This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

In today’s instant digital economy, providing your customers with a unique experience can translate to a crucial advantage for your firm. Your payments strategy plays a critical role in this.

Join this webinar and discover how to design a customer-centric payments strategy driven by choice, convenience, and speed.

Key takeaways:

Understanding Customer Needs: Learn how to identify and analyze the specific needs and preferences of your customers when it comes to payment options.

Seamless Payment Processes: Explore strategies for creating smooth and frictionless payment experiences that enhance customer satisfaction.

Discover: Find out how to personalize payment experiences to build stronger customer relationships and loyalty.

A look at the companies demoing at FinovateFall in New York on September 9 and 10. Register today using this link and save 20%.

ComplyCo

ComplyCo offers the visibility and control needed to effectively oversee digital environments, leveraging end-user session recordings to support monitoring and observability for non-technical teams.

Features

Provides investigative controls for an organization’s digital environments

Includes population-based monitoring

Offers version control and effective testing

Who’s it for?

Financial institutions offering products of their own or through partnerships with fintechs in a digital environment.

FinTech Insights

FinTech Insights is an AI-powered competitive analysis platform for banks and fintechs. By analyzing digital banking offerings, FinTech Insights enables faster UX research, product releases, and innovation.

Features

FinTech Insights GPT allows users to:

Receive actual and actionable insights in seconds

Streamline product research processes from months to minutes

Make faster, bullet-proof decisions with accuracy

Who’s it for?

High-street banks, credit unions, community banks, regional banks, challenger banks, fintechs, and digital banking providers.

Quavo Fraud & Disputes

Quavo Fraud & Disputes is the leading provider of innovative dispute management solutions for issuing financial organizations. Launch is an all-new offering of their proven dispute management system.

Features

Requires zero onboarding time for immediate use

Offers an affordable base product that scales with FIs

Fully compliant with regulatory and network standards

Delivers highly automated dispute management systems

Who’s it for?

Banks, fintechs, processors, and credit unions of all sizes, and any organizations subject to regulation E/Z dispute resolution or serving institutions subject to it.

Scamnetic

Scamnetic’s everyday solution helps consumers detect every type of scam in real-time, removing human error from the equation. Their patented, AI technology can be easily integrated into enterprise platforms.

Features

Scan&Score™: Auto or quick scan with real time message validation

IDeveryone™: C2C authentication and verification before payment

ScamIntervention™: Proactive call center support pre-or-post scam

Who’s it for?

Banks, credit unions, payment providers, small-to-medium sized businesses helping their customers, members, and employees stay safe, especially from scams using their name.

Setuply

Setuply is an AI-powered client onboarding and lifecycle management platform for B2B solution providers purpose-built to accelerate revenue recognition and profitability.

Features

Delivers real-time insight into the revenue at stake to prioritize work

Offers scalable and repeatable onboarding processes

Increases client engagement and collaboration

Who’s it for?

B2B service and implementation providers.

Telesign

Telesign delivers their 2024 Fraud Protection Insights with PowerBI.

Features

Learnings from Telesign, the DI and Communications Security leader Proof of Concept data

Delivers 2024 fraud vector insights

Over 200 investigations analyzed since September 2023

Who’s it for?

Banks, credit unions, fintechs, and e-commerce SMB and enterprise businesses.

Vine Financial

Vine Financial is a cutting-edge commercial lending platform that is highly configurable and supports the entire loan lifecycle. With AI, it automates everyday tasks that tie up employee time.

Features

Offers AI-assisted document import, financial analysis, and document generation

Includes extensive configuration capability to support each FI’s workflows

Eliminates the need for an expensive third-party CRM

Who’s it for?

Banks, credit unions, private lenders, venture capitalists, private equity, and any other industries requiring financial analysis and due diligence.

The summer heat usually comes with a slowing of news activity, and while this is generally still holding true this summer, there have been some notable merger and acquisition activity throughout the past few months.

This season, the fintech landscape has had its fair share of strategic moves, as companies look to expand their capabilities, enter new markets, and expand on their offerings. These acquisitions are not just reshaping individual companies but they are also working to build out what the future of financial technology will look like.

As venture capital funding has dwindled over the past few years, the fintech sector has had to get creative in staying afloat. That may be one reason why we are seeing a growth in deal numbers. Let’s dive into the top 10 fintech acquisitions so far this summer.

Pluto acquired by Robinhood

Robinhood, a commission-free trading platform that aims to democratize finance acquiredPluto, a fintech startup focused on personalized financial planning and investment tools.

Deal Details: Financial terms were not disclosed. The deal is expected to close in Q3 2024.

Impact on Industry: The deal may encourage other trading platforms to improve their advisory services, increasing competition.

Future Outlook: Integrating Pluto’s technology will help Robinhood offer personalized financial advice, boosting user engagement and retention.

Theorem acquired by Pagaya

Pagaya, an AI-driven asset management firm that focuses on portfolio optimization through machine learning and big data acquiredTheorem, a provider of financial analytics and modeling tools.

Deal Details: The specific financial terms of the deal remain confidential.

Strategic Rationale: Theorem will strengthen Pagaya’s AI and data analytics capabilities, resulting in robust investment strategies.

Impact on Industry: Pagaya’s purchase highlights the importance of AI in asset management, pushing competitors to innovate.

Future Outlook: Pagaya’s platform will demonstrate enhanced analytical power, offering more value to institutional clients.

Aion Bank acquired by UniCredit

UniCredit, a leading European commercial bank that offers a wide range of banking services, acquiredAion Bank, which is known for its digital banking services and innovative financial products.

Deal Details: Financial details of the deal were not disclosed.

Strategic Rationale: Aion Bank will help UniCredit expand its digital banking capabilities and customer base.

Impact on Industry: The deal will help to increase competition in digital banking, driving more customer-centric services.

Future Outlook: Integrating Aion Bank’s technology will enhance UniCredit’s digital offerings and expand its market reach.

Envestnet acquired by Bain Capital

Bain Capital, a private investment firm that focuses on private equity, venture capital, and credit, acquiredEnvestnet, a provider of integrated portfolio, practice management, and reporting solutions.

Deal Details: The deal is valued at approximately $4 billion.

Strategic Rationale: Envestnet’s long-standing expertise will help Bain Capital enhance its capabilities in financial technology and wealth management solutions.

Impact on Industry: The move will bring Envestnet into the private sector.

Future Outlook: Bain Capital’s acquisition may fuel demand for other private equity firms to buy out wealth management fintechs.

Salt Labs acquired by Chime

Chime, a digital bank known for providing fee-free banking services, acquiredSalt Labs, an employee savings and rewards program.

Deal Details: Financial terms were not disclosed, but some sources report that the deal could close for as much as $173 million after Chime provides an up-front payment of $14 million.

Strategic Rationale: Salt Labs will enhance Chime’s offerings by integrating employee savings and rewards programs.

Impact on Industry: Integrating Salt Labs will help Chime promote financial wellness and engagement among employees, setting a new standard for digital banking services.

Future Outlook: The combination of Salt Labs with Chime Enterprise will expand Chime’s client base through employer channels.

Rooam acquired by American Express

Financial services giant American Express has acquiredRooam, a mobile payment and digital tipping platform for the hospitality industry.

Deal Details: Financial specifics were not disclosed.

Strategic Rationale: American Express is expected to expand its mobile payment capabilities in the hospitality sector.

Impact on Industry: The purchase will fuel demand for more innovation in mobile payment solutions that increase convenience for users and businesses.

Future Outlook: Integrating Rooam’s technology will improve American Express’s digital payment offerings and customer experience.

Strategic Rationale: Funding Circle will expand iBusiness Funding’s lending capabilities and customer reach.

Impact on Industry: The move will help strengthen small business lending options, ultimately supporting economic growth and entrepreneurship.

Future Outlook: Integrating Funding Circle’s platform into iBusiness Funding will enhance iBusiness Funding’s lending solutions and expand its market reach.

Invoiced acquired by Flywire

Flywire, a global payments enablement and software company, acquiredInvoiced, an accounts receivable automation platform.

Deal Details: Financial specifics were not disclosed.

Strategic Rationale: Invoiced is expected to enhance Flywire’s payment solutions by adding advanced accounts receivable automation.

Impact on Industry: The deal promotes efficiency in payment processing and receivables management solutions.

Future Outlook: Flywire will benefit from integrating Invoiced’s technology, which will offer comprehensive payment and receivables solutions and improving cash flow management.

Screena acquired by ThetaRay

ThetaRay, a provider of AI-powered transaction monitoring technology, has acquiredScreena, a cybersecurity firm specializing in fraud detection and prevention.

Deal Details: Financial terms were not disclosed.

Strategic Rationale: The deal will strengthen ThetaRay’s fraud detection capabilities with Screena’s advanced cybersecurity technology.

Impact on Industry: The move enhances current fraud prevention measures, which will increase security in financial transactions.

Future Outlook: Integrating Screena’s technology will improve ThetaRay’s AI-driven fraud detection and prevention solutions.

LemonSqueezy acquired by Stripe

Financial infrastructure platform StripeacquiredLemonSqueezy, a platform for managing digital product sales and subscriptions.

Deal Details: Financial terms were not disclosed.

Strategic Rationale: LemonSqueezy will expand Stripe’s capabilities in digital product sales and subscription management.

Impact on Industry: The deal will promote innovation in digital commerce, providing businesses with more comprehensive tools.

Future Outlook: Stripe will enhance its existing offerings with LemonSqueezy’s capabilities, further supporting digital entrepreneurs.

NCR Voyix is selling its digital banking business to private equity firm Veritas Capital.

The deal is expected to close by the end of 2024 for $2.45 billion in cash plus a future contingent installment of up to $100 million.

NCR Voyix, which recently split from NCR, expects the move will help it focus on its core software and services offerings for restaurants and retailers.

Digital commerce provider NCR Voyix is simplifying its operations this week. The Georgia-based fintech has agreed to sell its cloud-based digital banking business to an affiliate of private equity firm Veritas Capital. Under the terms of the agreement, NCR Voyix will sell its digital banking unit for $2.45 billion in cash plus a future additional installment of up to $100 million, contingent on terms.

The deal is expected to close by the end of 2024.

NCR Voyix launched its digital banking platform in 2014 and has since evolved significantly. The banking suite aims to offer its 1,300 financial institution clients a comprehensive banking environment for their 20 million active retail and commercial banking customers. For retail banking, NCR Voyix provides online and mobile banking, personal financial management, and customer engagement tools. For commercial banking, the platform includes services such as cash management, treasury services, and business banking solutions.

“Our Digital-First solution suite has been strategically designed to grow and expand with our customers over time as their retail and business banking distribution and customer engagement strategies evolve,” said NCR Voyix Executive Vice President and President of Digital Banking Brendan Tansill. “Veritas brings a proven track record of successfully executing similar business carveouts and subsequently driving growth. We look forward to working alongside their experienced team as we continue to pursue commerce and banking innovations that help our customers and their users succeed.”

Veritas’ CEO and Managing Partner Ramzi Musallam said that NCR Voyix’s digital banking platform shows “significant runway for growth.” He added that the purchase represented a significant opportunity to invest in a solution that will empower a range of financial institutions.

For NCR Voyix, the deal is a byproduct of efforts to streamline its operations to focus on its core software and services offerings for restaurants and retailers. The move comes after NCR separated its ATM-focused business from its digital commerce operations in October of 2023.

The company will use the proceeds of today’s deal to accelerate select financial objectives, including de-levering its balance sheet, which will allow for greater strategic investment in NCR Voyix’s core businesses. As company CEO David Wilkinson explained, “This transaction allows us to drive value for our shareholders by strengthening our financial position and focusing on our core restaurant and retail customers.”

Customer analytics platform unitQ secured a strategic investment from Zendesk Ventures.

The amount of the investment was undisclosed. unitQ had raised $41 million in funding to date.

unitQ made its Finovate debut at FinovateFall 2021 and returned to the Finovate stage a year later for FinovateSpring in San Francisco.

Here’s some funding news that slipped beneath our radar this summer: AI-powered customer analytics platform unitQ has secured an investment from Zendesk Ventures. The amount of the funding was not disclosed, but it turns Zendesk from a unitQ customer into a strategic investor, as well.

“We chose unitQ after evaluating and trying different solutions in the market,” Zendesk VP of Global CX Operations Shawn Slipy said. “The granularity and speed at which unitQ is able to deliver actionable customer insights is above and beyond what others could offer, and we’re grateful for our continued partnership.”

unitQ had raised $41 million in capital ahead of the June investment, according to Crunchbase. The current investment comes amid Zendesk Ventures’ determination to back companies that are leveraging AI to enhance both customer and employee experience. The venture fund will provide unitQ with access to CX and AI experts to help drive innovation and assist the company in recruiting talent, growing unitQ’s customer base, and building its brand.

“We’ve experienced the power of Zendesk’s community first-hand and are excited to explore joint go-to-market efforts with Zendesk’s ecosystem of customers, technology partners, and evangelists,” unitQ CEO and Co-Founder Christian Wiklund said. “Partnering with Zendesk means joining forces with a leader that opens doors to top-tier talent and industry networks. We’ve gained more than just funding – we’re now connected to a community and receive tailored mentorship to help our company’s growth.”

Customer service platform Zendesk leverages AI agents, workflow automation, and human agents to help businesses provide better service to customers and make workplaces more efficient for employees. The company has more than 100,000 customers in 160 countries and territories and 5,450 employees. Zendesk launched its Zendesk Ventures global venture fund in June with a mission to provide emerging companies with capital, CX and AI expertise, as well as strategic partnership opportunities – especially for AI-first companies.

“Every organization is on a path to becoming AI-driven, and we’re eager to form partnerships with companies leading this new era,” Ben Barclay, SVP of Strategy, Corporate Development, & Transformation at Zendesk, said.

unitQ made its Finovate debut at FinovateFall 2021, and returned to the Finovate stage the following year for FinovateSpring in San Francisco. In the time since then, the company has launched a range of new solutions, including its Impact Analysis Tool and its generative AI engine for measuring product quality, unitQ GPT. This spring, unitQ added Product Analytics to its User Feedback Platform to enable institutions to view and analyze real-time user feedback along with behavioral analytics data.

In recent months, the company has also forged partnerships with Chess.com, streaming media platform Plex, and most recently with product analytics platform Amplitude.

Founded in 2018, unitQ is headquartered in Burlingame, California.

The partnership will enable Varo Bank to offer a range of new products including digital wallet tokenization via Apple and Google Wallets for its cardholders.

Headquartered in Oakland, California, Marqeta was founded in 2010.

Card issuing platform Marqetahas signed a five-year deal with Varo Bank to serve as the financial institution’s issuer processor. Marqeta’s ability to blend virtual, tokenized, and physical card-issuing technology with faster speed-to-market was among the factors cited by Varo Bank in teaming up with the fintech.

“We sought an issuer partner that complements our unique position as both a technology company and a regulated financial institution,” Varo Bank CEO Colin Walsh explained. “This partnership with Marqeta enables us to offer cutting-edge card issuing technology, giving our customers enhanced ability to view and manage their transactions efficiently. This advancement aligns perfectly with our mission of financial empowerment.”

Widely recognized as one of the first nationally-chartered consumer-based techbanks in the U.S., Varo Bank offers fee-free checking accounts, high-yield savings accounts, secured credit-building credit cards, instant payment solutions, and free ATM access at more than 40,000 locations. Varo Bank’s mobile app enables customers to review and improve their financial health, and now, courtesy of the institution’s partnership with Marqeta, the bank will enable digital wallet tokenization with Apple and Google Wallets for its cardholders.

“Marqeta is proud to announce this deal with Varo Bank, which relies on the latest payments and banking technologies to help Americans who are striving to get ahead,” Marqeta CEO Simon Khalaf said. “Varo’s mission is aligned with ours and we can’t wait to start innovating with the Varo team, enabling their customers to see transactions in real-time thanks to Marqeta’s APIs.”

Marqeta is an alumnus of our developers conference series, FinDEVr. The company presented its technology at our event in Silicon Valley in 2016. In the years since then, the Oakland, California-based fintech has grown into a major, modern card issuing platform operating in 40 countries and processing more than $160 billion in volume in 2022. The company’s partnership news with Varo Bank comes less than a month after Marqeta announced that it had become the first issuer processor in the U.S. that was certified to enableVisa Flexible Credential, a product that provides access to multiple funding sources from a single payment card.

Founders are what make the fintech world go around. Without their grit, willingness to take risks, desire to enhance the status quo, and determination to bounce back after failure, fintech wouldn’t be here.

At FinovateSpring earlier this year, we spoke with four fintech leaders– Robbie Heeger, President and CEO and Endaoment; Alexandra McLeod, CEO and Founder at Parlay Protocol; Gwyneth Borden, Founder and CEO and Remynt; and Christian Widhalm, CEO and Bloom Credit– shortly after they stepped off the Finovate demo stage. We asked each of them for advice on pitching a product through a demo approach, refining presentations, and communicating their company’s value proposition.

Lessons from Finovate – Shaping your fintech showcase approach

Evolution through Feedback – Refining Fintech Presentations for Future Success

Unlocking Demo Success – Key Strategies for Communicating Fintech Value Propositions

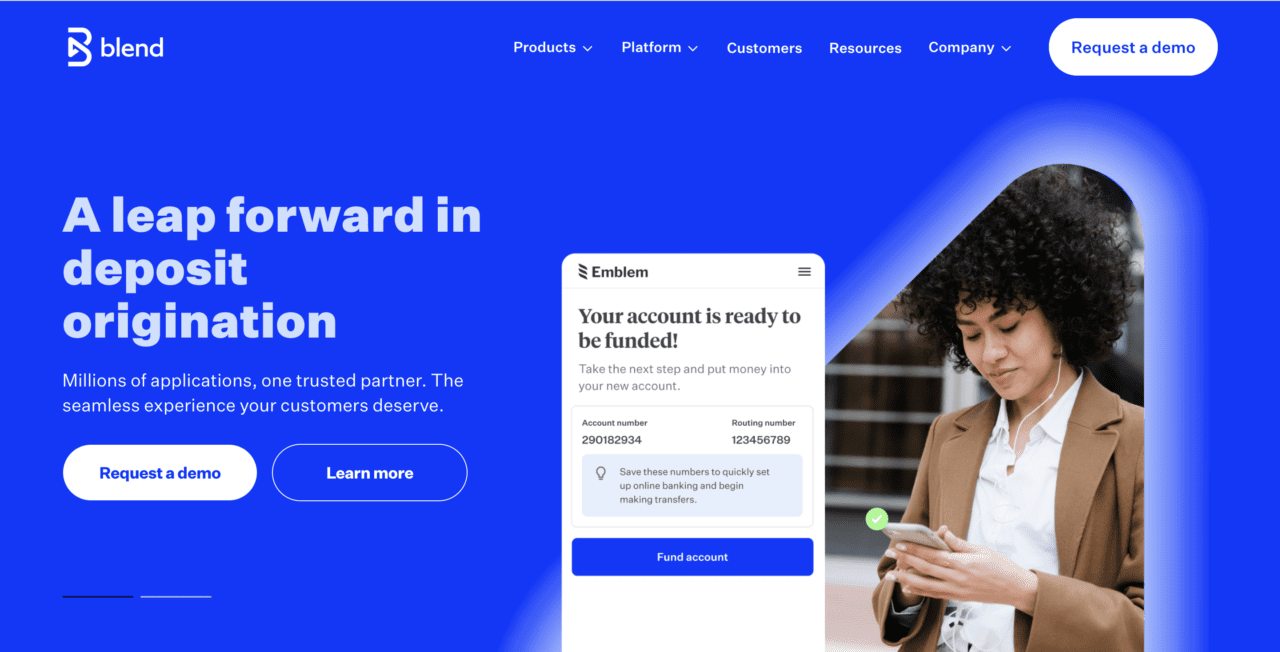

Digital banking solutions provider Blend has forged a partnership with instant payments-as-a-service company Astra. The partnership will integrate Astra’s Card to Account payment solution directly within Blend’s Deposit Account application flow. This will enable Blend customers to drive digital engagement beyond the initial application capture, lowering abandonment rates and helping consumers complete applications faster.

“Today consumers expect a frictionless, real-time product experience, and that starts at account opening,” Astra CEO and Co-Founder Gil Akos said. “Financial institutions and fintechs need to deliver a best-in-class onboarding flow to win new customers – instant account funding is the perfect solution, leading to improved activation rates of 30% or better on day one. We’re proud to partner with Blend to offer this experience to their customers.”

Funding by card is an increasingly popular option given the relative inconvenience of other methods, such as ACH transfers. By comparison, funding new accounts via debit cards is a faster and more seamless process (no routing or account numbers to remember). And because cards only enable transactions up to the available balance, card funding also helps avoid potential overdrafts when using ACH transfers, a risk for consumers who may have limited funds or irregular cash flow.

Further advantages include accelerated onboarding, more activated accounts, reduced abandonment, a smoother application experience, and less manual intervention.

Blend noted in a statement that card funding is also one of the more popular ways for consumers to fund new accounts. The company pointed to one of its customers, a major credit union, that reported that 82% of their new deposit accounts were funded using Astra card funding. Another credit union customer of Blend said that 66% of its consumers preferred funding via Astra card compared to other methods. Card funding for Blend Deposit Accounts is now generally available for all customers.

Astra offers a platform for instant payments that enables product teams to embed payments into their solutions. The company’s API facilitates seamless fund transfers between bank accounts and cards, providing a fast, secure, and built-for-scale alternative to traditional fund transfer methods such as ACH.

Astra launched its first, end-to-end instant payment solution with FedNow in the fall of 2023. In December, the company announced a partnership with merchant connectivity platform Knot to enable seamless card switching with instant funding. Founded in 2016, Astra is headquartered in Menlo Park, California.

Blend demoed its technology at FinovateSpring 2016. At the conference, the company demoed its Data-Driven Mortgage solution which leverages high-fidelity data sources to drive down origination costs, maintain digital compliance, and provide a positive user experience for borrowers.

Last month, Blend announced its acquisition of applied AI company nuvu, and expanded its partnership with DataIQ. In May, Blend secured an investment of $150 million from technology-focused private equity firm Haveli Investments.

Headquartered in San Francisco, California, and founded in 2012, Blend is a publicly-traded company on the NYSE. Trading under the ticker BLND, the company has a market capitalization of $678 million. Nima Ghamsari is CEO and Co-Founder.

PayPal is launching Fastlane, a one-click guest checkout experience for online merchants.

Fastlane automatically recognizes shoppers based on their phone number or email address, and autofills information forms in the checkout flow.

PayPal first unveiled Fastlane in January, and has been testing the solution with select merchants and ecommerce sites, including BigCommerce.

Fintech pioneer PayPal is launchingFastlane, its guest checkout tool, for all U.S. merchants this week. Fastlane aims to accelerate the guest checkout experience to help users complete their purchase in as little as one click.

Merchants can integrate Fastlane into their existing online checkout flow to create a simpler, faster checkout experience for the 43% of consumers who prefer a guest checkout experience. By using the customer’s email, Fastlane recognizes shoppers early in the guest checkout process and allows them to access their saved information with a one-time passcode sent via email. After entering their passcode, users can autofill the information in the checkout flow and complete their purchase in as little as one click.

When Fastlane does not recognize a shopper, it allows them to create a Fastlane profile by opting in during their purchase process, enabling faster transactions in the future.The tool does not require users to fill out forms or remember passwords.

“Fastlane by PayPal significantly reduces the time consumers spend using guest checkout – making for a more seamless checkout experience,” said PayPal President and CEO Alex Chriss. “With Fastlane, we are bringing an accelerated guest checkout to businesses of all sizes helping them to drive more sales.”

PayPal unveiled Fastlane in January and has since tested the technology with select businesses, including merchant SaaS provider BigCommerce, which is among the first ecommerce sites to test PayPal’s Fastlane. Over the past several months of trialing the technology, BigCommerce saw a 32% reduction in time it took for customers to check out. Additionally, as company CEO Brent Bellm noted, “Results from early-adopting test customers show that Fastlane users convert more than 80% of the time, which is up to a 50% improvement over guest shoppers who do not use Fastlane. For BigCommerce enterprise customers using PayPal, the Fastlane experience further improves on our checkout conversion rate of 71%.”

Fastlane is available for U.S. merchants on PayPalComplete Payments and PayPal Braintree, as well as via platforms including Adobe Commerce, BigCommerce, Salesforce Commerce Cloud, and others.

A look at the companies demoing at FinovateFall in New York on September 9 and 10. Register today using this link and save 20%.

Eko Investments

Eko Investments‘ white-label solution allows 10,000 banks and credit unions to offer digital investing directly on their existing banking platform.

Features

Offers digital investing natively integrated into digital banking

Supplies pre-made portfolios and self-selection of stocks, bonds, or ETFs

Makes end-users feel like they are investing with their FI via 100% white-labeling

Who’s it for?

Banks and credit unions of all sizes.

Fizen Technology

Verify by Fizen Technology is an all-in-one compliance screening platform for banks. Verify consolidates essential checks like KYC and OFAC, simplifying compliance, reducing risk, and enhancing efficiency.

Features

Featured checks:

Negative news

Politically exposed person (PEP)

Secretary of State

Who’s it for?

Banks, credit unions, and fintechs.

Further

Further connects consumers to the best credit unions for their needs, helping them achieve financial wellness and freedom.

Features

Consumers can:

Access pre-approved offers and funds easily

Monitor their credit score for free

Receive personalized financial insights and recommendations

Who’s it for?

Gen Z and Millennial consumers (21 and above).

GenRPT

GenRPT is an AI-driven insights and reporting platform that allows users to generate visual reports from databases in plain English, supporting SQL, Excel, PDF, CSV formats, and more.

Features

Connect to any database – structured or unstructured

Interact in plain English, without any prior technical knowledge

TodayPay is the world’s first instant payments network and inventor of Refunds as a Service, giving merchants an alternative payment method to issue instant refunds to customers.

Features

Offers a cheaper refund payment method to credit cards

Issues refunds instantly (average time of 26 seconds for consumers to receive refunds)

Allows consumers to choose refund payment methods, including cashback

Who’s it for?

Merchants, retailers, brands, marketplaces, insurers, card issuers, and logistics companies.

Union Credit

Union Credit is the pioneering marketplace for credit unions, enabling them to offer one-click loan options to new members within their daily activities, thereby boosting new member acquisition efforts.

Features

Allows credit unions to set product specific funding limits, marketing spend limits, lender underwriting criteria, rates, and more

Supports all consumer loan products

Captures census tract data on consumers for CDFI tracking

Ready to level up your networking game at FinovateFall? We’re here to help! At FinovateFall 2024, which is taking place September 9 through 11 in New York, we’re launching a new, personalized meeting platform called LevelUp.

Introducing LevelUp

LevelUp, Finovate’s new meeting program, is designed to help banks and financial institutions participate in tailored, valuable meetings. The goal of the meetings is to help our financial institution attendees efficiently find providers offering solutions that suit their requirements and ultimately meet critical business needs.

Seamlessly Integrated

LevelUp will be embedded into the FinovateFall agenda. We will offer time slots throughout the event to allow you to meet six solutions providers in an efficient, quickfire meeting format. To ensure you are meeting with companies offering real solutions to your challenges, we have hand-selected the best fintechs to optimize your time.

How It Works

Personalized Matches: Upon registering for FinovateFall, you’ll have the opportunity to detail your specific business challenges and needs. Our platform will then match you with the most relevant fintech providers.

Efficient Scheduling: LevelUp slots are strategically placed within the event agenda, ensuring that you have ample time to participate without missing other key sessions and presentations.

Focused Interactions: Each meeting slot is designed to be quick and focused, allowing you to get straight to the point and determine if the provider’s solution is right for your institution.

Why LevelUp?

Targeted Networking: Meet only with providers who are pre-vetted and matched to your specific needs, saving you time and effort.

Optimized Agenda: The seamless integration of LevelUp within the event schedule ensures that you maximize your time at FinovateFall.

Enhanced Collaboration: By focusing on relevant matches, you can build meaningful partnerships that drive real business results.

Join Us at FinovateFall 2024

Don’t miss out on this opportunity to revolutionize your networking experience. Whether you’re looking to explore new fintech innovations, solve specific business challenges, or simply expand your professional network, LevelUp is here to make it happen.

Register now for FinovateFall 2024 and take the first step towards leveling up your networking game. We can’t wait to see you there!

In partnership with financial literacy platform Doshi, Yorkshire Building Society is offering online financial education to first-time prospective homebuyers.

The new free tool, available on the YBS website to customers and non-customers alike, walks new homebuyers through the entire home-buying process.

Doshi made its Finovate debut earlier this year at FinovateEurope in London.

Yorkshire Building Society (YBS) has teamed up with gamified financial literacy platform Doshi to launch an online educational program for first-time prospective homeowners. The new tool is available in the mortgage section of Yorkshire Building Society’s website, and guides borrowers through the process of applying for a mortgage and buying their first home.

The program walks prospective homeowners through the entire home-buying journey, including how to prepare for buying a home, how to secure financing, understanding the various steps of the home-buying process, and the importance of maintaining their home once they’ve made their purchase. The program explains important concepts and potentially unfamiliar terms, and provides a timeline of the overall process. The tool is available free of charge to both YBS customers and non-customers.

“Partnering with Yorkshire Building Society to empower aspiring homeowners is a significant step toward making homeownership more accessible,” Doshi CEO Daniel Rose said. “Our program demystifies the mortgage process, providing engaging, bite-sized guidance every step of the way. We are excited to see the positive impact on first-time buyers.”

The new offering comes in the wake of research conducted by YBS that indicated that a lack of knowledge about the home-buying process was a major barrier for would-be homeowners. YBS noted that only 18% of those surveyed felt knowledgeable about the mortgage process, with even fewer respondents – 14% – saying that they knew what financial factors were key when applying for a mortgage. The survey further indicated that only 45% of respondents believed that a good credit score was an important factor in securing a mortgage. Only 34% stated that the ability to repay debts was important when it comes to obtaining the financing necessary to buy a home.

“We know from customer research that people feel more confident in their decision making when they are informed and know what to expect, which is why we are trialing this new learning tool, aimed at helping first-time buyers understand more about the home-buying process,” YBS senior manager for digital mortgage and enabling services Geddy Meguyer said.

The third-largest building society in the U.K., Yorkshire Building Society is a financial services mutual organization that offers savings, investing, insurance, and mortgage products. Headquartered in Bradford, West Yorkshire, YBS had total assets of more than £60 billion as of December 2023. Along with its assets – the Chelsea Building Society, the Norwich and Peterborough Building Society, Accord Mortgages, and savings business Egg – known as the Yorkshire Building Society Group, the group employs more than 3,000 and serves a membership of three million.

YBS’s partnership with Doshi is the latest effort by the building society to support first-time homeowners. This spring, YBS launched its £5k Deposit Mortgage product, which enabled first-time homebuyers to buy a property worth up to £500,000 with a deposit of only £5k, rather than the typical 5% down payment. The idea behind the £5k Deposit Mortgage was to deal with the biggest obstacle prospective homebuyers tend to face – raising the funds for a down payment.

Doshi made its Finovate debut at FinovateEurope 2024 in February. At the conference, the company demoed its white-label app, which leverages personalized learning journeys and community rewards to turn complex topics into engaging experiences. Doshi’s AI-powered financial assistant technology is built for banks, credit unions, and fintechs, and is available as an app, a plug-and-play web module, as well as via API.

Doshi was founded in 2021. The company is headquartered in London.