This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

In order to reflect the new timeline of the event, we have changed the name from FinovateSpring 2020 to FinovateWest 2020. The show will take place November 23 through 24 at the Hilton in San Francisco’s Union Square. Registration is now open (if you were already registered for the event our team has been in contact with you via email).

Over the past 12 years, many of you have come to feel like family to us, and we hope you are all doing what is needed to keep yourselves and your family safe.

As part of an effort to keep everyone safe, and to comply with current governmental recommendations surrounding COVID-19, we have rescheduled FinovateWest 2020 to take place November 23 through 24.

The venue will remain the same at the Hilton San Francisco Union Square. Attendees who have booked as part of Finovate’s room block will not incur any cancellation fees from the hotel. The hotel is in the process of moving attendees in our block to the new dates and attendees will receive a confirmation when the move has been completed. If you need to change your new reservation, please contact the hotel directly.

We will be in touch with respective parties – speakers, sponsors, and demo companies – with more detailed information about arrangements for the new dates. If you have any questions please contact us to discuss further.

We remain grateful for your continued support and understanding and very much look forward to welcoming you in November.

In the meantime, please let us know if there is anything we can do to foster innovation and community in the fintech sector. Our industry was created to fulfill unmet needs of society. We know that in these crucial months ahead, innovators in this space will continue to do so.

We’re all in this together, and we each have a role in continuing the heartbeat of fintech across the globe.

Digital identity company IdentityMind Global has agreed to be acquired by identity verification company Acuant five months after the two initially formed a partnership. Terms of the agreement were not disclosed.

The deal offers Acuant access to IdentityMind’s digital identity product, a SaaS platform that builds, maintains, and analyzes digital identities and helps companies perform risk-based authentication, regulatory identification, and detect and prevent synthetic and stolen identities.

While digital identity was a hot topic at the beginning of the year, it is even more so now that much of consumer interaction is being pushed from in-person to online channels.

“Never before has identity been so critical to building and maintaining a stable and productive economy,” said Acuant CEO Yossi Zekri. “Businesses must rely on trusted identities to successfully transact, fight fraud and stay compliant. Our Trusted Identity Platform, now with IdentityMind’s orchestration layer, creates a new standard in identity verification.”

Acuant has offered identity verification solutions for 20 years. Since then, the California-based company has completed more than one billion trusted transactions in over 196 countries. Today’s deal is Acuant’s second acquisition after purchasing AssureTec Technologies in 2016.

IdentityMind was founded in 2013 and has raised $21.5 million across three rounds of funding. The company most recently demoed at FinovateSpring 2018, showcasing its GDPR compliant KYC plug-in.

One of the brutal facts of the COVID-19 outbreak is that it will be difficult for small businesses to survive. The self-distancing and shelter-in-place orders, while temporary, are taxing for already cash-strapped merchants.

Adding to the hardship, small businesses may find it especially difficult to get a much-needed loan from their local bank or credit union since many have closed physical branches to encourage social distancing. And while banks offer many services online, only 1% are capable of extending a loan digitally.

This is where lending-as-a-service steps in. The technology works like a plug-and-play option that allows financial institutions to launch mobile and web financing applications, exchange documents digitally, and issue funds within a few days. While third party fintechs already offer digital lending services, many banks are years away from being able to develop and integrate their own online lending service.

When banks implement lending-as-a-service, they are in a better position to serve small businesses that need cash flow quickly. It means that instead of turning to unfamiliar third party financing solutions, businesses can maintain their relationship with their primary bank as they get back on their feet after the crisis.

Military veteran-focused small business lending platform StreetShares began selling a lending-as-a-service offering for banks last September after it launched the product at FinovateFall. Using the new service, banks can lend up to $250,000 in funding to small businesses via a process that takes place completely online using the applicant’s web or mobile device.

StreetShares’ lending-as-a-service program offers lenders a 100% digital loan application, instant underwriting, as well as loan servicing and tracking. The program doesn’t require software integration and can go live in under 30 days.

The company’s lending-as-a-service solution has already seen success, having amassed 30 clients, including banks, credit unions, and alternative lenders. Here’s the good news– StreetShares is waiving its software subscription fees through the end of the year for banks who fund small businesses impacted by the coronavirus.

The company is calling this initiative Main Street Heroes. Since banking has transformed to an almost completely digital industry, the new initiative enables lenders to add a completely digital lending tool and serve businesses they otherwise may have had to turn away.

“In the wake of the coronavirus, business owners and regulators are both asking lenders to do more to help Main Street,” said StreetShares CEO Mark Rockefeller. “But most banks and credit unions simply have no ability to make these loans digitally. StreetShares has the needed technology and can power lenders to be the heroes that Main Street needs right now.”

StreetShares was founded in 2013 and is headquartered in Reston, Virginia. Mark Rockefeller is CEO.

Further proving that every company is a fintech company, Plaid has formed a partnership with Microsoft.

Plaid will integrate with Microsoft Excel to help give the budget spreadsheet a major upgrade. Launching under the guise of Money in Excel, the new tool will use Plaid to import users’ financial information, bringing an automated approach to financial management.

With access to 11,000 financial institutions across the U.S., Canada, and Europe, Plaid is able to import the user’s entire financial picture in real time.

Money in Excel offers budgeting features typical of most PFM applications. Users can see a monthly overview of their spending habits, analyze recurring expenses, and understand their net worth.

Money in Excel is launching as part of the new Microsoft 365 subscription service that will go live on April 21. The subscriptions range from $6.99 per month to $9.99 per month and include real-time editing in Word, advanced PowerPoint layout and speech coaching, and access to creative content.

Plaid works with thousands of third-party fintech apps such as Transferwise, Betterment, and Venmo to connect with their users’ financial institutions. The company made headlines at the beginning of 2020 after it announced it had been acquired by Visa for $5.3 billion.

Credit management solutions provider CRIF has agreed to acquire PFM company Strands for an undisclosed amount. The deal will be finalized “in the coming weeks.”

The union will bring Strands’ personal financial management and business financial management solutions to CRIF’s client base that includes 6,300 banks, 55,000 businesses, and 310,000 consumers across 50 countries.

Strands’ technology will complement CRIF’s customer acquisition, portfolio management, and credit collection tools that help forecast market developments, improve business performance, reduce credit risks, and prevent fraud.

According to CRIF chairman Carlo Gherardi, the acquisition will “allow CRIF to create a worldwide digital solutions provider for open banking.” He added, “Through this deal, CRIF will combine its market knowledge and expertise with an innovative and well-positioned fintech player, creating synergies that will help our global clients to keep on growing and innovating through their digital transformation journey.”

For its part, Strands brings to the table 700 bank clients serving 100 million end customers. Strands CEO Erik Brieva said that the deal will help fuel Strands’ mission “to enable banks to anticipate customer needs and proactively suggest next-best-actions.”

Strands was founded in 2004 and has since raised more than $55 million in two rounds of funding. The company has offices in Barcelona, Spain; Buenos Aires, Argentina; Kuala Lumpur, Malaysia; and at its headquarters location in Miami, Florida. Strands’ most recent appearance on the Finovate stage was last year, where it demonstrated a cash flow solution for small businesses alongside Mastercard.

With more than 5,000 employees, CRIF is headquartered in Italy and was founded in 1988. Today’s deal is the company’s seventh acquisition, following its purchase of Vision-Net in 2018. CRIF demonstrated its Credit Framework solution at FinovateEurope 2014.

Last fall, blockchain payments company Ripple, in conjunction with Celent, conducted a survey to better understand payment services providers’ adoption of blockchain-based payments. The findings of that study are published in a report issued by Ripple, and illustrates how far the payments industry has come with regards to blockchain adoption, and what’s needed to keep the momentum going.

The study surveyed 1,050+ payment services industry representatives across 21 countries. Overall, it found that:

35% of respondents are in production of a blockchain payments solution

27% are nearing implementation of a blockchain-based payments solution

31% say that the blockchain offers the opportunity to expand existing services into new regions

71% are “very to extremely” interested in digital assets

Ripple indicated that leveraging the blockchain for payments has gained a significant amount of momentum thanks to its fair pricing for end consumers, attractive revenue for payments providers, and the overall level of trust placed in the technology.

Now all that’s needed is to pick up the pace of adoption– but what is holding back mass adoption of the technology? Ripple’s study identifies three drivers responsible for faster blockchain adoption:

Faster implementation

Payments companies are concerned about implementing a blockchain-based payments solution because they are worried it will be expensive and difficult to integrate into their existing platform. In fact, a third of respondents to the study cited implementation as a concern of using the blockchain for payments.

Regulation

When integrating new technology into existing platforms, regulatory hurdles are almost always a concern. With blockchain technology, however, this seems to be even more true, especially with legacy financial institutions. As one would expect, regulatory concerns of digital banking providers are less acute, since they are accustomed to operating using non-traditional models.

Digital assets

One of the top perceived benefits of using the blockchain for payments is the time savings. In fact, three quarters of the survey respondents were interested in leveraging the blockchain for digital assets in cross-border money transfers. Fueling this interest is the speed at which these transactions can occur when compared to traditional payments. The study found that early adopters of blockchain technology are most interested in using digital assets.

The physical border between the U.S. and Canada may be closed, but that’s not stopping tech startup financing provider Lighter Capital. The Seattle-based company announced today it has launched its services in Canada.

Canadian businesses can now take advantage of Lighter Capital’s debt financing offerings, including term loans and lines of credit, as an alternative funding source from bank loans and VC funding. Both debt financing options offer companies up to $1 million in capital.

The company’s flagship offering, Revenue Financing, will not yet be available to Canadian businesses. Lighter Capital’s Revenue Loans help borrowers access up to $3 million in loans that they repay based on their monthly cash inflow.

“With the Canadian tech industry’s continued growth, we’re seeing a correspondingly greater need among startups for access to venture capital as well as to various forms of debt financing,” said Meredith Powell, Vancouver-based venture partner at Voyager Capital, an investor in Lighter Capital. “Lighter Capital is a trailblazer in the area of debt-based financing and I have little doubt that, given the increasing demand for their services, they’re positioned for success across the nation.”

Fueling its Canadian expansion, Lighter Capital will open an office in Vancouver, British Columbia. The company is also partnering with the Canadian branch of the Founder Institute, a startup accelerator.

Founded in 2012, Lighter Capital has offered more than $200 million to 350+ U.S. startups. Of those, 20% have had successful exits.

The following is a guest post written by Apoorv Gehlot, founder of Matellio LLC, a software engineering studio based in California.

Fintech has drastically improved the products and the services of the traditional financial services in the past few years. However, even after many financial institutions have readily adopted fintech services, there are still some hidden risks in the aforementioned industry. For instance, the integration of the fintech services in the existing banking solutions raised a severe concern for data security. Also, the rapid growth of digital platforms made the fintech industry and its customers uniquely vulnerable to various breaches in IT security networks.

Hence, it is vital to know about various hidden risks involved in the fintech services. Let’s discuss some of them here.

Trending challenges in fintech

Third-party security risks

Internal security is not always enough, especially when it comes to banks. Hence, much of the time, when banks or other financial institutions leverage a fintech service from a not-so-trusted service provider, they end up losing their data, experiencing service failures, and may even suffer a loss of reputation because of inefficient data. These types of damages occur due to third-party security risks. To eliminate third-party risks involved with fintech services, banks and financial institutions should consider the fintech relationship-related risks in their risk management assessment.

Malware Attacks

Malware attacks and hacking are the most prominent types of security issues that are prevalent in the global market. The hackers are now targeting the Society for Worldwide Interbank Financial Telecommunication (SWIFT) more easily. SWIFT systems are used by almost all the banks and top financial institutions to exchange vital financial information.

However, the recent cyberattack on the SWIFT infrastructure indicated the level sophistication of the hackers and malware attackers. The banks and financial institutions have vulnerabilities in their processes, and the hackers take advantage of these vulnerabilities to launch malware attacks.

Data Breaches

We all know that data plays a crucial role in every industry irrespective of their domain. And when it comes to banks and other financial institutions, data automatically becomes a matter of utmost importance. However, with the introduction of inefficient fintech systems in the finance industry, the problems of data breaches rose to a great extent.

Payment card details and user information are readily available to hackers making online transactions prone to cyber thefts. The financial institution partners with third parties, and then data losses may occur due to their inefficient fintech services.

Application Security Risk

Fintech applications are used by many banks to access the real-time financial information of their customers. They leverage this real-time information to carry out transactions and for performing other banking operations.

However, if a software application does not have foolproof security modules and efficient codes, then it automatically becomes more prone to cyber thefts. The attackers leverage the weak security of the applications to steal the customer data and other vital information. So if a person is planning to develop a fintech software solution they need to be very sure that the application has all the vital security features included in it.

Money Laundering Risk

Fintech-driven banks often use cryptocurrency for carrying out financial transactions. These cryptocurrencies are an integral part of the fintech ecosystem, and they are not formally regulated by any set of standards and global regulations.

Hence, the frequent use of non-regulated currencies results in illegal money laundering and even in terrorist funding. Since identifying the beneficiary in any fintech-enabled transactions is not possible due to fintech’s pseudonymous nature, the money laundering operations get enough support from the fintech services.

Digital Identity Risks

With the introduction of digital tools in the banking and finance industry, the use of mobile-based services that used one-time passwords and security codes increased drastically. These security codes and passwords are not as safe and can be easily accessed by a hacker.

The vital data of the banking customers could be easily accessed due to the faulty fintech system provided by some of the fintech service providers. Hence, financial institutions need to revisit their online security architecture to address these risk factors before planning for fintech implementation.

Legacy Banking Systems

Banks are struggling hard to develop and introduce advanced fintech services in their non-patched core banking systems. These traditional banking systems are very much vulnerable to all sorts of cyber thefts. And the main concern is way more than that.

When the tech-friendly fintech services integrate with the existing non-secured banking systems, there are chances that they will be at the target of attackers too. So, the first duty for any financial institution before implementing fintech in their organization is to refresh their core banking systems. That will help the company eliminate losses due to cyber thefts.

Cloud-based Security Risks

Cloud-based solutions are one of the significant aspects of the fintech industry. From payment gateways and digital wallets to secure online payments, cloud computing services offer everything in the fintech ecosystem. Maintaining the confidentiality and security of financial data is critical to banks and financial institutions.

Even though the cloud-based services are considered a secure means of storing the data, lack of adequate security measures can result in the corruption of your sensitive financial information. There are instances when the company partners with an inefficient, cloud-based solution provider and then deals with significant data losses. Therefore, stay updated and be wise while selecting your cloud-based service partner.

To conclude, we can say that, if hackers are unbeaten in their efforts to access the fintech platform with ease and efficiency, the faith of banking customers in the technology-driven fintech platform will be significantly reduced. All this will result in the slow growth of the fintech industry. Hence, balanced innovation is needed to promote the growth of the fintech industry and mitigate the hidden risks of fintech services.

ApoorvGehlot takes a keen interest in exploring various aspects of the digital realm, and ideate solutions with his team of innovators.He believes in sharing his experience and knowledge with readers across the world to enlighten the audience through concise and meaningful write-ups.

The past couple of years in financial services have brought a lot of discussions about the client experience. In fact, that was the topic of my interview last fall with Martin Lange, Director of Client Experience Strategy at BNY Mellon. Is the sudden focus on customer experience all hype?

“Any of us who have been in client experience for a long time would say it’s been around for awhile,” Lange said, adding, “But the industry is looking for new ways of differentiation. And new ways of differentiation– as we’ve learned from other industries– is the client experience.”

Differentiation

So why is a focus on customer experience more important now than last year, last month (or even last week)? It comes down to differentiation.

Last year we wrote about fintechs vying for customer deposits and mindshare by boosting interest rates on savings accounts up around the 3% mark. With the Federal Reserve cutting rates to near-zero, that strategy will be increasingly difficult to follow through with.

Recognizing that this is a difficult time for everyone, banks can offer consumers two simple things that may be hard to come by to improve the customer experience (and no, it’s not toilet paper).

The first is kindness. When customer service representatives have a kind and friendly disposition over the phone it can bring customers a bright spot, especially if they are in isolation from other human beings. Kind words in email and social media correspondence are also easy ways to retain consumer attention.

Financial services companies can also differentiate themselves with compassion. Waiving certain fees, especially when they are small, can be an easy way to only maintain a customer when they are struggling. Even better, banks can follow in the footsteps of Goldman Sachs, GMC, Ford, and other financial institutions by waiving payments for a month without charging interest. When the economy improves clients will remember which firms stood by them during hard times.

Challenges

When it comes to challenges in creating a stand-out client experience, Lange noted two hurdles. The first is attribution. Firms need to know that a spike in sales or client acquisition is attributed to certain actions or events, such as an improved user interface, and was not driven by other changes such as pricing or an altered service structure.

“The other challenge is a culture challenge,” said Lange. He explained that instead of structuring operations around process improvements, where employees fall into the habit of looking for the next thing to fix, firms need to be proactive and design an experience first and allow the design to follow that experience.

Leading with a design idea, Lange said, “can be emotional, and it’s based on empathy. It’s not based on Excel spreadsheets, which the industry is very used to… there are human beings that are interacting and we want to design for human beings.”

Digital payments company Square announced it will launch its small business bank next year. Square’s application for the bank, Square Financial Services, has been conditionally approved for a bank charter.

Square Financial Services will operate as an independent subsidiary of Square. The new bank’s primary objectives will be to offer small business loans for Square Capital’s commercial lending business, and to offer deposit products.

“We appreciate the FDIC’s thoughtful approach to our application, and their recognition that Square Capital is uniquely positioned to build a bridge between the financial system and the underserved,” said Jacqueline Reses, Square Capital Lead and Executive Chairwoman of the board of directors for Square Financial Services. “We’re now focused on the work ahead to buildout Square Financial Services and open our bank to small business customers.”

In preparation for the launch of the new bank, Square has begun the hiring process to staff its new bank headquarters, which will be located in Salt Lake City, Utah. Square Financial Services CEO Lewis Goodwin and CFO Brandon Soto have been charged to lead the bank’s executive team.

This comes just one month after P2P lending company Lending Club announced plans to purchase Radius Bank. The move offers Lending Club users a full suite of banking tools. Square also follows in the footsteps of Varo Money, which received approval for deposit insurance from the FDIC in February.

When digital banking makes bank branches less necessary, should banks keep their branches simple and cater to those that are less technologically savvy or should they transform their branches into high tech havens with kiosks and robots? As it turns out, a handful of banks are trying something in between.

Six banks across the globe are piloting coffee shop branches. These locations not only serve as a way for folks to buy a coffee and a snack, they are also co-working spaces, meeting rooms for non-profits, a place to gain education about personal financial management and, of course, a location where customers and prospective customers can conduct banking activity and apply for a loan.

Check out each bank’s different approach:

Capital One

Capital One was the pioneer in the bank-coffee shop branch model, launching its flagship location in 2017. The bank now has 31 Capital One Cafes and has replaced its bank tellers with “ambassadors” to make banking more friendly and approachable. These locations also offer free, one-on-one money coaching sessions (that don’t apply any sales pressure) for members and non-members alike.

Capital One has partnered with Peets Coffee and offers Capital One cardholders 50% off coffee beverages.

Each cafe offers free wifi and power outlets, comfortable seating, and private community rooms that are free for nonprofit, alumni, and student group meetings and events.

Chase opened its first coffee shop branch in December of 2019. The bank teamed up with Joe Coffee for the pilot of a full service coffee shop in downtown Manhattan.

In some respects, calling Chase’s new branch a coffee shop is a bit of a longshot. It looks like the majority of bank branches I’ve walked into. Chase doesn’t even offer any differentiation on the home page of the branch.

That said, the new location has a more modern look, offers a kid’s play area, and is dog friendly. Another differentiating factor is that the branch has only one teller window and it is located in the very back of the branch.

Tangerine

Scotiabank subsidiary Tangerine has built its image around the cafe concept. As the bank’s website states, “People who know Tangerine know we’re not a typical bank. Typical banks have typical bank branches. We don’t. We have Cafés located in some of the busiest Canadian communities.”

Tangerine’s cafes have a laid back, modern atmosphere. Each location has free wifi as well as coffee and treats for sale (all proceeds go to charity).

Unlike other bank cafes, Tangerine does not offer any teller services since it is a fully digital bank. The bank offers ATMs for cash deposits and withdrawals and employs representatives (called cafe associates) for client acquisition, to upsell products, and to answer client questions.

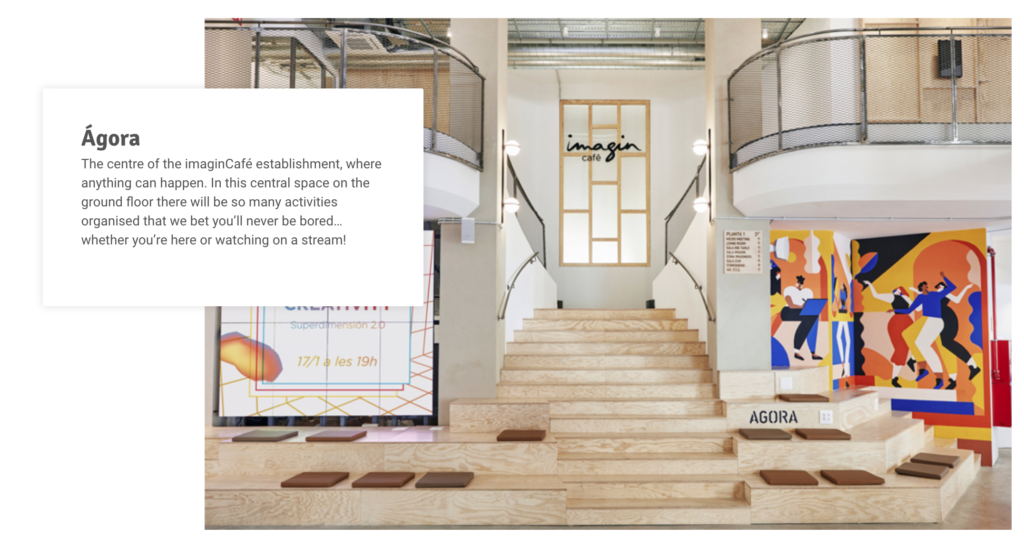

CaxiaBank

In 2016, CaxiaBank launched imaginBank, a mobile-only bank aimed to serve millennial customers. A year later the bank opened a single physical location, ImaginCafe, to appeal to its user base.

ImaginCafe isn’t quite a bank branch, however. It’s not a place where members can deposit cash or speak with bank representatives. Instead, as CaxiaBank CMO Xavier Mas explained, the cafe is “a place where the ‘imaginBank’ brand is rendered tangible thanks to a blend of innovation, immediacy, the combination of the online and offline environments, interaction with users, and the interests of young people.”

As with many bank-cafes, this location serves as a coworking space and has private meeting rooms and spaces available to rent for meetings and events. It also has an art exhibition space, a fashion showcase room, a modern theatre, a multimedia laboratory, and a gaming area. ImaginCafe hosts multiple events each month including art expos, music discussions, shows, gaming events, and concerts.

Umpqua bank calls its branch locations “stores” and incorporates retail and hotel-like amenities into the locations to make them more welcoming.

EVP of Umpqua Bank Brian Read explained that factors contributing to the uniqueness of the stores include free Umpqua-branded coffee, a dog-friendly environment, and community spaces that host yoga classes and non-profit meetings.

Santander

Santander has eight Work Cafes across the globe. These locations look like traditional coffee houses and aim to make visiting a bank something that consumers want to do, not an obligation.

As with many other banks’ concept branches, Santander’s locations offer spaces where events, conferences, and classes are hosted. These cafes are also geared toward offering entrepreneurs a co-working space and offers advertising opportunities for small businesses.

These concept branches have been successful for the Spain-based bank, which reports that anywhere from 2x to 4x more accounts are opened at Work Cafes than at its traditional branches. Additionally, at the bank’s Spain location the number of customers is increasing by 11% per year and new loan production has been boosted by 73%.

Financial services firm Fiserv made its 32nd acquisition today. The Wisconsin-based company purchased Bypass Mobile, a company that specializes in software and POS systems. Terms of the deal were not disclosed.

The acquisition is expected to help Fiserv support its clients in creating a seamless customer experience across physical and digital channels. By integrating with Fiserv’s universal commerce platform, Bypass will offer businesses a single point of contact. As a result, businesses will benefit from increased operational efficiency, enhanced security, and a more complete picture of customer interaction.

“Adding Bypass to our portfolio will make it easier for our clients to realize their digital transformation strategy, delivering interactions their customers are demanding,” said Fiserv Senior Group President of Global Business Solutions Devin McGranahan. “With this combination, we will improve the omni-commerce experience for businesses and their customers, making it easier and more efficient to pay for goods and services.”

Specifically, Bypass will enable secure Fiserv clients to accept payments in a secure environment across multiple devices. “In combination with Fiserv, we will help businesses accept payments efficiently while continuing to meet customer expectations by providing a variety of payment options,” explained Bypass CEO Brandon Lloyd.

Fiserv was founded in 1984. While the company’s most recent purchase was Merchant Pro Express earlier this month, its most notorious one in recent memory was the acquisition of First Data in January of last year. That deal closed for $22 billion.