It’s not easy making savings accounts sexy, but Social Money, with its GoalSaver and SmartyPig brands, is trying. The latest innovation? A Google Chrome browser extension called SmartyPig OneClick (link), that allows users to create savings goals on the fly while shopping online.

The service launched last week and can be found in the Extensions: Shopping section of the Chrome app store. The app has 30 users according to stats displayed in the store. In comparison, the most popular shopping extension, from Amazon, has more than 600,000 users.

The SmartyPig OneClick system can be licensed by banks looking to juice their savings account feature set.

How it works

1. Install from Google Play app-store (see screenshot 1 below)

1. Install from Google Play app-store (see screenshot 1 below)

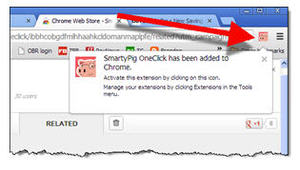

2. A SmartyPig icon is added to the upper right of the browser (see inset)

3. When shopping online (at any website), users click on the SmartyPig icon in the upper right, which launches a popup (screenshot 2)

4. After logging in (screenshot 3), users establish a goal and automatic savings plan to fund the purchase of the desired item (screenshots 4 & 5). SmartyPig automatically imports the item’s price and image and stores it for the user at SmartyPig.com.

___________________________________________________

Analysis

___________________________________________________

Goal-based savings is an important feature to add to online banking (note 1). And shopping helpers are a relatively popular browser extension (Amazon’s Chrome extension has 600,000 users). So marrying the two is an interesting play.

Will this boost savings-account balances? Perhaps a little. But the more important FI benefit is getting a branded button in the corner of the user’s browser (whether anyone will remember it’s there is another matter). That’s a bit of a Trojan Horse that can be used for a variety of services (note 2).

Bottom line: I like SmartyPig’s move. Smartphones have conditioned users to look for specialized apps. I believe consumers will use full-featured online banking via direct desktop links (see also Mint’s QuickView). Although, it will take education and marketing support.

————————-

1. Installing browser extensions is a painless process (Chrome store link)

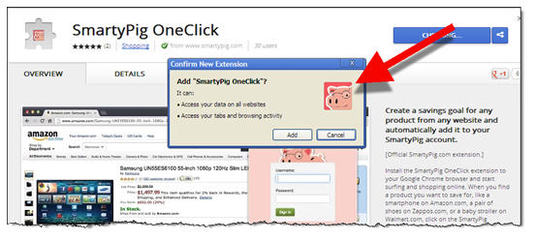

Note: Users must allow SmartyPig to “access your data on all websites” and “access your tabs and browsing activity.” The first one is likely to give users pause.

2. Creating a goal on the fly while shopping

3. Login to SmartyPig via popup box

4. Confirm the savings goal

5. Customize the savings goal

————————

Notes:

1. For more info, see our Online Banking Report (Nov. 2008, subscription) detailing various ways to leverage your online/mobile channel to boost deposits.

2. Long ago, we wrote a report (Aug 2002, subscription) on ways to put your bank onto the computer desktop. The strategy is still the same, though the specific techniques are somewhat different today.

The WSJ looks at angel investing via SecondMarket.

The WSJ looks at angel investing via SecondMarket. Source: TechCrunch

Source: TechCrunch

Major new executive-level

Major new executive-level