How important are mobile users to your sales efforts? 76% of Facebook’s ad revenue is from mobile (and it was considered by many to be a mobile laggard a few years ago).

How important are mobile users to your sales efforts? 76% of Facebook’s ad revenue is from mobile (and it was considered by many to be a mobile laggard a few years ago).

Prospective customers are already visiting your website from their smartphones in massive numbers. Are you making a good first impression? Does the UI work across key devices? And more importantly, is there an easy-to-find path to mobile purchase?

This afternoon, I visited 20 leading banking and personal finance sites (as a proxy for popularity, I used the 20 most downloaded free finance apps in the U.S. Apple App Store, see list in footnote). And it was like a trip back in time before (desktop) websites had adopted browser-design standards. By the numbers:

- Excellent: 19 of the 20 had mobile-optimized sites (Laggard = Navy Federal Credit Union)

- Satisfactory: 14 of 18 had a visible link for login (2 required a native app to login)

- Needs work: 11 of 20 had a visible link to download the native app (including the 3 below)

- Needs work: Only 3 of 20 used an initial “pop-up” screen that prompted download of the app, then the user needed to find a link to the non-app site

- Needs work: 12 of 20 made a visible attempt to sell something

- Fail: 6 of the 20 made a pretty marginal first impression, including several of the biggest financial institutions in the U.S. and the world: American Express, Chase, Citibank, Mint, PNC, Wells Fargo

My favorites (from this sample of 20, see footnote):

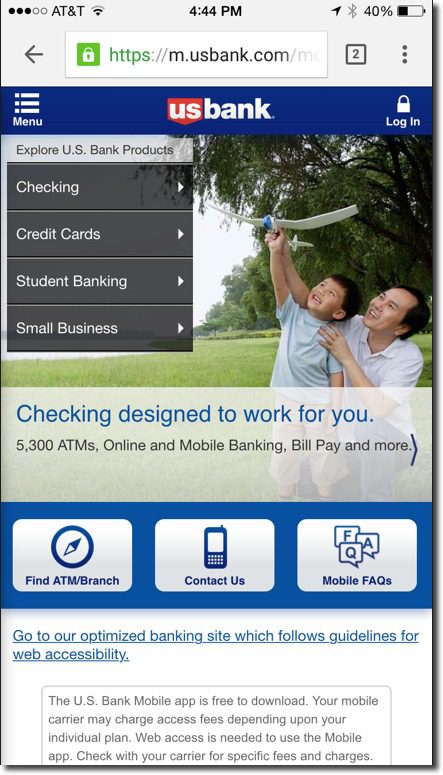

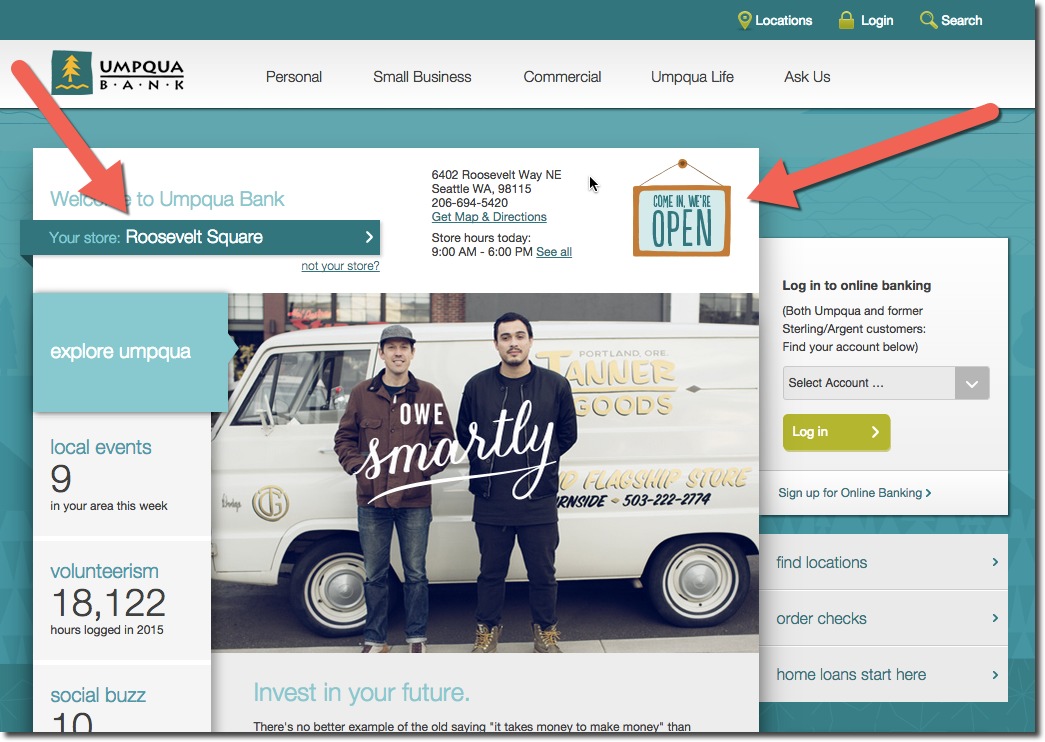

Bank: US Bank

Nice, engaging layout with clear path to more info, but missing a link to download the app

Runner-up: TD Bank

Easy-to-find customer service, login, location, but missing app-link

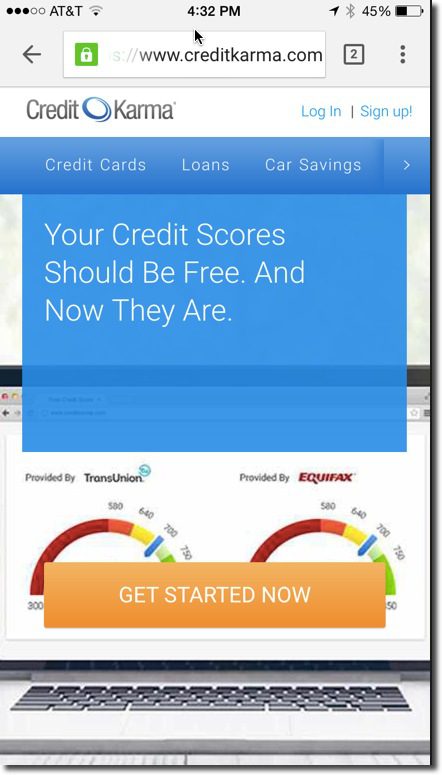

Favorite non-bank: Credit Karma

Good branding, clear get-started button, but no link to native app

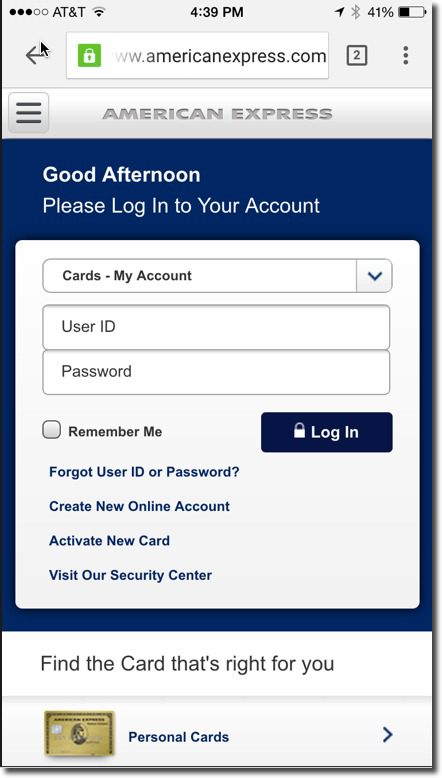

Least favorite FI: American Express (lots of competition for this one)

Too much emphasis on logging in, easy-to-miss card-finder at bottom

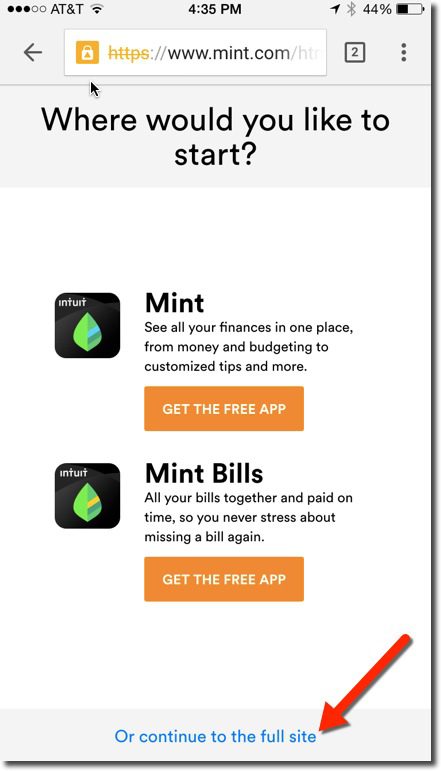

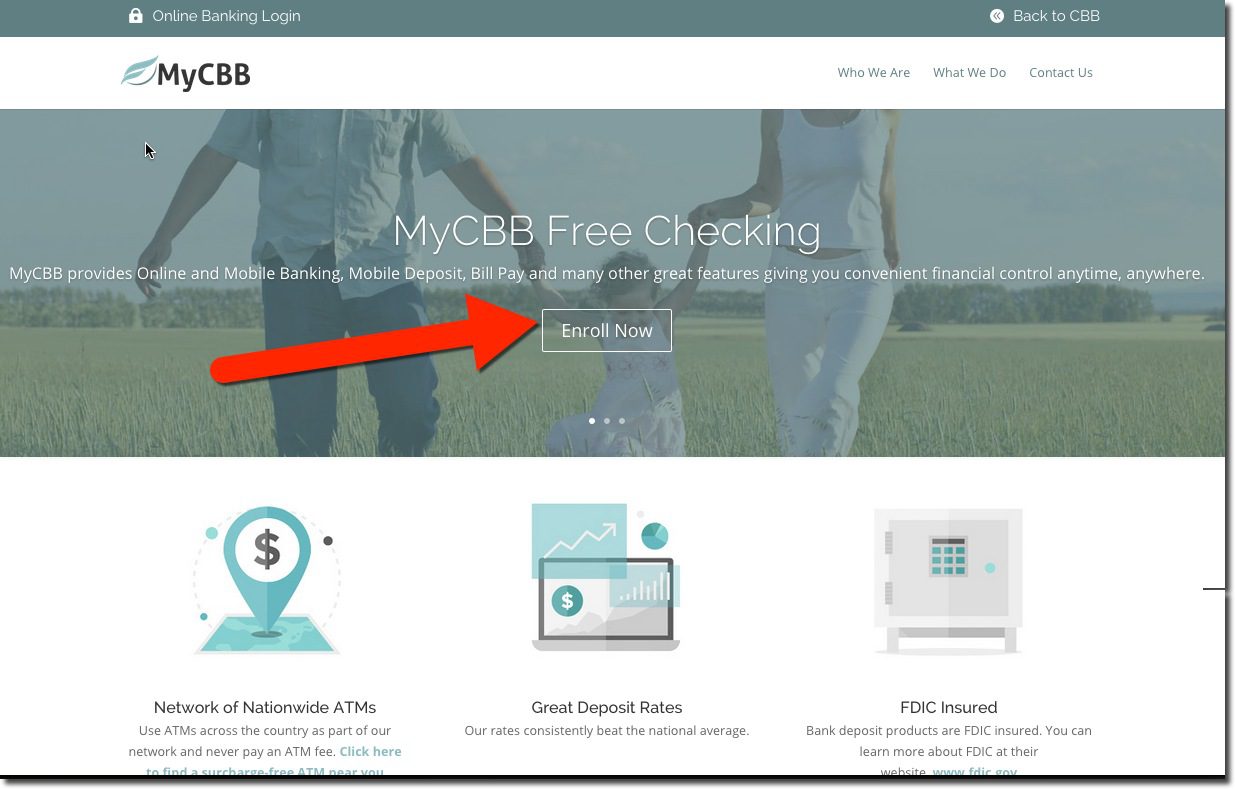

Least favorite non-FI: Mint

Straightforward app link, but needs to better engage new user before offering the two choices; not very graphically interesting

——–

Top 20 apps (in order at U.S. App Store, 5PM Pacific 31 Aug 2015): Chase, BofA, Wells Fargo, PayPal, Capital One, Venmo, Credit Karma, Square, Mint, Acorns, GEICO, Citibank, Discover, American Express, USAA, Progressive, US Bank, Navy Federal, TD Bank, PNC Bank

#RockChalk (for Karl, Joe and Mary)

")

")