This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

A look at the companies demoing at FinovateAsia Digital on June 22, 2021. Register today and save your spot.

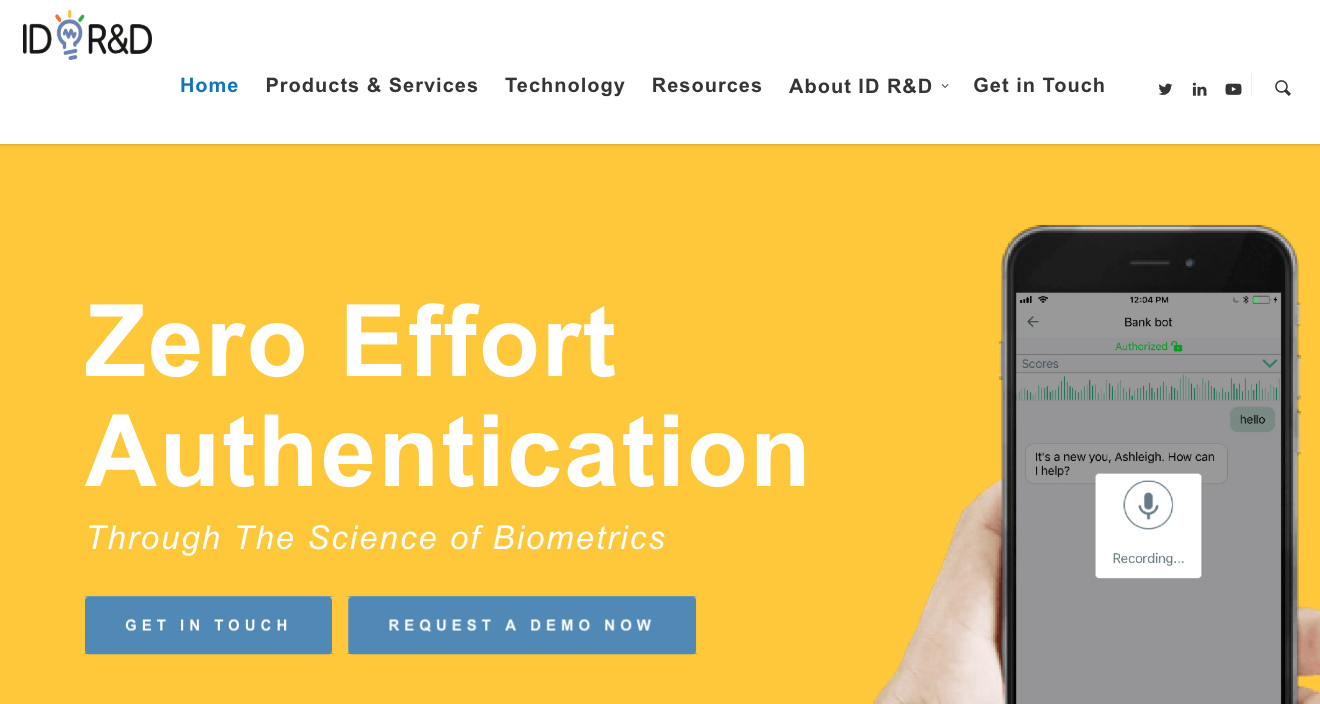

ID R&D’sSafeChat delivers the world’s first zero-effort authentication for mobile and web banking apps, providing the best possible user experience with higher security.

Features

No effort for users to authenticate; simply use the app normally

Multi-modal biometrics provide strong confirmation of identity

Authentication occurs on each transaction, increasing security

Why it’s great Low effort, biometric-based authentication will become the standard for all banking apps.

Presenters

Alexey Khitrov, President Khitrov’s recognition of user frustration and weak security in current authentication processes led him to use his deep experience in biometrics to found ID R&D. LinkedIn

John Amein, VP of Sales Amein has many years of experience in biometrics, contact centers, and telecommunications. He has helped several tech companies grow rapidly. LinkedIn

A look at the companies demoing at FinovateAsia Digital on June 22, 2021. Register today and save your spot.

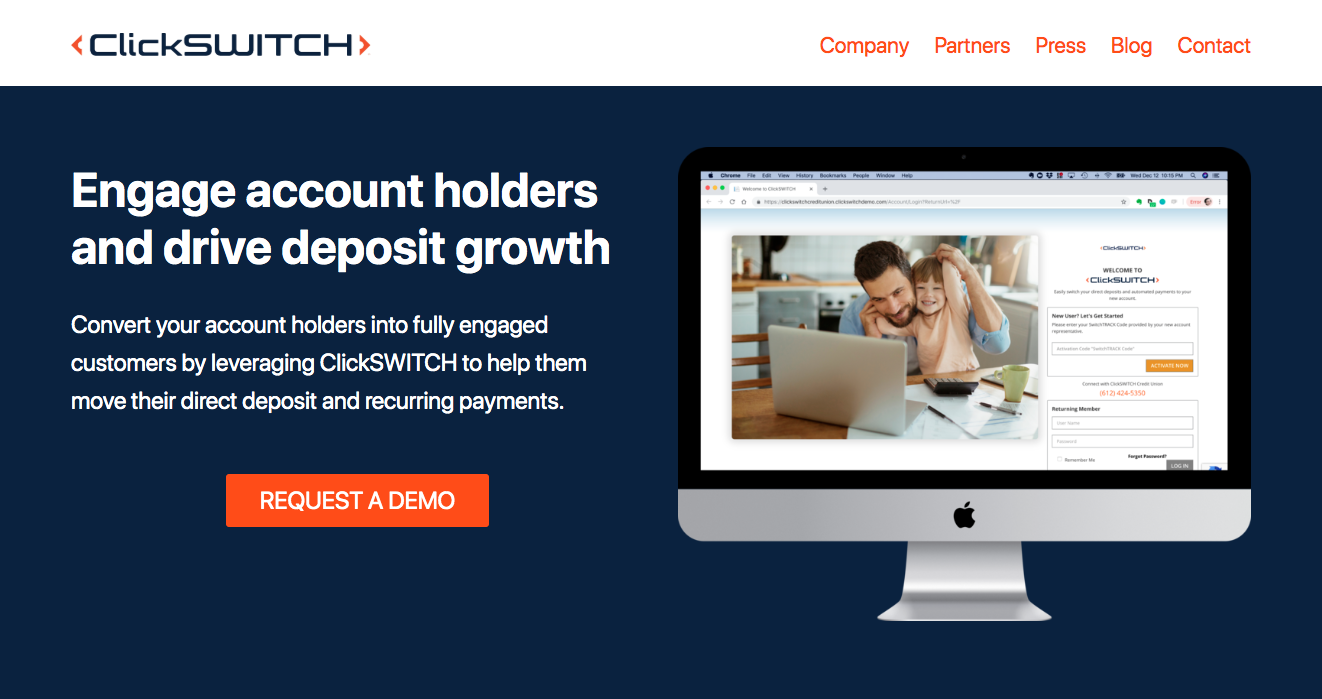

ClickSWITCH is an account acquisition technology for financial institutions and fintechs that automates the process of switching direct deposits and automatic payments.

Features

Automated switch solution for direct deposits and automatic payments

Ability to drive deposits and increase primary account holders

API capability enables you to build and design your own user interface

Why it’s great There’s a war for deposits in financial services. FIs are fighting to be the primary financial provider for their customers. ClickSWITCH can solve these problems by driving deposits and increasing efficiency.

Presenters

Cale Johnston, Founder & CEO Johnston is an entrepreneur who believes banking should be easy. He oversees global business strategy with a focus on innovation, growth, and investor and customer relations. LinkedIn

Adam Pearl, Regional Vice President of Sales Pearl is an experienced, results-driven sales leader specializing in bank technology. He is working out of Chicago with a focus on relationship management and national customer growth. LinkedIn

ACI Worldwide to help Indonesia interbank network ALTO to expand its payment capabilities.

Jack Henry & Associatesunveils its digital account opening solution, JHA OpenAnywhere.

Worldpay to releaseFraudSight machine learning-powered fraud solution.

PAUL UK selectsYoyo to introduce a combined mobile payments and personalized loyalty app to its customers.

Mintrolls out a new app experience for Android users

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

Lendio franchise opens in Erie to expand access to capital for local businesses

InComm’sAlder APIwins award from the Innovative Payments Association.

BioCatch’s behavioral biometrics-based digital identity solution now available on the ForgeRock Marketplace.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

Real estate investment platform Realty Mogulannounced this week that investors have funded more than 300 properties via its platform. The value of the 300 properties adds up to more than $2 billion.

“We are incredibly proud to share that we have now used crowdfunding to finance over 300 properties,” Jilliene Helman, RealtyMogul CEO told GlobeSt.com, which broke the news. “When I started RealtyMogul six years ago, there was a lot of questioning in the general real estate market about the potential impact of crowdfunding. I think this milestone proves that crowdfunding has become a viable source of funding transactions and also that digital investing is here to stay.”

Having 300 projects funded would be a notable achievement for a private equity firm, and is all the more impressive for a fintech. As Helman pointed out, “There are very few private equity firms in real estate that have financed 300 assets.”

Part of Realty Mogul’s strategy focuses on diversification. Sixty percent of the total properties were multi-family properties, many of which have 100 units or more. In fact, Realty Mogul has 17,383 units across its 300 properties, totaling almost 6 million commercial square feet.

Outlining the company’s plans for the future, Helman said, “Our goal is to continue to grow assets under management by investing in high quality commercial real estate where we like the risk-reward calculation.”

Founded in 2013, Realty Mogul has paid out $100 million to its 175,000 investors. The California-based company most recently demoed at FinovateSpring 2014.

Hypepotamus highlightsFeaturespace CEO Martina King, and her thoughts on a diverse workforce.

The WSJ featuresAI Foundry in its look at integrating AI into mortgagetech.

Kony DBX and IDologypartner to offer authentication and ID verification services.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

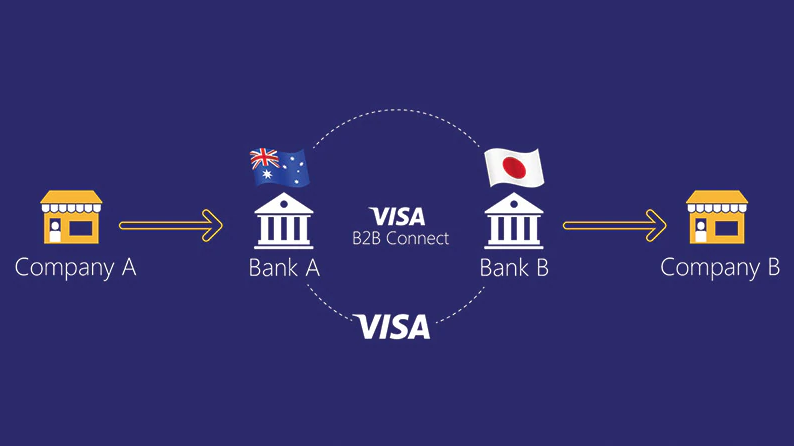

Financial services provider FIS and Visaformed an alliance today. Through the partnership, FIS’ commercial bank clients will have access to Visa’s B2B Connect, a tool that offers a fast and transparent way to process high-value corporate, cross-border payments.

“The combination of FIS’ global customer base and leadership in commercial payments and Visa’s extensive experience as a payment processing network, creates a strong partnership for adding value to the multinational commercial value chain,” said Raja Gopalakrishnan, International Head of Banking and Payments for FIS Global Financial Solutions.

Launched earlier this year, Visa B2B Connect is a suite of APIs that leverages the blockchain to offer banks a business-to-business payment solution. The distributed ledger-based tool facilitates faster transaction times for cross-border and cross-currency payments, reducing transaction times from weeks to one-to-two days.

“Innovation in cross-border B2B payments is long overdue. Visa’s core strategy is to help clients and partners drastically improve their customers’ friction-filled experiences,” said Kevin Phalen, global head of Visa Business Solutions. “We are excited to continue building momentum for Visa B2B Connect and to bring speed, efficiency and transparency to our financial institution clients through our partners, like FIS, who help make transacting on our platform more accessible and seamless.”

FIS most recently demoed at FinovateFall 2016. The company debuted its Cardless Cash solution that provides fast, secure options for sending and picking up cash at any ATM. Headquartered in Florida, FIS’ solutions move $9 trillion each year for 20,000 clients in 130 countries.

Visa demoed at FinovateSpring 2010 and also showcased at our developers conference in 2014. The company has 39 APIs that offer developers tools for commercial payments, data and analytics, identity an security, offers and benefits, payments, and more.

Credit reporting agency and financial health company Equifaxclosed its 19th acquisition this week with the purchase of commercial lending solutions company PayNet. Terms of the deal were not disclosed.

PayNet was founded in 1999 to help commercial lenders make better decisions. The company provides underwriting products for both banks and alternative lenders. Among the solutions offered are growth strategies, risk management, collections solutions, and business intelligence tools.

“I co-founded and ran PayNet with the belief that when commercial lenders are assured of risks, they are more likely to make credit available, unlocking opportunity for small businesses. I believe this aligns perfectly with the Equifax vision,” said Bill Phelan, PayNet president and co-founder. “The combined companies create the premier set of data on the private credit market in the U.S. and Canada.”

In addition to its tools, one of PayNet’s biggest attractions is its data on the commercial lending and leasing market. These two factors will help boost Equifax’s Commercial business, data assets, and analytics capabilities. Together, the companies can fuel client growth in the small and medium commercial business space.

“We are intensely focused on adding unique and valuable data assets to couple with our industry-leading data and analytics capabilities. The PayNet acquisition brings unique and valuable commercial leasing data assets to our leading commercial data assets and insights capabilities to enhance decisioning and access to credit for small and medium-sized businesses,” said Mark W. Begor, Equifax CEO.

PayNet and its employees have joined Equifax’s U.S. Information Solutions business unit.

Today’s deal isn’t the first example of Equifax chasing data. Last year the company acquired DataX, an alternative data provider that helps lenders expand credit access to underbanked populations.

At FinovateFall 2011, Equifax showcased the benefits of the Equifax Complete features of its mobile app. Founded in 1899, Equifax is publicly traded on the NYSE under the ticker EFX. The company’s market capitalization sits at $15 billion.

Ron Shevlin looks at the effects PayActiv’s technology has on the paycheck industry.

Thrive Global interviews Lynne Laube, COO and co-founder of Cardlytics.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

Expense tracking software company Expensify has integrated with Southeast Asia-based ridesharing startup Grab to automate expense tracking and rideshare reimbursement for Grab users.

When they connect their Expensify account to their Grab business profiles, Expensify customers who live in or travel to Singapore, Malaysia, Indonesia, Philippines, Vietnam, Thailand, Myanmar, and Cambodia can automatically create and submit expense reports for their Grab rides. Upon booking rides in Grab’s mobile app, the receipt for the trip is automatically sent to Expensify.

Expensify opted to integrate with Grab because receipt volume for the ridesharing platform grew 200% in 2018. “Business travel has become one of Grab’s priority segments, with more users discovering and using Grab Business Profiles every day,” says Shawn Heng, Regional Head of Business Development and Grab for Business. “Partnering with Expensify, a great app for anyone who needs to keep track of receipts and expenses, is an exciting next step to make business travel even smoother for all of Grab’s customers.”

Grab is not the first ridesharing company Expensify has integrated into its platform. The California-based company integrated with Uber in 2016 and with Lyft in 2017. Today’s deal does, however, mark the company’s first partnership in the Southeast Asia region. Expensify also has partners in the U.S., the U.K., and Australia.

Founded in 2008, Expensify most recently demoed at FinovateSpring 2013, where the company’s CEO David Barrett showed off invoicing technology. The company teamed up with rapper 2 Chainz and actor Adam Scott earlier this year to create a SuperBowl ad. You can check it out below:

Point of sale lending company Financeitteamed up with ServiceTitan this week to help Canadian home service contractors offer their homeowner clients immediate, integrated financing options.

“Alleviating home renovation debt and accelerating the home improvement business is an important focus for Financeit,” said the company’s Founder and CEO Michael Garrity. “Through this partnership, we’re providing ServiceTitan’s Canadian customers an integrated and efficient way to finance any project quickly and hassle free, beneficial to both homeowners and contractors.”

ServiceTitan is an all-in-one software solution for home services businesses such as residential HVAC, plumbing, and electrical. The company’s tools range from client scheduling and service dispatching to accounting, payroll, marketing, and more.

The Financeit integration, which taps Financeit’s payment plans, will help ServiceTitan’s contractor clients close larger deals more easily, as well as sell upgrades and higher-end products.

Financeit made its U.S. debut at FinovateFall 2013 in a joint demo with fellow Finovate alum FIS. In 2017, the company closed an investment round with Goldman Sachs that gave the financier a majority stake in the Toronto-based fintech.

Founded in 2011, Financeit has amassed more than 7,000 merchant partners and processed more than $3 billion (C$3.6 billion) in loan applications. The company has raised $38.4 million.

Financial services democratization company LenddoEFL (a merger of Entrepreneurial Finance Lab and Lenddo) appointed Paolo Montessori as CEO this week. Montessori, who has served as Lenddo’s Chief Operating Officer since 2015, is taking over the role from Richard Eldridge, Lenddo co-founder.

Paolo Montessori

Prior to his work at Lenddo, Montessori was CEO of mobile financial services software developer eServGlobal. In all, he has more than 20 years of multinational experience in financial services, IT, and telecom.

“Paolo has been working closely with me over the last 4 years as COO and has demonstrated all the qualities the organization needs to grow in 2019 and beyond. With his experience in the fintech sector in emerging markets, as a previous CEO of a listed company and his intimate knowledge of LenddoEFL, I am confident that Paolo will take the company to the next level”, said Richard Eldridge, who is staying with the company in a non-executive capacity.

LenddoEFL was formed in 2017 as the result of a merger between psychometric credit scoring company Entrepreneurial Finance Lab (EFL) and alternative credit scoring company Lenddo. EFL showcased its credit scoring tool at FinovateAsia 2012 in Singapore.

Through its efforts to make financial products available to 1 billion people across the globe, LenddoEFL has provided credit scoring and verification to 50+ financial institutions, helping them lend in excess of $2.5 billion to 8+ million people.