- Bank of America launched a new QR code sign-in for its CashPro offering.

- Paired with biometrics, the new sign-in option takes advantage of the trend in favor of QR code technology as a verification and log-in solution.

- Bank of America’s CashPro has received recognition from Celent, Global Finance magazine, The Asian Banker, and Treasury Management International (TMI).

One of the surprising fintech trends of the past few years has been the deployment of QR codes as an option to facilitate payments in an increasingly wide range of contexts. Today, Bank of America announced that it has launched a new QR code sign-in for its CashPro solution. This will enable Bank of America’s 500,000 CashPro users to scan a QR code with their mobile device and use their biometric information via the CashPro App in order to access the CashPro website. The new option will also alleviate the need for users to manually enter passwords.

“QR sign-in is a technology that’s familiar to our clients from their personal lives, and now they can use it to seamlessly access CashPro,” Global Product Head for CashPro in Global Transaction Services Tom Durkin said. “The technology kicks off a schedule of enhancements we plan to introduce to CashPro over the next 18 months that will further improve the simplicity and security of our award-winning platform.”

Bank of America’s CashPro offers a complete digital platform for managing payments, receipts, investments, FX, and trade. The technology enables users to conduct their banking business from anywhere via the CashPro App, viewing balances, approving payments in less than a minute, depositing checks remotely, and making payments. Businesses can leverage the CashPro API to access a wide range of treasury activities including payments, fraud prevention, liquidity optimization, and more. CashPro also has a forecasting feature. Powered by machine learning and predictive analytics, CashPro Forecasting provides visibility across all customer accounts – including accounts at other institutions – and helps firms better manage future cash flows. The technology, embedded in CashPro and unveiled at the beginning of the year, provides customizable, machine-generated, daily, weekly, or monthly forecasts and learns over time to make predictions smarter and increasingly accurate.

“Many companies today rely on manual, repetitive work to forecast their cash needs, leaving little time to analyze the data for making strategic decisions, which is the actual objective of the forecasting exercise,” Co-head of Global Commercial Banking, Global Transaction Services for Bank of America Ken Ullmann said. “With CashPro Forecasting, companies can automate their forecasting process while improving the accuracy of their predictions, all without making any IT investment.”

Among the world’s leading financial institutions, Bank of America serves 67 million consumer and small business clients with 4,000 retail financial centers. Bank of America also provides a digital banking experience with 55 million verified digital users. Serving customers throughout the U.S. and its territories, as well as 35 countries around the world, Bank of America is a publicly traded company on the New York Stock Exchange under the ticker symbol BAC. The institution has a market capitalization of $250 billion.

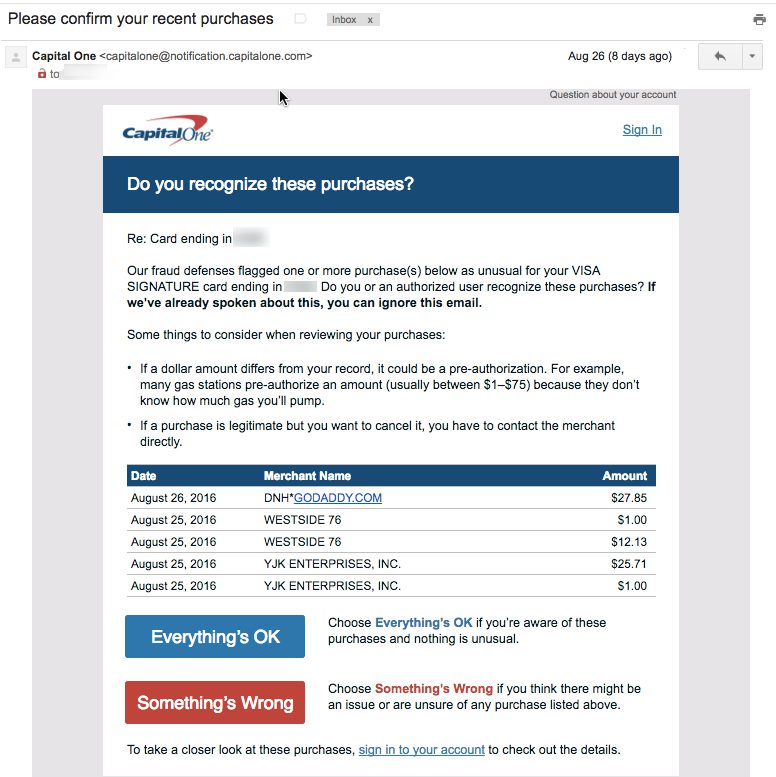

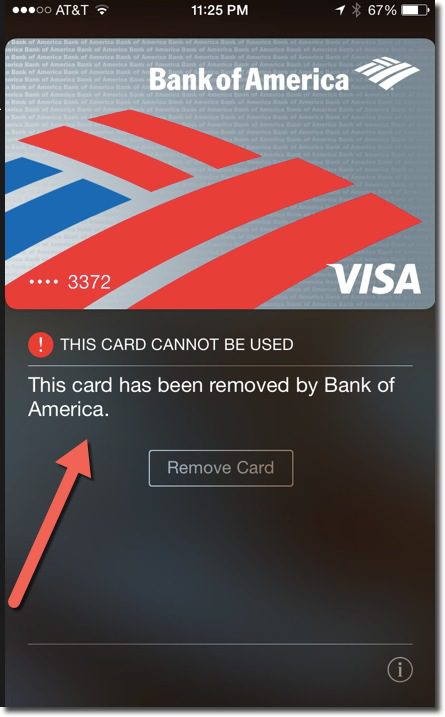

For the third year in a row, I traveled from Seattle to the L.A.-area to drop off my son at college. And for the third year in a row, Bank of America declined my card at Target, buying groceries and incidentals for him. And this time it was an EMV chip-card. Thank goodness I had my trusty Capital One card along, because it seems to do a far better job minimizing false positives (for fraud), at least for my account.

For the third year in a row, I traveled from Seattle to the L.A.-area to drop off my son at college. And for the third year in a row, Bank of America declined my card at Target, buying groceries and incidentals for him. And this time it was an EMV chip-card. Thank goodness I had my trusty Capital One card along, because it seems to do a far better job minimizing false positives (for fraud), at least for my account.

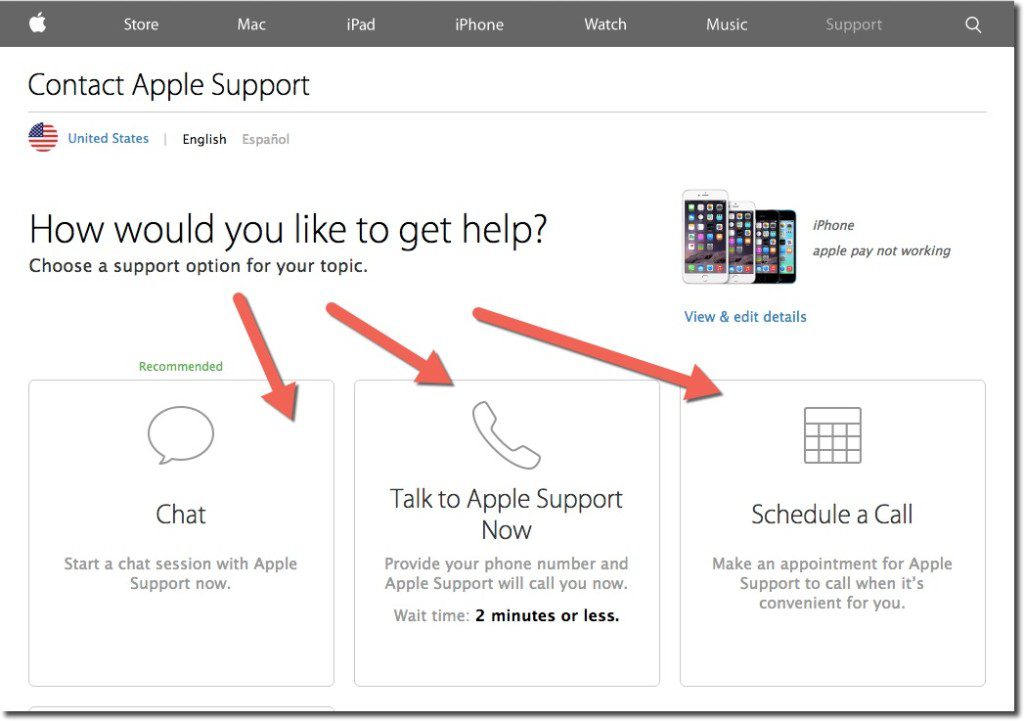

During my Google search, I stumbled into the correct area to get to Apple Care support (see A above). While I had to go through a few screens in the self-service area, it took only about 30 seconds to get to the one that offered a choice of online chat, call center (with 2-minute estimated wait time), or alternatively, I could schedule a call (see inset).

During my Google search, I stumbled into the correct area to get to Apple Care support (see A above). While I had to go through a few screens in the self-service area, it took only about 30 seconds to get to the one that offered a choice of online chat, call center (with 2-minute estimated wait time), or alternatively, I could schedule a call (see inset).

{kind=link}