This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Earlier this year banking technology company PlaidlaunchedPlaid Exchange, a new tool to facilitate open banking.

The new open finance platform offers banks a way to provide open banking connectivity to their clients while keeping their end customers’ data safe and giving them control of their data.

Plaid Exchange helps banks establish token-based API connectivity with the 2,600 third party apps in Plaid’s network. This single connection simplifies integration for banks, helping their clients connect with more third party providers securely. Plaid Exchange can help banks bring an API solution to market in 12 weeks.

A couple of weeks back, Plaid formed a key partnership to help it reach more banks to access the Plaid network. The company is working with Jack Henry & Associates to enable Plaid Exchange for banks on the Banno Digital Platform.

The deal helps Plaid reach more than 350 institutions currently using Jack Henry’s Banno Digital Platform. These financial institutions can benefit by offering their accountholders access to Plaid-powered fintech apps. Plaid has designed the integration process to be simple and Banno clients will be able to access the technology for free.

The deal with Jack Henry comes as an extension of the Plaid Exchange Partner Program, which is aimed to get banking platform providers, API management platforms, and software development companies on board to offer Plaid Exchange to their bank clients.

The network effects of the Plaid Exchange Partner Program will be a boon to the San Francisco-based company. That’s because the more banks Plaid partners with, the more attractive Plaid is to fintechs.

Plaid works with thousands of third-party fintech apps such as Transferwise, Betterment, and Venmo to connect with their users’ financial institutions. The company made headlines at the beginning of 2020 after it announced it had been acquired by Visa for $5.3 billion and made the news again after the U.S. Department of Justice filed a suit to block the acquisition last month.

Branded payments firm Blackhawk Network has always been busy over the holiday season. Between its gift cards, digital rewards, and prepaid cards, the California-based company has helped people embrace the spirit of giving.

And while Blackhawk Network is still helping fuel the gifting and rewards economy this year, it is moving to an even more 2020-friendly (that is to say, digital-first) approach.

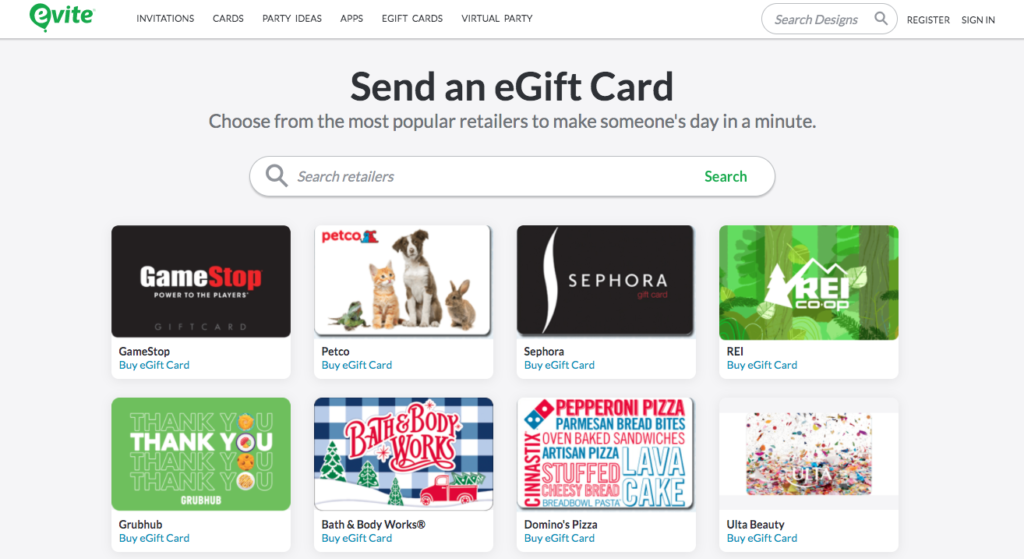

Last week Blackhawk announced it has teamed up with Evite to power the digital greeting card and invitation company’s eGift card program. Evite users can now choose from more than 100 eGift card options from popular brands including Lowe’s, Red Lobster, and Old Navy.

“It’s no surprise we’ve seen the demand for virtual gifts and greetings skyrocket in 2020. Contactless gifting is now a must-have, especially with the holidays approaching,” said Evite CEO Victor Cho. “Adding an extra touch like an eGift card can help people create personal connections with family and friends that they haven’t been able to see. It also helps our users stay safe, creates maximum flexibility for gifters and receivers, and modernizes the 2020 gifting experience. Thanks to Blackhawk’s expansive network of eGift card choices, our users have a broad selection to choose from at the tip of their fingertips.”

Brett Narlinger, head of global commerce at Blackhawk Network, noted that Blackhawk has seen a 70% increase in eGift sales– all before the peak holiday shopping season.

In addition to its partnership with Evite, Blackhawk announced a new payment solutions suite called Pay4It that connects physical and digital payments. The suite helps merchants reach underbanked populations with the ability to add cash to a digital wallet, mobile app or account, or make payments for digital goods with cash. It also offers consumers more choices to pay by enabling additional digital wallets and transforming loyalty points and rewards into purchasing power. Finally, Pay4It brings the gift card mall to non-traditional locations and into the digital realm.

“Retailers’ and merchants’ businesses changed instantly this year, and Blackhawk has responded with a product suite that brings once-disparate physical, digital and stored value payments together, keeping brands and consumers connected in a seamless way,” said VP of Global Product Strategy at Blackhawk Network Helena Mao.

An alum of FinovateFall 2012, Blackhawk Network was founded in 2001 and was acquired in January of 2018 by Silver Lake and P2 Capital Partners in a deal worth $3.5 billion. The company works with more than 1,000 brands and card partners, is in more than 200,000 retail locations in 28 countries, and connects with more than 300,000,000 shoppers each week. Talbott Roche is CEO.

A turnkey digital bank-in-a-box that can be deployed in as little as 30 days? That’s the product of a new partnership announced this week between a pair of Finovate alums: data-driven financial wellness innovator Moven and digital banking services provider Q2.

“Working with Q2 allows banks of all sizes to accelerate their consumer facing digital offering,” Moven CEO and CRO Kesh Talwar explained. “Having a complete view of customer financial behavior, along with Moven’s data analytics, will increase contextual customer engagement. He added that better customer engagement will lead to “lower attrition rates, increased revenues and acquiring new customers digitally at a lower cost.”

Initially, the collaboration will focus on the integration of Moven’s data aggregation and savings tools with Q2’s cloud-based core processor, CorePro. This will enable them to offer banks and credit unions an instant deployment solution with real-time alerts and notifications, as well as account issuance for savings and demand deposits accounts. The offering also includes features such as instant external account verification, wishlist savings, and an emergency account.

“We are thrilled that Q2’s CorePro system was selected by Moven to power this initiative,” GM of Q2 BaaS Paul Walker said. “Now any bank can have its own Marcus or Chime in a matter of a few weeks.”

The partnership is the latest evidence of Moven’s shift toward leveraging its financial wellness and behavioral data technology and away from the direct to consumer / neobank model of years past. Fintech expert and advisor Bryan Clagett, who approached both Moven and Q2 over the summer to discuss compatibilities between the two firms, underscored the importance of this strategy. “Digital banking, as we know it, is evolving quickly,” he said “and bringing together fintechs organizations that have complementary competencies is key to the future of the financial services industry.”

Founded in 2011 and becoming a Finovate alum after its debut at FinovateEurope two years later, Moven announced a partnership with Saudi Arabia’s STC Pay this spring. The New York-based company has raised more than $47 million in funding, and includes TD Bank and SBI Group among its investors. Brett King is founder and executive chairman. In a statement, King highlighted the significance of his company’s partnership with fellow Finovate alum, Q2.

“We started as a challenger bank in the U.S. market before collaborating with banks and FIs around the world, so we understand what it takes in the post-COVID digital world to stand out,” King said. “The Q2 alliance is our first major core partnership in the U.S., and no doubt will set a steep benchmark for other providers in the space.”

Headquartered in Austin, Texas, Q2 has become one of the leaders in the embedded finance movement, offering a range of digital financial solutions for consumers, business clients, and fellow fintechs. The company won a Best of Show award at FinovateFall in September for its Partner Marketplace, an app store that is integrated within the client’s digital banking platform.

Q2 is publicly traded on the New York Stock Exchange under the ticker QTWO, and has a market capitalization of more than $5 billion. See them next week as the company returns to the Finovate stage to demo its latest technology at FinovateWest Digital.

Identity verification and authentication provider Onfido has provided a guiding light when it comes to digital identity in 2020 and the company’s Q3 sales results can back it up.

Onfido’s global sales increased 82% over the course of the third quarter. The company also doubled the number of sales from its 103 new clients. Overall, Onfido saw a 237% increase in U.S. sales during the third quarter and attributes the growth to new customers switching from other providers.

Aiding Onfido’s success is its decision to partner with Identity Access Management (IAM) companies to spur demand for enterprise-level customers. Some of the company’s marketing plays in this area include hosting an e-voting roundtable with Okta, integrating into Auth0’s Marketplace, and listing on the Salesforce AppExchange.

Additional key partnerships for Onfido this year include:

Alior Bank partnered with Onfido to power digital onboarding.

Hub City Media partnered with Onfido to resell and distribute Onfido’s identity verification and authentication services.

Deliveroo expanded its partnership with Onfido to accelerate its onboarding process for drivers.

Curve partnered with Onfido to enhance its Digital Identity and Know Your Customer (KYC) processes.

SwissBorg partnered with Onfido to provide a compliant customer onboarding experience.

Delfin Health partnered with Onfido on its app that predicts, monitors, and tests the health and safety of workforces.

MyCash partnered with Onfido to power digital onboarding.

Bondora partnered with Onfido to streamline its onboarding and KYC processes.

Voima Gold partnered with Onfido to allow customers to securely buy, sell, and store physical gold.

EstateGuru partnered with Onfido to automate KYC and AML compliance processes.

Onfido leverages the power of machine learning and AI to help companies cross-verify users’ identity documents with a live biometric of their face. The company can verify more than 4,600 document types from 195 countries.

“Our mission is to create a more open world, where identity is the key to access. This starts with widening access, creating opportunities for everyone to connect with the services they need and making sure that it’s as inclusive as it can be,” said Husayn Kassai, CEO and Co-founder of Onfido. “We made significant strides over the last quarter to make our product offering not only more conducive to enterprise-level organizations, but also fairer when it comes to verifying people from different ethnicities. We believe these changes will only accelerate our growth further.”

Onfido most recently showcased its technology at FinovateFall 2018, where it debutedFacial Check with Video. The tool, available via an SDK, prompts users to film themselves repeating numbers and performing randomized movements to ensure liveness and enhance identity verification.

Even before the onset of the global health crisis, banks and other financial services companies were moving in the direction of greater digitization to improve efficiency, cut costs, and most importantly, deliver new and enhanced products and services to an increasingly-tech savvy – and tech-dependent – consumer.

But do firms in the financial services space need to do more than just digitally transform themselves? What strategies do these businesses need to adopt in order to further differentiate their offerings from rivals? How can they provide their customers with the kind of personalized, low- to no-latency, access anywhere, digitally-oriented service their customers have come to expect from all institutions – public or private, large or small, financial or not?

For this week’s Finovate Alumni Profile, we caught up with Stanley Huang, Chief Technology Officer for Moxtra, to discuss these challenges. Specifically, we talk about what he calls the “marketing mindset” that financial services businesses need to adopt in order to not just survive, but thrive in these uncertain times. A leading business collaboration platform designed for the mobile era, Moxtra offers an embeddable omni-channel client engagement solution for financial services companies. The company, founded in 2012 and headquartered in Cupertino, California, has been a Finovate alum since 2016.

Finovate: Digital transformation is the major buzzword for companies right now – understandably. However, would you say that there is more to making it through the current crisis – to say nothing of coming out better on the other side – than just digital transformation? What else do companies need to do?

Stanley Huang: Digital transformation is inevitable but it’s more about the overall industry transformation that needs to take place, especially in an industry like finance and banking which has been slower to adopt more modern, digital solutions. We encourage our customers to leverage this crisis in order to finish the long-term business service model transformation. It’s like shifting from using taxis to Uber.

Consumers have grown accustomed to and reliant on mobile in their interactions with businesses for more than a decade now, and that has raised customer expectations of all businesses fundamentally. It’s simply the reality, and it’s time for laggards to embrace that reality. In order to compete today, you need to place a premium on providing on-demand service with instant response and serving every client as a high-touch customer. The mobile era has created a level of service that customers are accustomed to – so getting ahead of the expectations and needs of customers is vital to better ensure loyalty during the entirety of the customer lifecycle, which in the financial industry is a lifetime if done right.

The silver lining of seemingly being forced into digital transformation during this unique time is that it’s serving to benefit not just some, but all customers in this time capsule we’re experiencing. Now is the time to ensure that no age demographic is left behind in the pursuit of digital adoption, for example. For financial institutions that previously didn’t have something like a OneStop Customer Portal to serve customers virtually, that was a missed opportunity to attract the younger generations who have grown up with mobile and digital solutions as an expectation, not a luxury.

And for financial institutions that had a digital solution headed into the pandemic, this period of time serves as a unique environment to bring older generations into the fold that previously may have been hesitant to do business virtually. Show them what they can do — safely — both physically and from a cybersecurity standpoint, with a OneStop Portal solution. Ensuring they feel comfortable to be served via this new channel with both a secure and user-friendly interface will make them a lifelong virtual banker, benefiting both parties long term.

Finovate: You’ve discussed a concept called a “marketing mindset” that you think more businesses need to adopt in order to survive and thrive in the current environment and beyond. What is a marketing mindset? Why do companies need it and how do they get it if they don’t have it? How did you come to this insight?

Huang: When we talk about doing business with a marketing mindset, it goes back to the shift in importance to how you provide service vs. what you offer – it’s evolving from a “product mindset” to a “marketing mindset”. By that, we mean creating a customer experience that is centered around brand consciousness. Marketers are naturally focused on this concept of brand consciousness in their role as they own the responsibility of overseeing the execution of how the brand is presented to customers as well as the messaging that is circulated. Oftentimes, banks aren’t as self-aware of their brand identity when interacting with customers on a day-to-day basis as they really should be.

Banks must have a marketing and customer-centric mindset to succeed in a digital age that has heightened consumer expectations for the type of experience they expect to receive, especially by an institution that is responsible for something so personal and important to them as managing their money.

When customers have other options for who they bank with, financial leaders — no matter their role — should consider leading with a marketing and customer-centric mindset to appeal to and retain customers. If this frame of mind and way of doing business isn’t innate within the company, it is up to bank employees to educate and promote the benefits of this new approach to banking. Especially during the early adoption phase of digital banking, a thought-out, handshake-replacing approach to doing business digitally is what will help banks gain customer confidence and trust to earn their loyalty long-term. If approached with a marketing mindset, your advocacy and education about this new approach to doing business will aid in customer adoption, comfort and, ultimately, loyalty.

Finovate: What industries or companies are doing the best job of embracing this mindset? Is there a reason why these businesses are better able to adopt a marketing mindset compared to other businesses/industries?

Huang: Industries embracing this mindset best are those that have the greatest reputations to uphold in comparison to other top-notch brand experiences, such as in retail and CPG (consumer packaged goods). While antiquated government institutions and utility companies can coast by with a lower caliber of service, retail and CPG brands can’t afford to slip up on the customer experience advertised — especially with all of the options available to consumers and the likes of Amazon coming for their customers.

That’s why retail banks serving your everyday consumer such as Citibank came to us to ensure the experience it offers its customers is thoughtful, thorough and robust to match their in-person banking experience, and in some ways surpass it with on-demand relationship managers.

High-touch businesses like Citibank are our sweet spot of service, because their OneStop Digital Branch requires comprehensive, collaborative capabilities — both on the front end and back end — that can manage a more complex level of services than a simple e-commerce site or app by a retailer needs. Banks need capabilities like secure messaging, digital signature, and a seamless tracking of finances, transactions, and banking communications in real-time.

High-touch businesses, such as those in the financial industry, law, real estate, education, event planning, etc. are the type of companies and organizations that may be slight laggards with digital transformation not because they don’t value their customers, students and other stakeholders, but because ten years ago the technology wasn’t out there to facilitate the complex facets of their business virtually in the way that a simple online clothing retail operation can pull off. We are working to fill that need at Moxtra with our Digital Branch Solution.

In today’s era of embedded finance, everything is available as a service. Digital banking services company Q2 is at the leading edge of this trend, offering a range of solutions for banks’ retail clients, their commercial customers, and fintechs.

Many fintechs sell an “as-a-service” offering that focuses on a single aspect of banking. Q2, however, takes a more holistic approach. Here’s a look at some of the company’s embeddable offerings.

Q2’s consumer solutions include remote onboarding, PFM tools, remote deposit check capture, lending tools, marketing offers, behavioral biometrics, and authentication. The company helps banks leverage client data using machine learning technology that brings the necessary intelligence to effectively market new products to customers.

On the commercial side of things, Q2 can aid with account opening, loan origination, ERP integration, and scalable tools to suit a range of business sizes.

Q2 offers fintechs both lending-as-a-service and banking-as-a-service tools to integrate into their existing offerings. The former focuses on the application, approval process, and loan funding, while the latter offers bank accounts, debit cards and payment solutions without the need to partner directly with a traditional bank.

In addition to these embedded finance offerings, Q2 is venturing into the bank-fintech collaboration space. In a Best of Show winning demo at FinovateFall last month, Q2 launched its Partner Marketplace, an app store integrated within the company’s digital banking platform. Fintechs can upload their tools on the platform’s app store and banks can browse the offerings they’d like to integrate.

By relying on fintechs to bring the tech, the Partner Marketplace broadens Q2’s reach as a provider of embedded finance. The company offers banks access to a variety of fintech solutions that range beyond what Q2 itself is able to create or provide.

For fintechs, the marketplace lowers customer acquisition costs by making the startups’ solutions visible to Q2’s network of bank partners on the platform. It also helps with integration and deployment– after integrating with Q2’s digital banking platform, fintechs can offer their product to 400+ banks and credit unions, one million businesses, and 16+ million end users.

The big changes we are seeing in the realm of customer engagement have to do with inevitable trends becoming immediate demands. Whether the need is reaching customers over the digital channel for the first time or automating and streamlining processes to improve efficiency and maximize productivity, the global health pandemic has been the midwife – if not the mother – of the fast-changing technology landscape we live in today.

“Meeting customers where they are” has been a rallying cry for customer engagement specialists for years. And as the number of channels grows, more companies are offering new solutions that provide easy-to-use, secure, and compliant ways for businesses to more comprehensively engage with their customers and clients.

One company in this space is Revation Systems. A Minneapolis, Minnesota-based firm, founded in 2003, Revation recently partnered with fintech and regtech solution provider Computer Services Inc. (CSI), who will offer Revation’s LinkLive Banking platform to community banks. LinkLive Banking provides regional and community banks, as well as credit unions, with key capabilities such as digital messaging, AI-powered chatbots, voice and video communications, and the ability to move seamlessly between physical and digital channels.

“Given the remote work demands of COVID-19, LinkLive Banking empowers our banks to provide a world-class customer experience while taking precautions to protect the health and safety of their employees and customers,” CSI Group President of Enterprise Banking Giovanni Mastronardi said. “Together with Revation Systems, we’re providing the innovative technology necessary to increase customer satisfaction and reduce friction in the customer journey.”

In addition to its messaging, chatbot, voice, and video functionalities, the platform also provides secure desktop sharing and encrypted email. LinkLive Banking leverages AI to power service chatbots with keyword recognition and the ability provide fast, automated responses to common banking queries. The video banking capabilities, announced in August, are the most recent addition to the platform.

“We are extremely excited about utilizing LinkLive’s video banking features as we seek to improve our member experience,” United Educators Credit Union CTO Dennis Griesgraber said. He noted that the new feature integrated not only with the LinkLive contact center the credit union used, but also with the institution’s digital banking platform. John Eyre, Assistant VP of Information Technology at TAPCO Credit Union underscored the technology’s value for enhancing communications among employees, as well. “LinkLive’s video banking feature will not only enhance the interactions between our members and representatives, but will also help improve communication among our own staff internally,” Eyre said.

Active in the healthcare vertical as well as financial services, Revation has more than 400 customers using its LinkLive Banking platform, representing more than 100 million digital banking customers. Adding the video banking component, Revation notes, requires only a few configuration changes to the LinkLive platform, and does not require the customer to download an app or manage a separate communications account to participate in video banking.

Perry Price, Revation CEO, echoed the now-common wisdom that the pandemic has accelerated pre-existing, if not inevitable technology trends. He noted that while adoption of video banking before COVID-19 had been a “long-term goal,” the onset of the crisis had turned those goals into “urgent” priorities.

Featured in CIOReview’s Most Promising FinTech Solution Providers for 2020 this spring, Revation is scheduled to make its Finovate debut next month at FinovateWest Digital. To learn more about our upcoming, all-digital event and how to watch Revation’s technology in action, visit our FinovateWest Digital hub.

While many fintechs were working on digital transformation, Linqto was focused on complete transformation. That’s because the San Francisco-based company recently made a major pivot.

Linqto was founded in 2010 as a digital banking technology company that provided software-as-a-service to fintechs. Perhaps most notable during the company’s first few years of operation was the launch of its Otter API which, along with a partnership with LEVERAGE, powered Linqto’s App Store for Banks, a marketplace where banks could select from new apps to brand them as their own and launch them in app stores for their end customers to download.

“By working with Linqto, credit unions are still able to offer their traditional services, but now they can also pair those services with premium technology from branded apps, enhancing mobile strategies and changing their members’ mobile experience,” said LEVERAGE President and CEO Patrick La Pine when the deal was announced in 2016. “This brings a dramatic shift in the relationship members have with their credit union and their mobile devices.”

Fast forward two years and Linqto had raised $1.6 million in two funding rounds and transformed itself into an investment service with its Global Investor Platform. Key to this transition, the company acquired investment trading platform PrimaryMarkets for $33 million in December 2018.

“Linqto is acquiring PrimaryMarkets, an established global trading platform, to launch its platform as part of the Global Investor Platform,” said Linqto Founder and CEO Bill Sarris. “The Takeover will allow the establishment of an inclusive trading platform and the capability for the Linqto Platform to broaden our revenue model from a strictly SaaS model to a transaction-based model, whereby Linqto will share in commissions and broker fees realized by the Platform.”

PrimaryMarkets a global online marketplace that enables users to conduct secondary trading of existing securities and investments, manage secondary securities trading on behalf of companies, and assist unlisted companies in raising new funds.

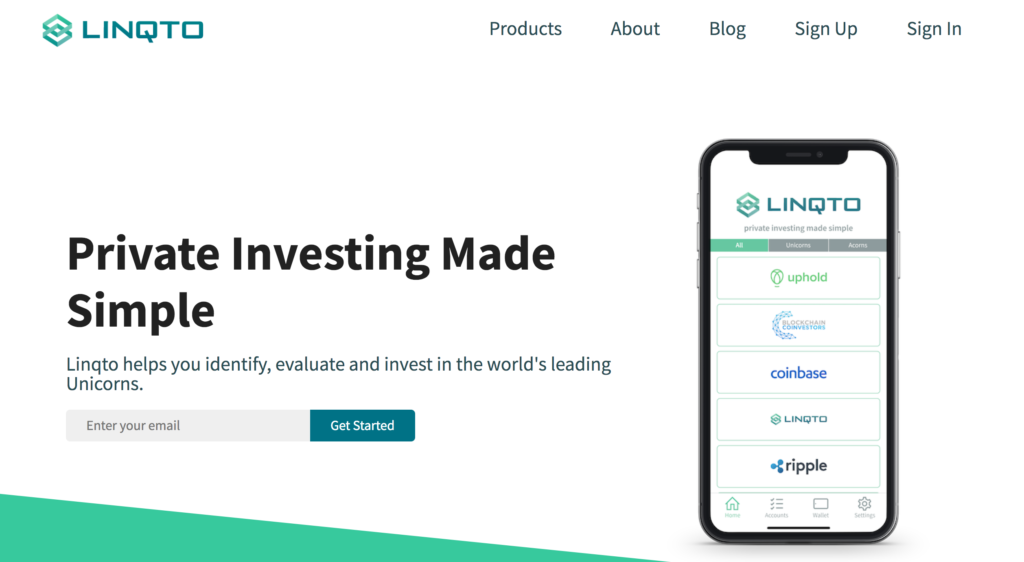

In February of this year, while the world’s attention was consumed with the threat of the then-epidemic-now-pandemic coronavirus, Linqto announcedEquity in Unicorns, a new investing platform for private securities. Equity in Unicorns is designed to help accredited investors invest in the private market via a simple, quick, and relatively inexpensive platform.

“Small Accredited Investors now have the opportunity to participate in the growth and superior returns of private markets, as large institutional investors have done over the past 30 years,” said Sarris. “Private investing made simple.”

Since its pivot, Linqto now counts more than 100,000 accredited investors in its global network. Currently, Linqto allows these users to invest in a range of pre-IPO startups, including Upgrade, Uphold, Ripple, SoFi, Blockchain Coinvestors, Kraken, and even in its own company.

Linqto was slated to debut its new platform at FinovateSpring earlier this year. However– thanks to COVID– the conference, along with Linqto’s demo, will be featured at FinovateWest on November 23 through 25.

One of my favorite sayings popularized by the current Democratic Party candidate for president is “don’t tell me your values. Show me your budget.” The implication is that, at the end of the day, talk is cheap. Show me how you actually spend your money, and I’ll learn all I need to know about what matters to you and what does not.

By that metric, the news that Dutch fintech and Finovate alum Ohpen has acquired Saas-based, crossborder mortgagetech Davinci tells us quite a bit about what what the Amsterdam-based cloud core banking engine maker thinks about the importance of expanding beyond its competencies in savings, investments, loans, and current account products.

“We are a growing company with huge ambitions,” Ohpen CEO Matthijs Aler said. “Together, we intend to lead the charge in directly challenging incumbent providers with outdated technology. Our mission is – and always has been – to set financial institutions free from legacy software. Now we can help a broader range of financial institutions deliver tangible change to meet the needs of tomorrow’s customers.”

Ohpen put the acquisition announcement in the context of its global growth strategy. This includes scaling operations in the Netherlands – where the company is a market leader – the United Kingdom, and Belgium initially, as well as expansion to other areas. Ohpen also plans to scale up its development centers in Spain and Slovakia.

The terms of the acquisition were not disclosed, but the combined entity will have 350 employees and $35 million in revenue. Davinci is Ohpen’s second acquisition. The company purchased core banking system implementation consultancy FYNN Advice in the fall of 2017.

Davinci leverages machine learning and AI to enhance and accelerate digital onboarding and acceptance during the mortgage lending process. Delivering cost savings of as much as 80%, the company’s signature solution is Close, a cloud-native platform for mortgage loan origination and servicing.

Calling the acquisition, “the natural next step” for both companies, Davinci Director Alwin van Dijk said, “We are the only two players with a real focus on back and middle office innovation for new and existing propositions.” van Dijk added that the ability to offer a broader range of products will be a “market game changer.”

With $47 million (€40 million) in funding from investors including NPM Capital and Amerborgh, Ohpen began the year teaming up with pensions administrator TKP Pensioen. The partnership with the Groningen, Netherlands-based digital pension platform enabled Ohpen to enter the pension market for the first time. Aler pointed out that the integration would enable the “originally conservative industry” of pension management to have a “fully digital and futureproof pension solution at its disposal.” This spring, Ohpen partnered with another pension management firm, Ortec Finance, integrating the company’s forecasting engine with the Ohpen platform.

If the future is digital –which it is– then the future must also be in real time. And while our industry typically thinks about real-time in terms of payments, there’s one fintech that’s working to bring information into the real time realm.

Banking technology company Plaid is launching instant account activity today. The new release allows financial institutions on Plaid Exchange to send user-permissioned transactions data to Plaid developers within seconds of the user’s activity. As a result, the consumer receives an up-to-date picture of their finances.

During a time when many consumers are working in the gig economy and budgeting for their expenses on a day-by-day basis, having the most recent information about their account balances is critical and could make the difference between overdrafting or staying afloat.

“Instant, real-time data has become standard for consumers today and it’s a critical piece of information that our users need to make sound financial decisions,” said Atif Siddiqi, CEO of Plaid client, Branch. “Plaid provides our users with the most current picture of their transaction history, empowering their daily financial decisions.”

Today’s development is the latest in a string of updates for Plaid, which recently launchedPlaid Exchange, an open finance solution that offers banks a way to provide open banking connectivity to their clients while keeping their clients’ data safe and giving them control of their data.

Last week, the company announced an addition to its suite of payment products with the launch of standing orders in the U.K. With standing orders, end users can make recurring payments with a single authorization for things like gym memberships and rent payments.

Plaid is an alum of Finovate’s developer conference. In 2014, the company’s CEO and co-founder, Zach Perret, showcased the Plaid API for financial institutions.

What have the companies that won Best of Show awards at last year’s FinovateFall conference been up to in the months since our New York show? With our autumn event less than a month away, we thought it would be a great time to check in on the nine companies that took home top honors this time last year.

BlytzPay – Integrated its digital payments technology with Dealer Management Systems (DMS) leader ABCoA Deal Pack. Announced strategic partnership with AFS Dealers.

Cinchy – Joined the 2020 MassChallenge FinTech Program in December 2019 along with five fellow Finovate alums. The program noted that 70% of the participants in its previous cohort launched a pilot or proof of concept within a year. Earned a $500,000 cash prize as one of the winners of the 2019 VentureClash competition. Raised $10 million in funding in May.

College Aid Pro – Partnered with Horsesmouth, a company that provides educational and marketing solutions for financial advisors and their clients. Announced collaboration with the American Institute of Certified College Financial Consultants. Teamed up with online student loan refinancing marketplace Credible.

ebankIT – Forged North American partnership with fellow Finovate alum Enterprise Engineering this spring. Announced updates to its multichannel banking platform.

Glia – Won Best of Show at FinovateEurope for a second year in a row. Integrated its technology with fellow Finovate alum Alkami’sOnline Banking Platform. Inked partnerships with 20 credit unions across the U.S.

MX – Topped 50,000 direct-to-bank API agreements to major financial institutions and fintechs. Launched data connectivity API, Path by MX. Named one of Inc. Magazine’s Best Workplaces 2020.

owl.co – Named one of Canada’s Most Innovative Tech Companies by the Canadian Innovation Exchange. Delivered $1 million in revenue within six months of launching.

Pinkaloo Technologies – Raised $1.25 million in funding. Joined Goldman Sachs-owned Ayco Marketplace for financial counseling and wellness services. Partnered with Eastern Bank to power its Give for Good charitable giving program.

Zogo Finance – Teamed up with fellow Finovate alum Bankjoy. Announced partnerships with 11 community banks and credit unions across 12 states. Surpassed 1,000,000 financial literacy modules completed.

FinovateFall Digital 2020 kicks off Monday, September 14 and continues through Friday, September 18 with hours of live and on-demand content. Visit our registration page today and join us for Finovate’s biggest, digital-first event to date.

After teasing the launch of its debit card in the U.S. earlier this year, Samsung announced that its digital debit card, the Samsung Pay Card, is now available in the U.K.

To make the launch possible, Samsung has teamed up with Curve, a fintech that consolidates all of a user’s existing Mastercard and Visa payment cards. The London-based company makes all of a user’s cards contactless and compatible with Samsung Pay.

Users will receive access to Curve features such as peer-to-peer money transfers, instant notifications about spending, competitive foreign exchange rates, 1% cash back on purchases made with a select group of three merchants, and 5% cash back on purchases made at Samsung.com. Samsung Pay Card users will also be able to use Curve’s Go Back in Time feature that allows them to switch payments from one card to another for up to 14 days after the purchase was made.

The deal is a win-win for both companies; Samsung will benefit from Curve’s e-money license with the U.K. Financial Conduct Authority, and Curve will gain from an increase in users. Interestingly, however, existing Curve users cannot also apply for a Samsung Pay card. As other sources have pointed out, the reason for this exclusion isn’t entirely clear.

“At Samsung we believe in the power of innovation and, through our partnership with Curve, the Samsung Pay Card brings a series of pioneering features that will change the way that our customers manage their spending, with their Samsung smartphone and smartwatch at the heart of it,” said Conor Pierce, Corporate VP of Samsung U.K. and Ireland. “This is the future of banking and we look forward to continuing this journey with our customers.”