In 2026, financial services have jumped well beyond the AI experimentation phase. At this point, firms are no longer considering whether or not to adopt AI, and are instead thinking about deployment strategies that will improve operations, decision-making, and internal productivity.

When organizations apply AI to their everyday processes, they can analyze data more effectively, automate workflows, glean insights, and help teams make better decisions with less manual effort. Regardless of the subsector, AI-driven platforms are becoming essential to creating modern banking infrastructure.

At FinovateSpring 2026, a fresh group of five companies will demonstrate their newest technologies that help banks turn AI from a buzzword into a practical tool for operational intelligence and efficiency.

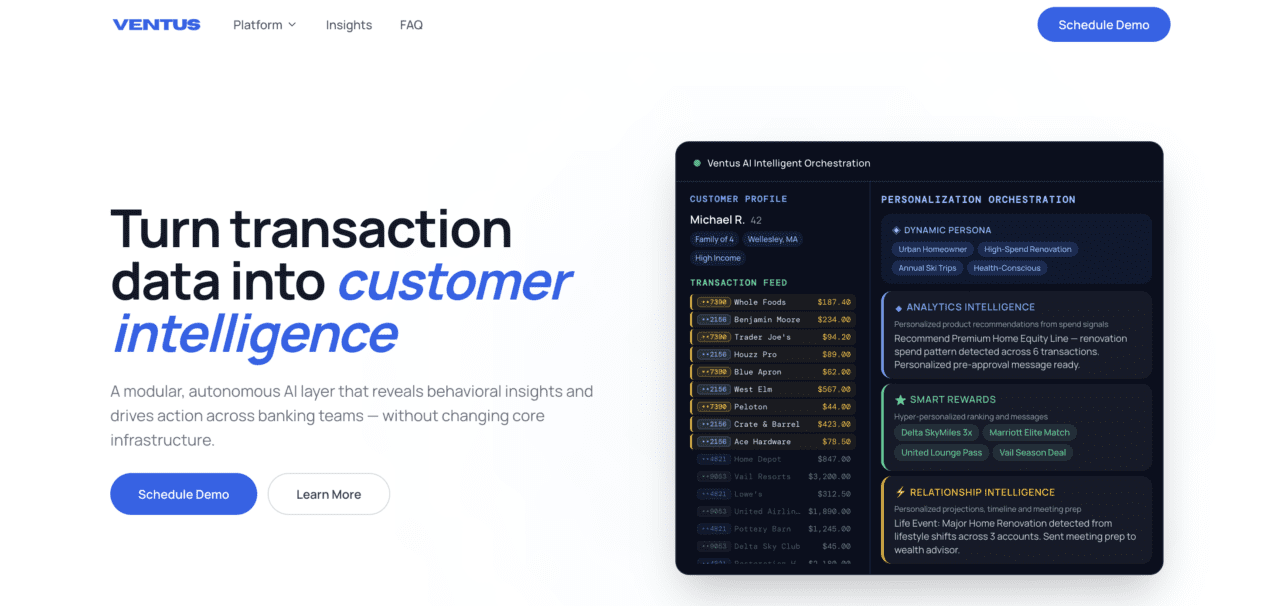

Founded in 2025, Ventus AI transforms raw banking transaction data into semantic customer intelligence to enable personalized experiences, smarter analytics, and human-centered digital banking without changing core infrastructure.

The Delaware-based company helps banks and wealth managers turn transactions into dynamic personas, proactively detect customer life events, and offer plug-in intelligence for any core banking system.

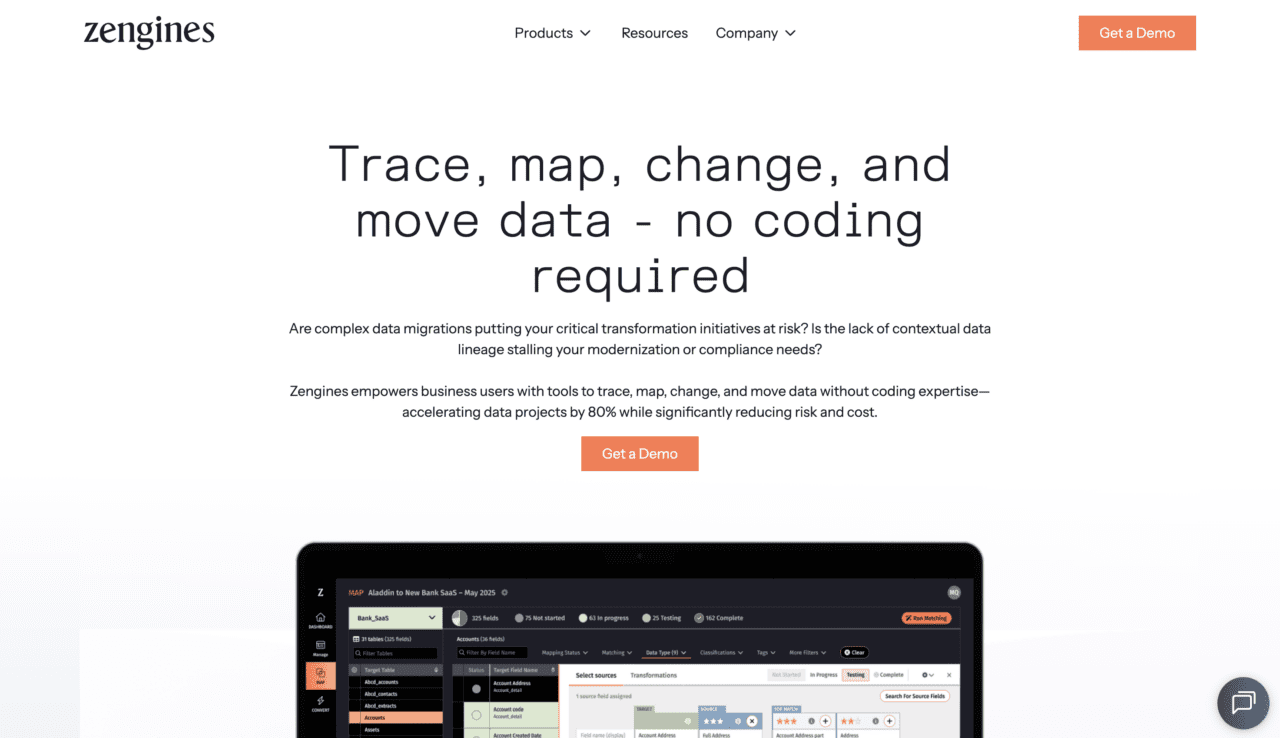

Zengines addresses data transformation challenges to modernize mainframes without losing logic. The platform helps organizations work with legacy code to seamlessly migrate data into modern systems. The company offers two products: Data Lineage, which offers critical and easy-to-understand insights into firms’ legacy systems; and Data Migration, which empowers business analysts to drive the entire process without coding expertise.

Headquartered in Bedford, Massachusetts, Zengines’ modern approach makes legacy systems searchable, which helps firms satisfy auditors faster so transformation and compliance don’t stall.

Lyzr Architect is an enterprise AI platform that converts natural language into governed, production-ready agentic applications. Founded in 2023, the company offers a platform that enables secure, compliant deployment across banking, financial services, and insurance enterprises.

The New Jersey-based company helps convert natural language into production-grade multi-agent applications, provides deterministic validation with governance and audit logging, and offers full-stack apps, exportable code, and GPU-optimized model execution.

Founded in 2024 and headquartered in San Francisco, California, Saris AI is an agentic AI solution that builds and launches AI agents to automate back-office workflows. The company helps banks and credit unions scale their operations without adding headcount by automating 90% of their tasks with zero change management.

Saris AI securely integrates with core banking platforms, loan origination systems, document repositories, and communication tools to help organizations lower workflow costs.

Syntex’s digital onboarding software helps banks and credit unions verify documents, track approvals, and reduce small-business onboarding to a matter of days.

Founded in 2025, the company offers a self-serve client intake with document verification; provides real-time tracking of documents, approvals, and ownership; and reduces onboarding from weeks to days with a Reg B audit trail.

Why banks should care

For financial institutions, the promise of AI extends well beyond simply delivering a better customer experience. In 2026, fintechs are bringing great opportunities to help firms modernize legacy operations without dramatically increasing costs or headcount.

Banks face mounting pressure to process more data, respond faster to customers, and maintain compliance in today’s increasingly complex regulatory environment. AI platforms that can surface insights from transaction data, automate internal workflows, and help teams navigate complex systems bring a practical way to improve productivity and decision-making.

FinovateSpring 2026 will take place at The Sheraton San Diego on May 5 through 7. Register today using this link and save 20%. Finovate attracts 600 bankers from across the spectrum—afrom the largest US banks to regional banks, community banks, and credit unions.