This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

After rumors swirled over the weekend, we now know that it is official: payments processing company Stripe has acquired stablecoin platform Bridge for $1.1 billion.

For Stripe, which was valued at $70 billion earlier this year, the Bridge deal marks its largest acquisition since it was founded in 2010.

Bridge was founded in 2022 to serve as an alternative payment method to compete with SWIFT and credit cards. The company’s technology allows businesses to move, store, and accept stablecoins using just a few lines of code. Companies can also leverage Bridge’s Issuance APIs to issue their own stablecoin and accept USD, EUR, USDC, USDT or any other stablecoin. After integration has taken place, companies can move money near-instantly and at a low cost around the globe.

“As we’ve gotten to know the Stripe team, it’s become clear that we both share a vision for what’s possible with stablecoins and an excitement around the opportunity to create and build this future,” said Bridge Co-Founder Zach Abrams in a LinkedIn post. “Stripe operates globally and understands better than almost anyone the problems created by our existing localized payment systems. Our teams share an excitement about stablecoins and vision for how to maximize their impact. Together, we’ll be able to solve bigger problems, support more developers, and help more consumers and businesses all across the world.”

Stripe processed $1 trillion in payment volume in 2023, a metric that places the fintech among the top payment processors in the U.S. With this influence, there are a few implications that Stripe’s Bridge acquisition holds for the U.S. stablecoin market.

Increased stablecoin adoption

Once it integrates Bridge’s technology, Stripe will be able to offer instant, low-cost settlements through stablecoins. Creating a low-cost alternative to traditional payments will make stablecoins more attractive for businesses and could lead to wider adoption in mainstream payment systems.

Cross-border payments expansion

The Bridge acquisition may enable Stripe to enhance its global payments infrastructure. This will place stablecoins as a go-to method for faster, cheaper cross-border transactions. In today’s landscape, where large, traditional players are developing new tools for cross-border payments, many still face high fees and longer settlement times. Stripe’s usage of stablecoins will help it circumvent many of those issues.

More competition

Stripe’s entry into the stablecoin space will increase competition among fintechs offering stablecoin-based payment services. The introduction of Stripe’s real-time, cross-border payment service may pressure other companies to create new offerings or improve their existing products to keep up with Stripe’s client base and new resources brought on by today’s acquisition.

Regulatory focus

As Stripe begins to use stablecoins in more traditionally regulated financial environments, it may gain the attention of U.S. regulators. This increased attention toward the stablecoin space may prompt regulators to increase enforcement efforts and could even lead to them creating clearer guidelines around stablecoin use.

Stripe’s acquisition of Bridge will position it as a key player in the stablecoin space. With Stripe’s long-standing payment processing infrastructure and global reach, once Stripe integrates Bridge’s stablecoin technology, it is poised to accelerate stablecoin adoption across mainstream payment systems.

Mastercard launched Move Commercial Payments, a real-time cross-border payments solution that operates 24/7.

The new commercial payments tool leverages a multi-rail system that includes SWIFT and Mastercard’s proprietary networks.

Move Commercial Payments offers features like liquidity management, integration with existing SWIFT systems, and helps to reduce counterparty risk.

Mastercard unveiled an offering this week that will allow commercial users to make cross-border payments in near-real-time. The payments giant introduced Mastercard Move Commercial Payments today, which facilitates payments 24 hours a day, 365 days a year.

Mastercard Move Commercial Payments leverages a multi-rail approach that includes SWIFT, and Mastercard’s proprietary networks to facilitate the cross-border payments. Relying on multiple rails enables banks and their commercial clients to send near-instant, transparent, and predictable transactions any time of day, any day of the week.

Cross-border payments have become increasingly crucial for businesses operating in a global economy. According to a 2023 McKinsey study, global payments revenue grew by double digits in both 2021 and 2022. However, many businesses still struggle with cross-border payments, frustrated by hidden costs and unpredictable settlement speed.

Mastercard Move Commercial Payments offers more than just real-time settlement. The tool also includes several features designed to enhance its value for banks. These features include multiple settlement options that improve liquidity management, a multi-party arrangement to reduce counterparty and default risks, integration with existing SWIFT messaging systems, and compatibility with current correspondent banking relationships. These elements help banks maximize operational efficiency while minimizing risk.

“By powering fast, predictable and transparent payments, Mastercard Move Commercial Payments will bring what is already the norm in domestic payments to the commercial cross-border payment space,” said Mastercard Head of Transfer Solutions Alan Marquard. “Our latest product innovation aims to directly address the pain points that are currently affecting the commercial cross-border payments market. By shifting to this new model, they will be empowered to generate new revenue streams while reducing risk and enhancing the offering for their corporate customers.”

Mastercard Move Commercial Payments, which is part of the company’s Move portfolio, was piloted in the U.K. with Lloyds Banking Group and UBS. This initial phase marked an important step in refining the platform’s capabilities for large-scale deployment. By collaborating with major financial institutions, Mastercard was able to validate the efficiency of its multi-rail payment system, demonstrating the platform’s market readiness and paving the way for broader adoption.

Mastercard’s launch competes with Visa’s real-time payments solution called Visa Direct, which enables fast and secure money movement to different endpoints across the globe. Similar to Mastercard’s Move Commercial Payments, Visa Direct also leverages a multi-rail approach that supports card-based and account-to-account transfers that integrate with The Clearing House RTP and FedNow.

Today’s launch comes amid a string of other payments-related news releases this month, as both fintechs and traditional financial services firms seek to capitalize on the recent consumer awareness of real-time payments generated from last year’s FedNow launch. Just last week, for example, we covered news from Worldline, which unveiled an account-to-account transfer tool in Europe, Tyfone’slaunch of Payfinia instant payments solution, and Token.io’s real-time payments partnership with Santander.

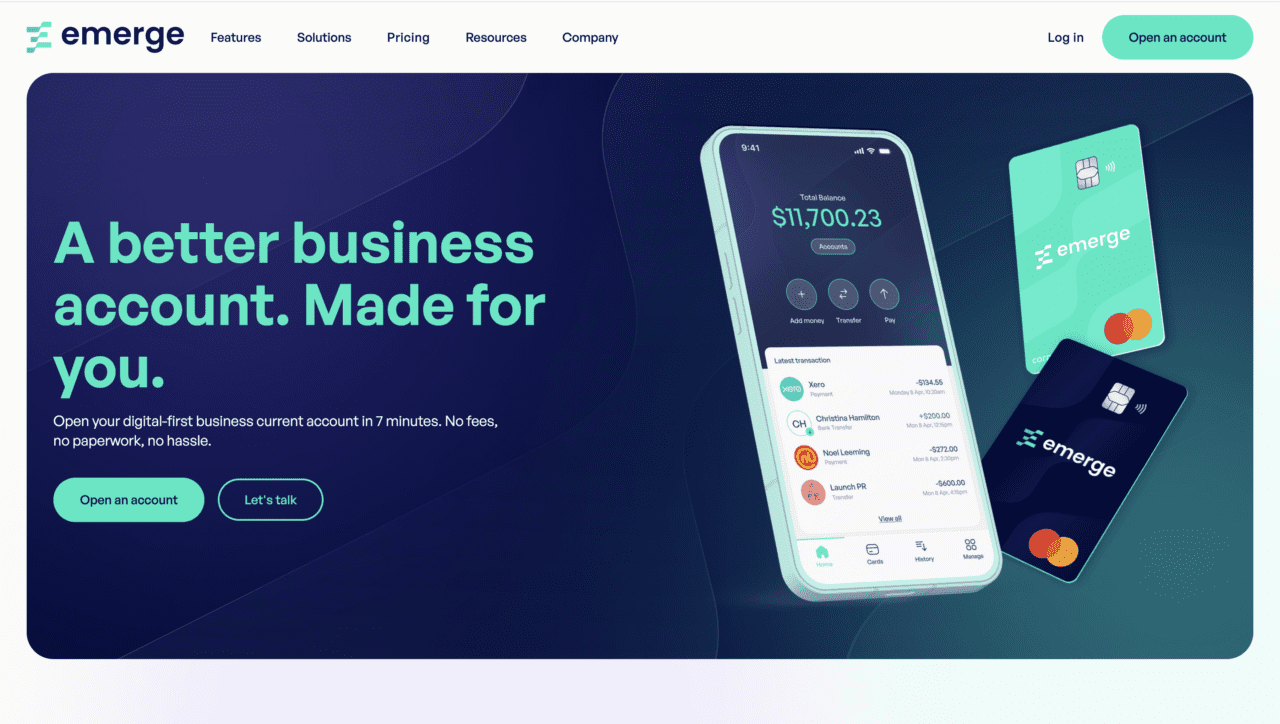

The round also featured participation from Icehouse Ventures, K1W1, NZ Fintech Fund, and Hard Yaka, a venture capital firm based in the U.S. Emerge will use the capital to support adding talent in marketing, sales, and product development. The company will also use the funds to accelerate its go-to-market strategy, including offering banking services to startups.

“Emerge was built to help Kiwi businesses do more, faster, better,” Emerge Co-founder Jovan Pavlicevic said. “In just a few minutes, you’ve opened as many Emerge accounts as you need, with features better than the banks, and team cards ready to go.”

A digital-first banking alternative, Emerge offers companies a single platform to manage their business finances. Emerge’s technology simplifies expense tracking, enables the creation of debit cards — including an unlimited number of virtual cards — and allows users to make and receive payments with a New Zealand business banking account backed by ANZ. Emerge provides bookkeeping and reporting tools and makes it easier for companies to track and manage their finances with a centralized view of their data. The company has also launched a service called EmergePay that converts a smartphone into a payment terminal.

Emerge evolved from a children’s financial literacy app called SquareOne that Pavlicevic and co-founder Jamie Jermain founded in 2020. Emerge was developed in January 2024, as the company shifted its focus toward providing banking services for SMEs, with the ultimate goal of becoming a neobank.

Headquartered in Auckland, Emerge was named to the Forbes Asia “Top 100 to Watch” in August.

FirstCape deploys wealthtech from InvestCloud

New Zealand’s largest wealth advice and asset management company, FirstCape, has partnered with InvestCloud to enhance the wealth management experience for advisors and clients alike. The deployment will help FirstCape increase the efficiency of its advisors, as well as provide a single platform for client engagement, experience, and advice at scale.

“We formed FirstCape with a stated intention of enhancing our client offering,” FirstCape CEO Malcolm Jackson said. “Integrating InvestCloud’s tools that streamline portfolio management and order execution is part of delivering on that promise. We continue to be focused on providing a complete suite of services tailored to every client’s unique needs at whatever stage of their investment life cycle.”

With more than 120 advisors and more than $30.3 billion (NZ $50 billion) in assets under management, FirstCape was forged earlier this year through the combination of four entities: JBWere NZ, Jarden Wealth, Harbour Asset Management, and BNZ Investment Services. The company has already deployed two InvestCloud solutions: Portfolio Manager and Order Capture. Portfolio Manager enables advisors to manage client portfolios with deeper insights that lead to tailored investment proposals. Order Capture provides a seamless interface for trading across asset classes, boosting operational efficiency by enabling advisors to act faster in response to client needs.

“We are thrilled to see the tangible success of our partnership with FirstCape as they embark on this modular digital transformation,” InvestCloud President of Digital Wealth International Christine Mar Ciriani said. “By leveraging our full suite of innovative front-office solutions, we are helping FirstCape create a robust digital backbone that will drive their growth, streamline advisor efficiency, and elevate client experiences.”

A global wealthtech company, InvestCloud serves wealth and asset managers, wirehouses, banks, RIAs, and insurers. InvestCloud’s clients represent more than 40% of the $132 trillion in total assets globally. A provider of digital wealth management and financial planning solutions since 2010, InvestCloud was named a CNBC “World’s Top Fintech Company” earlier this year. The firm is headquartered in West Hollywood, California.

International payments specialist Ebury arrives in New Zealand

Ebury, a specialist in international payments and collections, opened new offices in New Zealand this week. The move is designed to help the company provide a range of services to SMEs in the country, including cash management strategy and foreign exchange risk management.

“At Ebury, we embrace the complexity and risk of daily cross-border payments that enable business growth, in a way that traditional banks do not, or cannot,” Ebury Managing Director for APAC, Rick Roache said. “We make the sophisticated products and services that banks typically reserve for their biggest clients accessible to SMEs.”

The New Zealand office represents Ebury’s 40th office worldwide, and comes six years after Ebury expanded to neighboring Australia. The move to New Zealand also supports the company’s presence in nearby Shanghai and Shenzhen in China.

“Right now there are few options for SMEs looking for cross-border payment solutions and local advice in New Zealand,” Roache added, “so we’re really excited to bring our innovative technology platform into the market supported by a ‘boots on the ground’ team that differentiates us from other providers.”

Headquartered in London and founded in 2009 by a pair of Spanish engineers, Ebury serves primarily SMEs and mid-cap companies with payments, collections, and foreign exchange services in more than 130 currencies. Santander acquired a minority stake in the company for $459 million (£350 million) in 2020, and added to its stake two years later. With more than 1,700 employees across 25 countries, Ebury is reportedly preparing for an IPO in 2025 that would value the company at as much as $2.2 billion (£2 billion).

Here is our look at fintech innovation around the world.

Latin America and the Caribbean

Warburg Pincus acquired a minority stake in Brazilian accounting-based fintech Contabilizei for $125 million.

PXP Financial teamed up with Latin American payments platform Kushki.

Brazilian paytech Barte raised $8 million in Series A funding in a round led by AlleyCorp.

Asia-Pacific

Singapore-based finance platform for businesses, Aspire, secured in-principal approval for the Major Payment Institution license from the Monetary Authority of Singapore (MAS).

Bank of Hangzhou teamed up with Malaysia’s Maybank to support Chinese businesses as they expand operations in Southeast Asia.

Vietnamese private bank VPBank partnered with customer engagement platform CleverTap.

Sub-Saharan Africa

Somalia’s Premier Bank has teamed up with Mastercard and Tappy Technologies to launch Tap2Pay, a tokenized-passive payment wearable.

Fintech provider Flutterwave partnered with 9jahotel.com to launch a point-of-sale system to enhance hotel management in Nigeria.

Nigerian cryptocurrency exchange Yellow Card secured $33 million in Series C funding.

Central and Eastern Europe

Romanian payment service Pago secured $2.5 million (€2.3 million) to fuel expansion.

Budapest, Hungary-based B2B payment solutions provider, PastPay, raised $13 million (€12 million) in Series A funding.

Fingular, a neobank based in Singapore, launched a new digital lending business in Bangladesh.

TBC Bank Uzbekistan secured a $10 million line of credit from Switzerland’s responsAbility Investments AG. Read our Finovate Global interview with TBC Bank Uzbekistan’s Head of International Business Oliver Hughes.

One of the most popular use cases for AI in financial services is to leverage the technology to help companies deal with the challenge and opportunity of unstructured data.

In our latest Streamly interview from FinovateFall last month, Finovate VP and host Greg Palmer sits down with Perry Rotella, Managing Director of Financial Services at Box, to discuss the growth of unstructured data within financial institutions, the challenges these firms face in managing this data, and the role AI can play in helping them analyze unstructured data to enhance everything from personalization to compliance.

“Unstructured data really represents the vast majority of data in organizations. IDC did a study last year that found that 90% of an organization’s data is unstructured. And it’s been really challenging to extract insights out of that data at scale. What we’ve been finding working with customers is we can supercharge pulling insights out of that content, driving workflows for downstream processing, and really look across many documents to summarize and personalize communications with clients.”

The “Intelligent Content Cloud” company, Box offers a single platform that enables organizations to drive collaboration, manage the content lifecycle, secure critical content, and transform business workflows using enterprise AI. Founded in 2005 and headquartered in Redwood City, California, Box includes AstraZeneca, Morgan Stanley, and Nationwide among its customers.

In his role as Managing Director, Financial Services, Rotella provides leadership across product, marketing, business development, sales, and customer success teams. He is responsible for driving engagement with key strategic accounts, as well as customer satisfaction and retention.

Apex Fintech Solutions has agreed to acquire fintech design agency, FinTron. Terms of the transaction have not been disclosed.

The digital wealth management company will leverage FinTron’s technology to provide its customers with the ability to create customized user interfaces and experiences.

Apex Fintech Solutions’ subsidiary Apex Clearing made its Finovate debut at FinDEVr Silicon Valley in 2015.

Digital wealth management company Apex Fintech Solutions has agreed to acquire FinTron, a fintech design agency that creates high-end digital experiences for investors and advisors around the world.

Terms of the transaction were not disclosed and the deal is subject to approval by FINRA. Once completed, the strategic acquisition will enable Apex’s customers to deliver customized user interfaces and experiences for brokerage platforms that are pre-integrated into the Apex platform. This will enable them to easily deploy turnkey investing experiences and front-ends from within their current digital footprint, powered by Apex’s custody platform.

“FinTron has revolutionized the process of launching a brokerage or wealth management platform,” Apex CEO Bill Capuzzi said. “Their innovative platform aligns perfectly with our mission to empower the next generation of investors through technology. This acquisition is a significant step in our journey to provide a fully integrated, digital-first platform that meets the diverse needs of our clients.”

Known for its white-label and embedded components, as well as its Software Development Kit (SDK) for mobile and web platforms, FinTron empowers brokerages and wealth management firms to embed self-directed and managed investing functionality into their offering. Apex will leverage its acquisition of FinTron to expand its services to clients ranging from financial advisors and fintech firms to neobanks, insurance companies, and retirement planning companies. In fact, FinTron’s technology already has been integrated into the company’s suite of services to streamline investment processes, enhance the user experience, and bring more advanced investment capabilities to a wider audience of investors.

“We are thrilled to join forces with Apex,” FinTron CEO and Founder Wilder Rumpf said. “Our shared vision of democratizing financial services and providing intuitive, powerful tools to investors will only be strengthened through this partnership. Together, we can make a significant impact on the financial futures of many.”

Headquartered in Stamford, Connecticut, FinTron was founded in 2017. The company has raised more than $14 million in funding from investors including Connecticut Innovations and Sage Venture Partners. FinTron’s embedded wealth solutions help broker-dealers, community banks and credit unions, investment advisors, and fintechs lower CAPEX and time to market, capture engagement, and offer clients versatile digital wealth experiences.

Apex Fintech Solutions introduced itself to Finovate audiences at our developers conference, FinDEVr Silicon Valley in 2015, via its subsidiary, Apex Clearing. Recently, the New York-based company launched its real-time cloud-native investment infrastructure, Apex Ascend, and announced a collaboration with wealth management solution provider YourStake. FinTron is Apex’s fourth acquisition; the firm purchased AdvisorArch, its third acquisition, in March of this year.

Worldline has launched Bank Transfer by Worldline, an account-to-account payment tool.

The new pay-by-bank solution enables retailers to accept bank draft payments and handle high-value transactions, including B2B payments, across 10 European countries.

Bank Transfer by Worldline also facilitates cross-border payments, leveraging Worldline’s open banking network to connect with over 3,500 banks, providing merchants a seamless way to initiate payments directly from customer bank accounts, reducing transaction fees and declines.

Payments services company Worldline is launching yet another payment tool this week. After debuting its embedded payments tool earlier this month, the France-based company is launchingBank Transfer by Worldline, an account-to-account payment method.

The new pay-by-bank solution enables retailers to accept bank draft payments and allows for non-traditional payment methods, including invoices and high-value transactions. Bank Transfer by Worldline boasts many of the same benefits that popular pay-by-bank tools offer.

The solution is notably different from traditional pay-by-bank offerings in the U.S. because it facilitates cross-border payments. This is key for merchants operating across multiple geographies. Additionally, the new payments tool specializes in high-value transactions– including B2B transactions– that typically incur higher fees and reduces the number of declined transactions, since funds are validated directly from the bank account.

“With Bank Transfer by Worldline, we have developed a payment method grounded in trust and simplicity, leveraging existing European payment networks and offering innovative customer experience,” said company Head of Merchant Services Paul Marriott-Clarke. “This launch reinforces our commitment to making payment solutions accessible for all.”

Bank Transfer by Worldline, which went live in August of 2024, allows merchants to accept payments from around 300 million customers. After a nine-month pilot phase, the solution now counts about 500 Worldline merchants clients using Bank Transfer by Worldline’s online payment solutions and pay-by-link services.

“By integrating Worldline’s open banking solution, which connects to over 3,500 banks across European countries, Bank Transfer by Worldline offers merchants a solution that simplifies payment initiation via bank transfer and unifies the customer experience,” said Worldline Head of Financial Services Alessandro Baroni.

The new tool is available for merchants in 10 European countries, including Austria, Belgium, Croatia, France, Germany, Italy, Luxembourg, the Netherlands, Slovenia and Spain. The company aims to launch in another four regions– Poland, Slovakia, Czech Republic and Hungary– by the end of 2024. Eventually, Bank Transfer by Worldline will be available to all eligible merchants across the EU.

FedNow, the U.S. Federal Reserve’s instant payment service went live in July of 2023. Now, 15 months later, adoption rates have been unpredictably slow, especially when it comes to banks that are able to send FedNow payments.

Before considering the challenges behind sending and receiving FedNow payments, here’s a look at some of the data behind adoption rates:

Only around 900 financial institutions have connected to the FedNow network, a fraction of the 8,000 firms the Fed stated as its goal.

Close to 60% of the financial institutions on board with FedNow can receive payments, while only 40% of firms have signed up to send payments.

Banks connected to the FedNow network range in size from under $500 million to more than $3 trillion in assets.

Of the FedNow participants, 78% are community banks and credit unions.

There are a handful of reasons why firms might be hesitant to participate in FedNow. The service faces competition with The Clearing House’s RTP platform, which was launched well before FedNow went live. Additionally, banks may be holding back because of the fees that come with participating in FedNow. Banks must pay $25 per month per routing transit number to use the service, plus a $0.045 per credit transfer fee charged to the sender and a $0.01 per RFP message, charged to the requestor. The Fed also charges a liquidity management fee of $1 per transfer.

Another reason firms may be reluctant to join FedNow is that the new payment rail comes with a set of challenges for both sending and receiving payment. Below, I’ve outlined five challenges financial institutions face for accepting FedNow payments, and five challenges they face when receiving FedNow payments, along with strategies to overcome each obstacle.

Challenges in accepting FedNow payments

1. Transaction validation in real time Firms may have difficulty validating incoming payments instantly, especially considering the need to check for insufficient funds and fraud, plus ensure compliance, all in real time.

To combat this, firms can implement automated validation systems to check the accuracy, authenticity, and compliance of payment transactions in real time. They can also use AI tools for fraud detection to help banks validate transactions without human intervention. Additionally, they should enhance their AML compliance systems to conduct rapid checks.

2. Managing customer disputes Customer disputes are always a headache when facilitating payments. And with instant payments, customer disputes can be even more of a challenge. That’s because instant payments reduce the time that dispute resolution can take place, since the funds are transferred immediately.

Banks should create dedicated customer service channels and clearly communicate the dispute resolution process to consumers. Additionally, banks should create robust communication procedures with other banks in the FedNow network in order to resolve reversals and other issues quickly.

3. Handling a high volume of payments If the adoption of FedNow grows, banks will need to process higher volumes of payments as more customers use the new payment rail. This increase could strain legacy systems– especially if they are not optimized for 24/7 processing at high volumes– and ultimately lead to payment delays.

To overcome this, banks should scale their payment processing infrastructure by adopting cloud solutions and ensuring they have sufficient bandwidth to handle high transaction volumes, especially during peak times.

4. Ensuring compliance in real time Just as they do with ACH payments, banks need to ensure they are complying with regulatory requirements, including KYC, AML, and other regulations. This is an additional challenge with FedNow payments, since the compliance checks and documentation need to be made in real time.

Banks can leverage automation for compliance checks and integrate real-time monitoring tools into their operations to ensure that incoming payments are compliant without delaying the transaction. As with all compliance training, firms should ensure that their compliance officers’ training is up-to-date. Fortunately, there are multiple regtech solutions, including ComplyAdvantage, Trulioo, and Fenergo, available to help.

5. Creating a seamless user experience In today’s digital age, consumers are not only used to receiving things instantly, they expect it. With instant payments as the standard, any delays or issues in receiving funds could create a poor user experience and tarnish the bank’s brand.

To ensure the best user experience, banks should first invest in a user-friendly interface. Transparent and timely communication is also key. Firms should offer real-time notifications and ensure that customers have easy access to their transaction history.

Challenges in sending FedNow payments

1. Ensuring adequate liquidity With the recent increased scrutiny on adequate liquidity, it is essential that banks ensure they have enough funds on hand. With instant payments, banks must have sufficient liquidity available at all times, even during weekends and non-business hours.

To overcome this, firms can implement real-time liquidity monitoring systems and use the Federal Reserve’s liquidity management services. Banks should also establish internal controls to maintain and managing their liquidity reserves effectively.

2. Maintaining 24/7 availability This may be one of the biggest headaches for banks looking to send FedNow payments. Because FedNow operates 24/7, banks need to ensure they have adequate infrastructure and staffing to support continuous operations. This can be a particular headache for smaller institutions, which lack resources to support such uptime.

To keep up with availability requirements, banks can adopt automated processing systems, use cloud-based solutions to keep their operations scalable, and partner with third-party vendors who offer 24/7 payment support. Additionally, firms should conduct regular system maintenance during non-peak hours to ensure they are not disrupting operations.

3. Ensuring fraud and security protection Just as when receiving instant payments, accepting instant payments does not leave banks much time to identify and stop fraudulent transactions. This increases the risk for loss.

Banks can add a layer of protection by deploying real-time fraud monitoring systems to detect suspicious activities using AI and machine learning. Also, firms can implement advanced consumer authentication methods and mandate ongoing fraud prevention training for staff to further mitigate risks.

4. Managing customer payment errors With instant payments, there is not much time to correct mistakes. When consumers fat-finger the payment amount or send the funds to the wrong recipient, they lose the opportunity to correct errors. This could not only create customer dissatisfaction, but also lead to financial losses.

Fortunately, there are ways to mitigate such mistakes. Banks can add confirmation steps into the user interface that require users to verify payment details before the transaction is sent for processing. It is equally as important to educate customers about the finality of real-time payments and provide them with a clear process for dealing with errors.

5. Creating interoperability with other payment networks As with other payment rails, banks need to ensure their systems are compatible across other systems. Banks should create a system that is not only compatible with FedNow, but also with other real-time payment systems, including The Clearing House’s RTP.

To ensure compatibility, banks can invest in unified payment platforms that integrate multiple payment rails. Additionally, firms may find it helpful to participate in industry-standard development efforts to help shape the conversation around compatibility and functionality.

Monzo launched Team, a new offering aimed at larger small businesses that outgrow its Business Pro and Lite plans.

Team includes the same tools as Pro and Lite plans, but also offers features such as employee expense cards, bulk payments, and account access for up to 15 members.

Team is available in the U.K. and is priced at £25 per month.

U.K.-based digital banking platform Monzo is building out its small business offerings this week with the launch of Team.

Monzo’s Team offering complements Monzo Business Pro and Monzo Business Lite plans, which collectively serve more than 500,000 businesses. The digital bank created Team to serve businesses that are too large to have their needs met by either the Pro or Lite plans.

“With Team, we’re bringing that to bigger small businesses by introducing features that teams need to help run the business day-to-day,” the company said in its blog post announcement. “Bigger, more complex teams up and down the country whose needs weren’t being met by our Lite and Pro plans before.”

Monzo’s Team product comes with all of the products and services that Lite and Pro offer, including Tax Pots for tax savings accounts, invoicing, integrated accounting and more. Additionally, the new Team accounts come with employee expense cards, offer the ability to create payment approval limits, as well as the capabilities to tailor individual account access levels for up to 15 people.

Notably, Team also allows for bulk payments. Businesses can use Team to upload payee details and make multiple payments at the same time for things like salaries and suppliers, without having to worry about manually entering the payee details every time.

Limited companies can have up to 15 team members and sole traders can have a team of three people and set what individual team members can see and do. Pricing for Teams, which is currently only available to businesses in the U.K., starts at $32 (£25) a month.

Founded in 2015, Monzo is one of the earlier small business digital bank providers. The company also offers personal accounts. With 10 million personal credit card holders, Monzo also provides savings, pension, investments, debit cards, and loan products. Monzo’s competitors include well known brands such as Revolut, Starling, N26, and Monese.

Payments credit union service organization (CUSO) Velera has turned to Arroweye Solutions for its dual interface debit and credit card portfolio.

The multi-year partnership will provide faster speed to market and change orders, as well as zero inventory to avoid having to manage stores of pre-printed cards.

Headquartered in Nevada, Arroweye made its Finovate debut at FinovateSpring 2011.

Payments credit union service organization (CUSO) Velera has partnered with Arroweye Solutions to provide card production, personalization, and fulfillment for Velera’s dual interface debit and credit card portfolio.

The multi-year partnership announced this week will enable Arroweye to provide Velera and its financial institution partners with a variety of benefits for their card programs. These include fast speed to market and change orders; dynamic card personalization; zero inventory as cards are manufactured, personalized, and fulfilled as needed; quality materials, vertical or horizontal orientation, and other options.

“Supporting Velera’s card diversification strategy, Arroweye’s capabilities will help Velera enhance time to market and deliver a more seamless, frictionless card personalization experience to our financial institutions’ clients,” Velera SVP for Product Enablement & Growth, Cody Banks said. “We view Arroweye as a true financial services partner and look forward to integrating their suite of capabilities into our core offering.”

Arroweye CEO Dan Oswald praised Velera as a “premier fintech solutions provider for credit unions in North America.” Oswald added, “Arroweye’s solutions and capabilities align perfectly with Velera’s card issuance needs today and into the future, and we look forward to providing Arroweye’s best-in-class services to their financial institutions.”

Created via a merger between PSCU and Co-op Solutions earlier this year, Velera is both a premier payments credit union service organization (CUSO) and an integrated fintech solutions provider. Velera serves more than 4,000 financial institutions throughout North America, offering a product portfolio that features solutions for payment processing, fraud and risk management, data and analytics, digital banking, instant payments, strategic consulting, ATM and POS networks, and more. Charles E. Fagan III is President and CEO.

Founded in 2000, Arroweye Solutions made its Finovate debut at FinovateSpring 2011. In the years since, the Henderson, Nevada-based company has grown into a leading card delivery firm, offering EMV, dual-interface, and magnetic stripe cards approved by Visa, Mastercard, American Express, Discover, and UnionPay.

This year, Arroweye has formed partnerships with small business financial services platform Affinity Finance and professional banking services provider BankPro, a subsidiary of FxPro Group. The company has raised more than $76 million in funding according to Crunchbase, and includes Multiplier Capital and Landa Ventures among its investors.

Tyfoneannounced the formation of a new spinout today. The company launched the new entity, Payfinia, to provide instant payment solutions to both financial institutions and third-party organizations.

Payfinia aims to help financial institutions access and establish ownership of their instant payments services. The company also helps third-party organizations across various industries integrate instant payments with traditional payment tools into their existing payment and money movement use cases including A2A, P2P, Bill Payment, B2B and B2C disbursements.

Tyfone formed Payfinia by shifting its IP and technology, including advanced UX and security protocols, to the new company. Payfinia hinges on Tyfone’s Instant Payment Xchange (IPX), a money movement gateway to FedNow that will serve as Payfinia’s flagship offering.

Tyfone launched its IPX platform in July 2023, in conjunction with the Federal Reserve’s FedNow instant payment service. Since launch, IPX has converted nearly 30% of same-day ACH credit transactions into send transactions on push instant payment systems, routing existing payment solutions through networks like FedNow. Launching Payfinia will help Tyfone further build on the instant payments experience.

“We’ve seen remarkable results with our Instant Payment Xchange, achieving 50% less fraud compared to Same-Day ACH and fourfold reductions over other P2P solutions,” said Tyfone CEO Siva Narendra. “As we launch Payfinia, we’re doubling down on security with cryptographic, deterministic methods aimed at countering AI-driven fraud risks, while ensuring instant payments remain efficient, secure and accessible. This is just the beginning of Payfinia’s impact across industries.”

Integrating FedNow’s instant payments service, which the U.S. Federal Reserve launched in July of 2023, has led to a host of challenges for banks. These challenges include building a complex integration for real-time payment systems, maintaining compliance with security standards, and ensuring a seamless user experience across digital platforms.

With IPX, Payfinia is positioned to help financial services companies overcome these obstacles. That’s because the IPX platform offers real-time connectivity to both FedNow and RTP networks, helping banks eliminate the need for multiple integrations when adopting both instant payment systems. Additionally, Payfinia provides enhanced security and compliance as well as user-friendly digital tools that can help firms integrate the new technology into their existing interface. Payfinia also ensures a scalable, unified experience across multiple channels.

Tyfone is one of the earlier Finovate alums, having demoed at the first Finovate event to take place in San Francisco– FinovateSpring 2008. At the show, Tyfone Co-Founder Siva Narendra demoed a memory card for a mobile phone that facilitated contactless payments. The company, which used to focus on mobile-only solutions, began developing for multiple channels in 2014.

Tyfone was founded in 2004 and provides digital banking and payment solutions. In addition to its instant payments tools, the Oregon-based company offers nFinia, an enterprise solution that allows community financial institutions to deliver a hyper-personalized digital banking experience to both retail and commercial customers. The configurable solution offers more than 300 financial functions and provides an open ecosystem with direct integrations with more than 160 players.

Brex and Navan have teamed up to launch BrexPay for Navan, a business travel and payments solution that combines Brex’s global payments infrastructure with Navan’s travel-booking system.

The new tool leverages Navan Connect and Brex Embedded, and will allow companies to use their existing payment cards while benefitting from automated receipts and reconciliation.

This partnership will offer Navan a competitive edge by creating a scalable travel program with local currency cards and a seamless payments integration.

Corporate card and expense management fintech Brex has partnered with travel and expense solution Navan to launch a joint offering.

The new product, BrexPay for Navan, is an integrated business travel and payments solution for Navan users that streamlines travel payments into a single workflow when using the Navan travel management system. The new tool taps Navan Connect, a card-link technology that allows companies to use their existing payment cards and banking relationships, and Brex’s embedded finance tool, Brex Embedded.

The result of the collaboration is a direct integration between Brex’s global payments infrastructure and Navan’s travel-booking infrastructure. The new tools offer Navan’s business clients higher limits than legacy cards and local currency cards across more than 50 countries, a scalable travel program that facilitates compliance and helps reduce costs, and automated receipts and reconciliation that saves companies hours of accounting time each month.

“With BrexPay for Navan, we are bringing something truly unique and monumental to the market,” said Brex CEO Pedro Franceschi. “By combining Brex’s fast onboarding, global acceptance, and homegrown financial stack with Navan’s end-to-end business travel offering into one solution, customers now have access to a payments and travel experience that is beyond any other corporate travel and payments solution.”

For Navan, integrating payments into its existing corporate travel booking tool has the potential to both attract new clients and maintain its existing client base. That’s because for Navan, integrating payments into its existing corporate travel booking tool has the potential to both attract new clients and maintain its existing client base by offering businesses a single, cohesive solution for managing both travel and payments, eliminating the need to juggle multiple platforms.

By combining Brex’s multi-faceted financial infrastructure with Navan’s travel management system, companies benefit from higher credit limits, local currency options, and automated reconciliation, making it easier to scale travel programs globally while saving time and reducing costs. The move not only simplifies operations, but also enhances the overall user experience, giving Navan a competitive edge in a market that values efficiency and innovation.

Brex was founded in 2017 to create a digital-first business banking solution. The company offers business bank accounts with credit cards that have built-in rewards, spend controls, and expense tracking. The accounts provide businesses access to their online revenue, billpay tools, and integration with popular accounting tools.

Brex quickly rose to prominence in the fintech space after positioning itself as a digital bank account and card offering for startups. The company sought to solve pain points that often come with corporate cards, including lengthy approval processes and restrictive credit limits. Within just two years, Brex managed to raise billions of dollars in funding and achieve unicorn status.

In 2022, however, as Brex expanded its focus from small businesses to larger, venture-backed companies, the company experienced a downward shift. Because Brex discontinued some of its services geared toward small businesses– its original customer base– many customers left to seek alternative solutions. negative backlash.

Despite the dip, Brex remains a major player in the fintech space, serving “tens of thousands of businesses” ranging from small private companies to large public brands, including Airbnb and Classpass.

The goal of the collaboration is for the bank to leverage Token.io’s open banking connectivity and infrastructure to enhance the customer experience and develop new, real-time payment solutions. Santander will first use Token.io’s infrastructure to enable direct payments from external bank accounts as an option for credit card repayments, creating a more seamless payment experience compared to both direct debit and manual bank transfer. These direct account-to-account payments for card repayments also support biometric Strong Customer Authentication (SCA) for payments made on mobile devices.

“We are thrilled to partner with Santander, a forward-thinking institution committed to driving open banking innovation and enhancing the experience of millions of customers,” Token.io CEO Todd Clyde said. “Token.io’s technology, combined with Santander’s dedication to exceptional service, will undoubtedly set new standards for how financial institutions leverage open banking to create innovative value propositions that meet the evolving needs of consumers and businesses.”

A subsidiary of Banco Santander, Santander UK has more than 14 million customers in the U.K. The bank offers mortgages, auto financing, unsecured loans, credit cards, banking, savings and investment accounts, as well as insurance products. In addition to using Token.io’s technology to support its A2A offering, Santander UK also plans to leverage the fintech’s infrastructure to enhance its real-time money movement capabilities for its retail banking customers.

This week’s news from Token.io comes just days after the U.K.-based fintech announced that it had expanded its partnership with global payments platform Ecommpay. The global payments platform added Token.io’s virtual accounts in four new markets — France, Ireland, the Netherlands, and Spain — to its Open Banking Advanced solution. The virtual accounts will enable e-commerce companies to get real-time settlement confirmation and make API-powered refunds or payouts, boosting both the speed and efficiency of transactions.

“Our partnership with Ecommpay continues to demonstrate the immense potential of open banking in transforming payment experiences and also highlights the opportunities that PSPs can realize when they embrace innovative, customer-centric solutions,” Clyde said.

Token.io made its Finovate debut at FinovateSpring 2015 and returned to the Finovate stage two years later at FinovateEurope in London. The company provides direct connectivity to more than 567 million bank accounts in 20 markets. Token.io’s customers include HSBC, BNP Paribas, and Global Payments, as well as fellow Finovate alums Mastercard and ACI Worldwide. The company has raised $90 million in funding according to Crunchbase, most recently securing a Series C investment of $40 million in 2022.