This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Fraud is growing more sophisticated and has become supercharged by generative AI, deepfakes, and increasingly organized social-engineering networks. The changing dynamics have forced both banks and fintechs to rethink their defenses as criminals adapt faster, more frequently, and with more personalized attacks. Across fintech, it is clear that traditional fraud controls are no longer enough to protect customers.

But while the entire industry is facing the same escalating threats, fintechs have been especially creative in rolling out new layers of protection. Over the past year, a handful of standout features have emerged that combat fraud by proactively shaping customer behavior, interrupting social-engineering tactics, and closing gaps that legacy systems can’t reach. Here are three unique new innovations worth watching (and borrowing).

Revolut’s geolocation restrictions

Revolutreleased a safety feature yesterday that allows users to restrict money transfers to specific, user-approved geographic areas. If a transfer request is made from the customer’s device, but takes place at a location that the customer has not listed, the app blocks the transaction automatically, even if the fraudster has the user’s credentials. The feature uses both device GPS and Revolut’s internal risk engine to reduce account takeover losses.

Why banks should care: Geolocation locking adds a low-friction layer to fraud defense, especially for reducing authorized push payment fraud (APP) and account takeovers. By having the user determine their restricted, “safe” locations, banks could offer users more granular control over how and where their money can move.

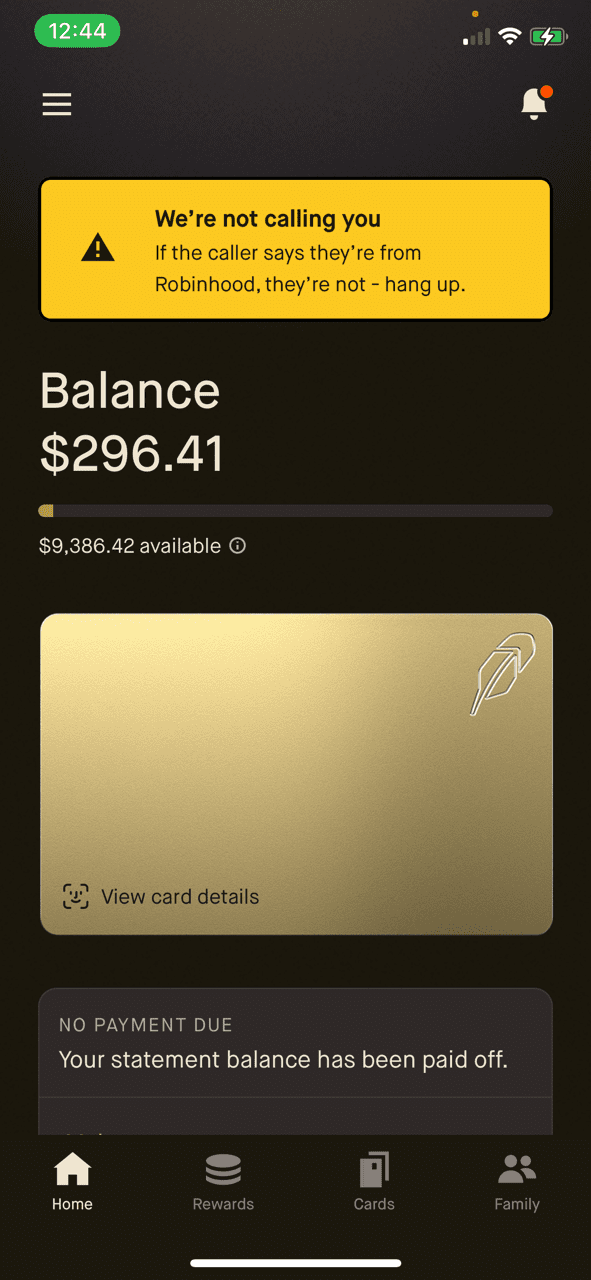

Monzo’s and Robinhood’s in-app scam warnings

Both Monzo and Robinhood help users determine whether an inbound call claiming to be from the bank is legitimate. When a customer is on a call and opens their mobile app, the app displays a banner that clearly communicates that the call they are on is not with the bank. In Robinhood’s case, the message states, “We are not currently trying to call you. If the caller says they’re from Robinhood, they are not. Hang up.”

Why banks should care: Impersonation scams are one of the most expensive forms of APP fraud. Adding an in-app, real-time verification banner is an extremely simple but effective way to interrupt fraudsters.

iProov is fighting deepfakes with biometric verification that detects AI-generated faces and synthetic video spoofing. The company analyzes pixel-level light reflections, which it calls “liveness assurance,” and uses deepfake-detection models to identify whether a live user is present. This is becoming essential for remote KYC, account recovery, and high-risk authentication.

Why banks should care: Banks increasingly rely on remote onboarding and passwordless authentication, but deepfakes are now able to defeat many of the legacy selfie-verification systems launched in the past decade. Deploying deepfake-resistant biometrics is becoming essential to prevent fraudulent account opening and social-engineering-driven account resets.

Each of these features has one thing in common: they put friction in exactly the right place. The friction isn’t applied to every transaction, and they won’t deter honest customers, but they will help stop fraud in common places. By using smarter triggers, real-time context, and design choices, fintechs are able to interrupt fraudsters. And while each solution won’t stop all fraud, they take care of some of the heavy lifting while minimizing the burden of friction on end consumers.

The International Organization of Securities Commissions (IOSCO) is out with a new report that highlights both the promise and the potential hazards of the tokenization of financial assets.

In a world in which stablecoins have increasingly defined innovation in the cryptocurrency/blockchain space, tokenization of financial assets is seen by some as the Next Big Thing in decentralized finance. Tokenization of financial assets refers to the process of representing ownership of a traditional financial asset, such as a share of stock or a bond, as a digital token on a distributed ledger or blockchain. Importantly, although tokenized assets can be transferred, traded, or exchanged between parties electronically, these assets are not cryptocurrencies—they are digital representations of regulated financial assets.

Valued for their ability to bring greater efficiency to the payments process—as well as their transparency, programmability, and potential to support financial inclusion via fractionalization—tokenized financial assets remain a new feature on the financial services scene. As such, there are myriad questions about how they can and should be used, as well as how they should be regulated. In their recent report, IOSCO, via its Fintech Task Force (FTF) and Financial Asset Tokenization Working Group (TWG) raised a number of these questions.

“The analysis shows that the majority of risks arising from the current commercial application of tokenization fall into existing risk taxonomies,” the report reads in its Executive Summary. “Market participants are not unfamiliar with managing such risk types. However, the manifestation of vulnerabilities and risks that are unique to the technology itself may require the introduction of new or additional controls to manage them.”

Here are three top takeaways from the IOSCO report on the tokenization of financial assets.

Legal Uncertainty and Ownership Rights

The biggest concern expressed in the report is the idea that there remains significant legal ambiguity about the tokenization of financial assets. This includes questions about the rights of ownership, transferability, and enforceability of claims.

“While there are currently well-established legal frameworks and structures for the treatment of financial assets created in paper certificate or book-entry form,” the report observes. “It can be unclear whether the existing legal treatment … applies to those created or represented in the form of tokens.”

In the absence of greater clarity on these legal framework issues, investors may find themselves unable to price or trade tokenized financial assets with confidence. This, at a minimum, can create asymmetry between investor expectations and outcomes and, at a maximum, contribute to more systemic uncertainty and challenges.

Infrastructure Risks and Operational Vulnerabilities

The second major risk discussed in the IOSCO report has to do with infrastructure risk, and the concerns range from the operational to the malicious. In either case, however, a major event that exposes these technical vulnerabilities could result in assets becoming permanently lost or cause an even wider market disruption.

Much of this concern is related to the relative newness of distributed ledger technology, as well as to some unique aspects of the technology compared to what is found in traditional financial markets. One example is the potential loss of a private key in a token structure, a phenomenon that does not exist in the world of traditional finance. The loss of a private key, which represents a sort of digital signature or ownership credential, would effectively result in the loss of access to the asset. To that end, a stolen private key would enable a criminal to steal the victim’s tokens.

“These assets face operational vulnerabilities and risks unique to this infrastructure, including cyber-attacks on blockchain nodes, congestion in transaction processing, data leakage, market fragmentation, smart contract bugs, and loss of private keys,” the report explains. “As tokenization scales up, regulators should also be cognizant of possible changes in market activities and market structure.”

Market Interconnectedness and Systemic Risk

A third concern is the creation of new dependencies and greater interconnectedness between market participants that is likely to happen as tokenization of financial assets scales. There are two versions of this. As an example of the first version, the report notes that a critical failure of a shared infrastructure, with multiple financial institutions tokenizing assets on the same blockchain network, could impact all tokenized assets on the network, rendering them temporarily or even permanently inaccessible.

Another example of the potential interconnectedness challenge arises as tokenized financial assets are increasingly used as collateral in cryptocurrency markets or as part of a stablecoin reserve. Here, the concern is that a crisis in the cryptocurrency markets such as a major or sustained stablecoin depeg could affect tokenized money market funds or government bonds being used as backing assets. The impact could readily spread to institutional investors with tokenized holdings, who would become involuntarily exposed to the heightened volatility of the crypto market.

Innovating for Known Unknowns

The quote from the report’s executive summary helps keep these and other concerns raised in the report in the proper context. While some challenges are more daunting, others more likely represent the kind of technological gauntlet that any product, service, or network must overcome as it scales. “Such risks and controls have been acknowledged by issuers and operators,” the report itself notes. That said, clear legal frameworks will be essential for addressing the broader challenges facing tokenized financial assets and unlocking their potential benefits.

Just days after we featured Canada in our weekly Finovate Global column, we can now add to our understanding of what is driving fintech innovation in Canada with a look at the country’s recently unveiled federal budget.

“Don’t tell me what you value. Show me your budget—and I’ll tell you what you value,” former US President Joe Biden liked to say. In this regard, Canada’s budget—with CAD $141 billion in new spending and CAD $51 billion in cuts and other savings—reflects a commitment to investing in the most transformative technologies of our time for the benefit of Canadian businesses and citizens, as well as for the wellbeing, defense, and even sovereignty of the country itself.

“The world is undergoing a series of fundamental shifts at a speed, scale, and scope not seen since the fall of the Berlin Wall,” the budget document begins. “The rules-based international order and the trading system that powered Canada’s prosperity for decades are being reshaped—threatening our sovereignty, our prosperity, and our values.”

“This is not a transition. It is a rupture—a generational shift taking place over a short period of time.”

Against this backdrop, here are four takeaways for fintech and financial services from Canada’s newly released budget.

Open Banking on Track for 2027 Implementation

The Canadian government will commit to introducing the last remaining pieces of legislation needed to complete the Consumer-Driven Banking Framework, advancing the country’s open banking system. The budget indicates that process will take place in two phases: data sharing (“read access”) followed by transaction initiation (“write access”), with full implementation set for the middle of 2027.

Oversight of open banking will remain with the Financial Consumer Agency of Canada (FCAC), which will ensure strong consumer protection and compliance. The country’s Department of Finance will continue coordinating the framework’s policy and legislative rollout. Meanwhile, the Bank of Canada, the country’s central bank, will oversee the broader payments ecosystem as new participants—from fintechs to non-bank Payment Service Providers (PSPs)—and new instruments such as stablecoins become a part of the country’s real-time payment infrastructure.

Stablecoin Regulation Framework Unveiled

Canada will introduce federal legislation to regulate fiat-backed stablecoins. Stablecoin issuers will be required to maintain asset reserves and meet consumer protection standards. These entities will also be mandated to establish and implement redemption policies and risk-management frameworks. The government also will amend its Retail Payment Activities Act, first passed in 2021, to enable payment service providers to use approved stablecoins for transactions.

Per the new budget, the Bank of Canada will receive CAD$10 million over two years (2026-2027) to administer the new framework and receive funding of approximately CAD$5 million a year afterwards. This sum will be offset by fees collected from regulated stablecoin issuers.

The move to embrace stablecoins is a major part of the country’s effort to modernize its payment systems and create new efficiencies. But, as with efforts in Europe and elsewhere, the initiative is also designed to avoid what some Canadian observers worry could be excessive and undue use of foreign-issued stablecoins, including those from the country’s larger neighbor to the south.

Real-Time Payment Rail Infrastructure on Track

The new budget also confirms that Canada’s Real-Time Rail (RTR) system will be operational in 2026. RTR will provide instant, cheaper payments for a broad range of transactions including payroll, expense reimbursements, and other business-related fund transfers. There will also be further updates to the Retail Payment Activities Act to enable new entities, such as non-bank PSPs, to apply for membership in Payments Canada and participate directly in national payment systems including RTR. Payments Canada is the public, non-profit entity that owns and operates Canada’s national payment clearing and settlement infrastructure.

Canada’s RTR project is very much intertwined with other fintech-based initiatives in the budget, such as open banking and stablecoins. For example, the budget notes that the combination of write access and RTR by mid-2027 will help usher in the “next phase of consumer-driven banking” characterized by safer, faster payments and greater choice for Canadian businesses and consumers.

A Billion-Plus Investment in AI and Quantum Computing

The budget allocates CAD $1.26 billion for AI and quantum computing technologies. The inclusion of quantum computing technology is especially interesting, affirming Canada’s determination that investment in quantum computing is key to ensuring the country remains on the cutting edge in terms of innovation-enabling technologies.

The allocation for AI represents the lion’s share of the sum at just over CAD $925 million. The funding will support the construction of a large-scale, publicly-accessible AI infrastructure. It also provides for investments in data center infrastructure and domestic compute capacity. The budget endorses a “Sovereign Canadian Cloud” to help ensure sufficient compute capacity as well as data sovereignty. Notably, there is also funding specifically focused on tracking AI technology adoption, a major concern for many decision-makers when it comes to investing in AI. Over six years, CAD $25 million will be allocated for a Statistics Canada program to implement the Artificial Intelligence and Technology Measurement Program, also known as TechStat.

With regard to quantum computing, the budget earmarks more than CAD $334 million over the next five years to bolster the country’s quantum ecosystem via the Defense Industrial Strategy introduced in the budget. The budget places quantum computing technology alongside AI in Canada’s broader innovation plan, describing it as “similarly transformative,” with promising use cases in finance and cybersecurity.

From the latest innovations in the fight against fraud to leveraging AI to make it easier for small businesses to secure the financing they need to grow, FinovateFall 2025’s Best of Show winners help us see exactly where fintech is making the most impact for companies and communities.

In his most recent podcast interview, Greg Palmer talks with LemonadeLXP CEO John Findlay.

Findlay explains how the company evolved into a comprehensive all-in-one learning and knowledge platform for financial institutions. Findlay and Palmer discuss the shortcomings of traditional learning management systems that focus on compliance training rather than skill development that leads to business growth and more effective customer service.

Finovate Podcast host Greg Palmer catches up with Shivangi Khanna (CEO) and Sophie Jewsbury (COO) of Krida.

The three talk about how Krida leverages AI and workflow automation to transform the commercial lending process. Khanna and Jewsbury discuss the universal pain point of document collection and processing and explain how Krida’s technology automates the feedback loops between borrowers and loan officers to shorten the time between lead generation and a completed loan application.

Palmer and Vos discuss how Eko makes it possible for early-stage investors to get started building their wealth through the credit union or bank they already know and trust. Vos explains how enabling financial institutions—especially smaller ones—to offer investment services can help them compete with third-party investing apps, many of which are embarking upon offering banking services of their own.

Mitch Rutledge, CEO of Vertice AI, joins Greg Palmer on the Finovate Podcast.

In this conversation, Palmer and Rutledge talk about how Vertice AI enables smaller financial institutions to “punch above their weight” with AI-powered solutions that help them transform institutional data into actionable insights. Vertice AI helps community FIs deliver personalized customer engagement and measurable growth outcomes.

Greg Palmer chats with Tim Li, Co-founder and CEO of LendAPI.

Li explains how LendAPI serves as a “super orchestration platform” that enables users to build their own financial products via an intuitive browser interface. The platform includes a product studio in which FIs can build personal loans, mortgages, and other products with integrated rule studios, models studios, pricing engines, and third-party plugins.

Finovate Podcast host Greg Palmer interviews Casap Co-founder and CEO Shanthi Shanmugam.

Palmer and Shanmugam talk about the challenges of first-party fraud and how this form of fraud—in which customers falsely claim they did not make purchases they actually did make—has become the leading fraud attack vector around the world, even more than account takeovers and scams. Shanmugam explains how Casap leverages AI agents that function like expert investigators to determine when disputes are legitimate.

Generative AI-powered shopping has been gaining steam in the latter half of this year and is shaping up to be one of the top trends as we move into 2026. The availability and convenience of Gen AI tools are shifting consumers’ shopping habits away from traditional browser-based shopping as these new tools become more deeply embedded in the shopping experience.

Adobe for Business published a report earlier this year that shows momentum in the use of generative AI-powered chat services. The report, which surveyed more than 5,000 US individuals, aimed to complement a study conducted during the 2024 holiday shopping season that examined consumers’ usage of Gen AI-powered chat services and browsers.

There are six standout findings from the report that exemplify the shift in consumers’ habits.

Generative AI traffic to retail sites exploded

Adobe found that the first surge during the 2024 holiday season reached a growth of 1,300% year-over-year. Following this, the recent data shows that traffic from Gen AI-powered chat tools and browsers has continued to accelerate, reaching a 4,700% year-over-year increase as of July 2025. AI-driven visits now represent a meaningful and fast-growing share of retail shopping and research activity.

Over one-third of US consumers have used AI for shopping

According to Adobe’s 5,000-person survey, 38% of consumers have used generative AI at some point during their shopping process, while 52% plan to do so this year. Shoppers are most commonly using it for product research (53%), recommendations (40%), finding deals (36%), creating shopping lists (30%), and gift ideas (30%).

AI shoppers are more engaged and informed

Consumers that arrive at a website from AI-powered sources spend 32% more time per visit, view 10% more pages, and have a 27% lower bounce rate than those coming from traditional sources such as search, social media, and email. Shoppers using Gen AI also report an increase in satisfaction, with 85% of users saying that AI improved their shopping experience and 73% now rely on it as their primary product research tool. Overall, shoppers using Gen AI tools are more engaged than shoppers using traditional ecommerce methods.

Conversions still lag

While consumers are increasingly using Gen AI tools for browsing, many stop there and fail to actually make the purchase. In fact, Adobe’s study showed that AI-driven traffic is still 23% less likely to convert than traditional traffic. This figure has actually shown a bit of improvement over the past few months. The study showed that conversion rates were 49% lower in January 2025 and 38% lower in April 2025. This suggests that consumers increasingly trust AI-powered recommendations enough to complete purchases directly.

Revenue-per-visit from AI sources is catching up to non-AI visits

When it comes down to dollar figures, it turns out that Gen AI-powered shopping isn’t as valuable, though that is quickly changing. Adobe’s study found that AI-driven revenue-per-visit rose 84% from January 2025 to July 2025. While AI-driven visits were worth 97% less than non-AI visits in July 2024, they were only 27% less than a non-AI visit a year later. This indicates shoppers are moving from using AI purely for research to actually buying through AI-driven paths.

Mobile is fueling AI-driven shopping growth

According to the study, in July 2025, 26% of AI-driven retail traffic came from mobile. This is up by 8 percentage points from 18% six months earlier. Adobe expects mobile AI use to further close the conversion gap, given consumers’ tendency toward more impulse-driven shopping on phones.

All of these statistics paint a picture of what we can expect to happen to ecommerce in the next few years. As consumers increasingly turn to their preferred Gen AI tool when they start their shopping journey, we’re witnessing the early stages of a new kind of marketplace. In ecommerce 2.0, we’ll see discovery, recommendation, and payment converge within a single interface. Competition in this new frontier will no longer be about who owns the checkout. Rather, it will centralize around who owns the conversation that leads there. As the 2025 holiday shopping season picks up, expect to see fintechs, retailers, and payment providers racing to claim their spot in the Gen AI shopping ecosystem.

This week I’m looking at a trio of stories from the wealthtech beat: SS&C’s completed acquisition of Calastone, the emergence of a new UK-based wealthtech, and a look at two, not-quite-contrasting interpretations of funding for wealthtechs in Q3 2025.

SS&C Technologies completes $1 billion acquisition of Calastone

Initially reported in July, SS&C Technologies announced this week that it has completed its acquisition of Calastone. The company purchased Calastone, a London-based, international funds network and provider of technology solutions to wealth and asset managers, from global investment firm Carlyle for a price of £766 million ($1.03 billion). The transaction was funded via a combination of debt and cash.

“Calastone’s network and technology further strengthen SS&C’s leadership across global fund operations,” Chairman and CEO of SS&C Technologies Bill Stone said. “Together, we will accelerate innovation for our clients, expand our reach, and continue to simplify the way the industry operates.”

The acquisition will bolster SS&C’s solutions for fund administration, transfer agency, AI, and intelligent automation. The union will also facilitate the launch of a unified, real-time operating platform to lower costs, complexity, and operational risk for fund industry participants while providing enhanced distribution, investor servicing, and operational scalability.

Founded in 1986 and headquartered in Windsor, Connecticut, SS&C Technologies provides mission-critical, cloud-based solutions to more than 22,000 companies in financial services and healthcare. A member of the Fortune 1000 and a publicly traded firm on the NASDAQ under the ticker SSNC, SS&C Technologies is the largest independent hedge fund and private equity administrator, and the largest mutual fund transfer agency, in the world.

Calastone runs the largest global funds network, linking more than 4,500 financial organizations worldwide across 57 markets. The company processes more than £250 billion ($334 billion) of investment value each month, and maintains offices in Luxembourg, Hong Kong, Taipei, Singapore, New York, and Sydney. With the completed acquisition, Calastone’s 250 employees will join SS&C Global Investor & Distribution Solutions, effective immediately.

“This is an exciting new chapter for Calastone,” company CEO Julien Hammerson said. “Joining SS&C gives our clients and employees access to greater scale, investment, and opportunity. We’re proud of what we’ve built and look forward to contributing to SS&C’s continued growth and global success.”

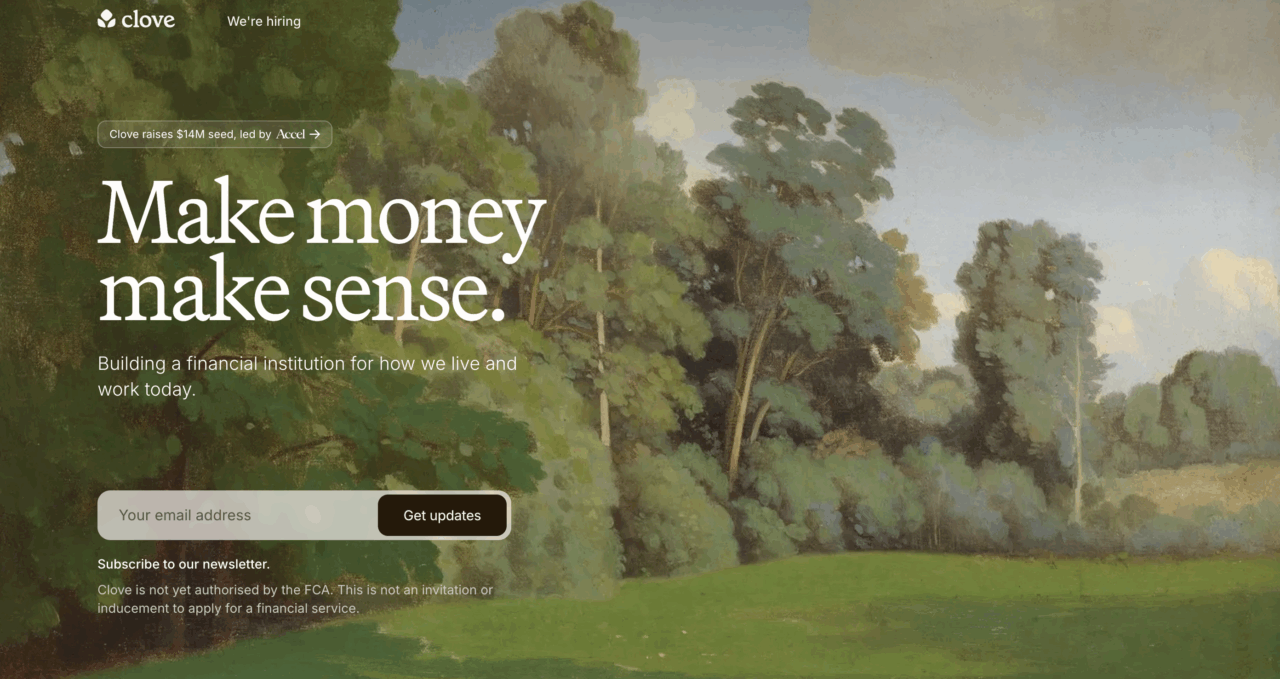

UK wealthtech Clove emerges from stealth

London-based wealthtech Clove has emerged from stealth with €12 million ($14 million) in pre-seed funding in its coffers. The round, which was led by Accel, is regarded as one of the largest early-stage financings for a European startup this year. Kindred Capital VC and Air Street Capital also participated in the investment, along with a handful of angel investors.

“With Clove, we are seeking to break the traditional economics of financial advice by combining the expertise of human advisers with the efficiency of AI,” Co-Founder Alex Loizou said. “Our goal is to make financial planning more accessible, affordable, and effective than ever before, for everyone from young professionals and aspiring entrepreneurs, to growing families and those starting to think about retirement.”

Clove was launched by Loizou and fellow founder Christian Owens at a time when the UK’s Financial Conduct Authority has determined that professional financial advice can make a significant difference—as much as 10%—in financial outcomes compared to those who do not have access to this advice. Loizou and Owens see an opportunity to provide this advice via a combination of human insight and AI intelligence.

“Our aim is to make it possible to deliver high-quality, personalized advice at an unprecedented scale,” Owens wrote on the Clove blog. “As we started exploring this problem we discovered that most of what financial advisers do isn’t actually advice, it’s admin. By using AI to reduce that burden, we hope to give advisers more time to do what they are trained to do: help people make better decisions.”

Clove will use the funding to hire additional talent ahead of a full launch in 2026, subject to FCA authorization.

Smaller, but busier? Wealthtech deal activity up, total funding down in Q3 YoY

According to FinTech Global Research, wealthtech investments in the US dropped significantly year over year in Q3 2025. Deal activity was robust by comparison, with 71 deals in Q3 2025 compared to 62 deals in Q3 2024, but total funding dropped to $861 million this year in the third quarter compared to $1.8 billion raised in Q3 2024. The average deal value also declined, falling to $12.1 million this year from an average of $28.8 million in Q3 2024.

The analysts cited “persistent macroeconomic uncertainty” and, interestingly, “evolving wealth management technologies” for what it said was a cautious, “lower-risk” approach by investors.

To that final point, there may be reason for optimism. Looking out over a longer time frame, the CB Insights State of Fintech Q3’25 Report noted that wealthtech funding was “maintaining momentum” and on track to double 2024 totals, having already topped 2024 levels. In fact, CB Insights highlighted “strong confidence in digital-first wealth management solutions” and vigorous hiring as positive signs. The report noted that financial advisor productivity tools, wealth management banking and lending platforms, and AI investment intelligence platforms were among the top sectors in fintech in terms of headcount growth year-over-year.

How is AI helping lenders make better loans to more qualified borrowers? How can stablecoins promote cross-border trade and help local merchants make more sales in more markets? How can banks overcome the limitations of their legacy systems and confidently embrace modernization? The latest round of interviews from Finovate VP Greg Palmer and the Finovate Podcast cover all these issues and more.

Here’s a look at the Finovate Podcast’s recently completed September slate. By the way, the first few podcast interviews with FinovateFall Best of Show winners have just begun to drop. If you want to get an early listen, check them out on our Finovate Podcast page.

Greg Sullins (LinkedIn), Head of the US Banking Center of Excellence for Newgen Software, talks with Greg Palmer about how AI is revolutionizing the lending process. Sullins explains why AI is especially valuable in the lending business, in part because it sits at the intersection of data intensity, risk management, and the customer experience. Episode 271.

Founded in 1992, Newgen Software offers lenders a low-code platform that provides end-to-end automation, AI-powered decisioning, configurable workflows, and enhanced customer experience capabilities. The company’s technology enables business analysts rather than programmers configure workflows and deploy changes quickly. This helps financial institutions modernize their legacy systems faster while remaining compliant.

Bridgit Antwi (LinkedIn), Head of Strategy and Planning at Flutterwave, talks with Greg Palmer about the rise of stablecoins, the importance of building strong relationships across the financial ecosystem, and what Flutterwave is doing to help local merchants expand their reach across borders. Episode 270.

Africa’s leading payments company, Flutterwave was founded in 2016 by Olubenga “GB” Agbola. The firm offers a single API platform that enables merchants to seamlessly collect payments across multiple countries, currencies, and payment methods. Flutterwave operates in more than 30 countries, holds licenses in 14 African nations, and maintains 35 money transfer licenses.

Rouzbeh Rotabi (LinkedIn) Chief Revenue Officer at Qolo and Greg Palmer talk about the challenge and opportunity of payment infrastructure modernization. With more than 20 years of experience in fintech and payments, Rotabi explains how the need to increase deposits, infrastructure limitations of legacy systems, and evolving consumer demands are pressuring banks to embrace new technological solutions. Episode 269.

Founded in 2018 and headquartered in Fort Lauderdale, Florida, Qolo offers an all-in-one platform for card issuing, ledger management, and payment processing. The company helps businesses launch faster, lower costs, and secure real-time visibility into the payment flow.

Stablecoins may have saturated headlines earlier this year, but September has marked a turning point to the industry. This month has brought four large announcements in agentic payments, demonstrating that the technology has moved from fringe to forefront.

And while the announcements speak volumes about how quickly technology developments move in fintech, it also sends seven major signals to banks and fintechs.

A preferred protocol layer emerges

Earlier this week, agentic commerce platform Circuit & Chisel landed $19.2 million to launch ATXP, a web-wide protocol. The protocol will not only position Circuit & Chisel as an orchestrator of agentic commerce, but it will also help streamline workflows and enable businesses to operate faster and more efficiently by leveraging revenue-generating autonomous agents.

The launch and growth of ATXP show the industry’s movement toward a web-wide standard for agentic payments. It also highlights how payments are shifting from app-specific functions into a common infrastructure layer.

Big Tech wants to lead

Google and PayPal made headlines last week when they announced their partnership on agentic shopping, embedded payments, payments processing, and more. The two are positioning themselves at the forefront of agentic payments and commerce and are providing developers with tools to engage in the new era of digital commerce.

The partnership between Google and PayPal shows that Big Tech wants to be at the forefront in shaping how commerce and payments flow online in the future. This early movement is a warning to players that sit back on the sidelines and wait for others to move first. Slow-moving banks and fintechs risk being relegated to backend providers unless they strategically find their own niche in the space.

Crypto and Web3 join forces with platforms

Also last week, Google announced that it is leveraging the x402 protocol within its Agent Payments Protocol (AP2) to allow AI agents to pay each other using stablecoins on Coinbase. With the ability to handle payments on behalf of their end users, agents will now be able to complete certain tasks that previously required manual oversight, such as paying for data crawls, services, or microtasks.

The launch merges crypto protocols and mainstream platforms, and is a great example of how agentic payments won’t be limited to decentralized finance environments. Instead, we’ll see agentic payments within web browsers, search, and commerce platforms.

Credit has an agentic future

After landing strategic backing from Citi Ventures earlier this month, agentic AI-powered credit data and payments platform Spinwheel plans to fuel growth, expand its agentic AI platform, build out its data sets and add new products. Additionally, Citi Ventures will advise the company on banking-specific product use cases.

This funding shows backing for the idea that consumer credit and agentic payments will be integrated in the future. It shows the breadth of potential for agents to manage payments, debt repayment, refinancing, and credit optimization.

The shift to autonomous decisioning

All four of these announcements demonstrate how payments will move from static, user-initiated tasks to autonomous, rule-driven events. To stay current, banks and fintechs will need to embed decisioning logic, risk scoring, and compliance into their payment flows.

Regulators will take notice

While regulators don’t have a lot of time (or expertise), agentic payments are sure to get their attention. These announcements around autonomous money movement have raised concerns around AML, KYC, and consumer protection issues. Firms that build compliance into agentic systems will be one step ahead in winning not only consumer trust but also regulators’ approval.

The race for standards is on

Much like open finance, the world of agentic payments will desperately need to abide by an agreed upon set of standards. Because competing protocols and ecosystems could fragment adoption, the disorganization could not only disrupt the user experience, but it could also wreak havoc on creating a clean, regulated environment. Whichever parties are involved in driving standards for payment rail interoperability will take the role that SWIFT did in shaping payments rails in the 1970s.

The ultimate question is, who will lead and who will follow?

Each year at FinovateFall, we look for new and exciting ways to showcase the breadth of fintech innovation that lies just below the radar of the mainstream fintech conversation. This year, we introduced The Impact Zone: a special program for fintech startups that gives them access to highly curated content and demos; unlimited high-level meetings with financial institutions, banks, credit unions, and venture capital firms; and a strategically located table outside the plenary hall to facilitate networking and maximum visibility.

“The Impact Zone debuted at FinovateFall this year, spotlighting eight startups with AI-driven solutions in bill management, wealth management, digital lending, and more,” Finovate VP and Director of Fintech Demos Heather Stowell explained. “Focused on growth and scaling, these innovators are ones to watch—expect to see them on the Finovate stage soon!”

Let’s meet the companies from FinovateFall 2025’s Impact Zone.

AiVantage

Headquartered in Vienna, Virginia, AiVantage provides credit unions, banks, and financial institutions with AI-powered solutions that help them improve efficiency, enable personalized customer engagement, and drive growth.

The company’s flagship solution, InteractiveAI, helps construct each customer interaction uniquely at scale to help financial institutions innovate and stay competitive. Karan Bhalla (LinkedIn) is CEO.

In June, AiVantage announced that it had secured a large strategic investment from Our Community Credit Union (OURCU). The amount of the funding was not disclosed. As part of the investment, OURCU will take a seat on the AiVantage CUSO board of directors.

Blue Street Data

Founded in 2022 and headquartered in Pittsburgh, Pennsylvania, Blue Street Data facilitates the process of finding, evaluating, and purchasing third-party data.

The company’s PQC Engine is an intelligent search platform that enables businesses to discover, compare, and buy high-quality datasets at the optimal price. Including use cases such as personalization, risk modeling, and market analysis, Blue Street Data’s technology helps financial institutions derive greater value from external data. Andy Hannah (LinkedIn) is CEO.

Earlier this year, Blue Street Data announced that it had joined the Sourcing Industry Group, also known as SIG|ORG, an international network for sourcing, procurement, and risk professionals. The company hopes its engagement with the group will elevate the standard for how organizations and businesses evaluate and transact with external data.

CloudBankin

CloudBankin offers an end-to-end cloud-based loan software solution to enhance digital lending. CloudBankin’s Loan Origination System enables a variety of financial institutions—including banks, NBFCs, and MFIs—to disburse loans in less than 10 minutes.

The company’s AI-powered lending agents monitor risk, improve decisioning, and enhance customer engagement across credit underwriting, fraud detection, document intelligence, repayment prediction, and collections. Mani Parthasarathy (LinkedIn) is CEO.

CloudBankin’s Loan Management System has delivered 97% operational efficiency, 50% reduction in time-to-market for product launch, 90% decrease in the data entry error, and 100% compliance with industry regulations. Founded in India, the company’s US headquarters is in Delaware.

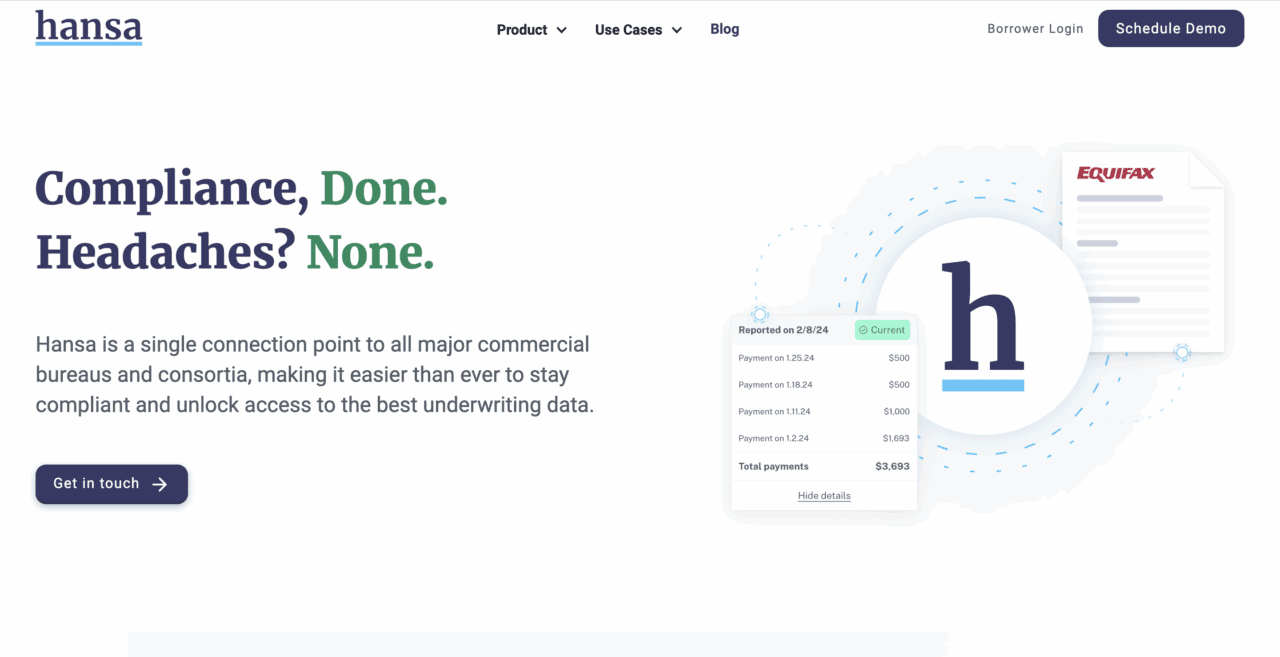

Hansa

Hansa helps lenders report commercial payment data to business credit bureaus. The company serves as a single connection point to all major commercial bureaus and consortia to make it easier for businesses to access the best underwriting data and remain compliant.

Hansa’s technology automates many of the pain points of credit reporting to help reduce delinquencies and support credit-building for small business borrowers. Henry Magun (LinkedIn) is Founder and CEO.

Founded in 2023 and headquartered in New York, Hansa began this year with the launch of its enterprise solution for commercial loan payment reporting. The new offering consists of two key components: a data reporting system that simplifies reporting by transforming and transmitting CSV file and API request data to credit bureaus, and a borrower dashboard that gives borrowers greater transparency on how their payments affect their credit.

Moneylab

Moneylab offers an AI-powered platform that enables banks and credit unions to optimize the way they manage their assets and liabilities.

Headquartered in Vancouver, British Columbia, Canada, Moneylab gives Chief Financial Officers a solution that consists of a collection of AI agents and expert systems that specialize on specific processes such as compiling and writing variance reports, monitoring loan portfolios, and pricing securities assets in real time. Vincent Wong (LinkedIn) is Moneylab Co-Founder and Chairman.

Founded in 2019, Moneylab announced this spring that it had acquired strategic intellectual property from Carfang Group. The all-share transaction will complement Moneylab’s platform offering by providing historical and current data points and analytical processes.

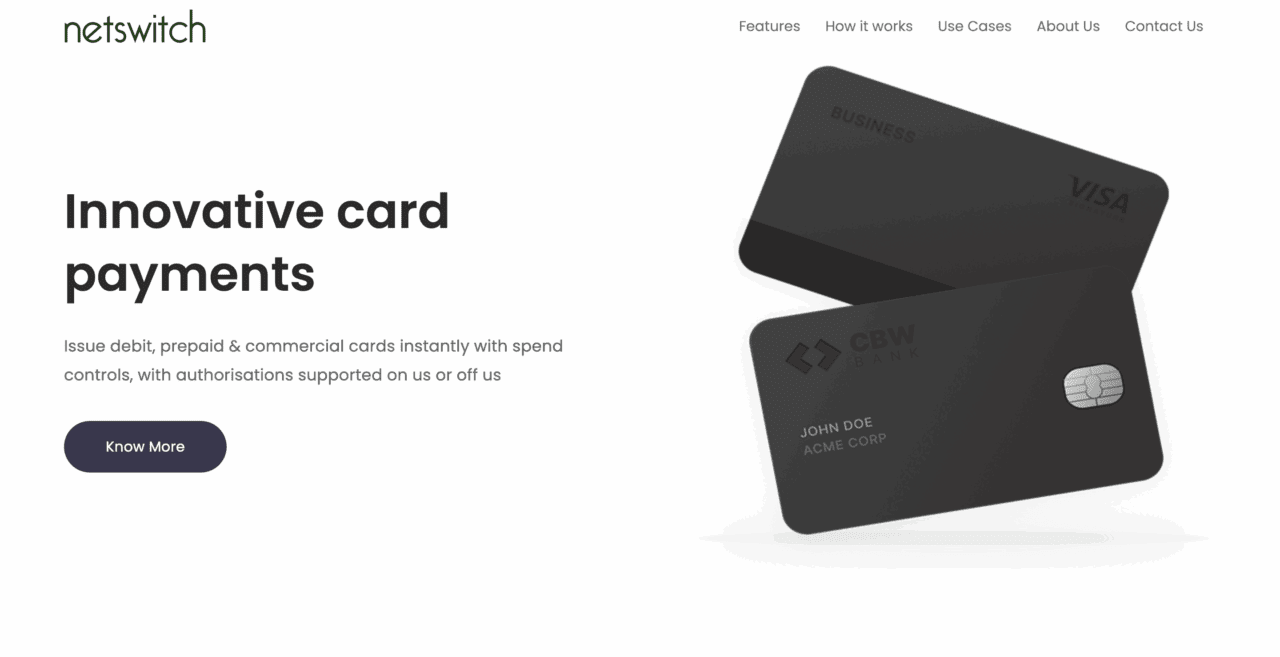

Netswitch Technologies

Netswitch offers a prepaid and debit card processing solution with a built-in ledger that is specially designed for fintechs and sponsor banks.

The company’s platform features pre-configured card controls and compliance workflows. Its custom Large Language Model (LLM) supports quick configuration and faster UI development to ensure rapid onboarding. Kris Lakshmanan (LinkedIn) is CEO.

Founded in 2020 and headquartered in Lawrence, Kansas, Netswitch supports the issuance and processing of debit, virtual, corporate, and employee cards, as well as travel and gift cards.

Nextvestment

Nextvestment offers an AI-native engagement layer for wealth management teams. The platform’s conversational co-pilots transform client questions into trusted conversations, actionable insights, and portfolio guidance.

The technology enables financial advisors to better engage with clients and provide personalized service at scale. At the same time, Nextvestment empowers clients to examine and explore their portfolio and the markets on their own, with a seamless handoff to professional advisors when they need guidance the most. Michael Davies (LinkedIn) is CEO and Founder.

Launched in 2024 and headquartered in Singapore, Nextvestment announced earlier this year that it had joined the NVIDIA Inception Program. The free, virtual accelerator enables startups innovating in AI, data science, and high-performing computing to access NVIDIA developer resources and technical training, go-to-market support and expertise, and exposure to venture capital firms via the NVIDIA Inception VC Alliance.

TrieveTech

TrieveTech offers an AI-powered, multi-tenant, white-label platform that sits at the intersection of bill aggregation, payments, analytics, insights, and customer experience enhancement to enable Energy Service Companies (ESCOs) to easily and quickly brand, customize, launch, and integrate new products and solutions. John Mulcahy is President.

Launched in 2020, TrieveTech is headquartered in Akron, Ohio. The company’s technology helps firms lower overhead costs, reduce customer care needs, and increase customer retention, leading to greater profit margins.

What are you looking forward to most at FinovateFall next week (September 8 through September 10; New York Marriott Marquis Times Square)? Is it the 60+ live fintech demos that will hit the stage first thing Monday morning? Maybe it’s our keynote address on banks and stablecoins, or one of our executive briefings on community banking or AI in financial services? Maybe you’re one of the lucky ones invited to our special Leaders+ event Sunday evening?

Whatever you’ve got your sights set on, we’re thrilled to have you join us in New York for our annual fall conference. And to further whet your appetite for all things FinovateFall, here are a few exciting options to add to your agenda that Finovate attendees over the years have cited as among their favorites.

Tickets to the show are still available! Visit our FinovateFall registration hub and save your spot today!

Analyst All Stars: How financial services have been changed forever

FinovateFall always kicks off Day Two with our Analyst All Stars session. One of our most popular features, Finovate’s Analyst All Stars showcases three leading fintech analysts who take the stage for just seven minutes each to focus on a specific issue in our industry. Our expert analysts will share their insights on the trends that are impacting fintech today and driving the innovations of tomorrow. Tue, Sept 9. 9:05 am.

Tech Trends That Will Define Financial Services & Fintech into the Next Decade

The Bank of 2030—How to Move from a Product Centric Design to Life Stage Banking

Beyond the Application: Making Customer Onboarding More Effortless

Speaker-Led Lunch Discussions: A Taxing Time for Fintech: JPMorgan Data Fees & What it Means for Open Banking in the US

Our Speaker-Led Lunch Discussions are a great way to network and share insights with leading fintech analysts, founders, and executives on some of the most topical issues in fintech and financial services. This year, we’re focusing on the challenges that open banking is facing in the US—from JPMorgan’s threat to charge for access to consumer data to the regulatory battles in Washington, DC and in the courts. Tue, Sept 9. 12:40 pm.

Investor All Stars: In turbulent times, what is the outlook for the market & what does it mean for funding levels, valuations & the future of financial services? Looking to the future, how can niche product fintechs be turned into platform companies?

What is the current state of fintech funding? How will the policies of the Trump administration impact investment in growing fintechs? What can we expect in the M&A space? What areas of fintech are seeing the strongest investment and where are fintechs most vulnerable to funding shortfalls? Our Investor All Stars panel will tackle all these questions and more! Wed, Sept 10. 3:35 pm.

Featuring:

Josh Tanenbaum, Managing Partner, Rebalance Capital (moderator)

After the CFPB withdrew its lawsuit over Section 1033 of the Dodd-Frank Act, the bureau stated that it would begin a new, “accelerated” rulemaking process with an Advanced Notice of Proposed Rulemaking (ANPR) within three weeks. That three-week period ended last week, on August 22nd, when the CFPB published its Personal Financial Data Rights Reconsideration, effectively kicking off the new rulemaking process.

Much is riding on how this rule takes shape, not only for banks, but for fintechs and consumers alike. Visa’s recent move to abandon its US open banking initiatives underscores just how high the stakes are. In its latest release, the CFPB asked for comments and data to guide its decisions on four critical issues tied to Section 1033. Below, we’ll walk through each issue and explore the potential impact.

Representatives: who deserves access to the data?

The first of the four issues is defining who can serve as a representative on behalf of the consumer. The question essentially asks who can make a request to access the consumer’s data on their behalf. Today, this includes not only the consumer themselves, but also third-party aggregators and fintechs, as well. If the CFPB decides to narrow this scope, it could potentially block third-party services from accessing consumer data, limiting it to the consumer and the bank itself.

The latter would favor incumbents as it allows them ultimate control. For fintechs, this would create a risky environment. The uncertainty would make it risky to invest and build APIs that could be restricted in the future.

Fee structures: who pays for data access?

The second of the four issues seeks to determine the optimal amount of fees that banks should be able to charge in response to a customer-driven request. As a result, data access may no longer be free for aggregators, which may require them and fintechs to reshape their business models in response.

Charging for data would allow banks to recoup compliance costs for API access, but may receive negative attention from fintechs and consumers. Additionally, fintechs with already thin margins may be forced to look for an exit.

Data security: weighing threats vs. benefits

The third of the four issues the CFPB spotlighted is the threat and cost-benefit analysis for data security associated with complying with Section 1033. If the Bureau requires compliance with tighter security requirements, all stakeholders will feel the repercussions of tighter security expectations.

With tighter compliance, small fintechs that previously had limited compliance requirements may now need to step up to higher standards. This could ultimately lead to consolidation, since large, well-resourced firms would be able to more easily meet compliance.

Data privacy: the cost of protection

The final of the four issues the CFPB spotlighted is the threat landscape surrounding data privacy associated with Section 1033 compliance. The Bureau may set new limits on how fintechs are allowed to monetize consumer data in an effort to maintain their privacy.

With new guardrails on how they are allowed to monetize consumer data, fintechs may face limitations on using data for personalized marketing or other secondary data uses. As a result, innovation may slow down, but consumers may gain more confidence.

Your turn to comment!

The CFPB’s recent call for comments is more than regulatory housekeeping. It is highly consequential and will determine the future of open banking in the US. The Bureau’s questions signal real costs, risks, and opportunities.

It is important to make your voice heard on these issues! In the six days that the comment period opened, only seven comments have been submitted. Send your comments to the CFPB by October 10, 2025 at 11:59 pm EST.

How have the opportunities and challenges for women in fintech and financial services changed in recent years? What can community banks do to better compete in the “consumer deposit wars?” And what do banks, credit unions, and other companies in the financial services space stand to gain from effectively deploying AI in their operations?

FinovateFall’s Executive Briefings will tackle all these questions and more next month, September 8 through 10, at the Marriott Marquis Times Square in New York. Check out our capsule summaries below. Then visit our FinovateFall registration hub to reserve your ticket. We can’t wait to show you what we’ve got in store this year!

Executive Briefing: Women in Fintech—How can we all make sure we are moving the needle?

Moderated by Michelle Tran, Founder, NYC Fintech Women, this Executive Briefing will examine a range of issues facing women in fintech and financial services. The conversation will include discussion on initiatives that are making a difference in growing and retaining female talent, the importance of diverse perspectives in AI development, and how to drive positive change in the industry. Mon, Sep 8, 10:20 am.

Featuring:

Sherry Wu, Chief Technology Officer, University of Michigan Credit Union

Executive Briefing: The Coming Storm for Community Banks

Moderated by Jason Henrichs, CEO, Alloy Labs, this Executive Briefing will investigate ways that community banks can develop a winning strategic plan that enables them to embrace innovation and better serve their customers. The panelists will share their insights on topics ranging from the so-called consumer deposit wars to the challenge of aligning culture, strategy, and execution when integrating enabling technologies like AI. Tue, Sep 9, 10:40 am.

Pam Kaur, Head of Bank Technology, BankTech Ventures

Executive Briefing: The AI Competitive Imperative—The ten AI solutions you need to know about today

Moderated by Kate Drew, Partner, Director of Research, CCG Catalyst Consulting, this Executive Briefing will focus on real-world applications and use cases for AI in financial services. The panelists will discuss how to implement AI safely and within regulatory requirements, as well as share strategies to ensure that AI is aligned with the institution’s business and change management strategy. Tue, Sep 9, 10:40 am.

Featuring:

Kimberly Kirk, Executive Vice President and Chief Operations Officer, Queensborough National Bank & Trust Company