This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

This week, Klarna Checkout, also known as KCO, announced its official rebrand as Kustom. The rebrand comes 12 years after the launch of Klarna Checkout, which at the time set a new standard for e-commerce in Northern Europe. The rebrand also arrives months after Klarna sold KCO to a consortium of investors led by BLQ Invest CEO and Founding Partner Kamjar Hajabdolahi.

“Klarna Checkout is very dear to me, and the impact it’s had on Klarna’s journey is immense,” Klarna CEO and Co-Founder Sebastian Siemiatkowski said in June when the divestment was announced. “I’m so pleased it’s finding a new home, with owners who are carefully handpicked to continue to create outstanding value for our merchant partners.”

A new home back then, and now, a new name. As Kustom, the digital checkout solution stands as one of the largest digital checkout providers in Europe. Kustom has 24,000 e-merchants and annual transaction volume of more than $14 billion (150 billion SEK). Kustom will focus on e-merchants and will add to its suite of payment methods, while keeping Klarna a key component of Kustom’s offering. Additionally, Kustom will focus on optimizing the checkout experience and building related services as opposed to offering its own payment methods or credit products.

“Our full focus will now be on our merchants and continuing to develop this great product based on their needs,” Hajabdolahi said. “We have an incredibly strong customer base, we are profitable, and we have secured financing for strategic acquisitions, which provides an excellent foundation. In the coming months, we will put all our efforts into further developing our infrastructure to expand our offering in 2025, including the introduction of new payment methods.”

Here are a trio of top takeaways from the rebrand.

Kustom will start strong

The rebrand comes at a time of strength for the digital checkout platform. The solution has a market share of more than 40% in Sweden and more than 20% across the Nordics. Kustom will also benefit from its new owners who have been credited for their “Buy and Build” strategy when it comes to acquisitions.

Strategic partnership with Stripe

In addition to its rebrand announcement, Kustom also shared news of a new strategic partnership with payments innovator Stripe. Stripe’s platform will be instrumental to Kustom’s plans to introduce new features and payment methods for e-merchants, starting in the first half of 2025.

Continued collaboration with Klarna

Despite the summer sale and the autumn rebrand, Kustom will retain its relationship with Klarna and, in fact, plans to offer Klarna’s payment methods in the future. Also many of the personnel moves accompanying the rebrand reflect more continuation than separation. Jesper Eriksson, previously Country Manager for Klarna in Sweden, will become Chief Commercial Officer for Kustom. Rasmus Fahlander, previously Senior Product Director for Klarna Checkout, will become CPO. Alexander Olsson, former finance director for the U.S. at Klarna, will take the role of CFO.

Whether you attended FinovateFall last month and missed a few demos, watched all of the demos but want to watch them again, or missed out on FinovateFall entirely, we have great news for you. The videos from the 66 FinovateFall demos are now live (and free to watch!) on Finovate’s website.

To get you started on watching over seven and a half hours of pure fintech demos, we’ve highlighted the eight Best of Show winning demos below to get you started.

Want to re-live the entire show? Check out the highlights reel below.

If you don’t want to miss out on the live action next time around, be sure to register for FinovateEurope, taking place February 25 and 26 in London. We’ll see you there!

It is no secret that banks are under pressure from a variety of sources: fintech upstarts, the rise of embedded finance, an increasingly dynamic regulatory environment, the pace of technological innovation–to say nothing of competition with one another.

For community banks, the pressure can be all the more intense. While many community banks enjoy a special relationship with local customers and businesses, this relationship does not prevent their patrons from wondering from time to time if the grass might be greener with a banking or fintech solution offered by another provider.

BNY recently surveyed community bankers to find out what they see as their top challenges–and opportunities–in the current environment. Conducted in partnership with the Harris Poll, BNY’s 2024 Voice of Community Banks Survey provides some interesting insights into where community banking is today, and what it needs in order to be successful in the years to come.

Wealth management and treasury services in demand

The growing interest in wealth management and treasury services was one of the more exciting insights from the BNY survey of community bankers. With the aging of the Baby Boomers and Millennials entering prime family formation years, it is little surprise to see a growing demand for everything from investment to estate planning. Relative to their larger rivals, community banks have not been as active in wealth management. But some have argued that community banks could change this by better leveraging their more personal relationships with their customer base to entice them away from faceless, corporate asset managers and large institutions. In fact, 100% of the community banks surveyed indicated that they want to add wealth management services to their offering.

At the same time, the interest in treasury services is perhaps even more eye-catching. The advent of real-time payments has made treasury services an increasingly attractive offering for financial institutions. In the same way that more personal relationships with individual customers can make wealth management services worthwhile for community banks to offer, so can the personal relationships these institutions have their local businesses encourage them to consider seeking treasury services where they are already doing much, if not all, of their banking business. According to BNY’s survey, fully 95% of community banks surveyed are inclined to agree that they would like to see treasury services added to their portfolio.

AI, tech, and digital transformation

While nearly half the community banks surveyed indicated that they saw themselves as “innovative within their communities,” that has not stopped most of them from wanting to enhance their products and services–as well as offer new ones– via digital transformation and enabling technologies. Interestingly, the survey did not just ask about technology per se, but instead queried them to find out specifically what they hoped these enabling technologies would do. To this point, nearly 30% pointed to efficiency and security as two major needs and indicated offerings like instant payments and automated loan processing both responded to these needs and helped community banks maintain “a competitive edge.”

Yet, while more than 90% of community banks said they were ready to embark upon digital transformations, significant uncertainty about the actual readiness remains. Approximately half of the respondents considered their data analytics capabilities–key for maximizing technologies like AI–to be “advanced,” and less than 20% believed that they had any real expertise when it comes to data analytics.

Non-fintech partnerships

Partnerships with technology companies and fintechs is one way for community banks to improve their ability to take advantage of enabling technologies like AI. However, one interesting reveal from the BNY survey was the interest that many community bankers have in non-fintech partnerships.

Almost 30% of respondents indicated that they saw non-fintech partnerships–collaborations with institutions in retail and education–as opportunities that would be as important as fintech partnerships over the next five years. This, arguably, should serve as a wake-up call for those fintechs that are innovating in adjacent areas–from e-commerce and consumer lending to financial education and even college prep.

You’ve likely been following the fallout from Synapse’s bankruptcy earlier this year. BaaS provider Synapse filed for Chapter 11 bankruptcy in April, leaving its clients, including Evolve Bank & Trust and multiple others, unable to verify and manage funds. In all, around $85 million in consumer funds are missing due to discrepancies in Synapse’s records.

Adding to the confusion, the dispute is ongoing in court, and because Synapse is a fintech and is thus unregulated, regulatory bodies are unable to protect consumers, many of whom are still missing their funds.

As a result of this nightmare, the FDIC has advanced a notice of proposed rulemaking for what it is calling Requirements for Custodial Deposit Accounts with Transactional Features and Prompt Payment of Deposit Insurance to Depositors. The regulatory body is currently taking public comment on the rule.

As it currently stands, the rule applies to bank accounts that fit into three categories:

The account is established for the benefit of beneficial owners

The account holds commingled deposits of multiple beneficial owners

A beneficial owner may authorize or direct a transfer through the account holder from the account to a party other than the account holder or beneficial owner

Here are five things banks with accounts that fit these categories should know about potential implications the rule may have on them.

Strengthened recordkeeping requirements

Advanced recordkeeping should already be part of a bank’s routine. However, the proposed rule is specific in its requirements, stipulating that banks working with non-bank entities (as in a BaaS partnership) must maintain accurate records that identify the beneficial owners of custodial deposit accounts that are held on behalf of consumers, which is typical in a BaaS agreement. Maintaining records of custodial accounts will help regulators ensure that deposit insurance can be quickly and accurately provided in the event of a bank failure.

Continuous third-party records access

The proposed rule states that if banks rely on non-bank companies to manage custodial deposits and their records, the bank must have continuous, direct access to records held at the third party organization. This requirement aims to prevent disruptions to operations, as what we saw in the Synapse bankruptcy case earlier this year. Ultimately, if banks have transparent access to third party records, they can help customers maintain access to their funds.

Annual compliance and validation

Under the new rule, FDIC-insured, BaaS-enabled banks will be required to conduct an annual, independent validation to verify that their third party partners are maintaining accurate deposit records. Banks will send the records, which must be accurate and compliant with the FDIC’s standards, to the FDIC and to the bank’s primary federal regulator. The purpose of this stipulation is to ensure consumers are able to access their funds without delays and to increase the reliability of custodial funds arrangements.

Consumer protection and transparency

Consumer protection is the underlying reason behind the new proposed rule. A large piece of this provides clarity about FDIC insurance. As such, BaaS-enabled banks will be expected to ensure that their consumers fully understand the coverage and protections of their deposited funds, particularly when dealing with non-bank custodians.

Heightened money laundering

The document also emphasizes that banks must exercise strengthened internal controls and anti-money laundering (AML) compliance requirements. Notably, the ruling also emphasizes that banks must ensure that their third-party partners do not facilitate financial crimes.

This week’s proposed rulemaking highlights two truths in financial services. First, the additional requirements can potentially add burdens on banks that are already weighed down by multiple reporting responsibilities. Yesterday, Vice Chairman Travis Hill voiced his concern, saying, “I recognize that certain types of pass-through arrangements have become much more complex in recent years, exacerbating the potential risks…” Hill said, however, that he is voting in favor of the proposal, explaining that, “improving recordkeeping and reconciliation practices (1) can reduce the likelihood of another Synapse-like disaster in the event of a third-party failure, and (2) may result in a more orderly resolution in the event the bank fails.”

The second truth today’s proposed rulemaking underscores is that the financial services industry needs a national fintech charter that can monitor, regulate, and enforce third parties that manage and handle consumer funds. Banks have long been subject to strict regulations and reporting requirements. But should banks that have conducted the proper due diligence be held responsible for the actions (or inaction) of their third party partners? It is time for fintechs to step up and share the responsibility.

2024 marks the 90th anniversary of the Federal Credit Union Act. Signed into law by President Franklin Delano Roosevelt in the summer of 1934, the Federal Credit Union Act authorized the formation of federally chartered credit unions in every state.

How are credit unions faring 90 years later? Today, total assets in federally insured credit unions sit at more than $2.3 trillion as of the first quarter of this year. That figure represents a year-over-year increase of 4.4%. Membership in federally insured credit unions has also picked up year-over-year, with membership topping the 140 million mark in Q1 of 2024.

But credit unions face significant challenges. Digital transformation is neither cheap nor easy. Competition with larger financial institutions–as well as Big Tech and Big Retail–has forced credit unions to seek new ways to better serve and engage their members.

FinovateFall 2024’sCredit Union Spotlight, presented by Curql, is designed to help credit unions overcome these challenges, offer new innovative solutions, and grow their membership ranks. The session, Wednesday afternoon, on September 11, will enable credit union executives to connect and speak intimately with a small, curated group of fintechs who are specifically focused on serving credit unions. The session will feature a series of rotating roundtables to give participants an ideal opportunity to interact, ask questions, and share best practices.

“It’s an exciting time to be a credit union looking at fintech,” said Greg Palmer, host of Finovate. “More and more innovators are creating solutions with credit unions in mind, and we’re delighted to be able to showcase some of those solutions to a room full of people who can start using them right away.”

Curious? Here are three reasons why you should attend our Credit Union Spotlight if you care about the future of credit unions in America.

Transformation

Digital transformation is reshaping businesses across industries. Credit unions are no exception. Moreover, many of the forces that are driving digital transformation in other industries are especially relevant to credit unions. Digital technology enables credit unions to offer more personalized services and better engage members. It also enhances processes to ensure that members’ data is secure, making the organization more efficient and capable of serving their current members more comprehensively.

And while every credit union is unique, there are commonalities when it comes to the digital transformation journey. Here, the lessons of those institutions that have already undergone this process can be invaluable for those institutions that have just begun–let alone those credit unions encountering challenges on their path to greater digitalization.

Competition

The opportunity to grow, accelerated by digital transformation, also means that credit unions are facing and will continue to face greater competition than ever before. Personalization makes it easy for larger financial institutions to customize their offerings and compete with credit unions when it comes to deeply engaging with individual needs and preferences. Larger financial institutions also often have resources to take advantage of technologies faster and more thoroughly than most credit unions. This can make it easier for these bigger rivals to offer innovations to their customers before credit unions can provide similar solutions for their members.

This is to say nothing of the non-financial entities in Big Tech and Big Retail, for example, who, through innovations such as embedded finance, have begun to offer a variety of financial and banking services to their customers.

Learning more about ever-evolving member preferences is an important initial step. But following up with new initiatives, new services, and new solutions can be a key hurdle early in the process. To this end, credit union professionals owe it to themselves to learn and share strategies that have helped credit unions of all sizes better understand their members, deploy new products that are eagerly adopted, and boost engagement.

Collaboration

One of the ways that credit unions are dealing with the challenge of competition–with Big Banks, Big Tech, Big Retail–is by embracing opportunities to collaborate with innovative fintechs, many of whom specialize in serving the credit union industry. This is important. For credit unions looking for partners to help them improve back-office operations, offer a new rewards program, or fortify their defenses against fraud, teaming up with fintechs that have demonstrated interest and experience in partnerships with credit unions can make the difference between achieving digital transformation goals that may have seemed unreachable–and falling short.

To facilitate these kinds of partnerships, credit union professionals need a forum that focuses exclusively on credit unions and the fintechs that serve them. Our Credit Union Spotlight, taking place next month at FinovateFall in New York, is that forum. To learn more about joining us and participating in the session, email our registration coordinator at [email protected].

The battle against fraud is a never-ending one. And recent fintech news headlines have helped remind us all of how broad the frontlines are. From the challenge of AI-powered deepfakes to the sad fact that many of our own bad habits continue to keep fraudsters in business, fintechs are busy developing solutions to help us get and stay at least one step ahead of the bad guys. Here are a trio of stories highlighting the latest efforts by fintechs to combat financial crime.

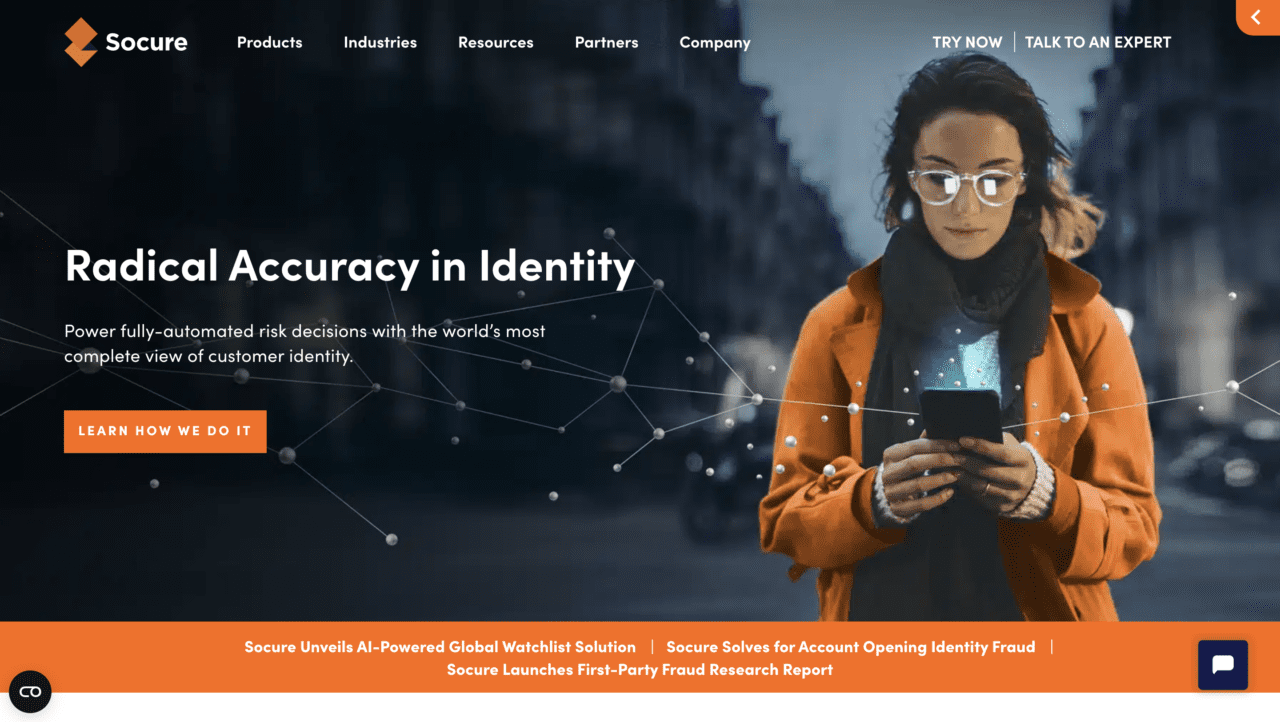

Digital identity verification innovator Socure has unveiled its Selfie Reverification solution. The new capability provides a way to validate return consumers online in less than two seconds with just a selfie. The technology matches incoming selfies with previously verified ID headshots, and features a true match rate of 99.9%. Built on the company’s Document Verification (DocV) solution, Selfie Reverification also detects signs of deepfaking, and readily identifies age discrepancies between the photo and the credential.

“Identity verification isn’t a one-time event. As consumers interact with an online service over time, their risk profile can change. That’s why it’s important to determine you are still who you say you are, without going through the full verification process again,” explained Socure Chief Product and Analytics Officer Pablo Abreu.

Selfie Reverification prompts the user to take a selfie, and sends real-time feedback on positioning, angle, and lighting. Once taken, the selfie undergoes a Level 2 NIST PAD compliant liveness check to prevent spoofing, as well as Socure’s injection attack detection process which makes sure that a fraudster has not injected a false or altered credential into the session. Lastly, the selfie is compared against a set of hundreds of thousands of curated deepfake samples created by more than 20 different AI generators.

The technology leverages biometric analytics to evaluate more than 80 facial features, from eye distance and nose width to jawline contours and emotional expression, to create a facial map and ensure an accurate match. Use cases for Selfie Reverification include preventing account takeover, securing high-risk transactions, streamlining account recovery and re-verification/re-validation, and more.

Founded in 2012 and headquartered in Incline Village, Nevada, Socure most recently demoed its technology on the Finovate stage at FinovateFall 2017. Today, the company has more than 2,500 customers, including four of the top five banks, the top credit bureau, and 400+ fintechs. Businesses ranging from Capital One and SoFi to DraftKings and the State of California rely on Socure’s technology for accurate identity verification and fraud prevention. Johnny Ayers is Socure’s founder and CEO.

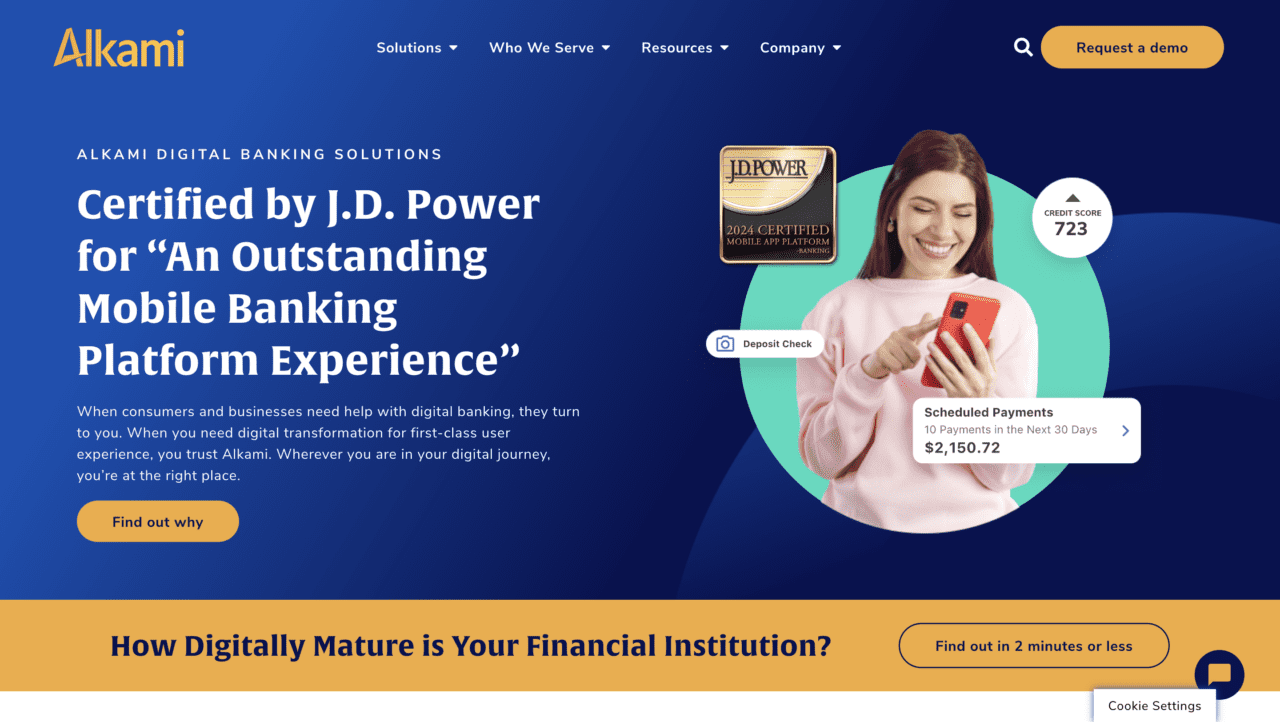

Digital banking solution provider Alkami has added credential stuffing protection to the challenge-response authentication process for its digital banking platform. The new functionality automatically checks for human behavior in the background, but does not require visual puzzles or any additional time spent by the user.

“This enhancement in Alkami’s platform has given us the ability to provide an additional layer of security for our account holders,” Quontic Bank SVP of Digital Banking Grace Pace said. “The secure and seamless login experience has contributed to reducing potential fraudulent activities, offering our customers greater peace of mind without added complexity.”

Credential stuffing refers to a type of cyberattack in which a hacker uses credentials obtained through data breaches or purchased from the dark web in order to attempt to access another service. A typical case of credential stuffing, for example, could involve a hacker using the credentials from a breach at a retail store to attempt to log into a bank’s website.

Credential stuffing is a common attack in part because it takes advantage of the tendency of individuals to reuse usernames and passwords. But its commonality takes nothing away from the damage these attacks do. One estimate determined that credential stuffing costs businesses $6 million a year on average, to say nothing of the negative reputational impact that often accompanies it.

The addition of credential stuffing protection is the latest example of Alkami’s layered approach to fraud detection and prevention in digital banking. “Alkami continues to evolve its platform as the security threats change for our customers, and we’re proud to integrate credential stuffing as part of our standard solution for everyone,” Alkami Director of Product Management Brad Cranford said. “Our goal is to help our customers manage security while providing the best experiences for their account holders.”

Headquartered in Plano, Texas, Alkami made its Finovate debut in 2009 as “IThryv.” Alex Shootman is CEO.

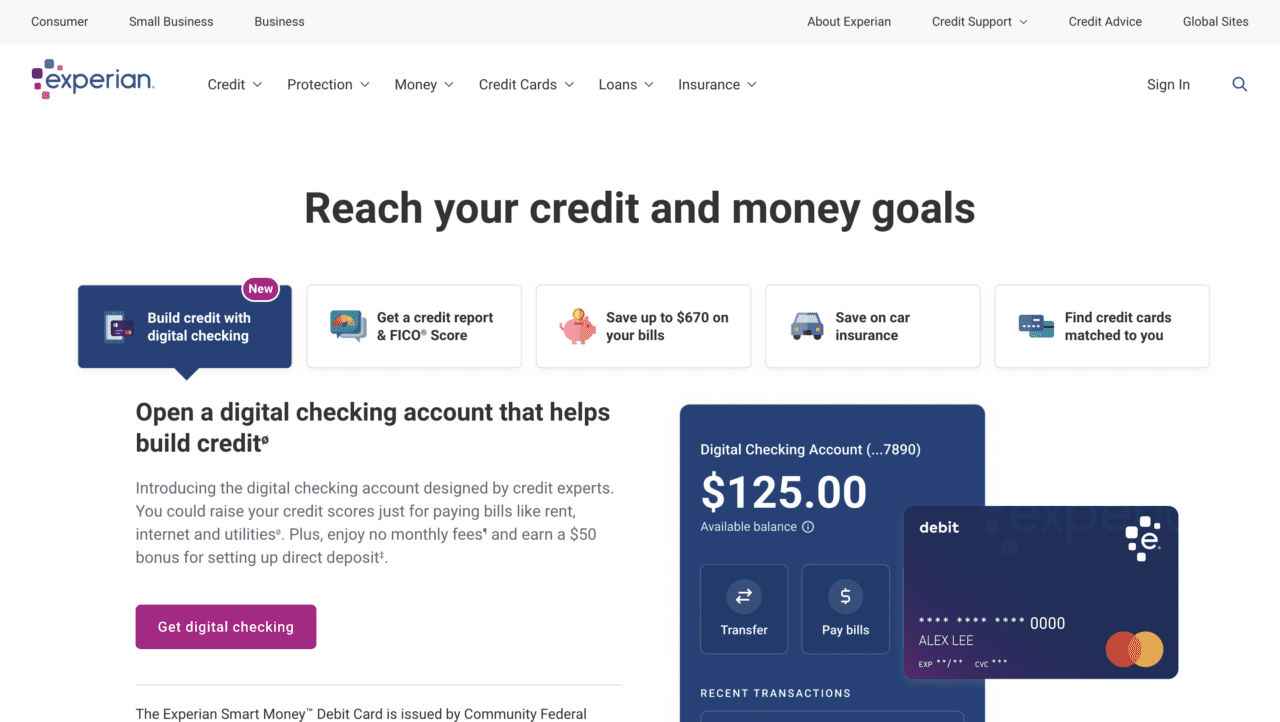

Data and technology company Experian is adding behavioral analytics to its fraud detection capabilities courtesy of a newly announced acquisition of NeuroID.

More specifically, Experian is looking to bolster its defenses against AI-generated fraud threats. With their ability to apply fraud detection strategies to key vulnerabilities such as origination and account management, insights from behavioral analytics can help mitigate fraud in real time and defend users against a range of malevolent actions including identity theft, account takeover, bot attacks, and fraud rings.

“Our acquisition of NeuroID highlights our commitment to provide our clients with world-class data, analytics, and insights to prevent fraud,” said President of Experian’s North American Identity & Fraud business, Robert Boxberger. “Together with NeuroID, we’re excited to build new blended offerings that detect risk but also empower businesses to confidently navigate the online landscape and trust in their transactions.” He added, “In today’s highly competitive and digital-first world, the use of behavioral analytics is now vital for innovating for the future of fighting fraud.”

NeuroID’s solutions are now available via CrossCore on the Experian Ascend Technology platform. The integration will enable platform users to use a single service provider to monitor and analyze real-time digital activity.

“NeuroID unlocks a new view into a user’s riskiness based on behavioral interactions,” NeuroID CEO Jack Alton said. “This view arms companies with a proactive, first line of defense to detect sophisticated fraud rings and bot attacks. By joining forces with Experian, we’re looking forward to helping companies confidently navigate this new era with solutions that enable more secure and frictionless experiences.”

A Finovate alum since 2011, Experian most recently demoed its technology at FinovateFall in New York in 2018. Headquartered in Dublin, Ireland, the company employs more than 22,000 people, including more than 9,000 technologists and product developers, working in 32 countries.

Are you an innovative fintech with new technology that’s ready for prime time? Join us in New York next month for FinovateFall and take advantage of the opportunity to showcase your solution before an audience of 2,000+ decision-makers.

The summer heat usually comes with a slowing of news activity, and while this is generally still holding true this summer, there have been some notable merger and acquisition activity throughout the past few months.

This season, the fintech landscape has had its fair share of strategic moves, as companies look to expand their capabilities, enter new markets, and expand on their offerings. These acquisitions are not just reshaping individual companies but they are also working to build out what the future of financial technology will look like.

As venture capital funding has dwindled over the past few years, the fintech sector has had to get creative in staying afloat. That may be one reason why we are seeing a growth in deal numbers. Let’s dive into the top 10 fintech acquisitions so far this summer.

Pluto acquired by Robinhood

Robinhood, a commission-free trading platform that aims to democratize finance acquiredPluto, a fintech startup focused on personalized financial planning and investment tools.

Deal Details: Financial terms were not disclosed. The deal is expected to close in Q3 2024.

Impact on Industry: The deal may encourage other trading platforms to improve their advisory services, increasing competition.

Future Outlook: Integrating Pluto’s technology will help Robinhood offer personalized financial advice, boosting user engagement and retention.

Theorem acquired by Pagaya

Pagaya, an AI-driven asset management firm that focuses on portfolio optimization through machine learning and big data acquiredTheorem, a provider of financial analytics and modeling tools.

Deal Details: The specific financial terms of the deal remain confidential.

Strategic Rationale: Theorem will strengthen Pagaya’s AI and data analytics capabilities, resulting in robust investment strategies.

Impact on Industry: Pagaya’s purchase highlights the importance of AI in asset management, pushing competitors to innovate.

Future Outlook: Pagaya’s platform will demonstrate enhanced analytical power, offering more value to institutional clients.

Aion Bank acquired by UniCredit

UniCredit, a leading European commercial bank that offers a wide range of banking services, acquiredAion Bank, which is known for its digital banking services and innovative financial products.

Deal Details: Financial details of the deal were not disclosed.

Strategic Rationale: Aion Bank will help UniCredit expand its digital banking capabilities and customer base.

Impact on Industry: The deal will help to increase competition in digital banking, driving more customer-centric services.

Future Outlook: Integrating Aion Bank’s technology will enhance UniCredit’s digital offerings and expand its market reach.

Envestnet acquired by Bain Capital

Bain Capital, a private investment firm that focuses on private equity, venture capital, and credit, acquiredEnvestnet, a provider of integrated portfolio, practice management, and reporting solutions.

Deal Details: The deal is valued at approximately $4 billion.

Strategic Rationale: Envestnet’s long-standing expertise will help Bain Capital enhance its capabilities in financial technology and wealth management solutions.

Impact on Industry: The move will bring Envestnet into the private sector.

Future Outlook: Bain Capital’s acquisition may fuel demand for other private equity firms to buy out wealth management fintechs.

Salt Labs acquired by Chime

Chime, a digital bank known for providing fee-free banking services, acquiredSalt Labs, an employee savings and rewards program.

Deal Details: Financial terms were not disclosed, but some sources report that the deal could close for as much as $173 million after Chime provides an up-front payment of $14 million.

Strategic Rationale: Salt Labs will enhance Chime’s offerings by integrating employee savings and rewards programs.

Impact on Industry: Integrating Salt Labs will help Chime promote financial wellness and engagement among employees, setting a new standard for digital banking services.

Future Outlook: The combination of Salt Labs with Chime Enterprise will expand Chime’s client base through employer channels.

Rooam acquired by American Express

Financial services giant American Express has acquiredRooam, a mobile payment and digital tipping platform for the hospitality industry.

Deal Details: Financial specifics were not disclosed.

Strategic Rationale: American Express is expected to expand its mobile payment capabilities in the hospitality sector.

Impact on Industry: The purchase will fuel demand for more innovation in mobile payment solutions that increase convenience for users and businesses.

Future Outlook: Integrating Rooam’s technology will improve American Express’s digital payment offerings and customer experience.

Strategic Rationale: Funding Circle will expand iBusiness Funding’s lending capabilities and customer reach.

Impact on Industry: The move will help strengthen small business lending options, ultimately supporting economic growth and entrepreneurship.

Future Outlook: Integrating Funding Circle’s platform into iBusiness Funding will enhance iBusiness Funding’s lending solutions and expand its market reach.

Invoiced acquired by Flywire

Flywire, a global payments enablement and software company, acquiredInvoiced, an accounts receivable automation platform.

Deal Details: Financial specifics were not disclosed.

Strategic Rationale: Invoiced is expected to enhance Flywire’s payment solutions by adding advanced accounts receivable automation.

Impact on Industry: The deal promotes efficiency in payment processing and receivables management solutions.

Future Outlook: Flywire will benefit from integrating Invoiced’s technology, which will offer comprehensive payment and receivables solutions and improving cash flow management.

Screena acquired by ThetaRay

ThetaRay, a provider of AI-powered transaction monitoring technology, has acquiredScreena, a cybersecurity firm specializing in fraud detection and prevention.

Deal Details: Financial terms were not disclosed.

Strategic Rationale: The deal will strengthen ThetaRay’s fraud detection capabilities with Screena’s advanced cybersecurity technology.

Impact on Industry: The move enhances current fraud prevention measures, which will increase security in financial transactions.

Future Outlook: Integrating Screena’s technology will improve ThetaRay’s AI-driven fraud detection and prevention solutions.

LemonSqueezy acquired by Stripe

Financial infrastructure platform StripeacquiredLemonSqueezy, a platform for managing digital product sales and subscriptions.

Deal Details: Financial terms were not disclosed.

Strategic Rationale: LemonSqueezy will expand Stripe’s capabilities in digital product sales and subscription management.

Impact on Industry: The deal will promote innovation in digital commerce, providing businesses with more comprehensive tools.

Future Outlook: Stripe will enhance its existing offerings with LemonSqueezy’s capabilities, further supporting digital entrepreneurs.

There was a time when robo-advisory represented the peak of fintech’s contribution to the wealth management industry. And these services continue to be popular options for a new generation of savers and investors. The Statista Market Forecast indicates that the robo-advisor market worldwide is expected to grow by more than 6% by 2028, with more than 34 million investors relying on robo-advisors.

At the same time, enabling technologies like machine learning and AI are generating new ways for fintechs to bring the benefits of technological innovation to the wealth management industry. But it is important for fintechs to avoid building solutions in search of problems. What are some of the real trends and true pain points in the industry that fintechs may be able to help solve?

Democratization

One major theme in wealth management is democratization. For generations, wealth management has been the province of, to put it bluntly, the wealthy. Services were often expensive and opaque for the growing number of upper-middle class and middle-class investors of the 1980s and 1990s.

There is still a healthy market for high net worth investors, of course. But we have seen a major trend toward leveraging technology to make some wealth management services that were previously available only to the elites accessible to investors of lesser means.

There is also another way of looking at democratization in wealth management. In the same way that technology is enabling average investors to access increasingly sophisticated wealth management services, so is technology making it possible for smaller providers to compete with larger wealth management rivals. Fintechs that can help smaller firms and family offices do more with less may find significant opportunities among the growing group of wealth management entrepreneurs.

Personalization

Personalization has increasingly been seen as table stakes in financial services, and with good reason. Whether you are involved in payments or lending or ecommerce, the ability to get relevant products and services in front of your customers is paramount. Not just knowing what customers might want but also being able to deliver is what separates those businesses that gain new customers and keep the ones they’ve got, from those who struggle to do so.

Fintechs can enhance the customer experience by, for example, ensuring that wealth managers can communicate with clients in their channels of choice – and are able to bring significant functionality to those interactions in those channels with video or co-browsing. Knowing which customers are more likely to respond positively to new or alternative investment strategies, for example, or to other complementary products or services can go a long way toward building better engagement and loyalty.

Operations

One of the less flashy areas where fintech technologies can help drive innovation in wealth management is in back-office operations. This is also where enabling technologies like artificial intelligence (AI) and machine learning are delivering Automation 2.0 to intelligently streamline manual tasks and complex procedures. This trend, which has brought speed, accuracy, and cost-cutting to industries throughout financial services, is one that will benefit wealth management service providers significantly.

Moreover, many of the other trends in wealth management – such as the challenges of managing (and securing) ever-growing volumes of data, keeping up with evolving regulatory changes – are made possible by operations teams that have these powerful, enabling technologies at their disposal. For wealth management service providers who are not yet maximizing their teams or these technologies, fintechs can help them close the gap.

Decisioning

From buy-and-sell decisions to strategic portfolio allocations, wealth management is about making good, consistent decisions. Not only do wealth management service providers constantly seek to improve their investing strategies – one area where fintechs can provide specific expertise – but also these firms need to think about more than just maximizing returns. Keeping portfolio volatility at an acceptable level based on the risk tolerance and profile of the individual investor is just one example of another important function of the successful wealth manager.

Making good decisions is also about accountability. Having systems in place that ensure that processes are explainable and auditable is critical to accountability. It is also vital to an institution’s ability to learn, adapt, grow, and improve.

Compliance

Keeping up with the latest regulations is important for all financial service providers – and wealth management companies are no different.

As mentioned previously, one of the biggest benefits of enabling technologies like machine learning, AI, and Automation 2.0 is the ability for firms to track regulatory changes and ensure that their operations are able to meet new standards. An article earlier this year in Financial Planninglisted 10 separate regulatory issues that wealth management firms are likely to face this year, from regulations on marketing language to rules governing digital assets. Moreover, many wealth management firms have internal rules and mandates based on the type of investments they offer and to whom. As such, remaining compliant with an institution’s own governing policies is also a challenge for which regtechs in our industry can provide assistance.

Growth

One of the most exciting ways that fintechs can bring innovation to wealth management services providers is to enable them to grow and expand their businesses by offering services that, while complementary, could be difficult to offer (much less integrate) without technology partners.

Whether through APIs or embedded finance, there are a range of complementary services that fintechs can provide to wealth managers. From insurance to estate planning to secure document digitization and storage, fintechs are able to provide services that wealth management customers often need, but are inclined to get elsewhere. By adding these solutions and services to their product mix, wealth managers can dramatically increase their capacity to grow.

We’re more than halfway through 2024 so there’s no better time for a trends temperature check to determine what we should be paying attention to throughout the second half of the year. Learning about the newest trends is crucial to understanding how your firm can better compete and ultimately succeed in the crowded fintech and banking arena.

Funding

Late last year, we were still in the metaphorical trenches of funding. As of mid-2024, fintech funding trends are mixed. For the most part, venture capital investment is still quite slow because of high interest rates and economic uncertainty. We may see a more positive shift after the U.S. election, as many investors have cited political uncertainty as a factor in delaying major strategic and investment initiatives.

There is, however, another aspect of the current funding scene. Startups in targeted subsectors that are leveraging generative AI in unique ways are still garnering attention and funding from investors, though not quite at the high levels we saw in 2021 and early 2022. These shifts have caused companies to focus on sustainable growth and profitability, rather than the aggressive growth-at-all-costs mentality that was common from 2010 to 2019.

Regulation

As expected, the regulatory landscape has tightened significantly so far this year. Regulators have intensified their scrutiny not only of financial institutions, but also of specific issues. In the U.K., the Basel III framework brought forth new regulations focusing on capital adequacy, liquidity, and operational risk. In the U.S., there has been increased scrutiny of banking-as-a-service partnerships. This has brought a pulse of new consent orders on a regular basis. On top of all of this, we’ve seen the CFPB take measures to further consumer protection, such as last week’s proposed interpretive ruling stating that some earned wage access tools should be considered loans.

Embedded finance and open banking

Predictably, the conversation around embedded finance and open banking has escalated in 2024 as consumers continue to seek digital experiences that offer seamless financial integration. Banks’ open banking initiatives have expanded, which is crucial given that the CFPB is expected to release the final ruling of Section 1033 of the Dodd-Frank Wall Street Reform, which will stipulate rules surrounding rules governing personal financial data rights.

Generative AI

It will not come as a surprise that both the use and mentions of generative AI technology in fintech and banking has increased. The use of the technology experienced major expansion after the general release of ChatGPT in late 2022. Now that both banks and fintechs have been able to see and experience first-hand the potential of generative AI, there has been a large spike in demand for integrating the technology into existing operations to help improve efficiency, personalize customer interactions, and enhance risk management.

CrowdStrike’s update to its flagship cybersecurity product, Falcon Sensor, late last week caused an impressive amount of panic across a wide swath of industries. Many computers running Microsoft were stuck on the “blue screen of death” (BSoD), which would not allow users’ computers to load.

Immediately, the update caused flight cancellations, train delays, broadcasting problems, hospital issues, and disruptions at businesses across all sectors that could not log into their computers for the day. But aside from these fleeting, yet major, problems the botched software update will have lasting implications.

Opportunity for competitors

Impacting the cybersecurity industry as a whole, many organizations will see last week’s update failure as an opportunity to market their own fraud fighting technology to organizations big and small that were impacted by last Friday’s events. We may even see a slight increase in new cybersecurity company launches. According to TechCrunch, as of last year, CrowdStrike enjoyed a 14.7% share of global revenue from security software sales. This may decrease as some clients seek alternative technologies. It is unlikely, however, that we will see a mass exodus from CrowdStrike.

Information for hackers

Perhaps one of the biggest concerns for CrowdStrike clients is that the update failure offered hackers all over the globe a visual of which companies use CrowdStrike as a vendor to fight fraud. Cybersecurity companies rarely disclose client names, especially in banking and finance, and for good reason. When hackers know which security software vendors a firm is using, they are able to gather a lot of information they can use to try to circumvent the software for nefarious purposes.

In addition to offering visibility into which banks are working with CrowdStrike as a security vendor, the fallout of the update also offers fraudsters an open door to send consumers phishing emails and phone calls to exploit the situation by asking consumers to divulge passwords and sensitive codes.

Loss of consumer trust

End consumers, especially in the banking and airline industries, will likely lose some amount of trust in the security of online businesses. Many saw firsthand how far reaching and potentially catastrophic software disruptions can be, and unfortunately, many consumers incorrectly assumed that the BSoD was the result of a cyberattack rather than an update glitch. As a result, consumers may be more wary of sharing their sensitive details online and may be less willing to trust the security of their financial institution, even if it was not impacted by Friday’s events.

Heightened regulatory concern

Regulators are consistently being challenged by today’s fast-moving technological environment. Now, they have a new worry to add to their list. Regulators have a responsibility to ensure that they are not only retroactively responding to IT outages, but also actively working to help prevent them from occurring in the first place. This will likely lead to more stringent regulatory guidelines for cybersecurity measures, mandatory incident response protocols, and regular stress testing of critical IT systems to ensure their resilience.

After months of deliberation, the finalists for the 2024 Finovate Awards have been selected!

In categories ranging from “Best Alternative Investments Solution” to “Top Emerging Fintech Company,” more than 130 innovative companies and individuals have made the short-list. We are now set for an exciting autumn showdown when winners are announced at Finovate Fall 2024 in New York in September.

“This year’s finalists are an amazing group!” Finovate VP Greg Palmer said. “From huge banks like JP Morgan, US Bank, and BNP Paribas, to cutting-edge fintechs like TodayPay, Kobalt Labs, and Wysh, there are amazing things happening all across the fintech ecosystem. The competition was intense for everyone who applied, and making it to the final round is an immense achievement. Congratulations to all of our finalists!”

Check out our finalists below. To learn more about the awards, visit our Finovate Awards hub.

Best Alternative Investments Solution

AlphaPoint Ctrl Alt Frec iCapital, Inc. Percent

Best Anti-Fraud/AML Solution

Credit Union of Colorado ING Turkiye JP Morgan AWM Mastercard Worldpay

Best Back-Office/Core Services Solution

FINBOA LoanPro Mastercard Cybersecurity Mitek Systems Taktile Zafin

Best Banking-as-a-Service Provider

B4B Payments Colendi Grasshopper Bank North Bay Credit Union Pathward, N.A.

Best Consumer-Facing Payments Solution

Engage People InPost Pay Pushpay Transact Campus Trustly

Best Consumer Lending Solution

JP Morgan AWM Jenius Bank Prosper

Best Corporate Payments Solution

BILL Global PayEx Helcim TransferMate TreasurUp US Bank

Best Customer Experience Solution

ACE Money Transfer DBS BAnk JP Morgan AWM Millennium BCP NF Innova – OTP banka Srbija Syfe

Best Digital Bank

Dave IndusInd Bank Papara Elektronik Para A.S. RCBC

APEXX Global Orum Papaya Global PayNearMe SWIVEL VGS

Best Financial Mobile App

BNP Paribas FINOM Industrial Bank of Korea JP Morgan AWM

Best Fintech Partnership

American Heritage CU and Datava Apiture and Newtek Bank Fnality International and Lloyds Banking Group Pagaya and US Bank Panacea Financial and Bankjoy Sunrise Banks and MoCaFi

Best Generative AI Solution

Bank of Montreal Intuit Credit Karma Nest Bank S.A. Socure Symphony AI Talkdesk

John Retting, BILL Sanjiv Yajnik, Capital One Chermaine Hu, Episode Six Jon Briggs, KeyBank Roben Dunkin, PGIM Nancy Langer, Transact Campus Matt Hawkins, Waystar Chris Hilliard, Winnow Solutions

Innovator of the Year

Matt Brown, CAIS Yelena Melamed, Catchlight Sindhu Joseph, CogniCor Josh Owen, Flourish Geralyn Hurd, K1x Ken Moore, Mastercard Kelly Uphoff, Tala Alex Matjanec, Wysh

Most Impactful AI-Based Solution

Brex Napier AI Pagaya Socure Uplinq Winnow Solutions

The U.S. House of Representatives wanted it. The Senate wanted it. Much, if not all, of the cryptocurrency industry wanted it. But on Friday, President Biden made good on his threat to veto a resolution that sought to loosen regulations regarding how financial institutions hold digital assets on their balance sheets.

“My administration will not support measures that jeopardize the well-being of consumers and investors,” President Biden said in a statement. “Appropriate guardrails that protect consumers and investors are necessary to harness the potential benefits and opportunities of crypto-asset innovation.”

The issue at hand was a repeal of the Securities and Exchange Commission’s Staff Accounting Bulletin 121. This bulletin was designed to compel financial institutions that are holding digital assets to keep those assets on their own balance sheets. Those backing the repeal – which included both Republicans and Democrats – claimed that the current policy was too restrictive and made it harder for financial institutions to work with cryptocurrency businesses.

The decision has enraged some and led observers to suggest that digital assets could become an issue in this year’s presidential election. Likely Republican Party nominee Donald Trump reportedly referred to the Democratic Party’s apparent distaste for crypto at a recent event – during which the former president promoted his own digital asset, a non-fungible token (NFT).

Whether Biden’s cautious approach to crypto will be a political liability in November remains to be seen. Crypto industry polls indicate that more than 20% of voters in swing states consider crypto a “major issue.” At the same time, a 2023 Pew Research Center Survey showed that most Americans continue to have major concerns about the safety and reliability of digital assets.

Blockchain and crypto solutions company Ripple has teamed up with cross-border payments solutions provider for regulated institutions, Clear Junction. The partnership will enable Clear Junction to facilitate instant and secure GBP and EUR-denominated payout coverage for Ripple’s payment clients – with additional currencies to be added later in the year.

Cassie Craddock, Ripple’s Managing Director for Europe, praised Clear Junction’s ability to support all of Ripple’s use cases. “Clear Junction already has strong relationships with a number of our existing clients, and its management team has many years of experience in cross-border payments and banking,” Craddock said.

Making its Finovate debut in 2013 as OpenCoin, Ripple has grown into a major cryptocurrency and blockchain technology firm with hundreds of customers in 55+ countries and payout capabilities in 80+ markets. Businesses rely on Ripple’s enterprise blockchain solutions to source crypto assets, facilitate instant payments, engage new audiences, grow revenues, and more.

The partnership news with Clear Junction comes in the wake of Ripple CEO Brad Garlinghouse’s suggestion that an exchange-traded fund (ETF) based on Ripple’s XRP coin is “inevitable.” Also, somewhat apropos of our opening story, Ripple recently donated $25 million to Fairshake, a super PAC dedicated to pro-crypto political advocacy in 2024.

The Bank for International Settlements (BIS) is investigating the use of wholesale central bank digital currencies (wCBDCs) to improve instant cross-border payments. The new initiative is called Project Rialto and is a collaboration between the BIS Innovation Hub Eurosystem and Singapore Centres, along with a number of central banks. The project takes its name from a famous bridge in Venice, Italy, that spans the banks of the Grand Canal.

“Decentralized solutions, CBDC and interlinked payment infrastructures are considered promising avenues to improve cross-border payments,” the BIS noted in a statement. “How they interact has not yet been explored and could yield answers that advance cross-border payments globally.”

Wholesale CBDCs differ from retail CBDCs in that the latter is designed for use by the general public. Wholesale CBDCs are used by banks and other licensed financial institutions for interbank payments and securities settlements. A third type of CBDC, hybrid CBDCs, combine features of both wholesale and retail CBDCs. All CBDCs offer greater efficiency compared to traditional trade and settlement methods, reducing operational expenses, enhancing transparency, and improving the overall reliability of transactions.

Deutsche Bank announced this week that it is partnering with Austrian cryptocurrency brokerage Bitpanda. Deutsche Bank will process customer deposits and withdrawals for the broker, and has agreed to give local bank account numbers to Bitpanda users in Germany.

The move is a significant one for the industry. Crypto businesses have found it challenging to find banking partners in the wake of high-profile collapses of crypto-friendly banks in 2023, like Silicon Valley Bank and Silvergate Capital Corporation.

That said, Deutsche Bank considers this a “very cautious” initial step. While the partnership does mean that fiat currency deposits and withdrawals from Bitpanda will flow through Deutsche Bank, the bank is not involved in the movement of any crypto assets. As Deutsche Bank Global Head of Cash Management Ole Matthiessen explained to Reuters, the bank will merely assist clients with their ingoing and outgoing transactions while supporting Bitpanda’s treasury and payments process.

Bitpanda was founded in 2014. The company has more than four million users on its platform, which offers trading and investing in cryptocurrencies, fractional shares of stock, and precious metals. This week’s announcement builds on Bitpanda’s existing relationship with Deutsche Bank for its cross-currency operations in Austria and Spain.

Be sure to check out this week’s Finovate Weekly newsletter on LinkedIn featuring a pair of crypto/blockchain-related articles!