This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

The demos are done. The votes have been counted. And the people have spoken. After two days of live fintech demos here at FinovateSpring 2024, we are proud to introduce the winners of Best of Show.

Bloom Credit for its technology that helps banks and credit unions offer a deposit retention and credit building tool to their client base.

Cascading AI for its platform that improves efficiency in banks by 30x by automating rote tasks, enabling banks to leverage that step-change in efficiency to grow their top and bottom lines.

Kobalt Labs for its solution that helps fintechs and financial institutions accelerate and strengthen their third-party diligence, leading to faster and safer paths to revenue-generating partnerships and operational efficiency that doesn’t increase headcount.

QuickFi for its technology that enables banks and manufacturers to give their business customers a fully digital, self-service finance experience that’s fast, intuitive, and consistent with how modern business borrowers prefer to do business.

Remynt for its platform that helps creditors achieve higher recoveries and recapture defaulted consumers as customers when their financial position improves.

SAVVI AI for its solution that helps financial services companies step into the age of AI, with faster, more accurate forecasting, without changing their workflow or processes and using their existing teams.

A heartfelt thanks to all of our demoing companies for sharing their latest fintech innovations with our FinovateSpring audience. Be sure to check out the Finovate Podcast featuring Greg Palmer in the weeks to come as he interviews FinovateSpring 2024’s Best of Show winners.

Notes on methodology:

1. Only audience members NOT associated with demoing companies were eligible to vote. Finovate employees did not vote.

2. Attendees were encouraged to note their favorites during each day. At the end of the last demo, they chose their three favorites.

3. The exact written instructions given to attendees: “Please rate (the companies) on the basis of demo quality and potential impact of the innovation demoed.”

4. The six companies appearing on the highest percentage of submitted ballots were named “Best of Show.”

5. Go here for a list of previous Best of Show winners through 2014. Best of Show winners from our 2015 through 2024 conferences are below:

This week, Finovate Global looks at recent fintech developments in France.

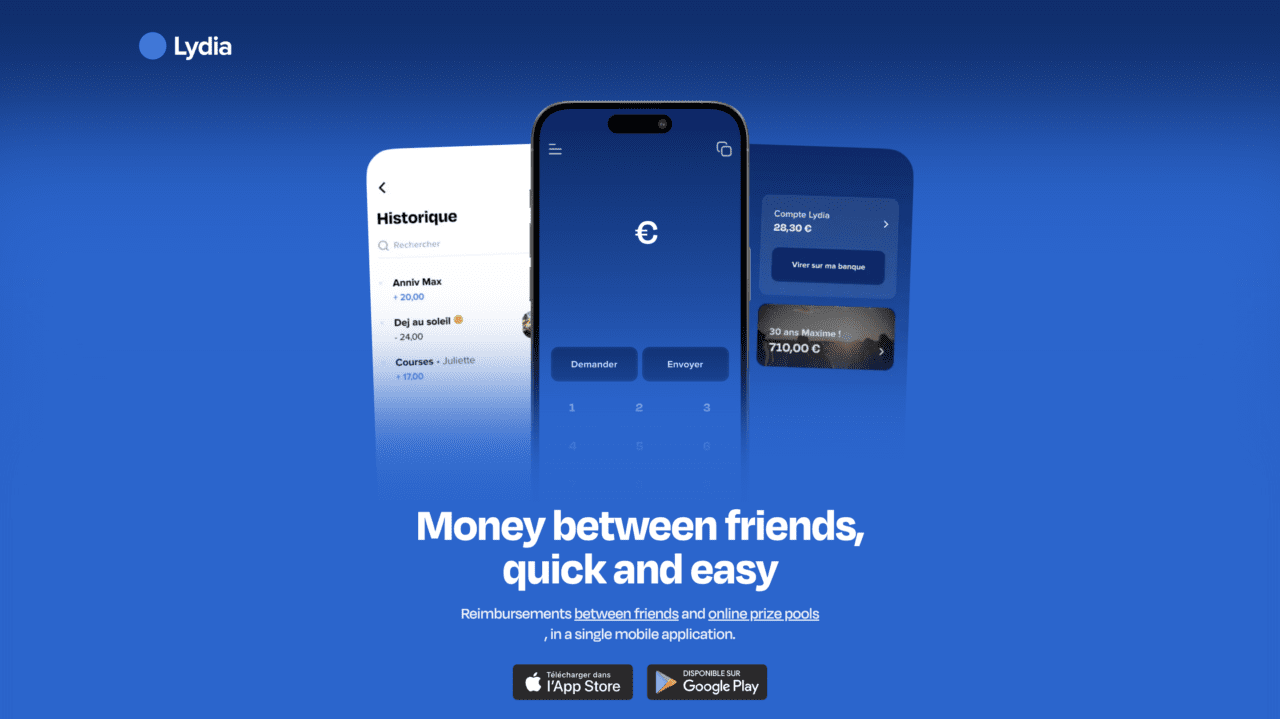

French start-up Lydiaannounced the launch of a new digital banking brand this week. Named Sumeria, Lydia plans to invest more than €100 million in the new initiative, as well as hire 400 people over the next three years. Sumeria, according to a post on LinkedIn, offers 4% interest and is designed to be a “simple and accessible banking super app.

“We are convinced that technology (cloud, mobile) is not an end in itself, but a way to simplify life, through everyday details,” the company noted in a statement on its website. Arguing that current accounts should be neither “trendy gadgets” nor make users captive to a given app, system, or institution, the company explained: “It should solve a real problem. This is why Lydia’s choices, with Sumeria, are motivated by common sense and its ambition to be universal: for everyone, for everything.”

Lydia’s brand announcement follows a decision by the company to split its digital banking app into two components. Originally launched in 2013 as a P2P payments app, Lydia’s solution scaled, adding more and more financial services features over the years. It was the launch of its Lydia Accounts offering convinced the company that a change was necessary to keep its early adopters – who relied heavily on the P2P service – onboard. The result was to offer the P2P services separately from Lydia’s digital banking proposition through the Lydia Accounts app. The original Lydia app will become Sumeria, with the new features mentioned above – such as stock trading, savings accounts and loans – to be ported to the new banking brand.

Headquartered in Paris, Lydia has raised more than $259 million in funding. The company’s investors include Accel and Echo Street Capital. In addition to the launch of Sumeria, Lydia is also seeking a credit institution license from the French Prudential Supervision and Resolution Authority.

Paris, France-based private wealth management startup RockFiraised €3 million in funding this week. The round was led by Varsity I and featured the participation of numerous business angels in technology and private management. The company plans to use the capital to grow its workforce by 3x by the end of 2024 so as to provide private banking and wealth management expertise to clients throughout France.

“Since the beginning of the year, we have seen strong client traction eager for a new model to manage their wealth,” RockFi Co-Founder and CEO Pierre Marin said. “With a market of €4.8 trillionin assets ahead of us and no tech leader yet in France and Europe, our ambition is very high for the coming years.”

RockFi’s model combines human expertise and technology to offer services including banking, wealth management, life insurance, and pension savings. The firm has a targetable clientele with assets of more than €100,000, representing six million households in France.

“Three months after our official launch this is an important step that anchors a strong momentum and allows us to further accelerate the construction of the new private management,” the company wrote on its LinkedIn page this week. “The ambition remains: to surround ourselves with the best talent and partners in each field and to deploy a tech ecosystem to unleash the potential of independent wealth managers at the service of their clients.”

Meet Finovate’s French Alums!

Over the years, Finovate has been proud to showcase a number of fintech innovators based in France. Here’s a look at some of French fintechs that have demoed their technology on the Finovate stage in recent years.

Digital identity verification innovator Socure announced a partnership with identity-secured transactions company Proof.

The partnership will combine Proof’s Defend solution with Socure’s Sigma Fraud suite to help companies fight fraud and forgery in authorizations, agreements, contracts, and forms.

Founded in 2012, Socure made its Finovate debut the following year at FinovateFall in New York.

A new partnership between digital identity verification innovator Socure and identity-secured transactions company Proof will bring new tools to the fight against fraud and forgery in authorizations, contracts, and forms.

“With the explosion of new fraud vectors, our mission at Socure remains steadfast: use AI to deliver the most accurate anti-fraud and identity verification solutions in the industry,” Socure Founder and CEO Johnny Ayers said. “Partnering with Proof allows us to uniquely ensure identity-assured transactions for contracts, authorizations, forms, and high-risk financial events across various sectors.”

While there is widespread understanding about threats like money laundering that cost businesses $18 billion every year, the challenge from document fraud is significantly greater. A 2021 report from FINCEN revealed that false records and forgery are responsible for more than $45 billion in fraud activity annually. Fraudsters also have become more effective at leveraging AI to deploy deepfakes, synthetic identities, and – in the case of document fraud – falsified records.

The partnership will blend the strengths of Proof’s Defend solution with Socure’s Sigma Fraud suite. Defend leverages 100+ behavioral, fraud risk signals to detect fraud in online customer interactions. Businesses get a risk score for every transaction that highlights any fraud issues behind the authorization, signature, notarization, or identity verification.

Sigma Fraud analyzes historic behavioral patterns across channels to spot anomalies that may indicate fraudulent activity at the identity level. The suite also is backed by consortium data from the Socure Risk Insights Network, which draws from nearly 2,400 customers from the country’s largest banks, fintechs, payment platforms, and payroll providers.

“Adding Socure’s digital identity verification capabilities to Defend, our fraud detection and prevention product, allows customers to secure transactions at every stage, quickly and accurately,” Proof CEO Pat Kinsel said. “We can’t think of a better partner and are excited to introduce Socure to Defend clients.”

Founded in 2012, Socure made its Finovate debut at FinovateFall a year later. Most recently demoing its technology on the Finovate stage in 2017, Socure has since grown into a leader in digital identity verification with more than 2,300 customers. Last month, the company unveiled its new global watchlist screening and monitoring tool. The solution gives financial institutions the ability to screen, monitor, and assess new and existing customers against the Office of Foreign Assets Control (OFAC) sanction lists and politically exposed persons (PEP) databases, adverse media, and custom watchlists.

Socure began the year announcing a pair of new partnerships. In January, the company reported that auto finance company Exeter Finance would deploy the Socure ID+ platform to onboard new customers. In February, Socure teamed up with fellow Finovate alum Trustly to offer a Pay-by-Bank solution with streamlined onboarding.

Identity verification solutions provider Data Zoo secured $22.7 million (AU$35 million) in Series A funding in a round led by Ellerston JAADE.

Data Zoo will use the capital to help foster broader adoption of its identity verification technology.

Headquartered in Sydney, New South Wales, Australia, Data Zoo was founded in 2011. Charlie Minutella is CEO.

International identity verification solutions provider Data Zoohas secured $22.7 million (AU$35 million) in Series A funding. The round was led by Ellerston JAADE, an Ellerston Capital fund; Data Zoo will use the capital to help drive broader adoption of its identity verification technology.

“There’s been a long-standing need for a more efficient and secure way to verify identities,” Data Zoo Founder and Chairman Tony Fitzgibbon said. “Data Zoo has spent years refining its solution – the result has been incredible innovation, UX optimization, and growth in a fiercely competitive market, putting us head-to-head with today’s most established identity providers.”

Data Zoo leverages direct access to authoritative data from more than 170 countries and advanced, logic-driven data sequencing to help institutions automatically verify identities based on the next best source. The company’s technology reduces dropout rates, lowers the total cost of ownership, and helps businesses boost customer approval rates and revenue realization. At the same time, Data Zoo prioritizes data protection and privacy by eliminating identity data storage.

Founded in 2011, Data Zoo is headquartered in Sydney, New South Wales, Australia. The company includes eToro, MoneyGram, and Experian among its partners, and competes in a crowded field of innovators including a number of Finovate alums such as Socure and Jumio. Earlier this year, Data Zoo announced the appointment of former London Stock Exchange executive Charlie Minutella as its new CEO. In a statement, Minutella spoke about the expansion opportunities this week’s investment will enable the company to pursue.

“Data Zoo is well-positioned to expand its footprint because of its patented ability to efficiently onboard a more diverse and global set of customers, meet compliance standards across jurisdictions, and enhance data privacy and protection,” Minutella said. “The investment from Ellerston JAADE will supercharge our capacity to operate in key markets, attract new business, and enter new strategic partnerships.”

For more coverage of fintech innovation around the world, check out our Finovate Global column published every Friday afternoon.

May is Asian-American and Pacific Islander Heritage month. And with FinovateSpring less than a week away, we wanted to take a moment to celebrate the Asian-American fintech innovators who will be demonstrating their latest technologies on the Finovate stage live in San Francisco, California on May 21 through 23.

Tickets for FinovateSpring are still available. Visit our registration page today and save your spot. We look forward to seeing you in San Francisco!

A former engineer at Dialpad, Dropbox, and Flexport, Ng is CEO and Co-Founder of Anvil. He is also a graduate of the University of Michigan and an alum of the Y Combinator Startup School Online.

Headquartered in San Francisco, California, Anvil was founded in 2018.

With experience in angel investments at 79 Studios, as a venture partner at Resolute, and a former I-banker at Chanin & CSFB, Saujin Yi is founder and CEO of LiquidTrust. Yi is a graduate of MIT and earned her MBA from UCLA Anderson, where she is a lecturer.

LiquidTrust was founded in 2019. The company is headquartered in Los Angeles, California.

A Venture Partner at JAZZ, Lin seeks to make everyone become “bionic” when it comes to investment research and analysis. Founder and CEO of Revelata, Lin is a graduate of Harvard University, earning his A.B. in Biochemical Sciences, as well as his S.M. and Ph.D. in Computer Science, at the institution.

Headquartered in Palo Alto, California, Revelata was founded in 2020.

Former Head of Operations for Juno Finance and Ownit, Chao is Co-Founder and Chief Operating Officer with Tennis Finance. Chao earned a B.A. in Economics and Psychology at University of California, Los Angeles.

San Francisco, California-based Tennis Finance was founded in 2022.

Financial crime compliance company Napier AI has partnered with Romania’s Salt Bank.

Salt Bank will deploy Napier AI’s transaction screening solution to protect transactions against a variety of fraud risks.

Napier AI made its Finovate debut at FinovateEurope 2018 in London.

Romania’s first neobank, Salt Bank, has teamed up with financial crime compliance company Napier AI. Salt Bank will deploy Napier AI’s Transaction Screening solution to ensure that the hundreds of millions of transactions Salt Bank handles are safe from fraud risks.

“We chose the Napier AI platform because it offered NextGen technology which enables us to strengthen our financial crime controls and matches our drive to offer clients a seamless digital experience, within a robust regulatory environment,” Salt Bank CEO Gabriela Nistor said.

Salt Bank sought out Napier AI’s technology to ensure that it is able to keep pace with evolving money laundering, terrorist financing, and fraud risks on the one hand, and consumer demand for a seamless digital experience on the other. Napier AI’s Transaction Screening product features a user friendly interface with customizable workflows, a cloud-based deployment, a sandbox environment for optimizing screening configurations, and a configurable dashboard with no-code rule building and AI insights.

“Napier AI’s industry-leading Transaction Screening solution is set to help Salt Bank succeed in setting a new standard for banking in Romania,” Napier AI CEO Greg Watson said. “It is an exciting time for the industry and market, and I am excited to see how we work together to bring best-in-class financial crime compliance to the next generation of digital banking users.”

Founded in 2015 and headquartered in London, U.K., Napier made its Finovate debut at FinovateEurope in 2018. At the conference, the company demoed its Customer Screening and Transaction Monitoring Enhancement software. By addressing gaps in current legacy systems’ AML and client screening solutions – and extending their shelf life – Napier’s technology enables organizations to enhance the performance of their current fraud prevention processes.

Napier AI’s partnership news comes one month after the company teamed up with impact asset manager Finance in Motion. Finance in Motion will deploy Napier AI Continuum – including its Client Screening solution and Client Risk Assessment module – as its AML and counter terrorist financing platform. Earlier this year, Napier AI secured an investment of $56.6 million (£45 million) from Crestline Investors.

“We are excited to work with the Napier AI team and believe their market-leading, AI-powered technology platform is well-positioned to help financial institutions and other regulated companies excel in an environment with rapidly expanding transaction volumes and increasing regulatory requirements,” Crestline Managing Director Will Palmer said when the investment was announced in February.

The week begins with a few research-related announcements in the fintech and financial services space. CB Insights announced the availability of its State of Insurtech report for the first quarter of 2024, and the Federal Reserve Board issued a summary of climate risk resiliences exercises conducted recently by a handful of big banks. While the focus on this column in on the former, the publication of the latter shines some light on potential answers to the problems raised in CB Insights’ report.

With regards to the state of insurtech, there is still a great deal of hesitation among investors. CB Insights noted that quarterly funding for Q1 of this year was only $0.9 billion, the lowest level since 2018. Property & casualty insurtech suffered the most, with a quarter-over-quarter decline of 25%. Q1 2024 was also the first time since 2018 that there were no “mega-round deals” – investments of $100 million or more. There was some good news in Europe, as the number of deals increased slightly, as did the median insurtech deal size. But the overall message continues to be caution when it comes to investor attitudes about investech.

What Ails Insurtech?

Digital disruption: The challenge of digital disruption is one that the insurtechs share with the broader fintech community. The rise of enabling technologies such as AI will both steepen customer expectations as well as accelerate competition between companies to effectively deploy new, innovative solutions.

The insurance business is ripe for innovation. From the massive volume of manual processes and the document-intensive nature of the business to the challenges of underwriting and refining statistical models, the idea that AI will be a powerful ally in the insurance business is a no-brainer. One firm, Zippia, has predicted that as much as 25% of the insurance industry could be automated via AI by 2025.

There are obstacles. The disposition of regulators toward change in the industry is a major concern as new technologies are introduced to enhance operations like underwriting and statistical modeling. A regulatory authority that is indifferent, or hostile, to new technologies or their application in certain use cases can send a powerful signal that innovators are better off deploying their solutions in other industries or other geographies. Looking at the U.S., if the behavior of regulators toward innovators in the crypto space and the Banking-as-a-Service space is any indication, then we can expect to see insurtech and their investors to tread cautiously.

There are also challenges with regard to talent. Now that almost every company in every industry is looking to up their AI game, the fight over top talent in AI and automation has become all the more competitive.

Nevertheless, there is no doubt that AI promises to revolutionize many key processes that insurers rely on. And as those processes become more efficient – and as those companies best exploiting those AI-enhanced processes take greater market share – it is easy to see investment dollars returning to insurtech as investors begin making their bets on winners and losers in the space.

Climate change: The impact of climate change is another instance in which challenge and opportunity go hand-in-hand for insurtechs. The growing incidents of extreme weather – from temperature extremes to increasingly powerful hurricanes, floods, and other phenomena – have put a major strain on both property and casualty (P&C) insurers as well as those homeowners and individuals who rely on their protection. Note that CB Insights reported the biggest quarterly drop in funding this year was among P&C insurtechs. And of the top 10 P&C insurtech deals of Q1 2024, only three were U.S. based companies.

While many fintechs involved in climate change and sustainability have focused on helping businesses and institutions measure and better manage their carbon footprints, there is a need for technology companies in the insurance space that can help these firms build the models they need to better anticipate climate change-related risk. I mentioned the Federal Reserve report on climate resiliency earlier. The Fed’s report was a summary of an exploratory pilot Climate Scenario Analysis (CSA) exercise held by six U.S. banks: Bank of America, Citigroup, Goldman Sachs, JPMorgan Chase, Morgan Stanley, and Wells Fargo. Among the conclusions that are especially relevant to this conversation were these two:

The role of insurance in mitigating climate change risks for consumers, businesses, and banks was emphasized, with a call to monitor changes in insurance costs and their impacts on specific markets and segments.

and

Participants expressed the high uncertainty and difficulty in measuring climate-related risks, making it challenging to incorporate them into risk management frameworks on a routine basis.

Insurtechs – and fintechs, for that matter – who are able to help financial institutions resolve these two issues, will find their services in demand as companies seek ways to quantify their own exposure to climate change risk. It is easy to envision other enabling technologies, such as quantum computing, also playing a part. Together, they could provide the kind of powerful modeling that would accurately gauge the risks of climate change and its potential impact on markets, communities, businesses, and families alike.

AI integration specialist AI Squared acquired open-source Reverse ETL (rETL) company, Multiwoven. Terms were not disclosed.

The acquisition follows AI Squared’s $13.8 million Series A funding round in April.

AI Squared made its Finovate debut at FinovateSpring 2023.

AI integration platform AI Squared has acquired open-source Reverse ETL (rETL) company Multiwoven. The transaction fortifies AI Squared’s ability to help organizations more easily move data and AI-based insights into business applications.

In a statement, AI Squared Founder and CEO Benjamin Harvey praised both Multiwoven’s technology as well as its open-source approach to innovation. “From my experiences as a data-science executive at the National Security Agency and as an early employee at Databricks, I recognize and respect the critical role that the open-source community plays in fueling innovation,” Harvey said. “Now as a singular organization, AI Squared and Multiwoven will continue to lead the way in open-source rETL, while simultaneously bringing critical data-movement functionality to our customers.”

Multiwoven is an open-source, reverse ETL platform that facilitates secure data segmentation, synchronization, and activation. The company’s technology makes it easier for firms to deploy this organized data into applications and business tools for sales, marketing, and advertising operations. By integrating Multiwoven’s rETL capabilities into its platform, AI Squared will be able to help organizations efficiently integrate robust data and AI insights into their applications.

“With our new combined team, we will be able to accelerate the development and growth of Multiwoven open-source, which will remain free to use,” Multiwoven Co-Founder and CEO Sojoy Golan said. “We are also excited to now introduce advanced capabilities to activate AI/ML data, together with AI Squared.”

AI Squared also will continue to support development of Multiwoven’s open-source technology. Golan called open-source “a wonderful enabler” that has helped uncover insights not only for Multiwoven’s own users and open-source contributors, but also for “the data practitioners on our Community Slack, and all the other generous people in the open-source community.” As part of the transaction, Multiwoven’s team will join AI Squared. Golan has been named Chief Product Officer; Multiwoven Co-Founders Nagendra Dhanakeerthi and Subin Thattaparambil will serve as Chief Technology Officer and SVP of Engineering, respectively.

Headquartered in Washington, D.C., AI Squared made its Finovate debut at FinovateSpring 2023 and returned to the Finovate stage later that year for FinovateFall in New York. In its most recent appearance, AI Squared demonstrated how adding Generative AI to the platform’s Predictive AI capabilities enables users to build tools such as chatbots to help them more efficiently query their data.

AI Squared was founded in 2019. Learn more about the company in our feature interview with AI Squared’s Benjamin Harvey.

U.K.-based challenger bank Monzo secured an additional $190 million (£150 million) in funding this week, adding to the $426 million (£340 million) raised just a few days ago. The Series I round, totaling $616 million (£490 million) gives the digital bank a valuation of $5.2 billion (£4.1 billion) and represents one of the biggest fundraising rounds for a European fintech since 2023.

The bank’s financial backers included Hedosophia and CapitalG, Alphabet’s growth fund. CNBC’s coverage of the funding notes that Singapore-based sovereign wealth fund GIC was also a participant in the funding, but GIC has yet to confirm the report.

Monzo will use the funds both to build new products as well as move forward with its international expansion plans. Expansion to the U.S. is near the top of the company’s wish list, having resumed efforts to secure a banking license in the country after retreating from a previous attempt three years ago. Monzo hired Conor Walsh, former Head of Product for Cash App, as its U.S. CEO in 2023.

“At the heart of it, we are a mission-oriented company that’s looking to build the single place where people can meet all of their financial needs,” Monzo Co-Founder and CEO TS Anil told CNBC. “What’s exciting to me is that, as we pursue that mission of changing people’s relationship with money, we’ve built a business model that is congruent with that, as well, with this model that is built entirely around the customer.”

Founded in 2015, Monzo has more than nine million retail customers and 400,000 business customers in the U.K. The challenger bank offers current and joint accounts, as well as an app to enable customers to see all their accounts and control spending. The company launched its first business bank accounts for SMEs and self-employed workers in 2020 and, later that year, unveiled its first loan products for its personal current account customers. In 2023, Monzo announced that it had achieved profitability for the first time.

As part of its expansion plans, Monzo is looking to begin offering mortgage and pension products, with the latter being available as early as six to nine months from now. Last year, Monzo launched an investment product, giving customers the ability to invest in a trio of funds offered by BlackRock.

Banked and NAB Promote A2A Payments in Australia

A new partnership between international payments network Banked and National Australia Bank will make it easier for merchants in Australia to adopt account-to-account (A2A) payments solutions. Specifically, the two entities are seeking to encourage the adoption of Pay by Bank technology via Australian Payments Plus (AP+) services.

Pay by Bank enables merchants to send PayTo Agreements to customers, and then initiate payments and refunds based on those agreements – which cover a variety of transaction experiences including online payments, and recurring payments with fixed, variable, or split payment amounts. Partnering with NAB gives Banked a partner with both an established presence in the Australian market, as well as a comprehensive knowledge of the needs of merchants in the country.

“The nascent A2A payments industry in Australia presents an incredible opportunity for Banked,” Banked CEO Brad Goodall said. “Local regulators have developed well-constructed mandates and the banking industry is primed for innovation, all of which sets the stage for rapid growth in real-time payments.”

An initial set of NAB business customers from industries such as e-commerce and retail, as well as non-bank lenders, is scheduled go live with A2A payments in the first half of 2024.

With offices in both Palo Alto, California and London, U.K., Banked was founded in 2018. Earlier this year, the company announced a partnership with FIS to promote use of Pay by Bank.

Meet FinovateSpring 2024’s International Alums

FinovateEurope typically gets top billing as our most international fintech conference. But FinovateSpring has showcased a sizable number of fintech innovators from around the world, as well. And this year’s FinovateSpring is no exception.

Here’s a look at seven companies demoing at FinovateSpring, May 21-23, that hail from outside of the United States.

There’s still time to pick up your ticket and save your spot for our annual Spring fintech conference in San Francisco, May 21-23. Visit our FinovateSpring hub to register.

Here is our look at fintech innovation around the world.

Sub-Saharan Africa

Nigerian fintech and non-bank credit card issuer O3 Capital partnered with American Express to issue four new AMEX credit cards.

South African fintech Lesaka acquired South African payments company Adumo in a deal valued at $85.9 million.

SasaPay, a fintech headquartered in Kenya, announced a partnership with investments solutions provider Etica Capital.

Central and Eastern Europe

Swiss Bitcoin Pay teamed up with Lithuanian regtech iDenfy to enhance its risk management and onboarding processes.

Latvian fintech Huntli partnered with U.S.-based Payall to improve security for cross-border payments.

Lithuania-based TransferGo secured $10 million in funding from Taiwania Capital Management.

Middle East and Northern Africa

Digital payments company Wink Pay launched in Lebanon in partnership with Visa and Codebase Technologies.

Saudi Arabian insurtech Rasan to sell 30% of its stake in a Riyadh IPO.

Central and Southern Asia

Nepal Clearing House inked a memorandum of understanding (MoU) with Ant International to enable QR payments via Alipay+ for visitors to Nepal.

Finovate Best of Show winner Zetalaunched its Digital-Credit-as-a-Service solution for banks in India.

Saudi Arabia’s Alraedah Digital Solutions forged a strategic partnership with Pakistan-based fintech ABHI to launch new financial services in the kingdom.

Latin America and the Caribbean

Brazilian digital bank Nubanktops 100 million customer mark.

Finovate’s Credit Union Spotlight is back! This month at FinovateSpring – May 21 through May 23 – Finovate will host a special session to give leaders and professionals working at credit unions an opportunity to meet and network with their peers as well as with fintech innovators who are building solutions specifically for credit unions.

Coordinated by Finovate Vice President and Director of Fintech Strategy Greg Palmer and Sam Das, Managing Director of TruStage Ventures, the Credit Union Spotlight gives those running credit unions the opportunity to speak freely and candidly about the challenges – and opportunities – facing credit unions and their members today.

We caught up with Greg Palmer to talk about the state of credit unions in 2024 and what the Credit Union Spotlight at FinovateSpring this year hopes to achieve.

What challenges are credit unions facing right now?

Greg Palmer: Credit unions are facing a myriad of challenges at the moment. High interest rates and economic uncertainty are putting pressure on everyone, but local financial institutions like credit unions are particularly vulnerable. The good news is that the fintech industry is increasingly aware of what CUs are going through, and we’re seeing more and more technologies built with CUs in mind. These technologies are arriving just in time, and it’s about to get a lot easier for smaller FIs to compete with the multinational banks that tend to dominate the headlines.

How can better, deeper relationships with fintechs help credit unions overcome these challenges?

Palmer: It’s difficult for CUs to compete with larger financial institutions with bigger budgets, more marketing power, and teams of technologists creating new innovations in-house. These same factors, though, are also making it more difficult for fintech companies to sell their solutions into those big banks. The result is that a lot of newer fintech innovators are looking at credit unions as a target demographic. CUs both need the technologies they can provide and are less likely to be able to create their own alternatives, which is why it’s so imperative for us to bring both groups together.

How important is it to give credit unions the opportunity to network more exclusively with fintech providers, as well as with each other?

Palmer: Credit unions are fundamentally different from for-profit financial institutions, and they look at new technologies through a slightly different lens. That’s why it’s so important to separate out CU executives into their own space where they can network with each other, share experiences, and view new technologies together.

Finovate’s Credit Union Spotlight will take place on May 23, Day Three of FinovateSpring. The session will be held around midday and will last for approximately 90 minutes.

Read more about the Credit Union Spotlight at FinovateSpring in this feature at Finopotamus and don’t forget to take an early look at our demo companies in our Sneak Peek series. And if you haven’t picked up your ticket yet, Friday is the deadline to take advantage of big, early-bird savings. Visit our FinovateSpring hub today and save your seat!

FIS unveiled its embedded finance platform, Atelio by FIS, this week.

The platform leverages FIS’ existing technology to enable businesses to embed a variety of financial products and services into their offerings.

FIS made its Finovate debut at FinovateSpring in 2013. Stephanie Ferris is CEO and President.

FIS is the latest company to introduce a platform to make it easier for businesses and software developers to embed financial services and fintech solutions into their products and services. Atelio by FIS, launched this week, is one of the first banking-as-a-service offerings from a major core provider. The technology will serve B2C fintechs and enable financial and non-financial services companies alike to implement embedded finance into their existing offerings

“Welcome to the future of financial services,” FIS President of Platform and Enterprise Products Tarun Bhatnagar said. “Atelio by FIS is our vision to lead where fintech is going, which is outside the boundaries of how businesses enable, and their customers consume, financial services today.”

Atelio leverages FIS existing technology by way of easily embeddable and consumable components. The platform enables non-financial companies to offer their customers a wide variety of financial experiences: collecting deposits, moving money, issuing cards, sending invoices, and more. Atelio also provides tools to help companies fight fraud, anticipate cash flows, and gain insights into consumer preferences and behaviors.

FIS’ latest offering comes at a time when growth in embedded finance is expected to soar. In its product announcement, the company pointed to research from Bain Capital that indicated that embedded finance will represent 10% of all transactions by 2026. The firm values these transactions at $7 trillion, or more than $50 billion in total revenue. Additionally, research from S&P Global Intelligence showed that banks that offered embedded finance solutions outperformed their peers in terms of deposit growth.

“More than just a new solution, Atelio is built to lend the expertise, tools, and distribution so that our users and clients can focus on creating,” Bhatnagar said. “Our scale, distribution and continued investment in technology have given us the foundation to unlock our financial capabilities to a wider audience and power the next generation of financial innovation.”

Three FIS clients – KeyBank, private student loan provider College Ave, and payment system and billing platform Royal Pay – have already deployed Atelio and are building solutions on the platform.

Jacksonville, Florida-based FIS made its Finovate debut at FinovateSpring 2013. Currently, the company enables 95% of the world’s banks, moves more than $1 trillion a month, and processes $50 trillion via its asset management technology every year. The company’s new product announcement came one day after FIS announced first quarter 2024 results which included the firm’s “fifth straight quarter of exceeding our financial outlook,” according to FIS CEO and President Stephanie Ferris.

U.K.-based fintech SumUp has raised $1.6 billion (€1.5 billion) in a private credit debt transaction.

The deal was led by Goldman Sachs Asset Management, and will enable SumUp to refinance debt and pursue international growth opportunities.

SumUp won Best of Show at FinovateEurope 2013, a year after the company was founded.

In a deal led by Goldman Sachs Asset Management, U.K.-based fintech SumUp has secured $1.6 billion (€1.5 billion) in a private credit debt transaction. The financing will enable SumUp to refinance current debt as well as take advantage of growth opportunities around the world.

The deal gives SumUp a set of new investors: AllianceBernstein, Apollo Global Management, Arini, Deutsche Bank AG, Fortress Investment Group, SilverRock Financial Services, and Vista Credit Partners. It also comes six months after the company raised $307 million (€285 million) in equity and debt in a round led by Sixth Street Growth. Bain Capital Tech Opportunities, Fin Capital, and Liquidity Capital also participated in that financing.

In a statement SumUp CFO Hermoine McKee pointed to an evolution in the company’s “requirements from capital markets” in explaining SumUp’s most recent fundraising effort. “Lenders understand and support our mission to create a world where everyone can build a thriving business, and recognize our successful methods of achieving, sustaining, and balancing profitability and growth,” McKee said. “This new financing will support us as we focus on providing best-in-class support experiences for our merchants and giving them the products and tools they need to succeed.”

To this end, SumUp noted in a statement that the company has generated positive EBITDA since December 2022, as well as achieving a “decade of sustained growth.” The company currently counts four million businesses among its partners, who rely on SumUp for services ranging from payments and order processing to customer acquisition and money management.

“SumUp has always enjoyed solid and steady support from the investor community, and it’s this continued backing which has enabled us to grow sustainably over the past 10+ years, serving millions of merchants of all sizes globally,” McKee said.

Founded in 2012, SumUp won Best of Show in its Finovate debut at FinovateEurope in 2013. The company began this year with its SumUp Beacon event which introduced merchants to a range of new SumUp solutions. These new offerings included SumUp Business Account,SumUp Invoices, SumUp Kiosk, and SumUp Online Store. SumUp also unveiled a pair of new Point of Sale (POS) solutions: POS Lite to enhance over-the-counter sales, and POS Pro to provide enhanced inventory management.