This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Cryptocurrency exchange platform Coinbaseannounced plans this week to launch its own NFT marketplace. Dubbed Coinbase NFT, the new marketplace will help users mint, purchase, showcase, and discover NFTs.

“Just as Coinbase helped millions of people access Bitcoin for the first time in an easy and trusted way — we want to do the same for the NFTs,” said Coinbase VP of Product and Ecosystem Sanchan Saxena.

Coinbase NFT, which the company aims to launch at the end of this year, will offer a user-friendly interface that the company said will be “as simple as tapping a few buttons.” The new platform will be creator-centric, placing art and the artist’s experience at the forefront.

Coinbase is putting creators first by leveraging decentralized contracts and metadata transparency to help artists maintain creative control. Additionally, the platform will cultivate a community for artists and their fans using social features to help users discover and discuss NFTs. Coinbase NFT will curate a personal feed based on users’ interests. User profiles will showcase all of their NFTs and will help them connect with like-minded collectors and artists.

“Our ambition with Coinbase NFT is to allow everyone to benefit from their creative spark; to contribute to a future where the creator economy isn’t a small subset of the real economy, but a central driver,” said Saxena.

Coinbase NFT will compete with NFT exchange platforms such as OpenSea, one of the major players in the space. According to TechCrunch, OpenSea facilitated $3.4 billion in transaction volume in August of this year. Coinbase NFT boasts two differentiating factors that set it apart from OpenSea. The first is that Coinbase is placing a large focus on the social and community aspects of its tool, something that OpenSea lacks. Coinbase’s second differentiation is that it comes with brand recognition and a built-in client base of 68 million users.

Currently, there is no word from Coinbase on the commission percentage it will charge artists, nor on the royalty percentage for perpetual trades. Whatever it decides, it will need to compete with OpenSea’s relatively-low 2.5% fee.

Coinbase went public on the NASDAQ earlier this year, trading under the ticker COIN. The San Francisco-based company’s user numbers increased 44% in the third quarter of this year, up from 56 million users in the previous quarter. Brian Armstrong is CEO.

Accounts receivable automation firm Billtrust made its first acquisition since going public via a SPAC merger a year ago. The New Jersey-based company purchased collections management company iController for $58 million.

Belgium-based iController was founded in 2017 and offers a SaaS product that provides credit and collections professionals visibility into cash flow management. Billtrust will acquire the iController team, along with the company’s 566 Europe-based clients. iController employees will continue working in the company’s offices in Belgium The Netherlands.

“Acquiring a great company like iController is consistent with our growth plan of strategic global expansion in targeted ways to broaden our customer footprint and provide extended value to our current customers,” added Billtrust Founder and CEO Flint Lane.

Billtrust was founded in 2001 and today’s deal marks the company’s eighth acquisition.

Billtrust offers a wide variety of products, including credit, ecommerce, invoicing, payments, managed services, training, and more. The company also offers a collections tool, which will be enhanced with iController’s collections product. Billtrust President Steve Pinado described iController as “a strong strategic fit,” saying that the company will help Billtrust not only expand its physical presence in the European market but also enhance its collections capabilities.

In 2013, Billtrust launched its Business Payments Network, a service that connects suppliers to accounts payable automation platforms buyers are using to pay, as well as to a network of third-party banks and ERPs. Earlier this year, the company updated the platform to now support bi-directional exchange of transactional data and documents. The new release now enables invoice presentment to accounts payable portals.

Data-driven decision-making is something most businesses aspire to. However, for the majority, significant data silos across the enterprise often means that the data they are using is delayed and inconsistent – resulting in decisions that are neither timely nor accurate. Instead, what organizations need is real-time access to their data and a consistent enterprise view. Fortunately, this is where a data fabric with both embedded analytics and self-service business intelligence (BI) can be extremely powerful.

The use of embedded analytics and self-service BI in combination with a data fabric allows organizations to give a wider range of users the ability to visualize and explore data more freely, empowering employees, partners, and customers with accurate information. Yet, while most organizations recognize the value of actionable analytics, currently most struggle to provide critical metrics and access to ad hoc analysis. In fact, our research shows that only 7% of organizations say more than half of their employees have access to a data analytics platform.

With a staggering 93% of organizations revealing that the majority of their employees don’t have access to analytics, let’s look at how they can set themselves up to become a more data-driven organization.

Bridging data silos with embedded analytics tools

To gain the most benefit from their data and analytics platform, businesses should look to start prioritizing and bridging data within their organization. While they are likely to be faced with a large number of silos, prioritizing key metrics and iteratively connecting data sources will allow companies to reduce redundant data and provide a common language across data sources.

Implementing a smart data fabric, a new architectural approach, will also help to remove silos and help organizations to gain a common semantic view of the data, even if that data remains distributed. Businesses that have grown through mergers, acquisitions or organic expansions benefit from both local and organization-wide visibility. A common semantic view will also enable performance comparisons over time – day to day or year over year, and allow for analysis of patterns and trends.

Vitally, this enterprise view will give businesses a firm foundation to introduce analytics capabilities.

Figure out what needs to be measured

Once they have started taking incremental steps to unify their data, organizations should seek to understand where the real business problems lie and the questions they need to answer. As part of this, they should consider what issues or challenges their CEO and business counterparts, such as the CIO and COO, currently face and what will help them characterize and measure improvements.

Using this as a starting point and working back will allow the IT teams who will be undertaking the implementation to understand what data and insights they need to provide to answer the questions those leading the business have. It is also important to leave capacity for additional metrics because once they are being used effectively, there will be a need for future measurements and answers.

This approach will ensure the organization is clear about where to apply analytics to derive the most value and to impact the most change. Following this method, they can then build out the capabilities across different parts of the organization.

Success lies in collaboration

While likely to be driven by IT teams, implementing analytics platforms isn’t just an IT initiative. Instead, it requires collaboration from individuals across the organization.

To guarantee success, different teams should work together iteratively and constantly assess the contributions being made by the introduction of analytics platforms and continue to refine the use cases and required metrics to understand whether they are providing value and what changes might be needed to measure progress.

Taking this approach will help to iron out any issues as they occur and ensure that all users are extracting real value from the platform.

Simplifying the complex

For most businesses, obtaining a single source of truth from which they can gain insights can be extremely complex. Not only do organizations tend to have a large number of data silos, but they already have a range of different technology in place, from data warehouses, data lakes and data marts, to integration platforms and BI tools. As such, the majority are ideally looking to simplify their technology infrastructure, but without having to rip and replace.

Smart data fabrics make this possible, helping businesses to unlock the true potential of their data by speeding up and simplifying access to data assets across the entire business. This is all while allowing existing legacy applications and data to remain in place, to enable organizations to maximize the value from their previous technology investments.

Realizing the value of embedded analytics

The benefits of embedded analytics capabilities span across all industries, allowing businesses to make more informed decisions and enabling a variety of business users to have access to actionable insights. A data platform like InterSystems IRIS which includes embedded analytics and ad hoc analysis tools, also forms an integral part of a smart data fabric architecture. InterSystems IRIS can provide organizations with access to live data on-demand, integrated from multiple applications such as trades, equity and fixed income positions, or treasury.

This technology ensures that businesses are able to make decisions on current data, including live transactional data, and eliminates latency from source systems. Additionally, it supports business user self-service analytics, enabling drill down and ad hoc capabilities and can also help to automate time consuming tasks such as ongoing integration and interoperability – freeing up the IT team to focus on more value-adding tasks.

With access to more comprehensive, accurate, and timely information, employees across businesses will be better placed to make informed decisions and measure the success of new initiatives needed to drive their organization forward.

Grab the popcorn. It’s time to watch some FinovateFall demos and chill. All 74 of this year’s live demos from FinovateFall 2021 are ready for your viewing pleasure.

Simply check out the demo tab on the Finovate website to browse, find, and watch any of the seven-minute demos from last month’s event for free. Already seen them all? Send a link to a colleague who wasn’t able to make it!

The best way to dive in is to check out the demos that the audience voted as Best of Show. Here’s a list to get you started:

Three payments powerhouses have partnered this week in a movement toward fast and seamless cross-border payments. France’s EBA Clearing, Belgium’s SWIFT, and the U.S.’s The Clearing House (TCH) are working together to launch Immediate Cross-Border Payments (IXB).

IXB is a new initiative that can synchronize settlements in two different, instant payment systems and convert real-time messages between both systems. A total of 11 banks contributed to IXB’s design. Seven banks, including Bank of America, BBVA Group, Citi, HSBC, Intesa Sanpaolo Bank, J.P. Morgan, and PNC Bank, participated in the proof of concept alongside EBA Clearing, SWIFT, and TCH, three private-sector, member-owned companies.

“IXB demonstrates how the current ecosystem of cross-border payments may be enhanced and made suitable for new high-volume 24/7 business,” said EBA Head of Service Development and Management Erwin Kulk. “In combination with an international request to pay, its potential applications would be limitless.”

The impetus of IXB is the fact that consumers and businesses have come to expect domestic payments to be sent and received in real time. In their minds, cross-border transactions should be no different.

IXP leverages regional payments infrastructure, such as the RTP network in the U.S. and RT1 in Europe, to help banks of all sizes offer instant, cross-border payments more easily. That’s because, by relying on existing infrastructure, banks don’t need to build or connect to a separate network.

“By utilizing existing faster payments systems, financial institutions can leverage existing processes, protocols, and technology to make the user experience seamless across payment types, whether domestic or cross border,” said TCH’s EVP for Product Development Russ Waterhouse.

One of the biggest experiments in bringing cryptocurrencies to the mainstream is taking place in the small Central American nation of El Salvador. Earlier this summer, the country’s legislative assembly authorized granting Bitcoin status as legal tender inside El Salvador beginning September 7th. One month after Bitcoin joined the U.S. dollar as the second official currency in the country, what can be said of the project so far?

This morning, Reuters took up the question of Bitcoin adoption in the country and discovered that the initiative has boosted use of the cryptocurrency, but that increase in use has come with more than a few “headaches” for many Salvadorans who have attempted to withdraw cash from Bitcoin wallets or make other transactions with the digital asset.

On the adoption front, Forbes reported late this week that the Bitcoin project has resulted in more Salvadorans having digital, Bitcoin wallets than traditional bank accounts. According to the article, approximately three million Salvadorans have downloaded Chivo, the new, government-sponsored digital wallet to facilitate Bitcoin transactions. This adds up to 46% of the country’s 6.8 million population. “By contrast,” Forbes noted, “as of 2017, only 29% of Salvadorans had bank accounts.” The Forbes account also observed that Chivo is not the only option available to those seeking to transact in the cryptocurrency; the availability of other digital wallets suggests that the estimates on early Bitcoin adoption by El Salvador’s citizens could be significantly higher.

El Salvador president and long-time Bitcoin backer Nayib Bukele boasted recently of negotiations with the country’s largest gas stations to offer reduced prices for those paying for gasoline using the Chivo app. But widespread adoption by the country’s retailers will still be one of the initiative’s biggest hurdles. Part of this issue is likely timing- a Reuters story reported that, according to the Salvadoran Foundation for Economic and Social Development, 12% of consumers have used Bitcoin in the month since the Bitcoin Law was implemented, and that 93% of the 233 companies it surveyed were reporting no payments in Bitcoin over the same time period. But another part of the issue may be easily explained by Chivo itself, which provides instant conversion from Bitcoin to dollars – meaning Salvadorans who own Bitcoin can still readily pay for transactions in dollars if they choose to.

Nevertheless, early indications are that the project may accomplish its most important role of promoting financial inclusion – especially among the country’s poorer, rural-based citizenry. While some in the business community remain skeptical – and more aggressive opponents of the measure have resorted to vandalizing and defacing Chivo ATMs – others point to the possible use of Chivo as a way for expat Salvadorans living in places like the U.S. to send money to family still in El Salvador as a use case that could help drive Bitcoin adoption in the country. Potential cost savings of using Chivo instead of traditional money transfer services – as well as the Salvadoran government’s willingness to incentivize Chivo use with Bitcoin bonuses of up to $30 – could help Bukele’s Bitcoin brainchild sustain the momentum it already has achieved in its first 30 days.

Here is our look at fintech innovation around the world.

Areeba, a Lebanon-based, issuing and acquiring service provider to financial services companies in the Middle East, teamed up with Netcetera to implement the latest 3-D Secure protocol 2.2.

MoneyGram, a pre-digital P2P payments player, announced a collaboration this week that will send funds faster and offer consumers more options.

The Texas-based money transfer company is partnering with Stellar Development Foundation, a non-profit that supports the development and growth of the Stellar blockchain network, and Circle, an online platform that enables users to send money. The partnerships will enable consumers using Circle’s USDC stablecoin to receive cash funding and payout in local currency, and will facilitate near-instant backend settlement.

As Stellar Development Foundation CEO Denelle Dixon explained, the partnership combines the reach of MoneyGram’s services with the speed and low cost of transactions on Stellar. As a result, “a new segment of cash users will be able to convert their cash into and out of USDC, giving them access to fast and affordable digital asset services that may have previously been out of reach,” Dixon said.

Once the partnership goes live, end consumers will be able to use MoneyGram to convert USDC to cash, or cash to USDC. United Texas Bank will serve as a settlement bank between Circle and MoneyGram. Thanks to Circle’s USDC, consumers will also see their funds settle in near-real-time, resulting in accelerated money movement, improved efficiency, and reduced risk.

“At MoneyGram, one of our top strategic priorities is to pioneer cross-border payment innovation and blockchain-enabled settlement, and we’re thrilled to now work with the Stellar Development Foundation to further our efforts,” said MoneyGram Chairman and CEO Alex Holmes. “As crypto and digital currencies rise in prominence, we’re especially optimistic about the potential of stablecoins as a method to streamline cross-border payments. Given our expertise in global payments, blockchain, and compliance, we are extremely well-positioned to continue to be the leader in building bridges to connect digital currencies with local fiat currencies.”

This isn’t the first time we’ve seen MoneyGram using blockchain technology. The money transfer giant partnered with Ripple in 2019 to leverage XRP for cross-border payment and foreign exchange settlement. That partnership has since ended, but MoneyGram has gone on to initiate other partnerships that provide broad consumer access to digital currencies.

We sat down with Stephanie Balint, Head of U.S. Strategy & Operations with N26 Inc. in New York, to talk about her experience in the fintech industry, and the continued evolution of technology to solve old and new problems for consumers, and create new opportunities we have yet to think of.

How you get involved in fintech?

Stephanie Balint: I got involved with fintech very early on in my career. Right out of college, I started working in investment banking, and one of my first areas of coverage was fintech, which included players within market structure, exchanges, trading, and technology platforms. By covering that space, I learned a lot about the industry, and eventually moved on to work for a fintech company because I wanted an opportunity to have direct impact in day-to-day operations and scaling fintech businesses. One of the reasons this industry stood out to me is because of the unique aspects of the business models; unlike consumer retail businesses, fintechs are less subject to short-term trends and the whims of consumer demand, and have higher margins and therefore more scalable and profitable economics.

How have you seen the industry change across your career?

Balint: I have seen the industry change immensely over the past 10+ years. When I was first getting started in 2009, there was much more of a focus on established and mature companies who were utilizing older, legacy tech stacks and serving traditional financial institutions, but starting to do so in more tech-forward ways. Over time, I saw an evolution begin to take place with lots of new entrants in the space trying to better serve retail and commercial customer needs by replacing legacy tech. It was incredible to see so many talented people, who had previously worked at older financial institutions, come back to identify a problem in the space and propose new solutions that would eventually improve financial services as a whole and bring it into the modern age.

There have been so many interesting companies founded over the past 10+ years. Many of the small fintech concepts I was watching during my banking career have grown significantly, including neobanking. This was a category that was barely considered or on the radar, and now is its own massive category within fintech – with no signs of slowing down. Q2 2021 was the largest quarter on record for fintech with nearly $31B invested worldwide across 657 deals.

Some of the innovations I’m most excited about are around what I call the “plumbing” of financial services. Things like enabling faster payments, like ACH payments, foreign money transfer, and trade settlements. A lot of companies – like Plaid, Orum, or Wise – have already brought forth incredible solutions. Behind the scenes, as a consumer, you would never know what is driving your ability to get money faster or facilitate complex transactions.

Can you tell us a bit about your current role? How is your company impacting the future of fintech?

Balint: In my current role, I am the interim GM of N26 US. With that, I oversee our operations in the U.S. market, focusing primarily on the strategic and operational side of things. This includes working closely with our legal and compliance team to manage critical business partners, selecting new partners, and overseeing customer service and banking operations. A large part of my role is creating a shared strategic vision for the entity to work towards, as well as developing roadmaps and long, medium, and short term goals to achieve our vision in the U.S.

Where do you see fintech heading in the next 12 months?

Balint: There is a very strong appetite from investors who are trying to find the interesting companies that will rise to the top. I believe there is still a huge opportunity in the “plumbing” side of financial services, particularly with B2B businesses who are working to do things like speed up payments, improve infrastructure, and provide solutions to help globalize money movement. Generally, these businesses are working to bring financial services into the 21st century and it’s fascinating to be a part of this evolution.

What more do you think can be done to support women in fintech?

Balint: At an entrepreneurial level, I think foundational change needs to occur. Encouraging female founders by providing access to capital is essential to helping generate a more diverse fintech startup economy. The issue is that historically women have been underrepresented within VC investing. There are generally not many women in VC investing, compounded by not enough representation and funding of women at a founding level, which in turn leads to underrepresentation of women in fintech across all levels over time.

Within startups, I think it’s important that leaders take steps early on to build out a team that ensures diversity across all facets of the business. Seeking individuals with various social and economic backgrounds will ultimately contribute to a stronger and more inclusive product and diversity of thought within and across teams.

For individuals, I think having strong mentorship from other influential leaders is key to building a strong supportive network that will pay dividends throughout your career.

Where did you find support in the fintech world?

Balint: I had a lot of support early on in banking. As the only revenue-generating female senior managing director, and the only one in an advisory role leading fintech as a practice, my mentor in investment banking took a keen interest in me and helped me to build my network and coverage area to do things earlier in my career than I would have been able to on my own.

Once I moved directly into fintech, I found most of my support from other peers, not necessarily women. Especially at N26, many of the early employees at the company were like-minded and we found similar comradery in terms of drive, motivation, intellect, and general interest in how to navigate a small and growing organization, think critically about things, handle tough negotiations, optimize contracts for best possible terms, and build the team. I found that support from early employees who had gone through it together with me incredibly valuable as I grew in my own career.

What advice would you give to women starting their careers in the industry now?

Balint: First, know your worth. Figure it out early and don’t be afraid to ask other people you know in the industry for comparisons/benchmarks. Demand the pay you deserve and don’t be afraid to negotiate.

Second, invest your money early and often. You may make the same salary as your peers, but if you don’t put your money to work, you’ll be left behind in the long term in terms of wealth creation.

Last, don’t be afraid to ask for things you want. I feel strongly about the “don’t ask don’t get” approach. Ask for a seat at the table, to be included in meetings, for someone to mentor you … what’s the worst that can happen? You can always move on from a rejection but you can never get back a missed opportunity.

In a round led by Aspen Capital Group, digital insurance platform Sureify has raised $15 million in Series C financing. The investment takes the company’s total equity capital to more than $26 million, and will enable Sureify to add to its platform and boost its research and development efforts.

“Ultimately, this funding lets us expand our insurers’ capabilities across digital sales, digital service, and digital engagement,” Sureify CEO Dustin Yoder said. “There is a massive opportunity to continue modernizing the legacy aspects of this industry and this investment in Sureify reinforces that we will help the traditional insurer compete against the emerging digital brands.”

Founded in 2012 and headquartered in San Jose, California, Sureify made its Finovate debut two years later at FinovateSpring 2014. In the time since, the company gained industry-leading life insurance companies as clients – including Allstate, Principal, State Farm, and Penn Mutual-owned Vantis Life. While a growing number of companies have pursued a direct-to-consumer approach to bringing innovation to the insurance industry, Sureify is among those insurtechs that is dedicated to helping legacy insurers successfully incorporate digital technology to better serve their customers. This includes leveraging personalized sales and service to enable insurers to deepen agent/policyholder relationships and boost ROI.

“Sureify has been on a mission to modernize the life insurance industry for nearly 10 years,” Yoder said. “We’ve now proven both large and small life insurers can digitally transform to compete against the direct-to-consumer entrants and meet the ever-changing consumer expectations year over year.” Yoder noted that Sureify’s technology enables insurance providers to pursue modernization without having to abandon their existing systems, and to do so quickly and without undue expense. “There are no longer questions about if traditional insurers can digitally transform sales, service, or engagement,” Yoder said. “The only real question is when?”

Sureify’s solutions include LifetimeACQUIRE, an omnichannel sales enabling solution that leverages quoting, e-application, and automated underwriting to drive placement rates; LifetimeSERVICE, which offers self-service portals and native apps for in-force customers; and LifetimeENGAGE, which features multi-faceted engagement programs and analytics to foster greater lifetime value of individual policyholders.

This year, Sureify has made a number of key executive changes and additions. The company began 2021 with the appointment of a new president Dan Gordon, who had served as Sureify’s Head of Strategy since 2018. The company brought on Ben Brantley as Chief Technology Officer in June and, last month, announced new Vice President of Product Rob Anagnoson.

U.K. bank NatWestacquired children’s allowance-tracking app RoosterMoney this week. Financial terms of the deal are undisclosed.

NatWest plans to integrate RoosterMoney’s Star Chart, Virtual Money Tracker, and Chore Manager into its own offerings in order to provide tools for families and children to learn to manage their allowance money and other funds.

“We want NatWest to be the easiest and most useful bank for families and young people,” said Head of Youth, Retail Banking at NatWest Group Simon Watson. “We know that the world of money is changing, and we want to help parents, carers, and young people feel confident and capable – Rooster helps us do just that.”

Rooster was founded in 2016 and helps its 130,000 U.K. users to learn the basics about money– earning, spending, saving, and giving. In addition to a digital chore chart, RoosterMoney offers a debit card that pairs with the app to offer parental control such as turning the card on and off, blocking certain merchants, and real-time spending notifications.

“At RoosterMoney we believe that if you build financial capability early on, you’re better prepared to take on the challenges that life throws at you,” said RoosterMoney CEO Will Carmichael. “That’s totally aligned with the bank’s purpose and we’re very excited about working together to help more parents and kids to build their financial confidence.”

NatWet said that it will allow RoosterMoney’s existing customers to continue to use the app as usual.

This isn’t NatWest’s first entrance into the youth banking products market. The bank has offered its MoneySense financial education program, that targets kids ages five to 18, for 25 years. Additionally, NatWest recently launched HouseMate, a bill-splitting app for renters, and Island Saver, a game to help young customers learn about money management.

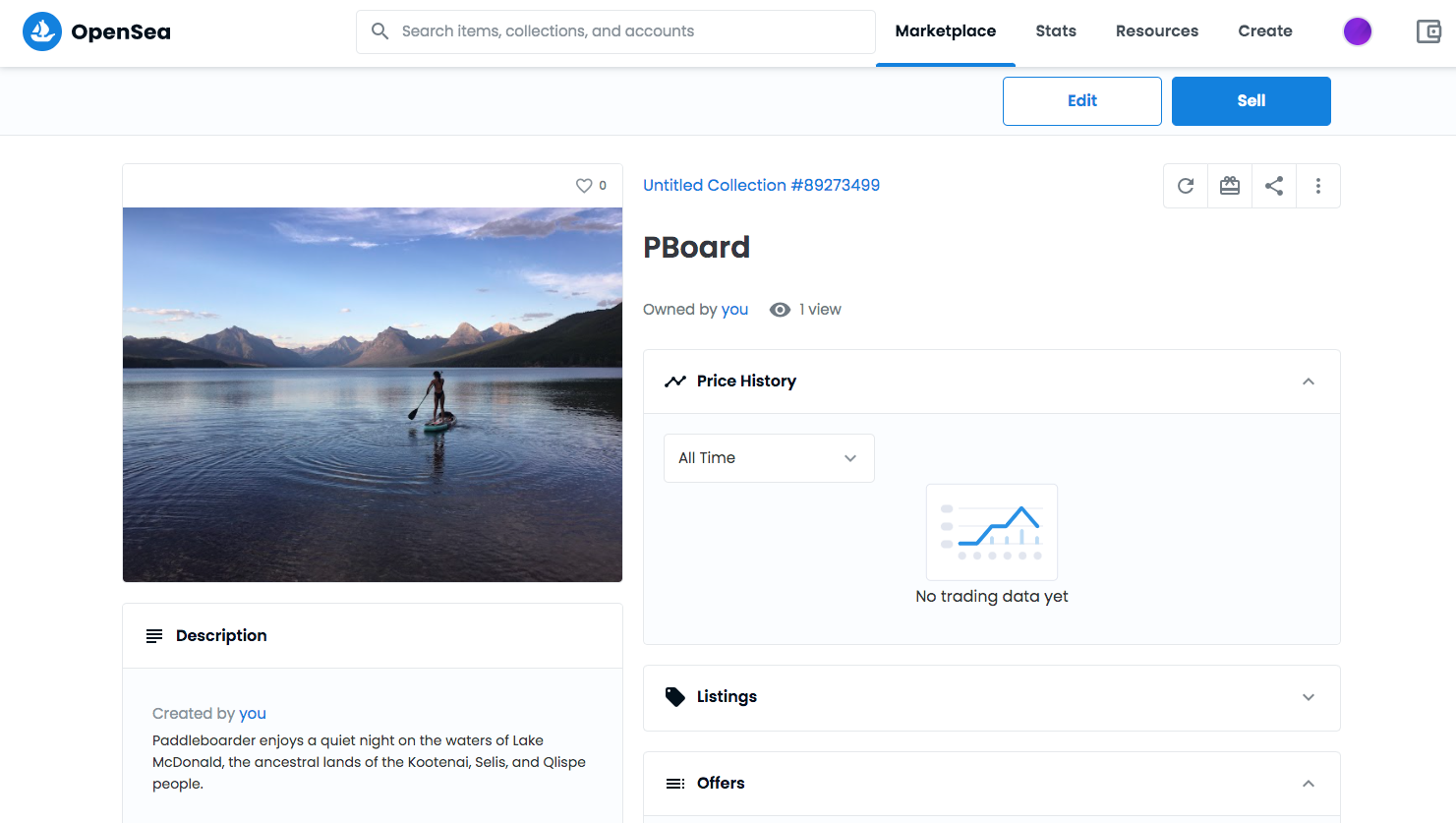

Non-fungible tokens, better known as NFTs, have been making their way into mainstream culture this year. From “breeding” digital kitties to collecting NBA trading cards, the possibilities of buying and selling digital media are endless.

If you’re NFT-curious, one of the best ways to discover more is to create or purchase your very own NFT. If you already have a crypto wallet, it is fairly simple. Create your own by uploading a photo to OpenSea or check out the OpenSea marketplace to browse media. It only took me around five minutes to create my first NFT:

As a quick-fire way to help you sort the ins and outs of NFT trading, here’s a quick list of seven things you need to know about the NFT craze.

1. NFTs are not just for fintech nerds

The fact that NFTs leverage the Ethereum blockchain doesn’t scare off creators nor buyers. Multiple marketplaces, including the aforementioned OpenSea, Binance, and Rarible make it very simple to upload, buy, and sell NFTs. As Time reports, teenagers as young as 15 are already making millions of dollars by creating, buying, and selling NFTs.

2. NFTs are good for creators

Instead of sacrificing commissions to art houses, publishing companies, and other middlemen, creators can keep the majority of the purchase price for their work. OpenSea, for example, charges only a 2.5% fee. Additionally, some NFTs enable the artist to receive a royalty payment each time the NFT is sold or changes hands.

3. NFTs benefit buyers

The value of buying and owning NFTs is a bit less clear than the value for creators. Aside from exercising bragging rights, NFT owners can use the NFT as a speculative tool by buying and selling NFTs, or they could use their purchase as a way to more directly follow and support artists.

4. Anyone can create an NFT

As long as a user has a crypto wallet and is able to upload media, they can create their own NFT. My NFT is proof of this– while I am certainly not an artist (I failed art in the fifth grade), I was able to upload a photo I already had to quickly create my own.

5. NFTs are one-of-a-kind

As the name suggests, NFTs are non-fungible, meaning they cannot be exchanged with assets of the same type. In other words, unlike currency which can generally be exchanged one-for-one (I can pay you a dollar for your dollar), each NFT is completely unique.

6. Yes, NFTs can be copied or downloaded

Because NFTs are digital media, they can easily be reproduced. Anyone can take a screenshot of an original NFT or download a copy of a video. The value, however, is in owning the original NFT. As an example, there are many copies of Van Gogh’s Starry Night, but none are as valuable as the original.

7. NFTs can potentially bridge the digital/ physical divide

While NFTs are restricted to digital assets, it is possible to use NFTs as a type of verification method for the purchase of an original, physical item. For example, Nike has patented a way for sneaker collectors to track ownership and verify the authenticity of sneakers.

Behavioral biometrics innovator BioCatchlaunched its latest fraud-fighting solution this week. Age Analysis is a new account opening protection capability especially designed to help protect older consumers from fraud and other forms of cybercrime.

“We developed Age Analysis with enhancing customer protection and user experience as our guiding principles,” BioCatch Chief Operating Officer Gadi Mazor explained. “At BioCatch, we work closely with our clients to develop the most forward-thinking behavioral solutions to solve the ever-evolving challenges in combating fraud. Age Analysis empowers financial institutions with the behavioral verification protections most needed to address the growing threat of application fraud.”

The new offering, currently deployed by a number of international organizations as well as a “major credit card issuer,” was developed after noting that 40% of confirmed fraudulent credit card applications involved an applicant above the age of 60. BioCatch also discovered that a significant number of these applications ended up in manual review, increasing both the time spent processing the application as well as diminishing the user experience for older applicants.

Age Analysis works by extracting physical, cognitive, and other behavioral characteristics as the user engages in the account opening process. The technology monitors the activity continuously, predicting what BioCatch refers to as the user’s “approximate behavioral age” and compares it to the applicant’s declared age. If there are significant differences between the two, BioCatch adjusts the user’s risk score to reflect the anomaly.

The technology is based on the finding that certain behavioral characteristics involved in data input tend to change as individuals age. These include factors such as mouse click duration, mobile device orientation preferences, and even actions as specific as the time it takes for a user to shift from the CTRL key to a letter key when inputing data. Learn more about how Age Analysis works, and how it has helped increase company’s ability to detect account opening fraud and boost ROI, in BioCatch’s case study, Top Card Issuers Partner with BioCatch to Protect Senior Citizens from Fraud and Saving Millions.

A Finovate alum since its debut at FinovateFall 2014, BioCatch was founded in 2011 by Avi Turgemen, Benny Rosenbaum, and Uri Rivner to leverage insights derived from Turgemen’s experience in military intelligence to fight online fraud and other cybercrime. Most recently, the company announced joining Alkami Technology’s Gold Partner Program to bring its behavioral biometric technology to Alkami’s bank and credit union customers. In August, BioCatch teamed up with digital financial solution provider MoData to help the company’s clients in Africa better defend themselves against online fraud.

BioCatch has raised more than $213 million in funding from investors including Barclays and HSBC. The company has offices in both New York City and Tel Aviv, Israel.