This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

As Finovate events return this fall, dozens of companies are getting ready to showcase their latest financial services technologies this September and November. And not surprisingly, many of these innovations are part of larger stories related to COVID-19.

As a sneak peek, we recorded an early digital demo interview with WealthConductor, who will also demo at FinovateWest. Along with Finovate VP of Strategy, Greg Palmer, WealthConductor explores the retirement income crisis, now more dire than ever when unemployment is at an all-time high.

To join WealthConductor and other companies demoing this fall, visit the FinovateFall and FinovateWest (formerly FinovateSpring) websites. Hope to see you apply!

Wealthfront has been around the proverbial fintech block a few times. The San Francisco-based wealthtech company launched near the dawn of fintech under the name KaChing in 2008 and demoed its investment platform at the second-ever Finovate conference in 2009.

Given its time in the space, Wealthfront is well-positioned during this pandemic. The legacy fintech benefits from a strong customer base, name recognition, and profitability. So when the pandemic hit and many firms were struggling with customer service or the transition of working from home, Wealthfront didn’t miss a beat.

Its secret weapon? Scalability. As Wealthfront’s client base has grown to almost 400,000 users, the company has relied on automation to ensure a high-quality customer experience. “Automation has been a key product principle at Wealthfront from day one,” said Wealthfront Founder and Chief Strategy Officer Dan Carroll in a blog post. “If we can’t automate a service, we won’t build it. When a client needs to email or call us, we consider that a failure in our product and work to build an automated solution.”

Instead of customer service representatives, Wealthfront refers to its team members as Product Specialists. The 12-person team is comprised of licensed financial advisors who are each responsible for fielding client questions and tracking and relaying customer feedback to the company’s product development team. Using these techniques, Wealthfront has been able to scale to 30,000 clients per specialist.

And while some banks were closing down call centers and struggling with customer hold times ranging from 30 minutes to three hours, Wealthfront’s team of 12 Product Specialists weren’t overburdened. To get ahead of the projected spike in client inquiries, the team moved to individual remote work settings and composed a list of questions they anticipated from customers. With the help of the company’s content team, the specialists deployed in-app pop-ups that offered answers to potential questions and provided advice to help clients navigate volatile markets and the CARES Act.

So what’s next for Wealthfront? “While banks grapple with something as basic as streamlining customer service, we’re working on the future of financial services — something we call Self-Driving Money,” Carroll said. The new product will automate users’ recurring transactions including billpay, savings, and goals. “Our ultimate vision is to optimize your money across spending, savings, and investments, putting it all to work effortlessly.”

If you’re trying to launch a successful global currency, getting the brand name right is key. That must be what Facebook was thinking this week when it changed the name of the digital wallet for Libra, its new global cryptocurrency payment project.

The new name of the wallet, Novi, was rebranded from Calibra. While Facebook did not say what prompted the name change, TechCrunch speculated in its piece that, ” By rebranding Calibra to Novi, Facebook is trying to make it super clear that the Libra project isn’t a Facebook project per se. Facebook is just a member of the Libra Association with dozens of other members, such as Andreessen Horowitz, Coinbase, Iliad, Lyft, Shopify, Spotify, Uber, etc.”

However, the new Novi brand has not completely left Libra out of its new look. The wallet incorporated the three waves of Calibra’s logo into the design of its new logo. The Facebook subsidiary said it did so, “to underscore our commitment to the Libra network.”

The Novi wallet, which was named as a combination of the words “novus via” (Latin for “new way”), will offer a standalone app for instant cryptocurrency transfers. Users will also be able to transfer funds via Facebook Messenger and WhatsApp.

As of now, there is no word on the fee structure. However, Novi said in its announcement that there will be no “hidden” fees for money transfers, indicating that the wallet will be transparent about the pricing. Novi is aiming to launch in a limited number of countries when the Libra network is available.

It’s a good time to launch a digital wallet. With consumers all across the globe eschewing cash for digital payments in order to be more conscious about transfering the coronavirus, there is likely to be higher demand for digital payment technologies. That said, mainstream consumers have been notoriously wary of cryptocurrencies, so they may opt for tap-to-pay or QR code payment methods before they are willing to use a cryptocurrency.

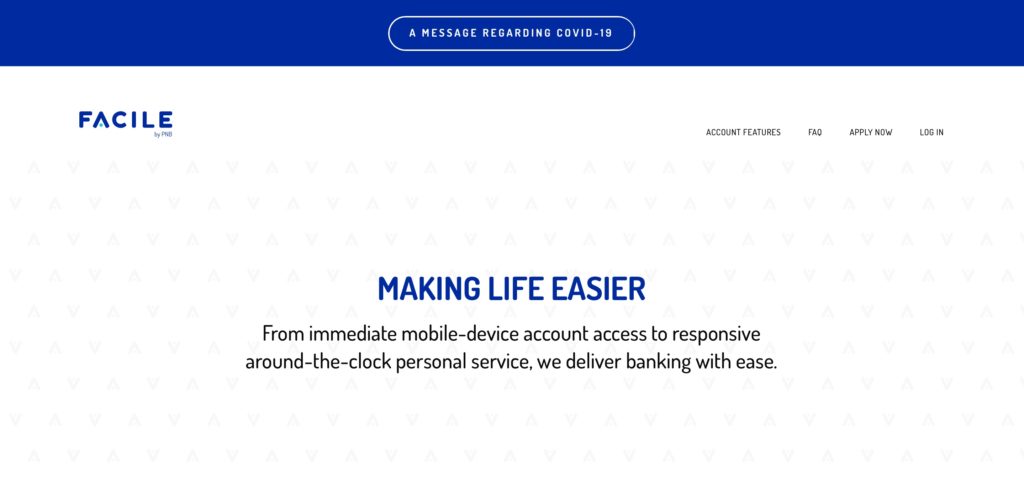

Cloud banking platform provider NYMBUS, which demonstrated its SmartLaunch banking-as-a-service solution at FinovateFall last year, has partnered with Pacific National Bank (PNB) to help the Florida-based company launch a digital-only bank, FACILE.

“We knew we had to act fast to meet the rising consumer demand for digital banking services,” Pacific National Bank CEO Carlos Fernandez-Guzman said. “Only NYMBUS could immediately offer us a proven, unified solution that delivers on-demand access to their wide-range of digital-first technology products combined with a 24/7/365 live call center and remote business process management support.”

The new offering from Pacific National Bank, an institution with more than $656 million in assets, is designed to provide on the kind of online and mobile banking services that young professionals increasingly demand. FACILE will offer both digital checking and savings accounts on a fee-free basis. Accountholders can make mobile transfers and payments, take advantage of personal financial management tools and resources, and access a network of fee-free ATMs. The account also comes with a debit card that features card controls for both better security and keeping spending at a manageable level.

Headquartered in Miami Beach, Florida and founded in 2015 by Scott Killoh, NYMBUS has raised more than $33 million in funding. The company began the year teaming up with PeoplesBank, a Massachusetts-based financial institution with assets of more than $2.9 billion, that deployed both NYMBUS’ SmartMarketing and SmartOnboarding solutions. “NYMBUS will integrate key aspects of our marketing, onboarding, and CRM ecosystems,” PeoplesBank president and CEO Tom Senecal said. “Together with instant end-to-end reporting that crosses business lines, we will ultimately be setup to strategically course correct future spending for even greater outcomes.”

Finovate Podcast Interviews Steve McLaughlin of FT Partners

In the latest edition of the Finovate Podcast, host Greg Palmer catches up with Steve McLaughlin, founder, CEO, and managing partner at Financial Technology Partners. Launched in 2001, FT Partners, as it is known, is the only investment banking firm dedicated solely to fintech. The company has been recognized by the M&A Advisor as “Dealmaker of the Year” and “Investment Banking Firm of the Year.”

Greg and Steve talk about the fintech industry from the perspective of an investment banker. They discuss the issue of capital availability, company valuation, and the idea of a harsher grading rubric for fintech.

Here is the latest news from our Finovate alums:

ThetaRaylaunches FAST START to help banks fight cybercrime during Covid-19.

Capita Consulting leverages low-code technology from Outsystems.

Minna Technologieslaunches pilot with Tatra banka in Slovakia.

SaltEdge’s new solution helps banks get exempted by the regulator from providing a fallback channel.

Token.io’s payments API to power open banking payment services for Upco’s Mobile Messenger.

DriveWealth to integrate with Access Softek’s new investing app, EasyVest.

ACI Worldwide to provide e-commerce payment processing for retail payments platform, Wundr.

Payment processor Trustlyteams up with Ecommpay to offer three months of free processing.

Finastralaunches its Fusion Credit Connect solution on Salesforce AppExchange, FusionFabric.Cloud.

Bokupowers direct carrier billing and e-wallet payment services for Korean game developer Pearl Abyss Corporation.

MXlaunchesAudiences, a new segment builder tool to help banks improve marketing efforts.

ID R&DreleasesIDFraud Contact Center to address subscription fraud in the contact center.

DriveWealth to bring U.S. stock investing to India-based INDmoney clients.

Coinbaseplans to be a “remote-first” company after COVID-19.

Ethoca and Mastercardpartner to help retailers deal with chargebacks and fraud during the COVID-19 crisis.

Kabbagereceives SBA approval to fund PPP applications totaling more than $3.5 billion.

FISlaunchesiQ Now, a mobile app for SMEs that enables owners to monitor real-time business performance.

WorldRemit teams up with Onfido to enhance the identity verification component of its onboarding processes.

iProov to bring its biometric authentication technology to the U.K.’s National Health Service (NHS).

Xeropartners with online small business bank Relay to offer real-time visibility of cash flow.

Finovate Alum Features and Profiles

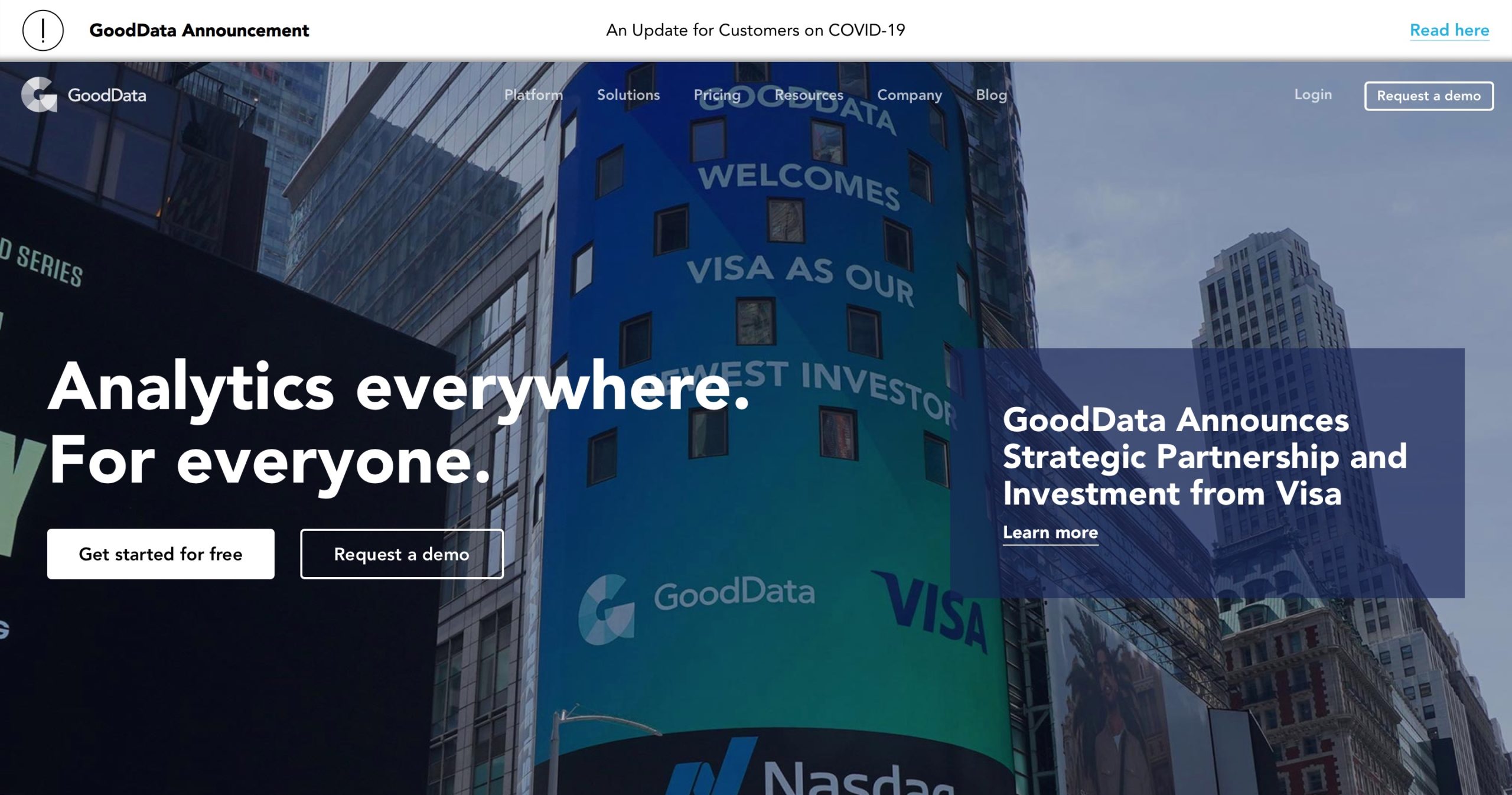

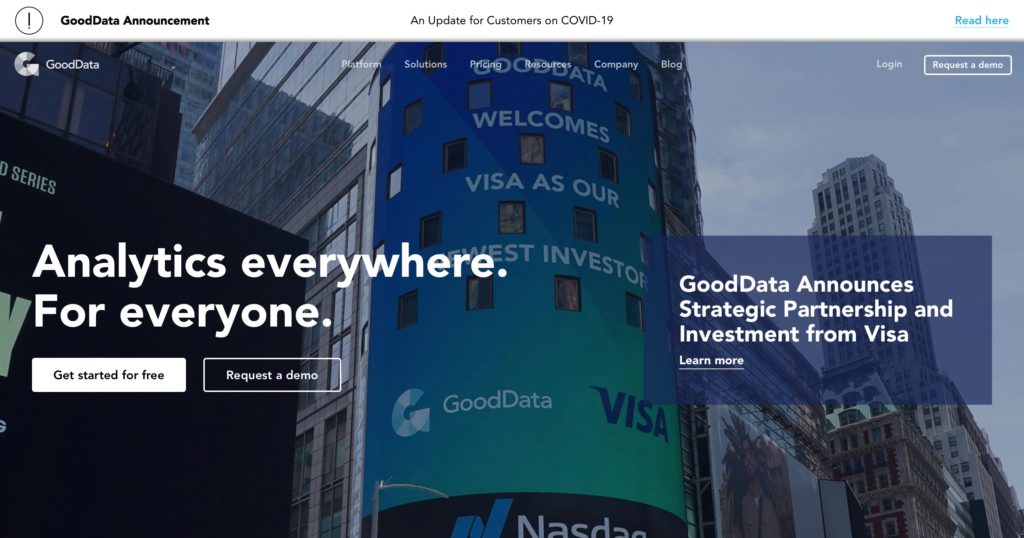

Visa Backs GoodData in New Strategic Partnership and Investment – The collaboration includes an investment in the global analytics company and is designed to enable Visa to offer its customers and partners better access to aggregated data and analytics.

Plaid Exchange Offers Open Banking in a Box – The new tool, Plaid Exchange, offers banks a way to provide open banking connectivity to their clients while keeping their clients’ data safe and giving them control of their data.

China is dominating geopolitical headlines – from the country’s unique challenge with COVID-19 to tensions with Hong Kong and the United States as Chinese leaders gather for the country’s annual National People’s Congress.

But fintech observers would do well to consider developments in China’s neighbor to the southwest, India, whose fintech sector continues to challenge China’s in terms of investment.

In the first quarter of 2020, fintech investment in India again outpaced fintech investment in China. GlobalData, a data and analytics company, released an analysis this week that showed Q1 2020 fintech investment in China came in at “approximately $270 million” while, in India, fintech investment in the first quarter of this year topped $330 million. GlobalData analyst Ayushi Tandon noted that the global pandemic had played a role in dampening VC enthusiasm for fintech investment overall this year so far, and that India had benefitted on a relative basis from this easing of investor passions.

Deal volume showed the same preferences in the first quarter, with 26 deals closed in China in Q1 compared to 37 deals in India.

VC investment in the two countries differed in terms of startup maturity and sub-sector, as well. In China, there has been more investment in cross-sector fintech startups that were looking to scale. In India, payments and lending were the top sectors, and seed funding dominated the quarter’s investments. GlobalData’s report noted that fintechs involved in analytics were the biggest recipients of VC funding in both nations.

India’s fintech industry certainly had the wind in its sails coming into this year. According to research from Accenture, investment in Indian fintechs grew from $1.9 billion over 193 deals in 2018 to $3.7 billion over 198 deals in 2019. The country began to successfully compete with China in terms of fintech investment last year.

Founded in 2016 and headquartered in London, U.K., GlobalData was formed by a consortium of established data and analytics providers. Covering a wide range of industries – from banking and payments to insurance, aerospace, and technology – GlobalData serves financial institutions, government agencies, and corporations, providing thought leadership and analysis, as well as proprietary analytic frameworks to help them make data-driven decisions.

Here is our weekly look at fintech around the world.

Middle East and Northern Africa

NEC Payments and stc Bahrain, a telecommunications company based in Bahrain, partner to launch new virtual prepaid Mastercard offering.

JinglePay, neobank based in Dubai, announces plans for launch.

Emirates NBD collaborates with proptech startup Urban to offer financing program for property rentals in UAE.

Central and Southern Asia

Lendingkart, an online lender based in India, raised more than $42 million in Series D funding.

Indian SME accounting app Khatabook raises $60 million in Series C funding.

SadaPay, a fintech based in Pakistan, wins approval to launch a mobile wallet.

Latin America and the Caribbean

Brazil unveils new regulations enabling banks, payments institutions, and other licensed companies to share customer data.

Koibanx, a fintech based in Argentina, announces plans to expand to Mexico.

Colombian lender ADDI raises $15 million in round led by Quona Capital.

Asia-Pacific

Philippines-based mobile wallet GCash to support cashless payments system for taxi service in Manila.

Samsung Pay and Malaysia-based e-wallet Boost team up to support cashless payments in Malaysia.

Ant Financial invests $73.5 million in mobile financial services company Wave Money.

Sub-Saharan Africa

South African business payments platform Peach Payments locks in growth funding with investment round led by UW Ventures.

Nigerian fintech Carbon goes live with new social banking service.

CompariSure, a fintech startup from South Africa, raises funding from UW Ventures.

Central and Eastern Europe

Billon partners with Austria’s Raiffeisen Bank International (RBI) to pilot a DLT-based national currency.

EU Startups features CEE fintechs Crypterium, Humaniq, Revolut, and ANNA in its list of promising startups with Russian founders.

Financier Worldwide looks at AML and financial crime in Romania.

With the coronavirus keeping drivers off the road, there has been a lot of discussion surrounding auto insurance. In fact, many providers have recognized the decreased daily mileage (and the increased need for cash) during this time, and responded by offering rebates and credits to consumers in return.

Because of this, the pay-by-mile insurance model is looking more sensible than ever. This is likely what CommerzVentures was thinking when it led By Mile’s $18.3 million (£15 million) round of funding. Existing investors Octopus Ventures, Insurtech Gateway, and JamJar also participated.

“This crisis has shown U.K. drivers what we’ve known for a while: the way car insurance works now isn’t working for everyone,” said ByMiles CEO and CoFounder James Blackham. “Our pay-by-mile car insurance provides lower mileage drivers with a flexible, lower cost policy that drivers can track in real-time.”

Launched in 2016, By Miles offers U.K. residents a new alternative for car insurance in which drivers only pay for the miles that they drive. The company offers two options, both aimed at users that drive less than 7,000 miles per year. The Standard option uses a Miles Tracker device, a black box that plugs into a car’s dashboard. The telematics device uses mileage data from the user’s car to help price their insurance. The device does not use other data, such as speed, to price the insurance. Newer cars can use By Miles’ Trackerless option that pull mileage data directly from the connected cars’ manufacturer.

ByMiles is already seeing growth thanks to the global pandemic. The company experienced its strongest sales in April.

For every conversation about AI that begins with insects, moves quickly through primates, and then launches into the stratosphere of high-minded conceptions of superintelligence, talk about artificial intelligence among executives and entrepreneurs in the financial services and fintech world is far more grounded.

“Technology is a tool to support the business, not a toy to engage and have fun in excellence centers,” she announced early in her address to our FinovateEurope audience. “Technology in our industry is a serious tool. (Technology) needs to follow business strategy, not the other way around.” She likened the responsibility to use technology ethically and with purpose to the responsibility of earning a license to drive. Durodié made it clear that, like a driver and a passenger sitting side by side in a moving vehicle, both technology creators and technology users stand to benefit from a commitment to responsible behavior.

Businesses that embrace a more ethical approach to technology – especially a technology as powerful as AI – are also those that are most likely and able to transition away from what Durodié has called a “product-centric” today to a “customer-centric” tomorrow. She has pointed out that AI can be a powerful tool for personalization in business contexts, while simultaneously enabling companies to move to a qualitatively and quantitatively new level in terms of automated business processes.

“The work we do is around deployment of ethnical AI for business growth and profitability.”

Who makes sure this happens? While the immediate onus is clearly on the business leader, CEO, or founder, Durodié emphasized that much of the business’ leadership will – or should – come from its board of directors, particularly in high-level areas like corporate governance, business strategy, and fiduciary responsibility, where ethical guidance is paramount. “This is challenge number one,” she said of startups and their relationship with their board of directors.

And not just any board of directors. Durodié referenced a study from MIT that indicated that simply having one individual with a “technology” background on a board of directors improved the likelihood that the company working with that board would yield 38% return on assets on a yearly basis. “And if you compound that every year,” Durodié added, “you can see why the people who actually do things right from the beginning will be ahead of the game.”

For Durodié, the conversation on governance is intimately linked (“married forever”) with the conversation on ethics, and it is important that companies develop processes and systems that are “explainable, auditable, and accountable.” This is especially important when the data involved is financial data, and when the technologies to be deployed against this data are as powerful as AI.

“Financial data on our customers is highly sensitive. And we need to treat it as such and protect it as such,” Durodié said. She noted that the companies that will succeed in effectively deploying AI will understand this challenge, and have the moral compass to build tools that are “robust and helpful.” “Algorithms have parents,” she noted. “Every bias, every conditioning we have, comes through the way we generate the data and design systems. It’s very important.”

Check out Clara Durodié’s keynote address from FinovateEurope. And visit our FinovateAsia page to learn more about her upcoming participation in our all-digital, fintech summer conference in July.

Cognitive Finance Group is a specialist consultancy that advises boards of directors on best practices in the adoption, selection, and implementation of AI-based systems.

San Francisco, California-based company GoodData, which demoed its Insights-Platform-as-a-Service technology at FinovateFall, has forged a strategic partnership with Visa. The collaboration includes an investment in the global analytics company (terms not disclosed) and is designed to enable Visa to offer its customers and partners better access to aggregated data and analytics.

GoodData founder and CEO Roman Stanek said that the investment both reinforced the company’s status as a leader in all-in-one data platforms, as well as bolstered GoodData’s mission to enable companies to maximize the way they use data. “Visa’s investment will allow us to increase our focus on interactive self-service analytics, user interfaces, and data visualizations, as well as expand our customer support for managing complex data governance, compliance, cybersecurity, and privacy matters,” Stanek said.

GoodData offers an integrated set of data management, analytics, and insight application development and management components that enhance operational decision-making for financial services companies and insurance agencies. Companies can connect the GoodData platform to multiple data sources in order to build their own standalone or embedded smart business apps.

Visa put the partnership in the context of finding opportunity in the middle of a crisis. “As the world faces pandemic and economic challenges, there’s no better time to invest in areas that will improve the lives of consumers and businesses,” Visa SVP and global head of Data, Security, and Identity products Melissa McSherry said. She added that the insights available via the GoodData platform will not only help Visa’s customers better meet consumer needs, but also will help firms meet them at a time “when those needs are changing fast.”

Before this week’s funding, GoodData had raised more than $115 million, with the company’s last fundraising bringing in $14.4 million in 2018. Earlier this year, GoodData announced that media CMS provider TownNews had partnered with the company to use its data analytics tools to improve revenue and audience engagement. Named one of the Coolest Business Analytics Companies in CRN’s 2020 Big Data 100 roster, GoodData also this month unveiled a new, web-based logical data model (LDM) modeler. This tool complements the company’s just-released, data source management interface to simplify data modeling when starting new data products or extending current enterprise reporting. Critically, the new LDM modeler helps data engineers and data analysts work more effectively together. GoodData co-founder and VP of Product & Marketing called this problem “the greatest challenge facing enterprises building new data products for customers.”

Retail commerce company Shopify unveiled a slew of announcements this week, one of which caught our eye. The Canada-based fintech joined forces with cryptocurrency payments processor CoinPayments to enable merchants to use crypto payments processing.

When Spotify merchants opt to add CoinPayments to their point of sale, they will be able to accept 1,800 cryptocurrencies. Transacting in cryptocurrencies not only reduce fees for sellers, it will also facilitate cross-border payments, enabling them to increase their global customer base.

CoinPayments was founded in 2013 and has since facilitated more than $5 billion in total transactions. The Cayman Islands-based company’s crypto acceptance platform enables merchants to accept more than 1,900 altcoins and charges 0.5% per transaction, much less than the standard 2% to 3% transaction fee typically charged with debit and credit card transactions.

“The combination of Shopify and CoinPayments is unstoppable in the payments industry,” said CoinPayments CEO Jason Butcher. “By bringing our easy-to-use global crypto payments platform together with Shopify’s extensive merchant base, we look forward to delivering a seamless process for anyone looking to do business using cryptocurrencies. As leaders in ecommerce and crypto payments, our combined expertise reflects the future of business transactions.”

Among Shopify’s other releases this month are:

Shopify Balance, a business bank account, card, and financial management tools

Local Delivery, a tool to help online merchants with local delivery logistics

Shop, a direct-to-consumer app and personal shopping assistant to facilitate purchasing and order tracking

Shopify has also added a handful of products to help merchants struggling in the midst of the COVID-19 pandemic. The company recently added a quick website launch to help brick-and-mortar stores go digital, and also added the option to help merchants collect tips and sell gift cards.

Between extreme wildfires, murder hornets, and the ever-present coronavirus, 2020 has been quite the year so far. Now that the year is almost halfway through, it’s a good time to catch our breath and look at some of the lessons learned.

In some ways, it seems as if we packed decades worth of news, digital developments, and economic losses into the first six months of this year, so there’s a lot to cover. That said, we still have another six months to go before we reach 2021 so there is plenty more room for further changes in the fintech industry.

To help digest what’s happened, we’ve picked up four key things we know for sure now that 2020 is halfway over.

Digital is the new brick-and-mortar

If there is a bright side of the coronavirus for the fintech industry, perhaps it is the positive effect stay-at-home orders have had on firms’ digital initiatives. When consumers aren’t able to conduct banking activities in person, they are pushed to online and mobile channels, even if they have never used digital banking in the past.

For banks that already had a robust digital strategy in place, this has been a time to shine. However, those that were still in the midst of developing and implementing their strategy have found themselves trying to catch up. In this instance, however, they are not catching up with their competitors, they are catching up with the new, online-only status quo.

What we know for sure is that this digital push is here to stay. Forced into the digital channel, consumers have had to adapt to practices they have never done before, such as remote deposit check capture. Now that they’ve experienced the benefits of the digital experience and have adapted their habits, many of these users won’t be visiting their bank branch as frequently.

Economic hardships will persist

Even though stay-at-home orders are being lifted in some areas, Consumers have decreased spending across the board. Whether it is because they have lost income or because they are afraid to leave their home because of the virus doesn’t matter– they are spending less and spending in different areas, which will cause many businesses to go under. In fact, it already has. The Washington Post recently reported that more than 100,000 small businesses have closed their doors forever.

Many have predicted that the worst of economic hardship is yet to come. And in all likelihood we won’t begin to fully recover until there is a vaccine. This means that it remains crucial to focus on supporting the customer. Banks can find even more creative ways to help consumers through their financial hardship and retain communication with them so that they know what to expect. In doing so, they will end up with a stronger consumer relationship on the other side of the crisis. Fintechs, on the other hand, have the opportunity to scoop up new clients who are in need of innovative products such as budgeting tools and services for gig economy workers.

Consolidation has begun

Fintech industry analysts have predicted that the economic side effects of COVID-19 will bring consolidation in the sector. And while some will acquire or become acquired, others will shut down as VC funding constricts. We’ve already seen a bit of M&A activity in the space over the past 6 months, though it is difficult to attribute all of it to the coronavirus.

In one vivid instance, neobank Moven announced in late March that it plans to shutter its B2C business and focus on the B2B side of things. The reason for the bank’s closing, explained founder and CEO Brett King, was that a major round of funding that Moven had in the works fell through. Since Moven’s enterprise business was growing because of the high number of banks making the move to go digital, it made more sense for the company to invest all of its resources into that side of the business.

In the traditional bank space, rumors began to circulate last week that Goldman Sachs is looking to merge with another bank. Among the potential partners are Wells Fargo, PNC, and U.S. Bancorp.

Payments will change for the better

Consumers in the U.S. have been hesitant to adopt a digital payments solution. That is, until now. The pandemic-fueled low-touch economy has both consumers and merchants looking for ways to transact without touching cash, cards, or keypads.

One of the most promising, pre-existing mobile payments technologies for the region is Apple Pay. Adoption for the tap-to-pay technology has been growing since Apple launched it in 2014. Now, six years later, Apple Pay transactions account for 5% of all global card transactions.

At the start of 2020, that 5% figure didn’t seem like bad traction. However, now that almost 100% of consumers are interested in making payments with the fewest number of touch-points, we’ll see hockey-stick growth not only with Apple Pay usage but also with its competitors Samsung Pay, Google Pay, and even peer-to-peer money transfer technologies such as Facebook Pay and Square Cash.

As the gig economy grows, so do opportunities for banks and fintechs.

That’s what’s on the mind of Oxygen, a challenger bank built for freelancers. The San Francisco-based startup, which recently launched its mobile app, is now collaborating with CPI Card Group to create a debit card option for its users.

Oxygen tapped CPI Card Group for its “advanced print design services” in hopes to better connect with its unique target market made up of freelancers, digital natives, and small businesses. At launch, two vertical card designs will be available. Both feature a “clean and crisply-designed” look with back-of-card personalization.

“At Oxygen, we understand that the physical brand experience – including everything from the card design to the packaging appearance – matters for our creative, tech-savvy clientele. With CPI’s cost-effective scale and design strengths, we were able to deliver a sleek card to customers in a unique, memorable fashion,” said Oxygen Founder and CEO Hussein Ahmed. “We are pleased to have such a reliable secure card provider and are thrilled to offer customers an eye-catching debit card that echoes their drive, ambition and lifestyle.”

Oxygen was founded in 2018 and caters to the growing set of customers that rely on gig work and multiple income streams to pay their bills. The challenger bank offers both personal and business accounts with features including cash-back rewards and virtual cards for personal accounts, as well as accounting tools and the ability to mail checks from within the app for business accounts. Both accounts boast no monthly fees.

Along with its digital capabilities and creative branding, Oxygen differentiates itself with a lending product that works for the self-employed workforce with fluctuating income. Instead of relying on job stability and credit scores to underwrite loans, Oxygen instead looks at a borrower’s historical cashflow to assess risk and repayment capability.

Oxygen and other challenger banks such as Wollit and Xolo are among the growing number of players eager to serve the gig economy. These customers have traditionally been ignored by larger traditional financial institutions, which haven’t seen the value in serving clients with unpredictable income. This may change in a post-coronavirus economy, however, as more of the population earns their paycheck with freelance work rather than a full-time job.

European wealth management firm Raisin is bringing its Savings-as-a-Service solution to the U.S. The new offering, the first U.S.-based product from the Berlin-based fintech, will enable banks and credit unions to provide private-banking services typically not available to the average banking customer.

Foremost, FIs that partner with Raisin will be able to leverage the company’s technology to quickly build custom retail deposit products. These products include market-linked solutions that enable customers to benefit from a resurgence in economic activity while at the same time providing 100% FDIC deposit insurance up to $250,000. Banks and credit unions can also create deposit products with dynamic features such as laddering, and ones that can be optimized for profitability or other individual preferences.

“Given the current economic uncertainty, financial institutions want a share of the big increase in deposits, but many don’t have the technological tools to optimize or meet customers’ current needs,” Raisin U.S. CEO Paul Kodel explained. He said that in order for banks and credit unions to help rekindle the economy, they will need to be able to offer a wider range of solutions. “Banks need affordable products that enable customers to stabilize their assets now, and then also grow with a recovery,” Kodel said.

Raisin Communications Manager Maggie Bell noted that the company’s new offering comes at a time of increased opportunity in deposit products for financial institutions. She cited data from the Federal Reserve indicating that while commercial bank deposit market volume had grown by more than 10% since the beginning of the year, deposits spiked from $13.5 trillion to nearly $15 trillion between the second week of March and the third week of April. Additionally, deposits could represent a significant part of the refinancing mix for banks, Bell wrote, “especially as bonds have become more cost-intensive within the last two months.”

With 92 partner banks, more than 260,000 customers and €23 billion in assets invested, Raisin was founded in 2012. The company provides access to guaranteed deposit products from across Europe and, in Germany, offers diversified, cost-effective exchange-traded fund (ETF) portfolios and pension products. Named a top five European fintech by the FinTech 50 awards, Raisin is backed by investors including Goldman Sachs, PayPal Ventures, Thrive Capital, and Index Ventures.