This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Two fintech megaliths, financial data and infrastructure platform Plaid and merchant services company Square formed a partnership this week that will offer merchants a smoother experience when it comes to ACH payments.

Through the deal, U.S. merchants can process ACH payments without storing clients’ bank account information. Square is leveraging a tokenized check system that uses Plaid to help customers connect their bank accounts. Plaid enables customers to enter their bank login credentials to connect their account and enable the payment.

This system works especially well for businesses that take payments for high-value orders. That’s because it increases the certainty that they payment will go through. Making acceptance even easier, Square offers fee-free refunds on ACH payments processed.

“Payment flexibility, security, and transparency are core to Square’s Payment Platform,” said the Head of Square’s Payment Platform Dennis Jarosch. “By offering ACH payments, we can help businesses process large transactions online at a low cost without worrying about bank authentication, compliance, or any managed payment complexities. We’re excited to offer ACH as one of many ways that businesses get paid fast and securely with Square.”

For Plaid, this news comes shortly after the company closed a $425 million round of funding. Plaid was founded in 2012 to build APIs to connect consumers, financial institutions, and developers. Today, the company also offers a suite of analytics products that provides further insights into transactions.

“nCino has a proven track record of helping financial institutions innovate while optimizing their processes,” nCino Director of Strategic Partnerships in APAC Zameer Momin said. “As more and more financial institutions are embarking on their business transformations, we are truly excited to be able to offer the power of KPMG Australia’s banking operations knowledge with nCino’s cloud technology to help create a robust and scalable digital experience.”

nCino’s Bank Operating System leverages the Salesforce platform to offer financial institutions a complete, end-to-end banking solution. nCino’s technology integrates with the institution’s core systems, and combines CRM, onboarding, account opening, loan origination, deposit accounts, credit analysis, ECM, and instant reporting capabilities. nCino notes that its client institutions have experienced a 92% reduction in servicing costs, a 54% reduction in policy exceptions, a 40% decrease in loan closing time, and a 22% increase in efficiency using its cloud-based Bank Operating Systems. These FIs have also experienced a 1.2x increase in account opening completion rates.

KPMG Australia Partner Alex Moreno pointed to the changing nature of the financial services landscape in Australia – including the arrival of both new digital competitors and increased regulation – as reasons for the collaboration with nCino. “Customers are expecting a better experience from their bank,” Moreno said. “Most banks have challenges with operational efficiency and internal time to competency, and secure and responsible lending is in the spotlight. The combination of KPMG’s Banking Operational Excellence Practice and nCino’s Bank Operating System is well positioned to help navigate these challenges.”

Headquartered in Wilmington, North Carolina, nCino was founded in 2012. The company, which went public last July, trades on the NASDAQ under the ticker NCNO and has a valuation of $5.4 billion.

Privacy.com has a new name and new funding this week. The card issuing platform has rebranded to Lithic and raised $43 million in Series B funding. This brings the company’s total funding to $61 million. The investment was led by Bessemer Venture Partners and saw participation from Index Ventures, Tusk Venture Partners, Rainfall Ventures, Teamworthy Ventures, and Walkabout Ventures.

The company initially launched as Privacy.com, a consumer-facing platform that offers tools to help shoppers generate virtual “burner cards,” which are single-use, disposable card numbers that shoppers could use to shield their actual card number. Going forward, Lithic will maintain this consumer-facing product under the Privacy.com brand.

Last fall, Lithic unveiled its card issuing API for developers. In the past four months, the company has seen impressive growth, with enterprise issuing volumes ballooning by 3x. Lithic will use today’s funding to fuel that growth even further.

The developer-facing tools help them create payment cards for their customers, optimize back-office operations, and simplify disbursements. These capabilities help developers issue a card instantly, reduce administrative burden, and earn a percentage of the interchange revenue.

“We built all these foundational card processing tools for ourselves to power Privacy.com,” said Lithic CEO and Co-founder Bo Jiang. “Then we found that other companies, especially developers, needed the same types of tools. The more we thought about it, the more it made sense to give these tools their own name—Lithic. Its own business, with its own separate customers and its own mission.”

Founded in 2014 by Bo Jiang, Jason Kruse, and David Nicholsand, Lithic is headquartered in New York City.

One of the great things about the return of FinDEVr was the opportunity to showcase the men and women behind the technology innovations that are driving fintech today. From veteran CTOs to up-n-coming developers, FinDEVr was a great opportunity to learn from – and celebrate – the talent behind the technology.

At FinDEVR this year, I had the opportunity to chat with Trevor Marshall, Chief Technology Officer with New York-based fintech Current. Starting out as a financial wellness solution for young people and their families, Current has grown into a neobank challenger that offers mobile payments, online banking, and other financial services. The company secured $220 million in Series D funding in April and, this month, announced a partnership with decentralized finance platform Acala. This first-of-its-kind alliance establishes a new category of finance, hybrid finance (HyFi), that leverages applications from both traditional and decentralized sources.

“We created Current because we could see how money was being re-networked through new technologies,” Marshall said. “Our initiative with Acala allows us to flex this muscle we have been developing for the past six years.”

Marshall’s interest in alternative payments was on display in 2015, when he built a Ripple payments prototype for Current. After gaming out the prototype’s flaws, he tried an Ethereum-based process – which he also found insufficient for Current’s needs. With this week’s partnership with Acala, Marshall believes that the ability to introduce in-app decentralized finance solutions into the Current platform may now be soon at hand.

“In some ways, this partnership is really just the beginning of the actual rollout of what we’ve been building toward this whole time,” Marshall said.

At FinDEVr, Marshall talked about recent innovations in payments, specifically how technology is enabling new types of payment transmission options. He also explained how fintechs and other companies are working to integrate alternative payments, including cryptocurrencies and API-based processing into their offerings.

Here’s a sample from our conversation. The full interview with Trevor Marshall will be available On Demand in the days to come.

With vaccination programs in full swing in many nations across the globe, the spread of COVID is finally beginning to slow. What is not slowing, however, is the change that the pandemic has brought to consumers’ finances, including how they spend their money.

With that in mind, here are five aspects of payments that will change in 2021, as consumers solidify the habits they picked up last year.

QR codes

As we’ve mentioned on the blog in the past, QR codes have been making a comeback as a mobile payments tool. That’s because QR codes are both versatile and universal– they can be printed out on physical paper and can be scanned by a range of devices across operating systems.

These attributes make QR codes the perfect tool to facilitate P2P payments and to implement low-touch checkout solutions at in-store points of sale. Earlier this year, PayPal partnered with InComm to launch its QR code technology at pharmacy chain CVS. Just last month, Fiservteamed up with PayPal to enable businesses to use QR codes to offer touch-free payments at the point of sale on Clover devices. And yesterday SafetyPay began enabling users to use QR codes for real time payments in Brazil.

These use cases, combined with the increased demand for low- and no-touch payment options, are fueling the rise of the QR code.

Digital

The case for digital is a no-brainer these days, as consumers have shifted their habits to conduct not only their shopping but also many other aspects of their daily lives online. When brick-and-mortar shops were closed, consumers were left with online shopping (and therefore payment) options.

It is clear that, even as the pandemic winds down, consumers are maintaining these digital-first habits. In fact, shoppers of all ages and demographics are more comfortable paying online than before.

Embedded

With the increase in digital comes the increase in embedded payments and embedded finance. Retailers and service providers have figured out that the more seamless they make the payments experience, the less friction will interfere with the customer experience and the more the customer will return.

By saving users’ payments credentials, ridesharing services, food delivery companies, and even online grocers increase the chance of a return purchase. It also provides the retailer with more data and offers enhanced data surrounding consumer habits.

Visibility

When it comes to security, with more data comes more responsibility. On the flip side, the extra data also brings additional visibility into consumer habits. From bank’s and merchant’s perspectives, this visibility can help them personalize products, services, and even the client experience.

Visibility into consumer spend data also helps banks and merchants anticipate customers’ needs and may enable them to more efficiently market up-sell and cross-sell opportunities.

On the consumer side of things the increased data can help them plan, budget, and manage their spending when the right tools are provided. Even technology as simple as purchase notifications can not only increase shoppers’ awareness of where their money is going, but also can help them prevent fraud.

Collaboration

It is becoming increasingly clear that in the banking and fintech space, no player is an island. By collaborating with other players, both banks and fintechs can maximize their competitive advantages by sticking with their core competencies.

So far this year, we’ve seen multiple successful bank-fintech partnerships, including this week’s mash-up between Ally Financial and buy-now, pay-later player Sezzle. Other headline-worthy mash-ups, such as Apple’s partnership with Goldman Sachs, highlight the benefits of leveraging others’ strengths, even when they appear to be a competitor on the outset.

A pair of identity solution providers – Ping Identity and ProofID – have partnered to enhance identity security for U.K.-based Tesco Bank.

The banking division of Tesco, the largest supermarket retailer in the U.K., Tesco Bank deployed both Ping Identity’s PingAccess and PingFederate to secure key applications. With ProofID as the bank’s implementation partner, the integration – which involved creating a single-factor login process deployed across a private AWS cloud – took only 12 weeks. Importantly, the solution “allow(ed) us to consolidate disparate identity data,” said Tesco Bank security architect David McConchie, “laying the foundation for a common customer identity.”

PingAccess is PingIdentity’s centralized cloud identity and access security solution for apps and APIs. The technology provides secure access down to the URL level and can secure APIs by applying policies to disallow specific HTTP transactions to users in untrusted contexts. PingFederate is an enterprise federation server that enables user authentication and single sign-on. The solution functions as a global authentication authority to enable authorized entities to securely access applications from any device.

“We saw how we could use PingAccess and PingFederate to work across web, mobile and API. The ease with which we could deploy across channels was a critical factor, along with the data governance capabilities,” McConchie said. “Ping Identity gives us the flexible authorization capabilities we need to minimize friction and deliver a customer-centric experience.”

A Finovate alum for nearly 10 years, Ping Identity was founded in 2003 and is headquartered in Denver, Colorado. Named a Top Workplace by The Denver Post earlier this month, Ping Identity partnered with global logistics provider DB Schenker in April, and launched its new, cloud-based identity verification service, PingOne Verify, in February.

Ping is publicly-traded on the New York Stock Exchange under the ticker PING. With a $1.2 billion valuation upon its IPO in September 2019, the company currently has a market capitalization of $1.9 billion. Andre Durand is founder and CEO.

Ally Financial’s Ally Lending announced this week it is now offering financing on buy-now, pay-later (BNPL) platform Sezzle. The new collaboration enables select shoppers to pay for purchases over time using Ally’s installment loans or Sezzle’s BNPL installment offerings.

If a purchase is eligible for an installment loan from Ally, the shopper will see the message “financed by Ally” at checkout. Loans will be available for purchases of up to $40,000 with terms ranging from three to 60 months. This broadens the availability of financing typically available on Sezzle, which currently limits shoppers to four installments paid over the course of six weeks on purchases up to $2,500.

“We’re on a mission to financially empower the next generation,” said Sezzle CEO Charlie Youakim. “With Ally Lending’s personalized, flexible financing solutions now available on our platform, we’re able to offer even more options for consumers to budget their purchases and responsibly pay for what they want and need.”

Today’s news comes during a time when both online shopping and BNPL are on the rise. Over the past year, BNPL increased 17% in Gen Z populations and 21% for millennials.

Sezzle initially went public on the ASX in July of 2019, and now has a market cap of over $777 million, a figure that is almost 5x higher than it was at the start of 2020. The company announced earlier this month it will IPO in the U.S. later this year.

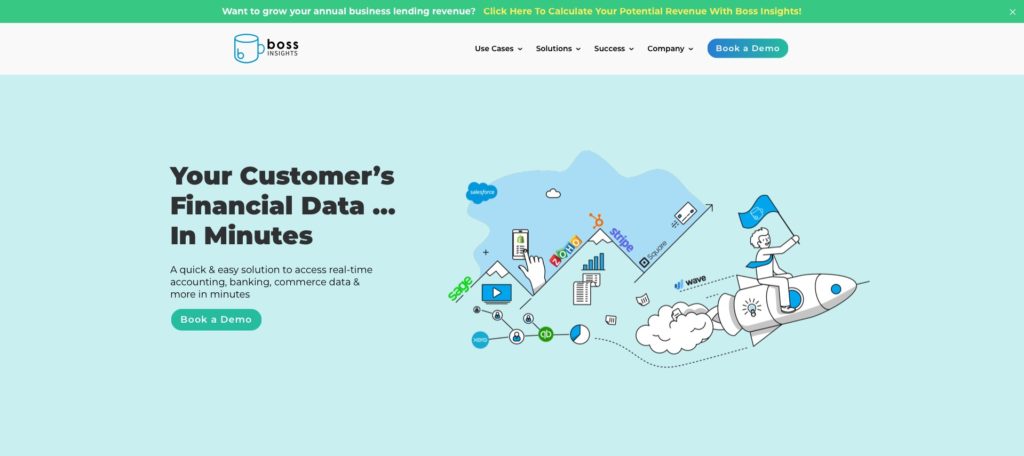

Earlier this year in our conversation on diversity in fintech and financial services, we looked at a partnership between Paybby, a challenger bank focused on Black and Brown communities; Carver Federal Savings Bank, an African-American owned bank; and Finovate alum Boss Insights.

Today, we pick up that conversation from the fintech’s perspective, talking with Boss Insights founder and CEO Keren Moynihan about her company’s innovations in the field of business-data-as-a-service, its participation in the Paycheck Protection Program, and the importance of impact and meaning when it comes to providing financial services.

Boss Insights specializes in Business Data as a Service. What does this mean?

Moynihan: We work with fintechs and private lenders, banks, and credit unions. We work with their business lending groups; it could be small and medium business lending, SBA, invoice factoring, commercial, all sorts of business lending types. And what we are giving the lenders is access to their business customers’ financial data in minutes. It sounds impossible, but actually only takes the lenders one hour of their time to set up.

What we’re enabling is for them to be able to pull real-time accounting information, banking, or commerce information on demand.

When you look back on 2020, what are your biggest takeways?

Moynihan: In March 2020 I was speaking with (a reporter) at a conference and she asked for a direct quote responding to “how are fintechs and entrepreneurial companies going to be responding to COVID?” And I’ll never forget it because I said, “Look, fintechs thrive on challenges and this is an unprecedented challenge but we will be looking at ways to respond to it.” Two hours later, we all got an order that the economy was going to shut down, that we were all going to isolate. I don’t think anyone knew what was happening. I called the reporter and said “I know what I said, but …” I knew I was going to eat my words, because this was on another level. She laughed and said, of course, and she appreciated my call.

That was more than a year ago. The next two weeks were an onslaught. This was before PPP. This was before any kind of government funding and people really did not know what was happening. And unless you were in it, it’s really hard to describe it. What we did as a company was that we saw in all the news articles there wasn’t enough personal protection equipment, we started to get reports out of Italy, it was a really scary time. Now people at Boss Insights could not create masks. But we did see that if you stopped a company from being able to make sales, they are not going to be able to say alive and to be able to grow.

I asked myself, how do you support the economy? Right away we said we will offer part of our technology for free for any lenders who will support new businesses. And by new businesses, I meant new business relationships with the lender. That is a harder uplift. And as a result of that, everything started to grow for us. Technology companies reached out. Banking companies reached out. We were covered in an industry journal and, as a result of just that one piece, we had so many people call us. And we learned so much just by being able to say we can help.

How much of what you’ve learned will you be able to translate into new initiatives and future growth?

Moyinhan: There are a lot of things that I see changing, and then there’s an even bigger category of things I wish would change and hope will change. And time will tell. One word, very overused, is digitization. That’s going to endure. CB Insights reported that banks were losing about 1% market share each year, so give or take 9% or 10% over a nine year period. In 2020, 9% was lost in one year. A couple more years like that and we’re looking at a very different economy.

That really made the industry stand up and take notice. Back in March 2020, the same lenders that were telling me that they had everything under control and were ready to go, were the same ones that admitted to me on private calls that they were placing orders for laptops at Costco. They literally could not get laptops from regular commercial suppliers and were ordering them from Costco because they couldn’t get them anywhere else.

This points to one trend: people were a lot more honest about where they were (in terms of digital transformation) because you couldn’t just say you had digitized, it was actually being tested. I believe that trend is going to endure because the expectations of people, of businesses, have changed. We all ordered groceries online for awhile. I don’t think that was true before 2020. We are all expecting that these documents and forms that you have to go into branches for will be available online.

That is the biggest thing I can say that has changed. The one thing that I hope will change is the collaboration. We put out something in the American Banking Association saying that social distancing led to social collaboration. What I mean by that is that people stopped talking and they started listening. This includes Boss Insights. We stopped talking about what we’re selling and we started just asking “what do you need?” And I do hope that trend continues. It’s mirrored in other areas outside of financial services. We think these things were long overdue. It’s not a trend that is continuing in the way that I would have hoped. But I do see a lot of changes and this issue surfaced in the second round of PPP. People were open to having conversations. They brought decision-makers in the room. People didn’t want to have high-level discussions. They wanted to clearly tell you “I need this. Can you get it for me?” Then it’s our turn to talk about what we can do.

That amount of collaboration is unprecedented before COVID, and we just hope that it continues.

Tell us about the importance of working with small business owners who struggled to access support from relief programs like PPP.

Moyinhan: In the middle of PPP I was on a podcast called The Powerful Ladies podcast and it was with Kara Duffy. All of this got arranged because of Sharifah Hardie, who also runs a podcast and we had been on her podcast also. There was a woman there named Ronda Brunson. She has a consulting practice where she works with people to educate them on financial health, people who would not necessarily have had that training. We learn a lot of things in school, but financial health is not one of them, and if you have not had that education elsewhere where are you going to get it? She empowers people.

As I’m listening to all of these incredibly accomplished women and what they do in their business lives, she heard what I was doing. I was a little bit the oddball out because I was working with businesses and everyone else was working with individuals. She said, “I hear what you do, but the first round of PPP got a little bit of social notice because it’s supporting large businesses.” The second round of PPP did correct for this. But at that time we didn’t know that was going to happen. She said “how are you actually working to get capital into the hands of people who wouldn’t get access to it?”

I knew exactly what she meant. I knew that she meant people who were either female-run companies or visible minority-run companies. She didn’t say it explicitly, but that was exactly what she meant because those were the people that she was working with on a daily basis.

The way the lending industry works is that it’s based on a percentage of the amount of the loan. Everything is based on that. The costs are the same whether the loan is two million dollars or $200,000 – so who’s going to get more resources? It’s not that banks and credit unions and private lenders are trying to do it this way, it’s that the costs don’t scale down but the revenue does. What I saw from banks at that time is they were working until two or three in the morning. What I’ve heard from the CEO of Carver Bancorp, Michael Pugh, is that he’s been on the phone with clients to get their documents in – which people couldn’t believe, but this is the dedication. And what (Brunson) was asking me was: “what exactly are you doing to ensure your technology gets in the hands of people who will make sure that the disenfranchised will get access?”

And I never forgot it and I started looking immediately. Because for the people at Boss Insights, it is about accelerating business lending from months to minutes. But it’s also about impact and meaning and making sure businesses are evaluated on their merit. It is because of Paybby that we got connected to Carver. And it is because of Paybby and Carver that we are in a position to answer her and say, Ronda, now I can tell you we are doing something.

In some ways, we just started listening. We listened for when the SBA announced that there was going to be a week in advance for lenders focused in this area. And we listened when Paybby said “we have a lender who is ready to do this uplift.” And the collaboration that Paybby and Carver and Boss Insights have is a daily investment to make sure that things are running smoothly so businesses can apply.

Read more about the partnership between Paybby, Carver Federal Savings Bank, and Boss Insights.

Multi-currency accounts are expanding beyond the realm of fintechs.

This week, HSBC U.S. is launching a multi-currency digital wallet. The new offering, HSBC Global Wallet, will enable U.S. business banking users to exchange foreign currencies and make transactions across borders without using third party tools.

The wallet, which is also being rolled out in the U.K. and Singapore today, will be available in other markets starting next year.

HSBC Global Wallet will offer small-and-medium-sized businesses instant capability to pay in foreign currencies, including Euros, U.K. Pound Sterling, Hong Kong Dollars, Canadian Dollars, Singapore Dollars, Australian Dollars, and Malaysian Ringgit. As a result, these business users will have the ability to make international payments to the U.K., Canada, Hong Kong, Singapore, Australia, Malaysia and 19 markets in the Eurozone using domestic real-time payment networks. The ability for businesses to receive these local currencies will be available later this year.

“We are excited that the U.S. is one of the first markets in which we are launching HSBC Global Wallet,” said HSBC Head of Liquidity & Cash Management, U.S. and Canada Drew Douglas. “We are excited for the launch and looking forward to expanding the breadth of currencies as we move forward and to introducing receive ‘like a local’ functionality in the very near future.”

Today’s news follows the launch of HSBC’s Global Money account in November of last year. Based on a similar concept, the Global Money multi-currency account enables the bank’s retail banking customers to convert, hold, and transfer multiple currencies from one account. Users can hold up to eight currencies at once and can send money instantly to other HSBC accountholders in more than 15 countries for free.

While the launch of a multi-currency account is a win for HSBC in today’s global economy, there is still one element notably missing– cryptocurrency. The multi-currency accounts that fintechs such as Revolut offer enable users to buy, sell, and hold multiple cryptocurrencies. While HSBC said it has “a pipeline of new currencies and enhancements,” the bank made no mention of future cryptocurrency plans.

In a round featuring new investors Saints Fund and Eric Benhamou of Benhamou Global Ventures, cross-border transaction monitoring solution provider ThetaRay has raised $31 million in new funding. Led by JVP and BGV Funds, the investment round also featured participation from current investors OurCrowd, Bank Hapoalim, SBT, and others. The funding takes the Israel-based company’s total capital to more than $90 million and will be used to help ThetaRay bring its cloud-based, transaction monitoring solution to new markets.

“We are on the verge of a real revolution in securing the global financial system,” ThetaRay CEO Mark Gazit said. “During this period, when the cross-border payment network has become the lifeblood of the world trade infrastructure, ThetaRay is here to instill certainty and reduce risks in secure, cross-border payments.”

ThetaRay’s announcement comes as the governments of both Nigeria and the Ukraine have implemented ThetaRay’s technology to protect cross-border payments from financial crime. The cross-border payments market, estimated at $25 trillion a year, increasingly has been targeted by financial criminals in the post-COVID environment. Unfortunately, the response to this threat has involved tightened controls and enforcement that have resulted in challenges – from slow service to outright blockages – for many of those businesses and banks that need to make legitimate cross-border payments.

To this end, ThetaRay’s SaaS offering analyzes SWIFT traffic, risk indicators, and data from clients, payers, and payees to spot patterns and anomalies that are indicative of suspicious activity – including money laundering and terrorist financing. The technology leverages a proprietary approach to machine learning called “artificial intuition” which simulates the decision-making aptitude of human instinct and subjectivity. Referred to as the “fourth generation of AI,” artificial intuition is being applied to help financial institutions spot large-scale, more sophisticated cybercrime strategies by analyzing the various parameters of the massive number of individual transactions that may make up a given fraud attempt.

“This revolution will enable many organizations and people around the world to transfer money faster, more securely, and with far fewer fees and stops along the way,” JVP founder and chairman Erel Margalit said. “What Swift did to the banking world 25 years ago, ThetaRay will do to the banking world in the next ten years.”

Founded in 2013 and making its Finovate debut two years later at FinovateFall, ThetaRay launched its cloud-based, anti-money laundering (AML) solution for cross-border payments last month. Also in April, the company appointed former Fundtech/Finastra Payments executive Dagan Osovlansky as its new Chief Product Officer. ThetaRay also won the Transaction Security Innovation Award this spring from the FinTech Breakthrough Awards program.

If you missed FinovateSpring last week, what did you really miss?

The conference was alight with new ideas and new connections, and if you were registered for the show, there is still time to see any sessions you may have missed; just check out the On Demand content section of the event platform. For everyone else, here are some of my biggest takeaways.

1. The focus is still on the customer, but with a 2021 twist

I was slightly disappointed when I realized that the mantra of this year’s show would once again be, “it’s all about the customer.” It became clear, however, that the conversation around the customer today is much different from the customer centricity we were talking about in 2017.

That’s because the way we think of community has changed. Consumers no longer align solely with those in their same geographical location. Instead, their community now encompasses others who share their identity. Or, as young millennials would say, their community is comprised of others in their tribe.

This shift is key for financial services organizations to understand. The “personalization” game is no longer about targeting consumers based on their geography and assets. Instead, it is about focusing on the unique needs of each tribe or identity segment.

This is something that digital banks do quite well. And as we move into a post-COVID economy in which individuals and businesses are struggling to get back on their feet, incumbent players can no longer look at personalization the same way by simply personalizing messaging.

Instead, incumbents need to look at the moves of digital banks over the past few years. Many of these smaller players have brought consumers what they’ve been craving: truly personalized solutions and tools that fit their needs. This identity-based banking is something we’ve seen crop up in the past few years and is getting even more specific: from banks that market to gig workers or specific ethic groups to women-specific banks.

2. Security is getting scary

Online data security concerns have been escalated since the onset of the COVID crisis. Since more of our daily business is taking place online, there are more opportunities for fraudsters to take advantage of the data by selling or misusing it.

In his discussion on quantum computing, Cambridge Quantum Computing Head of Quantum Cybersecurity Duncan Jones highlighted the reality that quantum computing is getting close to the point of breaking encryption. In effect, quantum computers can find patterns that no human eye can detect.

When we get to this point in quantum computing, Jones noted, bad actors will be able to hack encrypted material both in the past and present. This means that hackers will soon be able to listen in on and view any messages that were sent encrypted in the past– from personal identifiable information, to financial data, to pharmacy patents.

Fortunately, Jones estimates that we are still five-to-ten years out from running into issues with broken encryption. However, he urged banks to start acting now by switching to new encryption algorithms.

3. Our CBDC future is real, but we’re not there yet

Central bank digital currencies (CBDCs) peppered discussions throughout the four-day event.

Most panels and experts agreed that the U.S. is on-track to launch its own CBDC, even though it is likely still years in the future. Top on the mind of many is how a CBDC will impact banks, fintechs, and existing cryptocurrencies.

While there is some disagreement, most agree that a CBDC won’t completely obliterate banks or fintechs as we know them today. In fact, it may even enhance some aspects of the user experience. And as for cryptocurrencies, I heard general consensus that cryptocurrencies can and will co-exist alongside a CBDC (so don’t sell your bitcoin yet).

Switzerland-based banking technology provider Temenospartnered with digital assets platform Taurus this week. Through the partnership, Temenos integrated Taurus’ digital asset and blockchain infrastructure with Temenos Transact, the company’s core banking software.

As a result, Temenos’ 3,000 bank and FI clients across the globe will have access to digital assets. Taurus will enable them to integrate and manage any digital asset, traditional securities, and cash.

“Investors are increasingly aware of the performance of cryptocurrencies, which can effectively participate in the diversification of a portfolio,” said Temenos Product Director Alexandre Duret. “Taurus is leading the field in cryptography and blockchain technology. By joining forces, we can help banks to bridge the gap between traditional investments and digital assets.”

With its securities firm license from the Swiss Financial Market Supervisory Authority, Taurus can cover digital currencies, cryptocurrencies, as well as tokenized assets. The company offers three main products: Taurus-CAPITAL for tokenization and lifecycle management, Taurus-PROTECT for hot, warm, and cold digital asset custody, and Taurus-EXPLORER an API-based blockchain connectivity to more than 10 blockchain protocols.

Temenos has added Taurus’ tools to the Temenos Marketplace, a partner ecosystem of 50+ fintech solutions. All tools in the MarketPlace are pre-integrated for fast implementation.

Founded in 1993, Temenos is a public company, listed on the SIX Swiss Exchange under the ticker TEMN. The company has a market capitalization of $9.84 billion.