This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

We’re halfway through 2025, and with two Finovate events in the books, there are clear themes emerging around the future of financial services and fintech.

In this edition of the Finovate eMagazine, we bring you insights from both sides of the Atlantic, featuring key learnings from FinovateEurope and FinovateSpring.

Fill in the form and discover the trends shaping the future of financial services and fintech. Explore:

The latest approaches to innovation

Hear from David Barton-Grimley and Bhoomika Ghosh on how to make innovation meaningful and impactful. Plus, David Penn brings us insight into how credit unions want to digitise and partner.

How to navigate global growth in today’s economy

Julie Muhn brings us the key regulatory shifts on both sides of the Atlantic and David Grace from SHAZAM explores the importance of partnerships to face the upcoming challenges

The Finovate Library on Streamly

This eMagazine brings you insights to inspire your business strategy and your future endeavours.

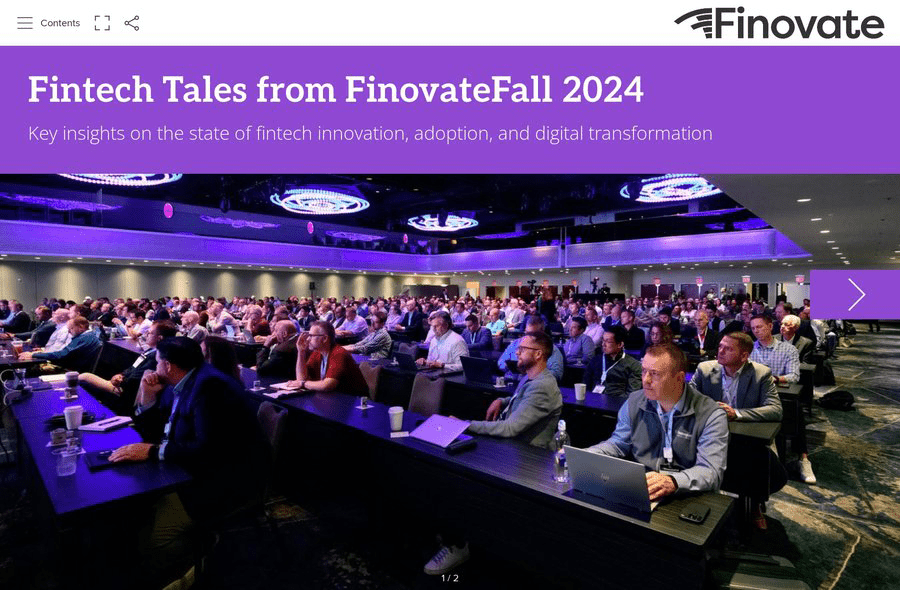

This edition of the Finovate eMagazine brings you insights from FinovateFall 2024. We spoke to dozens of experts, innovators, and strategists from banks, credit unions, wealth management firms, and insurance companies about the hottest topics in fintech. Learn how they:

Elevate customer experiences From approaching Gen Z and addressing the painpoints of change to empowering employees and enhancing customers’ digital journeys.

Build partnerships As financial institutions share their approaches and how they bring cultures together.

The funding drought in fintech is a very well-documented concern. Nevertheless, FinovateEurope 2024 featured more early-stage demoing companies than any of our events to date.

There’s certainly reason to be optimistic about the future of our industry. We’re seeing more innovation and more creativity every time we convene. We’re not only seeing new solutions to emerging problems. We are also getting first-hand accounts of how these solutions are being deployed within financial institutions.

In this eMagazine, we hear from key decision makers at ABN AMRO Bank, BBVA, Raisin, Zurich Insurance Group, and beyond on how they’re adopting technologies and how their customers benefit from them.

It’s no secret that we’re facing many challenges right now. Declining VC investment, rising interest rates, and the looming threat of a recession are all obviously significant obstacles that must be overcome, but we’re also seeing a surge of innovators tackling real-world challenges head on.

At FinovateFall, we’ve seen exciting automation and AI use cases, including generative AI! We also heard financial institutions talk about their digital transformation journey and how they’ve applied technology to improve their processes and enable their businesses to grow. Plus, we met with industry agnostic experts who inspired us to be better leaders and innovators and who helped us think about a future with AI and a future in the metaverse.

Welcome to the latest edition of the Finovate eMagazine. As we kick off another issue full of fintech insights and profiles, I’d like to start with an old joke that’s been on my mind recently. It goes something like this: two men were hiking in the woods when they came upon a bear. One of the men immediately knelt down and began lacing up his shoes. The other one said, “it doesn’t matter how tight your shoes are, you’ll never be able to outrun that bear.” The first one replied, “I don’t have to outrun the bear, I just have to outrun you.”

For a long time, fintech innovators have been able to survive simply by beating their closest competitors, making sure that they are one step ahead of those they perceive to be running from the same basic threats that they are. For the most part, this has been true. Banks that have ignored new technologies have failed to attract new customers, and they’re dying out, leaving a greater market share for those that remain. Legacy fintech providers that haven’t updated or upgraded aggressively are losing out to those that have. And fintech startups that haven’t wisely used the capital they’ve been allotted have been forced to endure painful layoffs or, in some cases, shutter their doors altogether, leaving more room for those that have been able to operate more efficiently.

In short, falling behind your closest rivals has been costly, while staying ahead of them has been rewarding.

Our Finovate conferences showcase key insights that will help you run faster. In this eMagazine, we bring fresh content from FinovateSpring 2023 and discuss the most important trends in fintech today.

Learn about the key developments making financial services more accessible for both consumers and businesses

Watch interviews with key industry giants, including Wade Arnold, Barb MacLean, Charles Potts, and Sarah Hinkfuss

Get up to date with new developments in generative AI and metaverse use cases, embedded finance, geopolitical risks, and more

Read unpopular tech opinions from our demoers and the key issues surrounding card programs

Catch up with our fintech founders and see what they have to say about launching startups in the current landscape

The past few years have been turbulent, and there’s reason to believe more turbulence is on its way. Technological innovation might be the answer to challenges that arise in the finance industry, but it’s important to take a moment to talk about the human side of this industry. Ultimately, everything in fintech is for the benefit of the people using our products, and right now that thought needs to be at the forefront of everything we do.

The companies that will succeed in this time of uncertainty are the ones that excel at understanding their customers, and who give them good experiences, and, of course, help them lead richer, more productive financial lives.

Download this Finovate eMagazine and get an overview of the upcoming challenges of 2023. Find out more about:

Generative AI, the metaverse in the finance sector, and other technology trends emerging in 2023

Exclusive interviews from FinovateEurope addressing the challenges of the fintech landscape, the future of customer experience, and coopetition in the industry and how to turn it into successful partnerships

As we approach the end of the year, it’s time to sit back with a fresh cup of tea, look out the window at the falling snow, and…think about what a significant year it’s been for fintech, of course!

2022 was a turbulent year in our industry. The past year offered real solutions to significant problems unearthed by the pandemic, but also the beginnings of a course-correction that is slowly working its way through the fintech sphere (and the larger tech ecosystem).

One fundamental aspect of the fintech industry is that it has always been able to hold two diametrically opposed truths at the same time. Right now, both of the following statements are true:

1) the future of fintech is as bright (or brighter) than it’s ever been, and

2) there are still more painful situations coming for us in 2023.

Analysis from our resident journalists on the top trends they expect to see making waves in the industry next year

Thought leadership from Headline Sponsor, Frost & Sullivan on how to protect and improve customer financial wellness amidst economic uncertainty

The full collection of Finovate 2022 Best of Show demos videos

Expert opinion on accelerating your data strategy, getting the most out of fintech/ bank partnerships, why crypto is “useless” and investor advice for start-ups looking to get funding right now

Exciting things are happening in fintech right now, and we’re incredibly grateful to have so many of you joining us at FinovateFall this year to take it all in for yourself. There’s a lot to be excited about! As you may have heard, this year’s FinovateFall is officially our largest show yet, with more than 1,600 of you here in the room with us. After a period of general upheaval and uncertainty, it’s great to see the fintech community coming together en masse to plot a course for the future.

What’s happening is bigger than just the number of people in the room, though. It’s no secret that the last few years have been challenging ones and what we’re seeing now is fintech’s response to that challenge. New ideas, new innovations, and new companies are taking shape right before our eyes; venture capitalists are actively seeking out early-stage investment opportunities; and financial institutions themselves are more receptive to change and innovation than ever before. And most importantly, at every step of the way, the industry is making a concerted effort to help the everyday people who need it most.

Analysis from our resident journalists on the top trends from the event and beyond

Thought leadership from Headline Sponsor, Provenir

The Best of Show demos videos

The Finovate Awards winners, and finalist profiles of Highnote and RBC Clearing

Expert opinion on accelerating your lending strategy, the do’s and don’ts of leveraging emerging technology in fintech and exploring virtual worlds and economies

It’s no secret that the last few years have been challenging ones, and the simple act of bringing our community together in the same space feels like a major accomplishment. So, while it’s great to be back at FinovateEurope 2022 in person in London, it’s not enough for us to simply be present. The last few years have brought about dramatic changes all over the world, and it’s clear that more changes are coming. The financial world has been searching for a new status quo since early 2020, and while we may be closer now to something more settled and sustainable, we still have some way to go before we get there.

The good news is that creativity in fintech abounds. The innovators and dreamers among us have given us new tools, technologies, and ideas to help us meet these challenging times, and steer our financial system towards a brighter future.

Download the FinovateEurope 2022 eMagazine, to discover why now is a crucial moment for the fintech industry, and what leading fintech, banks and industry players are doing to create the kind of inclusive, resilient, streamlined financial ecosystem that fintech has been building towards for years.

Featuring:

The FinovateEurope 2022 Fintech Trends Power Panel recording

On-demand Digital Demos, and the Best of Show winners (*when announced!)

Going Green – more information on Finovate’s new Sustainability Scholarship for fintechs

Women’s History Month interview with Meghan Lapides

Exclusive interviews from back-stage at FinovateEurope

And more!

Change is upon us; the question now is whether or not we use it to something meaningful.

The future of finance is being ushered in. And the pioneers of the new era lead the change from the FinovateFall stage this year.

We can’t tell you how exciting it was to welcome so many people back to Manhattan. It was made even sweeter by the fact that we were able to engage so many digital attendees at the same time. It felt good to be able to bring our community together again!

Following the long-anticipated meeting of minds and ideas, we looked back on the themes that emerged and will steer the industry forward into unchartered territory. It’s impossible, of course, to distill so many conversations down to a few high-level takeaways. However, within these pages are snippets and insights from on-and-off-stage to give you a taste of the action and a spark of the knowledge shared.

It’s hard to believe it’s only been one year since FinovateEurope 2020 wrapped. What a year it’s been! Looking back on the 2020 demo and speaker videos feels notable precisely because of how “normal” they all look. So much of the past year has been spent dealing with specific challenges and simply trying to weather the storm. It almost seems bizarre to see innovations that don’t specifically address COVID-related problems. But that’s exactly what we have to start doing again.

As we inch towards a gradual re-opening process and, with any luck, a new, more sustainable status quo, it’s vital that we don’t forget one of the biggest lessons of 2020: to prepare for the future, we have to look beyond the problems we can already see.

Fintech is an industry that rewards those who see problems before they arise, and there are no shortage of opportunities waiting just around the corner. Now is the time to look upstream and maybe even dust off projects you shelved a year ago. Put simply, it’s time to stop playing defense all the time and approach fintech with optimism again.

The writing is on the wall – we are going to return to “normal” again. Now it’s up to all of us to imagine how good “normal” can be.

According to the World Bank there are 1.7 billion unbanked adults in the world. In the United States, this number is just over 14 million, representing more than 6% of all households in the country. Analysts have suggested that, in Europe, while there are some well-banked countries (Germany, the Baltics in particular), there are others, especially in Central and Eastern Europe, where large numbers of citizens lack access to basic banking services. In Romania, for example, more than 50% of the country’s adults are unbanked.

I should say at the outset that it is impossible for me to write about financial inclusion without tipping my cap in the direction of Tosin Agbabiaka. An investor with Octopus Ventures, Agbabiaka’s presentation on what he called “Financial Inclusion 3.0” at FinovateEurope in February was as fascinating a discussion on the topic as I have come across. Catch his conversation with Finovate VP and host of the Finovate podcast Greg Palmer from earlier this year.

For our purposes, let’s start with the World Bank’s definition of financial inclusion. The World Bank defines financial inclusion as providing individuals and businesses with access to useful and affordable financial products and services that meet their needs. This leads us to ask: in the current context of COVID-19, nationalism, and lingering economic inequality, how can we achieve a financial inclusion worthy of the times we live in?

What?

One important question to ask when it comes to financial inclusion is quite fundamental: what are financial services trying to provide? There is a danger in “porting” services and solutions to one community simply because they may have worked in another. At a time of rapid technological innovation and adoption – such as we are in right now – this temptation can be difficult to resist. But failure to understand the specific needs of a given community – greater access to earned wages, or the ability to pay cash for online products or services, for example – can result in not only the failure of a well-intentioned initiative, but also potential negative feelings toward the idea of trying new technologies in the future.

This is one of the ways that fintechs can play innovative roles by developing solutions that highlight needs – such as broader access to cash – that may seem niche or be overlooked entirely by traditional, even community-based, financial institutions.

Who?

Who should be included in mainstream financial life? While the answer “everyone who wants to” is obvious, it is also insufficient. Who is going to make the investment to provide financial services in areas where the market may be broad but thin? Even more problematic are those needs that are severe, but relatively narrow and not easily remedied by methods successful in communities where conditions are different. Countries and regions where incomes are low and inconsistent, trust in traditional institutions poor, and the stability of the currency itself at times an issue come to mind.

And in the same way that the conversation on inclusion rightly has emphasized the importance of gender and ethnic diversity, it is also important to think about other communities that have been traditionally excluded from or had severely limited access to financial services. Families and businesses in rural areas and in farming communities, many of whom it should be mentioned are women- and/or ethnic minority-led, are often the most overlooked communities in financial life. This is true both in the developed and developing world. A recent broadcast by journalist Chris Hayes on the eve of Thanksgiving highlighted the life and work of those whose job it is to put food on the tables of millions during the holiday season. It was a helpful reminder of how “essential” this work is and these workers are, and why any financial inclusion must respond to their needs as well.

Where?

Meeting underbanked populations in the communities where they live is a critical component of not only providing them with the financial products and services they need, but also of engaging with them and learning about what those needs are in the first place. Outreach into ethnic minority neighborhoods via civic and even public sector institutions is one first step financial institutions can take, as is partnering with minority-, women-, veteran-, and LGBTQ-led businesses who have firsthand knowledge of the needs of their communities.

This is also true for virtual communities. In some instances, for example, offering financial services to underbanked individuals with mobility, sensory, or cognitive challenges may mean less outreach to physical neighborhoods and more engagement with online communities and networks.

When?

One truism about planning drawn from the world of professional hockey is the idea of skating not to where the hockey puck is currently, but instead, by accurately judging its trajectory, skating to where the hockey puck is going. Similarly, those looking to provide financial services to underbanked communities should be as alert to their future needs as they are to the current needs in those communities.

Some trends are easier to anticipate than others. If we believe that Millennials in general, for example, are entering their prime family formation years, then what is the appropriate response from the financial services and fintech community? I would argue it is an excellent time to intensify outreach to young women, as well as Millennials who are members of ethnic minority groups who might not have the same access to the kind of financial planning resources that are critical when starting a family. A special effort to engage young members of underbanked communities about financing opportunities for higher education seems like a similarly worthwhile effort for banks and community-oriented financial services organizations in late winter and early spring, as well.

But no crystal ball is required. Again, engagement with underbanked communities is key. The easiest way to know which way the train is headed is to climb on board.

Why?

Whether driven by rational self-interest, an renewed altruism, or some combination of the two, the growing desire to bring financial services to those who do not have them – and want them – is one of the most important developments in fintech and financial services. There will be missteps, overreaches and embarrassing assumptions along the way. And in the eyes of some critics and skeptics, this will be evidence that the cause is hopeless or that those attempting to fulfill it are incapable.

But, to steal a phrase, ensuring that the blessings of technology and modern, wealth-building financial services are available to as many people as possible, may be as important a goal as any other in our industry. And at a time when more people are seeing banks and other financial services providers in a brighter light than they have in a decade – thanks to their recent participation in PPP financial rescue efforts, for example, and the fading memories of the Great Financial Crisis – there may be no better time than the present to pursue it.