This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

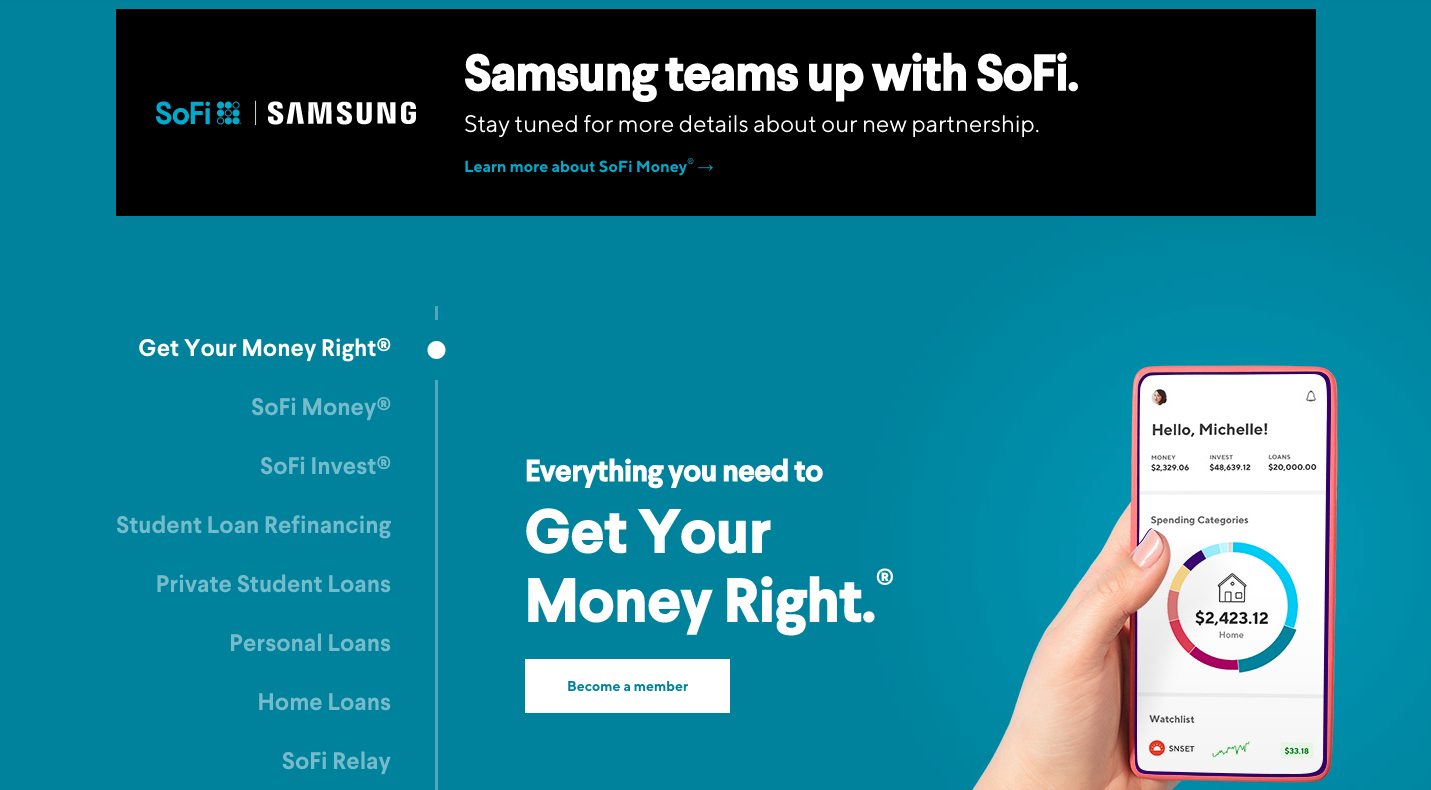

Alternative finance solutions provider SoFi and Samsung’s Samsung Pay joined forces this week to launch a debit card.

The two have spent the last year collaborating to make a mobile-first money management platform with its own debit card and cash management account.

The initiative is part of Samsung’s broader Samsung Pay mobile payments platform that the company launched in 2015. Samsung’s mobile payments platform uses built-in magnetic secure transmission technology (MST) and NFC functionality to enable users to make contactless payments.

“Our vision is to help consumers better manage their money so that they can achieve their dreams and goals,” said Sang Ahn, Vice President and GM of Samsung Pay, North America Service Business, Samsung Electronics in a blog post. “Now more than ever, mobile financial services and money management tools will play an even bigger role in our daily lives while also opening up new possibilities.”

Specific details about the card are still pending.

The new debit card offering will provide Samsung with a unique way to compete with Apple’s Apple credit card. Compared to Apple’s credit card, however, Samsung’s debit card product sounds more sticky. That’s because budgeting and cash management features built into the app will encourage users to spend more time in Samsung’s app and will keep the company’s debit card– along with its mobile payments service– top-of-mind for consumers.

Samsung’s announcement also comes shortly after news leaked that Google has its own debit card in the works. The debit card will work in conjunction with the Google Pay app.

Samsung’s timing on the launch is fairly ideal, despite the global economic crisis. The coronavirus has turned consumers’ attention toward their finances. Because of this, many banks are seeing record downloads of and engagement with their mobile banking tools. This shift to digital, combined with the new low-touch economy when it comes to everyday payments, provides an ideal environment to launch a contactless payment option.

Despite these conditions, the challenger banking space is becoming increasingly crowded in the U.S. However, Samsung’s choice to partner with an existing player instead of creating a product from scratch is a favorable one.

The CEE region – Central and Eastern Europe – has been the source of some of the week’s most compelling international fintech headlines. Among them was news that digital alternative bank Revoluthas gone live in Lithuania. The company said that it will passport its Lithuanian banking license – which it secured in 2018 – to launch in other markets in the CEE, and rely on Lithuania as its regional hub.

“Four years ago we set out to build a new kind of bank. The kind of bank that solves your problems and treats you fairly,” the company announced on Twitter this week. “Starting today, we’re excited to launch Revolut Bank to our 300,000 customers in Lithuania.”

Lithuania is the latest market Revolut has engaged; the company made its long-awaited U.S. launch in March, partnering with Metropolitan Commercial Bank to bring its banking app to market in the States. The difference is that Revolut will be able to operate as a licensed bank in the European markets it has targeted. The company has yet to officially apply for a banking license in America.

Speaking of Lithuania, Luminor Bank – the third largest bank in the Baltics – announced that it was introducing a digital onboarding solution that would enable new customers to set up accounts with a selfie. The technology, courtesy of a partnership with Ondato, compares the image on the new customer’s identification document with an image created by a 3D biometric map of the customer’s face. Ondato checks the data on the ID document, analyzes the images, and enables customers to confirm their identity with a mobile signature.

“When performing client identification, not only document validity is tested, but also with the aid of biometric data, it is established whether the individual in the document truly is a match of the individual seeking to open an account,” Ondato CEO Liudas Kanapienis said. He praised the bank as the first traditional bank in Lithuania to “fully embrace” the digitization of customer verification and account opening.

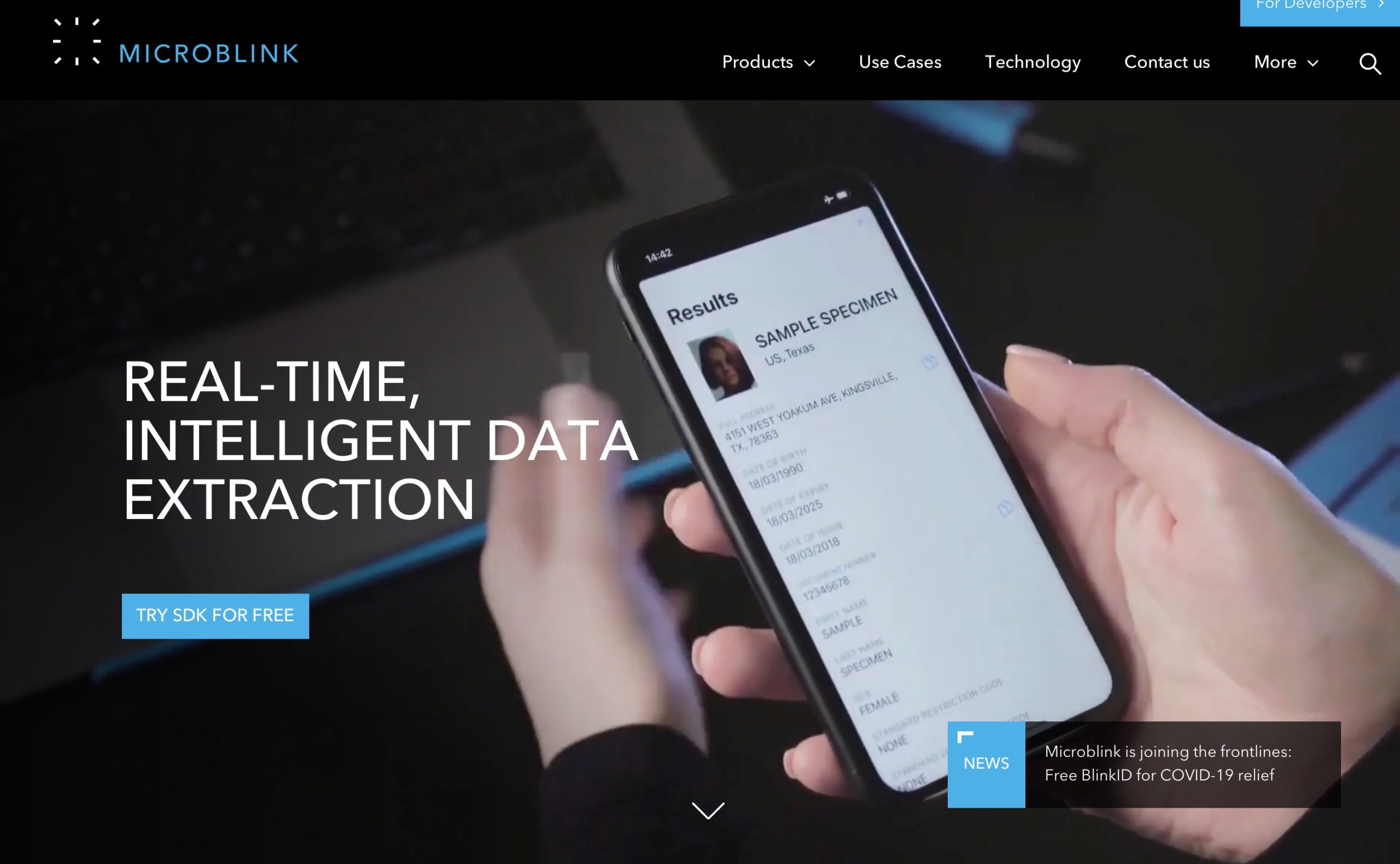

Leaning in on the COVID-19 crisis, intelligent data extraction specialist Microblink is offering free access to its flagship solution, BlinkID, “for all the heroes who have replace their capes with masks.” The company is reaching out to public healthcare, non-profit, and government organizations that are helping fight the coronavirus pandemic with an offer to integrate its data capture solution into their mobile or web app – free of charge.

BlinkID enables users to quickly and securely capture personal information from 400+ identity documents in the world. The data remains on the app and the identity document remains in the hands of the document bearer, providing for a safe, contactless experience. During the current public health crisis, the solution has been used in Indonesia by police officers conducting public health checks, in Dubai to track those delivering medicines, and in the U.K. to register volunteers who bring food to seniors and others in need of assistance.

Microblink said the offer will remain in place “until the virus subsides” and interested organizations should contact them directly to apply. “Tell us what you’re doing to mitigate the crisis,” the company said in a statement. “We’ll make sure you’re set up with the right license key and ready to fly off and save the world.” Based in London, U.K., and Zagreb, Croatia, Microblink demonstrated its technology last year at FinovateEurope.

This year FinovateAsia will be an all-digital affair. Starting on July 6 and running through July 10th, our new format offers more keynotes, more debates, and more insight into our demoing companies than we ever have offered before.

Check out our introduction to FinovateAsia from earlier this week – as well as our feature on the event’s keynote speakers – and start saving the dates. The biggest fintech event of the summer will be here sooner than you think.

Here is our weekly look at fintech around the world.

Sub-Saharan Africa

Dash teams up with cryptocurrency payments company AnkerPay to bring the DASH payments network to sub-Sharan Africa.

Just yesterday we previewed our new all-digital FinovateAsia conference coming in July. Today we’ll give you a sneak peek at some of the talent who will be providing keynote addresses at this special, mid-summer event.

Start-Ups and Digital Transformation

The first day of FinovateAsia will feature an afternoon keynote address with Chris Skinner, financial services and fintech expert, author of both the Finanser blog and the new book Doing Digital: Lessons from Leaders. Doing Digital looks at the successful digital transformations of five banks – JP Morgan Chase, BBVA, ING, DBS, and CMB – to learn how they are maximizing the opportunities that technological innovation can bring to financial services.

Skinner’s presentation – What Does COVID-19 Mean for Fintech and the Pace of Digital Change? – will look at the ways that the global health pandemic has put new strains on the financial infrastructure and examine which companies in which industries within fintech are most likely to turn the present challenge into future opportunity.

Digital Payments and Future Tech

Three keynote addresses on the second day of FinovateAsia are worth marking your calendar for. Start your day with Director of Innovation for Consult Hyperion David Birch who will provide a keynote address titled, Will COVID 19 Move Us To a Cashless Society?

Named one of the top 15 favorite sources of business information by Wired magazine and a top banking influencer, Birch has written about the various ways that society’s reaction to the coronavirus is likely to accelerate a number of technology trends that were already underway, such as the move toward digital ID. His presentation at FinovateAsia promises to be a fascinating extension of this conversation.

Later that morning, catch founder and director of Kapronasia Zennon Kapron as he discusses The Future of Real Time Payments in Asia. Kapronasia is one of the leading fintech consultancy services operating in Asia today. With more than 20 years of experience in fintech and blockchain, Kapron is also the author of Chomping at the Bitcoin: The History and Future of Bitcoin in China.

How will the Internet of Things transform financial services and how will the coronavirus impact the development of IoT are two questions that Ville Sointu, Head of Emerging Technologies for Nordea will answer in his afternoon keynote address on Day Two of FinovateAsia. With more than 15 years of experience in digital financial services, Sointu is also a member of European Commission’s Blockchain Observatory’s Use Cases and Transition Scenarios Working Group.

FinovateAsia will also feature the return of Clara Durodié, Chief Executive, Cognitive Finance Group, who is an expert on the nexus between artificial intelligence and its applications in financial services. Delivering one of the more challenging addresses of FinovateEurope in February – in which she stressed the importance of the distinctions between technologies like advanced machine learning and A.I. – Durodié joins our FinovateAsia line up to offer a similarly sobering and inspiring take on how financial services can effectively implement advanced technological innovations.

Our “main stage” presentations heat up on Wednesday as four speakers provide keynote addresses. Head of European Product Management at BBH Simone Vroegop starts things off with a look at how the investment management industry is handling disruption from fintechs.

Just before lunch, Helene Li, CEO and co-founder of GoImpact Capital Partners will discuss how new technologies, new players, and new customers will drive what she calls “the democratization of wealth services.” Li will also examine the rise of digital assets and ESG investing.

That afternoon, join us for Dr. Louise Beaumont as we turn our focus toward the challenges of Lending 2.0. As more and more small businesses look to non-traditional sources of financing, will strategic partnerships between banks, financial services companies, and fintechs become critical to getting the job done? Co-chair of the Open Bank Working Group, Dr. Beaumont recently joined Finovate VP Greg Palmer on the Finovate podcast as part of his Fintech in Extraordinary Times series.

Utpal Chakraborty, Head of Artificial Intelligence for YES BANK, provides our final keynote of the day. His address, Why the Democratization and Formalization of Data in Asia Will Open Up Marketing Opportunities in Lending for All, will also look at the way enabling technologies like artificial intelligence are empowering lenders to get more capital into the hands of those underbanked small businesses and individuals who need it.

Emerging Markets, Financial Inclusion, and the Future of Fintech

On a day dedicated to financial inclusion and the future of fintech, Kapronasia’s Zennon Kapron returns to lead a conversation on the status of emerging fintech marktets in Southeast Asia. Kapron will look to countries like Indonesia, Malaysia, Thailand, Vietnam, and the Philippines to discern the impact of COVID-19 on the growing fintech and financial services industries of these developing countries.

Frequent Finovate speaker, moderator, and panelist Theodora Lau will provide a keynote address that takes up the relationship between technology and financial inclusion. Specifically, Lau, founder of Unconventional Ventures, will examine how the rise of platform players and superapps is helping reach previously excluded communities.

Digital Customer Experience, Regtech, and Fighting Financial Crime

One of the highlights of our final day of FinovateAsia will feature Steven Van Belleghem, whose presentation on the future of the customer experience was one of the highlights of FinovateEurope in Berlin earlier this year.

This summer, Van Belleghem will tackle the issue of the customer experience during and after the COVID-19 crisis. How will the trends he introduced to us in February – faster than real-time service, hyper-personalization, and intuitive user interfaces – survive a world of social distancing, remote learning, and lockdown? Join us in July as Van Belleghem tackles some of the questions surrounding the fate of the customer in the age of the coronavirus.

We’re still building the agenda for FinovateAsia with more speakers and special guests, so be sure to check out our FinovateAsia hub for the latest updates on what’s in store July 6 through 10.

B2B cross-border solutions provider Currencycloud is teaming up with Canadian transaction processor Carta Worldwide to bring transparency, accuracy, and cost-competitiveness to international transactions.

“This is an exciting partnership and the first of its kind, combining our respective skills sets to drive innovation and give customers further transparency on their international card payments,” Currencycloud co-founder and Head of Strategic Partnerships Steve Lemon said. He noted that the partnership would put customers “at the center of the offer” and enable issuers to offer real-time foreign exchange rates at the point of sale to fintechs and challenger banks.

The two companies said in a statement that they are presently in the development phase of the collaboration. Their first joint offering is expected in the second half of 2020.

“We are very excited about this partnership,” Carta Worldwide Managing Director EMEA Richard Wray added. “Carta’s innovative processing capabilities collaborating with one of the most reputable platforms in the industry will enable us to deliver some real change to customers across the world.”

Named one of Canada’s top fintechs by the Digital Finance Institute, Carta Worldwide specializes in processing mobile and prepaid transactions. Founded in 2006 and headquartered in Ontario, Canada, and London, U.K., the company includes Vodafone, Westpac NZ, and Novum Bank among its customers.

Offering 85 APIs across four modules – Collect, Convert, Pay, and Manage – that support the full, B2B cross border payments workflow, Currencycloud provides enterprise-grade payments solutions to partners such as Visa and Starling Bank. Headquartered in London and founded in 2012, Currencycloud is regulated in the U.K., the E.U., the U.S., and Canada. The company began the year with an $80 million Series E fundraising round that featured participation of new backers such as Siam Commercial Bank, SBI Group, and Visa – whose SVP and Treasurer Colleen Ostrowski joined Currencycloud’s board of directors.

More recently, Currencycloud announced a partnership with Derivative Path to enable community and regional banks to offer more FX and interest rate derivative trading options to customers. The company has been a Finovate alum since 2012, and demonstrated its Global Collections solution at our west coast conference in 2018.

Fraud prevention solutions provider Emailage recently announced it has been acquired. LexisNexis Risk Solutions, owned by parent company RELX, closed the deal for $480 million.

Emailage was founded in 2012 by Rajesh Pandey and Rei Carvalho. The company offers an email risk score that uses email address metadata to help businesses assess transactional risk and validate digital identities. Access to this data enables companies to expedite approvals, prevent chargebacks, and automate workflows. Emailage also offers a Digital Identity score that layers in additional data to offer businesses a fuller picture of the user’s online reputation.

LexisNexis Risk Solutions purchased Emailage to integrate the company’s email assessment capabilities into its Digital Identity Network offerings. The integration should be somewhat smooth since the two had an existing commercial partnership prior to the acquisition.

“This acquisition is a natural fit as LexisNexis Risk Solutions and Emailage are both committed to continuously evolving our solutions to combat fraud,” said LexisNexis Risk Solutions Business Services CEO Rick Trainor. “This acquisition will enhance and expand our email data intelligence to provide our customers a more comprehensive view of risk with minimal friction for their customers.”

This isn’t the first fintech RELX has snapped up to boost its fraud and risk management services. The firm has been making a steady stream of purchases in the sector, including ID Analytics, ThreatMetrix, Accuity, and ChoicePoint. RELX has also formed numerous partnerships in the space, including with BioCatch and Blockbid.

LexisNexis Risk Solutions initiated its purchase of Emailage before COVID-19 had overtaken the globe. However, the increased interest in security players is something we can expect to see more of as the virus steers us toward the low-touch economy and drives traditionally brick-and-mortar services into the digital realm.

If auto manufacturers can make ventilators, and whiskey distilleries churn out hand sanitizer, then why can’t skiptracers be deployed to help put the “trace” in “contact tracing”?

“There’s an entire industry of seasoned skiptracing investigators that are out of work while debt collection is on hold,” President and CEO of masterQueue John Lewis wrote recently on his company’s LinkedIn page. Introducing his firm as a skiptracing platform used for contact tracing in debt collection, Lewis explained that when it comes to the “trace” component of the “test and trace” strategy to combat the spread of the coronavirus, masterQueue is your huckleberry.

“Many states are advertising the hiring of thousands of people to do the work these people are trained to do, and it should be done in a secure platform that’s turnkey and already built as this needs to happen now,” Lewis wrote, “with workflow automation, integrated click-to-dial recording with QA, regulatory compliance rule tracking and data privacy pieces built-in.”

“If you are a state that is interested in leveraging the experience of people who do this for a living,” he concluded, “let’s talk.”

Skiptracing is the art – and science – of finding an individual who is trying to avoid being found. The phrase itself refers to the slang term for fleeing a given area without leaving a trace: “to skip town.” Those who employ the services of professional skip tracers range from debt collectors and bail bonds agents to lawyers, journalists, and even members of law enforcement.

As you might guess, skiptracing involves accumulating, managing, and analyzing what can become massive volumes of information. Much of this data comes from incomplete or untraditional sources. But all of it needs to be verified, reviewed, and synthesized in order for skip tracers to gain actionable insights on their subjects.

masterQueue is a web-based solution that automates the skiptracing and collections process. The platform enables users to gather and organize publicly-available customer data, and integrate relevant state, Federal, and data privacy rules in order to remain compliant. Finally, masterQueue tracks loan portfolio, customer, account, employee, third-party vendor, and data provider metrics to provide robust reporting and audit functionality.

masterQueue’s John Lewis demonstrating the company’s platform at FinovateFall 2019.

“If there are three things you remember from what I talk with you today about, it’s three words: gather, organize, and track,” masterQueue’s Lewis told Finovate audiences in New York last fall. “Think about it in terms of data. We launched out masterQueue platform at Finovate in the spring of 2011 to be able to help debt collection (companies) find anyone they needed to find and in order to do that you need to gather, organize, and track data.”

Traditional methods in the debt collections business are especially problematic not only because of the large volumes of data to be collected, but also because of new data privacy laws that mandate how data must be handled. This has been overlooked in some of the media discussions over contact tracing in the context of COVID-19. But for masterQueue, these concerns are central – and on-going. At FinovateFall Lewis explained how, years ago, one efficient strategy of information collection – leveraging road cameras to identify the missing vehicle of a delinquent borrower instead of engaging in an outdated, time-consuming plow through paper records – was undermined by the arrival of new regulations from the Consumer Financial Protection Bureau. He highlighted the importance of innovation in the regtech space in the face of the latest shift in the regulatory sands – the California Consumer Privacy Act – and reminded attendees of the cost of getting it wrong.

“From $22 million against Google to $5 billion against Facebook tells you the stakes involved in data privacy,” Lewis noted, comparing the penalty assessed against Google by the FTC in 2012 with the fines levied against Facebook by the E.U. just six years later.

In recent years, masterQueue has scored seed funding after being self-funded by its founders and a pair of strategic Angel investors for the first years of its existence. The amount of the investment was not disclosed, but the capital did enable the company to add to both its workforce and to its top line. “This (funding) allows us to double staff and increase our year over year Q1 revenue from 2018 to 2019 by eight percent,” masterQueue co-founder and CFO Perla Lewis said.

In addition to working with some of the largest financial institutions in the U.S., the company recently has forged strategic partnerships with firms like PassTime a leading GPS solution provider, and expanded its relationship with PAR North America, a business division of KAR Auction Services. Founded in 2011, masterQueue is headquartered in El Dorado Hills, California.

With so much uncertainty these days, it’s nice to have something to be sure about. One thing we’re sure about is that our new digital format for FinovateAsia is going to rival the in-person version.

That’s right — FinovateAsia 2020 is now a completely digital event called FinovateAsia Digital. Given health concerns around COVID-19, running the event digitally ensures the safety of our attendees, speakers, and sponsors. It also enables attendees outside of Southeast Asia to participate, bringing more (and more diverse) opinions and perspectives to the event.

What will FinovateAsia Digital look like?

Extended dates The number of sessions will remain the same, and we will still feature all 100 of the original speakers of the event. The schedule, however, will be adjusted to make it easier for people to participate remotely. Instead of a two-day fintech immersion, everything will be spread out across five days. That means the event will now take place July 6 through July 10. With this extension, the content will be shorter each day and more manageable for digital participants.

Time zone The event will run on Singapore Time. The online agenda has been updated to reflect the new schedule so that you can see exactly what’s on when.

Engagement The digital nature of the event will make it even easier for individuals to interact with speakers. Attendees will be able to engage with the event in real-time, through Q&A with speakers, audience polling, and chat features.

Networking Making personal connections is one of the most valuable elements of an event, so we’ve worked hard to preserve it! To make sure everyone has ample time to connect with their fellow attendees, our networking app will run across all five days, helping you find and engage with others. All meetings will take place virtually via video call. To accommodate multiple time zones, the networking app will allow meetings to be scheduled 24 hours across all time zones.

Come join in the experience! If you previously booked your ticket, our customer service team has been in contact with you regarding details. If you have any questions, please reach out to [email protected].

Credit reporting agency TransUnionunveiled a new division this week that will unite the company’s fraud and risk offerings.

The new unit, Global Fraud & Identity Solutions Group, will tie together TransUnion’s identity verification and authentication tools that help businesses do everything from fight originations fraud to target consumers in their risk profile. The Global Fraud & Identity Solutions Group will also contain the company’s fraud detection and prevention solutions that range from detecting synthetic identities to providing background checks.

The initiative will also accelerate TransUnion’s go-to-market strategy for CallValidate and TransUnion IDVision with iovation. The CallValidate solution was formed in 2018 as the result of TransUnion’s acquisition of Callcredit Information Group. TransUnion’s IDVision solution is also the result of an acquisition the company completed in 2018.

TransUnion has brought on Shai Cohen, former general manager of RSA’s Fraud and Risk Intelligence business, to lead the effort. “We’re excited to bring in a proven leader from some of the world’s most respected cybersecurity and technology companies to unite these efforts and take our fraud prevention solutions to the next level,” said Tim Martin, executive vice president and chief global solutions officer at TransUnion.

The acceleration of a formalized fraud and risk division speaks to the global need for such solutions. The move comes at a time when demand for digital solutions has risen exponentially as consumers seek to conduct many aspects of their daily lives online during social distancing and stay-at-home orders.

TransUnion’s announcement comes on the same day its competitor Experian unveiledPrecise ID Model Suite, a new fraud fighting solution. The tools are specifically aimed to help organizations distinguish between first party fraud and third party fraud to determine their best course of action.

The Securities and Exchange Commission (SEC) announced today that it is temporarily easing up on reporting requirements for small businesses that use crowdfunding as a means for fundraising.

Small businesses looking to raise between $107,000 and $250,000 via crowdfunding are not subject to financial statement review requirements. The SEC also said it will fast-track the approval of crowdfunding listings.

The move is in response to small business’ need for funding to stay afloat while stay-at-home orders have diminished consumer demand– and therefore, revenue. While some were aided by the government’s stimulus package, the Paycheck Protection Plan, many small businesses either did not qualify for the funds or were not able to submit their application.

These small businesses may now more easily solicit the American people to help. “In the current environment, many established small businesses are facing challenges accessing urgently needed capital in a timely and cost-effective manner,” said SEC Chairman Jay Clayton. “Today’s action responds to feedback we have received from our Small Business Capital Formation Advisory Committee and others about the difficulties these companies may face in conducting an offering within a time frame that meets pressing capital needs, while continuing to provide appropriate protections for investors.”

To benefit, companies must disclose to investors that they are relying on the money because of COVID-19. Fundraisers must also meet eligibility requirements, including:

Must have been organized and operating for longer than six months prior to the start of the offering

Must be a U.S. business

Must not be a blank check or an investment company

Must have complied with Securities Act requirements in previous crowdfunding campaigns

The relaxed requirements will be in place until the end of August, so small businesses have just under four months to initiate their campaigns.

Small business expense management platform Bento for Business has a new man at the top. The company announced today that Guido Schulz will join the company as its new CEO. Schulz will team up with co-founder Farhan Ahmad who will remain as chairman of the company’s board of directors.

“Bento for Business has built an incredibly intuitive product that directly addresses the core cash flow and operational problems faced by the businesses that drive much of our economy, create jobs, and help build our communities,” Shulz explained. He called expense management “the single largest area of opportunity” for small businesses.

Founded in 2014, Bento for Business provides expense management solutions that are designed specifically for small businesses and nonprofits. Bento offers business debit cards with spending controls – including virtual cards that can be issued and used instantly – as well as Bento Pay, a B2B digital payments service that only requires the fund recipient’s email address in order to send money. Bento made its Finovate debut at our west coast conference in 2015.

“As we’ve reached a new phase of growth ourselves, bringing on Guido is an important step for delivering the same exceptional experience to businesses as Bento’s footprint continues to expand,” Ahmad said. He praised Schulz’s record in scaling companies and said he looked forward to working together to “deliver a healthy bottom line for businesses through unprecedented visibility and control over monthly expenses.”

Schulz comes to Bento from global hospitality payment gateway provider Merchant Link, where he was Chief Commercial and Strategy Officer. The company was acquired by Shift4 last August. Previously, Schulz worked for Bluefin Payment Systems, where he was also Chief Commercial Officer and, before that, at AFEX as Global EVP and Chief Strategy Officer. He was educated at the University of Erlangen-Nuremberg and was a visiting scholar at the University of Notre Dame.

Bento’s C-suite addition comes almost a year after the company bolstered its executive ranks with the addition of Paula Bachman as Chief Financial Officer. The news also arrives as the company announces a partnership with San Francisco Achievers, a youth development program that is using the Bento for Business app to manage scholarship funds and learn responsible budgeting habits.

“We have an orientation for our scholarship students,” Duane Wilson, the program’s Executive Director explained. “For some of them, this is their very first card. It allows them to have the experience.”

Headquartered in San Francisco, California, Bento for Business has raised $18.5 million in funding. The company includes Edison Partners, Anthemis Group, and Comcast Ventures among its investors.

When COVID-19 hit, the financial services sector was faced with an abrupt realization that digital transformation needed to accelerate. While moving to a digital-first approach is a massive undertaking, it can be tackled over a period of time. Financial services can see impactful digital changes implemented in hours, not years.

Most importantly, digital transformation places clients at the center of business. An exceptional customer support experience distinguishes leading financial services from the rest, helping to retain clients well beyond these unprecedented times.

Watch Zendesk’s Alex Mack, Sr. Solutions PMM, and Bank Novo’s Head of Customer Success, Brian Kale, for a live webinar. They’ll discuss quick steps financial institutions can take to digitize their customer experiences at a time when scaling support operations is crucial.

They’ll walk through digital customer support initiatives that are quick to deploy and can deliver big results. Learn how to:

Express empathy and build trust through personalization

Scale customer support with help centers and AI

Move customer conversations to SMS, social, and third party messaging platforms

Empower remote collaboration to expedite requests

See how these customer-centric initiatives can help scale your support today while strengthening your client experience for the future.

The millennial-focused social trading and investing app, which drew criticism during the market meltdown in March for repeated outages, is now sitting with $280 million in additional funding. The new capital comes courtesy of a just-completed Series F round led by Sequoia Capital, and gives the company a valuation of $8.3 billion. NEA, Ribbit Capital, 9Yards Capital, and Unusual Ventures also participated in the round.

“Amid challenging times and market volatility, we’re humbled that people are turning to Robinhood to participate in the markets and build their financial future,” the company’s blog read this week. The announcement included data points such as the three million funded accounts the company has added in 2020, as well as Robinhood’s effective outreach to new investors. The company also noted that the funding would be used to scale the Robinhood platform, develop new solutions, and add to its workforce.

Fortune’s coverage of Robinhood’s fundraising features observations on the company’s rumored IPO, the diversification of its revenue and profitability, as well as a potential launch in the U.K.

Founded in 2013 by Baiju Bhatt and Vladimir Tenev, Robinhood offers users the ability to trade and invest, commission-free, in a variety of assets including stocks and ETFs, options, gold, and cryptocurrencies. The app-based platform supports fractional share purchasing, enabling investors to buy equity in thousands of companies with as little as $1, and provides 0.30% APY on uninvested cash. The company began the year with news that its financial newsletter and podcast, Robinhood Snacks, had surpassed 10 million downloads. More recently, to help customers understand recent turbulence in the financial markets, Robinhood unveiled a new Market Volatility page with information on the various steps exchanges take to help mitigate market extremes.

Robinhood became notorious in some circles for the “race to zero” movement last fall in which major brokerages including E-Trade, Charles Schwab, and TD Ameritrade announced plans to eliminate trading fees in stocks and ETFs. Competition with Robinhood was cited as the reason.