The fintech sector attracted $332 million in new capital the first week of August. The number of deals totaled 30, slightly above the YTD average of 28 deals per week. Nearly two-thirds of the money went to solar energy lender, Mosaic.

The fintech sector attracted $332 million in new capital the first week of August. The number of deals totaled 30, slightly above the YTD average of 28 deals per week. Nearly two-thirds of the money went to solar energy lender, Mosaic.

Seven deals involved insurance startups, the most ever in a single week. Four of those came out of the most recent batch of companies launched from accelerator 500 Startups, where each received $125,000 in seed capital.

The total number of deals YTD stands at 869, about 400 more than last year’s 457. Total dollars raised YTD is $19.6 billion, double the $9.8 billion raised during the same period a year ago.

——-

Fintech deals by size from 30 July to 5 August 2016:

Mosaic

Lender for solar energy installations

Latest round: $220 million Private Equity

Total raised: $245 million

HQ: Oakland, California

Tags: Consumer, credit, loans, underwriting, solar energy, home equity

Source: Crunchbase

Kyriba

Cloud cash and treasury management solutions

Latest round: $22.7 million

Total raised: $95.1 million

HQ: San Diego, California

Tags: Enterprise, institutions, accounting, commercial banking

Source: FT Partners

Huize

Insurance portal

Latest round: $15 million Series B

Total raised: $15 million

HQ: Shenzen, China

Tags: Consumer, insurance, price comparison, discovery, lead gen

Source: Crunchbase

Paidy

Online payment service

Latest round: $15 million Series B

Total raised: $15 million

HQ: Japan

Tags: SMB, B2B2C, payments, online, security, merchants, acquiring

Source: Crunchbase

Clark

Mobile insurance broker

Latest round: $14.75 million Series A

Total raised: $14.75 million

HQ: Berlin, Germany

Incubator: FinLeap

Tags: Consumer, insurance, mobile, price comparison, lead gen

Source: Crunchbase

AxialMarket

Middle market capital matchmaker

Latest round: $14 million Series C

Total raised: $44.7 million

HQ: New York City

Tags: SMB, credit, loans, underwriting, commercial loans, M&A, investment banking

Source: FT Partners

Funding Societies

Lending marketplace for small businesses

Latest round: $7.5 million Series A

Total raised: $7.5 million

HQ: Singapore

Tags: SMB, credit, loans, underwriting, person-to-person, P2P, investing

Source: FT Partners

Kubo Financiero

P2P microfinance lender

Latest round: $7.5 million Series A

Total raised: $11 million

HQ: Mexico City, Mexico

Tags: Consumer, credit, loans, underwriting, person-to-person, P2P, investing

Source: Crunchbase

Coinify

Bitcoin point-of-sale solutions

Latest round: $4 million Series A

Total raised: $4 million

HQ: Copenhagen, Denmark

Tags: SMB, merchants, acquiring, POS, bitcoin, blockchain, crypto-currency

Source: Crunchbase

Privitar

Big-data analytics for financial institutions

Latest round: $4 million

Total raised: $5 million

HQ: London, England, United Kingdom

Tags: Institutions, analytics, BI, compliance, security

Source: FT Partners

VaultInvesting

Retirement plans for small businesses

Latest round: $1.55 million Seed

Total raised: $1.55 million

HQ: Seattle, Washington

Tags: SMB, investing, retirement planning, 401(k), employee benefits, HR

Source: Crunchbase

MovoCash

P2P payments

Latest round: $1.46 million

Total raised: $2.16 million

HQ: Palo Alto, California

Tags: Consumer, person-to-person, payments, funds transfer, remittances

Source: Crunchbase

Wealthify

Robo-adviser

Latest round: $1.3 million Equity Crowdfunding

Total raised: $1.3 million

HQ: Cardiff, England, United Kingdom

Tags: Consumer, advisers, wealth management, investing

Source: Crunchbase

Finja

Mobile wallet

Latest round: $1 million Seed

Total raised: $1 million

HQ: Lahore, Pakistan

Tags: Consumer, payments, mobile

Source: Crunchbase

RightCapital

Financial planning software for advisers

Latest round: $1 million Seed

Total raised: $1 million

HQ: New York City, New York

Tags: Advisers, wealth management, trading, investing

Source: Crunchbase

QuickGifts

Giftcard portal

Latest round: $500,000 Debt

Total raised: $3.97 million

HQ: Austin, Texas

Tags: Consumer, prepaid cards, gift cards, loyalty, payments

Source: Crunchbase

BrightPolicy

Home insurance portal

Latest round: $125,000 Seed

Total raised: $125,000

HQ: Evanston, Illinois

Accelerator: 500 Startups

Tags: Consumer, insurance, price comparison, discovery, lead gen

Source: Crunchbase

Homebot

Maximizing home equity

Latest round: $125,000 Seed

Total raised: $125,000

HQ: Denver, Colorado

Accelerator: 500 Startups

Tags: Consumer, mortgage, home equity lending, retirement planning, investing

Source: Crunchbase

INZMO

Mobile insurance provider

Latest round: $125,000 Seed

Total raised: $380,000

HQ: Tallinn, Estonia

Accelerator: 500 Startups

Tags: Consumer, insurance, price comparison, discovery, lead gen

Source: Crunchbase

StreamLoan

Workflow solution for residential home purchase

Latest round: $125,000 Seed

Total raised: $125,000

HQ: San Francisco, California

Accelerator: 500 Startups

Tags: Institutions, lenders, mortgage, lending, customer service, mobile, account opening

Source: Crunchbase

SureBids

Remittance provider

Latest round: $125,000 Seed

Total raised: $125,000

HQ: Lago, Nigeria

Accelerator: 500 Startups

Tags: Consumer, payments, remittances, gift cards

Source: Crunchbase

TaCerto

Online insurance broker

Latest round: $125,000 Seed

Total raised: $4.1 million

HQ: Sao Paulo, Brazil

Accelerator: 500 Startups

Tags: Consumer, insurance, discovery, price comparison, lead gen

Source: Crunchbase

Track

Self-employment tax payments

Latest round: $125,000 Seed

Total raised: $125,000

HQ: Palo Alto, California

Accelerator: 500 Startups

Tags: SMB, payments, tax prep, accounting

Source: Crunchbase

Trym

Insurance broker

Latest round: $125,000 Seed

Total raised: $125,000

Accelerator: 500 Startups

Tags: Consumer, insurance

Source: Crunchbase

AssetRover

Real estate investing tool

Latest round: $20,000 Seed

Total raised: $20,000

HQ: Cedar Rapids, Iowa

Tags: Consumer, investing, real estate

Source: Crunchbase

FixtHub

Fixed income markets enterprise software

Latest round: Undisclosed

Total raised: Unknown

HQ: New York City

Tags: Institutions, trading, bonds, investing

Source: Crunchbase

AxiCorp

Forex services

Latest round: Not disclosed

Total raised: Unknown

HQ: North Sydney, Australia

Tags: Consumer, SMB, FX, trading, investing

Source: FT Partners

DisLedger

Distributed ledgers for financial community

Latest round: Undisclosed Seed

Total raised: Unknown

HQ: Reston, Virginia

Tags: Institutions, blockchain, payments, bitcoin

Source: Crunchbase

Meeber

Mobile point-of-sale system

Latest round: Not disclosed

Total raised: Unknown

HQ: Singapore

Tags: SMB, payments, merchants, credit/debit cards, acquiring, POS

Source: Crunchbase

Qupital

Marketplace for corporate receivables

Latest round: Undisclosed

Total raised: Unknown

HQ: Hong Kong

Tags: SMB, credit, underwriting, factoring, trade finance, receivables financing

Source: Crunchbase

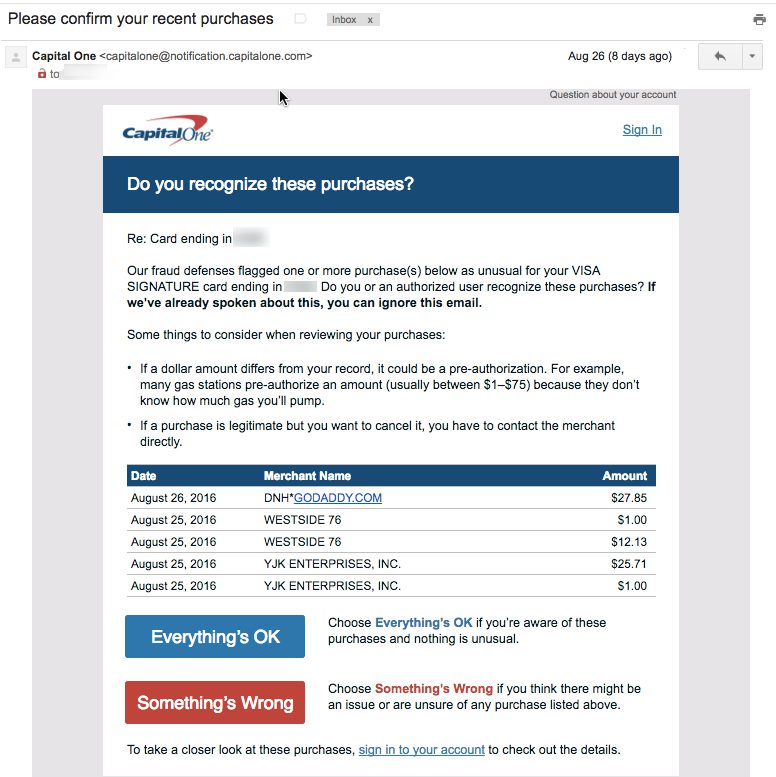

For the third year in a row, I traveled from Seattle to the L.A.-area to drop off my son at college. And for the third year in a row, Bank of America declined my card at Target, buying groceries and incidentals for him. And this time it was an EMV chip-card. Thank goodness I had my trusty Capital One card along, because it seems to do a far better job minimizing false positives (for fraud), at least for my account.

For the third year in a row, I traveled from Seattle to the L.A.-area to drop off my son at college. And for the third year in a row, Bank of America declined my card at Target, buying groceries and incidentals for him. And this time it was an EMV chip-card. Thank goodness I had my trusty Capital One card along, because it seems to do a far better job minimizing false positives (for fraud), at least for my account.

The ongoing migration to mobile provides financial institutions a chance to reboot their approach to delivering information digitally. Digital banking v1.0 (desktop online banking) was primarily about porting paper-based statements into an online format. It was a huge change and made banking more convenient, though not really any more effective than the paper-and-call-center system it replaced.

The ongoing migration to mobile provides financial institutions a chance to reboot their approach to delivering information digitally. Digital banking v1.0 (desktop online banking) was primarily about porting paper-based statements into an online format. It was a huge change and made banking more convenient, though not really any more effective than the paper-and-call-center system it replaced.