This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

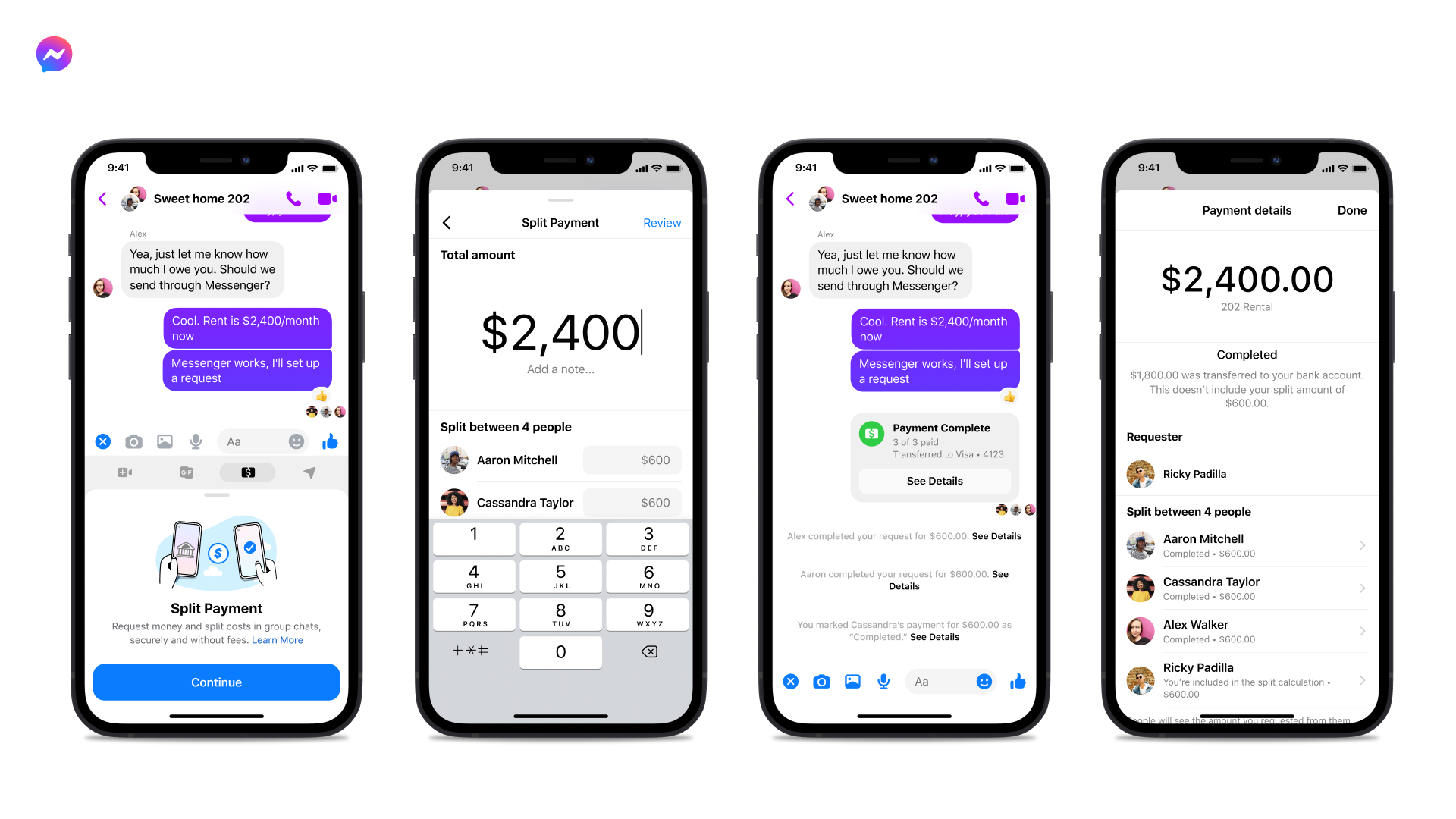

Facebook Messenger unveiled today that it will pilot a feature that will allow users to split payments in the Messenger app. Facebook will begin testing the “free and fast way to share the cost of bills and expenses” next week for users in the U.S.

In a group chat or payments hub within Messenger, users select “get started” and can split a bill evenly or modify each person’s contribution amount. After the amounts are determined, users enter a personalized message, verify their Facebook Pay details, and send their request in a group chat in Messenger.

The launch of Facebook Messenger’s Split Pay feature comes as “Request to Pay” is heating up in the fintech world. Venmo has used QR codes to facilitate person-to-person payments since 2017, and Messenger began using similar functionality in June of this year.

Outside of the P2P realm, Request to Pay is becoming a popular way to replace payment methods such as cards, invoices, and direct debits in B2C and B2B transactions. Essentially, customers can pay for everyday purchases within a messaging framework. Shoppers can, for example, pay for their lunch by opening a push notification on their phone and accepting the payment, thereby finalizing the transaction.

Merchant services aggregator and mobile payment company Square is rebranding to Block on December 10 and can be found at block.xyz. The new name will refer to the company as a corporate entity, which is the parent company to multiple subsidiary businesses.

Since it was founded in 2009, Block has built a sizable seller business that offers commerce solutions, business software, and banking services for merchants. This branch of the company will retain the brand name Square. The California-based company also offers Cash App, a challenger bank; TIDAL, a subscription-based music streaming service; and TBD54566975, a decentralized Bitcoin exchange. In addition to creating clarity around these brands, the company also notes that the rebrand “creates room for further growth.”

“We built the Square brand for our Seller business, which is where it belongs,” said Block Co-founder and CEO Jack Dorsey. “Block is a new name, but our purpose of economic empowerment remains the same. No matter how we grow or change, we will continue to build tools to help increase access to the economy.”

In addition to renaming the corporate brand, Block is also changing the name of Square Crypto, a company initiative to advance Bitcoin, to Spiral. Square, Cash App, TIDAL, and TBD54566975 will each maintain their brand names.

Being a three dimensional representation of a Square, the name Block gives more depth to the company’s image. The company said that the new name represents “building blocks, neighborhood blocks and their local businesses, communities coming together at block parties full of music, a blockchain, a section of code, and obstacles to overcome.”

Block went public as Square in 2015 on the New York Stock Exchange. The company’s ticker symbol, “SQ,” will remain the same.

This news comes after Block CEO and Co-founder Jack Dorsey announced his departure from Twitter earlier this week. Dorsey had been CEO of Twitter since he co-founded it in 2006. Interestingly, Dorsey said he left Twitter because he considers founder-led organizations to be “severely limiting and a single point of failure.”

Last year, while the pandemic was heating up, banks’ attitudes toward small business lending turned cold. With lockdown measures in place, underwriting became difficult and risk increased across commercial lending.

We tapped ForwardAICEO and Co-Founder Nick Chandi to discuss what the current lending environment looks like, how data can help, and what we can expect to see in 2022.

A serial entrepreneur, Chandi co-founded ForwardAI, a fintech that helps banks, lenders, and businesses access and analyze small business data. The company launched earlier this year to help fill the gap in small business-focused technology available to companies that serve small businesses.

What are some unseen advantages in leveraging financial data when underwriting small business loans?

Nick Chandi: The trend I’ve seen has been a shift to leveraging direct financial data, as in connecting to banking, accounting, payments, and commerce software using APIs instead of having potential borrowers export to spreadsheet or PDF. In the past, all lenders did the latter option and that caused a huge hiccup. After all, whereas with accounting data you can see insights like client base diversification, profits and loss statements, and more, that data can be manipulated to look better than reality. With banking data, it’s the opposite; data is often context-less but it’s practically impossible to fake.

Previously, when lenders looked at financial accounting data, they would have to manually cross reference transactions. This was a tedious task often taking weeks, but one that with API technology these days can be done in seconds using machine learning and AI. This can lead to exceptional savings for banks and lenders in their loan underwriting time.

In 2021, what kind of appetite have you seen from banks when it comes to small business lending? Has the pandemic caused more hesitancy than in years past?

Chandi: For a while in 2020, many lenders completely stopped lending to small businesses. In 2021, we saw much of the industry has returned to or pretty close to business as usual.

Have you noticed a specific type of lender take on more small business loans?

Chandi: We have seen that revenue-based financing has become very popular in the last year. This can be seen from the valuation of Pipe ($2 billion in May 2021) as it provides an opportunity for entrepreneurs to transform their future revenue into an asset with instant access to annual cash flows.

Previously, it cost lenders about the same amount to review a business for a $50k application as it did for a $250k application. As lenders begin to incorporate automation and process loan applications faster, that cost goes down and becomes more profitable. I have noticed lenders are incorporating more small business loans into their offerings, even if it wasn’t a market they put significant effort into previously.

What trends do you expect to see in small business lending going forward into 2022?

Chandi: The biggest trend change is going to be that direct data access I mentioned earlier. Simply put, with modern lenders using direct access to permissioned data instead of spreadsheets and PDFs, we can expect lenders to process significantly more financing applications and faster than ever before. Traditionally, SMBs have been a market that most companies haven’t focused on, but after the pandemic I think a lot of the public sentiment has shifted towards desiring and expecting more support for struggling small businesses in their community.

Going into 2022, I expect to see financial institutions and fintechs across the world upgrade their services and begin offering better products; enhanced financial management portals, expedited lending options, personalized financing offers based on predictive data, and proactive cash flow alerts may soon one day be normal. That’s part of the reason we created ForwardAI.

Watch ForwardAI’s demo from FinovateFall 2021 below:

When it comes to Florida’s credit unions, in terms of both assets and membership, it doesn’t get any bigger than Suncoast CU. Founded in 1934 as Hillsborough County Teachers Credit Union, the institution converted to a federal charter as Suncoast Schools FCU in 1978. The company has since become the largest credit union in the state of Florida, as well as the 10th largest credit union in the U.S. based on membership and assets, which total more than $14 billion. The credit union has 75 full-service branches and serves more than 991,000 members in 40 counties in Florida.

The credit union also has become the latest institution to team up with financial data platform and modern connectivity leader MX. Suncoast will leverage MX’s data enhancement platform, its PFM, and MXinsights technology to enable its members to proactively manage and take action to improve their finances. The partnership is designed to improve processing efficiencies for Suncoast, as well as fuel more customer-engaging experiences and accelerate growth, by putting the institution’s data more accessible and more actionable.

“By providing our members with a better experience, powered by accessible and relevant information about their financial lives – what they need and when they need it – we’re helping them solve real issues on their terms,” Suncoast Credit Union President and CEO Kevin Johnson said. “We believe this will lead to even more connected Suncoast members and provide more availability for our employees to provide personalized assistance.”

As part of the collaboration, Suncoast’s members will gain access to budgeting, auto-categorization, and debt management tools, as well as the ability to view all of their data in a single platform. The credit union will be able to leverage MXinsights to play a proactive role in their member’s financial health, communicating with them about their account activity and empowering them to develop and maintain healthier financial practices.

“The combination of cleansed, intelligent data powering personal financial insights that MX is providing Suncoast makes for a delightful money experience from a credit union that truly cares about the financial health of its members in Florida and beyond,” MX Chief Customer Officer Nate Gardner said.

A multiple time Finovate Best of Show winner, MX has teamed up with a number of customer-centric financial institutions in recent months. This includes a partnership with Massachusetts-based Cambridge Savings Bank to help the $5 billion asset institution launch its Money Management personal finance visualization solution. MX has also partnered with fintechs such SUMA Wealth, which is dedicated to serving the Latin/Hispanic community, as well as with payroll connectivity API company Pinwheel and credit union mobile banking solution provider Mahalo Technologies. Headquartered in Lehi, Utah, MX was founded in 2010. Ryan Caldwell is co-founder and CEO.

It’s hard to read about David Marcus’ departure from Meta’s cryptocurrency project Diem (formerly Libra) and digital wallet Novi, and not wonder what’s next for the stablecoin.

Marcus announced over Twitter yesterday that he is leaving the company. In a tweet, he said, “Personal news: after a fulfilling seven years at Meta, I’ve made the difficult decision to step down and leave the company at the end of this year. While there’s still so much to do right on the heels of launching Novi — and I remain as passionate as ever about the need for change in our payments and financial systems — my entrepreneurial DNA has been nudging me for too many mornings in a row to continue ignoring it.”

While it’s easy to make assumptions based on Marcus’ tweet, there is still a lot we don’t know about the fate of Diem and Novi. With all of the uncertainty, let’s look at what we do know about Meta’s stablecoin project. Here are the five chapters in the life of Diem (so far).

Launches as Libra Facebook announced Libra in June of 2019. The company said that its new cryptocurrency would help users transact and transfer funds with near-zero fees via the corresponding wallet, Calibra, that would be integrated into WhatsApp, Messenger, and Facebook. In order to decentralize control from Facebook, The Libra Association was formed to govern the new cryptocurrency and wallet. The 27 founding members included Visa, Uber, and Andreessen Horowitz.

Politicians object Criticism of the project began building up and, months after launch, global privacy regulators, central bankers, and finance ministers all voiced their concerns about the new cryptocurrency and wallet. Specifically, Federal Reserve Chairman Jerome Powell aired his concerns of privacy, money laundering, consumer protection, and financial stability.

Major founding members withdraw By October of 2019, just four months after Facebook unveiled Libra, some of the top founding members pulled out of the project. PayPal, eBay, Visa, Mastercard, and Stripe announced they would no longer be part of Facebook’s cryptocurrency project.

Changes name to Diem and pivots to a stablecoin In December of last year, Facebook changed the name of its cryptocurrency from Libra to Diem. The move came after the company changed the name of its wallet from Calibra to Novi. Facebook said that the rebrand signals the project’s “growing maturity and independence.” At the same time, the company announced that Diem will be a stablecoin, which is a cryptocurrency pegged to government-issued currency.

Marcus departs, former PayPal exec Stephane Kasriel steps in The most recent chapter in Diem’s storied history is yesterday’s news on Marcus’ departure. Starting next year, former Upwork CEO and former VP of Product for Novi Stephane Kasriel will lead Meta’s cryptocurrency unit.

As for what’s next for the cryptocurrency, it doesn’t appear to be fizzling out any time soon. The project still has a handful of major industry backers and, being the child of Meta, has plenty of funding to back it up. These factors, combined with an increased interest in decentralized finance, are enough to keep Diem afloat for at least another year.

Small business financial platform Fundboxclosed a $100 million Series D funding round this week. With this funding, the California-based company is now a freshly-minted unicorn with a valuation of $1.1 billion.

The round, which brings the company’s total funding to $553 million, was led by Healthcare of Ontario Pension Plan (HOOPP) and had contributions from existing investors Allianz X, Khosla Ventures, and The Private Shares Fund. New investors Arbor Waypoint Select Fund and funds managed by Newton Investment Management North America also contributed.

Fundbox was founded in 2013 to help small businesses access working capital through credit and payments solutions. The company has invested $100 million into AI technology with an aim to gain deep insights into the small business ecosystem.

Today’s investment comes at a time of growth for Fundbox. The company has experienced new customer acquisition growth of over 200% this year, has surpassed $2.5 billion in transaction volume, and has connected with over 325,000 businesses since launch.

The new capital will also help Fundbox expand into payments. The company is launching a tool called Flex Pay that will offer small business owners additional payment options and flexibility for business expenses. In addition to repaying loans via bank account or credit card, businesses have a buy now, pay later option in the form of a Line of Credit draw.

“The addition of Flex Pay to our product offerings is critical as small business owners look to utilize buy now, pay later solutions for business,” said Fundbox CEO Prashant Fuloria. “We remain committed to leveraging our superior AI, data-native approach, and small business insights to solve working capital needs and power the resurgence of the small business economy.”

Fundbox has additional financial products in the pipeline for next year. The company is working on a subscription revenue stream, a product for entrepreneurs with multiple small businesses, and tools to help new businesses that lack financial history.

A new partnership between credit underwriting software provider Zest AI and Wyoming’s largest credit union, Blue Federal Credit Union, will enable the institution to provide faster and more accurate loan decisioning across its auto, credit card, and personal loan portfolios.

Blue Federal Credit Union Chief Credit and Risk Officer Jason Buchanan called the partnership with Zest AI “a big win for our members.” He added that “Zest will also allow Blue to reach underserved borrowers across the credit spectrum while maintaining our standards of compliance and credit risk management. The granularity we have access to through Zest is broad and provides all of the features and details we need to explain our credit decisions.”

Zest AI leverages more data and better math to enable banks and credit unions to move beyond the limitations of their legacy credit scoring methods. The company claims that its models use 10x more variables to provide a more accurate picture of borrower risk and empower its financial institution partners to approve more borrowers safely. Blue FCU expects to deploy Zest AI’s technology early next year, and anticipates a 30% boost in loan approval rates as well as the ability to make loan decisions in less than five seconds.

“A Zest-built model gives them transparency, control, and a faster and more accurate decision that approves more members,” Zest AI CEO Mike de Vere said. “Blue’s investment in Zest is really an investment in its community.”

Headquartered in Los Angeles, California, and founded in 2009, Zest AI is a registered Credit Union Service Organization (CUSO) whose credit union customers represent $56 billion in assets and four million members. Named one of Fast Company’s “Next Big Things in Tech” last month, Zest AI won the 2021 Finovate Award for “Best Use of AI/ML” in September. This year, the company forged a partnership with student payment platform Climb Credit, and collaborated with Florida’s largest credit union Suncoast Credit Union. Over the summer, Zest AI secured $18 million in funding in a round led by strategic investors VyStar Credit Union and First National Bank of Omaha. The investment took the company’s total capital raised to $250 million.

With more than 100,000 members in communities across Wyoming and Colorado and beyond, Blue FCU was launched as Warren Federal Credit Union in 1951. The institution merged with Community Federal Credit Union in 2016, and rebranded as Blue FCU. The credit union moved its headquarters to Cheyenne earlier this year, and currently has more than $1.4 billion in assets. Stephanie Teubner is CEO and President.

Cryptocurrency exchange platform Coinbaseacquired Israel-based security company Unbound Security today. Terms of the deal, which Coinbase calls the next phase of its security journey, were not disclosed. Coinbase expects the deal to close in the coming months.

Unbound specializes in cryptographic security technologies, including secure multi-party computation (MPC), an emerging subfield of cryptography that allows parties to jointly compute a function over their inputs while protecting their data. Essentially, MPC enables crypto assets to be stored, transferred, and deployed more securely, easily and flexibly.

Today’s deal will give Coinbase access to cryptographic security experts, including Unbound Co-founders Guy Peer and Yehuda Lindell, who is considered a world leader in MPC. Coinbase will also gain a presence in Israel and plans to establish a tech center in the country. The company states that this global reach will “add an additional powerful prong” to its global talent acquisition strategy.

“We’ve long recognized Israel as a hot bed of strong technology and cryptography talent, and are excited to continue to grow our team with some of the best and brightest minds in these fields,” the company said in its blog post announcement. “The Unbound Security team will form the nucleus of this new research facility, which we plan to grow over time.”

The purchase of Unbound marks Coinbase’s twentieth acquisition since the company was founded in 2012. Coinbase has acquired six companies this year alone, including financial software company BRD, voice AI startup Agra, crypto wallet API provider Zabo, financial infrastructure company Skew, and blockchain security firm Bison Trails.

Coinbase, which demoed at FinovateSpring 2014, went public earlier this year and now trades on the NASDAQ under the ticker COIN. The company has a current market capitalization of $67 billion. Earlier this fall the company announced plans to launch its own NFT marketplace, Coinbase NFT, to help users mint, purchase, showcase, and discover NFTs.

South Korea-based Shinhan Bank recently wrapped up testing the use of stablecoins for cross-border transactions. The bank completed a proof-of-concept issuing and distributing stablecoins with an unnamed “megabank” outside of Korea. The two are leveraging the Hedera Network’s Hedera Token Service (HTS) and Hedera Consensus Service (HCS) to make the transfers.

Shinhan Bank will mint stablecoins backed by the South Korean Won (KRW), while the unnamed bank will mint stablecoins backed by its local currency. Under their partnership, customers can buy Shinhan’s KRW-based stablecoin and send them to an account at the other, unnamed bank. The recipient of the funds can then exchange the stablecoins for local currency.

Shinhan Bank opted to target international remittences because it is one of the sub-sectors with the most room for disruption. Cross-border transactions generally cost customers high intermediary bank costs, take three-to-seven days to complete, and don’t allow customers to track the funds while they are in progress.

“International remittances were a massive market of $702 billion in 2020, with $539 billion going to low- and middle-income countries,” said Hedera CEO and Co-founder Mance Harmon. “There is a massive opportunity to cut out the middleman and make this process dramatically more efficient and cost-effective, getting the most money possible to people who often need it urgently. We commend Shinhan and their partner for developing this solution, and are proud that it takes advantage of the economic and speed benefits that only the Hedera network can provide.”

This isn’t Shinhan Bank’s first time leveraging decentralized finance. In March, the bank partnered with LG CNS to create a platform for central bank digital currencies (CBDCs). The banks has also invested in Korea Digital Asset Custody (KDAC), a group of businesses that provide digital-asset custody services, and joined the Hedera Governing Council in April 2021.

An investment of $35 million will enable Solutions by Text (SBT), a compliant text messaging platform for consumer finance companies, to power broader adoption of its solution across the consumer finance lifecycle. The growth financing round was led by Edison Partners, and featured the participation of Stifel Venture Bank, a division of Stifel Bank.

In addition to the funding news, Solutions by Text also announced the appointment of former ACI Worldwide executive David Baxter as its new Chief Executive Officer

“Now more than ever, consumer finance organizations are taking a hard look at how to strengthen digital consumer relationships while maintaining compliance with national standards,” Baxter said. “Our opportunity to capture market share through existing and expanded platform capabilities is immense and we’ve assembled an exceptional team and board to turbo-charge this next chapter of growth.”

As part of the investment, co-founder Mike Cantrell and Edison Director Network members Ron Hynes and Nick Manolis will join the Solutions by Text board of directors.

Headquartered in Dallas, Texas, and maintaining remote teams and offices throughout the U.S. as well as in Bangalore, India, Solutions by Text was founded in 2008. The company’s technology is used by more than 1,400 consumer finance companies – ranging from auto finance and lending to banking – who use SBT’s compliant texting solutions to support origination, servicing, and collection operations. Solutions by Text helps ensure that communication policies and practices are compliant with key regulations such as the Consumer Finance Protection Bureau’s Fair Debt Collection Practices Act (FDCPA), including a new Regulation F which went into effect today. The revision clarifies the ability of consumers to stop collection calls and/or text messages and is intended to respond to the rise of new communications methods.

Solutions by Text offers two-way texting to ensure seamless communication with customers, as well as a pay-by-text product, Text Pay, and a customizable URL shortening tool called SmartURL. SBT’s technology can be integrated via the company’s API, which enables access to the full range of the company’s text messaging tools including budgeting, reporting, file imports, message templates, and distribution lists.

“(SBT) is uniquely positioned to scale growth in the fintech market with a team of deep regulatory compliance, messaging, and payments expertise, not to mention a sizable loyal customer and partner base with significant embedded opportunity,” Edison Partners General Partner Kelly Ford said. “Eight in ten U.S. adults use text messaging on a regular basis,” Ford noted. “With Solutions by Text, financial institutions are meeting these consumers where and how they want to be met, and doing so with peace of mind.”

Open finance network Plaid commissioned a survey from Harris Poll earlier this year to provide insights and analysis on fintech’s consumer impact in the U.S. and U.K. This fall, Plaid published a report based on the survey that detailed three overarching conclusions about the state of fintech.

Here’s a look at each of the findings below, along with what they mean for banks and fintechs in 2022.

Users’ switch to digital is permanent

Plaid’s survey found that for about half of the respondents using technology to manage finances is a habit. In fact, 58% said that they, “can’t live without using technology to manage their finances.”

Additionally, almost 70% of survey respondents said they use technology “as much as possible” to manage their money due to the pandemic. And it appears that this trend isn’t isolated to pandemic times. The study found that between 80% and 90% of respondents who used fintech in the past year plan to use it the same amount or more in the future.

Fintech spans demographics

According to the answers from respondents in Plaid’s survey, fintech is helping to level the playing field of financial management. Respondents across racial lines and generational divides are turning to technology to help them not only manage their finances, but also get further ahead.

For example, 37% of Black respondents and 31% of Hispanic respondents use online-only banking services to minimize fees they may incur with accounts. Additionally, 32% of Hispanic respondents use earned wage access tools to receive their pay early and avoid payday loans. In addition to offering access to tools, fintech also enhances financial education. Plaid’s study found that 28% of Black respondents and 24% of Hispanic respondents didn’t track their credit scores at all before they started using fintech.

The survey indicated that the youngest generation surveyed (Gen Z) and the oldest generation surveyed (Baby Boomers) have been the most impacted by fintech. More than 70% of Gen Z respondents said that fintech helps them build better financial habits. When it comes to Baby Boomers, almost 70% of them reported that they feel confident using technology to manage their finances. This figure is up 16% from the year prior.

Fintech is becoming part of every day life

Perhaps the most noteworthy statistic in Plaid’s survey is that almost half (48%) of Americans use fintech on a daily basis. This figure is up 30% from the year prior, when 37% of respondents said they use it daily.

Interestingly, the survey indicates that this usage is more heavily weighted toward positive aspects of financial management, such as budgeting and investing, versus negative ones, such as billpay. In its analysis, Plaid suggests this is because the negative aspects are often automated.

In its conclusion, Plaid indicates that fintech is no longer separate from traditional financial institutions. Rather, because of embedded finance, fintech is simply the new way of conducting finances digitally.

Looking ahead

What do these shifts mean for banks and fintechs in 2022? In short, they indicate that there’s no going back on the road to digital. Even some of the most reluctant user groups have switched to digital and their usage is only increasing. The findings also indicate that the sector is poised for even more growth. The increase in demand, combined with new capabilities brought forth by enabling technologies, ultimately means that there will be new opportunities to serve users in new ways in the years to come.

Payment card startup Slice received a $220 million Series B investment today, bringing its total funding to $291 million and boosting its valuation to over $1 billion, unicorn status. This is an impressive jump in valuation. According to TechCrunch, the India-based company was valued at under $200 million less than six months ago when it raised $20 million in funding in June of this year.

Today’s round was led by Tiger Global and Insight Partners and saw contributions from Sunley House Capital, Moore Strategic Ventures, Anfa, Gunosy, Blume Ventures, and 8i. Slice plans to use the funds to expand its product line by launching a payment card for teens. The company is also working on adding support for the country’s real-time payment rails, unified payments interface (UPI), and a digital ID product.

Slice is aiming to disrupt India’s credit card industry by relying on its own underwriting system. The company, which targets millennials, has five million registered users and is currently issuing more than 200,000 cards every month, making it the third largest card issuer in India.

Because of its in-house underwriting, Slice doesn’t require a credit score; anyone over the age of 18 can apply. Credit limits are relatively low, starting at $26 (₹2k). Additionally, the fintech doesn’t charge a joining fee, or an annual fee. Cardholders can get up to 2% cashback on purchases and receive weekly deals from brands such as Amazon and Netflix.

Slice’s name comes from one of its most differentiating features. The company allows cardholders to “slice” all of their bills over the course of three months into multiple installments.

“Slice targets an underpenetrated market in India and seamlessly allows users to make online payments, pay bills and more,” said Insight Partners Managing Director Deven Parekh. “There is a large opportunity in the credit and payment space in India, and Slice is well-positioned to become the leader in the industry. We look forward to this partnership with slice as they continue to scale up and grow.”