This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Banks have discussed ways to target the youth market for years. Capturing a customer under the age of 18 builds brand loyalty at a young age, increases a customer’s potential lifetime value, leads to cross-selling opportunities as they age, and increases the parent users’ engagement.

While these benefits are well-known across the fintech space, the youth market can be difficult to tap into; banking tools for minors are not yet widespread. Things may be changing, however. Developments in the youth banking market have been peppering the news this year, starting with Acorns’ acquisition of GoHenry in April. Things have really started to pick up this fall, however. Here’s a timeline:

August 10: Greenlight launched a new solution to help teens begin building credit.

September 22: Invstr launched Invstr Jr., a digital bank and investing account for users under the age of 18.

September 25: The Reseda Group partnered with financial literacy platform Goalsetter to offer a white-labeled version of the app for its members.

October 3: Acorns announced the launch of a new premium tier that integrates access to GoHenry.

October 3: Youth investing platform Stockpileteamed up with Green Dot to offer debit cards to its users under the age of 18.

It appears that youth banking tools may be having a moment. But why now? Below are a few reasons behind the recent flurry of activity in the space.

Transfer of wealth

It’s been well-publicized that the largest transfer of wealth in history is currently taking place. In fact, Cerulli Associates estimates that in the next 25 years, older generations will transfer a total of $84 trillion to younger generations. As a result, these young recipients– many under the age of 18– will need a safe account to hold and grow their newfound wealth. Youth savings accounts and investing tools are a good starting place.

Millennials maturing as parents

A decade ago, much of the discussions in the fintech industry centered around how to serve new millennial clients. Millennials are a digital-savvy generation and now range between 27 and 42 years of age. This mobile-first generation is more likely to seek out banking tools for their kids online rather than take them into a branch to open their first savings account. The recent spate of banking and investing tools all suit the need for digital-first accounts for minors.

Competition

Success invites competition. As more companies succeed in gaining users in the youth banking space, more will join in. That’s why we’ve seen not only new players enter into the space, but also established institutions create new tools to serve the market. As these tools continue to generate attention by launching new features, entering new partnerships, and adding new clients, other fintechs will begin to enter the market.

Greenlight Financial Technology unveiled its Greenlight Family Cash Mastercard this week.

The Greenlight Family Cash Mastercard helps teens build credit before they reach adulthood.

Headquartered in Atlanta, Georgia, Greenlight has raised more than $550 million in funding. The company has a valuation of $2.3 billion.

Greenlight Financial Technologylaunched its Greenlight Family Cash Mastercard this week. The new card fosters financial literacy by helping teens build their credit before they reach adulthood.

Available with all of Greenlight’s subscription plans, the Greenlight Family Cash Card enables families to earn up to 3% cash back on all purchases. Parents can add their teen children as authorized users on the card, and teens can track their credit card balances using the Greenlight app. At the same time parents can establish spending limits and receive real-time purchase alerts to help them monitor card activity. The addition of the Greenlight Family Cash Card means that Greenlight’s in-app financial literacy game, Level Up, now features instruction on the responsible use of credit, as well.

Greenlight subscription plans start at $4.99 a month. Other plans are available that add features such as identity theft, purchase, and phone protection (Greenlight Max for $10 a month), as well as family location sharing and crash detection (Greenlight Infinity for $15 a month). The Greenlight Family Cash Card is issued by First National Bank of Omaha.

In an interview with TechCrunch, Greenlight co-founder and CEO Tim Sheehan highlighted the company’s 3% cashback, Level Up financial literacy game, and parental controls as a trifecta that trumps offerings from other credit cards – including those that cater to families and youth. “Nobody has all three of these features,” Sheehan said.

Headquartered in Atlanta, Georgia, Greenlight was founded in 2014. The company has raised $550 million in funding, which includes a $260 million Series D round in 2021. This investment gave the fintech a valuation of $2.3 billion. The following year, Greenlight unveiled its Greenlight for Classroooms offering, a web-based financial literacy library. The library includes more than 100 animated videos, and a bank of thousands of vocabulary words and test questions. Additional features include quizzes, ideas for individual projects, discussion activities, and a teacher’s guide. Aligned with K-12 national standards, Greenlight for Classroom is available to schools, teachers, and students across the U.S. for free.

We caught up with Taylor Burton, co-founder of Till Financial, one of the many companies that are innovating in the youth financial wellness space. The Massachusetts-based startup, launched in 2018, introduced its free, collaborative family banking platform this spring. At the same time, Till secured $5 million in funding in a round led by Afore Capital – which is where our conversation begins.

You’ve just secured a significant investment. What does the funding mean for Till?

Taylor Burton: It means an increased ability to positively impact the trajectory of kids as they prepare for launch. The group of investors that we assembled share our vision for how collaborative family banking should look—we are excited to continue to add more supporters as we scale our platform.

We are thrilled to have the support of like-minded investors including Elysian Park Ventures, Pivotal Ventures with Magnify Ventures, Afore Capital, Luge Capital, Alpine Meridian Ventures, The Gramercy Fund, SM Ventures (the family office of the founders/CEOs of Stadium Goods) and Lightspeed Venture Partners’ Scout Fund. Also participating were angel investors such as the founders of fintech Petal, the founders of alcohol marketplace Drizly, the president of Transactis, and the president of 1800Flowers.

We will be adding to our high-quality team in all areas that support our customers through their journey on Till. Marketing that provides the content to help families have the first “real” conversation about money. Development to accelerate our vision of what our product can be, plus integrate all the great ideas coming out of the Till user community. And customer success to ensure that a Till family is maximizing its experience on the platform.

How does Till help empower children to become smarter spenders?

Burton: Till is designed to encourage open and honest discussions between parents and their kids. The goal is to help kids learn by doing and to gain confidence in spending decisions. We do this in the following ways:

The right tools: Till equips kids with their own bank account, digital and physical debit cards, and goal-based savings tools.

Emphasis on community: A child can easily set up a goal on the app that they can use to start saving toward and give family members (such as grandparents, other family members or community members) the opportunity to help pitch in. This gives members of the child’s network an opportunity to support them towards their goals. After all, it takes a village, and Till helps facilitate that.

Visualizing financial responsibility: Kids can also set up recurring payments for different ongoing responsibilities or subscription services that will get them used to the concept of paying bills on a timely basis.

That being said, along with teaching kids valuable saving habits, we want to be advocates for kids to feel empowered in their spending decisions just as much, if not more. Parents and the traditional legacy banking options tend to focus mostly on a child’s savings. At Till, we believe that we need to prioritize preparing kids to be smarter spenders, while supporting them through savings and investing. On our platform, kids learn to spend with intention and purpose, while parents gain confidence and trust based on transparency and accountability.

What is unique about the method that Till Financial uses?

Burton: One unique part of the app are the financial agreements which allow kids to have greater agency and responsibility over their money. Parents can create agreements and tasks that encourage kids/teens to understand the value of every dollar. By visualizing the financial responsibility of earning every allowance, they are able to be active participants in their financial journeys.

Additionally, as families are more spread out over time, Till reinforces the impact of community by leveraging family, friends, and members of their close networks to help the child reach their financial goals. Till also offers merchant partners curated with kids’ interests in mind. As we continue to grow, we will have more opportunities to add on to this list and provide kids with more incentives.

How does Till make money?

Burton: Till aims to be “first in wallet” and “only in wallet,” unlike other card offerings targeted at adults fighting to be “top of wallet.” Till captures value (revenue) when we deliver value to our customers. Unlike other legacy banks—and even some early digital ones that often time charge monthly or subscription fees—Till is free to all consumers, making us accessible to all users.

Till earns revenue in three ways: We earn an interchange fee (like all debit/credit cards) for facilitating the transaction between our users on vendors. There are also affiliate fees. We want our user’s dollars to go farther. We are negotiating both broad and proprietary relationships with the vendors that our kids spend with each day. Our kids get access to discounts and exclusive access and we get a percentage when the kid does choose to make a purchase. Everyone’s a winner: the kids receive a steeper discount on items that they were already planning to buy, while the merchant gains a new customer.

Lastly, there’s origination. Consumers’ needs change over time and our ability to create the best outcomes for our families depends on focus. It is not Till’s intention to be a kid’s forever bank, just their first bank. With that in mind a Till kid should be treated with the respect that they have earned on our platform for positive financial decisions at launch. When the time comes for kids to leave the house and strike out on their own, Till introduces them to our launch offers market. There, they can receive preferential treatment on loans, credit cards, and adult debit/checking. The adult financial institution gets a better, more valuable client; our consumer receives the advantages they deserve for being of sound financial mind; and Till receives an origination fee.

How important are partnerships to Till’s business plan?

Burton: Till’s merchant and venture partners are interwoven into our business plan to seamlessly offer kids/teens and their families the best resources to develop responsible spending habits. As Till continues to expand their merchant partnerships, kids will have greater access to exclusive offers that they can use on items that they are already planning to purchase. These key partners include top tier brands that kids already shop at such as Adidas, Stadium Goods, and Dick’s Sporting Goods. And, of course, we also believe that the partnerships with our investors are a key component of the continued success of Till. We want our investors to share the same mission of empowering the next generation of economic actors.

What in your background gave you the confidence to tackle this challenge?

Burton: For starters, all three of us co-founders are dads and we’ve all had our share of financial awakenings whether with our kids or ourselves personally. That being said, Till is not just for us, but for the 50 million families that know there is a better way to raise a family; where financial conversations are collaborative not confrontational, and where all of our kids are better prepared for the modern economy.

On the company-building front, the founding team brings together everything needed to build a valued and valuable company. I bring expertise in direct-to-consumer products in a heavily regulated market (Drizly and alcohol delivery), coupled with innovation success in payments rails and merchant partners integration (PayPal and card-linked offers). Tom (Pincince) came to me with this idea after selling his third company. This serial entrepreneur has built a career by finding gaps and opportunities created by market movements and technology changes. And then Brian (Chemel), a multi-time technical founder equipped to marry the best of the old and the new to build a secure and scalable infrastructure backing a delightful and engaging user experience.

Looking back on 2020, what is your biggest professional takeaway?

Burton: We learned to be comfortable with being uncomfortable. COVID-19 impacted people’s businesses differently and when you layer in a fundraise and being an early stage start up, that can either make you or break you. In our case I think it really codified our commitment to our mission and vision and has ultimately put us in the position we are in now.

What can we expect from Till over the balance of 2021 and beyond?

Burton: Our first job is to become an integral part of millions of families’ every day financial activities. We do this by building an engaging platform that delivers both economic and social value. Along the way you will see Till add features that help parents and kids understand where they are on a financial journey and how their decisions can be rewarded by access to opportunities, experiences, and offerings. We are here to serve our users who are already helping us set priorities and guide us to new features and functionality. We are already getting requests for collaborative investing and philanthropic giving features, for example.

We are thinking big because the market is massive– there are currently 50 million pre-banked kids in the U.S. and yet, the average middle-class family in America spends $284,570 per child by age 18. At Till, we believe kids are a major economic force, as $18 billion per year is given by parents to children in the form of an allowance (mostly as cash). We recognize that they are influencers on larger family decisions, such as cars, vacations, etc. By putting the spending power back into the hands of young people, we want to be the driving force that replaces awkward family conversations about money with real actions and experiential learning.

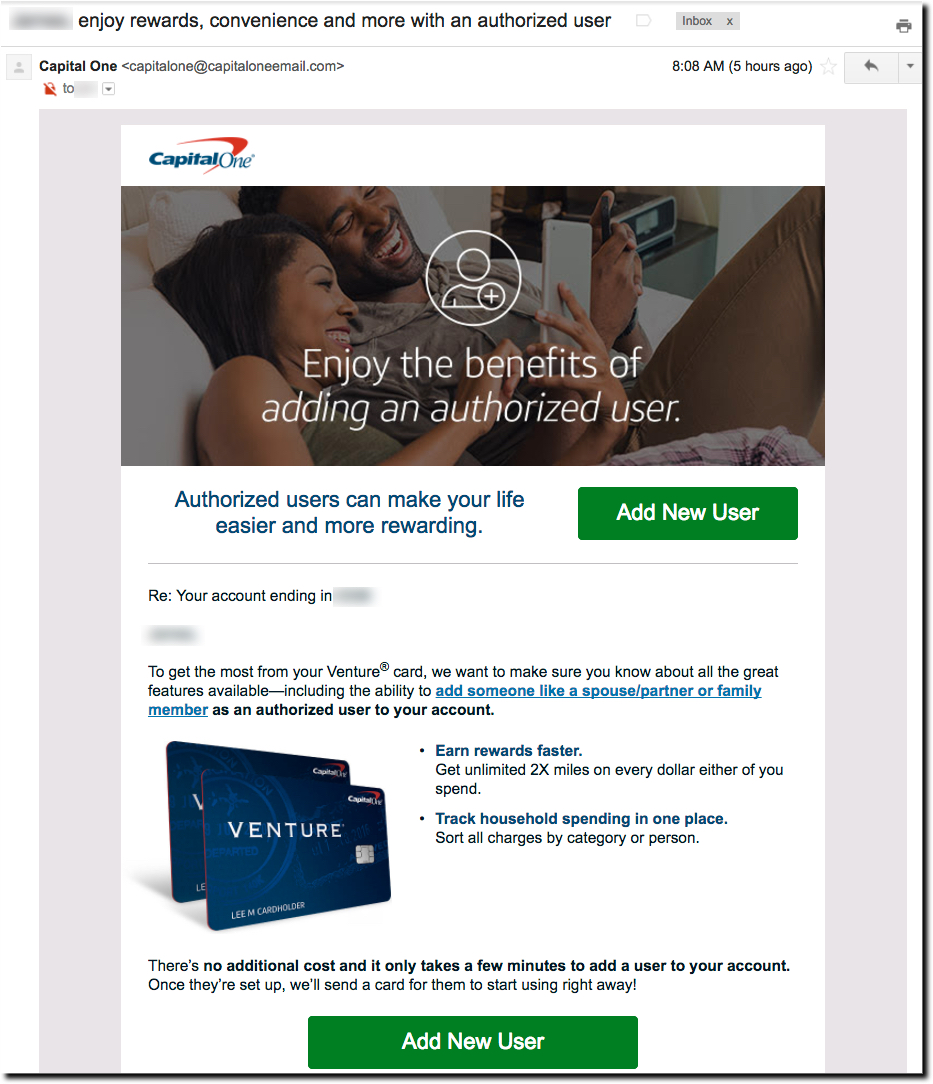

By my calculations, I’ve received more than 25,000 emails from financial institutions. But I don’t recall ever getting one, outside of an onboarding message, encouraging me to add an authorized user to my credit card account (see above). So congratulations to Capital One for finding something new to talk about in the last week of the real summer.

And it makes sense to push for new authorized users. It’s win-win. More revenues for the bank and improved convenience for the customer.

Case in point: I’ve been meaning to get a card for my son in college, so I’ll go with Capital One instead of my other options. It will cost the bank $2 for the chip card and mailer, maybe a few bucks for the credit check (though honestly, they don’t need one as I’m backing his spending) and some misc onboarding expenses. But with near-zero additional credit risk, most of the new interchange (and potential revolving) revenues will go right to the bottom. And they have a much better opportunity to turn my son into a long-time customer if they have a card in his hand now.

Bottom line: Capital One could improve the user experience once you click through the email (seeUX analysis here). But overall, it’s a good effort.

Author: Jim Bruene (@netbanker) is Founder & Senior Advisor to Finovate as well as Principal of BUX Advisors, a financial services user-experience consultancy.

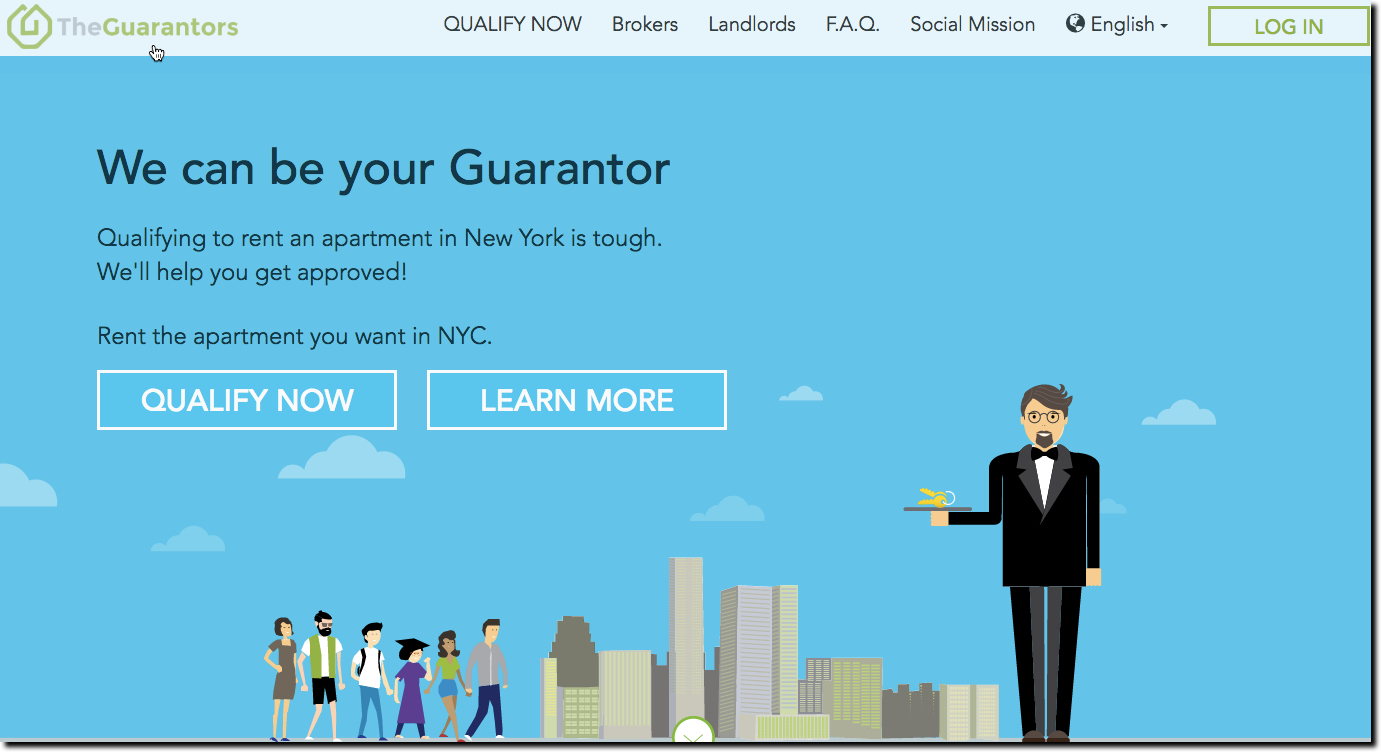

As a blogger/analyst/entrepreneur, it’s a mixed blessing when someone delivers on a market need you’ve been ranting about (here and here). You feel vindicated and you have a blog post that writes itself, but it knocks one thing off the top of your businesses-to-start list.

So begrudgingly, I introduce you to TheGuarantors, an N.Y.C.-based startup that is stepping up to meet the needs of renters trying to qualify for an apartment in New York City, and eventually other markets such as Boston, Chicago and California. I was directly involved in one such qualification excercise two months ago.

The company essentially acts as your parent (if your parents could fill out reams of paperwork within 12 hours, were extremely well heeled and backed by surety bonds), stepping in to co-sign and guarantee your rental agreement. To make landlords trust the stand-in parent arrangement, the startup backstops its guarantees with insurance from The Hanover Insurance Company. If the renter does not fulfill the terms of the lease, The Guarantors, makes the landlords whole. It is a brilliant idea, and perfect for financial institutions to license or build themselves.

The only problem is cost. Depending on risk profiles, The Guarantor charges U.S. citizens 5% to 7% and international renters 7% to 10% of the annual rent, about 3 to 4 weeks’ rent to backstop a 12-month lease; leases up to 18 months are a higher rate). But by eliminating deposits that can equal that amount or more, it can be cash-flow-positive to the renter. Though, unlike a deposit, that money is gone for good. So it doesn’t help first-time renters without the initial cash surplus of two-month’s rent. However, a financial institution offering the service could loan the renter all or part of that. There is no cost to the landlord.

The company, currently operating in NYC, is open only to renters with a 630 or higher FICO score and annual income at least 27x the rent. Alternatively, the company allows co-signers with at least 45x the monthly income, or liquid assets of 75x the monthly rent, to guarantee the guarantee. Applications are approved with 12 hours.

The company launched in 2014 and spent 18 months nailing down the insurance deal with Hanover. It has taken a seed investment of an undisclosed amount from nine investors (50 Partners, Alven Capital, Arnaud Achour, Fides+Ratio, Kima Ventures, Partech Ventures, Residence Ventures, Silvertech Ventures and White Star Capital).

Bottom line: Renter financing/assistance is a promising new lending/customer service for financial institutions. You not only get new customers, new loans, new checking accounts, a foothold in the millennial market, a unique service to offer employers, satisfied renters (and their parents), but also become a local hero with write-ups in every newspaper, blog, and housing forum in your market. And, with a phone call or two, you will be on the nightly TV news every fall when it’s “apartment hunting” season.

Contact The Guarantors now and offer to be their first distribution partner outside New York City, or their first strategic investor. And if you are Wells Fargo, Capital One, American Express, or Chase, just buy them outright already.

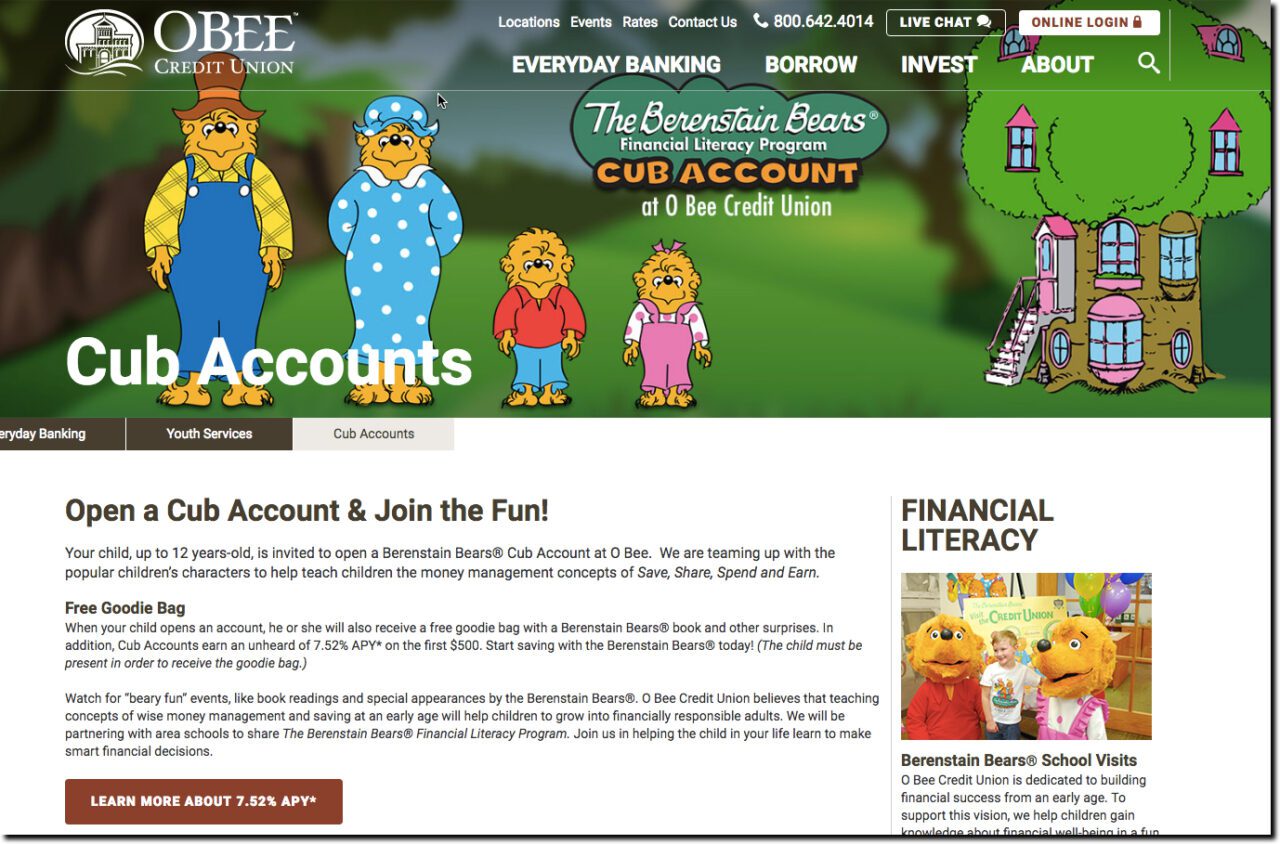

I thought I’d left behind Berenstain Bears 15 years ago when my youngest graduated to Animorphs books. But they made an appearance today when I discovered how they are helping kids get involved with saving and managing money. And before you dismiss their appeal, did you know the Bears have sold 300 million copies in a 54-year run which includes 300 titles!

Three years ago, Franklin Mint FCU, through its CUSO CUNFL, developed a financial literacy program based on the series. It includes a book written by none other than Mike Berenstain himself, called Berenstain Bears Visit a Credit Union. It is licensed to other credit unions to appeal to grade schoolers.

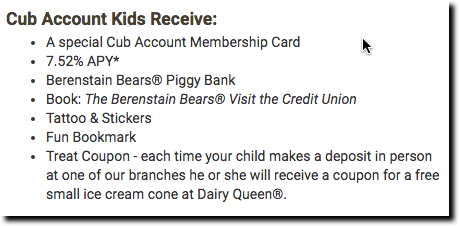

The book is in use at a number of credit unions, but none more prominently than O Bee FCU in the Tacoma, Washington, area. Its Berenstain-themed Cub Account for under-12 members includes a 7.5% rate on the first $500 in savings, an important feature so you can use something other than pennies to show your youngster the benefits of savings. More impressive for the kids, every branch-deposit earns a free Dairy Queen ice-cream cone coupon (see inset for full list).

O Bee also offers a classroom financial literacy program with visits from the bears themselves, along with a jumbo version of the book to read to the class.

O Bee Credit Union’s Cub Account landing page

Bottom line: Efforts aimed at banking the kids of your customers are a clear win-win. It’s the right thing to do; kids, and their parents, need these services. And it helps keep both the child and their parents as customers for the rest of their lives. See our previous posts for more examples.

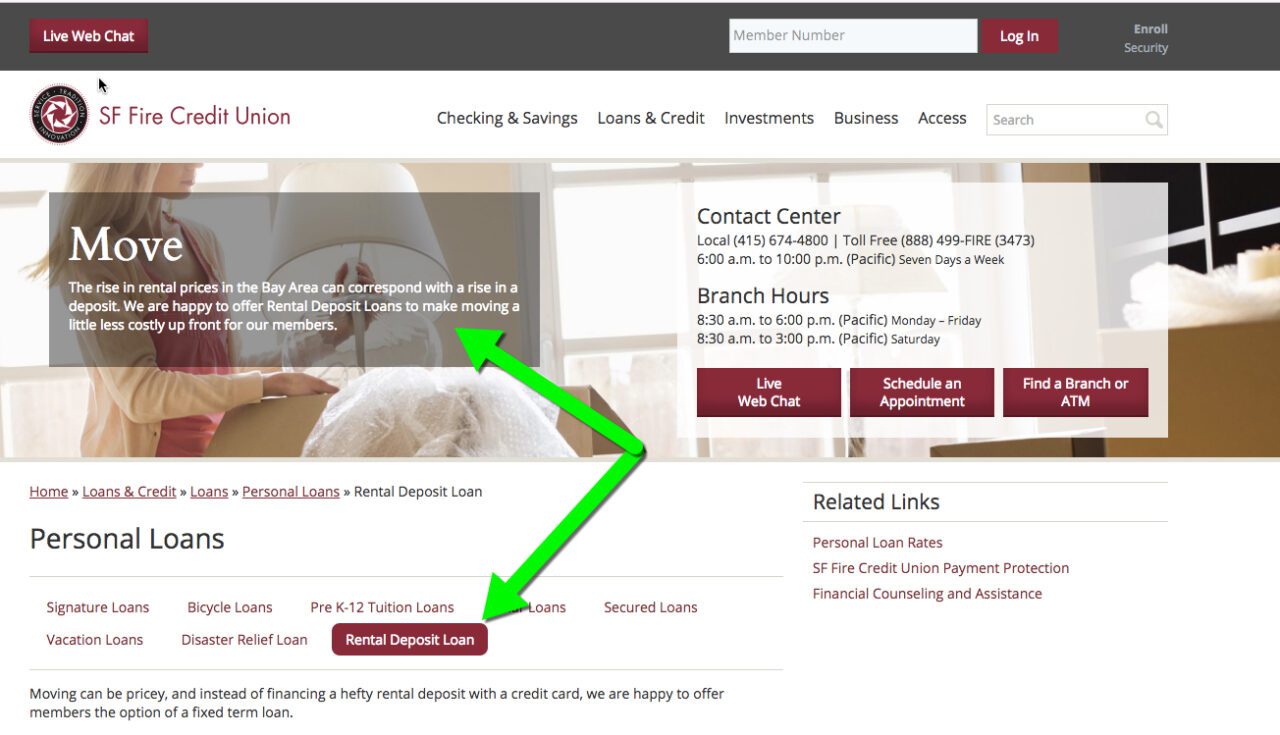

SF Fire Credit Union offers loans up to $10,000 to cover rental expenses

Looking to provide real value to younger customers, especially the children of your core deposit base? Help them get started in the rental game. I have five family members who have recently rented in the Seattle and Los Angeles metro areas, and it’s a brutal seller’s market for apartments. Landlords are picky and require financial assurances similar to, or even more stringent, than a mortgage (pre-2008 anyway).

For example, as a co-signer on my son’s lease, I was asked to provide two years of tax returns despite the fact that he has a good job lined up (albeit not until after graduating in May) and sufficient current resources to pay the monthly tab. And then there’s the initial cash outlay (in his case, $4,000 in certified checks). All this is quite daunting for new renters or anyone looking to make a move.

Where financial problems exist, banks and credit unions have opportunities. Ideas include:

Make it easier to save with a goal-based account: First-time renters often don’t realize the financial cost of getting started in an apartment. Offering a systematic savings program to help build the required balance is a win-win. For extra credit, provide a bonus when certain milestones are met and/or allow parents, aunts, uncles and grandparents to contribute as well. Simple, Moven, Mint and most PFM platforms offer goal-based savings; most financial institutions do not.

Provide rental-deposit loans: If savings won’t cover it, offer a modest installment loan with an easy co-sign option. These small loans can also help build a positive credit history. Though rare, a few U.S. credit unions offer small loans specifically to cover rental deposit, first/last months’ rent, utility deposits, and so on, but it’s not typically something you see at banks. See the SF Fire Credit Union page above for an example.

Help students in their apartment/roommate hunting: Team up with companies helping students and others find a place to live. For example, Rent College Pads, recently raised $1 million.

Offer renter’s insurance: A low-cost, but valuable bit of peace-of-mind for young renters who can ill-afford to replace stolen or damaged items.

Encourage more low-cost housing options: In tight rental markets, use your resources to find spare rooms within the community that could house students or others needing housing. A bank or credit union could offer loans to remodel or build new rental spaces.

Bottom line: One of the best ways to cement a long-term relationship is to help someone (or their kids) find a place to live, and provide a means of handling the initial financial burden. I encourage financial institutions, and their fintech partners, to make a home for this strategy in your 2017 gameplans.

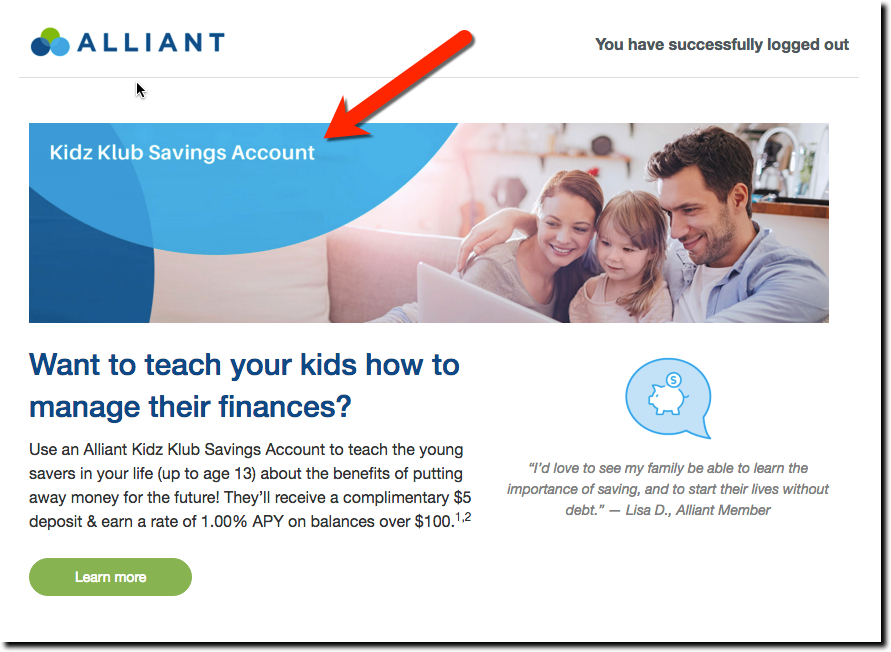

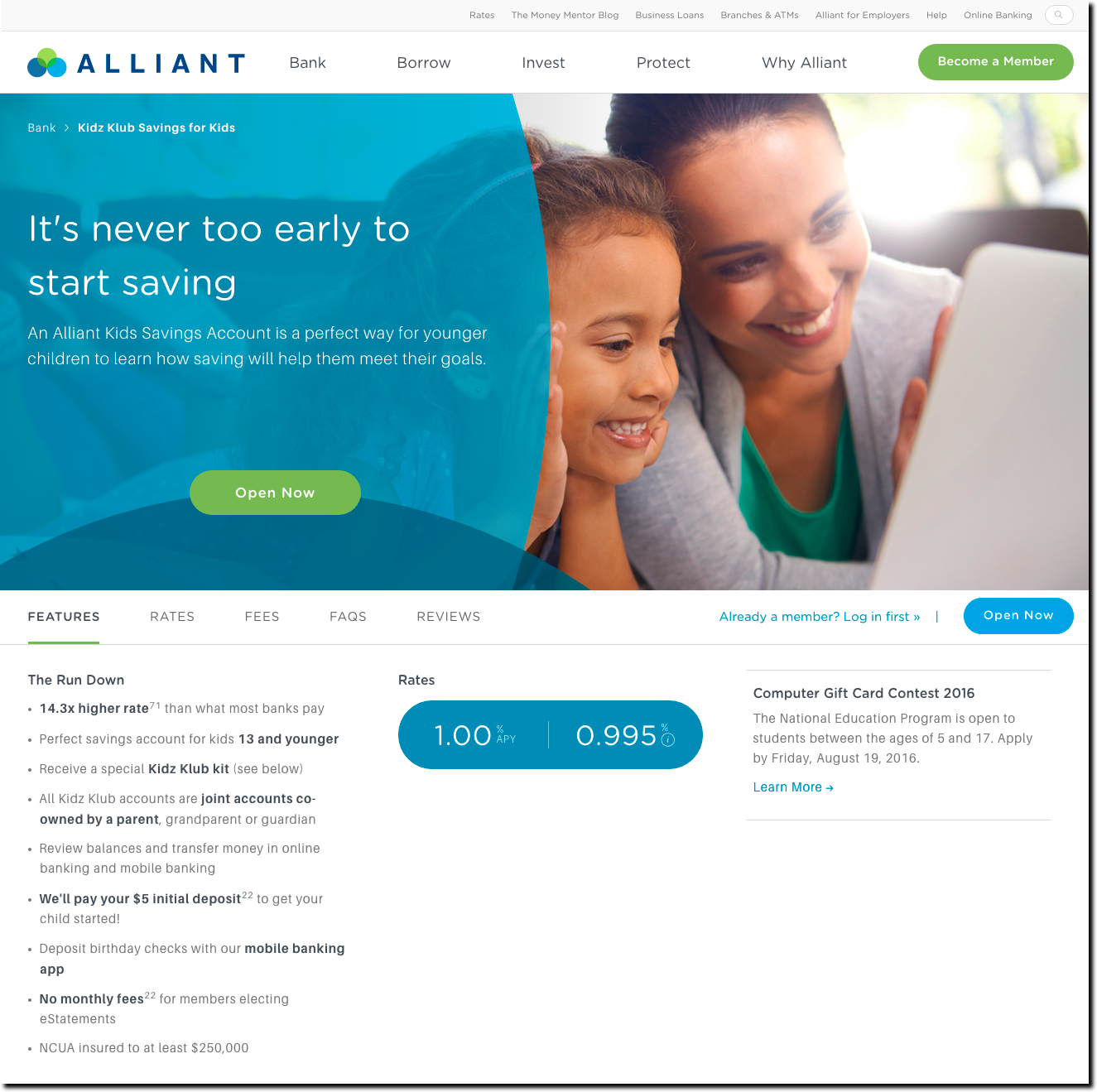

The logoff page that pops up following a secure session is one of the choicest real-estate parcels in a financial institution’s inventory. Typically, this logoff page is seen on a desktop pc, but the same opportunity exists on mobile. Earlier this summer (late June), we spotted Chicago-based Alliant Credit Union pitching its Kidz Klub savings account with a 1% APY (adults get the same rate).

Bottom line: The logout screen is well-designed and the green call-to-action button is easy to see. The button leads to an attractive Kidz Klub landing page (see screenshot below). While The Klub is a savings account that mirrors rates available for adult members, the thrill for kids is that each Kids Klub member receives an individual member’s card and account kit.

Given that today’s 10-year-old could be a bank/CU customer for the next 70 or 80 years, it makes sense to cater to members’ children with a dedicated account. But it needn’t be a fancy standalone account. The primary goal is to get kids (and their parents) to start saving together and that can be done with a repurposed basic savings account.

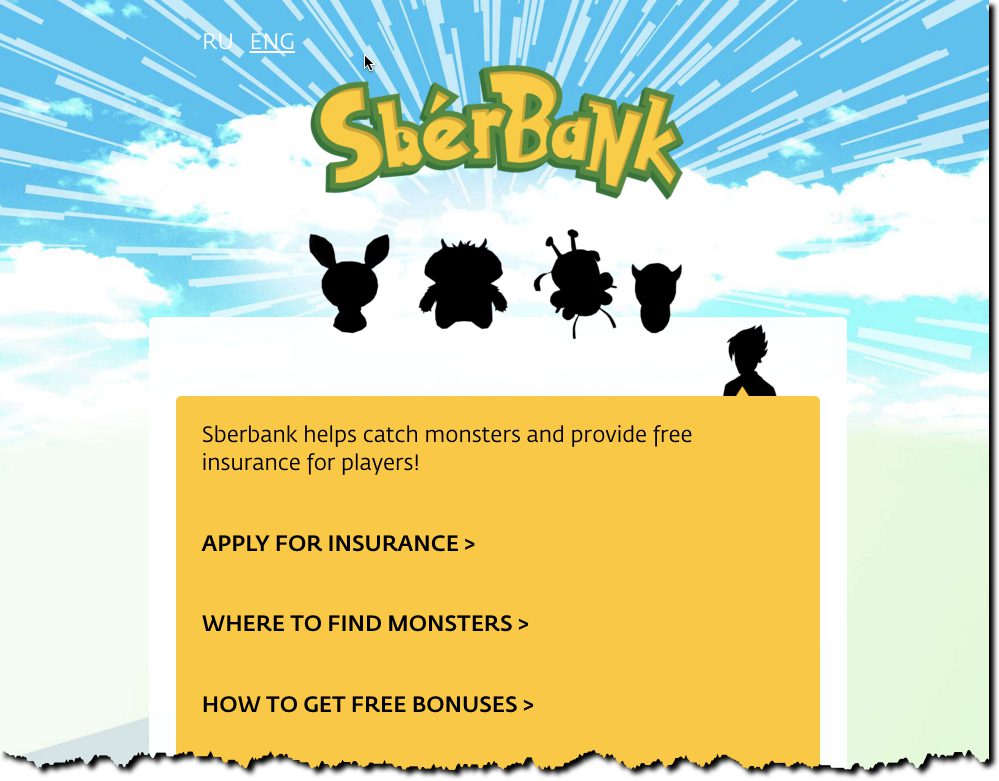

The Pokemon Go craze doesn’t surprise me at all. Both my boys grew up with the little beasts so I get their appeal, especially with the AR boost. But what I didn’t expect to see were multiple financial institutions jumping on board, during the first week no less. And one, SberBank, that would pull off a clever product tie-in that might actually have a positive ROI.

Coinciding with the official countrywide Pokemon Go release (expected any day now), the Russian bank and insurer (and Finovate alum) is offering free accident insurance for anyone while they are playing the game. Users must register with the bank first (nice monetization through lead-gen) and provide evidence in the case of a claim (and some big costs).

The bank plans to use special game pieces called Lures, to drive players to branch locations. They are also providing additional bonuses for anyone catching a Pokemon in the branch.

SberBank created a special website just for the promotion at SberBankgo.com which explains the offer in both Russian and English (screenshot right). In addition, they’ve added a Facebook page to support the promotion (screenshot above).

While the free insurance promo is probably too costly to work in litigious U.S. markets, banks can still use the game to drive traffic. For example, Florida’s CenterState Bank has already experimented with lures at its branches (see full writeup on its promotion). Or if you just want to have a little fun on social media, drive your branded truck into the background while capturing one of the little critters. Kudos to CACL FCU in Pottsville, Pennsylvania, for acting on that first.

Bottom line: Jumping on the Pokemon Go bandwagon isn’t going to replace anything in your 2016 marketing plan; however, it could be a low-cost way to:

Provide interesting content for your social media outlets

Gain some free PR (limited to first bank/CU that does it in a given market)

Provide leads for certain products (youth bank accounts, insurance, mobile banking)

Back when my kids were able to save—both are in college now, so that’s not happening—ING Direct and others offered interest rates that actually created an incentive to save. My oldest even enjoyed 5% rates for a while, quite helpful in showing how the “free” $5 to $10 per month he earned at the bank grew his total over time.

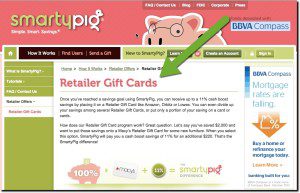

But today’s middle-schoolers and younger teens have come of age in an absurdly low interest-rate environment (see note 1), with little chance to experience the joy of compound interest. SmartyPig (inset, note 2) and others have created savings bonuses centered around merchant gift cards. That’s a clever way to add value, but it can also send a mixed message, “Hey Junior, save $250 and you’ll get an extra $5 if you spend the whole thing at Best Buy.” For parents who’d like their kids to hold onto that cash (at least until college), few options exist, other than bribing your kids with parent-funded bonuses.

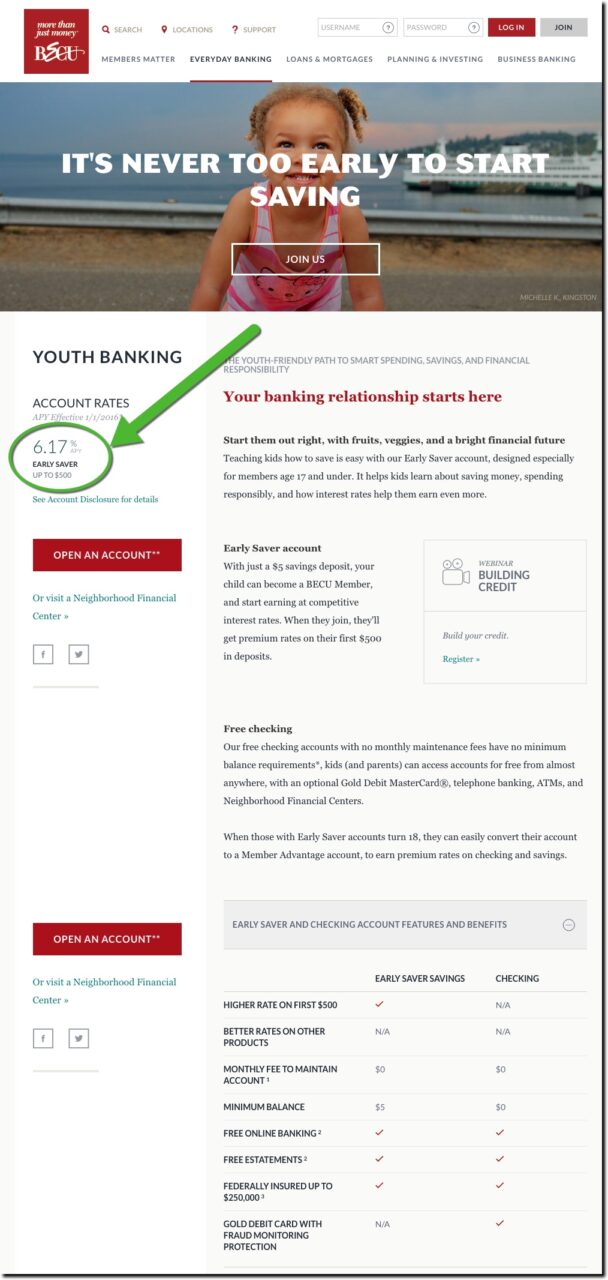

But a few financial institutions have addressed the forlorn kiddos and their disappointed parents by dramatically boosting the rates paid on the first few hundred of a balance. For example, in the greater Seattle area, BECU pays 6.17% on the first $500 deposited in its Early Saver account (see screenshot below). Granted, the rate reverts to pretty much zero (0.1%) after that, but kids at least get enough interest every month ($2.50/mo on $500 balance) to make it feel like it’s worth holding the money at the credit union (note 3).

Bottom line: Your customers’ children are your future. It’s worth investing in services to keep them at your FI for the next decade or six. If the $30 annual subsidy is beyond your budget, enable parents to pay for the rate bonus. Let parents “boost” the interest paid on their child’s account as much as they want. To provide an extra incentive, you could match parental contributions up to a certain point (e.g., $10/year).

———

BECU Youth Savings landing page (link, 11 Jan 2016) Note: BECU has elevated Youth Banking to one of six choices on its Everyday Banking primary navigation item.

———–

Notes:

1: For example, Bank of America currently offers 1 basis point interest on a child’s account, which means your child’s $1,500 average balance earns 1 cent per month!

2. Social Money, owner of SmartyPig, was acquired by Q2 Holdings last month (Dec 2015).

3. BECU offers a similar boost for the first $500 banked by 18+ year-old members as well, but the rate is only 4%.

4. Off topic: BECU has done a great job optimizing its homepage for responsive design. Open it in your browser and then shrink the window and watch how it resets. Very nice!

A major consequence of ubiquitous digital banking will be a long-term improvement in customer retention, at least for the “primary” bank/checking account. Digital natives will perceive little need to change banks as they move from home to college and then to multiple jobs. Assuming you keep them satisfied and connected to family members, today’s 15-year old might stick with their primary bank or credit union for seven or more decades.

But you can’t retain a customer who never opens an account.

That’s why I believe FIs should do their best to get an account started for every child in every customer household, probably bundling them into a “family wrap account” which could carry a premium fee (though the individual kids’ accounts should probably come at no additional fee).

And the family account needs to be fully connected and in sync with the parents, guardians, and other current and potential family members. That enables real-time money movement along with expense tracking. And as children grow into adulthood, the accounts should be able to be easily be converted into their own family account, and the cycle can be repeated with their kids.

There’s a big, missing piece with today’s money management (aka PFM) offerings:

Age appropriateness

What I mean is that most FIs offer a one-size-fits-all mobile app and that just won’t cut it going forward. As development costs drop (see Building it Out, below), it will be easier to cost-justify tightly segmented apps. One of the better examples (from the desktop), is CapitalOne 360’s Teen Money a program it inherited from ING Direct (which launched it exactly four years ago with a $10 million ad campaign).

How will this multi-app trend manifest itself? One of the more likely initial phases will be segmenting by life stage. For example, here’s a common example of 10 stages, along with key money-management issues along the way:

Active retirees: asset management, estate planning

Homebound seniors: sharing control with kids, health insurance management, estate planning

All of those segments will likely have their own app or at least a way to easily customize a general app in a way that syncs with their needs without the clutter typical of many banking websites (though they are getting much better as building for mobile (responsive design), demands prioritizing features/content.

Building it out

Given the 6, 7 and even 8-figure costs of major mobile initiatives, building 10 apps may seem ridiculously expensive. And it would be if it weren’t for cost savings enabled by third-party and SaaS services fed through APIs, a subject we touched on recently in a post about the coming Golden Age of Fintech APIs.

If you are willing to forgo branding, you could provide age-appropriate apps for virtually no cost. For example, some smaller banks gladly refer their customers to Mint for budgeting/money management help or Credit Karma for credit management. It’s not a bad strategy. Sure, they’ll see targeted financial advertising, but that’s not going to matter if you provide a valuable service.

But we expect most banks and credit unions will eschew custom development and choose a full white-label solution such as MX, Backbase or dozens of others. Or alternatively, go with a hybrid co-brand, such as BancVue’s KasasaorFamZoofor the teen/pre-teen crowd.

——

We’ll be looking at these issues and more at our second annual financial services developers event,FinDEVr, in October.

The book is in use at a number of credit unions, but none more prominently than

The book is in use at a number of credit unions, but none more prominently than