If there are any lingering doubts about the power (and popularity) of the Buy Now Pay Later (BNPL) movement, installment payments platform Splitit has 71.5 million reasons to cast those doubts aside.

The New York-based company, which made its Finovate debut as PayItSimple in 2014, announced that it has raised $71.5 million in a private placement and share purchase plan (SPP). With institutional investors such as Woodson Capital Management, the company plans to use the capital to “accelerate sales and marketing, plus (make) further investments in product and technology” according to a statement. Splitit boasts more than 1,000 ecommerce merchants using its technology, and 300,000+ shoppers with an average order value of $893.

Splitit’s fundraising comes as the company reports record Q2 growth, including processing more than $65 million in merchant sales volume, and growth of 1.76x quarter over quarter and 2.6x year over year. In discussing the company’s success, CEO Brad Paterson credited a new willingness on the part of consumers to “maximize their existing credit to preserve cash flow” while at the same time not incurring additional new debt.

Paterson also noted that while the COVID-19 crisis has helped move digital transformation in ecommerce toward the top of the agenda, it was important for those involved in payments to make it easier for merchants to accommodate their customer’s cash management requirements.

As such, it’s hard not wonder if, once again, crisis is responsible for accelerating innovation. After all, one of the initial innovations in retail, the layaway program, emerged during the Great Depression as a way to maintain at least a minimal level of consumption of non-essential goods during a severe economic retraction. By enabling customers to pay for items in small increments over time and then receive those items once they had been fully paid for, the growing retail economy was able to survive an extended period of historically low demand.

The buy now pay later phenomenon is layaway in reverse, allowing customers to gain the benefits of the purchase immediately and moderating the impact of the cost by paying for that purchase over time. But the goal – to accelerate consumer activity and expand the ability of people to spend – remains the same. The only difference is that layaway tended to disappear once credit cards became ubiquitous, while buy now pay later appears to be rising at a time when we are realizing that affordable consumer financing might not be as ubiquitous as we thought.

For Finovate fans, Klarna has been the pioneer in the Buy Now Pay Later space, with fellow alums like Sezzle also earning recognition for its interest-free buy now pay later option. Founded in 2005 and 2016, respectively, both companies are reminders of how fintechs have been providing consumers with alternative financing options well before the coronavirus hit.

That said, it is clear that COVID-19 has stimulated interest in Buy Now Pay Later options. The Business of Finance reported earlier this week that BNPL had become “fashion’s go-to during the pandemic.” Also this week, American Express announced that it would extend its buy now pay later service to more of its cards. The Wall Street Journal featured Australian Buy Now Pay Later specialist Afterpay at the beginning of this month in the wake of the firm’s announcement that it had signed up more than 1.6 million U.S. users since the onset of the coronavirus in March. And Shopify announced this month that merchants on its platform would have access to BNPL financing from installment payment company Affirm. Affirm looks like it is ready to maximize the Buy Now Pay Later moment with an initial public offering, according to reporting in the Wall Street Journal.

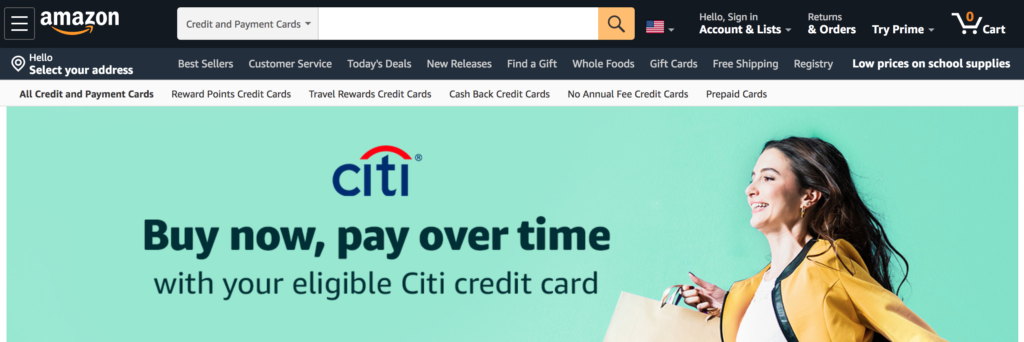

Even the big banks are getting into the Buy Now Pay Later game. Goldman Sachs has introduced a new, installment payment feature called MarcusPay – in partnership with JetBlue Airways – as part of a bigger “build-out” of its Marcus by Goldman Sachs digital banking platform. This week, Citi partnered with Amazon to launch its own BNPL offering Citi Flex Plan.

Photo by Artem Beliaikin from Pexels