In a round led by Tiger Global, financial services and technology company Brex has raised $425 million, boosting its valuation to more than $7.4 billion.

“Our investors – new and existing – believe in our team, our business model, our product vision, our customers, and the future of Brex,” company co-CEO Henrique Dubugras said. “We are delighted to have them on board for the next phase of our journey.”

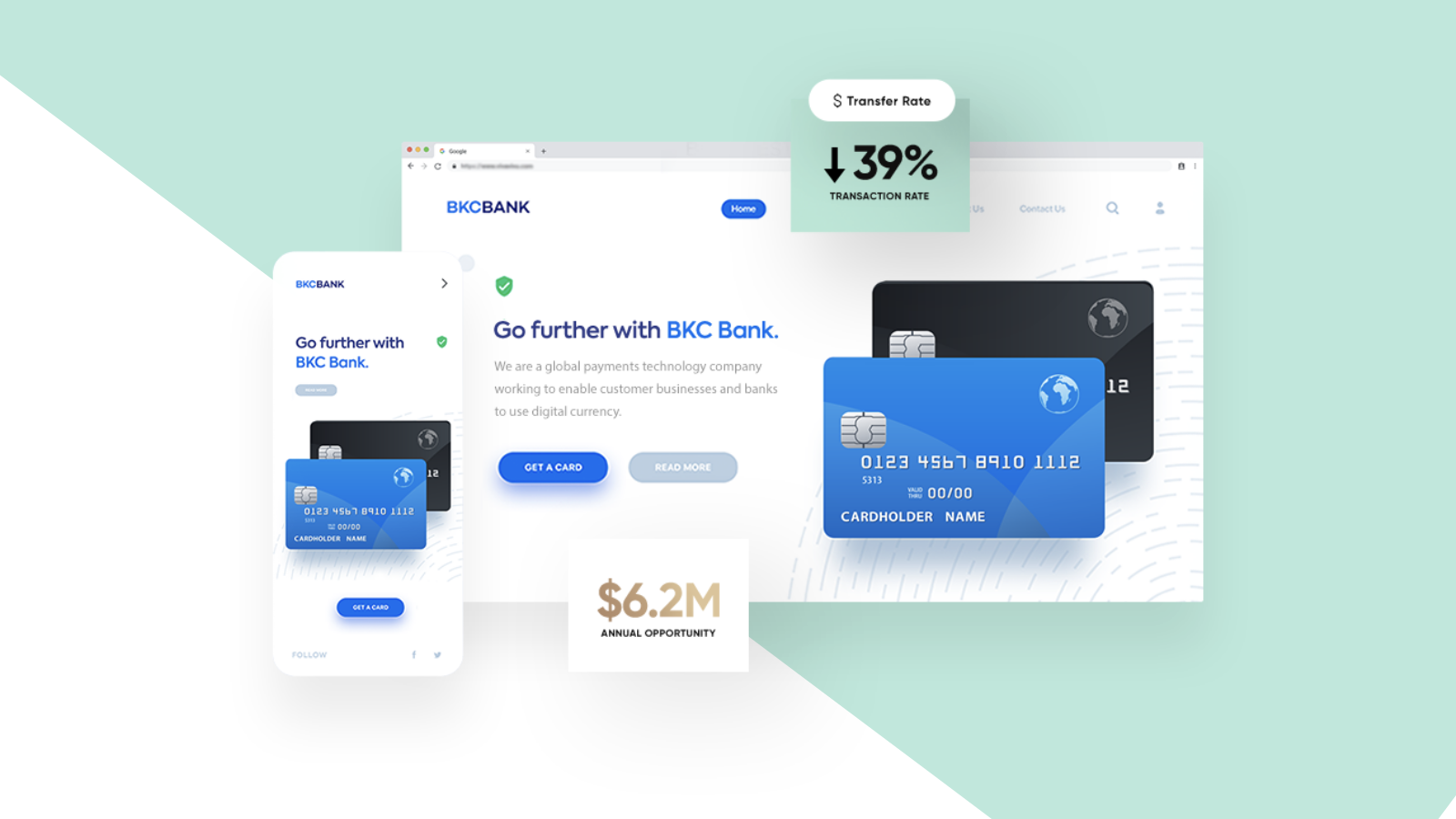

Speaking of the next phase, today’s investment comes as the company, which began with a corporate credit card product for venture-backed startups four years ago, announced the launch of a new all-in-one finance platform. The new offering combines spend management technology with billpay in a single dashboard and will be available for $49 a month. The platform facilitates responsible employee spending via corporate and vendor cards, eliminating the need for expense reports and personal reimbursements. Business owners can also easily track spending across business divisions to better understand spending trends by department, merchant, account, as well as by individual employees.

“Growing and maintaining a business should not depend on how good a small business owner is at managing their finances,” Brex CTO Cosmin Nicolaescu said. “Our all-in-one finance solution gives business owners peace of mind, and the time back to do more of what they love and remember why they started their business.”

In addition to this news, the fact that Brex applied to establish a “Brex Bank” earlier this year suggests that the company also could be en route to offering FDIC insured products to small businesses without requiring an intermediary bank as a partner.

“Brex Bank will expand upon its existing suite of financial products and business software, offering credit solutions and FDIC insured deposit products to small and medium-sized businesses (SMBs),” the company noted in February. “Brex and Brex Bank will work in tandem to help SMBs grow to realize their full potential.”

Located in San Francisco, California, Brex includes ecommerce platforms like Cheers and Dr. Squatch, accounting companies like Pilot and Kruze, and startups like Hourly and Bounce among its customers. Founded in 2017, Brex enables companies in a variety of industries to better manage their finances via a combination of payment and cash management solutions. In the first quarter of this year, Brex reported customer growth of 80% and total monthly customer addition gains of 5x. The company said that 45% of its customers are currently small and medium-sized businesses.

“Brex is building the future of finance for the next generation of businesses,” Tiger Global partner Scott Shleifer said. “We are excited to partner with them as they continue growing rapidly, innovating their product offerings, expanding their customer base and leading an industry that is dominated by incumbents.”

Also participating in this week’s Series D round were new investors TCV, GIC, Baillie Gifford, Mardrone Capital Partners, Durable Capital Partners LP, Valiant Capital Management, and Base10. Existing investors Y Combinator Continuity, Ribbit Capital, DST Global, Greenoaks Capital, Lone Pine Capital, and IVP were also involved in the investment.

Photo by Felix Mittermeier from Pexels