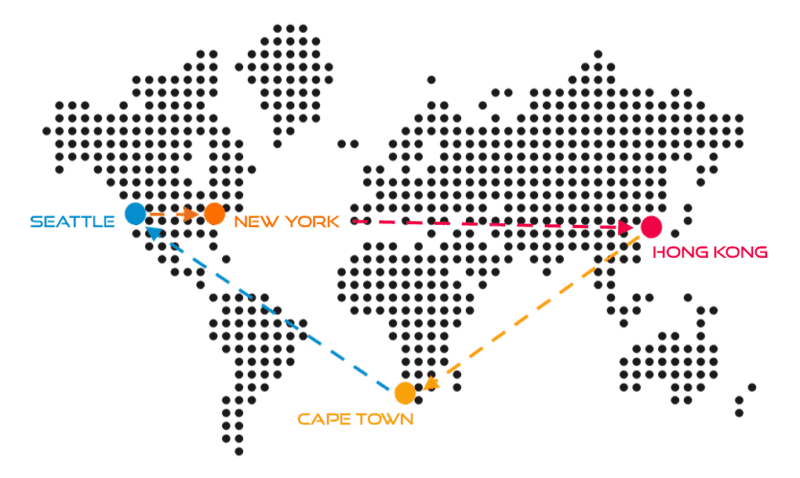

As Finovate goes increasingly global, so does our coverage of financial technology. Finovate Global: Fintech News from Around the World is our weekly look at fintech innovation in developing economies in Asia, Africa, the Middle East, Latin America, and Central and Eastern Europe.

Asia-Pacific

- InComm launches Google Play gift cards in Thailand as it celebrates its 10th anniversary in the Asia-Pacific region.

- Bank of Thailand announces plans to develop a central bank digital currency (CBDC).

- Indonesia’s KoinWorks, an online P2P lending marketplace, locks in $16.5 million in funding.

- Singapore-based crypto payments startup, Terra, raises $32 million in funding.

Sub-Saharan Africa

- Azimo forges strategic partnership with African payments business, Interswitch Group.

- Nigerian payment startup Paystack picks up $8 million Series A investment in round led by Stripe.

- South Africa-based bitcoin wallet Luno tops two million customer milestone.

Central and Eastern Europe

- Sberbank becomes Founding Partner of World Economic Forum Centre for Cybersecurity.

- A pair of fintech entrepreneurs from Latvia have bought Colorado National Bank for $8.97 million.

- Bank of Russia’s Corporate University hosts workshop on functioning of regulatory sandbox.

Middle East and Northern Africa

- Modo teams up with Etihad Airways to build loyalty solution for airline industry.

- Emirates NBD launches DirectRemit service to the U.K.

- Forbes Middle East profiles the fintech industry in Lebanon.

Central and South Asia

- India-based startup PaySpoon to provide mobile-first credit options for consumers.

- ZestMoney, a digital lending startup based in Begaluru, has raised $13.4 million in Series A funding.

- Entrepreneur India explains why new entrepreneurs should “consider fintech as a sweet spot.”

Latin America and the Caribbean

- Compass Plus migrates Brazilian prepaid card issuer, BPP, to its platform.

- PYMNTS.com looks at partnerships between fintechs and traditional FIs in Mexico.

- Wirecard Brazil introduces new financial features for its entrepreneur customers.

“Don’t tolerate disrespect or discrimination against you or anyone else. Don’t wallow in imposter syndrome because someone gaslights you. Don’t apologize and don’t explain/justify/mitigate your existence in the room. Be accountable, and hold others accountable for themselves.” Ghela Boskovich, head of fintech/regtech partnerships, Rainmaking Innovation, spent the last ten years focused on business development for core insurance and banking system solutions, and is the founder of FemTechGlobal that bridges the gender gap in fintech and the financial services industry. We speak to her about her career, inspirations and advice for fellow

“Don’t tolerate disrespect or discrimination against you or anyone else. Don’t wallow in imposter syndrome because someone gaslights you. Don’t apologize and don’t explain/justify/mitigate your existence in the room. Be accountable, and hold others accountable for themselves.” Ghela Boskovich, head of fintech/regtech partnerships, Rainmaking Innovation, spent the last ten years focused on business development for core insurance and banking system solutions, and is the founder of FemTechGlobal that bridges the gender gap in fintech and the financial services industry. We speak to her about her career, inspirations and advice for fellow

Presenters

Presenters Russ Prettitore, Chief Revenue Officer

Russ Prettitore, Chief Revenue Officer

Presenters

Presenters

Presenters

Presenters Ana Ines Echavarren, CEO, Infocorp

Ana Ines Echavarren, CEO, Infocorp

Presenters

Presenters Clayton Weir, Co-Founder, Chief Strategy Officer

Clayton Weir, Co-Founder, Chief Strategy Officer

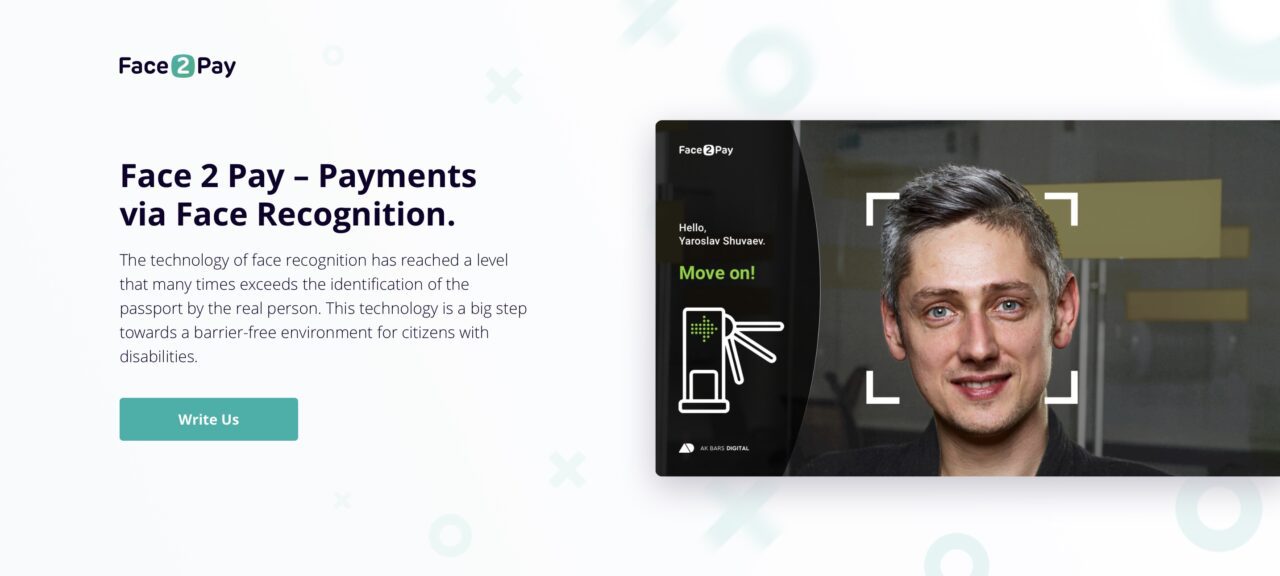

Presenters

Presenters Damir Galiev, MBA, Business Development

Damir Galiev, MBA, Business Development Yaroslav Shuvaev, Head of R&D

Yaroslav Shuvaev, Head of R&D

Presenters

Presenters Daniel Wideman, VP of Product

Daniel Wideman, VP of Product