This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

“The shift to a more digital world requires real solutions to secure every transaction and instill trust in every interaction,” Mastercard president of cyber and intelligence solutions Ajay Bhalla said. “With the addition of Ekata, we will advance our identity capabilities and create a safer, seamless way for consumers to prove who they say they are in the new digital economy.”

Seattle, Washington-based Ekata offers global identity verification to enable businesses around the world to link digital transactions to the people who make them. Via APIs and a SaaS tool, Ekata leverages data science and machine learning to help businesses detect fake accounts, cross-verify consumer data, reduce payment risk, and fight transaction fraud. With more than 2,000 corporate partners ranging from global merchants and financial institutions to marketplaces and digital currency platforms, Ekata enables its businesses to gain unique and valuable insights that allow them to make better risk decisions about their customers.

“The acceleration of online transactions has thrust global digital identity verification to the forefront as one of the biggest opportunities to build digital trust and combat global fraud,” Ekata CEO Rob Eleveld said. “The right identity verification solutions enable inclusive and frictionless experiences while, at the same time, ensuring customer privacy, control and security. Becoming part of the Mastercard Identity family ensures a broader, collective approach to meeting the growing demands of the digital economy.”

Founded in 2019, Ekata unveiled its merchant onboarding solution earlier this month. Designed to meet the needs of PSPs, B2B lenders, and marketplaces working with smaller, micro-merchants and sole proprietors, Ekata’s new platform automates the onboarding process via API and provides for more efficient manual review with a SaaS solution.

“Merchants today have plenty of options and will quickly turn to another payment service provider if an organization adds too much friction at onboarding or takes too long on approvals,” Ekata VP of Global Marketing Beth Shulkin said in a statement. “This is much more than a customer experience issue for PSPs and lenders; losing the lifetime value of a merchant has real bottom-line impact.”

A new partnership between AbbyBank and FinovateFall Best of Show winner Sensibill will enable the Wisconsin-based community bank to give its customers the ability to de-clutter and digitize their financial lives.

“In today’s online world, customers expect more convenience to bank how they want,” AbbyBank AVP of Marketing Natalyn Jannene said. “Our partnership with Sensibill will help our customers and employees with digitizing the shoebox of receipts or overstuffed purses and wallets, making it easier for them to track receipts, exchanges, and warranties in one place.”

Founded in 2013 and headquartered in Toronto, Ontario, Canada, Sensibill offers a receipt management solution that makes it easier to organize and track everything from Health Savings Account receipts to expenses from government relief programs like the Paycheck Protection Program. Sensibill’s everyday financial tools give financial institutions the ability to tap into – and act upon – SKU-level transaction data in order to provide their customers with the kind of personalized financial insights that can help them build better financial habits. More than 60 million individuals across North America and the U.K. use Sensibill’s AI-powered technology.

The company’s newest solution – Sensibill Platform – features a pair of new tools – Spend Manager and Spend Insights – that provide financial institutions with more ways to drive digital engagement with their customers and members. Spend Manager leverages predictive analytics to help customers track and manage their everyday spending, while providing personalized tips and custom advice based on their transactions. Spend Insights enables financial institutions to draw upon more than 150 unique points of data from purchases, and pair them with transaction data to anticipate customer needs and preferences in real-time.

“Sensibill is empowering institutions of all sizes to harness SKU-level data to offer personalized experiences and recommendations that help make customers’ hard-earned money go further,” Sensibill co-founder and CEO Corey Gross explained when the platform was unveiled in January. “The time to act is now – by better contextualizing the transaction-level data they already have with SKU-level insights, institutions can help their customers make smarter financial decisions. Those that do will retain loyalty and expand market share while making financial wellness more attainable for all.”

In addition to its newly-announced partnership with AbbyBank, Sensibill in recent months has also teamed up with Leaders Credit Union of Jacksonville, Tennessee ($520 million in assets) and Progress Bank, a $1.4 billion asset bank that serves customers in Alabama and in the Florida panhandle. Last month, Sensibill earned recognition as the winner of the “Personal Finance Innovation” category of the FinTech Breakthrough Awards.

A Finovate alum since 2017, Sensibill has raised more than $55 million in funding. The company’s investors include First Ascent Ventures, Information Ventures Partners, Impression Ventures, Mistral Venture Partners, and Radical Ventures. Sensibill also secured $5 million in debt financing from CIBC Innovation Banking a year ago.

This week’s partnership with Sensibill is only the latest instance of AbbyBank working with innovative fintechs in order to add to its own offerings. Last month, the Wisconsin-based community bank – with more than $616 million in assets – teamed up with another Best of Show-winning Finovate alum, MX, to power its new PFM solution.

“The goal is to help our customers improve their financial awareness,” Jannene said when the collaboration with MX was announced in March. “Knowing where money is spent allows you to manage your money more effectively. When our customers succeed, we succeed and that is truly what AbbyBank is here for.”

A look at the companies demoing at FinovateSpring Digital on May 10 through 13, 2021. Register today and save your spot.

BaseCap Analytics is a software company that makes it easy for organizations to improve the accuracy and quality of their data.

Features

Apply rules dictionary on data sources to monitor failures and root cause trends, before any data is delivered

Analyze data from databases, spreadsheets, document images, etc.

Why it’s great All companies rely on data for intelligence and decision making. BaseCap’s software uses a collaborative approach for companies to fix data issues efficiently.

Presenters

Nicolas Guillen, Co-Founder Guillen is a business strategist and entrepreneur with more than 14 years of experience in finance and technology. He is passionate about data and building teams. He also holds an MBA from Chicago Booth. LinkedIn

Steve Smith, Co-Founder Smith has more than 12 years of experience driving initiatives to build, consolidate, and streamline complex systems to assist organizations with regulation, compliance, and technology needs. LinkedIn

A look at the companies demoing at FinovateSpring Digital on May 10 through 13, 2021. Register today and save your spot.

Glia is a digital customer service platform that connects financial institutions to their customers using chat, voice, video, co-browsing and AI.

Features

Seamlessly move between modes of communication

Receive improved sales results and customer satisfaction via richer customer interactions

Deliver the best experience for customers and agents

Why it’s great Glia is seamlessly converting boring phone calls into exciting digital interactions and customer experiences.

Presenter

John Fernandez, SVP Marketing Fernandez is the SVP of Marketing at Glia, where he is responsible for revenue marketing and business development all over the world. LinkedIn

A look at the companies demoing at FinovateSpring Digital on May 10 through 13, 2021. Register today and save your spot.

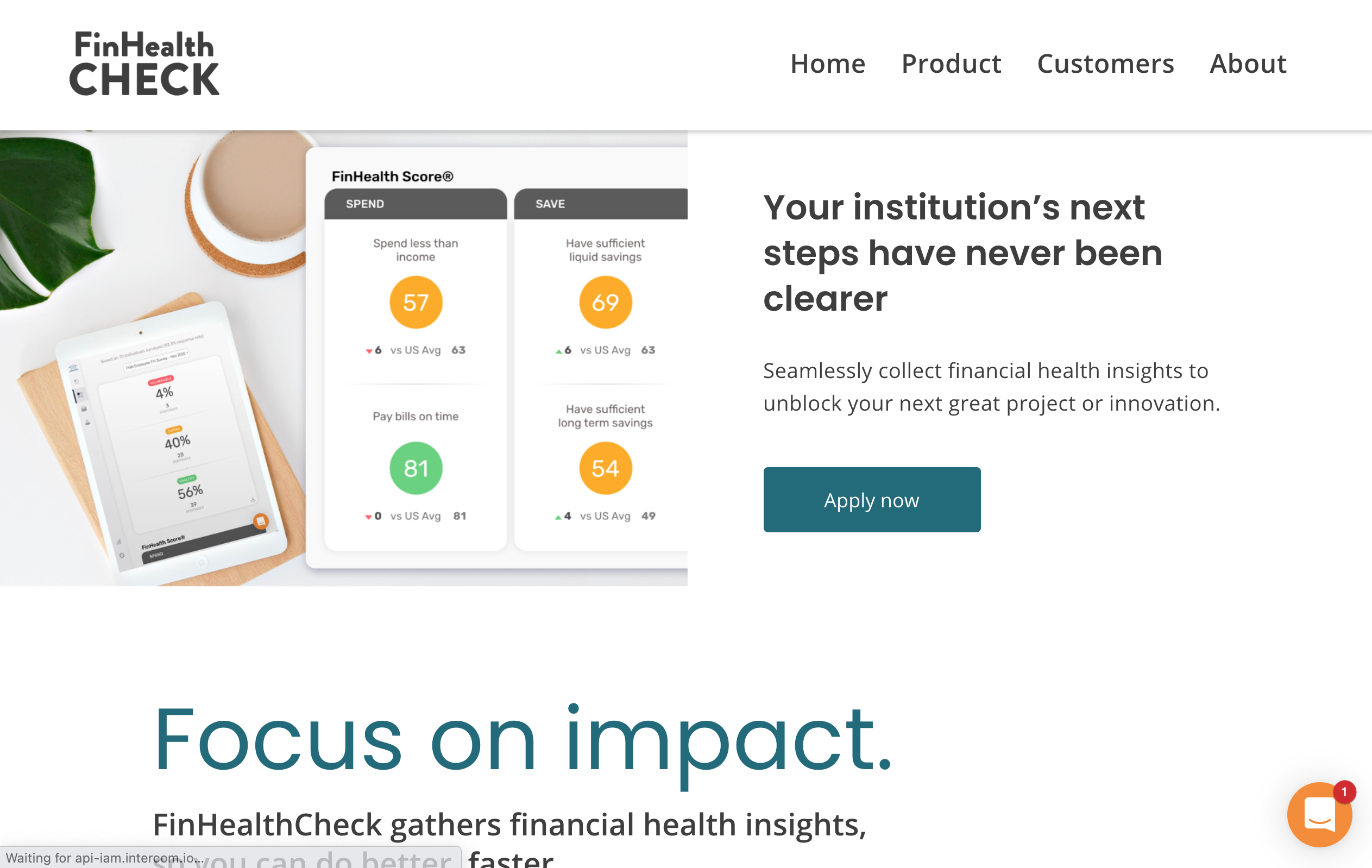

Attune is an insights platform that enables organizations to optimize for financial health.

Features

Quantifiably measure the financial health of customers/employees over time

Benchmark against growing data sets

Get tangible recommendations for actions, then track impact and results

Why it’s great Built from years of research and in-market implementation of measuring and improving financial health outcomes, especially for LMI and people of color who are disproportionately financially challenged.

Presenters

John Thompson, President Thompson is former Chief Program Officer of the Financial Health Network, leading its research, consulting, innovation, network, data, and policy practices. He has private sector experience in tech, payments, and banking. LinkedIn

Andy Bandyopadhyay, Head of Product Bandyopadhyay is the former Head of Science at Even and Director of Research and Consumer Insights at Varo. He holds a PhD from Georgia Tech. LinkedIn

A look at the companies demoing at FinovateSpring Digital on May 10 through 13, 2021. Register today and save your spot.

Join U.S. Bank and learn how to create and send virtual corporate cards in real time for immediate use.

Features

Provision a virtual corporate card in real time

Define card limit and expiration date

Push to a mobile wallet for secure payments

Why it’s great Learn how easy it is to extend corporate spending to the people who need it in real time, with full control and transparency using virtual cards and a mobile wallet.

Presenters

Laretha Hulse, VP Product Development Hulse is Vice President of Product Development for U.S. Bank Corporate Payment Systems. She led the design and launch of the first commercial mobile app and continues to champion mobile and digital payment solutions. She has over 15 years experience in the commercial payment industry working in the aviation, healthcare, payables, and travel verticals. LinkedIn

Jon Zimmermann, VP Zimmermann is a vice president and group product manager within the Corporate Payment Systems division of U.S. Bank. He is responsible for the U.S. Bank Instant Card and Card as a Service products. LinkedIn

After the world went digital last year, the digital identity crisis began taking on new life. Most fintech players are involved in digital identity in some way, and Experian is no exception.

We recently spoke with Eric Haller, Experian’s Executive Vice President and General Manager of Identity, Fraud & DataLabs, to get an idea of how digital identity is changing.

In the interview below, Haller offers his expert opinion and shares how enabling technologies such as AI and the blockchain are impacting how firms think about digital identity.

Digital identity has been on the radar of financial services firms since the dawn of online services. How has this past year of digital acceleration changed how firms approach digital identity?

Eric Haller: The pandemic has shifted segments of the population to the web that weren’t as engaged online as they were prior to the pandemic. For this segment, shopping “face to face” felt safer in many ways. But with a biological threat surfacing, the risks of shopping in the physical world traded places for online risks. All of a sudden, online services seemed much safer.

This plays out in our research where we saw a 20% increase in online shopping this past year with 43% of consumers believing they will even increase their online activity over the next year. And with this shift, 55% of consumers say security is their top priority in a digital experience.

Tell us about the role that AI plays in enhancing digital identity verification for banks.

Haller: To validate someone’s digital identity, literally hundreds of data elements are evaluated to assess whether an individual is a bot, an imposter or the person they claim to be. And all this data is collected, analyzed, and acted on in milliseconds. AI allows for these complicated links and behaviors to be tied together in a variety of ways quickly, efficiently, and accurately to assign the correct conclusion to each customer.

If everything goes well for a legitimate customer, the experience is smooth sailing and both the consumer and merchant conduct “fraud free” business. Most often, there is no fraud. It only happens a very small percentage of the time. But it’s important that if it is a bot or an imposter, that the models in place are precise.

The blockchain seems like a valuable enabling technology when it comes to proving identity. Is this an idea you’ve seen gain popularity? Or is it more of just a fad?

Haller: The portability of a trusted identity in a digital ecosystem integrated with a blockchain could serve a lot of value for consumers and businesses. But it requires quite a bit of effort to get both those that want to share their identity and those willing to invest in accepting it participating in it.

If there were a lot of businesses that would accept a particular blockchain based ID, consumers would put in the effort to have on and use it. If there were a lot of consumers with it, businesses would put in the effort to invest and accept it.

Which side grows with scale first? There are many chasing this ideal. I wouldn’t characterize it as a fad — just very ambitious and challenging to achieve.

This is a guest post written by Dr. Anette Broløs of Broløs Consult and Dr. Erin B. Taylor of Finthropology.

Finances have long been considered a man’s domain. Women’s economic power is, however, growing along with growing equality in education, changing family patterns, and more focus on gender diversity.

With growing economic power, the market potential to serve women with suitable financial solutions is growing, too. During the last 5 to 10 years, there has been rapid growth in the number of organizations offering female-focused financial services. Yet Oliver Wyman estimates that companies are missing out on $700 billion in profit by not catering to the female market.[1]

What can we do to tap into the female financial market?

This question is at the center of two reports we published in the last year asking why women might need or want their own financial services.[2] How does women’s behaviour differ from that of men? What kinds of features might women need in financial services that are different to those for everyone? And is there anything special about serving women, or is it just part of the broader trend towards developing client-centric solutions?

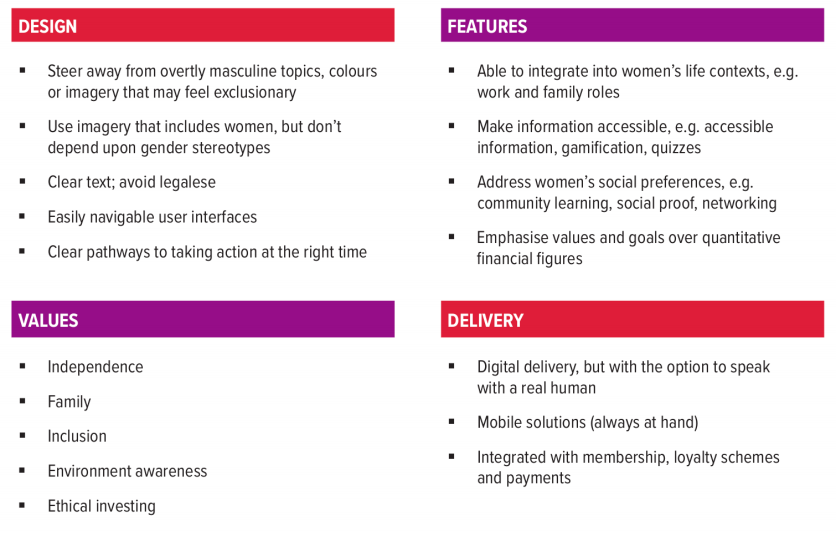

Figure 1: What goes into designing financial services for women?

In the first report, Female Finance: Digital, Mobile, Networked (2020), we explored solutions for women in-depth and presented an analysis of what makes financial solutions ‘female.’ In the second report we studied the characteristics of 102 organizations offering financial services to women, comparing them with external statistics and reports.

We found that there are– at least for now– definite differences between what men and women look for in financial services. In Figure 1 we provide an overview of what makes a product or service targeted at women: looking at design, features, values, and delivery.

We also found that many providers offer “traditional” services (savings, investment, credit, etc.) embedded in other services such as advice, impact solutions, education, mentorship, and networks. Women seem to value these integrated services more than men because they provide a more personal and social approach to finances. Interestingly, there are an increasing number of networks, associations, and NGOs that offer services like learning and networks without actually offering traditional financial services— a new development in the market.

The values of companies that focus on women are also different from those catering to a broader market. The latter tend to focus on “value for money,” whereas the female-focused organizations focus on culture, empowerment, creativity, and freedom.

And so, providing female-focused financial services isn’t just about improving messaging or offering ‘wrap around’ services on existing offers. The majority of organizations that we studied designed their services for women from the outset, and many of them were founded— and led— by women. Many founders come with a solid background in financial services.

So, what can fintechs and incumbent financial service providers do to tap into this important market?

We find that two elements are at the core of successfully reaching this market. [3] The most important is to develop a holistic understanding of customer needs. Women look for assistance to achieve financial health and wellbeing for themselves and their families, and so they prefer solutions that fit into their real life, rather than just considering factors like risk and return.

This means, for example, that investment services for women should not only focus on helping them get the highest profit possible, but also on investing in education, a better life, and security for women and their families.

Offering services to women also means going beyond questions of financial literacy. Good financial services for women will help them to gain control over economic decisions in both the short and long term.

Another important element to understand is how digital solutions can support the provision of holistic services. Women are avid users of integrated, easy-to-access solutions.

A good place to start is to invest in better understanding the female market and its characteristics. This may be assisted by connecting with other organizations to share best practices and create co-learning opportunities.[4]

Another important focal point is the generation of reliable data and insights. To assist with this, companies can collect sex-disaggregated data on customers to shed insights into gender differences in product and service use. They can also take the time to research female customers’ behaviour and user experience, including their life contexts, needs, and preferences.

Companies can adapt the innovation and development process to be more customer-focused and less technology-driven. They can introduce customer knowledge into innovation and put co-creation at the centre of the process.

We encourage organizations to develop holistic value propositions that integrate financial offerings into everyday activities, as well as personal networks and communities. As part of this, they can communicate with women in ways that speak to their life contexts, and which are inclusive rather than exclusive.

When developing services for women it is also important to have an appropriately diverse team to research and design them. Companies can work on internal organizational diversity, including capitalizing on team diversity to reduce the risk of unconscious biases entering into service design. This may be assisted by partnering with fintechs that are already experienced in providing services for women.

This is a simple enough recipe that also fits the general trend towards customization, so there is really no excuse not to get started.

[1] Oliver Wyman. 2020. Women in Financial Services 2020. May

[2] Anette Broløs and Erin B. Taylor. 2020. Female Finance: Digital, Mobile, Networked. EWPN and Keen Innovation and Erin B. Taylor and Anette Broløs. 2021 Female Finance in Figures. EWPN, Keen Innovation and Bank Cler.

[3] We decided to focus on the general findings and perspectives here. There are many important learnings to put to use in developing services for women-led SME’s and particularly to the economic access and development in poorer economies.

[4] We take inspiration from the Financial Alliance for Women. In their October 2020 report they indicate a number of ways to push forward: 1) Collecting sex disaggregated data; 2) Understanding women’s realities, needs and preferences; 3) Working with gender biases; 4) Developing holistic value propositions; 5) Setting these in marketing that appeals to women.

The news is abuzz with excitement about Coinbase’s IPO. The San Francisco-based digital currency platform began trading on the NASDAQ under the ticker COIN for $381 per share today and closed out the day at just over $328 per share.

It’s always exciting when a fintech company goes public, but there are a few reasons why Coinbase’s debut is particularly compelling:

Legitimacy

Coinbase’s listing helps legitimize cryptocurrency in general. Many everyday consumers consider cryptocurrency as a medium of exchange for fraudsters and bad actors on the dark web. This will shift, however, to placing digital currencies in a more positive light and consumers will begin to understand the true benefits of crypto– a tool for faster payments, a way to lower fees, and an agent for a more inclusive financial system.

Sets the stage

The Coinbase IPO sets a precedent for others in the cryptocurrency industry to go public. Digital currency wallets and crypto marketplaces are closely tied to the price of cryptocurrencies, which have historically been extremely volatile.

Despite the uncertainty, Coinbase has proven to be profitable. According to the New York Times, Coinbase made $730 million to $800 million in net profit on $1.8 billion in revenue in the first quarter of this year. The company’s performance in the public eye will dictate the moves of others in the cryptocurrency industry, including bitcoin exchange Kraken, which is considering a public listing next year.

Ready for CBDCs?

One effect we may see come from Coinbase’s move into the public eye is its potential to prime the U.S. market for central bank digital currencies (CBDCs). This reflects back to the first discussion point about offering a sense of legitimacy to the cryptocurrency realm.

The U.S. hasn’t taken any formal actions toward the launch of its own digital currency. However, multiple other nations, including China, Brazil, and Russia, have recently made announcements regarding their own nations’ CBDCs. Bringing cryptocurrency into the realm of traditional finance helps ready the everyday U.S. consumer for the eventual proliferation of digital currencies.

An increase in demand

Will Coinbase’s exposure outside the cryptocurrency space increase the number of people holding digital currencies?

Ben Weiss, CEO of crypto ATM provider CoinFlip answers it this way, “While it is hard for us to know if more people will get into crypto just because Coinbase is trading publicly, we know for sure that at least people who were too scared of the volatility of bitcoin can now take a more traditional approach by buying Coinbase stock. There will definitely be a lot of these people and hopefully this is a gateway for them to get into bitcoin over time.”

While Finovate is all about demoing the newest fintech, we’re also into discussing it.

At this year’s FinovateSpring conference, which will be held digitally on May 10 through May 13 in Central Standard Time, we’re hosting hours of discussions on the hottest topics in banking and fintech. Thinking of joining us? There’s still time to buy your ticket before the price increases on April 20.

Here’s a highlight of some of the topics you can expect:

Neobanks vs Traditional Banks

A look at who has the advantage and how neobanks will find a path to profitability

Embedded Finance & Banking As A Service: A Game-Changing Opportunity For Incumbents?

A discussion of how banks can leverage open finance

Fintech, ESG & Climate Change: How Financial Services Companies Can Play A Key Role Helping Clients On Their ESG & Climate Change Journeys

A look into how banks should act on the explosive ESG trend as it transcends investing into everyday finances

The ABC Of CBDCs: Why Central Bank Digital Currency Initiatives Are A Gamechanger

CBDC initiatives are moving fast. Here’s what you need to know.

Buy Now Pay Later: A Great Product For Customers Or A Debt Trap?

Experts debate the pros and cons of buy now, pay later schemes.

Seven in Seven

7 Expert Speakers Have Just 7 Minutes to Tackle Critical Issues Facing Financial Institutions & Fintechs.

Analyst All Stars

Alyson Clarke, Principal Analyst at Forrester; Daniel Latimore, Chief Research Officer at Celent; and Jacob Jegher, President of Javelin Strategy & Research discuss the top trends in fintech and banking.

Want to see more? Check out the full agenda on the FinovateSpring event page.

Demoing companies showcasing new and innovative technology are at the heart of Finovate events. We caught up with FinovateEurope 2021 demoer Erez Zohar, CEO & Co-Founder of Obsecure, about the company’s beginnings and the adaptations and takeaways from launching during a pandemic.

Tell us about Obsecure, when was the company founded and what problem was the company founded to solve?

ErezZohar: Obsecure was founded in January of 2020 with a mission to provide next generation identity trust biometric solutions for assuring the highest level of trust at time of digital onboarding and high risk transactions.

What in your background gave you the confidence to tackle this challenge?

Zohar: I spent the last 20 years helping financial service organizations fight financial crime and fraud. One of my key observations was that the industry spends so much effort to spot bad actors and suspicious activities but as a result good customers are being treated as suspects as well. A lot of authentic account opening applications are being declined or abandoned because of complex verification steps. Transaction limits and various authentication challenges are being imposed on good customers. This results in frustrated customers who are likely to abandon a digital onboarding process or switch to a different financial institution, especially in such a competitive market.

So I decided to develop products that focus on the good customers vs. the bad actors, increase identity trust and remove friction.

Who are your primary customers and how do you attract them?

Zohar: Our technology is applicable to any digital service. However, our primary market focus at the moment is within financial services and payments / ecommerce. The value proposition is simple. We help you accept more customers which means growing your business. We further help you take on riskier business and keep your customers happy – all while protecting you from bad actors.

Tell us a little bit about the technology behind your solution.

Zohar: Our core technology uses privacy-preserving face biometrics with state-of-the-art biometrics matching and liveness detection. We use this core technology plus other very unique techniques to develop innovative solutions that are different than anything else in the market today. Our two main solutions are:

CyberPrint™ – a biometrics identity verification solution that corroborates identities against their online visual persona. This solution can augment and in some scenarios replace document verification. The goal is to increase trust at time of onboarding and accept customers that otherwise would be rejected. We came up with an innovative approach that both increases trust but also maintains customer privacy which is key to everything we do

AuthenticAction™ – a notary-grade digital action signing solution that signs any digital transaction with the biometrics of the customer, ensuring that no one but the true customer can initiate the transaction. Very powerful for high risk transactions such as large wire or alcohol purchase. The innovation here is about using continuous biometrics authentication and combining identity with action into a single channel.

How did COVID-19 impact your company and its customers? What were some of the big adaptations you had to make? What are your biggest takeaways from the experience?

Zohar: COVID-19 hit not long after we started our journey and we were initially concerned. However, the accelerated shift to digital turned out to be a great driver for solutions like ours. This is also when we decided to expand our offering beyond high risk transactions to remote digital onboarding which is so critical today.

My key takeaway from this experience is to always be thoughtful about how to mitigate risks and at the same time seize opportunities which are presented when the market changes.

What can we expect from Obsecure in the months to come?

Zohar: Our products are innovative and unique in their nature and as such are adopted by innovative and nimble organizations first. Our focus in the next few months is on helping our customers and design partners gain the most value from our solutions and make the necessary enhancements. In parallel we plan to expand our customer base in both the financial services and payment / ecommerce markets. And of course, our roadmap is full of new and innovative ideas which we plan to add to our products.

Alternative banking services company SoFi unveiled a new product last month that will enable eligible members to participate in upcoming IPOs.

The tool will sit within SoFi Invest, a suite of investment tools that offers automated investment services, retirement accounts, a cryptocurrency wallet, and more.

Here’s how it works- users with at least $3,000 in their Active Invest accounts can select the IPOs they’d like to participate in by submitting an indication of interest. Once the IPO is live, investors will receive a notification asking to confirm their order and secure their shares.

If you’re a fintech veteran, this concept may sound familiar. There have been a handful of companies that have opened up IPO participation for retail investors, which are generally excluded from IPOs since they don’t generate the same revenues as institutional investors or high net worth individuals.

The first fintech to offer IPO access to retail investors was Loyal3, which was founded in 2008. The company launched a social IPO platform in 2014 that partnered with pre-IPO companies to enable them to include consumers, employees, partners, and fans in their IPO. Investors were required to purchase a minimum of $100 in stock but were not charged a fee. Loyal3, however, may have been ahead of its time. The company closed its doors in 2017.

Linqto, which recently demonstrated its platform at FinovateWest 2020, allows accredited investors to invest in pre-IPO unicorns. The company requires investment minimums ranging from $5,000 to $10,000. Among the companies currently available to investors are Impossible Foods, Ripple, and Nerd Wallet.

Yet another fintech in this arena is MarketX, a cross-border marketplace that allows investors to browse deals and invest in pre-IPO companies across the globe. MarketX currently offers investors access to pre-IPO companies in the U.S., China, Singapore, Indonesia, India, the UAE, and more. While MarketX advertises to accredited retail investors, the company requires a minimum of $50,000, a figure that is much higher than others working in this space.

With higher minimums and accredited investor restrictions, the IPO investment offerings from Loyal3, Linqto, and MarketX aren’t as accessible as SoFi’s proposed IPO investment tool. Stock trading app Robinhood, however, is also rumored to be entering this space with an offering that will compete on the same level as SoFi.

Reuters reported last month that Robinhood plans to democratize IPO investing by enabling its users to buy into IPOs. According to the news source, Robinhood is allowing its users to buy into its own IPO (which is slated for later this year) and will then use the technology it built to create a more general IPO investment tool for its 13 million users.

SoFi showcased at FinDEVr New York 2017 in a presentation about leveraging bank authentication. FinDEVr will be returning to the Finovate lineup with its own stage at this year’s FinovateSpring digital event. Check out the event page to learn more.