This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

HSBC has onboarded Ant International as the first client to use its Tokenised Deposit Service (TDS) for cross-border payments.

TDS leverages distributed ledger technology to turn bank deposits into transferable tokens, enabling instant settlement, programmable payments, and 24/7 treasury operations.

The partnership signals the beginning of commercial acceptance for tokenized deposits as a regulated alternative to stablecoins.

UK-based global banking giant HSBCannounced this week that Ant Group’s digital finance leader Ant International, a global payments leader serving millions of merchants worldwide, has become the first client to use the bank’s Tokenised Deposit Service (TDS) for cross-border payments.

The news comes five months after HSBC initially launched TDS for corporate cash management in Hong Kong. TDS relies on distributed ledger technology (DLT) to instantly settle remittances and payments. The DLT allows HSBC’s clients to create digital records of their traditional, fiat deposits. While HSBC maintains the fiat deposits, each one of the digital records on the DLT is a token that can be transferred.

HSBC anticipates that TDS will set a new standard for liquidity management. In part, this is because, unlike stablecoins, which are issued by private companies or protocols, tokenized deposits remain liabilities of regulated banks, bringing blockchain efficiency into traditional finance.

HSBC aims to help its corporate clients leverage TDS to improve treasury management. The bank created a separate, secure platform to allow clients to transfer funds past cut-off times and around the clock, without having to wait for batch processing, with automated reconciliation, greater speed, enhanced security, and seamless integrations with treasury systems.

Tokenized deposits can also be used for programmable payments, a capability that allows payments to be triggered based on preset rules to streamline cashflow management.

For Ant International, leveraging TDS for cross-border transactions will help streamline treasury operations, enable around-the-clock settlement, and support its mission to deliver faster, more efficient financial services to its global partners.

Ant sees HSBC’s tokenized deposits as a way to scale its global treasury operations and complement its push into cross-border digital finance. “Our relationship has enabled us to work across different geographies and cover a wide range of global payment businesses,” said Ant International General Manager of Platform Tech Kelvin Li. “The Tokenised Deposit Service is one of the main means to enable us to do real-time payments globally and also enable us to achieve real-time treasury management on a global basis.”

HSBC’s rollout of tokenized deposits with Ant International may mark a change of how organizations think about corporate treasury. With programmable payments, 24/7 settlement, and global reach, tokenized deposits are moving from concept to reality. This is especially true in the commercial space, where tokenized deposits could soon become a standard feature of cross-border finance.

Verification platform Argyle announced a strategic investment round that featured participation from Mastercard, Bain Capital Ventures, Checkr, Rockefeller Asset Management, and SignalFire.

The investment follows Argyle’s launch of verification of assets powered by Mastercard’s open finance technology earlier this year.

New York-based Argyle made its Finovate debut at FinovateSpring 2022 in San Francisco. Shmulik Fishman is Co-Founder and CEO.

Consumer-powered verification platform Argyleannounced a strategic investment round that featured participation from Mastercard as well as existing investors Bain Capital Ventures, Checkr, Rockefeller Asset Management, and SignalFire. The amount of the investment was not disclosed.

“This investment is more than capital—it’s validation,” Argyle CEO and Co-Founder Shmulik Fishman said. “We’re deepening our ability to serve customers with a comprehensive verification platform built on real-time payroll connections and open finance capabilities. By combining these strengths, we’re eliminating friction from verification workflows and giving lenders, fintechs, and tenant screeners a smarter path to faster, more accurate decisions.”

Argyle’s investment announcement comes a year and a half after the company reported securing $30 million in Series C funding. That round was led by Rockefeller Asset Management’s Fintech Innovation Fund. This week’s investment also follows Argyle’s launch of verification of assets powered by Mastercard open finance technology in June of this year. This new offering enables Argyle customers to access real-time consumer-permissioned payroll connections covering 90% of the US workforce. Customers are also now able to generate GSE-compliant reports—including verification of income (VOI), verification of employment (VOE), verification of assets (VOA), and combined verification of assets/income (VOAI)—from a single platform.

Argyle noted that the investment is a sign of growing demand for consumer-permissioned verifications. In a statement, the company highlighted a series of recent partnership accomplishments, including Checkr’s ability to reduce verification timelines from days to seconds at 90% lower cost compared to legacy solutions, Regional Finance’s success in automating verifications for more than 65% of borrowers, and Mutual of Omaha’s saving of more than $50,000 per month on verification costs.

“Argyle has built critical infrastructure for a category that’s long been overlooked by modern fintech,” Bain Capital Ventures partner Ajay Agarwal said. “We’ve supported the company from the early stages, and this latest round reflects our continued belief in their team, their momentum, and the long-term potential of consumer-permissioned data to transform verifications across financial services.”

Founded in 2018 and headquartered in New York, Argyle made its Finovate debut at FinovateSpring 2022. At the conference, the company demonstrated its Link 4.0 design update, which provides a more transparent and trustworthy experience for customers when linking their accounts.

New York-based spend management platform Extend has secured $20 million in combined debt and equity funding.

The equity investment was led by B Capital and featured participation from March Capital, Point72 Ventures, FinTech Collective, and Commerce Ventures.

Extend made its Finovate debut at FinovateSpring 2019 in San Francisco, California.

Spend and expense management platform Extend has raised $20 million in funding. The amount includes new venture debt and an equity investment led by B Capital. Also participating in the equity side of the deal were March Capital, Point72 Ventures, FinTech Collective, and new investor Commerce Ventures.

“We just took another step toward reshaping how businesses manage spend and expenses: We secured $20 million in new funding and welcomed Francois Horikawa as our CFO,” the company noted on its LinkedIn page. “Finance teams deserve modern tools layered onto their existing bank card programs. This investment will help us do that by strengthening our issuer partnerships and accelerating the delivery of new spend and expense management features to better serve businesses.”

Extend offers businesses the ability to control and manage spending with the company credit card they already use. Extend’s platform enables companies to create both standard and recurring virtual cards and manage them from either the Extend mobile app or its web-based platform. The virtual cards come with configurable spend controls such as card limits and expiration dates. The platform also can be used to create guest cards to send directly to vendors and contractors that do not have Extend accounts. The firm is currently implementing solutions that leverage automation to manage approvals, capture receipts, and reconcile expenses.

“This funding represents a pivotal moment for Extend as we accelerate our path to profitability and launch our paid SaaS offering,” Extend CEO and Co-Founder Andrew Jamison said. “With strong backing from B Capital and our investor group, we’re building a comprehensive spend and expense management platform while maintaining our focus on capital efficiency and deepening our relationships across the banking ecosystem.”

Extend’s funding announcement arrived at the same time that the firm introduced new Chief Financial Officer Francois Horikawa. Horikawa was previously Head of Finance for PayPal’s Consumer business division, which includes Venmo, P2P, Cards, and Small Business Lending. In his new role as CFO, he will be charged with helping Extend achieve operational excellence and sustainable profitability.

“I joined Extend almost by accident,” Horikawa wrote on LinkedIn this week. “I knew one of the co-founders and a few other folks from American Express. Few months in, people are super nice, the culture is great, and I am excited about the product!”

Founded in 2017, Extend made its Finovate debut at FinovateSpring 2019 in San Francisco, California. In the years since then, the New York-based fintech has grown into an out-of-the-box virtual card issuing platform with more than 10,000 business customers. The company’s technology has helped its customers move between 26% and 40% of their spending to virtual cards, and more than a dozen major banks in both the US and Canada are using Extend’s technology. Extend is currently pursuing strategic integrations at the top 10 banks and with a range of smaller issuers.

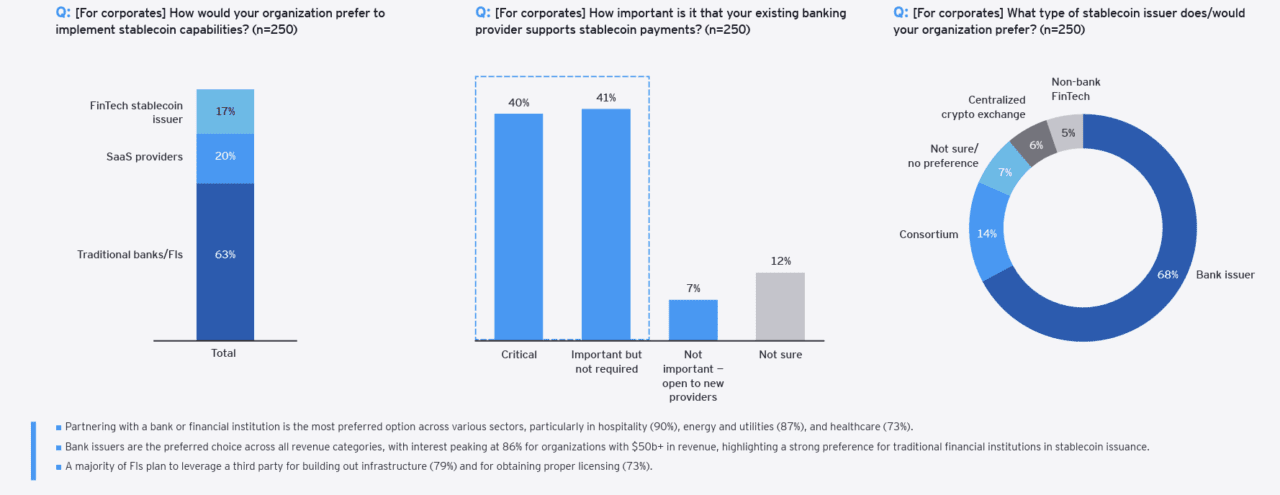

This year marks the year of the stablecoin, especially in the US. From the start of the year, we have watched as stablecoins evolved from a concept in trials overseas to a market force attracting billions in daily transaction volume, partnerships with major payment networks, active pilots among US banks, and a central focus of US financial regulation in the form of the GENIUS Act.

After the passage of the GENIUS Act in July, Ernst & Young’s (EY) strategy consulting services group EY-Parthenon surveyed more than 350 executives from financial and nonfinancial sectors about their views on stablecoins. Based on its findings, the firm generated a 31-page report that highlights adoption, usage, benefits, challenges, regulatory implications, and more. We’ve highlighted the report’s five major takeaways below.

Stablecoins are no longer fringe

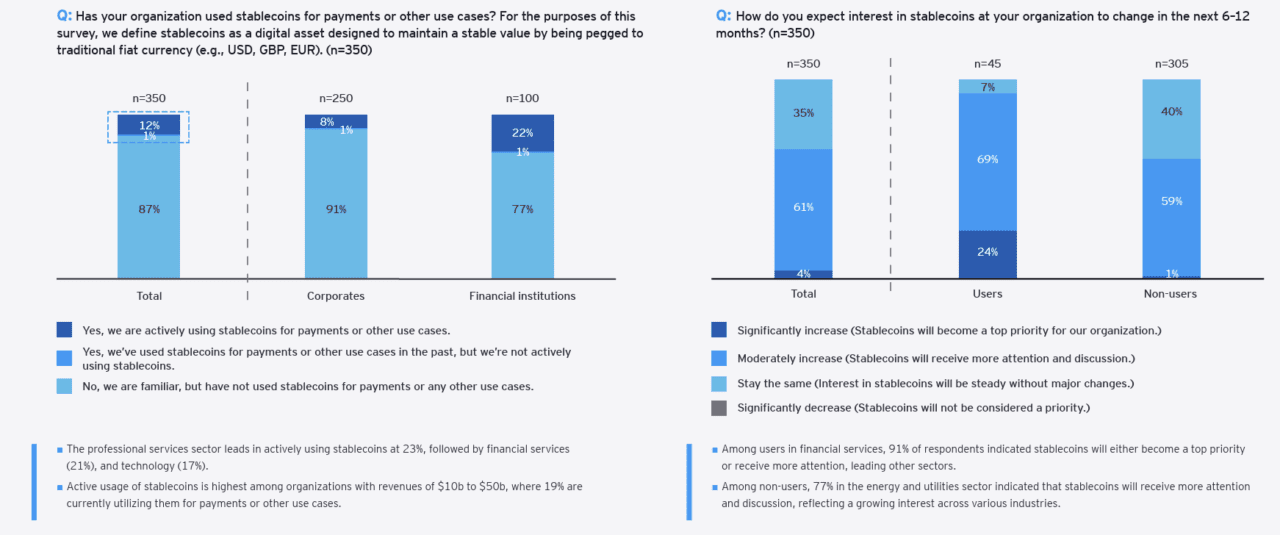

All of the 350 executives surveyed are aware of stablecoins. Of those, 13% have already used stablecoins and 65% expect interest in stablecoins to rise in the next 6 to 12 months.

The fact that 100% of executives surveyed are aware of stablecoins demonstrates how quickly stablecoins have moved into the mainstream. For banks and corporates, the conversation around stablecoins is no longer a question of “if,” but rather “how fast” adoption spreads and what role the organization should play. This shift from niche to norm shows that institutions that wait to make a move may miss out on shaping standards and capturing early market share.

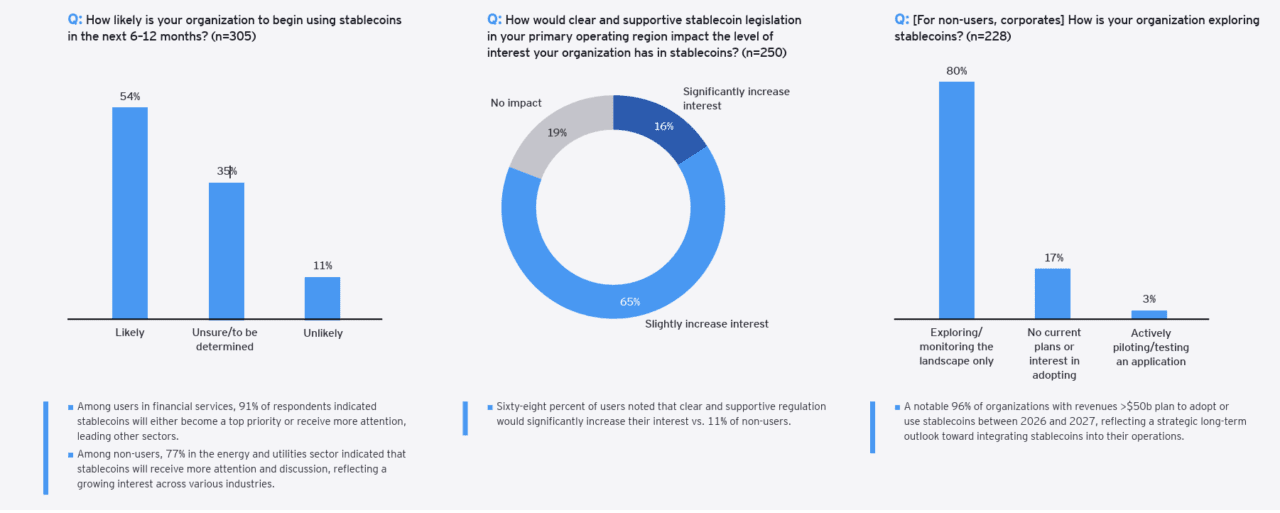

More than half, 54%, of financial institutions and corporates that are not using stablecoins expect to begin using them in the next 6 to 12 months. For 81% of participants surveyed, clear and supportive legislation increases their interest in stablecoins, either significantly or slightly.

With more than half of firms signaling plans to adopt stablecoins within a year, the market will likely see an acceleration in usage. For policymakers, this highlights the importance of regulatory clarity, given that it would directly boost adoption. For banks, it shows an opportunity to deepen their relevance by offering compliant, stablecoin-enabled services before competitors get there first.

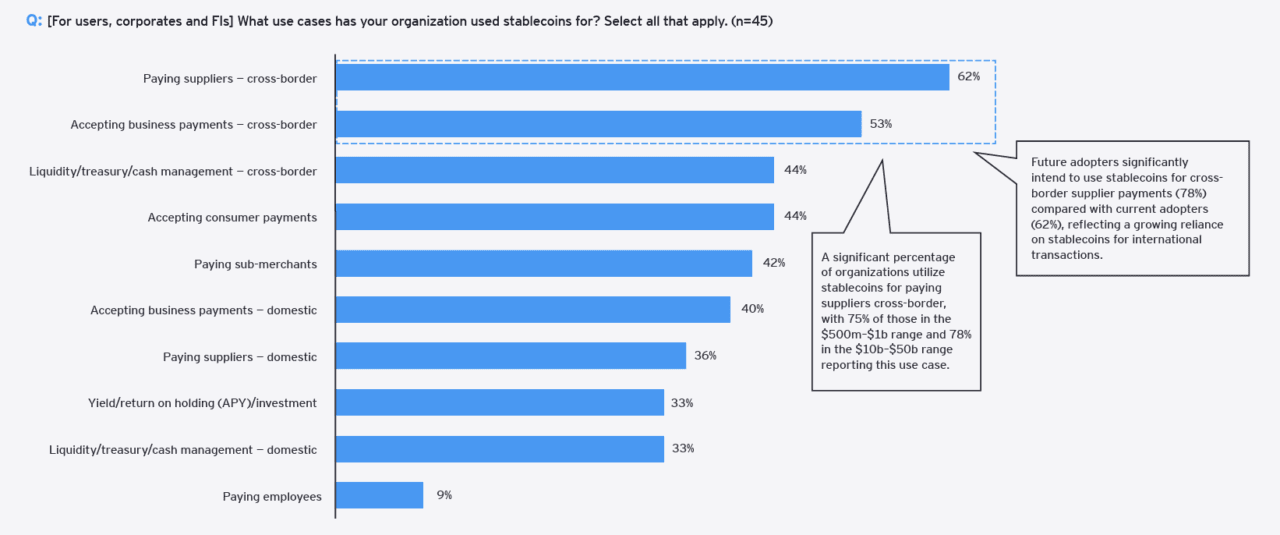

The survey asked about 10 different use cases. Of those ten, the top three use cases centered around cross-border payments.

This shows that stablecoins are tackling real, persistent pain points, especially in cross-border payments. Despite previous disruption by alternative players such as Wise, Remitly, and Revolut, international transfers remain slow and expensive. Stablecoins are a credible alternative that resonates with businesses and consumers. This focus could disrupt entrenched correspondent banking networks and give stablecoin adopters an edge in the lucrative field of cross-border payments.

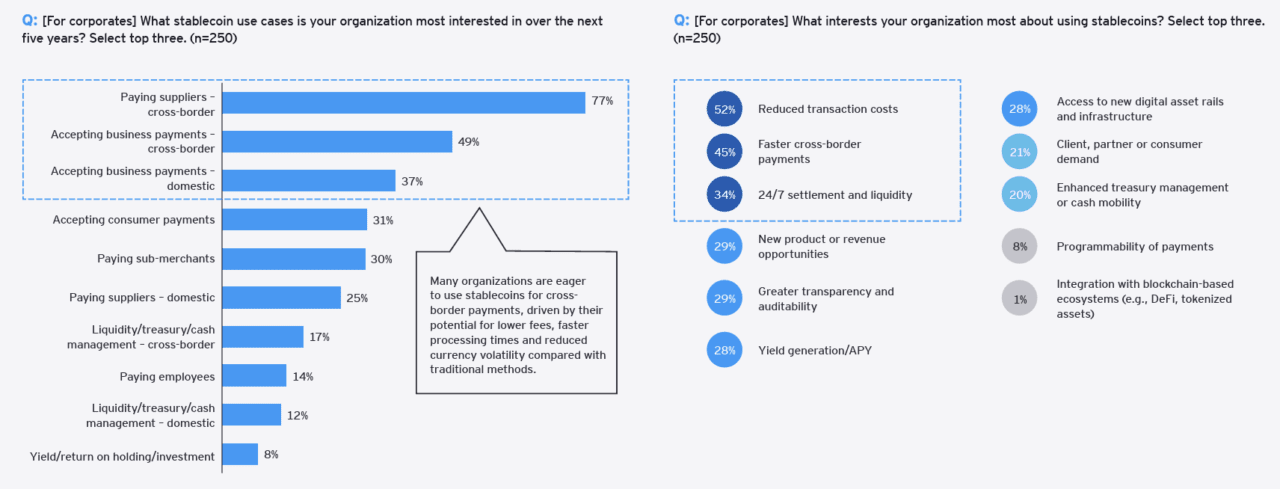

Firms most interested in reducing cost and increasing payment speed

The most interesting use case is cross-border payments (77%), with interest largely driven by reduction in transaction costs and faster payments.

The overwhelming interest in cost savings and speed is a reminder that stablecoins will succeed or fail based on tangible value, not hype. For businesses, even modest reductions in cross-border fees can translate into significant savings at scale. Banks face the challenge of turning this efficiency into a competitive advantage, offering better pricing and faster settlement while managing risks.

The survey found that organizations are looking to their traditional banking partners for access to stablecoins, and that most financial institutions, 79%, plan to leverage a third party for stablecoin infrastructure.

The finding that most organizations plan to access stablecoins through existing banking partners is significant. It suggests that businesses want access to stablecoins without having to deal with the complexity that comes with the new payment rail. Instead of investing in-house to leverage the new technology, they’re looking to trusted intermediaries like banks to handle the heavy lifting of facilitating the infrastructure. For banks, this is both an opportunity and a warning. Institutions that move quickly to build reliable, third-party-powered stablecoin services can strengthen client relationships, while laggards risk being bypassed entirely.

Flybits has launched its Agentic Banking capability, using agentic AI to create “human-centered” banking journeys that guide customers through major life events.

The AI agents unify products like cards, loans, deposits, and insurance into seamless experiences, such as financing and maintaining a car.

Flybits is backed by strong venture funs and is supported by its research and development arm Flybits Labs, that partners with academic institutions and industry innovators to prototype future banking experiences.

Agentic AI-powered banking may still feel like a futuristic scenario, but customer experience platform Flybits is making it a reality. The company recently unveiled the launch of its Agentic Banking capability.

Flybits is leveraging agentic AI to create a new interface for banking that will help financial institutions provide “human-centered” experiences that guide their customers through life events. The new agents will help customers unify cards, loans, deposits and other banking activities into customer experiences that feel more connected.

The agents will, for example, be able to help customers during a car purchasing experience. When the customer uploads a photo of the vehicle they plan to purchase, the bank’s agent will help them calculate affordability, show them financing options, and help them compare insurance coverage with offering the customer contextual card benefits like savings on fuel service expenses. The agent streamlines the entire experience around the vehicle, saving them from having to open multiple apps for loans, cards, and insurance.

“This isn’t about another chatbot or rewards app,” said Flybits Founder and CEO Dr. Hossein Rahnama. “It’s about helping banks build intelligent agents that integrate their products and services into life-based journeys—delivering outcomes that resonate, while ensuring trust, compliance, and explainability.”

Flybits’ AI agents have a natural language interface, can be integrated across banks’ internal systems and their partners, and offer end-to-end auditability and transparency.

While the new agentic capabilities look very seamless, two challenges stand out. First, some consumers may hesitate to trust their bank with such a deep level of personal data sharing, especially when it includes lifestyle information. More importantly, banks will face an uphill battle convincing customers to use these tools in place of the platforms they already rely on, such as ChatGPT for advice, or Pinterest for planning life events. The technology is compelling, but driving adoption will require overcoming both trust and usability hurdles.

Flybits was founded in 2013 as a spin-off from a university research project. Today, the Toronto, Ontario, Canada-based company helps financial institutions leverage their data to create multidimensional customer experiences that ultimately drive loyalty and business results.

Backed by Point72 Ventures, Information Venture Partners, Bosch Ventures, and others, Flybits also has an applied R&D division, Flybits Labs, that partners with academic institutions and industry innovators to prototype future banking experiences such as Perspective-Aware AI, human-centered UX, and immersive design.

Today marks the official start of autumn here in the Northern Hemisphere. In addition to the wealth of fintech news out of Saudi Arabia (!) in recent days, we’re seeing a number of new partnerships and some big investment rounds in Europe, Asia, and the States as the week begins. Be sure to check back here at the Fintech Rundown for the latest updates.

Walmart for Business has partnered with TreviPay to expand its Pay-by-Invoice program that gives eligible business customers 30-day credit terms for online and in-store purchases.

TreviPay’s AI-powered receivables technology enables faster dispute resolution, reduces errors, and improves conversion by automating underwriting and invoicing.

The program has launched with select Walmart Business customers and will expand in the coming months, aiming to capture growing demand in B2B retail payments.

Walmart for Business, an ecommerce site tailored to suit business needs, announced this week it has partnered with global transaction management company TreviPay this week.

Walmart has tapped TreviPay to launch the next phase of its Pay-by-Invoice program that enables eligible business customers to access a line of credit with a 30-day term for online and in-store purchases. The new program will be powered by TreviPay’s payments and accounts receivable automation technology.

TreviPay was founded in 1980 and helps business buyers across industries stop chasing payments. The company’s accounts receivable automation technology optimizes order-to-cash and integrates with all channels and ERPs. In 2020, TreviPay was acquired by Corsair Capital for an undisclosed amount. Today, TreviPay processes over $8 billion in global money movement.

TreviPay’s Pay-by-Invoice product leverages AI-enhanced underwriting and smart invoicing to deliver a guaranteed number of days of sales outstanding (DSO) and ultimately improve conversion. When compared to manually managing accounts receivable, Pay-by-Invoice speeds business growth, decreases errors, and reduces friction at the point of purchase.

“The biggest opportunity in retail now is in B2B. Companies that capture this valuable segment will win with flexible payment options that integrate directly into the buying experience and maintain efficiency and control for the buyer,” said TreviPay CEO Brandon Spear. “Pay-by-Invoice helps companies purchase and pay in a convenient, effortless way.”

At launch, Walmart Business’ Pay-by-Invoice offering is available to a select group of Walmart Business customers. The company plans to expand access to more customers in the coming months.

This week’s edition of Finovate Global looks at recent fintech news from the Kingdom of Saudi Arabia (KSA).

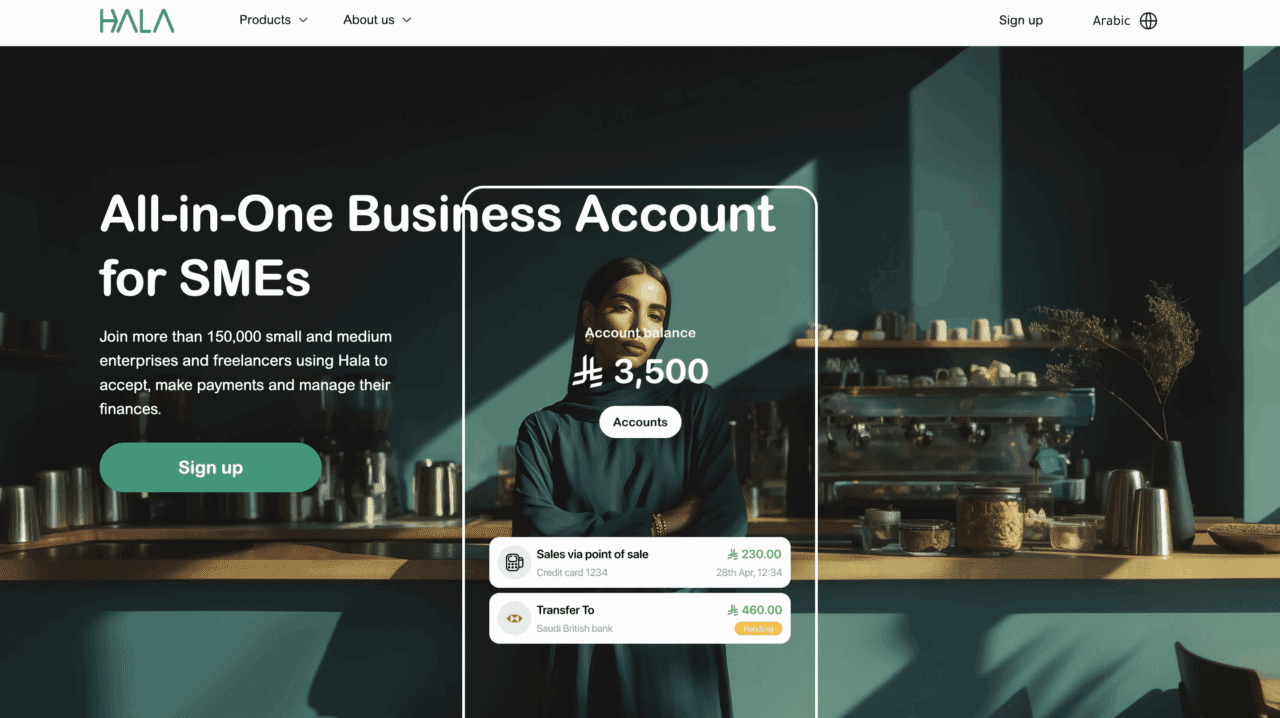

Saudi fintech HALA raises $157 million to fuel embedded finance

Saudi Arabia-based fintech and embedded financial services provider HALA has raised $157 million in Series B funding. The round is being billed as one of the largest fintech Series B rounds to date for a company based in the Middle East. Led by The Rise Fund and Sanabil Investments, the investment will be used to enhance HALA’s position in the Saudi market. This includes empowering the company to launch more embedded financial services and lending products to support micro, small, and medium-sized (MSM) enterprises, as well as freelancers, in the region.

Founded in 2017 and headquartered in Riyadh, HALA offers a comprehensive embedded financial services including business accounts; card issuance, payment and transfer services; POS solutions, financing, and corporate cards. To date, HALA has supported more than 150,000 businesses and processed more than $8 billion in annual transactions.

“This landmark investment is a turning point for HALA, reflecting on our relentless pursuit of innovation and excellence in serving small businesses,” HALA Co-founder and Chairman Esam Alnahdi said. “We are honored that our new investors recognize the potential of our vision and the impact we aspire to make in the MSME landscape. Our journey is just beginning, and this support fuels our drive to create meaningful change.”

Also participating in the investment were QED, Raed Ventures, Impact46, Middle East Venture Partners (MEVP), Isometry Capital, Arzan VC, BNVT Capital, Kaltaire Investments, Endeavor Catalyst, Nour Nouf Ventures, Khwarizmi Ventures, and Wamda Capital.

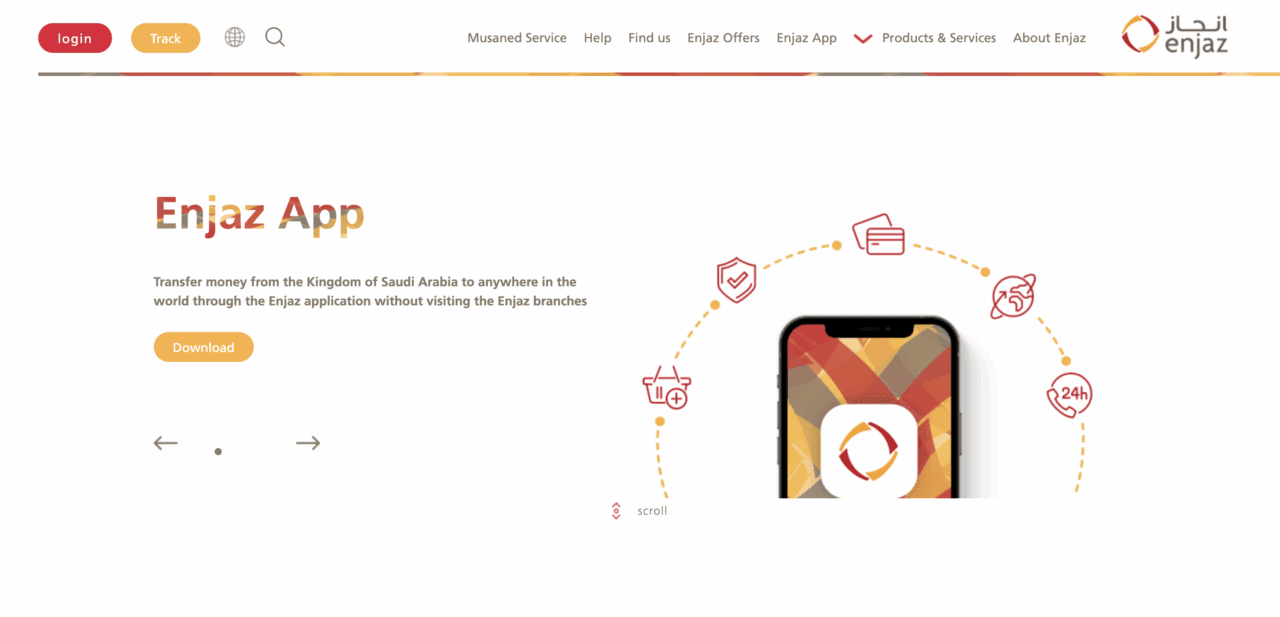

Paymentology teams up with Enjaz to enhance digital payments in Saudi Arabia

“At Enjaz, our focus has always been on giving our customers speed, convenience, and security, whether they are transferring money abroad or making everyday payments,” Enjaz CEO Bassam AlEidy said. “By collaborating with Paymentology, we can now extend our card services that expand choice and enhance financial freedom. This partnership represents a major step in shaping the future of payments in Saudi Arabia, delivering innovation that is inclusive, dynamic, and tailored to the needs of our market.”

Integrating Paymentology’s issuing and processing platform will enable Enjaz to offer prepaid, debit, and virtual cards, all of which will seamlessly integrate with the company’s current services. The partnership will also bring functionalities such as international and domestic scheme enablement; tokenization for Apple Pay, Google Pay, Samsung Pay, and Mada Pay, as well as tools to boost security and enable real-time decisioning. Enjaz will also be able to leverage its new relationship with Paymentology to offer features such as loyalty programs and multi-currency wallets.

“Saudi Arabia is building one of the world’s most dynamic payments ecosystems under Vision 2030. Enjaz’s ambition adds to that momentum, and Paymentology’s role is to power innovators with secure, scalable issuing. Together with Enjaz, we’ll expand choice, accelerate time-to-market, and raise the bar for customer experience in the region,” Paymentology CEO Jeff Parker said.

Enjaz was established in 2022 as a wholly-owned payments arm of Bank Albilad. The firm is licensed by the Saudi Central Bank as a Major Electronic Money Institution (EMI). The partnership with Paymentology comes at a time when the Saudi Central Bank is reporting that electronic payments represented 79% of total retail transactions in 2024, up from 70% in the previous year.

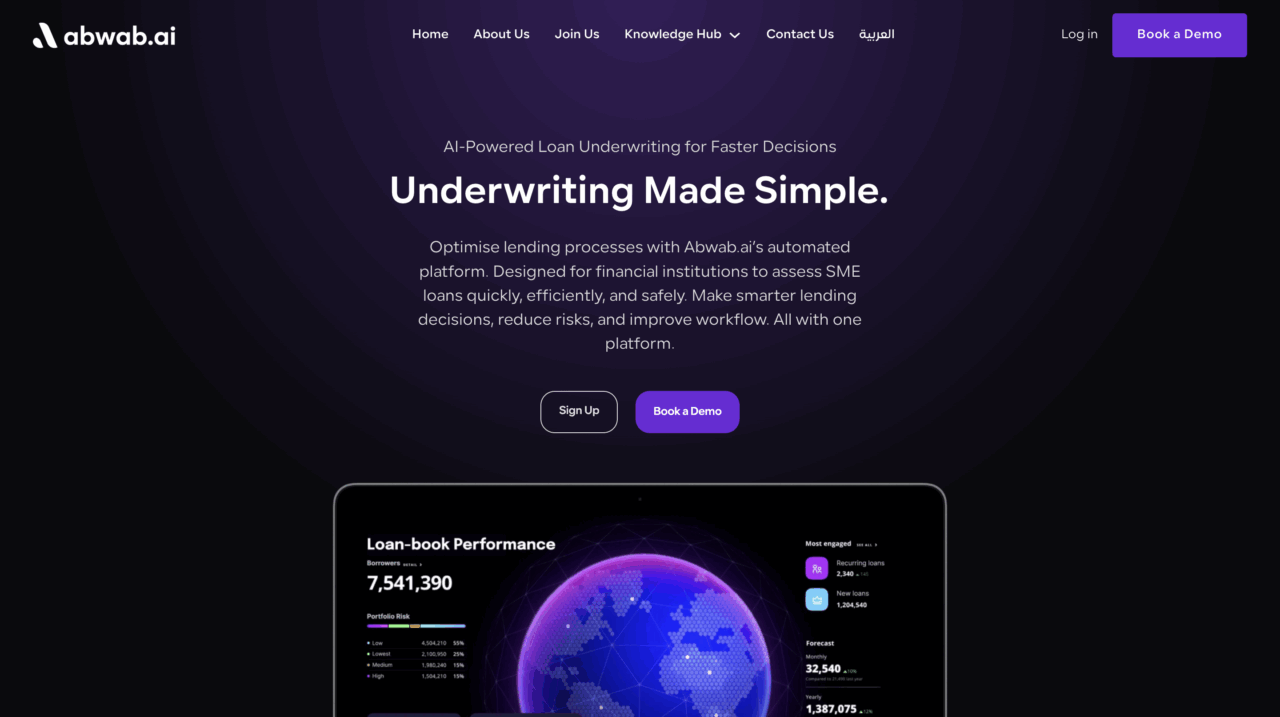

Riyadh-based financial services enabler Abwab.ai forges strategic partnership with Tuum

Abwab.ai, a financial services company that specializes in credit decisioning, risk management, and customer engagement solutions, has announced a strategic partnership with core banking platform provider and Finovate Best of Show winner Tuum. The partnership will enable Abwab.ai to deliver a seamless, end-to-end digital lending solution for small and medium enterprises (SMEs) throughout the Gulf Cooperation Council (GCC).

“SMEs are the backbone of every economy, yet they remain underserved by traditional lenders,” Abwab.ai Founder and CEO Baraa Koshak said. “By combining Abwab.ai’s AI-driven intelligence with Tuum’s next-generation core banking capabilities, we are empowering financial institutions to unlock SME growth at scale.”

Founded in 2022 by a team that includes technology veterans from companies like NVIDIA and HALA, Abwab.ai offers an underwriting automation platform that helps lenders make better decisions by transforming unstructured data into actionable insights. The combination of Abwab.ai’s credit decisioning and analytics capabilities with Tuum’s modular core banking and lending platform will help financial institutions launch, scale, and optimize their SME lending products faster, more efficiently, and with greater transparency.

“Our mission at Tuum is to modernize financial services with modular technology,” Tuum Chief Revenue Officer Miljan Stamenkovic said. “Partnering with Abwab.ai allows us to bring a truly end-to-end, AI-enhanced SME lending solution to the region, one that addresses a real market need and accelerates digital transformation.”

UK-based Tuum won Best of Show in its Finovate debut at FinovateEurope 2024. At the conference, the company showed how its modular, cloud-native, API-first banking platform leveraged its microservices architecture to deliver high scalability and flexibility, as well as lower maintenance costs.

Here is our look at fintech innovation around the world.

Asia-Pacific

Tech in Asia discussed the profitability of a trio of South Korean fintechs: KakaoPay, Naver Financial, and Toss.

UnionPay International (UPI) piloted a cross-border QR payment connection between China and Indonesia.

Estonian fintech Creem locked in €1.8 million in pre-seed funding as it builds its financial infrastructure for AI-focused startups.

Middle East and Northern Africa

valU introduced Egypt’s first licensed Buy Now, Pay Later service, on digital marketplace Noon.

MENA-based financial infrastructure provider Lean Technologies teamed up with Know Your Payee (KYP) solutions company iPiD.

UAE-based fintech Kamel Pay secured In-Principle Approval from the country’s central bank for both Stored Value Facilities (SVF) and Retail Payment Services (RPS) licenses.

Central and Southern Asia

TechCrunch profiled Jar, an India-based fintech that enables its users to invest in gold via its app, that recently announced reaching profitability.

Kazakhstan’s third-largest bank, Bank CenterCredit (BCC) turned to core banking provider Tuum to power its new Banking-as-a-Service (BaaS) proposition.

Bank of India launched its BOI Trade Easy instant loan offering in partnership with Cashinvoice.

Latin America and the Caribbean

Mexican fintech Klar acquired digital bank Bineo from Grupo Financiero Banorte.

Mercado Pago, the financial arm of Latin American e-commerce company Mercado Libre, acquired Brazil-based distributor of investment products Nikos DTVM.

Cryptocurrency exchange Binance launched its Mexican entity Medá to help advance demand for the company’s services throughout Latin America.

Banking and payments software company Compass Plus Technologies has launched FraudAxis, its new fraud management platform.

The new offering will help financial institutions better detect, prevent, and anticipate fraud attacks in real time across payment channels.

Founded in 2005, Compass Plus Technologies made its Finovate debut at FinovateFall 2012.

Banking and payments software provider Compass Plus Technologieslaunched its new fraud management platform, FraudAxis, this week. The technology is designed to enable financial institutions to detect, prevent, and predict fraud in real time across payment channels.

FraudAxis is a hybrid solution that blends rule-based analysis with adaptive machine learning models to enable banks, processors, and payment services providers to use a proactive approach to fraud management. Built on a modern, microservices architecture, FraudAxis analyzes customer behavior, anomalies, and risk patterns in real time to reduce the number of false positives, accelerate fraud detection, and safeguard customer trust. The solution does all of this without bringing additional friction to the user experience.

FraudAxis will enable financial institutions to respond sooner and faster to new fraud threats, anticipate and prevent more fraud before it occurs, and reduce false positives at scale. The solution also provides cross-channel analytics to help defend against fraud across digital and physical channels. Customizable workspaces and real-time dashboards provide 360° visibility and control, as well as access to actionable insights that enable fraud management teams to continuously evaluate and enhance performance.

“Fraud is becoming more sophisticated and coordinated, making it harder to fight with traditional tools,” Compass Plus Technologies Managing Director and Founder Maria Nottingham said. “FraudAxis combines the power of AI with proven rules-based analysis to give our customers a smarter way forward. It adapts in real time, reduces false positives, and protects the people who trust them—all without slowing down operations or sacrificing the user experience.”

Founded in 2005 and headquartered in Nottingham, UK, Compass Plus Technologies made its Finovate debut at FinovateFall 2012. In the years since, the company has successfully migrated its customers from more than 30 global platforms, and notes that 43% of its customers have been with Compass Plus Technologies for more than a decade. With its flagship offering, TranzAxis, Compass Plus Technologies offers a cloud-native, API-first, token-based alternative to legacy card-based payments infrastructures.

Compass Plus Technologies’ launch of FraudAxis comes in the wake of the company’s announcement of an expanded strategic partnership with enterprise-class data security solutions provider Futurex. This agreement will enable Compass Plus Technologies’ Payment Gateway and Access Control Server (ACS) solutions to support Futurex’s VirtuCrypt Payment Cloud HSM (Hardware Security Module).

Each year at FinovateFall, we look for new and exciting ways to showcase the breadth of fintech innovation that lies just below the radar of the mainstream fintech conversation. This year, we introduced The Impact Zone: a special program for fintech startups that gives them access to highly curated content and demos; unlimited high-level meetings with financial institutions, banks, credit unions, and venture capital firms; and a strategically located table outside the plenary hall to facilitate networking and maximum visibility.

“The Impact Zone debuted at FinovateFall this year, spotlighting eight startups with AI-driven solutions in bill management, wealth management, digital lending, and more,” Finovate VP and Director of Fintech Demos Heather Stowell explained. “Focused on growth and scaling, these innovators are ones to watch—expect to see them on the Finovate stage soon!”

Let’s meet the companies from FinovateFall 2025’s Impact Zone.

AiVantage

Headquartered in Vienna, Virginia, AiVantage provides credit unions, banks, and financial institutions with AI-powered solutions that help them improve efficiency, enable personalized customer engagement, and drive growth.

The company’s flagship solution, InteractiveAI, helps construct each customer interaction uniquely at scale to help financial institutions innovate and stay competitive. Karan Bhalla (LinkedIn) is CEO.

In June, AiVantage announced that it had secured a large strategic investment from Our Community Credit Union (OURCU). The amount of the funding was not disclosed. As part of the investment, OURCU will take a seat on the AiVantage CUSO board of directors.

Blue Street Data

Founded in 2022 and headquartered in Pittsburgh, Pennsylvania, Blue Street Data facilitates the process of finding, evaluating, and purchasing third-party data.

The company’s PQC Engine is an intelligent search platform that enables businesses to discover, compare, and buy high-quality datasets at the optimal price. Including use cases such as personalization, risk modeling, and market analysis, Blue Street Data’s technology helps financial institutions derive greater value from external data. Andy Hannah (LinkedIn) is CEO.

Earlier this year, Blue Street Data announced that it had joined the Sourcing Industry Group, also known as SIG|ORG, an international network for sourcing, procurement, and risk professionals. The company hopes its engagement with the group will elevate the standard for how organizations and businesses evaluate and transact with external data.

CloudBankin

CloudBankin offers an end-to-end cloud-based loan software solution to enhance digital lending. CloudBankin’s Loan Origination System enables a variety of financial institutions—including banks, NBFCs, and MFIs—to disburse loans in less than 10 minutes.

The company’s AI-powered lending agents monitor risk, improve decisioning, and enhance customer engagement across credit underwriting, fraud detection, document intelligence, repayment prediction, and collections. Mani Parthasarathy (LinkedIn) is CEO.

CloudBankin’s Loan Management System has delivered 97% operational efficiency, 50% reduction in time-to-market for product launch, 90% decrease in the data entry error, and 100% compliance with industry regulations. Founded in India, the company’s US headquarters is in Delaware.

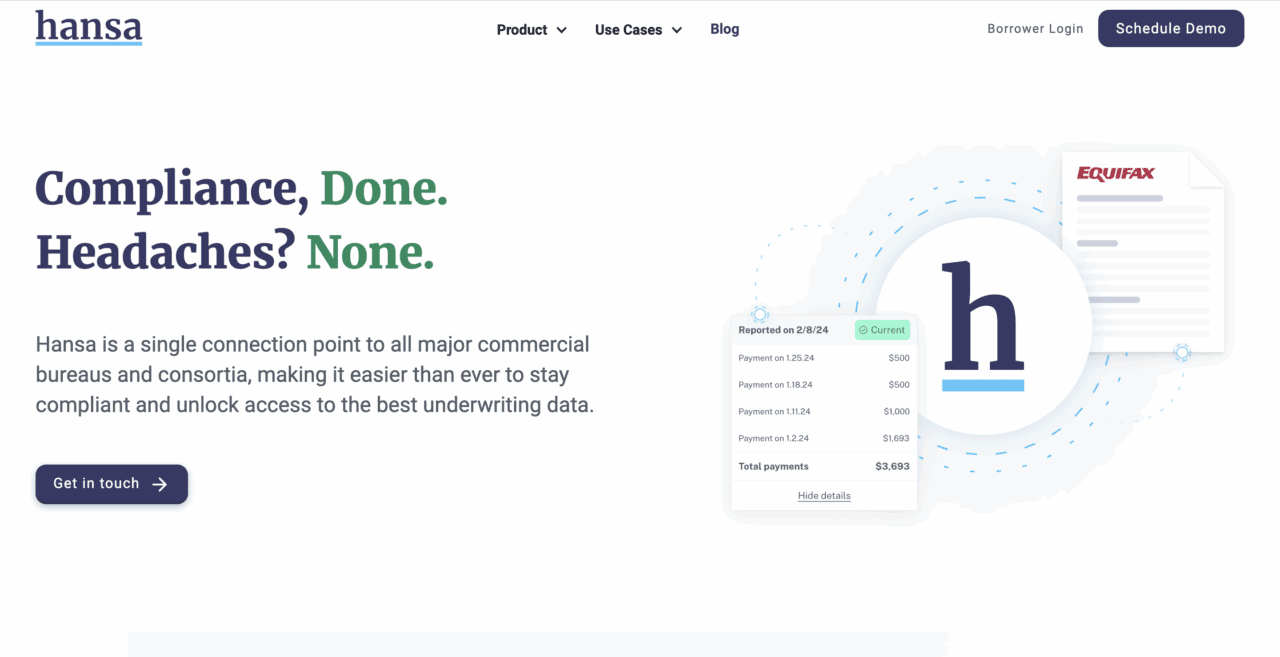

Hansa

Hansa helps lenders report commercial payment data to business credit bureaus. The company serves as a single connection point to all major commercial bureaus and consortia to make it easier for businesses to access the best underwriting data and remain compliant.

Hansa’s technology automates many of the pain points of credit reporting to help reduce delinquencies and support credit-building for small business borrowers. Henry Magun (LinkedIn) is Founder and CEO.

Founded in 2023 and headquartered in New York, Hansa began this year with the launch of its enterprise solution for commercial loan payment reporting. The new offering consists of two key components: a data reporting system that simplifies reporting by transforming and transmitting CSV file and API request data to credit bureaus, and a borrower dashboard that gives borrowers greater transparency on how their payments affect their credit.

Moneylab

Moneylab offers an AI-powered platform that enables banks and credit unions to optimize the way they manage their assets and liabilities.

Headquartered in Vancouver, British Columbia, Canada, Moneylab gives Chief Financial Officers a solution that consists of a collection of AI agents and expert systems that specialize on specific processes such as compiling and writing variance reports, monitoring loan portfolios, and pricing securities assets in real time. Vincent Wong (LinkedIn) is Moneylab Co-Founder and Chairman.

Founded in 2019, Moneylab announced this spring that it had acquired strategic intellectual property from Carfang Group. The all-share transaction will complement Moneylab’s platform offering by providing historical and current data points and analytical processes.

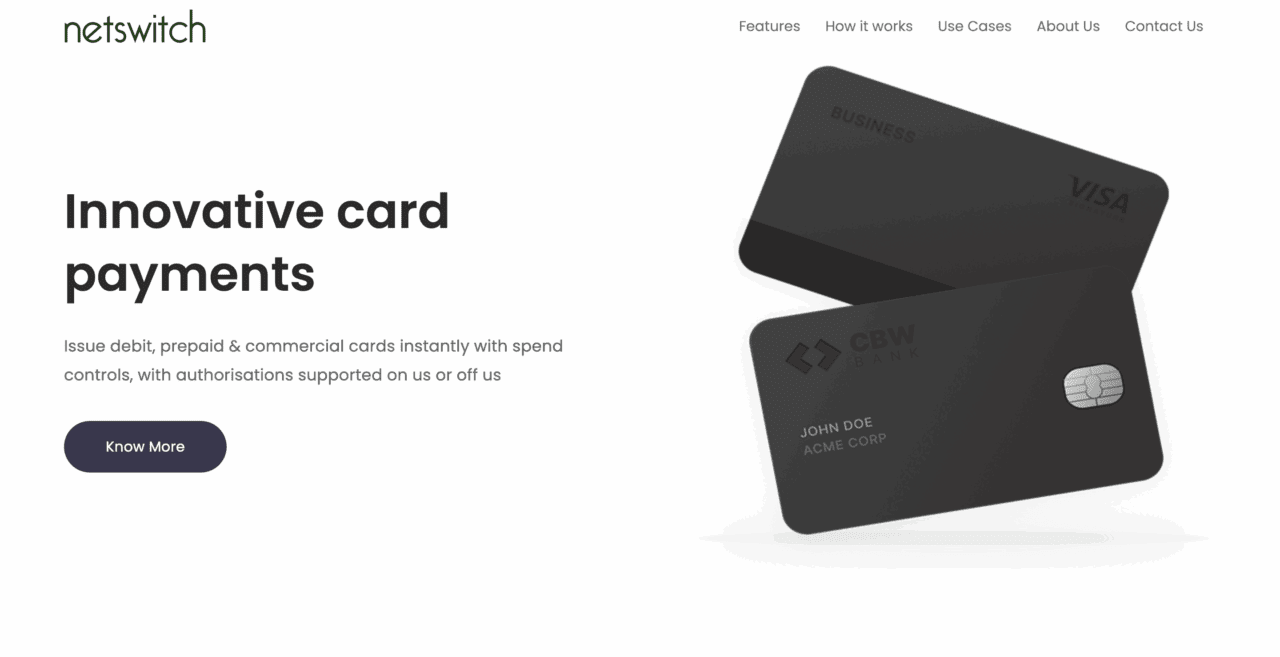

Netswitch Technologies

Netswitch offers a prepaid and debit card processing solution with a built-in ledger that is specially designed for fintechs and sponsor banks.

The company’s platform features pre-configured card controls and compliance workflows. Its custom Large Language Model (LLM) supports quick configuration and faster UI development to ensure rapid onboarding. Kris Lakshmanan (LinkedIn) is CEO.

Founded in 2020 and headquartered in Lawrence, Kansas, Netswitch supports the issuance and processing of debit, virtual, corporate, and employee cards, as well as travel and gift cards.

Nextvestment

Nextvestment offers an AI-native engagement layer for wealth management teams. The platform’s conversational co-pilots transform client questions into trusted conversations, actionable insights, and portfolio guidance.

The technology enables financial advisors to better engage with clients and provide personalized service at scale. At the same time, Nextvestment empowers clients to examine and explore their portfolio and the markets on their own, with a seamless handoff to professional advisors when they need guidance the most. Michael Davies (LinkedIn) is CEO and Founder.

Launched in 2024 and headquartered in Singapore, Nextvestment announced earlier this year that it had joined the NVIDIA Inception Program. The free, virtual accelerator enables startups innovating in AI, data science, and high-performing computing to access NVIDIA developer resources and technical training, go-to-market support and expertise, and exposure to venture capital firms via the NVIDIA Inception VC Alliance.

TrieveTech

TrieveTech offers an AI-powered, multi-tenant, white-label platform that sits at the intersection of bill aggregation, payments, analytics, insights, and customer experience enhancement to enable Energy Service Companies (ESCOs) to easily and quickly brand, customize, launch, and integrate new products and solutions. John Mulcahy is President.

Launched in 2020, TrieveTech is headquartered in Akron, Ohio. The company’s technology helps firms lower overhead costs, reduce customer care needs, and increase customer retention, leading to greater profit margins.

Anti-scam solution provider Scamnetic has unveiled the latest edition of its flagship KnowScam 2.0 fraud protection solution.

KnowScam 2.0 features a variety of enhancements including a new Auto Scan feature and deepfake detection.

Founded in 2023 and headquartered in Tampa, Florida, Scamnetic made its Finovate debut at FinovateFall 2024 in New York. The company returned to the Finovate stage last week for FinovateFall 2025.

Scam protection and digital identity verification company Scamneticrecently introduced its new KnowScam 2.0 offering. The latest edition of the firm’s flagship solution features significant upgrades, including a new three-point scoring system, an Auto Scan feature for Microsoft Outlook and Android RCS, and new deepfake detection and ID verification functionality.

Offering holistic scam-detection, KnowScam 2.0 consists of four major components. Scan & Score automatically scans email and text messages—including QR codes, links, and images—to assess the level of risk from incoming communication. IDeveryone provides defense against dating scams, Facebook marketing scams, crypto scams, and more by identifying the identity of any counterparty whether the interaction is via video, audio, or text. KnowScam 2.0’s Scam Intervention feature helps restore assets and support scam victims as they re-establish their digital security. Lastly, Scam Education provides users with the latest tips and resources on how to protect themselves from scams.

“KnowScam 2.0 marks a major leap forward in proactive scam protection by combining broader platform coverage, automated detection, and instant identity verification—features not offered together by any other consumer-facing anti-scam solution. KnowScam 2.0 advances our goal to provide the most trusted, consumer-first platform for scam detection and digital identity verification, and our mission to make digital interactions safe and secure, providing peace of mind in an increasingly complex digital world,” Scamnetic Chief Operating Officer John Evans said.

KnowScam 2.0 features built-in explainability to inform users of the factors used to produce a scam score and provides highly tailored recommendations based on the type of scam and the overall risk level of the threat. The solution leverages automation and customized machine learning to both remove the potential for human error, as well as avoid relying on third-party LLMs. KnowScam 2.0 instead leverages its own customized machine learning and proprietary technology to spot nine out of every 10 scams.

Headquartered in Tampa, Florida and founded in 2023, Scamnetic made its Finovate debut last year at FinovateFall 2024 in New York. At the conference, the company showed how its technology enables consumers to detect all types of scams in real-time. Scamnetic’s technology can be integrated directly into enterprise platforms, empowering service providers to take a greater role in helping their customers avoid scams. The company returned to the Finovate stage last week for FinovateFall 2025.

Scamnetic’s product update comes at the same time that the company announced that it had been selected to participate in Mastercard’s StartPath Security Solutions program, along with four other security-based startups including fellow Finovate alum OneID. The first cohort of Mastercard’s new security-oriented startup engagement program, Scamnetic, OneID, and three other fintechs will gain access to Mastercard’s network, resources, and market experience. The startups will also benefit from the program’s partnership with organizations such as the Global Anti-Scam Alliance (GASA) which raises awareness and provides enabling tools for both consumers and law enforcement to help facilitate knowledge sharing and the development of best practices against scams and their perpetrators around the world.

PayNearMe raises $50 million in Series E funding, bringing its total funding to $168 million since its founding in 2009.

The company is rebranding its platform as PayXM, signaling a shift from payment processing to Payment Experience Management.

The shift shows PayNearMe’s focus on the customer experience in which it aims to make payments seamless, strategic, and embedded across industries.

Payments innovator PayNearMe is raking in $50 million in Series E funding from Atlantic Vantage Point (AVP). The investment brings PayNearMe’s total raised to $168 million since it was founded in 2009.

The California-based company will use today’s funds to expand into new markets and fuel its product offerings. As part of this, PayNearMe is renaming its platform PayXM, recognizing its product evolution in what it calls Payment Experience Management. The company aims to use PayXM to enable businesses to manage the entire payment journey with a single platform and integration.

“PayNearMe has redefined what it means to deliver a modern payment experience. The company is uniquely positioned to solve challenges in a space long underserved and overlooked,” said AVP General Partner and Head of Growth Fund, North America Elizabeth de Saint-Aignan. “PayNearMe’s vision and proven execution are changing how non-commerce businesses approach payments, and we’re excited to support them in this next stage of growth.”

PayNearMe was founded in 2009 to enable unbanked individuals to transact online by paying with cash at brick-and-mortar retailers. Today, the California-based company offers payment processing, exception management, and diverse payment options for banks, toll companies, mortgage servicing companies, online gaming, auto lenders, and buy here pay here payment collectors.

The move from a pure payments processor to a Payment Experience Management provider reflects PayNearMe’s effort to position its payments offering as a strategic driver of customer experience, not just a back-office function.

“For too long, payments have been treated only as a cost of doing business,” said PayNearMe CEO Danny Shader. “We see improving payments as a powerful opportunity to help businesses differentiate, drive customer satisfaction, and improve business results. AVP’s funding will allow us to deliver the benefits of Payment Experience Management to more clients and in new markets.”

Today’s $50 million investment shows that investors see opportunity in rethinking payments not as plumbing, but as an experience. In launching PayXM, PayNearMe is betting that the next wave of fintech will come from embedding payments to make them invisible, seamless, and integrated into the customer experience.