy brings to an industry widely in need of immediate and sustainable business growth opportunities.”

Most recently demonstrating its technology two years ago at FinovateFall, banking-as-a-service innovator Nymbus provides financial institutions with both the technical and operational tools necessary to digitally transform their businesses. The company’s solutions – ranging from its flagship SmartCore, SmartDigital, and SmartPayments offerings to its full-service, standalone digital banking alternative SmartLaunch – give banks, credit unions, and other financial services-based companies greater ability to streamline processes and offer new digital services – without requiring a major core conversion or significant additional human resources.

This week’s investment is only the latest infusion of capital the Miami Beach, Florida-based fintech has received this year. The company picked up $15 million in funding from private equity firm Financial Services Capital this spring and, in February, Nymbus announced a $53 million Series C round led by Insight Partners. The company’s total funding now stands at more than $121 million, according to Crunchbase.

Nymbus has been one of the busier banking-as-a-service innovators of late, partnering with a variety of fintechs and financial institutions in the past year. These partnerships have included collaborations with fellow Finovate alums like Plaid and Segmint, credit unions and challenger banks like VyStar CU and PeoplesBank’s ZYNLO Bank, as well as with innovators in open finance and cryptocurrencies like Red Hat and NYDIG. The company also launched a new credit union service organization (CUSO) in March, Nymbus CUSO, to help credit unions take better advantage of fintech offerings that can enable them to create new revenue opportunities and boost engagement with their members.

“Our CUSO signifies a commitment to credit unions by providing strategic partnerships and flexible technology that will create sustainable growth and loyal members,” Kendall said when the new organization was introduced earlier this year. “For those wanting to innovate, Nymbus CUSO moves past traditional vendor thinking to create supportive structures for credit unions ready to grow and reach new niche markets.”