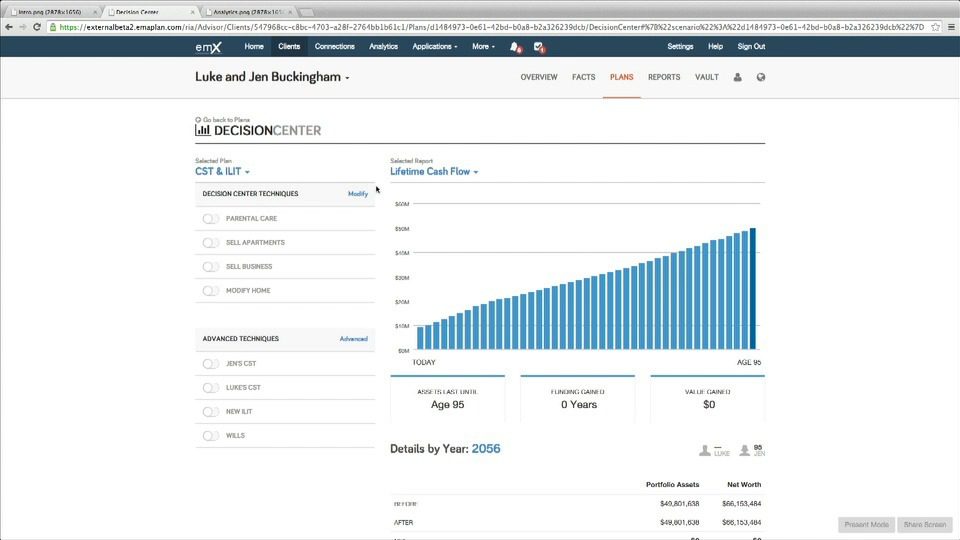

How they describe themselves: eMoney Advisor, based in Conshohocken, PA, is the leading wealth-planning system for financial advisors. A technology envisioned and created by advisors for advisors, eMoney’s award-winning “software” is bigger than the term suggests — it’s a way of doing business. Tailored to transform an advisor’s ability to deliver expertise, eMoney is the silent partner in the practice of more than 20,000 of the industry’s top financial professionals, helping them leverage technology to gain new assets, strengthen client relationships, and compete on a whole new level. Driven to lead through innovation, eMoney is committed to positioning its advisors for greater success.

How they describe their product/innovation: Smarter, faster, friendly, and easier to use, EMX is the next generation of the eMoney Advisor experience. While we’ve always led the pack in financial planning, we’ve stepped up our game, creating a platform for an unparalleled interactive experience for advisors and their clients, improving efficiency with new integrations and better connections. And with robust analytics and a more intuitive interface, EMX empowers our advisors to maximize the potential of their book of business. Learning from over 14 years of experience and feedback from more than 20,000 advisors, with EMX, we’ve built the ultimate wealth-management solution that will redefine success in an advisor’s business.

Product distribution strategy: Direct to Business (B2B), through financial institutions, licensed

Contacts:

Bus. Dev.: Kyle, Wharton, Bus. Dev. Director, [email protected]

Press: Kelly Waltrich, Communications Director, [email protected]

Sales: Drew DiMarino, SVP Sales, [email protected]

How they describe themselves: At HedgeCoVest, we believe the next generation of alternative investments has arrived. HedgeCoVest has created an online marketplace for today’s investors who are searching for smarter, more transparent, and secure options to allocate to hedge funds. Through our technology, we are able to offer clients the benefits of traditional hedge fund investments, without many of the risks associated with commingled investments. Our solution is designed to put our clients in control of their assets and investments and lower minimum investment requirements with simple flat fees.

How they describe their product/innovation: HedgeCoVest is an investment tool allowing you to mirror hedge fund investments in your own brokerage account. Using HedgeCoVest, you can research hedge funds, their risk/return profile, management team and more. Then, when you find a fund to mirror, you can allocate with the click of a button. Our proprietary trading technology, the Replicazor, sees hedge fund portfolios and duplicates them in your account in real time. Anytime your chosen fund makes a trade, the Replicazor will make a corresponding trade for you within milliseconds. No guesswork, no investing based on outdated reports. One-to-one tracking of real hedge funds.

Product distribution strategy: Direct to Consumer (B2C), Direct to Business (B2B), through financial institutions, through other fintech companies and platforms, licensed

Contacts:

Bus. Dev. & Sales: Alex Smith-Ryland, 561-835-8690

Press: David Schroeder, 561-835-8690

How they describe themselves: Fiserv (NASDAQ: FISV) is a leading global provider of information management and electronic commerce systems for the financial services industry, providing integrated technology and services that create value and results for our clients. Fiserv drives innovations that transform experiences for more than 14,500 clients worldwide.

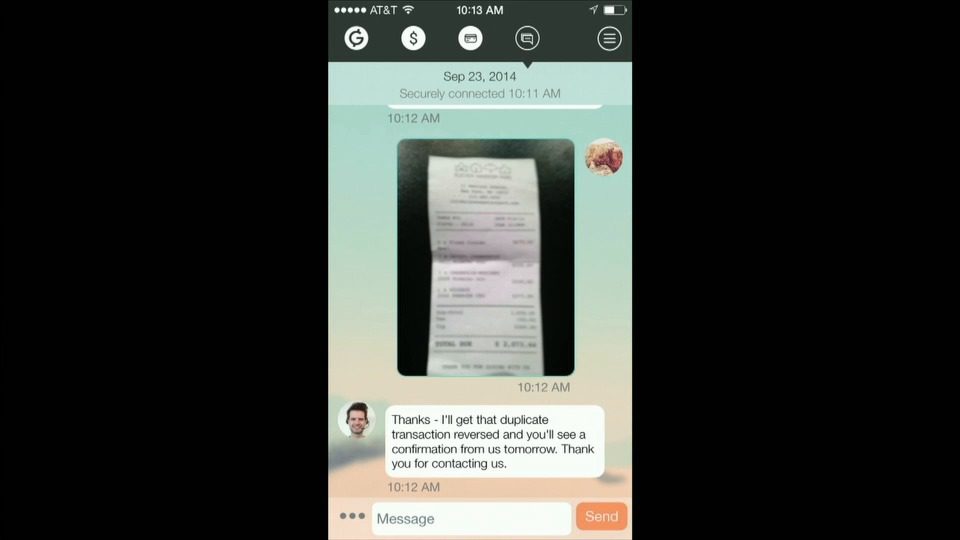

How they describe their product/innovation: Fiserv is demonstrating what next generation customer-to-bank interactions will look like, particularly in a mobile-first world. The ‘App of the Future’ innovation based on the Mobiliti™ platform assembles three distinct consumer interaction methods – Live Chat, Secure Mailbox & Messaging, and Click-to-Call – and makes them contextual (i.e. providing context information to the representative of the bank as part of the interaction). All inside the mobile banking application.

This innovation has a number of benefits to consumers and financial institutions, including: increased efficiencies of interactions, more secure than various existing authentication methods, and portrays the banks’ brand as helpful, modern, and compelling.

Product distribution strategy: Direct to Business (B2B), through financial institutions

Contacts:

Bus. Dev.: Kelly Rodriguez, VP Strategy & Bus. Dev., [email protected], 678-375-1095

Press: Ann Cave, PR Director, [email protected]

Sales: Joe Christenson, VP Sales Mobile Solutions, [email protected], 210-378-0893

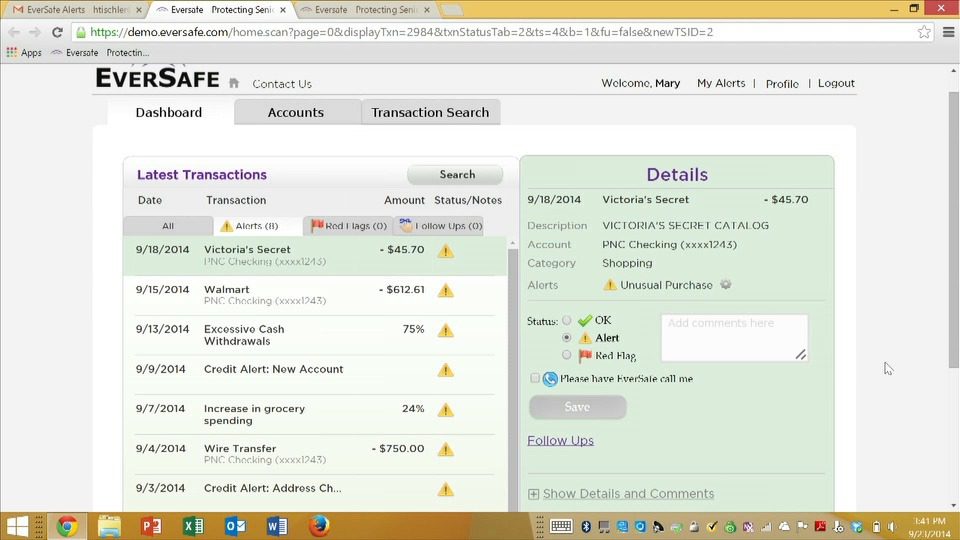

How they describe themselves: The financial abuse of older Americans is a growing epidemic costing seniors billions of dollars annually. EverSafe is the first technology-based solution to address this challenging problem. Founded by financial services and credit management industry veteran Howard Tischler — whose mother was a victim of elder financial abuse — EverSafe scans financial accounts, credit cards, and credit report activity daily, alerting members of suspicious activity. A proactive financial defense network, EverSafe protects seniors against financial abuse.

How they describe their product/innovation: EverSafe applies technology to combat elder financial exploitation. The service reviews the senior’s financial transactions and credit report activity daily and if suspicious activity is detected, an alert is sent immediately. EverSafe’s sophisticated software employs a set of rules developed specifically for seniors to comb every transaction looking for abnormalities, including unexpected patterns in spending, deposits, and withdrawals. If suspicious activity is confirmed, the resolution process begins. EverSafe tracks the remediation plan and sends follow ups to help curtail further financial exposure.

Product distribution strategy: Direct to Consumer (B2C), through financial institutions

Contacts:

Bus. Dev. & Sales: Howard L. Tischler, Founder & CEO, [email protected],

410-343-9674

Press: Christopher Grover, VP Marketing, [email protected], 301-482-0277

How they describe themselves: Founded in 2006, Geezeo is a leading Personal Financial Management (PFM) solutions provider for financial institutions. We help banks and credit unions engage their base, leverage data, reach new market segments, and increase wallet share though our PFM solution and integrated Engagement Banking Marketing Platform. Our API takes this a step further, and allows best-in-class service providers to leverage the features and benefits of PFM via just about any channel. We’re excited to take what we learned from the consumer PFM market and apply our knowledge in a way that FIs can better support the needs of small and mid-size businesses.

How they describe their product/innovation: Small and middle market businesses represent critical markets for FIs. TruBusiness is a white label business financial management tool that helps FIs better engage the market. At the same time, the tool offers robust online financial management to business banking clients, offering business customers and FIs predictive insight and capability beyond the expected.

Product distribution strategy: Like all Geezeo products, we expect our business financial management solution will be offered to financial institutions directly and via channel partners through other fintech companies with a keen interest in the small to mid-size business banking market.

Contacts:

Bus. Dev.: Pete Glyman, President, 866-876-3654

Press: Bryan Clagett, CMO, 757-243-3453

Sales: Steve Nigri, VP, 866-876-3654

How they describe themselves: EyeLock, a leader in iris authentication, provides the highest level of security with EyeLock ID. The company’s proprietary, embeddable technology enables convenient, secure authentication of individuals across physical and logical environments. EyeLock’s software has been integrated across consumer and enterprise platforms, eliminating the need for PINs and passwords. No two irises are alike, and outside DNA, iris is the most accurate human identifier. Corporations across the Fortune 500 recognize the level of security EyeLock provides due to its FAR, ease of use, and scalability. As a sponsor member of the FIDO Alliance, EyeLock is dedicated to providing digital privacy security.

How they describe their product/innovation: Never type a password again— myris is a USB powered Iris Identity Authenticator that grants you access to your digital world.

myris uses patented technology to convert your individual iris characteristics to a code unique only to you, then matches your encrypted code to grant access to your PCs, e-commerce sites, applications, and data – all in less than 1 second.

Product distribution strategy: Direct to Consumer (B2C), Direct to Business (B2B), through other fintech companies and platforms

Contacts:

Bus. Dev.: Anthony Antolino, CMO & Bus. Dev., [email protected]

Press: Jeanne Templeton, Weber Shandwick, [email protected]

Sales: Darlene Crumbaugh, VP Financial Services, [email protected]

How they describe themselves: GREMLN provides software for social media management within the financial services industry. With features such as message archiving, team supervision, message approval, and content filtering, GREMLN enables financial services companies to communicate in networks like Facebook, Twitter, and LinkedIn. Financial firms need much more than just a security tool, however; they need integrated marketing and customer service tools to help them better engage with customers, reach new clients, and track their return on investment. GREMLN provides this additional functionality, making it a full social media marketing, engagement, and customer service tool, wrapped in a security blanket to help maintain compliance with government regulations.

How they describe their product/innovation: GREMLN is demonstrating its latest social media compliance features. Pre-approved Content Libraries enable firms to provide great content to their teams that can circumvent the message approval process. LinkedIn Lead Prospecting enables financial advisors and other employees to find new clients via LinkedIn. And finally, GREMLN is launching a new mobile platform that enables marketing and compliance departments to stay engaged in social media and handle approval processes right from their phone or tablet.

Product distribution strategy: Direct to Business (B2B)

Contacts:

Bus. Dev./ Sales: TJ Tavares, VP Sales 314-492-6445

Press: David Bell, CMO 314-915-8738

How they describe themselves: Financeit is a platform that makes it easy for businesses of any size to boost their sales by offering payment plans to their customers. The company brings point of sale consumer financing tools to main street merchants to increase close rates and transaction size.

How they describe their product/innovation: Financeit, in partnership with FIS, is announcing the launch of and showcasing a USA-compliant platform. Their Finovate demo shows all of the components required to ensure processes are compliant while still providing end users with an amazing product.

Product distribution strategy: B2B Marketing, Sales and Partnerships

Contacts:

Bus. Dev.: Casper Wong, COO, [email protected]

Press: Braden Rosner, PR & Communications Manager, [email protected]

Sales: Craig Haynes, VP Sales, [email protected]

How they describe themselves: Created by two financial advisors, FlexScore is a web-based platform that “gamifies” financial planning by giving you a score based on your overall economic health. After aggregating your financial data, FlexScore assigns you a score and provides a list of recommended Action Steps to improve your financial wellbeing. Each time you complete an Action Step, you earn points as your FlexScore gets ever closer to a perfect 1000, which represents financial independence. FlexScore makes financial planning easy, objective, and even fun. Financial institutions love our digital platform for its ability to engage customers in a unique and profitable way.

How they describe their product/innovation: FlexScore is now available in a mobile version, allowing users to take FlexScore with them wherever they go. FlexScore maintains its core features – the scoring engine, the Action Steps, the Peer Ranking feature – while empowering the user further through our new pocket-sized, accessible format. Just as with our desktop version, the user interface is spacious, simple, and easy to understand, all while retaining the full power of automated financial advice.

Product distribution strategy: Direct to Consumer (B2C), Direct to Business (B2B), through financial institutions

Contacts:

Bus. Dev., Press & Sales: Jason Gordo, CEO, [email protected], 415-967-1173

How they describe themselves: Hoyos Labs is a digital infrastructure security company with security, computer vision, and biometrics and big data experts. The goal of Hoyos Labs is developing and deploying enterprise and consumer identity assertion technology platforms that will conveniently and securely address the identity assertion challenges of today. Hoyos Labs currently has offices in New York, Boston, Bucharest, Beijing, Oxford, and Puerto Rico.

How they describe their product/innovation: Our mobile app is finally putting an end to the frustration that comes with usernames, passwords, and PINS. This app leverages a user’s smartphone to acquire his or her biometrics, which conveniently and securely replaces log-in information for all their favorite websites.

The app acquires various biometrics, including facial, periocular, fingerprint, and iris. Additionally, the app utilizes a unique, state-of-the-art “liveness” detection system that is capable of distinguishing a real person from an image or video in order to authenticate your identity and log you into sites, from social media to your online banking account and beyond.

Product distribution strategy: Direct to Consumer (B2C), Direct to Business (B2B), through financial institutions, through other fintech companies and platforms, licensed

Contacts:

Bus. Dev. & Sales: Vincent Endres, [email protected]

Press: Caitlin Kasunich, Senior Account Executive, [email protected], 212-896-1241

How they describe themselves: Businesses of all sizes choose e-SignLive™ by Silanis when e-signatures matter. Thousands of organizations, including the leading banks, credit providers, insurers, and government agencies trust e-SignLive™ as their electronic signature platform.

How they describe their product/innovation: The e-SignLive™ Use Your Own Device (UYOD) capability solves a fundamental problem in financial services and banking: how to capture a customer’s handwritten signature electronically, without asking the customer to come into the branch. This innovation enables the customer’s smartphone or tablet to be used as a signature capture device. It does not require an app or any in-branch hardware. Banks can now make remote customer onboarding convenient and secure with any smartphone.

Product distribution strategy: Direct to Business (B2B), via fintech companies and platforms

Contacts:

Bus. Dev. & Sales: Ilene Vogt, SVP Sales & Marketing, [email protected]

(o) 310-937-9853, (m) 310-710-6465

Press: Sarah Milner, PR Relations & Social Media Manager, [email protected]

250-216-1762

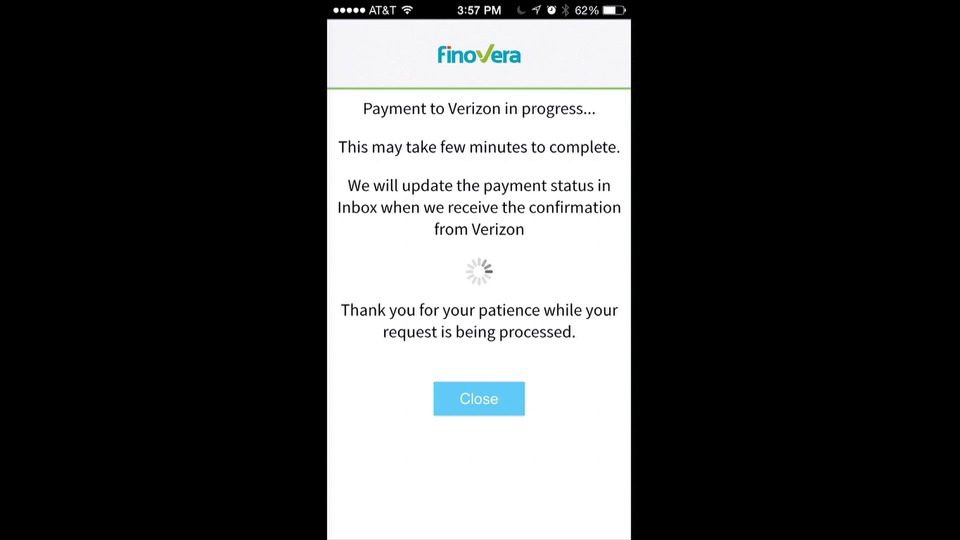

How they describe themselves: Finovera is redefining how people receive and pay bills and manage their finances online and on mobile. Online Bill Pay growth is flat and the eBill view is disappointing in its current state. However, research has shown that eBill users are nearly 40% less likely to switch their bank and are worth 25% more than just the bill pay customers. Finovera helps banks and credit unions to build a loyal customer base by bringing simplicity, efficiency, and convenience to household bill and account management. Now consumers can say goodbye to late fees, forgotten passwords, and a disorganized bill pile.

How they describe their product/innovation: Imagine Bill Management the way you have always dreamed it could be: simple, attractive, convenient, and mobile. Imagine all your bills automatically delivered to you every month in a neatly organized Inbox on your bank site so you can pay them with the click of a button effortlessly from your checking account or on the biller site with a credit card. Now if you are a banker, imagine being able to transform your bank site into a customer’s Financial Hub that lowers attrition, increases revenue, and reduces cost.

Product distribution strategy: Direct to Business (B2B), through financial institutions, through other fintech companies and platforms, licensed

Contacts:

Bus. Dev.: Purna Pareek, CEO, [email protected]

Press & Sales: Amanda Zepeda, Marketing Manager, [email protected]