This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Shortly after expanding its offerings to include consumer banking tools, fintech innovator Blendannounced it has landed $300 million in new funding.

The series G financing round was led by Coatue and Tiger Global, and brings Blend’s total funding to $665 million. With the investment, Blend is also seeing its valuation nearly double to $3.3 billion, up from $1.7 billion just five months earlier.

In a blog post, company CEO Nima Ghamsari said that Blend will use the funds to fuel “aggressive plans” for this year. “We want to build the banking software infrastructure for the future,” said the CEO, “with an end-to-end digital experience for any consumer banking product and a complete homebuying and financing journey from start to close.”

Blend offers banks no-code, drag-and-drop workflows to help them customize the end user experience and launch new products quickly in response to consumer demand.

The company launched in 2012 with a focus on helping banks revamp the mortgage application process for consumers. Last September, Blend introduced a consumer banking suite, a set of tools to help banks focus on more than just the lending process. The suite includes modules to help banks launch their own deposit accounts, credit cards, personal loans, vehicle loans, and home equity line of credit offerings.

Last year, Blend facilitated $1.4 trillion in loans, more than double what it did in 2019. The company counts 285+ lender partners, which together are responsible for around 30% of all mortgage volume in the U.S. Partners include BMO Harris Bank, Navy Federal Credit Union, and Wells Fargo, which sees more than 75% of its mortgage applications submitted via its Blend-powered application tool.

In addition to growing its loan volume and client portfolio, Blend also grew its team. The company added more than 200 employees last year remotely via Zoom, a move that increased its team by more than 60%.

“Today’s news is just another step in Blend’s journey; we’re in it for the long haul, and we look forward to continuing to build the best lending and banking experiences for all,” said Ghamsari.

Some fintech observers may have gotten an inadvertent peek at the news yesterday. But today the big funding rumor has been confirmed: Less than a week after announcing its strategic partnership with fellow Finovate alum Hydrogen, money experience innovator MX is back in the fintech headlines with word of a $300 million fundraising.

TPG Growth led the round with a $150 million commitment. Also participating were existing investors CapitalG, Geodesic Capital, Greycroft, Canapi Ventures, Digital Garage, Point72 Ventures, Pelion Venture Partners, and Regions Financial Corporation. The Series C round takes MX’s total capital to $505 million and increases the firm’s valuation to $1.9 billion – making MX fintech’s latest unicorn.

In a statement, company CEO Ryan Caldwell said that in addition to hiring more talent, MX will use the capital to boost its platform’s data collection and enhancement capabilities. He specifically mentioned the importance of “scaling and finding additional ways to market” which underscores MX’s recent forays into embedded finance and its just-announced partnership with Hydrogen.

“The financial industry is at an inflection point as organizations look to become not only intermediaries, but true advocates for their customers by offering personalized insights and data-driven money experiences,” Caldwell explained. “Along with incredible partners, we are helping financial institutions and technology companies accelerate their digital roadmaps and launch next generation services and apps that will fundamentally transform how people interact with their money.”

MX helps businesses turn raw, unstructured data into valuable, insight-rich assets. This empowers them to build new solutions and services for their customers, drive growth, and boost brand loyalty. In addition to cleaning and categorizing data, MX’s technology adds key metadata that enables companies to better fight fraud, make faster loan approvals, and help their customers make better financial decisions.

In the funding announcement, Derek Zanutto of CapitalG praised MX’s ability to “leverage data strategically” and favorably compared MX’s potential impact on the financial industry to that of Netflix in the streaming content space and to Amazon in the e-commerce space. TPG Growth’s Mike Zappert noted that his firm was committed to investing in the digital transformation that is sweeping through financial services and sees MX as a big part of it. He called MX’s technology “a clear differentiator” that has delivered “tremendous growth for the Company over the last 12 months.”

MX currently works with more than 2,000 banks, credit unions, fintechs, and other companies, and includes 85% of digital banking providers among its partners. This has given the Lehi, Utah-based company a combined reach of more than 200 million consumers. A multiple Finovate Best of Show winner, MX last demonstrated its technology at FinovateFall 2019.

First things first: congratulations to SoFi. The financial services platform has earned a $8.65 billion post-money valuation after agreeing to a merger with Social Capital Hedosophia Holdings, a publicly traded special purpose acquisition company or SPAC that specializes in consumer-focused fintech businesses.

Now, what in the world is a SPAC? And why would merging with one be a sound route to the public markets?

A SPAC is pretty much as described. It is a corporation that is built specifically to buy other corporations. A SPAC, which has no other business operations, works by raising money via an initial public offering, and then using that capital to acquire other companies. These entities are taking advantage of the contemporary interest in the IPO market, leveraging demand for new companies – mostly in technology – into demand for firms betting on the ability to know which among these companies are longer-term winners.

The decision to merge with Social Capital – and to pursue this new route to going public – says a lot about the company initially known as “Social Finance” when it was founded almost ten years ago.

“SoFi is on a mission to help people achieve financial independence to realize their ambitions,” company CEO Anthony Noto said. “Our ecosystem of products, rewards, and membership benefits all work together to help our members get their money right.”

By giving its members a one-stop-digital-shop for financial services such as consumer financing, investments, and insurance, SoFi is well-positioned to take advantage of what Noto called “the secular acceleration in digital first financial services offerings.”

This momentum is in evidence within SoFi’s own ecosystem, as well. Social Capital founder and CEO Chamath Palihapitiya noted the “acceleration of cross-buying by existing SoFi members” as creating “a virtual cycle of compounding growth, diversified revenue, and high profitability.”

Speaking on CNBC, Palihapitiya compared SoFi favorably to Amazon and said that the company best represented the kind of banking solutions people want most. From its origins as a student loan refinancing company to its current incarnation as a diversified financial services platform, SoFi reported more than $200 million in total net revenue in Q3 2020 and is on pace generate $1 billion of estimated adjusted net revenue this year. Noto will continue as CEO of SoFi post-merger.

The deal comes just months after SoFi earned “preliminary, conditional approval” from the U.S. Comptroller of the Currency for a national bank charter. A bank charter, the company noted in the merger announcement, would lower the cost of funds and “further support SoFi’s growth.” In an interview with Yahoo! Finance, Noto explained that this was key to having the ability to provide lower interest rates to consumers and would drive innovations like SoFi Money, the company’s cash management account.

Another plum in the purchase is Galileo, a leading provider of customer-facing and backend technology infrastructure services for financial services providers that SoFi acquired last April. There are 50 million accounts on the platform.

From SoFi’s perspective, “deal certainty” was one of the reasons why the company took advantage of the SPAC route to the public markets rather than a traditional IPO. Palihapitiya is a veteran of the nascent SPAC craze, having taken a number of companies, including Virgin Galactic Holdings in 2019, public in this fashion.

Founded in 2011, the San Francisco, California-based company participated in our developers conference, FinDEVr New York 2017. At the event, SoFi teamed up with data platform Quovo to demonstrate their innovations in providing secure authentication for bank accounts. SoFi currently has more than 1.8 million members and has raised $2.5 billion in funding to date.

This is a guest post written by Shannon Flynn, managing editor at ReHack.com.

Financial tech and nonprofits have an opportunity to build partnerships and make the world a better place. If fintech companies want to work with nonprofits, they must establish trust and clearly outline the benefits of collaborating for the greater good.

Households in the United States are generous. According to National Philanthropic Trust, Americans gave $449.64 billion to various charities in 2019. However, people are increasingly demanding that the giving be easy and intuitive, which brings fintech into play. Even the way nonprofits manage the funds donated to them is changing.

Examples of fintech companies include Lending Club, Kabbage and Stripe. Meshing fintech and charity isn’t always an obvious choice. However, nonprofit technology is on the rise, and organizations benefit greatly from some of the advantages these brands bring to the table. Here are some of the benefits of fintech charity partnerships.

How Fintech and Charity Work Together

There is a growing move toward non-cash payments in charitable giving. Forbes reports in countries such as Sweden, cash-based payments make up 13% of transactions. This can impact traditional fundraising efforts, such as in-person collection baskets.

Fintech advances in the last decade have made it much easier for people to participate in charitable giving. There are numerous ways nonprofit technology helps organizations raise money. Rather than an in-person fundraising push, organizations raise money via social media and email campaigns. Not to mention philanthropies saw an increase in virtual fundraising campaigns in 2020, boosting the need for online financial services and resources at an unprecedented rate.

Nonprofits can only thrive because of the generosity of patrons and local businesses. A fintech business can team up with a charity, and both can develop stronger community relationships as a result. Individuals who support the organization will look to partner companies for their own fintech solutions. The charity benefits from gaining access to the business’s software for easier donations and tracking funds.

Nonprofit Technology Advances

The M + R Online Giving Benchmark Study found that online revenue grew about 10% in 2019. Facebook alone made up around 3.5% of online giving, with much of it occurring on Giving Tuesday.

In addition to ramping up the ways people give to nonprofits, financial management has gone into the cloud. Rather than keeping a paper book, nearly every organization uses some type of accounting software and big data to track giving and donors and figure out ways to increase revenue from year to year.

Benefits of Teaming Up

There are numerous benefits to fintech and charity partnerships. While some are quite obvious, others are more subtle.

More Exposure

When two companies team up, they both gain access to one another’s customer lists. For example, if a business offers an online payment gateway and it teams up with a local charity, it might send out a press release. Simply gaining exposure may bring in more donations for the nonprofit.

They also will let their members know they are using a partner’s payment system. If the software is donated, the nonprofit will offer a thank you. Some of its patrons are likely business owners who may need services. By working together, the charity and company both expand their reach.

In a study by Omnicom Group’s Cone Communications, researchers found 83% of millennials felt loyal to companies helping them contribute to causes. A partnership helps both the fintech firm and the non-profit organization.

Financial Help

Some fintech companies throw their financial support behind an organization. They offer technology advantages and also come alongside them to raise money for the cause. Businesses should care about the purpose of the charity it supports. It should tie into the company’s philosophy and help advance its own goals. Any donations can likely be written off on taxes while helping a local group.

Testing Systems

Offering software at no cost allows businesses to try out new features and work through bugs. Part of the agreement can be that it provides the nonprofit with updates first, and they’ll report issues so the company can fix them. They get the program for free, and the business receives instant feedback on what works and what needs tweaking.

Better Tracking

Most fintech companies offer better tracking features for all types of businesses. Charities will be on top of where donor funds go and if they’re being used wisely. When people give to an organization, they expect them to be good stewards of that generosity. With the right programs, the nonprofit can run reports and know in an instant how money gets spent and if they are actually making the difference they promised.

Fintech Charity Partnerships Can Improve Performance

When it comes to making a difference in the world, improved performance enhances productivity and allows volunteers to do more than they ever thought possible. Technology allows people to stay on top of tasks and ensure cash flow is never an issue. By working together, fintech and nonprofits can make a huge difference in the lives of those they serve.

ShannonFlynn is a technology and culture writer with two plus years of experience writing about consumer trends and tech news.

You’ve finally perfected your digital transformation strategy that was accelerated because of 2020’s global pandemic. What should you focus on now? Here’s an idea: stablecoin transactions.

The U.S. Office of the Comptroller of the Currency (OCC) last week published Interpretive Letter 1174 detailing that banks may use stablecoins and independent node verification networks (INVNs) to facilitate payments for customers. That is to say, banks can transfer stablecoins to other banks.

To catch you up to speed, INVS are distributed ledgers. And stablecoins are a type of cryptocurrency that minimize volatility by pegging their value to an external factor.

There are a few key things this means for traditional financial institutions.

Transactions become decentralized

Stablecoin transactions are essentially decentralized cryptocurrency transactions. Because of this, they enable banks to send and receive money without a government intermediary.

Faster payments

Stablecoin transactions do not rely on traditional payments rails, rather, they utilize public blockchains. Because of this, stablecoins, just like other cryptocurrencies can be transferred in near-real time from one party to the next.

On 24/7

Once again citing freedom from traditional payment rails, because stablecoin transactions occur outside of the traditional payments infrastructure– and because they occur instantly– they can essentially be made at any time, including on the weekends and holidays.

Compliance is still on the table

According to the letter, stablecoin transactions, “should have the capability to obtain and verify the identity of all transacting parties, including those using unhosted wallets.” So banks are still responsible to adhere to KYC guidelines.

Additionally, banks using stablecoin transactions are responsible for managing the multiple risks associated with cryptocurrency transactions. Per the letter, “The stablecoin arrangement should have appropriate systems, controls, and practices in place to manage these risks, including to safeguard reserve assets. Strong reserve management practices include ensuring a 1:1 reserve ratio and adequate financial resources to absorb losses and meet liquidity needs.”

This is positive news not only because it offers banks more options, but also because it serves as a signal that the OCC and the Acting Comptroller of the Currency Brian Brooks are bullish on cryptocurrencies.

Pay attention to the cryptocurrency/stablecoin sector this year. We’re expecting to see significant developments in the decentralized finance area, and banks’ involvement in initial cryptocurrency efforts will be crucial. There will be little-to-no room for laggards in this space.

Data and analytics company Equifaxannounced its acquisition of digital identity player Kount this week. The deal, which is pending regulatory approval, is set to close for $640 million in the first quarter of this year.

Kount was founded in 2007 and offers a range of products and solutions, including chargeback protection, account takeover and bot protection, ecommerce fraud protection, and friendly fraud prevention. The company’s identity network, the Kount Identity Trust Global Network, leverages AI to link trust and fraud data from 32 billion digital interactions, 17 billion devices, and five billion annual transactions across 200 countries and territories.

All of Kount’s products will be integrated into Equifax’s Luminate Platform, a fraud platform that combines the company’s solutions with machine learning to give clients the information they need to make better decisions about fraud.

Kount has more than 9,000 clients across the globe, including Barclays, Staples, PetSmart, and Chase. Equifax anticipates the purchase will expand its global prevalence in digital identity and fraud prevention solutions.

“The acquisition of Kount will expand Equifax’s differentiated data assets to bring global businesses the information and solutions they need to establish identity trust online,” said Equifax CEO Mark W. Begor. “Equifax is taking advantage of our strong 2020 outperformance and cash generation to make this strategic acquisition. Our data and technology cloud investments allow us to quickly and aggressively integrate new data and analytics assets like Kount into our global capabilities and bring new market leading products and solutions to our customers.”

Kount employees will continue to work from the company’s headquarters location in Boise, Idaho, and will join Equifax’s U.S. workforce.

Digital banking platform Modularbank has secured a $4.8 million (€4 million) investment in a round led by Karma Ventures and Blackfit Capital Partners. The company, founded in 2018 and headquartered in Estonia, said that the seed funding will help it establish operations in the U.K., as well as add engineering and product development talent to meet its expansion goals.

Modularbank’s banking-as-a-service technology leverages APIs and microservice architecture to offer a core banking solution to serve both retail and business banking customers. And because Modularbank is, in fact, modular, companies can select the specific services they want – core banking, deposits and savings accounts, assets and collateral, lending, financial accounting, and payments – to build the solution that best fits their needs.

“Increasingly, people are demanding more flexible and convenient services that fit around the way they work and live and in response, there is a wave of digitalization and embedded finance on the horizon, beginning to build,” Modularbank CEO Vilve Vene explained. “To harness this momentum there is a real need for lean, yet sophisticated core banking technology and that’s where Modularbank comes in, as we do exactly that. Modularbank was set up to enable banks and other customer-facing businesses to devise and roll out personalized banking services quickly and easily.”

Also participating in the round were Plug and Play Ventures, Siena Capital, and Ott Kaukver, angel investor and former CTO of Twilio and Skype.

Modularbank made its Finovate debut at FinovateEurope in 2019. Since then, the company has collaborated with Germany’s Senacor Technologies and announced a strategic partnership with payments processor NETS Estonia. In December, Vene was named one of the most impressive women in fintech in 2020 by Fintech Futures.

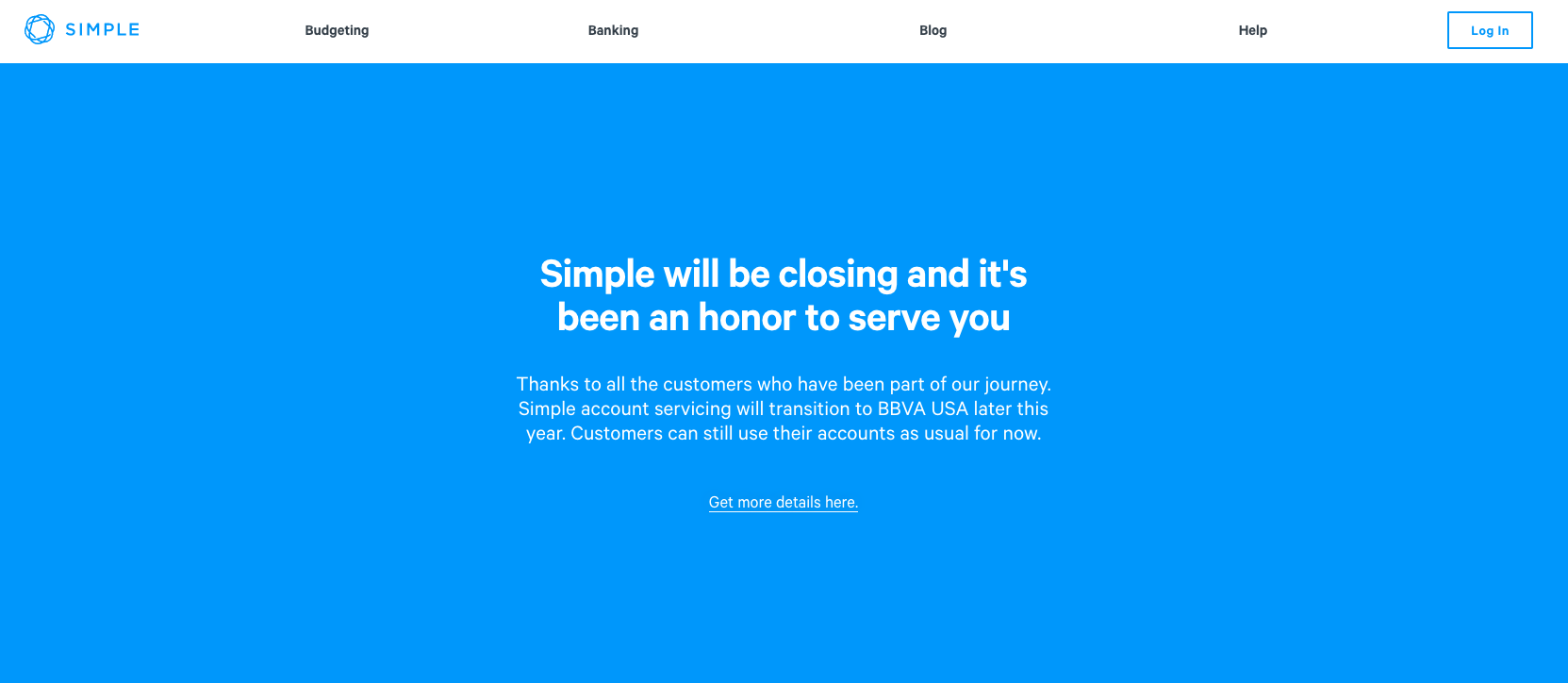

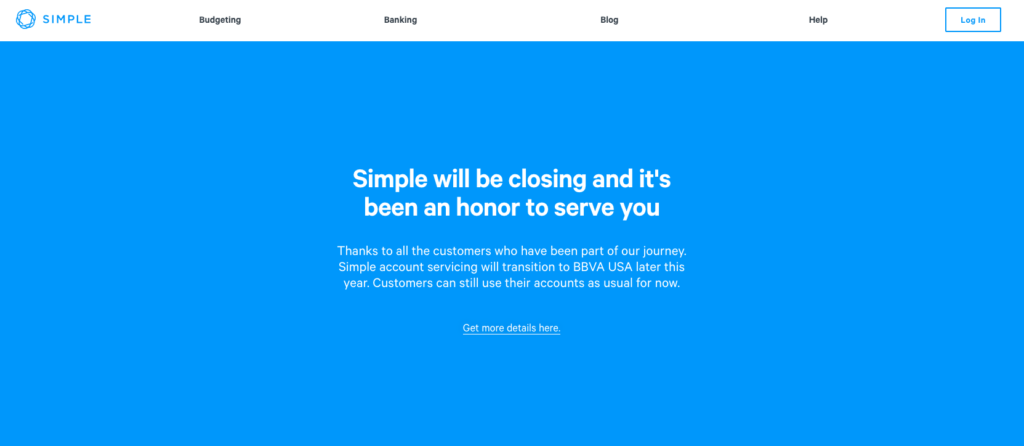

You’ve likely heard that BBVA has decided to shutterSimple, its in-house challenger bank. Yesterday, the company sent an email to accountholders stating, “BBVA USA has made the strategic decision to close Simple.”

The reactions across fintech are mixed– some say they’re not surprised, and others have expressed more nostalgia than anything.

Those who aren’t surprised cite PNC’s recent acquisition agreement with BBVA. The two may have been trying to streamline their businesses in order to minimize duplication of market coverage and services. There’s also the fact that competition in the challenger bank space is hotter than ever, and it doesn’t make sense for BBVA (or PNC, for that matter) to try to keep up with the marketing spend that others such as Chime have shelled out to acquire customers.

Since this is a eulogy, however, I’ll focus on the nostalgia. Simple was founded in 2009 as BankSimple and quickly became one of the top pioneers in the challenger banking space. I like to think of Simple as the grandfather of challenger banks (perhaps the grandmother is Moven, which closed its B2C model last year).

Simple was ahead of its time in focusing on the millennial client base that is untrusting of banks and prefers a straightforward, transparent approach. The bank also offered features that were unique at the time, such as geolocation via an integration with Google maps for every transaction, instant purchase notifications, and a “safe to spend” balance that indicated the user’s discretionary spending balance.

The bank’s young, Portland, Oregon-based staff were consistently quirky and upbeat on customer service phone calls. Simple maintained this culture even after BBVA acquired it in 2014.

Does anyone remember Simple’s catchphrase when it launched? “We don’t suck.” Hopefully the new generation of challenger banks will keep this mantra in mind as they work on creating the new wave of consumer-first banking technology.

As for what’s next, Simple’s email to clients went on to detail what to expect, stating, “In the future, your Simple account will become exclusively serviced by BBVA USA, but until then you can continue to access your account and your money through the Simple app or online at simple.com. You will receive additional information in the near future about the transition of your account servicing to BBVA USA.”

CRED, a credit card repayment company based in Bangalore, India, has scored $81 million in funding courtesy of a Series C round announced earlier this week. Led by existing investor DST Global, the investment featured the participation of Sequoia Capital, Ribbit Capital, Tiger Global, and General Catalyst, and gives the company a valuation of $806 million.

The company’s founder Kunal Shah said in a statement that the funds would help support CRED’s growth and added that CRED is committed to providing wealth-creation opportunities for its employees, as well. Shah said that the company has allocated 10% of its cap table for ESOPs (employee stock ownership plans).

CRED processes a fifth of all credit card bill payments in India. The membership-based company rewards those who pay via CRED with CRED coins that can be used to win exclusive rewards or to earn access to curated products and services. More than 35% of premium credit card holders in the country use CRED, which has seen its overall user base climb to more than 5.9 million users. The company also benefits from creditworthy borrowers – the median credit core for CRED users is 830. CRED members reportedly spend on average 2x the amount of the average CRED user.

For some, news that German digital bank N26 was entering the increasingly competitive challenger banking market in Brazil was met with a loud “it’s about time!” The neobank, which previewed its intentions to launch operations in Brazil back in 2019, may have been temporarily wrong-footed by the twin complications of Brexit and COVID-19. But the news this week suggests that the firm is back on track with its Latin American expansion plans – and a showdown with Nubank.

Not only is Nubank the home team when it comes to neobanking in Brazil, the institution is also the biggest challenger bank in the world in terms of customers and valuation (25 million of the former, $10 billion of the latter). This compares favorably with N26’s five million customers and valuation of approximately $3.5 billion. That said, the Berlin-based challenger bank has significant wind at its back, having just celebrated the one-year anniversary of its arrival in the U.S. back in August and, more recently, locking in $100 million in one of the largest funding rounds of 2020.

Russian bank Tinkoff announces that its voice assistant is now available as both Oleg (male) and Olya (female).

PYMNTS.com features Toms Niparts, CEO of Jeff, an app-based lending platform headquartered in Latvia.

Middle East and Northern Africa

A new 425 million euro line of credit from the European Investment Bank will help Egypt’s Banque Misr support small businesses affected by the COVID-19 pandemic.

A partnership between Visa and fiat-to-crypto service provider Simplex will enable the Israel-based fintech to issue crypto debit cards.

RuPay launches new payment solution for Indian merchants – RuPay PoS – courtesy of a partnership with RBL Bank and PayNearby.

The normalization of relations between Israel and some of its neighboring countries has encouraged the State Bank of India to offer trade finance solutions to Israeli corporations.

Critics have called a new regulation in Mexico that bars third-parties from using platforms or APIs to offer financial services directly “a death sentence” for the fintech-as-a-service model in the country.

Kenya-based MSME financing platform Pezesha takes first prize at the 2020 AFI Inclusive FinTech Showcase.

Chairman of the Digital Lenders Association of Kenya Kevin Mutiso weighs in on the role of “customer-centric regulation” in shaping the growth of fintech.

In a round led by existing investor Insight Partners, multi-channel digital customer experience specialist Glia has raised $78 million in capital. The Series C round takes the company’s total funding to $107 million, and will be used to help scale the company’s digital customer service offerings with an emphasis on product development and an eye toward potential strategic acquisitions.

“Just as Zoom has transformed the way consumers communicate with colleagues, family and friends, Digital Customer Service is changing the way businesses support and engage with customers,” Glia co-founder and CEO Dan Michaeli explained. “This is an area that has gone mainstream, as evidenced by Facebooks’s recent billion-dollar acquisition of Kustomer.”

Glia’s fundraising comes as the company reports growth of more than 150% in 2020. This is due in part to the impact of COVID-19 related lockdowns and Work From Home policies that drove consumers and employees alike toward digital channels for commerce and work. Glia’s platform enables customers to communicate with businesses using any channel – voice, text, video – and to seamlessly transition between those channels during the interaction. The technology allows customer service representatives to guide customer journeys, increasing personalization and efficiency and boosting customer satisfaction and retention rates.

Insight Partners Lonne Jaffe praised Glia’s platform for providing the tools required for businesses to engage customers digitally and “communicate through the customer’s channel of choice.” Dan Brown, founder and CEO of Interactive Intelligence, who also participated in this week’s investment, added that Glia represents a solution for companies that are “still focused on moving antiquated, on-premises telephony systems to cloud contact centers that essentially offer the same functionality.” Brown added that if he were to build his company again today, “I would take Glia’s approach.”

Founded in 2012 and headquartered in New York, Glia last demonstrated its digital customer service technology at FinovateWest Digital 2020, earning Best of Show honors. Formerly known as SaleMove, Glia has teamed up with more than 150 financial institutions, insurance companies, and fintechs, most recently partnering with intelligent virtual assistant company Interface, and fellow Finovate alum and AI-powered chatbot developer, Finn AI.

Our keynote speaker series has been a major feature in the transformation of Finovate from a demo-only showcase to its current incarnation as a digital-friendly, intellectual marketplace for fintech insight and thought leadership, as well.

With a new set of digital and in-person events planned for 2021, we wanted to take a quick look back at some of the speakers who have provided some of the most unique insights into the nexus of finance, technology, and society over the past year. Stay tuned for big announcements this month on what we’ve got in store!

Steven Van Belleghem, author of Customers The Day After Tomorrow

Providing a special address at FinovateEurope just over a year ago, Belleghem took attendees on a fun and insightful journey that looked at how enabling technologies – from 4G and social media – have forced businesses to reconsider the nature of customer service. And with even more powerful enabling technologies like quantum computing and AI right around the corner, he suggested further disruptions to and opportunities in the relationship between customers, businesses, and the products and services they provide are almost assured.

Interestingly, Belleghem points to a new relationship – B2A or business-to-assistant – that will actually make it easier for all parties to negotiate this new, more personalized, but more complex and challenging e-commerce experience. But even as he sees the consumer taking a less active role in everyday financial decision-making, Belleghem still sees human nature behind the wheel. “It’s not going to just be technology that drives new customer expectations,” he said, “it is also going to be personal dreams and wishes, and also the challenges the world will be facing.”

Pablos Holman, Futurist, Founder of Turing AI

“Please crawl out your window,” folk singer Bob Dylan once crooned. “Use your arms and legs, they won’t ruin you.” A similar sentiment was at the center of the keynote address by futurist and founder of Turing AI, Pablos Holman. Speaking at our first all-digital fintech conference, FinovateFall Digital, back in September, Holman urged his audience to focus on solutions to real problems and to avoid the comfort zone of the tried and true. “Nobody has ever invented a new technology by reading the directions,” Holman noted.

For fintechs specifically, Holman – who is also an Inventor with the Intellectual Ventures Lab – urges two strategies. First he encourages startups to see bank partnerships as a way to understand more clearly the needs of financial institutions and their customers. Second, Holman bluntly recommends “running a lot of experiments” to ensure that you remain open to often-overlooked solutions that might actually work best.

Nancy Giordano, strategic futurist and TEDx curator

In her keynote opening address at FinovateWest Digital, Navigating the Big Shift – How Exponential Technologies are Changing … Everything, Nancy Giordano highlighted the fact that as we are struggling to keep up with rapid technological change, we must be vigilant to the pitfalls of becoming paralyzed in the face of it.

For businesses, the strategic futurist cautions against the temptation to “not make decisions,” encouraging them instead to be readier to “act dynamically” in the face of uncertainty. A little over a generation ago, it was the political that became personal. Increasingly, Giordano observed, it is the professional that is becoming personal. And technology is playing a major part in making this happen.

SaaS banking platform Mambu is even more prepared to support the banking-as-a service trend that’s sweeping the fintech industry. That’s because the Germany-based company received $135 million (€110 million) in new funding this week.

The investment was led by TCV, followed by new contributors Tiger Global and Arena Holdings and existing investors Bessemer Venture Partners, Runa Capital, and Acton Capital Partners. TCV General Partner, John Doran, will join Mambu’s board of directors.

The company also disclosed a new valuation of more than $2 billion (€1.7 billion), which places it in the fintech unicorn club (two-times over!).

Mambu will use the funds to accelerate growth and boost its presence across the globe. Specifically, the company announced intentions to deepen its footprint in Brazil, Japan, and the U.S.

“As an increasing number of challenger and established banks sign on to prepare themselves to thrive in the fintech era, we have, and will continue to provide them with a world-class platform on which to build modern, agile customer-centric businesses,” said Mambu CEO and Co-founder Eugene Danilkis. “This latest funding round allows us to accelerate our mission to make banking better for a billion people around the world and address one of the largest, most complex global market opportunities that’s still in the infancy of cloud.”

Mambu was founded in 2011 and emerged as one of the pioneering players to move banking software to the cloud. Since then, the company has seen success from its concept of composable banking that allows clients to build a banking experience to suit their needs without being tied to a specific vendor, product, or technology. This shift away from legacy core banking platforms, along with plug-and-play integrations, helps banks future-proof their systems to better serve their customers. Among Mambu’s customers are ABN AMRO, N26, OakNorth, Orange, and Santander.

Today’s news comes after a strong period of growth for Mambu. The company has seen around 100% YoY growth and is planning to support it by doubling its team to more than 1,000 by next year.