This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

FinovateFall 2023 takes place in New York over September 11 through 13 with the demos on the first two days. Register today and save your spot.

In less than a month, you’ll see it all at FinovateFall. Technology launches, startup debuts, fresh perspectives, and industry leaders from over 60 demoing companies. Here’s a look at the latest lineup:

With so many diverse organizations taking the stage over the first two days, you may want to narrow in on the technology that best fits your needs. Check out the sneak peeks for a quick look into each demo company, its innovation and features, and what makes it great.

Stayed tuned for new demo additions leading up to the event, and don’t miss your chance to register!

In the dynamic realm of financial advisory, the voice of experience is vital in understanding the present landscape. We recently spoke with intelliflo Vice President of Customer Management Lisa Jacobs on the challenges, opportunities, and trends in the advisory space.

Jacobs brings her 15+ years of experience to our conversation that sheds light on how firms can overcome labor shortages, resource constraints, constantly changing technology, and volatile regulations in the financial advice space. She also addresses how advisors can balance and manage the ongoing high-tech vs. high-touch approach.

What are some of the top challenges and opportunities currently facing the financial advisory space?

Lisa Jacobs: We recently surveyed over 400 financial advisors and found that 80% of them believe more people are seeking advice and can’t find or access that help. This is both an enormous challenge and opportunity. Even though more people are seeking professional guidance, advisors across the board are stretched thin, making it nearly impossible to take on new clients without additional support. This prohibits advisors from growing their revenue and supporting more people, leaving many without the help they need. intelliflo was formed to bridge the advice gap; we’re committed to providing the tools and solutions to help advisors widen access to financial advice.

How can technology be leveraged to overcome these challenges and support financial advisors?

Jacobs: Modern technology has the power to help advisors address these resource restraints. In just about every industry, technology yields efficiencies, but the best tech also increases your customer’s satisfaction, too. In our industry, this is becoming known as a hybrid advice strategy – a flexible model in which clients in earlier stages of the financial advice journey are primarily served via digital channels and tools, and technology adds more to the customer experience for top clients with better outcomes.

To effectively embrace more digital tools, advisors are increasingly moving away from stand-along software tools that can’t integrate with other parts of their tech stack to avoid having to learn and log on to multiple systems. Many are seeking an all-in-one advisor experience to increase efficiencies and, in turn, provide a more unified client experience. If approached the right way, technology has the power to enable advisors to accomplish more with existing resources while simultaneously strengthening client relationships.

What advice do you have for financial advisors that are evaluating the many different technology providers out there?

Jacobs: Technology can only be effective if it is easy to use and manage. Otherwise, it might act as more of a hindrance than a benefit. That same survey of advisors underpinned this idea, revealing that the top three biggest barriers to adopting new technology for advisors are integration challenges (57%), time to install (41%), and employee time and resources to manage the technology (38%).

When vetting the many providers and solutions available in the market, advisors should consider these common areas of friction, prioritizing technology that is open and easily integrated, is flexible (which often means cloud-based), and has proven, responsive service and support teams.

Changing regulation seems to be a pressing topic this year for the fintech industry at large. What is the best way for wealth management companies to stay ahead?

A strong way to stay on top of changing regulations and compliance mandates is to collaborate with resources such as peer groups, associations, and technology partners to discuss these issues and what needs to be altered in response. We also increasingly see firms rely on partnership models with third party vendors, looking to outsource key functions and support such as compliance. However, advisors must be sure their partners are thoroughly vetted and monitored on an ongoing basis; not all partners are created equal.

What are the top trends in the advisory space to watch for the second half of the year?

Jacobs: In addition to the continued rise of the hybrid advice model, the evolving role of the advisor is an important trend to watch. A wider skill set is increasingly expected from advisors, including the ability to provide comprehensive guidance around critical life events and situations that fall outside of the traditional financial advisory relationship. For instance, clients are more frequently asking which insurance plans and options are best for their unique scenarios. And as their parents age, Millennials are seeking guidance from advisors on long-term care and arrangement options. These conversations can be emotionally charged, and empathy will become a key trait for the modern advisor. This is another reason why advisors must determine how to strategically leverage technology to make time for higher-value conversations and plans.

Mahalo Banking and Larky have announced an expanded partnership to enhance account holder engagement for Mahalo clients.

The partnership will integrate Larky’s nudge platform into Mahalo’s online banking platform.

Larky made its Finovate debut in 2014. Mahalo Banking will make its Finovate debut next month at FinovateFall.

An expanded partnership between a pair of Finovate alums is designed to help boost account holder engagement. Mahalo Banking, a banking solution provider for credit unions, and account holder engagement technology company Larky announced this week that they are building on their relationship by integrating Larky’s nudge technology into Mahalo’s online banking platform.

“Our partnership with Larky enables us to offer our credit union clients an invaluable tool for member engagement at a time when the market needs new approaches to nurture and grow depositor relationships,” Mahalo Banking co-founder and COO Denny Howell said.

The integration with Larky’s nudge platform will give account holders notifications about the different product and service offerings from their financial institution. Notifications also alert account holders to contextually relevant information about their branch. Financial institutions benefit from access to analytics and A/B testing to learn how their customer and member engagement programs are working. Mahalo customers will also be able to access Larky’s nudgeScore. This solution leverages AI to predict the performance of new push notifications.

“We’re thrilled to expand our partnership with Mahalo, opening doors for their clients to harness the power of our nudge platform’s tailored and proactive engagement capabilities,” Larky VP of Growth Scott Brown said. “This reinforced partnership interweaves the unique assets of both organizations, bolstering the digital banking landscape for consumers and fostering expansion for community based financial institutions.”

August has been a busy month for the Ann Arbor, Michigan based company. Larky just reported that Innovations FCU has gone live with its customer engagement platform. And a few days ago, Larky announced a collaboration with credit union technology partner Trellance and Michigan State University Federal Credit Union (MSUFCU). The goal of the partnership is to build a unique, data-centric solution that leverages enhanced, AI-driven segmentation and targeting for MSUFCU. This will enable MSUFCU to create and execute more engaging campaigns to boost tap rates and increase engagement.

Founded in 2012 and headquartered in Ann Arbor, Michigan, Larky made its Finovate debut at FinovateFall in 2014.

Mahalo Banking will be making its first Finovate appearance next month at FinovateFall. The company is a Credit Union Service Organization (CUSO) that serves as a banking partner for credit unions. The company’s platform features deep integrations into credit union cores to provide robust features sets across all delivery platforms in order to deliver a true omni-channel experience. Mahalo is also unique insofar as its platform features functionality to support customers with cognitive distinctions such as dyslexia, autism, epilepsy, visual impairments, and more.

Like Larky, Mahalo also has been on a furious partnership-making pace this year. Last month, Mahalo announced a partnership with Gerber Federal Credit Union, a Michigan-based financial institution with $225 million in assets. In June, Mahalo teamed up with RiverLand FCU, an FI based in New Orleans with more than $300 million in assets. Also, in May, Mahalo announced new partnerships with two credit unions: ParkView FCU and Rock Valley Credit Union. ParkView FCU is based in Harrisonburg, Virginia, and has $350 million in assets. Rock Valley Credit Union is headquartered in Loves, Park, Illinois, and has assets of $150 million.

Mahalo Banking is based in Troy, Michigan. Jim Stickley is CEO.

Agora Data has landed $160 million in privately placed term financing.

The investment marks Agora Data’s fourth privately placed term financing round.

While there is no word on total funding, today’s financing adds to the $100 million revolving credit line Agora Data received from Credit Suisse in September 2022.

Agora Data, a company that helps buy here pay here (BHPH) car dealers offer in-house financing, secured $160 million in privately placed term financing this month. The round represents the fourth privately placed term financing the company has received since it was founded in 2017.

“Fueling Agora’s mission to enable any car dealer to be a finance company, this $160 million private term financing provides additional funding capacity and reiterates our commitment to our customers’ future growth,” said company CEO Steve Burke.

While there is no data on the amounts of the company’s previous three privately placed term financing rounds, Agora Data said that each of them performed better than projected. Today’s financing adds to the $100 million revolving credit facility the company received from Credit Suisse last September.

Founded in 2017, Agora Data’s Agora Capital helps car dealerships lend to non-prime customers. Lending to unattractive borrowers ultimately helps dealers sell more cars. To provide a competitive interest rate on these sub-prime loans, the company leverages AI to analyze over $350 billion in loan data. Agora Data also offers Agora Trade, a product that allows investors to buy a portfolio of seasoned auto loans at a lower rate of default.

Texas-based Agora Data targets the underbanked community and its strategy will likely fair well as the cost of living crisis, combined with a high interest rate environment, continues. Competitors in the auto financing space include CreditIQ, Creditas, Caribou (formerly known as MotoRefi), and others.

A look at the companies demoing at FinovateFall in New York on September 11 and 12. Register today and save your spot.

SESAMm is a fintech company specializing in big data and artificial intelligence. It provides analytics and investment signals from over 20 billion web data points using NLP.

Features

SESAMm is incorporating a version of Chat GPT into its solutions. Going forward, users will have the ability to interact with SESAMm to seamlessly monitor ESG controversies and produce ESG analysis.

Why it’s great

These new features, powered by generative AI, reinforce SESAMm’s commitment to developing solutions that enhance risk mitigation and streamline processes for financial firms.

Presenter

Sylvain Forté, CEO Forté’s passion for artificial intelligence and finance led him to create SESAMm in 2014. He holds a double degree in engineering from Germany and France. LinkedIn

A look at the companies demoing at FinovateFall in New York on September 11 and 12. Register today and save your spot.

Fundica’s funding search engine serves as a business client acquisition and retention tool for FIs and other business-support organizations by enabling them to truly democratize access to funding.

Features

Effortlessly generate new business leads and retain clients

Gather business firmographics and funding needs

Organically promote diversity, equity, and inclusion

Why it’s great

Fundica’s funding search engine makes business-support organizations a more complete, one-stop funding destination for SMBs by effortlessly extending their service offering at scale.

Presenter

Mike Lee, CEO & Co-Founder Lee has held leadership roles in technology organizations, secured over $350M in government funding, and holds Engineering, MBA, and CFA designations. LinkedIn

A look at the companies demoing at FinovateFall in New York on September 11 and 12. Register today and save your spot.

1Kosmos’BlockID provides workers and customers with convenient, passwordless, multi-factor authentication with the added security of identity verification to help prevent identity fraud and account takeover.

Features

Self-service, KYC-compliant identity proofing with tailorable onboarding journeys

Reusable, NIST certified IAL3/AA3 MFA for strong customer authentication

GDPR-compliant privacy-by-design with immutable audit trail

Why it’s great

1Kosmos’ software-as-a-service platform, certified to NIST, FIDO2 and iBeta PAD2 specifications, supports identity proofing and passwordless multi-factor authentication for workers and customers.

Presenters

Sheetal Elangovan, Product Manager Elangovan is the Product Manager of the admin experience on the BlockID platform and Product Design Lead for all products being built at 1Kosmos. LinkedIn

Jens Hinrichsen, SVP, North American Sales Hinrichsen is a career business growth leader, having held a variety of sales and marketing roles across the cybersecurity, fraud, and digital user experience spaces. LinkedIn

A look at the companies demoing at FinovateFall in New York on September 11 and 12. Register today and save your spot.

LemonadeLXP is an award-winning digital growth platform for FIs and fintechs.

Features

A learning experience platform that turns staff into digital experts

A digital enablement platform (Digital Academy) that supports staff and customers in the flow of work

Why it’s great

LemonadeLXP is trusted by over 70 FIs and fintechs. Why? Lemonade LXP has increased digital fluency amongst frontline staff by more than 93%, and the company’s support tools are increasing digital banking confidence by more than 92%.

Presenter

John Findlay, CEO & Founder Findlay co-founded Launchfire in 1999, a game-based promotions company. In 2018, LemonadeLXP emerged to help FIs and fintechs grow their digital banking business. LinkedIn

A look at the companies demoing at FinovateFall in New York on September 11 and 12. Register today and save your spot.

Regulo.ai provides leading FCC innovators with patented face hashing and is backed by an expert team, proprietary datasets, and zero-false-positive fraud tech.

Features

Face Recognition: Pioneering face recognition for novel use cases

Face Datasets: Unique datasets drive exceptional outcomes

PET: Proprietary tech ensures privacy in sharing face biometrics

Why it’s great

The face is unique to every individual; therefore, face screening helps eliminate false positives. Regulo’s proprietary, face-based, privacy enhancing technology helps companies comply with privacy regulations.

Presenter

Ravi Madavaram, Co-Founder & CEO Madavaram is an experienced AI leader skilled in crafting cognitive services, machine vision, and reinforcement learning products deployed across customer service, marcom, audit, and fraud domains. LinkedIn

A look at the companies demoing at FinovateFall in New York on September 11 and 12. Register today and save your spot.

Leading financial institutions implement Trustworthy for their digital banking experiences to secure and manage customers’ and members’ most sensitive information.

Features

Modern digital safety deposit box

Multiple collaborators in one digital platform

Most sensitive information tokenized, including passwords, identification, and account numbers

Why it’s great

Trustworthy helps FIs build strong customer and member relationships by quarterbacking a household’s complexities for a business’ customers and members.

Presenter

Daniel McCool, Co-Founder & CPO McCool has 20 years of product management experience as a founder and product leader within fintech, energy, and consumer technologies.

A look at the companies demoing at FinovateFall in New York on September 11 and 12. Register today and save your spot.

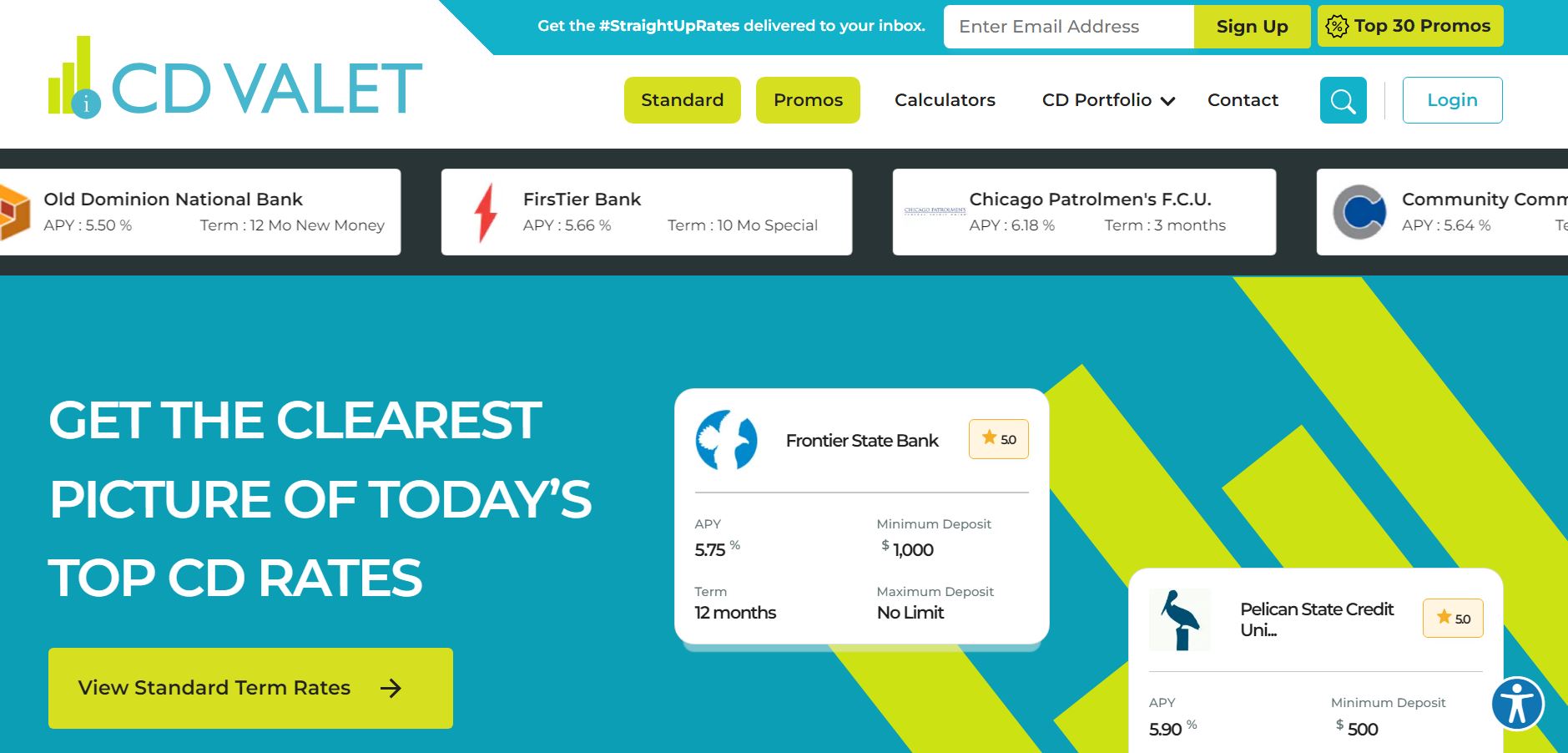

CD Valet offers a new channel for financial institutions to easily raise retail deposits from a nationwide CD marketplace where they can market their rates, acquire leads, and open new accounts.

Features

Low-cost, end-to-end account opening solution with major core platform integration

Origination platform with smooth, intuitive user experience

Customizable to FI size

Why it’s great

Given that new account application abandonment rates are as high as 50% for many traditional banks and credit unions, CD Valet solves this problem with a smooth digital account opening solution.

Presenters

Josh Williams, Head of Partnerships Williams collaborates with fintechs, marketplaces, and brands to integrate financial services into their customer experience. LinkedIn

Howie Wu, Head of Product With over 15 years of experience providing leadership and strategic planning in digital banking, Wu drives innovation of digital banking solutions to enhance client experience. LinkedIn

Courtesy of a just-secured regulatory approval from the National Futures Association, Coinbase’s U.S. customers will soon get the opportunity to trade futures contracts on cryptocurrencies. Coinbase’s Coinbase Financial Markets has been granted authority to operate as a Futures Commission Merchant (FCM) and offer eligible customers in the U.S. access to crypto futures trading on the Coinbase platform.

In a blog post at the Coinbase website, company Head of Institutional Product, Greg Tusar called the approval a “watershed moment” in the project to bring regulated cryptocurrency products to U.S. customers. The ruling comes as Coinbase is at odds with other regulatory bodies – such as the SEC – over its operating practices.

The ruling also comes at a time when the crypto derivatives market around the world has climbed to 75% of all crypto trading volume. Tusar called this market “a critical trader access point.” This is because crypto derivatives enable traders to participate with more leverage and less upfront capital, as well as give cryptocurrency holders the ability to express long and short positions, and hedge risk.

“Where regulations are clear and sensible, we will work with regulators to receive the authorizations needed to offer products that align with our purpose of using crypto to update the financial system to advance economic freedom and opportunity,” Tusar wrote.

Coinbase made its Finovate debut in 2014. The San Francisco, California-based fintech was founded in 2012.

eToro’s Crypto Trends

Social trading and investment platform eToro announced a new partnership to help its customers stay on top of the latest information about cryptocurrencies. The firm has teamed up with analysis company Reflexivity Research in a content partnership called “BTC etc.” that will provide a weekly overview of the cryptocurrency market as well as a monthly podcast. The weekly overview will focus on key trends. The podcast will feature experts from eToro, Reflexivity Research, and the broader cryptocurrency industry.

“As a crypto pioneer, we see it as our responsibility to provide accessible, timely, and relevant content for our users,” eToro Editor in Chief Mati Alon said. “As the market matures, cryptoassets deserve the same level of attention and coverage as other financial assets. We are excited to collaborate with Reflexivity to increase understanding of crypto.”

A Finovate alum since 2011, eToro has won Best of Show at each of its six Finovate appearances. The company offers trading and investing in stocks, options, and exchange-traded funds (ETFs), as well as cryptocurrencies. eToro offers 0% commissions, the ability to trade fractional shares, and a social network to enable traders and investors to benefit from the wisdom of the platform’s top performers.

EToro has become increasingly bullish on the prospects for cryptocurrencies. The company’s Global Markets Strategist Ben Laidler was quoted earlier this week highlighting three key developments that could put cryptocurrencies back on track by making it easier for institutions to participate in the market.

CBDCs Gain Ground in Brazil, Raise Doubts in Canada

The arguments for and against central bank digital currencies (CBDCs) got an international airing of sorts in recent days.

In Brazil, the country’s central bank has given its CBDC an official name – and logo. Commonly referred to as the “digital real,” the Brazilian Central Bank has decided to call its new digital currency, the Drex. The name refers to both the assets colloquial name, “Real Digital,” with an “e” for “electronic” and an “x” to represent a variety of notions including the concept of “modernity and connection.”

“Drex arrives to make life easier for Brazilians” a press release from the country’s central bank pronounced. “It will provide a secure and regulated environment for developing new businesses and more democratic access to the benefits of the economy’s digitization, both for individuals and entrepreneurs.”

Among the projected use cases for the digital currency are government benefit payouts, which would use a tokenized version of the currency. The bank also believes that the Drex will help accelerate digitalization in the financial sector and ultimately promote financial inclusion.

Meanwhile, some five thousand miles north, the concept of central bank digital currencies is getting a much cooler reception. A new report from the Bank of Canada cast a dim light on the prospect of mass CBDC adoption by Canadians. The blame was placed on the wide number of payment options Canadian consumers and businesses already have.

The staff discussion paper, “Unmet Payment Needs and a Central Bank Digital Currency,” envisions a hypothetical cashless environment, and then considers how a CBDC would solve unmet payment needs in such a society.

The report concludes that for a CBDC to benefit those who have unmet payment needs, the digital currency would first have to secure widespread adoption among the majority of the population. This would be necessary to ensure sufficient digital currency adoption by merchants. The challenge is that insofar as the majority of consumers “already have access to a range of payment options,” it would be unlikely for a significant enough number of these consumers to both widely adopt the digital currency as well as use the CBDC at scale.

The insights from the paper should prove valuable to those who support digital currencies, especially to the degree that digital currencies allegedly support financial inclusion. “The minority of consumers with unmet payment needs will be able to benefit from a CBDC,” the report writers conclude, “if the majority of consumers experience material benefits and therefore drive its use.”