This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

In a COVID-19 world, the rich may not necessarily be getting richer, but it has become clear that the virus is taking a toll on lower income populations. And with this, the global pandemic is shining a light on income disparity.

Do you remember the last movement to highlight income inequality?Occupy Wall Street. The movement started in September 2011 as groups assembled at major financial districts and banks to make their voices heard about income distribution, bank reform, student loan forgiveness, and capitalism in general. Nearly 200 protestors camped out in Zuccotti Park in New York’s financial district, ultimately costing the city $17 million.

So with the income inequality fresh on consumers’ minds, here are a few ideas on how banks and fintechs can be their ally instead of their perceived enemy.

Be flexible

While you don’t need to bend over backwards, offering some flexibility is key. And even though offering flexibility on payment plans can be essential, it’s not all consumers are looking for. Your call center, for example, is likely overloaded right now. Instead of having callers wait on hold, can you direct them to a chatbot or make an option for them to request a call back from an agent at a certain time?

Straying from traditional operations and bending some rules (in a compliant manner, of course!) can make a huge difference to a stressed-out consumer that is just looking for someone to understand their situation.

Be generous

You don’t have to forgive a customer’s mortgage payment for them to like you. Peer-to-peer payment company Venmo is doing a great job at engaging with its customers during this time. The company is depositing $20 into consumers’ accounts in exchange for their generosity toward healthcare workers or others in need.

Select an idea that works for your organization’s image. You can give away gift cards to Netflix or offer free gift cards to local restaurants for take away meals. The giveaways can be in under $10 and done at random or as a daily or weekly online drawing. For something more simple, you could host a larger cash giveaway with only one or two winners.

Show unity

Play a role in your community, even if it’s not an in-person effort. Advertise in the local paper that your staff is volunteering to drop off groceries for elderly citizens, display uplifting sayings to encourage passersby, or even place rolls of toilet paper on front steps of houses in nearby neighborhoods. If toilet paper isn’t your style, mail coloring sheets and simple art supplies to customers with small children. For smaller banks, publish the phone number of a representative who can help customers sort through financial issues.

Small actions can have big outcomes during a crisis like this. During a time when people are “looking for helpers” as Mr. Roger’s instructed, banks have a great opportunity to be the helpers in their community.

Blockchain-based payments company Sila announced today it has pulled in $7.7 million in Seed funding. The round was led by Madrona Venture Group and Oregon Venture Fund with contributions from Mucker Capital, 99 Tartans, Taavet Hinrikus, and Jerry Neumann.

Sila was co-founded in 2018 by Shamir Karkal, one of the entrepreneurs who co-founded Simple in 2009 and was responsible for integrating the challenger bank’s system into BBVA after it was acquired by the mega bank in 2014 for $117 million. Karkal now serves as Sila CEO.

The company will use today’s funds to accelerate growth, introduce new product features, and acquire more customers. As part of today’s deal, Madrona Venture’s Hope Cochran and Oregon Venture’s Rick Holt will join Sila’s board of directors.

The Portland, Oregon-based company has a single API that offers what it’s termed Infrastructure-as-a-Service. Overall, Sila helps companies authenticate consumers via a partnership with Alloy, connect with consumer bank accounts via a partnership with Plaid, and move money. All three of these capabilities come together to enable companies to create their own in-app, white-labeled digital wallet. Sila’s customers range from startups to established businesses working in finance, insurance, real estate, and blockchain.

To power the funds transfers, Sila is using SILA, its own ERC token that is pegged to the U.S. penny. Since the money is held in Evolve Bank and Trust, a traditional bank, all funds are FDIC insured.

“The global financial system is broken,” said Karkal. “(It) doesn’t serve consumers, small businesses, or the innovators trying to reach them. It is too expensive, inefficient, tightly regulated, and difficult to integrate into fintech applications.” Sila is addressing these challenges in multiple ways, one of which is its price point. The company’s pricing ranges from $0 per month plus fees for startups, to just under $10k per month plus fees for enterprises.

As for what’s next, Sila is currently working on adding support for card payments, business ID verification, and international payments. The company, however, has yet to disclose timing on these projects.

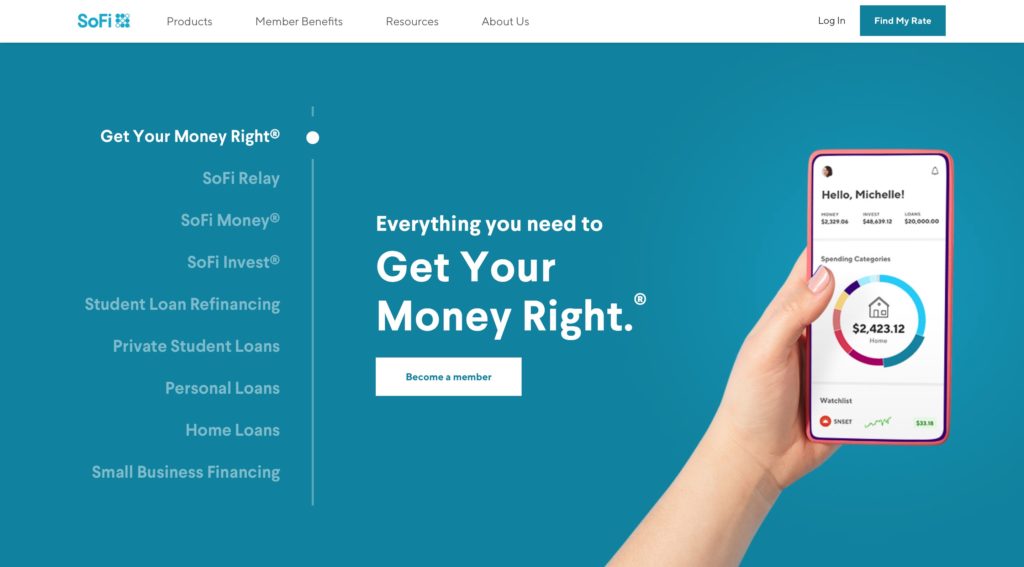

In a cash and stock deal valued at $1.2 billion, online lender and personal finance innovator SoFi has agreed to acquire financial services API and payments platform, Galileo Financial Technologies.

Galileo enables companies to build innovative consumer and B2B fintech services via its suite of open APIs. The company’s technology powers a variety of functions including:

account set-up

funding

direct deposit

ACH transfer

IVR

early paycheck deposit

billpay

transaction notifications

check balance

point of sale authorizations

Galileo processed $53+ billion in annualized payment volume in March of this year, more than doubling its September 2019 tally of $26 billion. Notably, SoFi and Galileo are already quite familiar with each other; SoFi’s Sofi Money solution is currently integrated with Galileo’s payments platform and leverages a number of the platform’s account and events functionalities.

Together, the two companies will further combine their efforts to create value for customers of both firms, who will benefit from a feature set that enables them to participate in the transition from “physical-only to a multi-channel digital and physical platform.”

“SoFi has established itself as a leader in the fintech sector, providing our more than one million members a full array of financial products to help them get their money right,” SoFi CEO Anthony Noto said. He credited SoFi’s members for motivating the company to continue innovating, and for encouraging “bigger, bolder, and more expansive” thinking. “Together with Galileo, we will partner to build on our companies’ strengths to drive even greater financial technology innovation, making those products and services available to both current and future partners.”

Galileo will operate as an independent subsidiary of SoFi, post-acquisition, with Galileo CEO Clay Wilkes remaining on board to continue leading the company. Praising SoFi’s suite of solutions for borrowing, saving, spending, and investing, Wilkes said, “these are products that many of our leading fintech clients are asking for. Distributing products through our enterprise class API is the vision behind this combination. I think it’s very powerful.”

SoFi made its Finovate debut in 2017, partnering with Quovo to presentHow Quovo and SoFi Perfected Bank Authentication at our developers conference, FinDEVr Silicon Valley. The company, based in San Francisco, California and founded in 2011, has raised $2.5 billion in funding, earning a valuation of $4.3 billion as of May of last year.

What does it mean to be financially literate? Is it more important to be able to balance a checkbook or to understand the power of compound interest? Does a financially literate person pay down student debt or consumer debt first? And does a truly financially literate person even take on debt in the first place?

A growing number of fintechs – many of them Finovate alums you’ll meet below – have devised innovative ways to help young people in particular, become better earners, savers, spenders, and investors. The majority of these innovations leverage rewards and gamification to make the educational medicine go down easier. These strategies use everything from gift cards to actual cash to encourage users to successfully complete lessons on personal finance or watch videos on common sense money management.

As companies, these fintechs partner with financial institutions – community banks and credit unions in particular – to help make their financial literacy offerings available to their customers and members. In some instances, companies have successfully partnered with educational institutions which have used their solutions as part of their financial education curricula.

April is financial literacy month. And as the coronavirus-induced economic slowdown – and potential recession – has everyone reconsidering the stability of their financial circumstances, now seems like an especially good time to be reminded of the importance of a solid – contemporary – financial education.

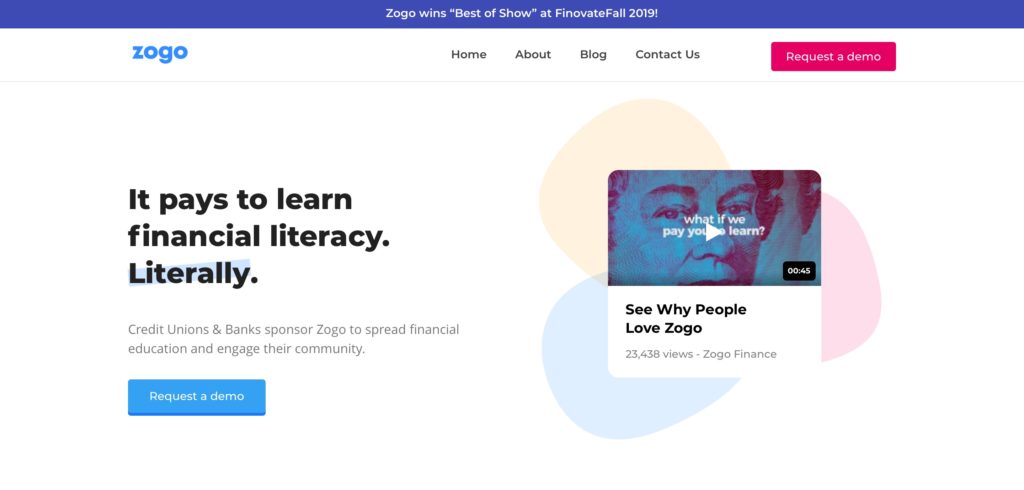

As recently as last fall, Finovate audiences were ranking financial literacy among the top of fintech’s most important themes. Zogo Finance, a Durham, North Carolina-based fintech that made its Finovate debut at FinovateFall, took home a Best of Show award for its Teen Financial Literacy app. Zogo’s solution pays users cash rewards – in the form of gift cards from leading brands – for successfully completing lessons on topics such as budgeting, credit, and investing.

The platform’s more than 300 educational modules were designed by educators at Duke University and ensure that users meet national standards for financial literacy. Zogo has teamed up with more than 11 community banks and credit unions in 12 states since its inception in 2018. The company began this year announcing a new partnership with fellow Finovate alum Bankjoy.

EVERFI, a Washington, D.C.-based company founded ten years before Zogo Finance, is another recent Finovate alum that has made a commitment to promoting financial literacy. The company powers community-oriented financial education for more than 850 financial institutions and 3,500+ partners in all 50 states of the U.S., as well as in Canada and Puerto Rico.

EVERFI, which offers workplace training and other educational programs as well as financial literacy, demonstrated its Achieve solution at FinovateSpring last year. The financial wellness technology enables financial institutions to offer personalized financial education to customers, employees, as well as to small business and corporate banking clients. From savings for college to navigating the homebuying process, EVERFI’s Achieve platform offers financial education that is as relevant as it is comprehensive.

Last fall, EVERFI announced a partnership with Zelle parent Early Warning Services to provide free financial education coursework to more than 1,000 high schools and 50,000+ students. The company began this year working with the MassMutual Foundation and the Washington Wizards NBA team to host the FutureSmart Challenge – an interactive financial literacy event for middle school students. Named to Fast Company’s 2020 World’s Most Innovative Companies roster, EVERFI unveiled a new financial education website earlier this month dedicated specifically to the financial challenges of the coronavirus pandemic.

Plinqit is another platform that made its Finovate debut last year and combines being an actual savings app with financial literacy features. Developed by Ann Arbor, Michigan-based HT Mobile Apps (HTMA), Plinqit leverages its Build Skills feature to pay users for engaging with its educational content. Once users sync their Plinqit account with their bank or credit union checking account and set up as many as five savings goals, Plinqit will help the user set aside a pre-determined amount of money on a customized schedule. Users can earn Plinqit cashback rewards (of approximately 1%) by reaching savings goals, referring friends and family to Plinqit, or by viewing articles and videos on personal finance and financial wellness topics.

A partnership with Arkansas-based First Community Bank ($1.5 billion in assets) put Plinqit back in the fintech headlines at the beginning of the year. The 26-branch bank teamed up with Plinqit parent company HT Mobile Apps in order to provide HTMA’s savings and financial literacy solutions to its customers. More recently, HTMA brought its financial education solutions to ChoiceOne Bank and Marquette Savings Bank.

Provo, Utah-based Banzai is another fintech oriented around financial literacy that made a major splash in its FinovateFall debut in 2018. The company picked up a Best of Show award for a demonstration of its turn-key, Community Reinvestment Act-eligible solution to enable organizations to add personal finance-based educational content – including interactive online simulations – to their websites.

Partnerships with community banks and credit unions enable Banzai to offer its financial literacy solution free of charge. The company provides three tiered courses for youth – Junior, Teen, and Plus – to ensure that the information provided and real-world scenarios are age-relevant and appropriate. Banzai’s curriculum has been used by 60,000 teachers across the U.S. and can be accessed from desktops, tablets, and mobile devices, as well.

In launching a new financial education resource for adults last fall, Banzai Coach, the company made a significant addition to its financial literacy offerings. Banzai Coach provides adult users with financial advice and instruction on how to get out of debt, how to manage basic business finances, and how to maximize their tax-advantaged investments such as retirement accounts, health savings accounts (HSA), and flexible spending accounts (FSA).

“Kids in schools love knowing that their decisions in the game actually have an impact,” Banzai’s Bryce Peterson wrote on the company’s blog announcing the availability of Banzai Coach. “As adults, we have quite the opposite concern: just about every decision we make has some kind of impact we didn’t predict or control.”

HR and payroll software solutions provider Paylocity made an acquisition today that will bring the company into the COVID-19 era. The Chicago, Illinois-based company announced it has purchased video platform provider VidGrid for an undisclosed amount.

Paylocity made the purchase to reinforce its services with VidGrid’s peer-to-peer learning courses. The company expects that adding workplace video communication tools will boost employee collaboration, engagement, and retention.

“We believe video will play a critical role in transforming workplace communication,” said Paylocity CEO Steve Beauchamp.

Today’s acquisition stems from Paylocity’s previous partnership with VidGrid that powered Paylocity’s learning management system (LMS), a tool that enables clients to learn from interactive videos featuring subject matter experts. “As part of our product expansion, we introduced our Learning Management System and worked with VidGrid to provide learning opportunities that the modern workforce expects,” Beauchamp said. “VidGrid’s approach aligns with our culture of caring deeply for our clients and we couldn’t be more excited to welcome their talented and innovative team to Paylocity.”

The acquisition– Paylocity’s first– comes at a time when traditionally in-person consultations and services have been pushed to online channels in order to comply with social distancing requirements. Secure video communications channels have proven to be invaluable during the COVID-19 era. Many experts are predicting consumers’ habits to pursue services online instead of in-person to continue even after it is once again deemed safe to gather in person.

Founded in 1997, Paylocity has more than 3,300 employees, more than 60% of whom work remotely (this was, of course, before everyone was required to do so). The company has more than 20,000 clients and 2,200 partners. Paylocity is publicly traded on NASDAQ under the ticker PCTY with a market capitalization of $4.71 billion.

One of the most immediate impacts of the worldwide effort to combat the COVID-19 virus is social distancing. And however effective social distancing is in limiting the ability of the coronavirus to spread, it is equally effective in crushing the revenues of businesses large and small.

To help small businesses in the retail sector cope with this challenge, small business cash flow solution provider Kabbage has partnered with Facebook. Together, the two companies will help merchants continue to generate revenue at a time when their customers – for sound reasons based on public health – are largely staying away.

Via the partnership, small businesses can sign up on a new website sponsored by Kabbage: www.helpsmallbusiness.com. This will enable them to sell online gift certificates through Kabbage’s KabbagePayments portal and automatically list them on Facebook. These offers will be visible to Facebook users through their Facebook mobile app; Facebook users can then purchase gift certificates from the www.helpsmallbusinss.com website.

The integration makes it easy for small businesses to sell online gift certificates and place them where they are most likely to be seen by consumers increasingly resorting to online shopping in lieu of traveling to brick and mortar stores. It’s also a way for consumers to support their favorite retailers.

“Now with the powerful reach of Facebook, small business owners have greater opportunity to share gift certificate offers to the community that rely upon them,” Kabbage CEO Rob Frohwein said. “Small businesses are the most impacted in this crisis and this is one way Kabbage is applying its technology and resources to save them.”

The initiative with Facebook is only a small part of Kabbage’s participation in the effort to help SMEs survive the economic consequences of the coronavirus pandemic. The company is one of many helping facilitate relief funding to SMEs via the Small Business Administration’s Paycheck Protection Program (PPP). The PPP provides funding up to 2.5x average monthly payroll, and the SBA forgives the portion of the loan that is used for critical business operations such as payroll, rent, mortgage interest, or utilities if all employees are kept on staff. Kabbage reports that it has received more than 37,000 applications for the PPP, totaling more than $3.5 million.

“The smallest businesses in America are always the hardest hit, the most vulnerable, and the most in need when a crisis strikes, and together with our bank partner, we are working tirelessly to support them,” Frohwein said.

Founded in 2009 and headquartered in Atlanta, Georgia, Kabbage has been a Finovate alum since 2010 when the company debuted its Kabbage Loan at FinovateSpring.

What happens when third party fintechs try to access banking data on behalf of their consumers, but each way has a different way of doing so?

That’s exactly what’s happening in the U.S. right now, and it’s a major factor in preventing the country from adopting an open banking culture. In an era when consumers conduct their banking activities with multiple providers, open banking not only safeguards consumer data but also places them in control of how they want their data used and for how long.

Speaking different languages

The lack of a consistent approach is also the reason why customers of some U.S. banks have been locked out of third party applications such as Robinhood and Digit. While these customers were prevented from using their own banking data, banks had good reason to lock out the third party providers, citing security concerns. Our piece Are U.S. Banks Leaning Towards Closed Banking? covers the drama in more detail.

What’s needed is a standardized regulation for data sharing. Banks can’t trust third parties and what they may do with customer data. With new regulations such as CCPA and GDPR, banks are required to keep track of how their clients’ data is used. Once a third party possesses customer data, the bank can no longer guarantee it will be used and stored properly.

Aligning the approach

So how does the fintech industry get everyone on the same page when it comes to data sharing?

The Financial Data Exchange (FDX) was created to solve that very same problem. “FDX is member-driven and governed by majority vote and we’re united by a common mission and purpose: providing secure and convenient financial data sharing,” said FDX Managing Director Don Cardinal. “Our Working Groups are inclusive, transparent and benefit from our members’ decades of experience and professionalism.”

FDX is a non-profit organization that is creating what is essentially a playbook of data communications rules for banks and third party fintechs. FDX currently counts 102 organizations– only one third of which are banks– that vote on an agreed upon global standard for data sharing.

Keeping the end consumer in mind

Importantly, FDX not only helps its member organizations speak the same language, the alignment trickles down to benefit end consumers as well. That’s because FDX helps place consumers in control of their own data, allowing them to decide which organizations can use their data and for how long. Aiding in this transparency, some banks have created dashboards that allow customers to view and edit which apps have access to their data.

To promote more consumer awareness, FDX is working to create a certification stack that would indicate to consumers whether a bank, fintech, or organization is part of FDX. You can think of this similar to a bluetooth logo on a device that informs consumers that a product has undergone the Bluetooth Qualification Program.

So when can we expect mainstream adoption of FDX?

“While we cannot give an exact date, we know from similar innovations (online banking, billpay, mobile banking, EMV chip cards) that we are moving from the Innovator to the Early Adopter stage and that acceleration of adoption will accelerate once we pass the mid-market peak,” said Cardinal. “To date, our members have moved nearly 12 million U.S. consumers over to the FDX API.”

With many U.S. citizens out of work these days, some are struggling to put food on the table. Recognizing this need, the U.S. government has agreed to come to their aid by issuing $1,200 checks to every adult earning less than $75,000 per year and $500 per child. The actualization of this effort, however, has been slow. While some families haven’t been able to work in weeks, they will not receive their check for another two-to-three weeks.

Because of this lag time, U.S. challenger bank Chime is supporting its user base by helping select members access their stimulus money early. So far, the bank has provided a group of randomly selected 1,000 of its members that meet certain criteria to immediately receive an additional $1,200 in their account while they wait for the government’s funds to come through.

“…these randomly selected members will have access to spend an amount equaling their estimated government payment 2-3 weeks early and be able to use that money right away on everyday needs such as groceries and bill payments with their Chime card,” the company noted in its blog post announcement.

The California-based company is using SpotMe, Chime’s free overdraft protection service that allows eligible users to hold a negative balance of up to $100 while they wait for their next paycheck. Instead of charging interest on this microloan, however, Chime requests users to “pay it forward.” As stated on the company’s website, “When your SpotMe negative balance is repaid, we’ll give you the option to leave us an optional tip to pay it forward. Whether or not you tip won’t affect your SpotMe eligibility. SpotMe is a fee-free service, and friendly tips from our community help it stay that way!”

So who is funding all of this? Chime is leveraging its relationships with The Bancorp Bank and Stride Bank, as well as its investors (and specifically Mark Cuban), to forward the funds.

With a valuation of $5.8 billion as of December 2019, Chime has raised nearly $809 million. Last fall, rumors indicated that the company had 5 million customers and CNBC reported last December that Chime was adding 150,000 accounts each month.

Open banking platform for Fortune 500 companies like IBM, Yapily has picked up $13 million (€12 million) in Series A funding. The round was led by Lakestar and takes the company’s total capital to $18 million. Also participating in the funding were existing investors HV Holtzbrinck Ventures and LocalGlobe, as well as angel investors including TransferWise’s Taavet Hinrikus and Twilio’s Ott Kaukve.

This week’s funding comes a year after the company’s last capital infusion – a seed investment of $5.4 million. Yapily will use the new funds to help support adoption of open banking by institutions across Europe.

Based in London and founded in 2017 by former Goldman Sachs executive Stefano Vaccino, Yapily helps drive open banking adoption by connecting banks to fintechs and other financial services providers. The company notes that its recurring revenues have grown by more than 5x over the past six months. Yapily also has increased the size of its London office to 45 employees, and expanded into Italy, Ireland, and France.

“We believe open banking is a force for good. Using our API and infrastructure, we’re not only providing our partners with strong and powerful connectivity to boost their user experiences,” Vaccino said. “But we’re also giving their customers, whether they be customers or businesses, greater control of their finances, through the creation of products and services which can fuel greater financial management and accessibility.”

Vaccino added that this flexibility for institutions and developers was especially valuable “during this period of uncertainy.” This point was echoed by Lakestar partner Stephen Nundy who cited the COVID-19 outbreak in crediting Yapily’s technology as being “best placed” to support financial innovation that drives business growth “across the financial ecosystem.”

In addition to IBM, Yapily includes GoCardless and Intuit Quickbooks among its customers.

Finovate events have always been celebrations. Celebrations of innovation, celebrations of technology, celebrations of industry. But this spring was not a time for celebration, and our thoughts are with every single person and company impacted throughout the community.

As heard from our followers and in news recently, we are turning a corner and seeing the light. The fall season has always been a big time for product launches, and these will be more important now than ever as companies reemerge. And that’s something to celebrate.

This fall for the first time, Finovate hits both coasts: FinovateFall in September in New York and FinovateWest (formerly FinovateSpring) in November in San Francisco. And we’re accepting applications from companies interested in demoing their technology at each.

Showcasing products and solutions – not just talking about them – is the best way to do business. It allows 1,000+ potential buyers, partners and investors to see how your technology works and how it can benefit them. Not convinced? Hear from some of our alums:

It’s one of the leading fintech conferences around the world, so there’s no better place to launch a product. With any conference, it’s about the return on investment — you never know if you’ll meet one person of five, but we’ve already met 10 potential partners that I’m really excited to work with.

Dana Budzyn, CEO & Founder, UBDI

It’s been successful here! We’ve already had around 30 to 40 people visit our booth and 15 requests from people saying, “Can you come and show us your technology?”

Ned Phillips, CEO & Founder, Bambu

I think we’ll be here every year – we met 90% of our clients at Finovate. We meet our clients; we meet our prospects. If you’re a bank or fintech and want to know about the trends and get a sneak peek into the future, this is the place.

Uday Akkaraju, CEO, Bond.AI

Finovate is the best place for our startup to get exposure to potential clients and investors, all under one roof!

Emil Tarazi, Chief Data Scientist & Founder, ETFLogic

Finovate is a great way to meet the right people at the right organizations! It was really exciting to have them approach us after seeing our demonstration on stage!

Mark Friedenthal, CEO & Founder, Tolerisk

For more information on demoing this fall, visit the FinovateFall and FinovateWest websites. Hope to see you apply!

With a global pandemic reshaping the way we live and work, Finovate VP Greg Palmer and his Finovate Podcast turned to two of our industry’s most insightful observers this week to help put the current challenges to fintech in context.

Ron Shevlin, Managing Director of Fintech Research at Cornerstone Advisors, is one of the world’s top fintech influencers. Author of the book Smarter Bank and a columnist for Forbes, he has provided keynotes and moderated panels at industry events including FinovateFall.

On the challenges facing business leaders during the COVID crisis

We’re wrestling, all of us, with three major concerns: our physical health, our mental health, and our financial health. And if you’re an executive at a fintech company, a bank, a credit union, whatever it might be, you’re wrestling with those things in multiple dimensions: your personal physical, financial, and mental health; your family’s physical, financial, and mental health, your employees’ three areas of health and your customers’. You add that up and it’s pretty daunting …

Alyson Clarke is a Principal Analyst with Forrester Research. Among our Analyst All-Stars at FinovateFall 2019 last year, she is a specialist in digital business transformation, creating digital and customer “obsessed” cultures, and digital strategy and innovation.

On how a likely post-COVID-19 recession will affect fintechs and financial services firms

I think we’re clearly going to see fintech funding slow – especially for new or less established startups. In fact, I think it will slow across the board from VCs to corporate funding. I think that will be some of the downside for the fintechs.

In terms of financial services and banks, they’re going to do what they naturally do and that’s focus on cost-cutting and making the operations more efficient. Sadly, some of that focus will be on automation and things like that for the sake of reducing headcount. The problem with that is that they really need to be focused on productivity, not just cost-cutting, because (managing) recessions is about preparing for the upturn.

IdentityMind Global Acquired by Acuant – The deal offers Acuant access to IdentityMind’s digital identity product, a SaaS platform that builds, maintains, and analyzes digital identities and helps companies perform risk-based authentication, regulatory identification, and detect and prevent synthetic and stolen identities.

Vymo Offers Work From Home for Sales Professionals – Vymo, the company whose intelligent sales assistant makes life easier for on-the-go sales pros, has unveiled a new enhancement to help sales teams at this time when customer engagement is even more challenging.

Azimo Partners with Siam Commercial Bank – SCB clients will benefit from Azimo’s digital money transfer program that uses RippleNet, a blockchain-based money transfer service. Using RippleNet, Azimo will be able to instantly deliver payments from Europe to SCB client accounts.

CRIF to Acquire Strands – The union will bring Strands’ personal financial management and business financial management solutions to CRIF’s client base that includes 6,300 banks, 55,000 businesses, and 310,000 consumers across 50 countries.

EVO Payments Raises $150 Million to Help Manage COVID-19 Crisis – Merchant acquirer EVO Payments, the parent company of EVO Snap, has secured $150 million in cash to help fortify the company’s balance sheet, retire debt, and provide funding for future investment opportunities during the COVID-19 crisis.

How Lending-as-a-Service Can Impact Small Businesses in Need – One of the brutal facts of the COVID-19 outbreak is that it will be difficult for small businesses to survive. The self-distancing and shelter-in-place orders, while temporary, are taxing for already cash-strapped merchants.

Nordic challenger bank Lunar announced a new tranche of funding today, boosting its Series B round. The new $21.6 million (€20 million) installment adds to the $28 million (€26 million) the digital bank disclosed in August of last year.

Today’s investment brings the company’s Series B round to $49.6 million (€46 million) and raises its total funding to $74.7 million. Leading the extension round is Seed Capital, with participation from Greyhound, Socii, Augustinus, and Unity Technologies founder David Helgason.

Lunar’s free bank account includes transfers, payments, debit card, billpay, and access to in-app budgeting tools. The Premium accounts offer a fancier-looking card, three personal accounts, travel insurance, virtual cards, and more at a cost of just under $7 (69 krona) per month. The challenger bank also offers a business bank account for $194 per year that integrates with third-party software providers comes with commercial lending opportunities.

Lunar was founded in 2015 and received its banking license in August of last year from the Danish Financial Supervisory Authority. In all, the company touts 150,000 users. Ken Villum Klausen is founder and CEO.