This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

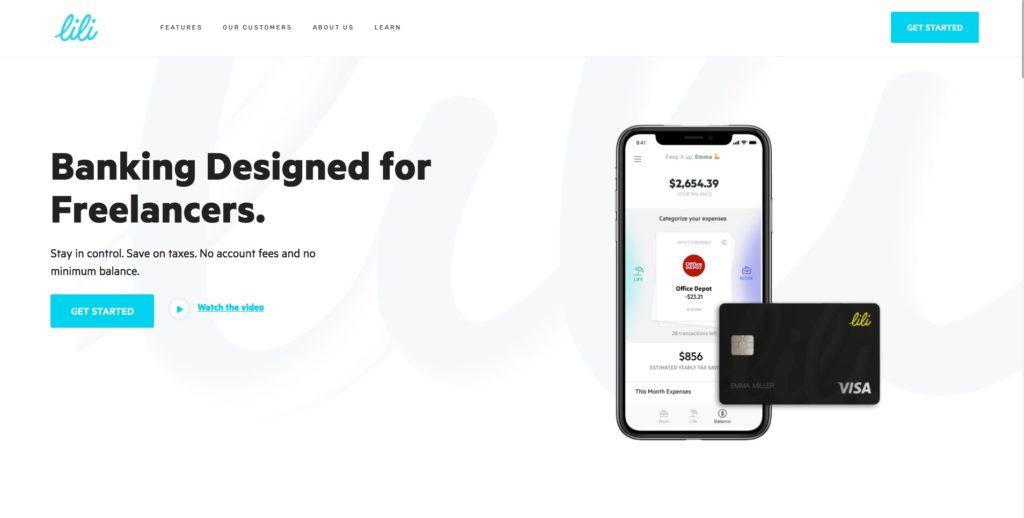

In a round led by Group 11, banking app Lili has secured $55 million in Series B funding. The capital will help the New York-based fintech grow its product range over the next few months. This will include the addition of new features for invoice and payment management and a new loans product.

“We’ve created the tools you need to spend more time building your venture and less time on things that historically your employer would handle: sorting expenses, managing financials, and filing taxes,” Lili CEO and co-founder Lilac Bar David explained.

The Series B took the two-year old company’s total capital to $80 million. Also participating in the investment were Target Global and AltaIR.

Having doubled its account base over the past six months and currently boasting 200,000 users, Lili offers real-time expense management, tax preparation, and no-fee accounts designed for freelancers and gig economy workers. Lili also provides direct deposit and a Visa business debit card with free ATM withdrawals at more than 32,000 locations.

Named to the Forbes Next 1000 list for 2021, Bar David co-founded Lili having spent three years as CEO of Israeli challenger bank, Pepper. Along with current Lili CTO and co-founder Liran Zelkha, Bar David’s goal was to build a solution for workers in the freelance economy that combined banking and business management services into a single platform. She estimated that Lili has saved its users 60 hours on administrative tasks and $1,700 a year in fees, costs, and tax savings.

The 60 million freelancers in the U.S. – more than a third of the workforce – often struggle to secure timely payment for services rendered, accurately meet tax obligations, and manage their overall financial work/life balance. With the expectation that this relatively young cohort will only grow in size over time, investors like Group 11 see Lili as well-positioned to take advantage of this evolution in the “future of work.”

“Lilac and Liran’s forward-looking vision is changing how modern workers manage their finances, while saving them valuable time and money,” Group 11 founding partner Dovi Frances said during the company’s seed funding round announcement just under a year ago. “Lili is redefining banking for freelancers and we’re thrilled to be partnering with the team.”

This is a sponsored post in collaboration with InterSystems, Gold Sponsors of FinovateSpring, and Monica Summerville, head of capital markets, Celent, a division of Oliver Wyman.

Financial institutions and data have had a love-hate relationship for many years.

On the one hand FIs and data are a match made in heaven. It is a symbiotic relationship where business functions create and consume data over and over until the result exceeds the sum of the parts. Ideally this partnering results in revenue or alpha-producing insights. On the other hand, siloed, unreliable or simply too much data creates frustration and risk as the business potential is teased, but ultimately unattainable as FIs struggle to extract value from their data (see figure 1).

Business use cases for leveraging data across financial services are plentiful, from management reporting, enterprise risk, liquidity and treasury management, and more recently, driving innovative customer experiences. More specifically within capital markets and banking, trends such as the embracing of multi-asset trading or the desire to simplify architectures have triggered a rethink of data approaches. There is also, now more than ever, the desire for cost savings – equally important to FIs whose margins are increasingly coming under pressure from increased regulation and competitive factors. Indeed, research by Oliver Wyman and Morgan Stanley found that the benefits from having clean, consistent, and automated data management could be a two-to-four percent reduction of infrastructure and control costs. When IT spend ranges into the billions of dollars, as is the case with larger FIs, every percentage point of savings is a big win.

No wonder then that cracking the data management challenge has long been considered the perfect marriage of technology achievement and business function. FIs have made repeated attempts and invested hundreds of millions of dollars through the years to get this right. From simple relational databases storing structured data, to data warehouses and more recently data lakes capable of holding all types of data, there has been no shortage of excitement that maybe (whisper it) this latest approach could be “the one.” Heartbreaks inevitably followed as the heady days of getting to know new technologies turn into frustrations and recriminations. A pristine data lake becomes a swamp.

The latest research by Celent discovered that leading FIs including Bank of America, Citi, Goldman Sachs, JP Morgan and RBC, to name a few, have lately been getting serious with a new data management approach called Smart Data Fabric. As these entities move from a process- to platform-driven organisation, their business focus has shifted to ensuring the best customer experience possible. This shift however requires mastering and leveraging data to generate insights at an enterprise level. The reality is that a history of disjointed business expansion common to financial services, means data is siloed across numerous platforms, tuned for very different use cases. There are multiple “single sources of truth,” and these vary depending on whose truth you are seeking.

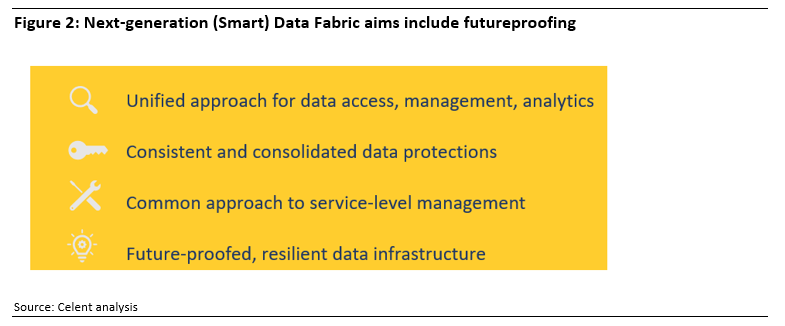

The right data management approach should empower FIs to become better versions of themselves, without fundamentally changing who they are. Unlike previous data management architectures, Smart Data Fabrics offer centralized access and a single unified view of data across the organization. Crucially, Data Fabrics do not require that copies of the data be created and stored outside its original location, so can offer a useful bridging solution between modern and legacy systems – the latter often holding the most business crucial data. In this way Data Fabrics can also avoid the creation of more data silos, which is especially important as FIs increasingly embrace cloud. A Data Fabric becomes “Smart” when it inherently supports advanced data analytics and aims to future-proof data management (see Figure 2).

Financial institutions, from asset managers to banks and brokers, have always known that they need to become smarter about data. Business end-users and clients are demanding better user experiences, targeted insights, and increased access to analytic capabilities which requires free access to accurate and harmonized data drawn from disparate sources across the entire enterprise. At the very core of modernization is the ability to innovate at scale, and this relies on freer access to data. Celent’s latest research report sponsored by InterSystems found that the business necessities and benefits of better data management is driving adoption of Smart Data Fabrics. This time it might just be for real. Read the full report here >>

The people have spoken and the votes for Best of Show for the second, all-digital FinovateSpring have been counted. After two days of innovative fintech demos, here are the companies that have been awarded Finovate’s top prize.

Dreams for its financial wellbeing platform that helps banks attract the new generation and create superior digital engagement by leveraging the latest insights from cognitive and behavioral science. Video.

Glia for its digital customer service platform that connects financial institutions to their customers using chat, voice, video, co-browsing, and AI. Video.

Signal Intent for its financial calculators for the digital age – built to win you more customers, capture better customer data, and help you move fast in the era of digital transformation. Video.

Thank you to all of our demoing companies, our speakers and presenters, our sponsors and partners and, of course, our wonderful audience and digital attendees.

Stay connected to the Finovate blog for more from our FinovateSpring companies and presenters, as well as updates about our upcoming events in July for FinovateAsia and our return to in-person conferencing in September for FinovateFall.

Notes on methodology:

1. Only audience members NOT associated with demoing companies were eligible to vote. Finovate employees did not vote.

2. Attendees were encouraged to note their favorites during each day. At the end of the last demo, they chose their three favorites.

3. The exact written instructions given to attendees: “Please rate (the companies) on the basis of demo quality and potential impact of the innovation demoed.”

4. The three companies appearing on the highest percentage of submitted ballots were named “Best of Show.”

5. Go here for a list of previous Best of Show winners through 2014. Best of Show winners from our 2015 through 2020 conferences are below:

The last time eBay truly dominated news headlines may have been in 2015, when it split from payments giant PayPal. Since then, the online marketplace has been quietly fending off new competitors including Amazon, Etsy, Rakuten, Mercari, and even Facebook Marketplace.

Today, however, the California-based company made an announcement that will help differentiate it from every other online marketplace– the company’s users can now buy and sell non-fungible tokens (NFTs). According to eBay’s updated policy, trusted sellers can now list and sell NFTs across multiple categories.

“This isn’t new to eBay,” said Senior Vice President and General Manager for eBay’s North America Market Jordan Sweetnam. “For 25+ years we’ve been the world’s destination for collectibles, connecting millions of buyers with sellers who have deep knowledge of the things they care about most. Our platform has helped collectors turn their hobbies into their livelihoods and, along the way, collectibles – ranging from beanie babies and railroad memorabilia to high-end art and rare coins – became an alternate asset class, combining passion with investment.”

Currently, eBay is allowing NFTs that fit categories such as trading cards, music, entertainment, and art. However, the company notes it will expand to facilitate the sales of NFTs across more categories.

You may inherently associate NFTs with cryptocurrencies because they, too, are held on the blockchain. However, eBay has not indicated any current plans to accept cryptocurrencies as a form of payment, so users can expect to pay for their NFT using a traditional online payment method such as a credit card.

Self-proclaimed “financial super-app” Curve announced it will soon go live with a crowdfunding campaign.

The campaign, which will launch “sometime in May,” will be held on Crowdcube and will enable Curve’s more than two million customers to invest and be part of its journey. Curve will use the funds to fuel its launch into the U.S. market and help it to expand further into Europe.

“We know many new customers missed out on our 2019 crowdfunding, and we’ve fielded constant requests to open a new round,” said Curve Founder and CEO Shachar Bialick. “Since we place our customers at the heart of everything we do, we wanted to offer another chance for them to be involved in our success, enabling them to be part of our journey.”

Funds raised from the campaign will add to the $169 million Curve has raised since it was founded in 2015. This includes the company’s recent $103 million (£72.5 million) Series C round it closed in January which received contributions from Fuel Venture Capital.

“With increasing fragmentation in financial services, and growing demand from consumers for a simpler way to control and manage their finances, the scene is set for Curve to seize a global opportunity,” said Bialick. “We are investing in our people and the business to make that happen.”

This news follows Curve’s 2019 crowdfunding round, which raised $5.7 million (£4 million) in 42 minutes. The move tripled the company’s valuation. The announcement also comes after a year of growth during which Curve hired over 100 new employees, doubled its customer base to over two million, and saw its transaction volume increase to $3.7 billion (£2.6 billion).

Curve has big plans for 2021, including the launch of its crowdfunding campaign. This year, the company is also working on the rollout of its Curve Credit product and will increase its workforce by 60%, hiring 200 additional employees.

The firms are Fort Community Credit Union, headquartered in Fort Atkinson, Wisconsin; Alltrust Credit Union (formerly Southern Mass Credit Union) based in Fairhaven, Massachusetts; and Statewide Federal Credit Union, headquartered in Starkville, Mississippi.

“We couldn’t ask for a better way to start 2021, signing these three progressive credit unions,” Bankjoy CEO Michael Duncan said. “Since we are now officially in the digital age thanks to the pandemic, these credit unions are now poised to hit the ground running with our most advanced online, mobile, and voice banking technologies. We are excited to see how they will perform and how their members will take advantage of these new offerings.”

Founded in 2015 and making its Finovate debut a year later at FinovateFall in New York, Bankjoy provides financial institutions with a variety of digital banking solutions ranging from mobile / online banking, and e-statements to online account opening and loan origination, as well as access to conversational AI-based products. From flagship banks to credit unions, Bankjoy offers an out-of-the-box alternative to outmoded legacy systems that prevent banks and credit unions from being able to meet the rising digital expectations of their customers and members.

“Bankjoy will improve our credit union’s digital banking solution and offer an experience that is in line with our members expectations,” Alltrust Credit Union Vice President of Operations Stephanie Medeiros said. “Our partnership with Bankjoy will allow us to maintain our commitment to our members while delivering the latest digital technology.”

“The Bankjoy solution will allow our members to access and manage their account from anywhere,” Statewide Federal Credit Union CEO Casey Bacon added. “They will have access to all of the conveniences of modern banking at their fingertips.”

Headquartered in Troy, Michigan, Bankjoy has raised $1.8 million in funding from investors including SixThirty and CheckAlt. The company is an alum of the Y Combinator incubator program.

You can thank Gen Z’s “I want it now” mentality for Credit Karma’s freshest release. Dubbed Instant Karma, the newest product is the latest to come from Credit Karma Money, the company’s challenger banking service.

According to TechCrunch, which covered the launch, Instant Karma rewards users by randomly reimbursing their purchases.

Credit Karma General Manager Poulomi Damany told TechCrunch that, since the purpose behind Credit Karma Money is to “change people’s relationship with money” the new rewards product is an extension of that goal.

There are two major differentiating factors of Instant Karma over traditional payments rewards programs. The first is that the rewards are issued based on purchases made on debit cards, not credit cards. That’s because, as Credit Karma Product Manager Kyle Thibaut said, “Gen Z do not necessarily like credit cards. When you talk to them, they like debit cards and debit cards are the way they spend. Debit card usage is higher than credit cards in the U.S., and it’s actually growing while credit card usage is declining.”

The second point of differentiation is that the reward is issued the instant the user makes the transaction. Traditional cash-back programs, in contrast, will only issue rewards based on a time scale (eg., monthly) or once they reach a certain threshold (eg., the balance reaches $25).

So far, Credit Karma has rewarded $5 million in rewards on 100,000 transactions.

Founded in 2007, Credit Karma added a checking feature to its Credit Karma Money suite in October of last year. This complements the savings tool the company launched in October of 2019, when it initiated its entrance into the neobanking space. Prior to this, Credit Karma operated solely in the financial wellness space, in which it continues to offer its 110 million members access to credit scoring data, loan and credit card marketplaces, identity monitoring, and tax filing tools.

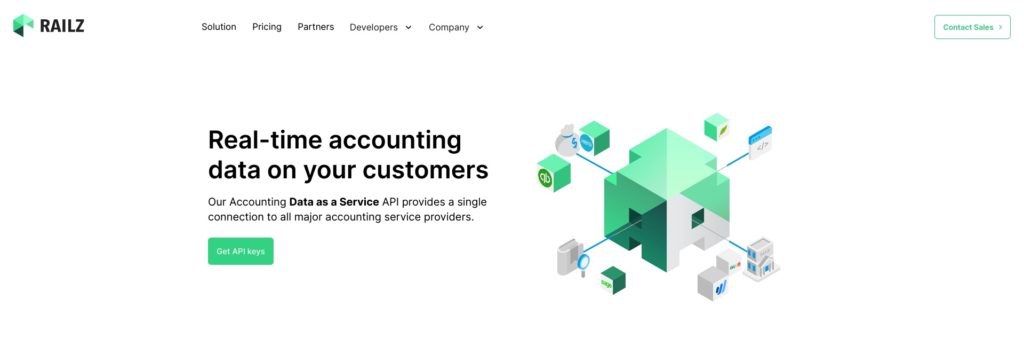

Railz, an API developer that helps connect financial institutions and fintechs with their customers’ accounting information in real-time, has secured an investment of $12 million. The Series A round, led by Nyca Partners, takes the Toronto, Ontario, Canada-based company’s total funding to more than $15 million.

“While there are many players who focus on collecting data across various accounting packages, the challenge of understanding what the data actually means, and how to categorize it, continues to be a major hurdle for the users of this information,” Railz CEO Sohaib Zahid said. “Railz’s data normalization solution, coupled with our insights and analytics engine, is the secret sauce that can address this challenge – and tackle it more accurately and quickly than any other service offering in market.”

Also participating in the Series A were Vestigo Ventures, Susa Ventures, Plug and Play, N49P, Hack VC, Global Founders Capital, and Entrée Capital. The company plans to use the new capital to add more talent to its sales and engineering teams.

Railz offers a single API that integrates with all major, SME-oriented accounting platforms to enable on-demand access to financial transactions, analytics, and insights. The fast, low-cost, accounting-data-as-a-service solution gives small businesses the ability to be better served by financial institutions by giving them an easier, less cumbersome way to share their critical financial information.

“Businesses use accounting software as a single source of truth to record the financial health of their company,” Nyca Partner Jeremy Solomon said. “Sharing this data with another party is currently a manual process that is slow, expensive, and error-prone.”

With just a few lines of code, Railz claims that it can get customers up and running with its technology in less than a day. The company’s real-time financial analytics and insights offer risk scoring and fraud identification, in addition to standardized accounting entries that use a universal format for easier modeling and reporting. Founded in the summer of 2020, Railz says its customers have benefitted from up to a 53% reduction in costs and a 75% reduction in fraud.

Corporate expense management platform Divvy has agreed to sell to small business financial software provider Bill.com for $2.5 billion.

Adding Divvy’s technology to its platform expands Bill.com’s solution. The new capabilities will help the California-based company enable its 115,000 customers to automatically manage accounts payable, accounts receivable, and corporate card spend. Additionally, Divvy’s tools will offer businesses real-time insight into their B2B spending and provide them access to multiple payment solutions.

Combining the two companies also boosts Divvy’s capabilities. The Utah-based company will be able to offer its 7,500 small business customers automated payable, receivables, and workflow capabilities. “As we listened to our customers, we heard them ask for a comprehensive payments platform so that they don’t have to use multiple software systems to manage their finances,” said Divvy CEO and Co-Founder Blake Murray. “Today I’m proud that Divvy is joining Bill.com to bring the one-stop-shop platform that our customers and the market have been asking for.”

“Since founding Bill.com, I have been driven by the desire to build solutions that make a real difference for small and mid-sized businesses. Customers have been asking us to help them with their spend management, and I am excited that together with Divvy, we can deliver on that ask, furthering our vision to transform SMB financial operations. Our expanded platform will provide more automation and real-time information to SMBs, enabling them to make more informed decisions,” said Bill.com CEO and Founder René Lacerte. “We are excited to work with the talented Divvy team. We have a shared passion for helping SMBs succeed and both companies are driving our customers’ digital transformations. Together, we can further empower SMBs to transition quickly and easily.”

Today’s deal is expected to close by the end of September and is subject to regulatory approvals closing conditions.

Bill.com was founded in 2006 and went public in 2019. With a market capitalization of $12.33 billion, the company trades on the New York Stock Exchange under the ticker BILL.

Founded in 2016, Divvy has raised $418 million from investors including PayPal Ventures, Insight Partners, and New Enterprise Associates.

How have financial services companies coped with the rising challenge of cybercrime in the Work From Anywhere era? We caught up with Tamas Kadar, co-founder and CEO of SEON, a cybersecurity startup based in Hungary, to learn how the company – featured in Forbes’ Hottest Young Startups in Europe – helps firms meet regulatory obligations and better defend themselves against fraud.

Tell us about SEON. When was the company founded and what problem was the company founded to solve?

Tamas Kadar: Founded in 2017, SEON was born out of necessity. Prior to its launch, co-founder Bence Jendruszak and I owned a budding crypto exchange, which was repeatedly hit by instances of fraud. We urgently needed a solution that would help us resolve the problem, but found that there were none on the market suitable for our business structure.

The problem was that most anti-fraud solutions in the industry had long integration times, lengthy contracts, and different packages for different sized businesses. We needed a solution that was more flexible and could be integrated and functional almost immediately. So we took matters into our own hands and developed a solution that would meet these needs. This later became SEON.

SEON’s services remove the barriers to fraud prevention that many companies face today. The solution can be integrated into business structures in minutes – a far cry from the usual weeks it takes for many mainstream solutions. It is suitable for businesses of any size, has a free trial period, and works on a rolling monthly contract, meaning that businesses can cancel and take up our services without being bound by long contracts – much like a Netflix for fraud prevention.

What in your background gave you the confidence to tackle this challenge?

Kadar: Having studied Deep Info Comms at the elite Corvinus University, where Bence studied General Management, we both had the knowledge needed to get SEON off the ground. It was there that I learned about the fraud tactics being used to get around the latest fraud prevention strategies. Having this insight, along with my technical know-how and Bence’s managerial skills, we had the confidence to move forwards with SEON.

It was clear that there were some pain points in the fraud prevention industry that needed addressing. We felt that we were the right people to do so.

Who are your primary customers in financial services and how do their needs differ from those of your customers in other industries?

Kadar: Neo banks, traditional banks, PSPs, buy now pay later (BNPL) and other fraud tech companies, account for about 25% SEON’s portfolio. The rest is made up of a whole range of different industries, including some of the most high-risk. Other sectors we serve include iGaming, eSports, cryptocurrencies and online trading, and travel.

The services we provide to financial institutions differ from others as they focus more on regulatory compliance, reducing cost when it comes to Know Your Customer (KYC) checks, and preventing money laundering. We also protect account openings, reduce customer acquisition costs, decrease bonus abuse, and flag fraudulent merchants using stolen credit cards.

By contrast, other industries use us to protect themselves against fraudulent activity such as account takeover, while we mitigate chargebacks for ecommerce merchants. We also prevent fraud surrounding ticketing in the airline industry.

Tell us a little bit about the technology behind your solution. What are the most effective tools for combating cybercrime?

Kadar: SEON has a number of solutions that are highly beneficial for helping businesses prevent fraud, including the SEON Sense Platform and Intelligence Tool. We draw on data from across the internet to establish customers’ digital footprints, weaning out false accounts and actively preventing fraudulent transactions from taking place.

Driven by transactional data, the SEON Sense Platform provides a comprehensive end-to-end solution for fraud managers that can be tailored to the individual needs of a company.

Meanwhile, our Intelligence Tool increases fraud detection accuracy with just one click. Users can simply enter an email address, IP address, phone number or location into the browser extension to get background information, which then enables fraud managers to see complete user profiles and flag suspected fraudulent ones. As a result, companies can detect fake accounts with ease.

These solutions address a number of problems in the fraud prevention industry. They can be integrated via a Google Chrome link or API within minutes, and as they work in entirely in the back-end, there are no added layers of friction for consumers.

In addition, our solution acts as a marker for the move away from the industries overreliance on artificial intelligence (AI) and machine learning (ML) alone. AI and ML are often seen as a magic pill that will solve all of a business’ fraud woes and are left to resolve issues without the proper supervision. This impacts reportability because it isn’t always easy to establish the reason for certain decisions that a solution has made. Instead, our solutions are based on a supervised learning approach, giving fraud managers the information needed to make effective decisions.

How has COVID-19 impacted your company and its customers? What are your biggest takeaways from the experience?

Kadar: The flexibility of our solution has meant that we have been able to easily adapt to changes imposed by the pandemic. One of the largest changes we’ve seen in terms of fraud is the amount that is taking place. Many businesses moved into the online space in order to survive lockdowns and social distancing measures. The problem is that online fraud grows in line with online activity, so the amount of fraud that is taking place there has rapidly grown. As a result, our main focus has been on industries that have felt these changes the most – especially high-risk industries such as iGaming and eSports.

The solutions developed by SEON have made an enormous impact on the way our customers can manage, monitor, and mitigate fraudulent activity. Key to our ability to provide such solutions has been our open lines of communication with our customers. It’s important that newly digitised businesses understand that fraud prevention is an evolving practice and their feedback is vital to its success.

For example, our customers know they are encouraged to contact us whenever something changes within their business, be that a release of a new software update or simply a realisation that their customers often use other social registries that we haven’t been monitoring. With this knowledge, we can quickly begin developing new lines of defence.

What is the most important thing about the technology scene in Hungary that many people outside of the area might be surprised to learn?

Kadar: Setting up SEON wasn’t all plain sailing. Bias can often hamper the growth of startups outside of traditional European hubs such as London and Munich, meaning it’s difficult for businesses to secure the investment needed in order to scale.

This is especially true for Central Europe. Bence and I found this out the hard way. When getting SEON off the ground, we found that many European investors were skeptical when it came to startups from Central and Eastern Europe.

Still, we see launching SEON in Hungary as not only a blessing, but an advantage when it came to creating a unique product that the fraud prevention industry was desperately in need of. Being outside a typical startup hub has resulted in the company being more creative, more agile and, contrary to many seed level businesses, more resilient.

Establishing SEON in Hungary also greatly reduced our outgoings, allowing us to use the initial investment we secured to grow. This is because the talent pool in Eastern Europe met the needs of the business. It’s naturally abundant in people with mathematics, computer science, and AI-based skills, which has provided us with the human capital necessary to develop and maintain our fraud solution, without initially having to set up offices elsewhere.

You recently received a major investment – the biggest Series A round in Hungarian history. How important was this funding and what will it enable SEON to do?

Kadar: As part of the funding round, which was led by leading European early-stage investor Creandum, we secured €10 million (USD 12 million) in series A investment. This is a pivotal point in our company’s growth and will drive us in our mission to democratize fraud prevention by removing the barriers that many companies face.

With the investment, we plan to expand our presence in the U.S. and U.K., with the aim of having our London headquarters account for more than 30% of our revenue. We will also be shortly announcing the launch of our new U.S. office, along with our plans for the region.

In all, this investment will take our company to the next level, enabling us to not only better serve our existing customers but also provide our services to even more businesses across the globe.

Here is our look at fintech innovation around the world.

Upcoming webinar Title: Beyond Images: How Video is Reshaping Digital Customer Engagements in Banking to Drive Agile Growth Date: Wednesday, June 09, 2021 Time: 2:00 pm Eastern Daylight Time Duration: 1 hour

Leading brands are adding real-time video to digital customer engagements as a way to improve customer service and sales effectiveness. Video can enable service and support workers to add human empathy to digital customer engagements. Forrester advises that adding video can boost loyalty and revenue.

Join the latest webinar to explore:

How the COVID pandemic accelerated the need for better digital customer experiences that can convey humanity and empathy

Review real-world success stories of enterprises that have created a video-based “guided customer experience” in their apps and websites to drive higher customer satisfaction, higher revenue, and higher customer retention

The difference between using a third party video meeting tool and adding video-as-a-service embedded into your existing website or app… and which strategy is right for you

Featuring Tom Martin, CEO, Glance Networks and David Penn, Research Analyst, Finovate.

Payments network Ripple is bolstering its ranks this week with the appointment of Kristina Campbell as CFO.

Campbell has been tapped to drive Ripple’s financial strategy, accelerate growth, and deliver value to shareholders. She most recently served as CFO at PayNearMe and has also held multiple roles at GreenDot.

“Digital asset technology allows us to rethink and improve the systems and infrastructure around how money moves. With this technology, we will make the global financial system accessible to all,” said Campbell. “Ripple is uniquely positioned to improve global payments in ways that have yet to be defined and I’m excited to be a part of that solution.”

Ripple also revealed that Rosa Gumataotao Rios, 43rd Treasurer of the United States, has joined its Board of Directors. In her role as Treasurer, Rios oversaw all currency and coin production and focused on economic development, urban revitalization, and real estate finance.

“I’ve dedicated my career to financial inclusion and empowerment, which requires bringing new and innovative solutions to staid processes. Ripple is one of the best examples of how to use cryptocurrency in a substantive and legitimate role to facilitate payments globally,” said Rios. “Blockchain and digital assets will underpin our future global financial systems. Cryptocurrency is the what. Ripple is the how.”

Ripple CEO Brad Garlinghouse said that the new appointees come “at a pivotal time for the company.” Garlinghouse’s phrase, “pivotal time,” is in reference to Ripple’s international expansion efforts; earlier this spring the company acquired a 40% stake in Asia-based cross-border payment specialist Tranglo. It is also a head nod to the lawsuit Ripple is currently facing.

The U.S. Securities and Exchange Commission (SEC) alleged that Ripple co-founder Chris Larsen and CEO Brad Garlinghouse conducted an illegal securities offering that raised more than $1.3 billion through sales of Ripple’s XRP currency. Ripple, which considers XRP as a currency and not an investment contract, is denying the allegations.

Backed by SBI Holdings, Santander, Andreessen Horowitz, and Lightspeed, Ripple has raised $294 million and is valued at $10 billion.