This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Retail commerce company Shopify unveiled a slew of announcements this week, one of which caught our eye. The Canada-based fintech joined forces with cryptocurrency payments processor CoinPayments to enable merchants to use crypto payments processing.

When Spotify merchants opt to add CoinPayments to their point of sale, they will be able to accept 1,800 cryptocurrencies. Transacting in cryptocurrencies not only reduce fees for sellers, it will also facilitate cross-border payments, enabling them to increase their global customer base.

CoinPayments was founded in 2013 and has since facilitated more than $5 billion in total transactions. The Cayman Islands-based company’s crypto acceptance platform enables merchants to accept more than 1,900 altcoins and charges 0.5% per transaction, much less than the standard 2% to 3% transaction fee typically charged with debit and credit card transactions.

“The combination of Shopify and CoinPayments is unstoppable in the payments industry,” said CoinPayments CEO Jason Butcher. “By bringing our easy-to-use global crypto payments platform together with Shopify’s extensive merchant base, we look forward to delivering a seamless process for anyone looking to do business using cryptocurrencies. As leaders in ecommerce and crypto payments, our combined expertise reflects the future of business transactions.”

Among Shopify’s other releases this month are:

Shopify Balance, a business bank account, card, and financial management tools

Local Delivery, a tool to help online merchants with local delivery logistics

Shop, a direct-to-consumer app and personal shopping assistant to facilitate purchasing and order tracking

Shopify has also added a handful of products to help merchants struggling in the midst of the COVID-19 pandemic. The company recently added a quick website launch to help brick-and-mortar stores go digital, and also added the option to help merchants collect tips and sell gift cards.

Between extreme wildfires, murder hornets, and the ever-present coronavirus, 2020 has been quite the year so far. Now that the year is almost halfway through, it’s a good time to catch our breath and look at some of the lessons learned.

In some ways, it seems as if we packed decades worth of news, digital developments, and economic losses into the first six months of this year, so there’s a lot to cover. That said, we still have another six months to go before we reach 2021 so there is plenty more room for further changes in the fintech industry.

To help digest what’s happened, we’ve picked up four key things we know for sure now that 2020 is halfway over.

Digital is the new brick-and-mortar

If there is a bright side of the coronavirus for the fintech industry, perhaps it is the positive effect stay-at-home orders have had on firms’ digital initiatives. When consumers aren’t able to conduct banking activities in person, they are pushed to online and mobile channels, even if they have never used digital banking in the past.

For banks that already had a robust digital strategy in place, this has been a time to shine. However, those that were still in the midst of developing and implementing their strategy have found themselves trying to catch up. In this instance, however, they are not catching up with their competitors, they are catching up with the new, online-only status quo.

What we know for sure is that this digital push is here to stay. Forced into the digital channel, consumers have had to adapt to practices they have never done before, such as remote deposit check capture. Now that they’ve experienced the benefits of the digital experience and have adapted their habits, many of these users won’t be visiting their bank branch as frequently.

Economic hardships will persist

Even though stay-at-home orders are being lifted in some areas, Consumers have decreased spending across the board. Whether it is because they have lost income or because they are afraid to leave their home because of the virus doesn’t matter– they are spending less and spending in different areas, which will cause many businesses to go under. In fact, it already has. The Washington Post recently reported that more than 100,000 small businesses have closed their doors forever.

Many have predicted that the worst of economic hardship is yet to come. And in all likelihood we won’t begin to fully recover until there is a vaccine. This means that it remains crucial to focus on supporting the customer. Banks can find even more creative ways to help consumers through their financial hardship and retain communication with them so that they know what to expect. In doing so, they will end up with a stronger consumer relationship on the other side of the crisis. Fintechs, on the other hand, have the opportunity to scoop up new clients who are in need of innovative products such as budgeting tools and services for gig economy workers.

Consolidation has begun

Fintech industry analysts have predicted that the economic side effects of COVID-19 will bring consolidation in the sector. And while some will acquire or become acquired, others will shut down as VC funding constricts. We’ve already seen a bit of M&A activity in the space over the past 6 months, though it is difficult to attribute all of it to the coronavirus.

In one vivid instance, neobank Moven announced in late March that it plans to shutter its B2C business and focus on the B2B side of things. The reason for the bank’s closing, explained founder and CEO Brett King, was that a major round of funding that Moven had in the works fell through. Since Moven’s enterprise business was growing because of the high number of banks making the move to go digital, it made more sense for the company to invest all of its resources into that side of the business.

In the traditional bank space, rumors began to circulate last week that Goldman Sachs is looking to merge with another bank. Among the potential partners are Wells Fargo, PNC, and U.S. Bancorp.

Payments will change for the better

Consumers in the U.S. have been hesitant to adopt a digital payments solution. That is, until now. The pandemic-fueled low-touch economy has both consumers and merchants looking for ways to transact without touching cash, cards, or keypads.

One of the most promising, pre-existing mobile payments technologies for the region is Apple Pay. Adoption for the tap-to-pay technology has been growing since Apple launched it in 2014. Now, six years later, Apple Pay transactions account for 5% of all global card transactions.

At the start of 2020, that 5% figure didn’t seem like bad traction. However, now that almost 100% of consumers are interested in making payments with the fewest number of touch-points, we’ll see hockey-stick growth not only with Apple Pay usage but also with its competitors Samsung Pay, Google Pay, and even peer-to-peer money transfer technologies such as Facebook Pay and Square Cash.

As the gig economy grows, so do opportunities for banks and fintechs.

That’s what’s on the mind of Oxygen, a challenger bank built for freelancers. The San Francisco-based startup, which recently launched its mobile app, is now collaborating with CPI Card Group to create a debit card option for its users.

Oxygen tapped CPI Card Group for its “advanced print design services” in hopes to better connect with its unique target market made up of freelancers, digital natives, and small businesses. At launch, two vertical card designs will be available. Both feature a “clean and crisply-designed” look with back-of-card personalization.

“At Oxygen, we understand that the physical brand experience – including everything from the card design to the packaging appearance – matters for our creative, tech-savvy clientele. With CPI’s cost-effective scale and design strengths, we were able to deliver a sleek card to customers in a unique, memorable fashion,” said Oxygen Founder and CEO Hussein Ahmed. “We are pleased to have such a reliable secure card provider and are thrilled to offer customers an eye-catching debit card that echoes their drive, ambition and lifestyle.”

Oxygen was founded in 2018 and caters to the growing set of customers that rely on gig work and multiple income streams to pay their bills. The challenger bank offers both personal and business accounts with features including cash-back rewards and virtual cards for personal accounts, as well as accounting tools and the ability to mail checks from within the app for business accounts. Both accounts boast no monthly fees.

Along with its digital capabilities and creative branding, Oxygen differentiates itself with a lending product that works for the self-employed workforce with fluctuating income. Instead of relying on job stability and credit scores to underwrite loans, Oxygen instead looks at a borrower’s historical cashflow to assess risk and repayment capability.

Oxygen and other challenger banks such as Wollit and Xolo are among the growing number of players eager to serve the gig economy. These customers have traditionally been ignored by larger traditional financial institutions, which haven’t seen the value in serving clients with unpredictable income. This may change in a post-coronavirus economy, however, as more of the population earns their paycheck with freelance work rather than a full-time job.

Since the dawn of APIs, the U.S. has struggled to create a consistent open banking approach. Banks and fintechs have battled with each other on screen scraping, customer data, and open access to third party providers.

Banking technology company Plaidannounced a new launch today to solve this struggle and unite banks, fintechs, and consumers. The new tool, Plaid Exchange, offers banks a way to provide open banking connectivity to their clients while keeping their clients’ data safe and giving them control of their data.

Plaid Exchange helps banks establish token-based API connectivity with the 2,600 third party apps in Plaid’s network. This single connection simplifies integration for banks, helping their clients connect with more third party providers securely. Additionally, the API helps banks build a control center that empowers their customers to manage which third parties they share their data with.

To help banks with legacy systems, Plaid is working closely with integration partners to ease the transition. The company’s partners in this effort include Kunai and Core10.

“We believe APIs are the future of open finance, and we want to make it as easy as possible for all financial institutions to incorporate APIs into their broader digital transformation agendas regardless of budget size and resources,” said Plaid Product Lead Niko Karvounis in a blog post.

Plaid Exchange can help banks bring an API solution to market in 12 weeks. The company is already working with financial institutions for Plaid Exchange and expects to partner with even more as banks seek to meet increased customer demand for digital services in the post-COVID-19 era.

Mobile financial services provider and financial inclusion company Wave Money is receiving a boost today from Alipay parent Ant Financial. In an agreement announced, Ant Financial disclosed plans to invest $73.5 million in Wave Money, bringing the company’s total funding to $92.9 million.

The move will position Ant Financial as a substantial minority stakeholder in Wave Money, which is a joint venture between existing stakeholders Telenor and Yoma Bank.

Wave Money is headquartered in Myanmar and seeks to drive financial inclusion across the country. The company operates 57,000 Wave shops located in 295 out of 330 townships nationwide, covering approximately 89% of the country. In all, more than 21 million people have used Wave Money’s services, including Wave Pay, which is used for remittances, utility payments, airtime top-ups, and digital payments.

On the strategic side of the investment, Wave Money will tap Ant Financial’s expertise in mobile payments to help build out its digital capabilities and enhance its user experience.

“Myanmar’s population is still massively underserved by formal banking institutions with only a quarter of people having a bank account,” said Yoma Strategic CEO Melvyn Pun. “Ant Group brings a wealth of expertise in mobile payment and financial services. The covid-19 situation is accelerating the trend towards a cashless society and drives the growth of ecommerce, and we expect this strategic partnership to massively boost Wave Money’s capabilities to support these trends.”

The investment comes amid a time of growth for Wave Money. Last year the company’s transfer volume more than tripled year-on-year to $4.3 billion. During the same period, Wave Money’s revenue and transaction numbers also tripled. Additionally, the number of monthly active users for Wave Pay have increased 14% per month since the service launched in 2018.

The following is a guest post written by Josephine Jacobs, writer at Academicbrits.com and PhdKingdom.com and an executive coach and organizational consultant.

As we move into an unprecedented

era of remote working (or rather, working from home!), companies and employees

need to consider how to protect sensitive data. Several security considerations

must be explored. Employees working from home will have access to work systems

without the protections an office brings – they will be using different IT

infrastructure, bandwidths and Wi-Fi connections that may not be secure. This

all brings an element of danger to your company’s data – as your employees

access your database or databases remotely, the risk to that data grows.

Usually the risk is only between the server, internal network and end user

machine. External working adds the risks of public internet connections, local

networks and consumer-grade security systems.

Here are some of the best ways to

protect your data whilst your employees work from home.

Tutor your Employees in Data

Protection and Computer Security

“It’s worth giving your employees

a basic training on how to stay safe online and digitally,” says Joey Garcia, a

tech writer at 1Day2Write and NextCoursework. “This can include

warning them about phishing emails, avoiding public Wi-Fi, securing home Wi-Fi

routers and verifying the security of devices they use for work. Remind

employees not to click links in emails from people they don’t know, not to

install third-party apps, and to be aware that hacking and phishing attacks

will increase during the quarantine period.”

Create an Emergency Response

Team

Whilst teaching your employees

some basic computer security is a useful preventative measure, you need an

emergency response team for the unfortunate event of your data being

compromised. Ensure this team can be contacted by everyone in the company and

everyone knows exactly what to do in the event of a cyber-attack.

Provide your Employees a VPN

Using a VPN (virtual private

network) is a good way to ensure data remains secure. A VPN provides more

security by hiding the user’s IP address, encrypting data as it is transferred,

and masking the user’s location. Most companies use some sort of VPN already –

all you need to do is expand it to all of your employees as they work from home

and allow them to use it for all business-related activity.

Security Software

Provide your employees with the

best security protection on all of their devices – this can be anti-virus

software, firewalls, and device encryption.

“Have a look at the best security

software for Macs or Windows, depending on what devices your company employees

use,” says Melisa Cueva, data analyst at Australia2Write

and Britstudent. “Norton Anti-Virus

consistently ranks highly, but there are many other options out there.”

Password Audits

It’s a good idea to have your

employees regularly change their passwords, and to teach them how to make the

best passwords. Perform an audit and ensure all passwords meet a strict

security police: alphanumeric codes are much better than names or dates that

are easily guessed. Two-factor authentication should be put in place as a

mandatory procedure.

Update all Software

Windows and Apple Mac’s have

their own useful security measures in place to protect devices from attacks.

Ensuring all updates are completed and software is at its latest version can

also prevent devices from attacks. Ask your employees to check their computers

and phones are up to date and activate automatic updating on all devices.

Don’t Store Information

Locally

You can instead store information

on the cloud, using services like Google Drive or Microsoft Office 365 Online.

This also includes avoiding the use of USB sticks, as these devices can be

infested with malware. Content should be stored on cloud-based software

wherever possible, and employees should use cloud-based apps, too. Locally

stored information means it is stored on a physical disk, like the hard drive

of a computer. Cloud software is great because you can backup all data here,

too.

Backups

In case of any need to reset and

wipe devices of viruses, encourage your employees to back up all their data –

whether that’s on the cloud, or to local storage (but this isn’t recommended

for reasons mentioned above!).

Josephine Jacobs is a writer at Academicbrits.com and PhdKingdom.com, an executive coach and organizational consultant with more than 10 years of experience enhancing the performance of individual executives, teams and organizations. Her background encompasses a wide range of programs and initiatives for individual development, team building, organization design, and facilitation. She also writes for Essay Help Service.

Across the globe, many people have shifted their attention to focus on two things: their health and their finances. Fintech companies have stepped up in recent weeks to help citizens with the latter. In fact, many are seeing record app downloads, usage, logins, and a surge of new users.

eToro is one such fintech. In fact, the U.K.-based company recently announced it has now reached 13 million active users. This milestone comes in part thanks to the comparatively large number of new users that have registered in the first quarter of this year. eToro saw more than a fourfold increase in the number of new users in the first quarter of 2020 than it saw in the first quarter of 2019.

“Coronavirus induced market volatility has been a focus for media globally and has brought the topic of investing increasingly onto people’s radars,” said eToro CEO Yoni Assia. “We have seen a large increase in trading volumes on eToro since the start of 2020 from both new and existing users.”

Activity on the stock-trading platform has also ramped up this year, with stock trading transactions increasing by 3x since January 1. Much of this activity can be attributed to the fact that eToro launched commission-free stock investing for its Europe-based users in May.

As for what’s next, eToro said it plans to expand its commission-free stock investing to users in the U.S. and Asia Pacific regions later this year. The company also noted that it plans to ramp up its acquisitions to keep up with customer demand.

EToro is, by all accounts, in the middle of a growth spurt. In addition to its boosted user numbers and acquisition plans, the company is also in the middle of a hiring spree. It is currently seeking to fill 60+ job vacancies at a time when many fintechs are laying off or furloughing their staff.

With ongoing stay-at-home orders in place due to COVID-19, companies of all sizes across many industries have had to find a way to take their operations into the digital realm. So while digital transformation had previously been on financial services firms’ radars, it has quickly evolved into a priority.

Bajaj Allianz has experienced particular success with its digital transformation efforts. To get some insight into best practices, we caught up with KV Dipu, President – Head Operations, Customer Service & Communities of Bajaj Allianz.

Many firms have recently had to fast-track their digital transformation efforts. What is your advice to ensure a smooth transition?

KV Dipu: The key is to move from the classic two-speed approach to a big bang approach. Since the accelerator (CEO, CXO or COVID-19 – no prizes for guessing!) for digital transformation is obvious, the most effective starting point is the touch point which generates maximum friction in terms of process performance vs. customer feedback. Secondly, transformation efforts follow use cases, not the other way around. Only when business owners own use cases do transformation efforts bear fruit! Thirdly, look for early wins to create competitive fervor across departments.

Disproportionate awards for early birds can help propel the lagging units forward. Fourthly, since deployment and adoption are entirely different buckets of fish, a strong reward program for fast adoption helps. Lastly, agility – defined here as the ability to recalibrate one’s approach with amoebic speed- in an era when the situation is changing by the day is important to carry the transformation through!

Bajaj Allianz has success in collecting and digitizing data with IoT-based devices. Talk to us about this initiative.

KV Dipu: Charles Darwin said, “It is the long history of humankind that those who learned to collaborate and improvise most effectively have prevailed.”

At Bajaj Allianz, we strongly focus on collaboration and 100% adherence to regulatory compliance when initiating IoT projects. DriveSmart, our IoT-based telematics program, offers five unique benefits to customers: driving optimization, geofencing, 24/7 road assistance, social integration, and gamification. Some of these benefits are possible only through IoT. For instance, geofencing lets you know if the car strays off the beaten path! Similarly, social integration lets you know if a friend is on the route to your weekend destination!

Likewise, when we launched our “connected school” initiative which included an IoT-enabled solution combining safety, security, as well as insurance coverage for school students, we addressed parents’ worries around school travel. We tracked children using RFID cards and geofenced their travel routes to ensure maximum safety.

Do you have other IoT device projects in the works?

KV Dipu: We have also leveraged IoT to digitize our health insurance medical check-up process. It is now automated and paperless end–to-end; we even won the Celent Model Insurer 2020 Award for the same!

What other tools have you relied on to enhance digital operations?

KV Dipu: We have deployed an array of tools to enhance digital operations. For starters, we walked the talk on blockchain when we deployed it in the area of claim settlement for international travel insurance. In case your flight is delayed beyond the terms and conditions in the policy, you don’t even need to notify us of the claim! Once you submit your documents, we get to know of the flight delay and can send you the amount even when you are still in the airport. Similarly, our bot leverages AI to offer 24/7 assistance via the website, Whatsapp, and even Alexa! We have also deployed robotic process automation (RPA) to automate a range of activities in the back office.

One of the most difficult aspects to digitize can be tools that rely heavily on collaboration and communication. What was your experience in making communication digital?

KV Dipu: We have had a wonderful experience making our communication digital! Our motto during the current phase of social distancing was to stay digitally connected with our employees, customers, and partners while being physically distanced. With our employees and partners, work from home became an opportunity to bond from home by celebrating virtual birthday parties and organizing painting, cooking, and singing team activities using digital collaboration tools. With customers, digitizing communication involved a shift from the call centre to digital servicing tools such as Whatsapp, bots, website, app, and portal.

We also leveraged social media to connect with customers. The highlight was digital launches of new products! In fact, based on recent engagement levels, we scored the highest brand engagement rate in the insurance industry! Since we continuously engaged our customers using email, SMS, and digital platforms and enabled transactions on digital assets, our customer satisfaction scores actually improved!

How are you balancing the need to keep things as stable as possible for customers and employees during an uncertain time with the need to drive digital change?

KV Dipu: Communication is the key when trying to perform a balancing act between stability for the present and digital change for the future. We embarked on a multi-modal communication exercise, informing customers that we are just a call or click away. With employees, we propelled our home-grown engagement program christened “Celebrating You” with a strong focus on four fulcrums: fun at work, digital learning, virtual town halls, and videos and podcasts for mental health and physical workout tips.

Digital change gets established as customers experience the ease and convenience of digital assets. Work from home, for instance, given the win-win for both – employees save on commutes to work, firms save on expensive real estate – is likely to be a permanent feature. Similarly bots, Whatsapp, portals, and websites with 1-click features are here to stay. Tomorrow’s organization chart may well show a manager leading a team of both humans and machines!

Behavioral analytics technology provider Featurespaceannounced today that it closed a $37.4 million (£30 million) round of funding.

The round, which brings Featurespace’s total funding to $108.6 million, was led by Merian Chrysalis Investment Company Limited with additional contributions from existing investors.

“During these challenging times, our machine learning models have automatically adapted to the shift in consumer, business and criminal behavior,” said Featurespace CEO Martina King. “It is our continued focus to deliver industry-leading, fraud and anti-money laundering solutions to our customers and partners.”

Featurespace will use the funding to “support continued growth” of its financial crime detection technology. The company launched its adaptive behavioral analytics platform, the ARIC Risk Hub, in 2008. The ARIC Risk Hub helps organizations fight financial crime by leveraging machine learning and anomaly detection to flag suspicious activity in real time.

The company has more than 30 major bank clients including four of the five largest banks in the U.K. Among Featurespaces customers are HSBC, TSYS, Worldpay, RBS NatWest Group, Danske Bank, ClearBank, and more.

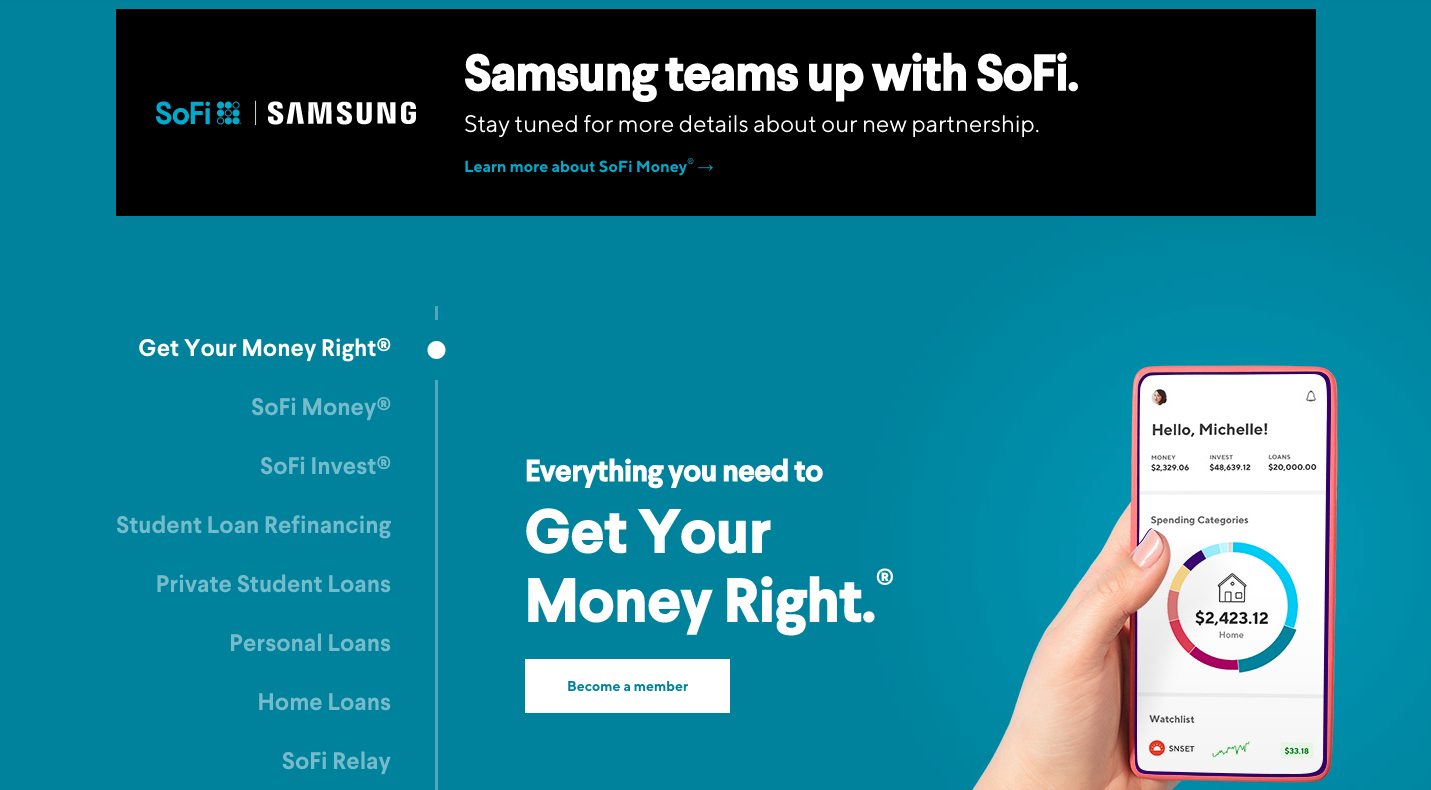

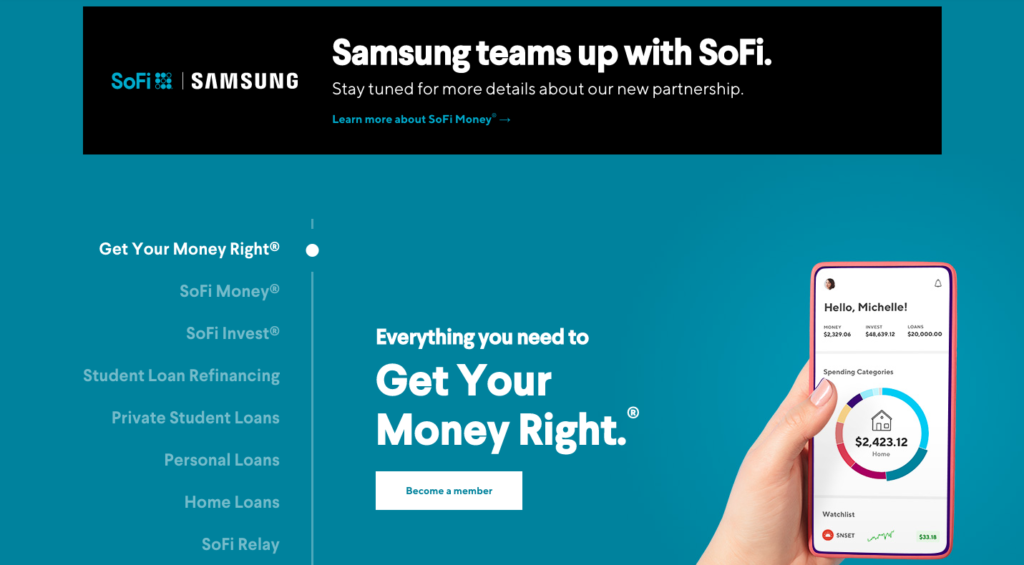

Alternative finance solutions provider SoFi and Samsung’s Samsung Pay joined forces this week to launch a debit card.

The two have spent the last year collaborating to make a mobile-first money management platform with its own debit card and cash management account.

The initiative is part of Samsung’s broader Samsung Pay mobile payments platform that the company launched in 2015. Samsung’s mobile payments platform uses built-in magnetic secure transmission technology (MST) and NFC functionality to enable users to make contactless payments.

“Our vision is to help consumers better manage their money so that they can achieve their dreams and goals,” said Sang Ahn, Vice President and GM of Samsung Pay, North America Service Business, Samsung Electronics in a blog post. “Now more than ever, mobile financial services and money management tools will play an even bigger role in our daily lives while also opening up new possibilities.”

Specific details about the card are still pending.

The new debit card offering will provide Samsung with a unique way to compete with Apple’s Apple credit card. Compared to Apple’s credit card, however, Samsung’s debit card product sounds more sticky. That’s because budgeting and cash management features built into the app will encourage users to spend more time in Samsung’s app and will keep the company’s debit card– along with its mobile payments service– top-of-mind for consumers.

Samsung’s announcement also comes shortly after news leaked that Google has its own debit card in the works. The debit card will work in conjunction with the Google Pay app.

Samsung’s timing on the launch is fairly ideal, despite the global economic crisis. The coronavirus has turned consumers’ attention toward their finances. Because of this, many banks are seeing record downloads of and engagement with their mobile banking tools. This shift to digital, combined with the new low-touch economy when it comes to everyday payments, provides an ideal environment to launch a contactless payment option.

Despite these conditions, the challenger banking space is becoming increasingly crowded in the U.S. However, Samsung’s choice to partner with an existing player instead of creating a product from scratch is a favorable one.

Fraud prevention solutions provider Emailage recently announced it has been acquired. LexisNexis Risk Solutions, owned by parent company RELX, closed the deal for $480 million.

Emailage was founded in 2012 by Rajesh Pandey and Rei Carvalho. The company offers an email risk score that uses email address metadata to help businesses assess transactional risk and validate digital identities. Access to this data enables companies to expedite approvals, prevent chargebacks, and automate workflows. Emailage also offers a Digital Identity score that layers in additional data to offer businesses a fuller picture of the user’s online reputation.

LexisNexis Risk Solutions purchased Emailage to integrate the company’s email assessment capabilities into its Digital Identity Network offerings. The integration should be somewhat smooth since the two had an existing commercial partnership prior to the acquisition.

“This acquisition is a natural fit as LexisNexis Risk Solutions and Emailage are both committed to continuously evolving our solutions to combat fraud,” said LexisNexis Risk Solutions Business Services CEO Rick Trainor. “This acquisition will enhance and expand our email data intelligence to provide our customers a more comprehensive view of risk with minimal friction for their customers.”

This isn’t the first fintech RELX has snapped up to boost its fraud and risk management services. The firm has been making a steady stream of purchases in the sector, including ID Analytics, ThreatMetrix, Accuity, and ChoicePoint. RELX has also formed numerous partnerships in the space, including with BioCatch and Blockbid.

LexisNexis Risk Solutions initiated its purchase of Emailage before COVID-19 had overtaken the globe. However, the increased interest in security players is something we can expect to see more of as the virus steers us toward the low-touch economy and drives traditionally brick-and-mortar services into the digital realm.

With so much uncertainty these days, it’s nice to have something to be sure about. One thing we’re sure about is that our new digital format for FinovateAsia is going to rival the in-person version.

That’s right — FinovateAsia 2020 is now a completely digital event called FinovateAsia Digital. Given health concerns around COVID-19, running the event digitally ensures the safety of our attendees, speakers, and sponsors. It also enables attendees outside of Southeast Asia to participate, bringing more (and more diverse) opinions and perspectives to the event.

What will FinovateAsia Digital look like?

Extended dates The number of sessions will remain the same, and we will still feature all 100 of the original speakers of the event. The schedule, however, will be adjusted to make it easier for people to participate remotely. Instead of a two-day fintech immersion, everything will be spread out across five days. That means the event will now take place July 6 through July 10. With this extension, the content will be shorter each day and more manageable for digital participants.

Time zone The event will run on Singapore Time. The online agenda has been updated to reflect the new schedule so that you can see exactly what’s on when.

Engagement The digital nature of the event will make it even easier for individuals to interact with speakers. Attendees will be able to engage with the event in real-time, through Q&A with speakers, audience polling, and chat features.

Networking Making personal connections is one of the most valuable elements of an event, so we’ve worked hard to preserve it! To make sure everyone has ample time to connect with their fellow attendees, our networking app will run across all five days, helping you find and engage with others. All meetings will take place virtually via video call. To accommodate multiple time zones, the networking app will allow meetings to be scheduled 24 hours across all time zones.

Come join in the experience! If you previously booked your ticket, our customer service team has been in contact with you regarding details. If you have any questions, please reach out to [email protected].