This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Greg Palmer, VP at Finovate, takes five minutes with Chris Karageuzian, CEO & Co-Founder of Help with My Loan, to explore some of the pain points that still exist for both customers and bankers when it comes to getting loans approved, and how Help with My Loan is cutting through the noise and coming to the rescue.

Digital investment platform Scalable Capitallaunched a crypto offering this week called Scalable Crypto. The new tool, which Scalable Capital is launching in partnership with Europe’s largest digital asset investment company CoinShares, helps users invest in cryptocurrencies.

Scalable Crypto will help everyday investors participate in crypto markets by offering access to crypto investments via regulated stock exchanges in Germany. The new tool will integrate with the company’s existing wealth management and broker offerings, and will hold cryptocurrencies in secured, cold wallets at regulated custodians.

“We make trading crypto as easy as trading shares or ETFs,” said Scalable Capital Co-founder and CEO Erik Podzuweit. “Crypto currencies are well established as an asset class in a balanced portfolio. With ‘Scalable Crypto’, we are providing an affordable and intuitive offering to help even more people to enter the crypto world. The expansion is the next stage in our journey to become Europe’s leading digital investment platform.”

Scalable Capital is making it easy for crypto-novices to experiment with digital currencies. Users trade on the Xetra and gettex exchanges and do not need to open a separate wallet to do so. Instead, cryptocurrencies are held in the form of securities in the customer’s existing account. Additionally, Scalable Capital takes care of the tax details for crypto securities.

Founded in Germany in 2014, Scalable Capital was launched during the roboadvisor craze and now has more than $6.8 billion (€6 billion) under management on its platform. Today, the company offers both B2C and B2B tools. The company provides private individuals digital wealth management, a broker with a flat rate, and overnight and time deposit offers. For B2B clients, Scalable Capital develops solutions for digital investment. Some of the company’s current clients include ING, Barclays, and Santander.

Scalable Capital, which demoed its technology at FinovateEurope 2016, has 330 employees across its offices in Munich, Berlin, and London. Earlier this year, the company landed $180 million in new funding, bringing its total to more than $317 million. Scalable Capital has an estimated valuation of $1.4 billion.

In many ways, my predictions of what to expect in fintech in 2021 still stand in 2022. Indeed, the trends I anticipated– embedded banking, open banking, automation, and banking-as-a-service– are still hot-button issues that banks and fintechs need to address.

Last year we were recovering from the deluge of the digital transformation agenda and it was difficult to see what was beyond pandemic-related trends. This year, however, there has been an obvious shift. The conversation around decentralized finance is transitioning from a quiet murmur to a louder and more pervasive discussion.

What are some important topics banks need to address in 2022? Below are four conversations banks and fintechs must have next year:

Digital identity

Now that the pandemic has driven so many services to the digital channel, the topic of digital identity must be addressed. This issue ties directly into the security of not only money movement, but also the security of users’ data. Without an efficient way to authenticate users, banks and fintechs expose both themselves and their customers to risk.

Decentralized finance

Decentralized finance (DeFi) is taking off across the globe. According to DeFi Pulse, there is currently $96 billion locked in DeFi, up from $25 billion a year ago. If banks want to be part of the conversation, it is no longer a topic they can ignore. While some experts believe that DeFi will eventually kill off banks, others see banks as an integral part of the future of DeFi.

CBDCs

Central bank digital currencies (CBDCs) is a topic that dovetails from DeFi, but is even more relevant for banks. That’s because CBDCs will be government-issued, and because the government doesn’t have the infrastructure to distribute and manage digital currencies, traditional banks will be key in the issuance of CBDCs. If you haven’t already, it’s time to think about the role your bank can play in this space.

Open finance

The U.S. is overdue for regulation on open banking. In fact, we are so late to the game that the topic has already evolved from open banking to open finance. Though there have been murmurs of open banking discussions in the U.S., nothing formal has taken hold. Consumers are ready, however. Not only have their online presences expanded, they are also becoming increasingly aware of their own data privacy and data usage.

A partnership between cloud-based digital banking solution provider Alkami Technology and Idaho Central Credit Union will enable ICCU members to buy and sell bitcoin within their mobile apps and on the credit union’s online banking platform. Bitcoin services are provided by cryptocurrency technology company NYDIG with Alkami’s platform facilitating the deployment.

Claiming the mantle of both the fastest growing credit union in the state, as well as one of the best performing credit unions in the country, ICCU Chief Information Officer Mark Willden said that adding new services such as bitcoin investing are key to ensuring that the credit union maintains its “momentum” and “deliver(s) additional value.” He added, “Fully integrated bitcoin services through NYDIG and the Alkami Platform take us to the next level when it comes to the member experience.”

Idaho Central Credit Union was founded in 1940 and serves more than 480,000 members throughout the state. With 1,600+ employees, ICCU has more than $8 billion in assets.

NYDIG works with Alkami to allow financial institutions to offer their customers and members bitcoin services in a secure and compliant way. NYDIG joined Alkami’s Gold Partner Program over the summer, making it easier for financial institutions to add bitcoin products and services to their offerings and provide them to their customers and members under their own brand.

“The demand for and utilization of digital currencies have expanded exponentially in recent months, leaving many FIs struggling to keep pace and retain these deposit streams within their institution,” Alkami Chief Strategy & Sales Officer Stephen Bohanon said. “Alkami’s partnershp with NYDIG further supports our mission to enable FIs to compete directly against the megabanks and challenger banks to capture this valuable market.”

A Finovate alum since 2009, making its Finovate debut as iThryv, Alkami has grown into a leading cloud-based digital banking solution provider with more than 280 financial institution customers. The company went public this spring, earning a market capitalization of $3.4 billion in its debut on the NASDAQ. Trading under the ticker ALKT.O, the Plano, Texas-based firm raised $180 million in its IPO.

Since its public listing, Alkami has forged a number of partnerships with financial institutions including STAR Bank in November and MainStreet Bank in October. Also this fall, the company announced its acquisition of digital account opening and loan origination provider MK Decision and introduced its new Chief Executive Officer Alex Shootman, formerly the CEO of Workfront. Alkami Board of Directors Chairperson Brian R. Smith said Shootman’s experience in “growing and scaling enterprise software companies” was “essential at this stage of Alkami.”

Today’s announcement from Idaho Central CU comes as NYDIG reports a massive $1 billion growth equity round that gives the company a valuation of $7 billion. The round was led by WestCap and featured participation from Bessemer Venture Partners, FinTech Collective, Affirm, FIS, Fiserv, MassMutual, Morgan Stanley, and New York Life.

The New York-based company now has a total capital of $1.4 billion. The new investment will help NYDIG further develop its platform, taking advantage of recent changes to the bitcoin protocol to introduce functionalities such as bitcoin and lightning payments, asset tokenization, and smart contracts. The company will also use the new funding to add talent to its team worldwide.

“Our roster of partnerships and strategic investors lays the foundation for NYDIG to become the leading provider of Bitcoin solutions for businesses in any industry,” NYDIG co-founder and CEO Robert Gutmann said. “(This) new equity capital will further accelerate progress towards making this exciting network accessible – and useful – to all.”

One month after introducing its next generation development application platform, OutSystems has announced that it is entering a strategic partnership with fellow Finovate alum ieDigital. The alliance will enable ieDigital’s financial services company partners – ranging from bank to mortgage lenders – to access a suite of pre-built, low-code applications that support a variety of operations including originations, self-servicing, retention, and collections.

The goal of the new relationship is to give financial service providers new resources that will help accelerate growth, become more cost-efficient, and better manage risk. The partnership also allows for additional functionalities to be added as part of broader, future digital transformation efforts. One example of this would be enabling companies to analyze data collected during the completion of online applications for a new financial product or service.

“By pioneering the low-code market and having a vision to transform how enterprise software is delivered,” ieDigital Commercial Director Garry Larner said, “the OutSystems platform perfectly complements our existing product-offering. We look forward to working alongside them to continue delivering market-leading financial technology that makes a real impact to all that use it.”

ieDigital noted that the partnership will leverage and further build upon the Interact Application Suite, an approach ieDigital used in a previous collaboration with Cambridge & Counties Bank to help the firm combat financial crime. The result was a more streamlined customer onboarding process, enhanced automation for both middle and back office workers, and better capacity and knowledge to support the development of applications going forward – including an option for Cambridge & Counties Bank to build its own in-house development capability.

Founded in 1984 and headquartered in London, U.K., ieDigital demonstrated its Money Fitness solution at FinovateFall 2018. The technology helps credit unions effectively compete with the wave of competition from “digital-first” providers with a forward-looking personalized service that credit union members can use to better manage their day-to-day finances, make better financial decisions, and improve their overall financial health.

More recently, ieDigital launched its customer retention solution Interact Switch, which is designed to help mortgage lenders retain customers at product offer maturity. The technology enables mortgage lenders to function more efficiently by cutting down on paper-based, mortgage representative, and third-party costs. Also this fall, ieDigital announced a partnership with Darlington Building Society and a collaboration with DF Capital to help the savings and commercial lending bank to launch a new digital interactive channel for its savings customers.

An alum of our developers conference, FinDEVr NewYork 2017, Boston, Massachusetts OutSystems specializes in cloud-native, low-code app development. More than 14 million people currently use OutSystems’s platform to build solutions such as mobile apps and consumer websites, as well as extensions of core systems from Microsoft and Salesforce. The latest platform edition from the company, code named Project Neo, marries the productivity benefits of visual, model-based development with state-of-the-art container- and Kubernetes-based cloud architecture. The technology is hosted on Amazon Web Services to make it easy for any company to build customized, cloud-based apps that scale globally and can be continuously updated.

“Developers should be the artisans of innovation in their organization, but they are mired in complexity that stifles their ability to innovative and differentiate,” OutSystems CEO Paulo Rosado said. “Instead of using their talents to fix, change, and maintain code and aging systems, you can give them industry-leading tools that unleash their creativity on your business, and achieve massive competitive advantage.”

Consumer payment services company Klarna has selected account-to-account (A2A) payments company GoCardless to offer debit bank payments to its U.S. clients.

Specifically, Klarna will use GoCardless’ technology to transfer funds via ACH for its Pay in 4 offering that enables customers to split any purchase into four interest-free payments both online and in-store.

GoCardless CEO and Co-Founder Hiroki Takeuchi said that he anticipates alternative payment methods to experience rapid growth as leveraging debt falls out of favor. “Over the next few years we expect account-to-account payments to challenge the dominance of cards as they tap into changing consumer demand and provide merchants significant benefits in terms of cost, conversion and churn,” Takeuchi said.

Klarna CTO Koen Köppen noted that the U.S. is a key market for Klarna. The company doubled its customer base in the last year, and now has more than 21 million U.S. customers. “To continue along that trajectory,” Köppen noted, “we need partners that not only provide our consumers and retailers more choice and control but also offer us cutting-edge technology and best-in-class service. We’re excited to work with GoCardless and leverage its expertise in account-to-account payments as we expand in the U.S.”

GoCardless, which wonBest Enterprise Payments Solution at the Finovate Awards earlier this year, was founded in 2011. The U.K.-based company’s technology helps merchants collect recurring and one-off payments from customers via ACH transfers. Businesses can integrate GoCardless’ API to automate payment collection and reconciliation billing for subscription and invoice payments. Among GoCardless’ clients are DocuSign, Survey Monkey, and Box.com.

Today’s news about Klarna’s new ACH payment capabilities for U.S. customers is the latest in the company’s recent push into the North American region. Last month, Klarna announced it is adding its Pay Now option to its U.S. payment services. The company also unveiled plans to launch its physical debit card in the U.S. market.

GoCardless entered the U.S. market in 2019 and has since opened two offices in New York City and one in San Francisco. By the end of next year, GoCardless plans to grow its U.S. team by another 125%.

The announcement that global identity verification specialist Trulioo has signed up a sextet of cryptocurrency companies as its latest round of customers is a testament to the growing maturity of startups in the digital asset business. The six firms – Centbee, GMO Trust, Omni Matrix, Skilling, Strike Protocols, and Vintech Capital – will use Trulioo’s GlobalGateway to enable them to meet KYC and AML compliance requirements.

“The pandemic democratized the world of financial services, helping casual or novice investors explore financial trading online,” Trulioo CEO Steve Munford explained. “With cryptocurrencies becoming mainstream, digital asset issuers and exchanges understood the need to bolster their identity verification programs to securely and seamlessly onboard a huge uptick in users while meeting compliance obligations.”

Trulioo’s GlobalGateway gives companies access to more than 400 data sources to confidently and securely verify the identities of more than five billion individuals worldwide via a single API. The platform provides identity verification with real time comprehensive match results, ID document verification using intuitive image capture and automated verification technology, and AML (anti-money laundering) watchlists with extensive international coverage. This coverage includes sanction lists from law enforcement and government regulatory entities such as financial and securities commissions.

The solution also provides Business Verification, which Trulioo demonstrated during its most recent appearance on the Finovate stage last year at FinovateEurope in Berlin, Germany. At the conference, the company demonstrated its GlobalGateway Business Verification technology which provides regulated entities with certainty about their business customers and assures compliance with Customer Due Diligence (CDD) requirements. Leveraging key company data from government sources in more than 80 countries and from non-government sources in more than 195 countries, GlobalGateway Business Verification automates the complete Know Your Business workflow, enabling companies to verify business entity data, conduct watchlists reviews, and identify and verify a business’ beneficial owners.

Founded in 2011 and headquartered in Vancouver, British Columbia, Canada, Trulioo has raised more than $474 million in funding. The company’s most recent fundraising was a Series D investment in June of this year that added $394 million to the firm’s coffers. The round was led by TCV.

As the name implies, super apps are super in nature. They differentiate themselves from traditional apps by offering a much wider variety of services than fintechs typically offer, acting as platforms that fulfill more than just a singular purpose.

We recently spoke with Marcell King, Chief Innovation Officer of Payveris, for his view on the battle among banks, fintechs, and super apps, as well as his outlook on the future of super apps both in the U.S. and abroad.

What’s your definition of a super app?

Marcell King: A super app is a single place for users to go to for all of their financial, communication, money movement, entertainment, and shopping needs. It’s designed to provide consumers with the utmost convenience and frictionless access to a variety of services they use on a day-to-day basis. A super app earns a piece of the spend on everything the consumer purchases and can leverage this data to deliver personalized experiences and cross-sell products or services. The consumer gets ultimate convenience and the owner of the Super App increases the size of its revenue pool.

How do Super apps threaten FIs and fintechs?

King: The possibility of one dominant super app emerging in the US poses the biggest threat to smaller-asset financial institutions in particular because they often can’t match the resources Big Tech and Big Finance bring to the table. This answer grows more complicated depending on how you define what constitutes a true “fintech” company these days. Many fintechs have developed micro-niche applications, which a super app could likely consider to be a “feature” in the app. In that case, it would be easier for a consumer to access the feature in the super app versus opening up another app for the same purpose.

What opportunities do super apps have for Fis and fintechs?

King: I believe this could go one of two ways, or both. Use case number one is that the super app partners with specific types of financial institutions and fintechs for specific white label services. For instance, PayPal could partner with a large bank to support added new financial management features, offering consumers checking and savings accounts from the partner bank or credit union. The other is that multiple financial institutions link their branded services to the super app brand, enabling the super app to be a consolidator of services, similar to a brick and mortar mall. In both cases, the super app uses its brand power to consolidate services, making it easier for the consumer to get the benefit of convenience. The super app generates revenue and receives data that can be leveraged to cross-sell relevant products and services to that individual consumer.

Why haven’t super apps been successful in North America and Europe?

King: There are a few reasons for this. First, with intense competition between tech giants, the market is more fragmented with popular services such as Facebook’s WhatsApp and Apple’s iMessage. There isn’t one player dominating a specific part of the market, which makes it more challenging to create a super app experience.

Another reason is super apps rely on a plethora of user data to be successful, which is a challenge in the U.S. and Europe, where there are more laws in place to govern consumer data and privacy. Both countries have a record of limiting the growth of companies that become powerful to protect consumer rights. Most recently, the U.S. Consumer Financial Protection Bureau issued orders for info to tech giants, including Google and Amazon, on their use of consumer data. This will make it more challenging for one company to become a dominant super app.

What will it take for super apps to gain popularity in geographies outside of Asia?

King: We’re beginning to see the super app model emerge in places like Latin America. Due to regulation, it’s clear that North America and Europe will need government support in order for super apps to gain popularity. For instance, China’s WeChat and AliPay have benefited from strong government support and its regulation to block WhatsApp, Signal, and Facebook, which has removed the risk of competition.

A super app will need to gain popularity and trust in one market in which it can then expand into other services to succeed. Uber, for example, started out as a rideshare app disrupting a legacy industry when ridesharing was an untapped market. Even with competition emerging since its inception, Uber commands a majority of the market share. Due to its early success, Uber has been able to expand and establish itself as a top meal delivery service.

Walgreens is in the fintech headlines again. Today, the drugstore chain and challenger bank Chime have partnered to allow Chime customers to deposit cash at Walgreens’ brick-and-mortar locations.

Customers can deposit their cash for free at 8,500+ Walgreens locations. In its announcement, Chime makes the comparison between Walgreens locations and bank branches, mentioning that the new partnership offers more walk-in locations than users have with any bank in the U.S. Also worth noting is the fact that 78% of Americans live within five miles of a Walgreens store.

“We know having access to a physical location for cash deposits is important to our members, and until recently, the options have been limited,” said Chime Co-founder and CEO Chris Britt.

Chime users can make deposits by handing the Walgreens cashier their cash and their Chime debit card. Once the cashier loads the funds into the user’s account, the money is available immediately. Customers are limited to three $1,000 cash deposits each day and $10,000 each month.

Chime’s Walgreens partnership adds to the company’s existing cash deposit capabilities. Customers can also deposit cash at 75,000+ other retail locations including Walmart, CVS, and 7-Eleven, though these stores charge a loading fee of anywhere from $3 to $5. Partnerships with pervasive retailers such as these are key for Chime, since many of the challenger bank’s users receive earnings and tips in cash.

Today’s news comes as Walgreens itself is entering the alternative banking arena. The company announced earlier this year it is partnering with InComm and Mastercard to launch a new bank account offering with a debit card that will pair with a mobile banking app and in-person service at Walgreens locations.

Chime was founded in 2013 and has since risen to the top of challenger banks in the U.S. The company has 20 million customers and boasts a valuation of $25 billion (though the accuracy of that number has been disputed).

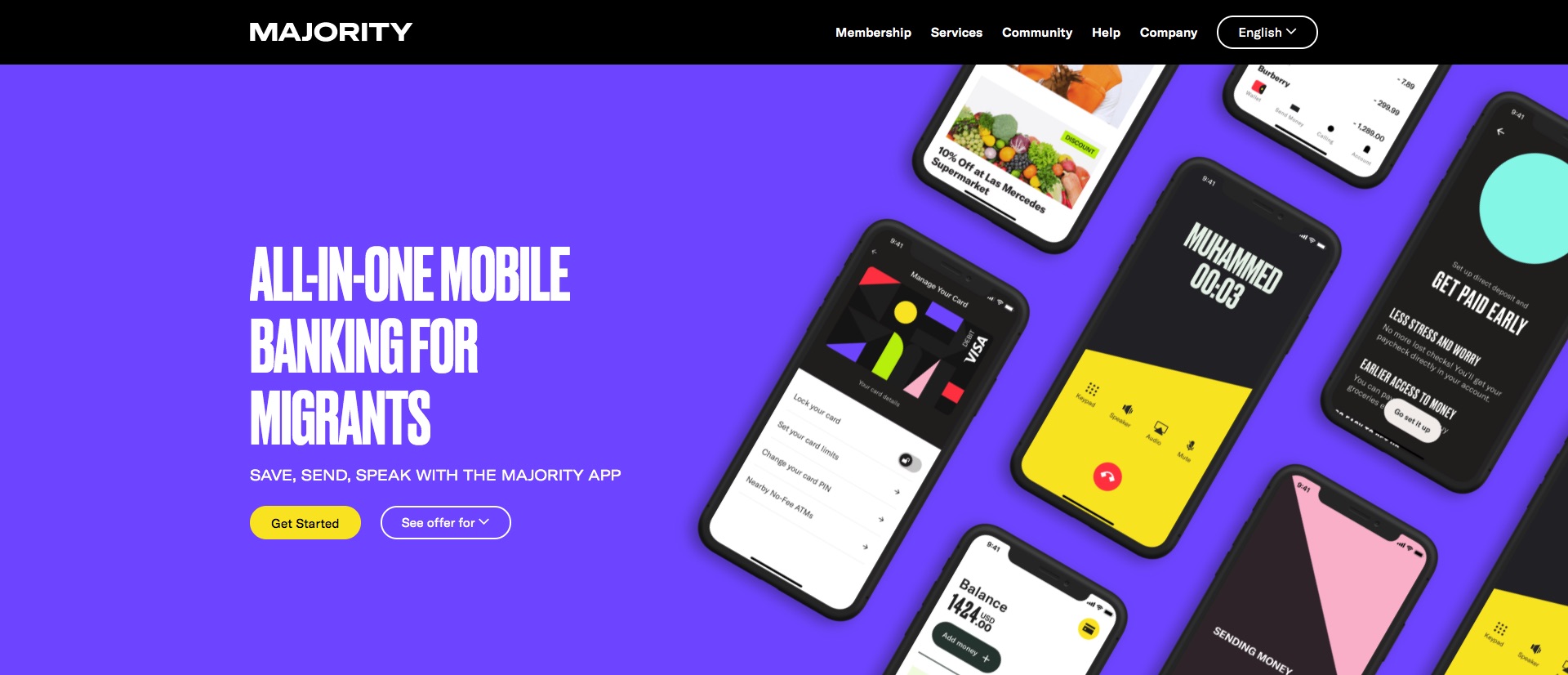

At a time when concerns about illegal immigration have complicated the mostly positive attitude most Americans have toward immigrants in general, it is heartening to see that innovators and entrepreneurs in the fintech space are finding ways to bring vital services to those fleeing often-horrific conditions to find better lives in another land.

One such company is MAJORITY, a U.S.-based, mobile banking service designed specifically to serve the migrant communities in the States.

Founded in 2019, MAJORITY offers a banking app that provides an no-overdraft-fee, FDIC-insured bank account, a debit card with community discounts from local merchants, no-fee remittances, and “at-cost” international calling. The app is available for $5 a month. Company founder and CEO Magnus Larsson said that MAJORITY already has saved its Cuban members $21 a month on average and its Nigerian members $10 a month on average thanks to its “cost-efficient service offerings.”

MAJORITY also offers members the services of its hundreds of local advisors who help onboard and support new customers in their native languages. And while MAJORITY’s banking services are available in all 50 states, the company’s advisors are currently operating only in Texas and Florida.

Larsson explained the utility of the company’s human advisors in a conversation with TechCrunch. He described how a MAJORITY customer could meet up with an advisor outside of a grocery store and, within minutes, have their bank information, a Visa debit card, and the ability to use that grocery store to send money to another country.

“Migrants, by their very definition, are the most ambitious people in the world, striving for success in a new country – but they are lacking the necessary tools,” Larsson said. “Migrant-relevant financial services come with extensive fees that feel overwhelming for all people, but even more intimidating for those trying to navigate an unfamiliar system. At MAJORITY, we seek to remove the uncertainty that comes with international financial services and do our part to better facilitate a world where people are valued on their positive impact, not their country of origin.”

MAJORITY estimates that there are more than 258 million migrants worldwide, with nearly 50 million migrants in the U.S. – who are under-banked, un-banked, or otherwise experiencing “insurmountable barriers” when it comes to financially integrating into their new country. And courtesy of a $27 million investment MAJORITY announced last week, the company now has new resources to help.

“Our mission, as a migrant-led company, has always been to serve the migrant communities with the unique resources they need—financial and otherwise—and this latest funding will help us continue to perfect our services and support this community that is the backbone of America,” Larsson said.

The Series A round was led by Valar Ventures and featured the participation of Avid Ventures, Heartcore Capital, and a number of Nordic fintech founders. MAJORITY now has $46 million in total funding, which includes $19 million in seed funding the company raised earlier this year.

Accompanying its funding news, MAJORITY also announced that it is introducing a new feature that will enable migrants to sign up for a bank account without requiring a social security number. Instead, applicants will be able to use a government ID from any other country and proof of U.S. residency to access MAJORITY’s banking services.

“A bank account is the starting point to so many other things for someone moving to a new country, and American bureaucratic delays and backup shouldn’t prevent people from being able to establish themselves here,” Larsson said. An immigrant himself from Sweden, Larsson is currently waiting for visa approval in order to move from Stockholm to Miami, Florida, to further build out MAJORITY. He also looks forward to being able to grow the company from its current 65+ employees in Sweden and the U.S.

Supply chain finance company Tradeshift has raised more than $200 million in combined equity and debt funding. The San Francisco, California-based firm, which made its Finovate debut in 2012 at FinovateEurope, now has an estimated valuation of $2 billion according to Reuters. Tradeshift CEO and founder Christian Lanng, who did not confirm the valuation with Reuters, did tell the company that the new funding will help Tradeshift “refinance parts of our balance sheet focusing us on long term continued growth.”

The investment featured participation from Koch Industries, IDC Ventures, LUN Partners, Private Shares, and Fuel Capital. According to Crunchbase, the investment gives Tradeshift more than $1 billion in equity funding.

Founded in 2010, Tradeshift has become a leading B2B e-invoicing and accounts payable automation company. With more than 1.5 million companies connected on its platform, Tradeshift has processed more than $1 trillion in cumulative value since inception, a figure that has doubled in two years. The company’s offerings include its B2B marketplace for e-procurement Tradeshift Buy, its automated accounts payable platformTradeshift Pay, a supplier analytics solution Tradeshift Engage, early payment option Tradeshift Cash, and its virtual credit card offering Tradeshift Go.

By hosting all of these features on a single trade technology platform, Tradeshift enables businesses to transition from being “future proof” to “future flexible,” and to scale their operations virtually without limit. An early adherent of the value of embedded technologies, Tradeshift empowers companies to “continually digitize” their supply chain and take advantage of a dynamic, digital network of connected buyers and sellers.

“Embedding financial services directly into our product unclogs the flow of working capital across supply chains, eliminating a significant pressure point in the buyer-suppliers relationship,” Lanng explained. “As one of the first companies to recognize the potential for embedded finance in SaaS, we have been betting on the convergence of Fintech and SaaS products for awhile. We’ve built the technology and distribution channels to capitalize on what is now one of the defining trends in our industry.”

Named to Fast Company’s list of the World’s Most Innovative Companies for 2020, Tradeshift launched its cross-border e-invoicing solution last month, reducing friction in cross-border transaction flows for companies doing business in China. In October, the company announced that its Tradeshift Go virtual credit card solution was on track to process $2.5 billion in charge volume in 2021, a 6x increase over 2020. Tradeshift has forged partnerships this year with the Danish Export Credit Agency, trade and supply chain financing platform Raindew Trade, and Qatar-based Gulf Warehousing Company (GWC).

Selling nearly 290 million shares priced at $9 in its initial public offering on the New York Stock Exchange this week, Brazilian digital bank Nubank has raised $2.6 billion, reaching a market value of $41 billion. An alumni of Finovate’s developer’s conference FinDEVr in 2016, Nubank is now the most valuable financial institution in Latin America in addition to being the world’s biggest digital bank. CEO David Vélez, who co-founded the company in 2013 with an initial investment of $2 million from Sequoia Capital and Kaszek Ventures, now owns a stake in the company worth $8.9 billion at the IPO price.

“We don’t think the banking branch will survive the way it is,” Vélez said to CNBC this week. “It is too costly to serve the majority of users, especially in emerging markets where you have a very high cost of operations, so a lot of that physical infrastructure will probably disappear.” Vélez predicted that most financial services providers will transition into digital entities in the next five to ten years because of this, leading to an increased focus on customer service as well as lower costs and interest rates.

With more than 48 million customers in Brazil, Mexico, and Colombia, and onboarding more than two million new customers a month on average, Nubank offers financial products for spending, savings, investments, loans, and insurance. The company claims to have provided more than five million people with their first credit card or bank account as of September 30, and to have saved its customers more than $4 billion (R$27 billion) in bank fees and more than 113 million hours of waiting time since inception.

Vélez said that the capital from the IPO will help fuel Nubank’s expansion in Mexico and Colombia, en route to becoming a truly pan-Latin American banking services provider. “There is a lot of opportunity to build the next generation of financial services, so we will continue to invest and grow for a very long time,” Vélez said an interview with the Financial Times.

FinovateEurope 2022 is right around the corner. If you are an innovative fintech company with new technology to show, then there’s no better time than now and no better forum than FinovateEurope. To learn more about how to demo your latest innovation at FinovateEurope 2022 in London, March 22-23, visit our FinovateEurope hub today!

Here is our look at fintech innovation around the world.

CinetPay, a digital finance platform serving merchants in French-speaking Africa secured $2.4 million in seed funding from 4DX Ventures and Flutterwave.

Online fraud prevention company SEON inked an agreement with a pair of African neobanks, Carbon and FairMoney.

South African device identity and authentication solutions provider Entersektannounced a “significant investment” from U.S. private equity firm Accel-KKR.

German biometrics and digital identity verification company Passbase secured $10 million in Series A funding, as well as another $3.5 million in seed-2 investment.