This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

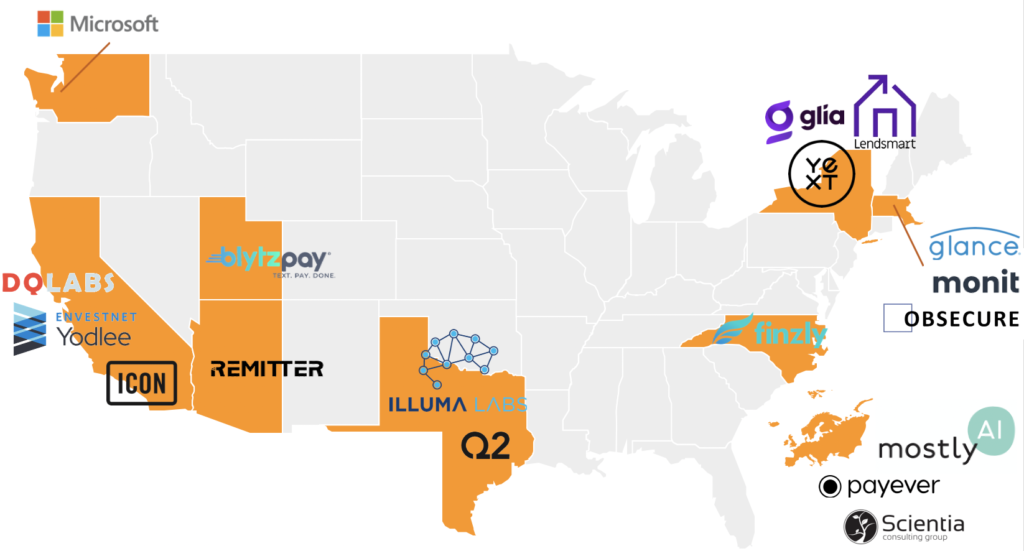

This is probably not your first time hearing about Finovate’s commitment to digital — digital finance, digital innovation, digital events. But it’s likely your first time seeing the FinovateFall Digital demoing companies. All selected because the future of finance is digital, and they are ready to transform your business.

Here’s a look at the demoing companies already confirmed for this year from across the US:

These companies’ products and solutions have been developed (and selected) to meet your business needs from all sides:

Unlock sensitive data in complete compliance

Meet small business needs with a 360° commerce solution

Deliver actionable insights to drive better behavior

Connect employees with an easy-to-understand retirement plan

Optimize debt recovery and collection

Monitor the overall health of your small business customers

Equip your employees with reliable AI-generated next steps

Transform your legacy systems to meet today’s banking needs

Invest in mobile payments because over 60% of the world’s populace uses cell phones

And see how you stack up against other banks, fintechs, and techs

See these companies live next month! Book this week for $795 (a $400 saving).

Describing the opportunity to use AI to create tools and solutions that make society better off, Pablos Holman (pictured right) said, “we get the chance to work for the humans yet to come.”

I like the way of looking at a controversial technology in such a positive light. Instead of focusing on the potential of AI to displace us at our jobs or make our lives unfair in some ways, maybe it is better to examine how we can use AI to craft products, technologies, and services that make our world better to live in.

To do this we need to ask ourselves and the community we work in, “All of this technology is in our hands, what do we want to accomplish with it?” It’s important to ask questions like these in the fintech sector, so that the industry can control how we use new technologies such as AI. As Holman puts it, “Speculate about the possibilities, focus on the positives.”

Holman is a hacker, inventor, entrepreneur, and technology futurist who is on a quest to solve the world’s problems through the innovation of technology. He will be the keynote speaker kicking off FinovateFall on September 14, offering his thoughts on innovating in the post-COVID landscape.

He is certainly a speaker you won’t want to miss. Holman has helped build spaceships; the world’s smallest PC; artificial intelligence agent systems; and the Hackerbot, a robot that can steal passwords on a Wi-Fi network. He is a world-renowned expert in the fast moving 3D printing space, and is currently working on printing the food of the future among other things.

Holman will discuss some of the invention projects under way at the Intellectual Ventures Lab, and their efforts to create an Invention Capital market. He will also be showing off some of the super powers that hackers possess.

FinovateFall Digital will run September 14 through 18 and will be broadcast live in Eastern Standard time. There’s still time to register (at a discount!) so take advantage and book your ticket today.

Led by David Marcus, co-creator of Facebook’s cryptocurrency project Libra, Facebook Financial is the social media giant’s latest effort to enhance the company’s payments initiatives.

Facebook has not made an official announcement about Facebook Financial – referred to internally as F2. Reporting at both MarketWatch and Bloomberg suggests that the new unit will also feature Stephane Kasriel as payments vice president. Kasriel comes to the project from Upwork, where he was CEO. Marcus currently runs Novi, a division of Facebook that is developing a digital wallet for Libra, and will continue in that capacity as Novi moves under the F2 umbrella.

“We have a lot of commerce stuff going on across Facebook,” Marcus told Bloomberg earlier this week. “It felt like it was the right thing to do to rationalize the strategy at a company level around all things payments.” Notably, Marcus has significant payments experience, having been PayPal president from 2012-2014.

Facebook Financial will also handle WhatsApp Pay, recently launched in Brazil, and Facebook Pay, the social media platform’s e-commerce payment system. Engadget’s reporting on the conversation surrounding the new division noted that Facebook sees unifying payments on its different platforms as key to boosting value for advertisers and increasing in-app transactions.

The discussion over Facebook Financial comes just a week after the firm announced another e-commerce-friendly initiative: a Commerce Accelerator that will partner with 60 startups from countries in Europe, the Middle East, Africa, and Latin America to help build out Facebook’s online marketplace.

“In this critical time, Facebook is doubling down on commerce and accelerating its work to enable every business to sell online and help people gain inspiration and discover and buy the products they love. We can’t achieve this alone,” the company announced in a blog post, “so we are looking for startups to build technology with us.”

Zuckerberg himself has praised the role of payments in Facebook’s future. In a recent earnings call, the Facebook CEO noted that “as payments grow across Messenger and WhatsApp, and as we’re able to roll that out in more places, I think that that will only grow as a trend.”

Have you ever heard of open-banking-infrastructure-as-a-service? American Express has, and it has tapped U.K.-based Yapily as the provider.

The open banking infrastructure company has signed an agreement with American Express to take the financial service giant’s open banking payment initiation product, Pay with Bank Transfer, to select European markets. Yapily’s API will enable Amex’s end users to complete a payment without being redirected to a different channel or website.

Pay with Bank Transfer is self-explanatory– it leverages open banking to enable users to transact via bank transfer. The payment method uses biometric authentication and instant payment APIs for faster, more simple, and secure payments.

“The partnership is the first real step to bringing open banking payments to everyone across Europe and the U.K.,” said Yapily CEO and founder Stefano Vaccino. “Now, a significant number of international merchants will finally be able to access, and benefit from, an open banking API.”

Yapily was founded in 2017 to help financial service providers leverage the open banking opportunity by connecting them with banks. The company enables its clients to access data in 15 countries across Europe, and at more than 180 financial institutions. Yapily has raised $18.4 million.

This week’s announcement that Stripe had hired former General Motors Chief Financial Officer Dhivya Suryadevara as its own new CFO is a reminder that the hunt for top talent in fintech has never been hotter. As tech titians and financial services giants embrace fintech solutions, the pressure to find the most effective leaders, the most insightful technologists, and other key executives is forcing companies to up their game when it comes to attracting the best of the best.

With that in mind, here are another nine companies who in 2020 have done just that: made a major, C-suite addition to their leadership ranks that should help propel their respective companies to the next level.

Nicolas Weng Kan – Yolt CEO – news. Former Google Compare CEO Kan took the helm of ING’s smart money app, Yolt, as well as Yolt Technology Services (YTS), a provider of open banking services in Europe last month. Yolt won Best Personal Finance App at the Wealth & Finance FinTech Awards earlier this month.

Anna Manz – London Stock Exchange CFO – news. The London Stock Exchange has a new Chief Financial Officer as former Johnson Matthey CFO and executive director Anna Manz succeeds David Warren, who had held the position since 2012. Prior to her time at Johnson Matthey, Manz spent more than 16 years in executive roles with Diageo.

Lucy Hagues – Capital One UK CEO – news. Hagues, who spent three years as Chief Marketing Officer at Capital One UK and is an alum of the firm’s graduate program, replaced outgoing CEO Amy Lenander. Hagues is the first program graduate to reach the CEO’s office.

Nkihil Rathi – Financial Conduct Authority CEO – news. Appointed CEO of the FCA at the age of 40, U.K. head of the London Stock Exchange Rathi is the first member of an ethnic minority to lead the regulatory body.

Steven van Rijswijk – ING CEO – news. ING Chief Risk Officer Steven van Rijswijk is the company’s latest CEO. He took over for outgoing Ralph Hamers who is headed toward a CEO post at UBS. Van Rijswijk’s promotion comes after 25 years of service at the bank.

Brady Harris – Dwolla CEO – news. Former President of payment solution provider Payscape, Harris was tapped by Dwolla founder Ben Milne to lead the company this spring. Milne praised Harris for helping lead Payscape’s merger with Payroc, “creating a full-service payment powerhouse that operates in 46 countries.”

Michael Miebach – Mastercard CEO – news. “Putting products first” might be one way to describe Mastercard’s decision to replace its outgoing CEO Ajay Banga – who is transitioning to the role of executive chairman – with the company’s chief product officer Michael Miebach. A 10-year Mastercard veteran, Mieback is credited for being a “key architect” of the company’s “multi-rail strategy.”

Hironori Kamezawa – MUFG CEO – news. The appointment of Kamezawa as Chief Executive Officer of Mitsubishi UFJ Financial Group was a bit surprising, insofar as the outgoing CEO has only been in place for a year. But observers speculated that Kamezawa’s leadership will likely mean a broader and more aggressive embrace of fintech by the company.

Asger Hattel – Signicat CEO – news. A new year, a new CEO for the Denmark-based digital identity solution provider as former CEO and Head of Nets Merchant Services Asger Hattel took leadership of Signicat in January. Hattel replaces company co-founder Gunnar Nordseth, who will remain as a shareholder and help support business development.

Mortgagetech has historically been one of the last sectors of fintech to see innovation. However, with digitization en vogue because of COVID-19, there has been an uptick in interest in companies looking to make closing on a home mortgage easier.

As evidence, U.S.-based Blend is gaining attention today for a fresh round of funding and a new valuation. The company landed $75 million in Series F funding, bringing its total raised to $365 million and increasing its valuation to almost $1.7 billion.

The round was led by Canapi Ventures. Existing investors Temasek, General Atlantic, 8VC, Greylock, and Emergence also participated.

“Financial institutions have traditionally taken time to modernize legacy systems, but digital is now table stakes. Shelter in place and social distancing mandates have forced banks and other lenders to accelerate digital transformation plans from years to months,” said Jeffrey Reitman, a partner at Canapi Ventures. “Blend is at the forefront of this innovation, offering flexible digital solutions to help lenders like Wells Fargo, U.S. Bank, Truist, M&T Bank, and other key regional banking institutions meet their accelerated timelines and their customers’ changing needs.”

Blend, a banking-as-a-service company that aims to create a “less stressful, more accessible lending experience,” will use the funds to expand its products and broaden its strategy. Specifically, Blend will likely bolster the consumer banking and auto loans offerings it launched late last year.

“Our goal is to deliver software that gives lenders the flexibility to meet the evolving needs of consumers,” said Marc Greenberg, head of finance at Blend. “We’re committed to being the digital layer that enables millions of people to gain access to the capital they need, while helping our customers be there as trusted advisors for every milestone in a consumer’s financial journey.”

Among Blend’s new launches this year are a digital closing solution for mortgages and home equity loans, a mobile app for loan officers, and new reporting tools for lenders. Since the start of 2020, Blend has brought on 130+ new employees and helped its bank clients process more than $771 billion in consumer loans– over $3.5 billion each day.

In the latest example of the New Economy leveraging the best of the Old Economy, online payments innovator Stripe (founded 2010) announced that it has hired Dhivya Suryadevara as its new Chief Financial Officer. Suryadevara will leave her position as CFO for General Motors, a company that was founded in 1908.

“Dhivya is a rare leader who has run an industry-leading leviathan but also gets excited about enabling the brand-new products and the yet-to-be invented products, too,” Stripe co-founder John Collison said in a statement. “She has the expertise and the instincts to help steer Stripe through our growth in the years ahead.”

More than just the corporation’s most recent CFO, Suryadevara was a long-time General Motors veteran. She joined the company’s Treasurer’s Office as a Senior Financial Analyst in 2004, and became the Chief Investment Officer and CEO of GM Asset Management by 2013. Appointed Vice President of Corporate Finance for General Motors in 2017, she was named CFO a year later. Suryadevara was educated at the University of Madras and earned an MBA from Harvard Business School.

As CFO for General Motors, Suryadevara oversaw financial operations involving more than $100 billion in annual revenue. She was credited for providing leadership in capital allocation decision-making, and for “spearheading numerous strategic transactions for the company.”

“I am very excited to join Stripe at a pivotal time for the company,” Suryadevara said. “Stripe’s mission to increase the GDP of the internet is more important now than ever.” She emphasized her enjoyment of “leading complex, large-scale businesses” adding that she hopes to “accelerate Stripe’s already steep growth trajectory.”

News of the new CFO encouraged some speculation that Stripe may be readying for an initial public offering. Company co-founder John Collison had said this is not the case.

Suryadevara’s hire comes shortly after Stripe made another major appointment: bringing on Mike Clayville as Chief Revenue Officer. Clayville arrives at the company having served as Vice President of Worldwide Commercial Sales and Business Development at Amazon Web Services (AWS).

In other recent Stripe news, the company announced that it was expanding its partnership with Jobber, a home service management provider that will leverage Stripe Capital to help its partner businesses get the financing they need to grow. Last month, Stripe teamed up with Irish online marketplace DoneDeal, enabling sellers on the platform to use Stripe for secure, contactless transactions.

San Francisco, California-based Stripe has raised $1.6 billion in funding, including $600 million announced in April as part of a Series G round that began last fall.

Whatever benefits the challenger bank revolution may bring to retail banking customers, the opportunities these neobanks provide to small businesses may be even more significant. In fact, there is a growing cadre of digital-first challengers who have decided to put innovating on behalf of small business banking at the top of their priorities.

One such company is Wise, a BBVA-backed challenger based in San Mateo, California, that announced the release of its premium checking account in the U.S. this week. The new offering, available for $10 a month, enables businesses to earn up to 1% APY on deposits through a combination of a 0.5% base APY and an additional 0.1% for every $1,000 purchase using a Wise debit card. Accountholders get 25 free ACH deposits and 25 free outgoing bank transfers a month, as well as additional payments services. Among the functionalities to be added are remote check deposit, the ability to send digital checks and international wires, and support for Quickbooks.

The new offering comes in the wake of the company’s first major fundraising: a $5.7 million seed round in April led by Base10 Partners and featuring the participation of several other investors including Abstract Ventures and Backend Capital. The company told TechCrunch earlier this year that it has 1,000 business customers, with average workforces ranging from 2 to 10 employees, and “between $500,000 and $5 million in ARR (annual recurring revenue).”

Finovate audiences met Wise last year when the company made its Finovate debut at our September conference in New York. At the event, Wise co-founders Arjun Thyagarajan (CEO) and Suresh Venkatraman (CTO) demonstrated the company’s “small business banking-in-a-box” solution, and previewed additional products and services for small businesses including payments and invoicing.

From left: Wise co-founders Arjun Thyagarajan (CEO) and Suresh Venkatraman (CTO) at FinovateFall 2019.

Thyagarajan founded Wise after a stint managing product for Mojio, a platform for connected cars. Before that he was a classic serial entrepreneur, launching a personal organizer (LivingOrganized), and a pair of password management platforms (TeamsID and Gpass). But a sense that he wasn’t “doing what I really wanted to do” led him to leave the “hot startup” in search of what he called “problems that needed solving.”

“My explorations led me to FinTech and I was pleasantly surprised with the rapid advancements in technology transforming the financial industry, especially in banking and payments,” Thyagarajan wrote on the company blog last summer, looking back on his decision to launch Wise. “It got me thinking: what if we could build a banking product that can deliver on the promise of putting the customer first … And solving real world problems.”

Thyagarajan’s reflections are similar to those his co-founder Venkatraman, who in a companion post observed that Wise’s own experience as a small business trying to secure quality banking services was vindication of the company’s mission.

“The day started innocently enough as we walked into a local bank with all our paperwork in hand,” he wrote. “That was the beginning of a chase around Silicon Valley to find a bank that would take our money and open up an account. Banks would reject us for all sorts of reasons or just ignore us.”

These days, with an new offering, a big investment and a major banking partner in BBVA in hand, it looks like the fintech world might be ready to wise up.

Adding to the big-bank-to-big-tech partnerships announced in recent weeks, Standard Charteredsecured a three-year partnership with Microsoft today.

The bank will leverage Microsoft to take a multicloud approach that will port its significant applications to the cloud. Specifically, Standard Chartered is planning to make its core banking and trading systems and digital ventures such as virtual banking and banking as-a-service cloud-based by 2025.

“Cloud is a cornerstone of Standard Chartered’s strategy to meet the present and future banking needs of our clients,” said Group Chief Information Officer of Standard Chartered, Michael Gorriz. “Using cloud services improves our ability to be agile and innovative, while increasing our operational efficiency and resilience. As disruption in the financial industry continues, we can focus on client benefits by deploying our solutions quicker and allowing for faster integration of new business models and partners.” Gorriz added that today’s partnership is a “major milestone” in Standard Chartered’s journey to become cloud-first.

Standard Chartered will pilot the launch by moving its trade finance systems to Microsoft Azure. The move is expected to facilitate cross-border trade at the bank.

The partnership extends to Microsoft’s workplace tools. Standard Chartered’s 84,000 employees will be working on Office 365 and communicating via Microsoft Teams.

This news comes during a time of widespread digital transformation across the banking sector. Banks and fintechs are seeking to move their operations to the cloud to update their infrastructure and create a better customer experience. There are two factors driving this change: the global health crisis that has moved many in-person interactions to online channels and the rise of competition from challenger banks.

“Cloud computing is an enabler for financial institutions to modernize their infrastructure and systems, to gain the agility they need to respond to competitive pressures, regulatory environments and customer demand,” said Bill Borden, Corporate Vice President of Worldwide Financial Services at Microsoft. “We are committed to helping Standard Chartered Bank in its ongoing digital transformation journey as it strives to address evolving customer needs and build the next generation of banking experiences.”

Branded payments provider Blackhawk Network has teamed up with open finance data and intelligence platform Moneyhub to ensure compliance with open banking standards. Via the partnership, Blackhawk Network will be able to validate third-party providers, connect to them through live applications, and enable them, with user consent, to access user data and initiate payments.

“Using Moneyhub’s compliance solution means that we can adopt the industry best-practice approach to PSD2 in authorizing our unique prepaid card offering,” Stacey Richards, who handles Product Management for Blackhawk Network, explained. “We share the fundamental desire to deliver a transformative experience for the end-user with Moneyhub, and we look forward to working with the team to deliver on our ambitious vision for the future.”

Blackhawk Network helps businesses leverage branded payments to reach more customers, build engagement and loyalty, and increase revenue. A Finovate alum since 2012, the company has more than 3,000 workers around the world, and serves 26 countries with its branded payment solutions. Blackhawk features 1,000+ brands in categories ranging from dining and entertainment to retail and home improvement. The Pleasanton, California-based company went public in 2013, and was acquired by Silver Lake and P2 Capital Partners in 2018 in a deal valued at $3.5 billion.

More recently, Blackhawk acquired Edge Loyalty Systems, an Australian sales promotions and loyalty firm, for $23 million (A$32.2 million). This spring, the company purchased SVM Cards for an undisclosed sum.

Moneyhub’s partnership with Blackhawk is the company’s third collaboration this year. In June, Moneyhub teamed up with Lumio, a money management app. The following month, the company partnered with investment performance analytics firm, ARQ.

“Our Open Banking expertise means that we are able to deliver a comprehensive compliance solution to Blackhawk Network, ensuring that it remains a leader in the market and delivers excellence to current and future clients,” Moneyhub CTO Dave Tonge said. “Our growing product offering and the multi-use nature of our proposition means that we are able to work alongside Blackhawk Network and help support their growth and aspirations.”

Founded in 2011 and based in Bristol, U.K., Moneyhub made its Finovate debut at our European conference in 2015. Nationwide Building Society is the company’s primary investor, having led a corporate round for Moneyhub in the fall of 2018.

For better or for worse, modern society has adapted to expect things instantly. We want a quick lunch delivery, a fast Uber pick-up, and we expect Netflix to buffer our movies in microseconds. Even Amazon’s two-day shipping takes too long.

Recognizing the value of the real-time economy, Orumlaunched its flagship product, Foresight, last week. The new tool helps banks move money in real time for instant account funding, overdraft protection, and consumer-focused pre-delinquency tools.

Instead of leveraging the blockchain for real-time transfers like Ripple does, however, Orum takes a different route. The startup uses AI to predict the availability of funds within an account and pre-authorizes transactions, incurring limited risk.

“At Orum, we are creating a paradigm shift for the way money moves,” said Orum founder and CEO Stephany Kirkpatrick. “We are leaving behind siloed accounts and manual transactions and building toward fully automated and point-to-point money movement. Technology has created an on-demand economy, but our money has yet to catch up.”

In addition to Kirkpatrick, Orum’s team includes former N26 employee Ryan Cooke and former Stash VP Christine Hurtubise.

Along with Orum’s new product announcement, the New York-based company landed $5.2 million in Seed funding led by Homebrew with contributions from Inspired Capital, Acrew, Bain, Clocktower, Box Group, and angel investors. Impressively, the round was both opened and closed during a pandemic.

“Today’s tools for immediate money movement leave enterprises decades behind what customers demand. Orum is tackling this challenge head on,” said Homebrew Partner Satya Patel. “We’re excited about Orum’s vision. The early demand they’ve seen—both from cutting-edge fintechs and incumbent financial institutions—speaks for itself. It’s clear the market understands the value of moving money in a new, more efficient way.”

According to Crunchbase, Orum is already working with 50 customers and has a waiting list.

The incumbents in the real-time payment (RTP) space in the U.S. have seen some traction, however none have seen widespread adoption. Aside from Ripple, other players working on RTP solutions include The Clearing House, which launched its RTP scheme in 2017 and now counts 32 banks and 19 technology providers as clients. According to Forbes, however, fewer than half of these members are operational on the RTP platform.

The U.S. Federal Reserve is also in on the game, having announced its own RTP scheme, FedNow, last year. Since its announcement, there has been much debate within the fintech industry over whether or not the government can effectively compete with the private sector with real time payments. However, given the lack of traction in the area, the Federal Reserve ultimately decided to pursue FedNow. In true government fashion, however, the offering is not slated to launch until 2023 or 2024.

Remember how society expects everything to happen instantly? The slow traction of incumbent players in the RTP space isn’t meeting expectations. That said, there is a lot of room for Orum in the RTP space and I think we’ll be hearing about a lot more traction from them in the second half of this year.

2020 may be a tough year overall, but it has been quite good to the cryptocurrency space. PayPal announced plans for a cryptocurrency offering, Visa revealed plans to incorporate cryptocurrencies into its payment network, and Mastercard expanded its existing cryptocurrency program.

Late last week, another development took shape: cryptocurrency payments platform Wirex announced it received its first money transmission license in the U.S. The license, issued by the State of Georgia Department of Banking and Finance, comes two years after Wirex received its e-money license from the U.K. Financial Conduct Authority.

Receiving the license is a major step in the direction of a U.S. launch. In fact, Wirex said it will formally launch in the U.S. “in the coming months.”

“We are very excited to receive our license as a money transmission business for the State of Georgia,” said Wirex CEO and co-founder Pavel Matveev. “With the sector growing rapidly, approval of this license is an important step in Wirex’s endeavor to ensure the company complies with money transmission regulations and cryptocurrency laws worldwide. This is an important step in realizing our vision to grow cryptocurrency adoption and use with a mainstream audience in the U.S.”

Wirex was founded in 2014 and helps its 3 million customers in 130 countries buy, hold, and exchange fiat money and cryptocurrencies. Among the company’s offerings is a contactless, crypto-compatible debit card that enables customers to transact at the 54+ million locations where Visa is accepted. Wirex is also known for Cryptoback, a cryptocurrency rewards scheme that offers up to 1.5% back, paid in Bitcoin, to customers who use their Wirex card in-store.

The fintech industry will look back at 2020 as a year of change in many areas, including digital transformation, payments, and in-person services. However, one of the most impactful changes taking shape this year is the broader acceptance and usage of cryptocurrencies.

Part of the evidence here is the formation of partnerships between crypto companies such as Wirex and traditional incumbents such as Mastercard. Last month, the two struck a deal that allows Wirex to directly issue cards on Mastercard’s network.

Wirex has received $3.2 million in funding and became profitable earlier this year.