This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

The fallout from JP Morgan’s plan to charge companies for access to client bank account data continues as—according to a report from Bloomberg—Visa has announced that it is shuttering its open banking unit.

We’ve got a lot to say about the fight for open banking next month at FinovateFall. For now, be sure to check in to Finovate’s Fintech Rundown for all the latest fintech news!

AI-powered credit intelligence company martini.ailaunches its Financial Autonomy Ladder, a framework for measuring an institutions evolution from manual to autonomous decision-making systems.

MeridianLinkexpands its partnership with Jack Henry, which will resell the suite of Meridian Link One platform solutions, including MeridianLink Mortgage and MeridianLink Consumer.

First Northern Credit Union selectsAppli to modernize member lending experience.

Small business solutions

Expensifyannounces upgrades to its Expensify Travel offering including central billing, event management, and employee itineraries.

What happens when an ongoing revolution in payment innovation meets a regulatory regime determined to ensure secure and safe transactions for individual consumers, business entities, and even governments? This is the payments landscape in the UK and EU in 2025. As a proliferation of payment options promises to streamline banking and commerce, regulators, fintechs, and financial services companies are looking for ways to make sure that the challenges to these new payment options—from technical complexity to new forms of fraud and financial crime—are met.

To discuss these and other issues involving payments and the emerging regulatory environment, we caught up with Stuart Neal, Chief Executive Officer of Boku. Appointed CEO in January of 2024, Neal previously served as the company’s Chief Financial Officer and Chief Business Officer of Boku’s Identity Division. A champion of payment choice, Boku supports a global network of localized payment solutions, including Direct Carrier Billing (DCB), digital wallets, and account-to-account connections. Founded in 2008, Boku is headquartered in London.

Local Payment Methods (LPMs) have proliferated around the world over the past decade. Socially and technologically, what has powered this growth?

Stuart Neal: Local Payment Methods (LPMs) have had a meteoric rise over the past decade. It’s hard to overstate what a significant and rapid change we’ve seen, and behind it are two main driving forces: changing consumer preferences and rapid technological innovation.

Payments as an industry is finally beginning to reflect the diversity of people’s preferences around the world. And that’s a really positive development. It’s fair to say that traditional financial systems left many people and communities underserved, but LPMs—from mobile wallets in Africa to RTP schemes like UPI in India—bridge this gap, and they’re empowering billions of consumers to participate in the digital economy. This financial inclusion is great for society, for merchants and for the payments industry as a whole.

At Boku, we want to be at the heart of this transformation. People just want convenience, and we’re here to help them buy what they want, the way they want. With one of the biggest LPM networks in the world, we’re making it easier than ever for global merchants to meet consumers where they are.

Looking at Europe specifically, what role has the European Payments Initiative (EPI) played in driving this trend?

Neal: While still in its early stages, the European Payments Initiative (EPI) is playing a crucial role in reshaping the EU payment landscape. Its focus on creating a unified, pan-European payment solution, fostering instant payments, acquiring established players like iDEAL and Payconiq, and advocating for regulatory changes positions it as a future leader in European payments. By competing with global giants, EPI is pushing Europe toward a more integrated, efficient, and competitive payment system. However, full market transformation will likely take a few more years, with real change expected in 2025.

So far the EPI has excelled in laying the groundwork for this payments evolution by clearly articulating its vision and aligning strategically with the key pillars of ecommerce. By fostering strong relationships with merchants, PSPs, and issuing banks, EPI is now in a great position to effect significant change and shape the future of digital payments across Europe.

Part of this was the launch of the real-time payment system Wero last summer. Can you tell us a little about the significance of the Wero launch and how adoption has been so far?

Neal: The Wero Wallet, launched by the European Payments Initiative (EPI), serves as a strong entry into the EU market with the goal of unifying Europe’s fragmented payment landscape. Initially focusing on person-to-person (P2P) payments, Wero will expand to e-commerce in 2025 and in-store payments by 2026, offering various options such as instant payments, installment plans, and subscriptions. With the acquisitions of Dutch payment solution iDEAL and Luxembourg-based Payconiq International or the transition of the former Paylib P2P user base in France to Wero, EPI / Wero is well-positioned for success. However, EPI has opted for a phased market rollout, like what we have seen by other payment schemes in the past, starting with smaller-scale P2P launches in countries like Germany and France, while the true transformation is expected to unfold in 2025. Notably, these acquisitions continue to operate under their original brands, allowing for organic user growth before transitioning fully to Wero.

Has adoption of Wero been uniform across Europe or have some markets remained more reluctant? What distinguishes the eager adopters from the more cautious?

Neal: This is an interesting question, and one that will be clearer by the end of 2025, when we can fully assess the impact of Wero’s initial e-commerce launches. However, what we can say so far is that Wero’s adoption has been strongly shaped by key market dynamics. Starting in July 2024, users of participating German banks were able to sign up for Wero, with Belgium following suit by the end of 2024, also seeing gradual, organic growth. Around the same time, Wero benefited from a significant boost in France, where the transition from Paylib to Wero provided a built-in user base of approximately 35 million registered Paylib users. Looking ahead, the exit of local payment schemes like Giropay in Germany is expected to reshape the competitive landscape, presenting new opportunities for Wero to establish itself as a leading player in the market.

What can be done to encourage broader acceptance of solutions like Wero and less reliance on cards?

Neal: Accessibility is key to the adoption of anything. And if solutions like Wero are to be more broadly adopted, they must become more accessible for consumers and merchants. So to start with we need to integrate these solutions seamlessly into merchant payment ecosystems and do so in a way that matches–or ideally betters–the convenience of cards. You need a frictionless experience for people on both sides of the counter, as it were, if you want to drive adoption.

And then trust. When it comes to sending and receiving money, trust is non-negotiable. Wero and other solutions like it must be really secure, have robust fraud prevention, and partner with regulators to ensure compliance. When consumers and businesses feel confident, they’ll naturally shift to these modern, local payment methods.

The final piece is education and awareness. A lot of consumers, especially in places like the UK and the US, stick to cards out of habit. If it’s familiar and it works, why change right? That being said, in the last year we’ve seen a huge shift in payment habits and greater awareness and adoption of alternatives. Research by Juniper reveals that 60% of all ecommerce transactions will happen via local payment methods by 2028. To put that into context, it’s equivalent to $7 billion a year flowing through hundreds of different payment methods and away from the legacy card networks. Merchants and payment providers need to highlight the benefits of solutions like Wero—whether it’s lower fees, faster transactions, or better alignment with local preferences.

You have just concluded your first year as CEO of Boku. What are your biggest takeaways from the first year and what are you hoping for in 2025?

Neal: It’s been a whirlwind year for sure. I’m very proud of the progress we’ve made, which has been underpinned by the demand for more convenient payment solutions from consumers. From where we were at the start of 2024, we’ve positioned ourselves as one of the world’s largest and most innovative global networks for Local Payment Methods with significant expansion in key global markets and more significant launches planned for this year.

I think my biggest takeaways would be the size of the opportunity for LPMs and the interwoven nature of the industry. Collaboration is so important, between merchants, PSPs, local payment providers, and indeed consumers. All of these need to be on the same page for digital commerce to flow smoothly, which is why the breadth and depth of our network is so important.

Looking ahead to 2025, ecommerce is going to continue to grow as you’d expect. Research that we’ve commissioned actually estimates that the industry will reach an astonishing $10.6 trillion in value by 2028 (from $5.75 trillion today). Local payment methods are no longer an alternative, they are mainstream. For my part, and for Boku, our focus will be on continuing to innovate and scale our offering across Europe, APAC, Africa and Middle East, as well as some exciting planned launches for Latin America, all as part of our push and our mission to give people the freedom to buy what they want, the way they want.

Here is our look at fintech innovation around the world.

Central and Southern Asia

Indian B2B Software-as-a-Service (SaaS) company Perfios acquired financial crime detection and risk management platform Claris5.

Pakistan fintech ABHI launched its microfinance bank.

Indian insurtech InsuranceDekho raised $70 million in a funding round co-led by existing investors including Beams Fintech Fund and Mitsubishi UFJ Financial Group (MUFG).

International enablement and payments platform Nayax announced its strategic acquisition of Brazilian digital payments firm UPPay for $5.3 million.

Chilean fintech Banca.me locked in $3 million in new funding.

Asia-Pacific

CTBC Bank Philippines turned to Hitachi Asia to upgrade its digital corporate banking platform.

inDrive partnered with Fingular to launch its inDrive.Money solutions for customers in Indonesia.

Malaysia’s central bank and finance ministry granted licenses to a pair of new digital banks: KAF Digital Berhad and YTL Digital Bank Berhad.

Sub-Saharan Africa

Flutterwave secured a payment system license from the Bank of Zambia.

The Bank of Ghana and the National Bank of Rwanda inked an MoU to provide companies with a license passporting framework and cross-border payment interoperability.

Nigerian fintech ProsperaVest EGG introduced eNsc, a stablecoin pegged 1:1 to the Nigerian Naira.

Central and Eastern Europe

Lithuanian identity verification service iDenfy announced a partnership with Highvibes to help protect artists from fraud.

Online payment and checkout solutions provider Montonio expanded its partnership with Inbank to bring BNPL and Hire Purchase options to customers in Latvia and Lithuania.

Austrian Reporting Services (AuRep) teamed up with the Nasdaq to provide regulatory reporting technology and support to companies in Austria’s financial services industry.

Middle East and Northern Africa

UAE fintech Flow48 raised $69 million in combined debt and equity funding.

Egyptian fintech Khazna secured $16 million to power its expansion into Saudi Arabia.

Sadad teamed up with Mastercard to enhance digital payments in Qatar.

A holiday-shortened week begins with news of an acquisition, a new partnership, and a new solution to enhance lender-borrower communication. Be sure to check back all week long for updates on the latest headlines in fintech.

This week we began our celebration of FinovateEurope’s earliest alums. In honor of FinovateEurope’s Alumni Alley Showcase – a new feature designed to highlight the innovations of FinovateEurope alums – we’re highlighting the companies that introduced their innovations to Finovate’s European audience more than a decade ago – and are still among the top innovators in fintech today.

Founded in 2003, Backbase has been demonstrating its fintech innovations on the Finovate stage for more than a decade. Making its Finovate debut at FinovateEurope in 2011, the company made its most recent on-stage appearance at FinovateFall in 2021, demoing the Backbase Engagement Banking Platform. In that ten years, the Amsterdam-based company was awarded Best of Show on four occasions, including three from the company’s demos at our conferences in London.

From its origins as a Bank 2.0 innovator, helping banks take advantage of the growing consumer interest in online and mobile banking, to its current incarnation as an Engagement Banking specialist, Backbase has demonstrated a consistent mission of enabling FIs to turn emerging technologies into opportunities for better customer service and engagement. The company’s official rebrand this fall only underscores much of what Backbase has been about all along.

Backbase founder and CEO introducing Backbase’s technology at FinovateEurope 2011.

“Our proven growth model has brought us to where we are today and it’s time to evolve our branding to reflect that growth,” Backbase founder and CEO Jouk Pleiter said. “Backbase is the innovation partner enabling traditional banks and credit unions to take the leap into the platform era, and we’re just getting started.”

Most recently, Backbase announced an expanded relationship with Boston, Massachusetts-based Eastern Bank ($22 billion in assets). The institution deployed Backbase-as-a-Service (BaaS) and Backbase’s Engagement Banking Platform to enable it to offer new digital banking solutions.

Boku Blossoms as Mobile Payments Boom

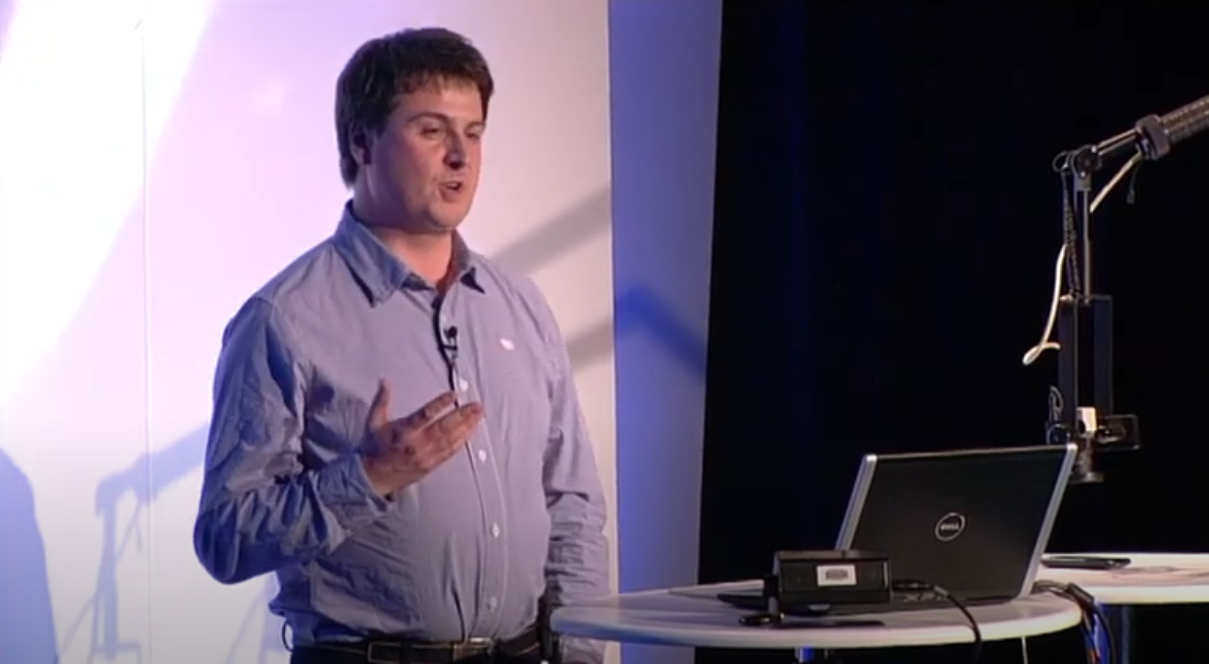

When Finovate audiences first met Boku at FinovateEurope 2011, the San Francisco-based company had 60 employees and $40 million in equity funding. Today, the direct mobile payments company is a publicly traded entity with more than 300 employees and a market capitalization of more than $390 million. Boku processes more than nine billion in payments every year, and includes some of the largest digital brands – from Google and Spotify to Netflix and Microsoft – as customers of what it bills as the largest mobile payments network in the world.

Boku founder Mark Britto demonstrating the company’s mobile payment technology at FinovateEurope 2011.

Boku was among the fintechs to recognize early on the potential mobile payments had to bring financial services to un- and underbanked consumers that owned mobile phones, but did not own credit cards or traditional bank accounts that would enable them to participate in online commerce. The company launched mobile wallet payments in the Philippines in 2012, brought mobile payments to Sony’s PlayStation Store in 2014 and, in 2020, acquired the Estonia-based carrier billing company Fortumo for $41 million.

This fall, Boku announced that it will supply Amazon.com with its digital wallet and other local payment methods as part of a new, multi-year agreement. Boku CEO Jon Prideaux said that the partnership helped reinforce the company’s “strategic move” into digital wallet payments.

SecureKey: Acquisition As An Enabler of Further, Faster Innovation

More than ten years after SecureKey won Best of Show at FinovateEurope 2011 for its authentication technology that leveraged contactless cards to streamline the online checkout process, the Toronto, Ontario-based company announced that it had agreed to be acquired by NortonLifeLock’s digital security and privacy firm, Avast.

SecureKey CEO Greg Wolfond demoing the company’s technology at FinovateEurope in 2011.

“SecureKey’s vision has been to revolutionize the way consumers and organizations approach identity and the sharing of personal information in the digital age,” SecureKey CEO Greg Wolfond said when the acquisition was announced this spring. “By working closely with governments, financial institutions, and businesses, we have an established track record of trusted and mature identity networks that provide consumers with the secure digital capabilities they deserve.”

SecureKey’s digital identity technology enables more than 200 million secure transactions a year internationally. Prior to the acquisition, SecureKey also had made major inroads in helping organizations and institutions, including governments, embrace modern authentication technologies. The company’s Verified.Me distributed digital identity verification network and Government Sign-In by Verified.Me provide secure and convenient login options to hundreds of government services and applications online. Both authentication services are provided by Interac under an exclusive Canadian licensing agreement.

Mobile payments company Boku has sold its Mobile Identity unit to cloud communications firm Twilio.

Twilio will leverage the technology to create new packages in its Lookup API and Verify API offerings.

Terms of the deal were not disclosed.

Mobile payments company Bokuannounced it has sold its Mobile Identity unit to cloud communication company Twilio. Financial terms of the deal were not disclosed.

Twilio says the purchase is a reflection of its commitment to accelerate its vision for seamless mobile identity and digital intelligence. “Twilio and Boku Mobile Identity share a common goal– building a seamless consumer identity solution that doesn’t sacrifice user experience for security,” said Twilio’s General Manager of Account Security Aaron Goldsmid.

Boku’s Mobile Identity unit verifies customer data in real time using its database of mobile network operator identity connections. Ultimately, the tool helps business customers verify client data in real time, providing a smooth onboarding experience for their end users while mitigating fraud.

San Francisco-based Twilio said it will leverage Boku’s mobile identity technology to create new packages in its Lookup API and Verify API products. The company also plans to build on Boku Mobile Identity’s comprehensive mobile identity network to improve its existing security offerings.

Founded in 2008, Twilio seeks to reinvent how companies engage with their customers by digitizing communication channels via its APIs. The companies tools– which target voice, text, chat, video, and email– do everything from helping companies connect IoT devices to cellular networks to building real-time video applications.

Boku, which offers solutions that help deliver mobile payments, was founded in 2008. Last summer, the company launchedM1ST, also known as Mobile First. The new offering features 330+ mobile payment methods, including mobile wallets, direct carrier billing, and real-time payments schemes. M1ST reaches 5.7 billion mobile payment accounts across 90 countries.

Mobile payments company BOKUannounced its expansion beyond carrier billing today with the launch of M1ST, a mobile payments network.

M1ST, also known as Mobile First, features 330+ mobile payment methods, including mobile wallets, direct carrier billing, and real-time payments schemes. The payment methods reach 5.7 billion mobile payment accounts across 90 countries.

“Today, we’re launching the M1ST Network to enable global merchants to acquire, monetize, and retain mobile-first consumers,” said BOKU CEO Jon Prideaux. “For merchants to capitalize on the massive potential of mobile-first consumers, they need to accept the payment methods they have and prefer, which are increasingly behind glass screens, not rectangular pieces of plastic.”

The new network, which runs via a single integration, is a solution for the currently fragmented mobile payments space. The technology circumvents many hurdles that come with with payments, including the myriad of tax and legal regulations associated with different geographies.

With M1ST, merchants receive a single, global settlement which eliminates the complexity of local taxes, foreign exchange, and cash repatriation. Additionally, BOKU’s payment licenses enable merchants to accept regulated payments in nearly 50 countries.

BOKU’s new launch comes at a good time in the payments space. As consumers continue transitioning to digital banking and transaction methods, many are becoming increasingly comfortable with digital payments via mobile wallets.

Founded in 2008, BOKU offers digital customer acquisition, customer onboarding, and mobile user authentication tools. The San Francisco-based company currently serves more than 600 global merchant partners and processes $9 billion in payments every year.

As Finovate goes increasingly global, so does our coverage of financial technology. Finovate Global: Fintech News from Around the World is our weekly look at fintech innovation in developing economies in Asia, Africa, the Middle East, Latin America, and Central and Eastern Europe.

Central and Eastern Europe

FintechOS of Romania raises $1.23 million (€1.1 million) in post-seed funding.

Elvira Nabiullina, head of the Central Bank of Russia, talks about the state of Russian fintech.

Lithuania’s Evarest to launch a stock trading app in the second half of the year.

Enveillaunches its enhanced ZeroReveal 2.0 data-in-use security solution.

Bokuintegrates with digital payments solution Grab in order to expand payment options in Southeast Asia.

Equifax Canada announces partnership with SecureKeyTechnologies.

Artivesttaps Paul Nobile as its new Chief Marketing Officer.

Lattice80 interviews Ashish Gadnis, Co-Founder and CEO of BanQu.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

Carrier billing company Boku is set to expand its expertise with a new acquisition this week. The San Francisco-based company agreed to acquire mobile identification and authentication company Danal for up to $68 million. The acquisition is expected to close December 31, 2018.

The deal is being structured as a reverse triangular merger to ensure Boku acquires 100% of Danal, a subsidiary of DFS Services. To finance the acquisition, Boku is issuing 26.7 million common shares for $0.0001 each, $3 million in Boku warrants, and $1 million in cash. In addition, Boku will pay deferred consideration of up to $64 million, the exact amount dependent on Danal’s future performance.

Leveraging its connections to MNOs, Danal offers data matching, account baselining, phone identification, and proactive monitoring to verify users’ identities for verticals including banks, healthcare, hospitality, and ecommerce. The San Jose-based company also offers solutions to satisfy Know Your Customer (KYC) and Telephone Consumer Protection Act (TCPA) regulations. Some of Danal’s customers include Western Union, BNP Paribas, PayPal, Square, Moneygram, Login.gov, and USAA. The privately-held company has raised $14.5 million.

Boku will leverage Danal’s technology to offer mobile identity services to its existing customers and to provide global coverage to Danal’s U.S. customers. “Combining Danal’s customer base and technology with Boku’s international scale and global MNO connection capability, will allow us to build the world leader in this emerging space,” said Boku CEO Jon Prideaux. “This acquisition allows us to offer services that go further and to improve user quality for our customers while at the same time improving the mobile experience for users… Danal has shown that MNO data can also combat fraud, reduce friction in signup and ensure regulatory compliance on mobile.”

Boku was founded in 2008 and provides payments technology that allows consumers to charge purchases to their mobile phone bill. The company offers its operator network for acquiring, activating, and monetizing customers through their mobile phones. The Boku platform is used in large digital marketplaces such as the Google Play store, Apple’s App store, Spotify, and Facebook’s App Center.

At FinovateEurope 2011 Boku showcased its mobile payment service. Earlier this fall, Boku was awardedBest Newcomer at the AIM Awards. Boku is publicly traded on the London stock exchange with a current market capitalization of $124 million.

Coinbasecontinues to explore support for new digital assets.

The city of Rye, NY partners with Passport to manage parking.

Mortgage Cadenceintegrates Radian’s mortgage insurance service into its Enterprise Lending Center solution.

The CX Show interviewsSaleMove co-founder and CEO Dan Michaeli about creating contact center leaders.

TechCrunch interviewsTransferwise cofounder and CEO Kristo Käärman on growing money transfers despite global turbulence.

Pendo Systemspartners with Azimuth GRC and Global Comply.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

Carrier billing company BOKUplans to go public on the London Stock Exchange’s alternative investment market (AIM), an international market for smaller growing companies. Ahead of next week’s public debut, the company announced it expects to raise $60 million on a post-money valuation of $164 million.

Of the $60 million, $39.5 million will be distributed to individual investors. The company will reinvest $20 million to promote growth activities, such as bolstering its efforts in India and increasing partnerships with carriers.

BOKU was founded in 2008 and provides payments technology that allows consumers to charge purchases to their mobile phone bill. The company offers its operator network for acquiring, activating, and monetizing customers through their mobile phones. The BOKU platform is used in large digital marketplaces such as the Google Play store, Apple’s App store, Spotify, and Facebook’s App Center.

BOKU has raised a total of $91 million from investors such as Andreessen Horowitz, Benchmark, Index Ventures, Khosla, NEA and Telefonica. At FinovateEurope 2011 the company showcased its mobile payment service. Earlier this fall, BOKU inked a partnership with ALTBalaji, the largest digital platform for exclusive and original shows from India, to allow its clients to pay their bill through their mobile carrier. A few months prior, the San Francisco-based company added three new geographies to its partnership with Spotify, enabling consumers in France, Australia, and Malaysia to pay their subscription via carrier billing.