This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Sustainable Fitch will integrate AI-powered text analysis from SESAMm into its ESG Scores and Ratings solution.

The integration will help Sustainable Fitch offer a more comprehensive ESG insights to asset owners and asset managers.

SESAMm won Best of Show in its Finovate debut at FinovateEurope 2022 in London.

ESG data and analysis provider Sustainable Fitch will integrate AI-powered text analysis from SESAMm into its ESG Scores and Ratings solution. The integration will enable Sustainable Fitch to provide more comprehensive ESG insights to its asset owner and manager clientele.

The addition of SESAMm’s analysis will improve decision-making and help guide investment and due diligence. The partnership will also help provide broader data coverage for both public and private market data analysis.

“Working with SESAMm’s technology allows us to leverage their advanced solutions to enhance our ESG Scores and Ratings offering,” Sustainable Fitch Global Head of ESG Analytics Gianluca Spinetti said. “By integrating SESAMm’s extensive data coverage, we can offer our clients more comprehensive ESG insights.”

Headquartered in New York, Sustainable Fitch is a research firm that provides data, tools, analysis, and insights for the fixed-income market. The company provides ESG ratings, Second Party Opinions, thought leadership, and more to help individuals and institutions make informed decisions when it comes to ESG impact.

Launched in 2022, Sustainable Fitch has been recognized by Environmental Finance as one of the top five largest global Second Party Opinion providers. This year, the company won “Best Specialist ESG Ratings Provider” at the ESG Investing Awards and “Best ESG Data Provider/Vendor” at the Inside Market Data Awards & Inside Reference Data Awards.

“We are excited that a recognized leader in ESG analysis is using our insights for their ESG analysis,” SESAMm CEO Sylvain Forté said. “Our AI-powered text analysis will provide deeper insights and broader coverage, helping Sustainable Fitch to deliver high-quality ESG data and ratings.”

SESAMm won Best of Show in its Finovate debut at FinovateEurope in London in 2022. The company most recently demoed its technology at FinovateFall 2023, where the French AI firm showed an integration of ChatReveal, its proprietary generative AI solution. Bringing advanced chatbot technology to the SESAMm platform, ChatReveal examines more than 23 billion articles on five million public and private companies. The technology identifies if the company is the subject of ESG controversies or issues to help private equity firms and financial institutions better understand the potential risk of companies in their portfolios.

Last month, SESAMm unveiled its ESG Controversy Risk Exposure Heatmap. The solution delivers an overview of environmental, social, and governance risks to provide an easy way to visualize and assess a company’s reputational profile. This enables users to focus on particular areas of concern and prioritize next steps.

Headquartered in Paris, France, SESAMm was founded in 2014. The company has raised more than €50 million in funding and includes Elaia, Opera Tech Ventures, The Carlyle Group, and NewAlpha Asset Management VC among its investors.

This week’s edition of Finovate Global highlights recent fintech news from the Philippines.

Philippine mobile payments company Mynt, the firm behind super app GCash, has secured an investment of $393 million courtesy of an investment from Mitsubishi UFJ (MUFG). The funding comes at virtually the same time as the company reported another $393 million investment, this one from Philippines-based conglomerate Ayala Corporation.

“We are thrilled to welcome MUFG as a new strategic partner,” said Mynt President and CEO Martha Sazon. “With their global expertise and reach within the financial inclusion space, they will be instrumental in further expanding GCash’s social impact, especially to the underserved. Alongside this, Ayala’s unmatched commitment to Philippine economic growth and development, and its expertise in multiple industries will accelerate GCash’s mission.”

The investments give the Filipino firm a valuation of $5 billion, and gives MUFG an 8% stake in the company. Ayala’s share climbs to approximately 13%.

A subsidiary of Globe Telecom, Mynt’s GCash is used by more than 90 million individuals to buy prepaid airtime, pay bills, send and receive funds, transact with merchants, and access savings, credit, insurance, and investment products.

“GCash is an indispensable infrastructure for everyday life of Filipinos and we are delighted to join Mynt as a strategic investor to support the growth of the company,” MUFG Senior Managing Corporate Executive, Head of Global Commercial Banking Business Group Yasushi Itagaki said. “With our investment, we are excited to expand our contribution to the ongoing development of the Philippines’ digital economy and financial inclusion.”

MUFG’s investment comes at a time when the banking group has been funding a range of regional fintechs that are helping bring financial services to the underbanked. Among these fintechs are Ascend Money, a super app based in Thailand, as well as Grab of Singapore and Akulaku of Indonesia.

Earlier this year, Globe Telecom suggested that the super app may launch as a public company in the Philippines next year. This week, Bloomberg reported that the company may pursue a Philippine digital banking license, as well.

Mynt’s GCash is a big deal in the Philippines when it comes to mobile fintech apps. But how big are mobile fintech apps in the Philippines? A new report from UnaFinancial noted that among Southeast Asian nations mobile fintech app adoption has been strong overall, but nowhere more so than in the Philippines where mobile fintech app penetration reached 63% by May of this year. Malaysia was second at 55%. Interestingly, fintech powerhouse Singapore registered 45%, tied with Thailand and behind Indonesia’s 49%. Vietnam showed 32% mobile fintech app penetration.

Why such a strong performance for mobile fintech apps in the Philippines? The UnaFinancial analysts cited a handful of factors including the large number of unbanked Filipinos; regulatory support for developing digital financial technologies; a sizable, tech-savvy youth population; and growing rates of Internet adoption. Digital wallets and payment apps remain the most popular mobile fintech apps, with mobile banking apps making a strong second place showing. One area of particular growth is lending apps, which increased their share of mobile fintech apps from 1% to 5% between 2019 and 2024.

The report noted that the Philippines is likely to remain the regional leader in mobile fintech app adoption. But recent growth in Indonesia’s fintech sector has UnaFinancial predicting that Indonesia could take the second spot from Malaysia by the end of 2030.

The move will allow as many as ten digital banks to operate in the Philippines. Currently, six digital banks have been licensed to operate in the country since the introduction of the Digital Banking Framework in 2020. This week’s announcement will allow as many as ten digital banks, opening the door for the granting of an additional four licenses. Both new applicants as well as existing banks are eligible to apply, though the BSP noted that the licensing process will be “stringent.”

Additionally, the BSP made clear in a statement that it is looking for innovation rather than more of the same. “Applicants must bring something new to the table,” said bank governor Eli M Remolona, Jr. “We want to see unique product and service offerings that are different from that offered by the existing market players.”

Beginning on September 4th, banks in South Africa will suspend electronic fund transfer (EFT) services to Namibia, eSwatini, and Lesotho as part of a payments reclassification to help prevent financial crime.

Central and Eastern Europe

Austrian cryptocurrency platform Bitpanda partnered with Solaris to enhance its KYC capabilities in the German market.

For the first time, Finovate will offer a dedicated wealthtech/wealth management track at FinovateFall. Featuring keynote addresses, power panels, and more, our new wealthtech track will cover topics ranging from the rise of alternative assets to the role of technology and digitization in helping meet the needs of a new generation of investors.

“I’m really excited about the new Wealthtech track we’re offering at FinovateFall this year,” said Greg Palmer, host of Finovate. “So much innovation is taking place on the wealth management side of the fintech industry right now, and there are a lot of opportunities out there. Customer demographics are shifting, new assets are gaining popularity, and new technologies are raising the bar for every industry. It’s a crucial time to be paying attention to the space.”

Over the next few weeks, we’ll share a preview of the wealthtech content we have in store for you this year at FinovateFall. Today, we’re highlighting a pair of Power Panels that will take place on Day Three, September 11, of the conference.

Both of these Power Panels will be moderated by April Rudin, CEO and Founder of The Rudin Group. LinkedIn.

The Rudin Group is a global wealth management/wealthtech marketing consultancy serving banks, wealth management firms, fintechs, and wealthtechs.

The Future of Client Centricity in a Tech-Disrupted Wealth Landscape

Our Power Panel on the Future of Client Centricity will examine ways in which technology has altered the landscape of wealth management. The panel will discuss the impact of the Great Wealth Transfer from Baby Boomers to Millennials and what wealth managers should do to meet a new generation of investors’ growing preference for digital solutions and tools.

Andrea Finan, Head of J.P. Morgan Self-Directed Investing, J.P. Morgan Wealth Management

Finan is responsible for developing strategy, driving scale and profitability, and expanding capabilities to serve the firm’s Self-Directed and broader Wealth Management clients. She has 20 years of experience in financial services and is well-versed in creating high-performing digital products. LinkedIn.

Ali Geramian, Managing Director, Anthemis

Geramian is currently a Partner at Anthemis, where he steers the Anthemis ecosystem and investor relations platform to catalyze mutual value creation, collaboration, and transformative partnership opportunities across the firm’s global portfolio companies and strategic investor base. LinkedIn.

Michelle Julia Ng, Software Engineer, Apple

Ng is a software engineer with Apple. Educated at Stanford University (double majoring in Computer Science/Artificial Intelligence and History), Ng brings experience in the practical application of emerging technologies – including system intelligence, machine learning, and robustness analysis – having worked with Apple’s Vision Pro and Watch products. LinkedIn.

How Will Technology Transform How Alternative Assets are Managed?

This Power Panel will look at the rise of alternative assets through the lens of a shift toward diversification, a search for yield, a demand for uncorrelated returns, and a growing desire among a new generation of investors for investment opportunities that are aligned with their personal values. The Panel will also discuss how enabling technologies – from AI to the blockchain – will influence the way alternative assets are managed.

Bundeep Singh Rangar, CEO of Fineqia

A thought leader in blockchain technologies, Rangar is CEO of Fineqia International. Fineqia is a digital asset business that builds and targets investments in early and growth-stage technology companies. An investor in digital industries, Rangar has raised venture capital from entities such as Rakuten and secured private equity investment from U.S. financial institutions. LinkedIn.

David Teten, Venture Partner at Coolwater Capital

Teten is a Partner with Coolwater Capital. Known as the “Y Combinator for Emerging VCs,” Coolwater offers an accelerator for emerging VC fund managers and invests as a limited partner, into general partnerships and fund management companies. Coolwater also invests directly into startups. He is Chair of PEVCTech, a community of investors in private companies using AI, technology, and analytics to generate alpha. LinkedIn.

Unsecured loan provider Happy Money announced a strategic partnership with Method Financial.

Happy Money will use Method’s financial liability connectivity APIs to help credit union members better manage credit card debt.

Headquartered in Austin, Texas, Method made its Finovate debut earlier this year at FinovateSpring in San Francisco.

Happy Money, an unsecured loan provider that works with credit unions, has forged a strategic partnership with Method Financial. The company will leverage Method’s technology – a suite of liability connectivity APIs – to help Happy Money members consolidate and pay off high-interest credit card debt.

“Happy Money is helping consumers across the country access the capital they need to reach their goals in partnership with credit unions and other community-focused lenders,” Method CEO and Co-Founder Jose Bethancourt said. “With the integration of our technology, they are ensuring the process is as seamless, quick, and efficient as possible, creating value for all involved.”

Happy Money offers consumers personal loans with a low interest rate and a single, fixed payment to help them pay off high-interest credit card debt. Integrated into the Happy Money platform, Method’s liability connectivity APIs will facilitate more accurate identification of members’ outstanding credit cards, as well as real-time live balance retrievals and balance transfers. All this takes place without members having to enter account numbers or passwords.

Since the partnership began, Happy Money reports that its members have connected more than 50,000 accounts via Method’s APIs. Moreover, millions of dollars in consumer debt have been consolidated monthly through Method’s connectivity and payment rails. Together, Happy Money and Method have facilitated more than $7 million in balance transfers for Happy Money members.

“At Happy Money, we believe that prioritizing borrowers’ well-being is a winning strategy,” Happy Money Head of Product and Design Nick Pesce said. “Our platform allows consumers to meet their financial goals and enables credit unions to diversify their portfolios and grow.”

Founded in 2009, Happy Money is headquartered in Torrance, California. Since inception, the company has served more than 300,000 members and funded more than $6 billion in loans through partnerships with community-focused lenders. Happy Money has raised more than $337 million in capital, according to Crunchbase. Anthemis and TruStage Ventures are among the firm’s investors.

Method made its Finovate debut earlier this year at FinovateSpring, where the company demoed its connectivity, data, and payments APIs. Method’s technology enables lenders, fintechs, and financial institutions to leverage comprehensive, real-time credit data, evergreen connections, and integrated payment rails to offer customers personalized lending and financial management experiences.

Via a single integration, Method enables access to liabilities held at more than 15,000 financial institutions in the U.S., representing 95% of all outstanding consumer debt. The company has helped 200,000+ users connect more than $22 billion in consumer debt to their preferred financial institution.

Headquartered in Austin, Texas, Method was founded in 2021. The company’s investors include Andreessen Horowitz, Truist Ventures, and Leonis Capital.

Customer analytics platform unitQ secured a strategic investment from Zendesk Ventures.

The amount of the investment was undisclosed. unitQ had raised $41 million in funding to date.

unitQ made its Finovate debut at FinovateFall 2021 and returned to the Finovate stage a year later for FinovateSpring in San Francisco.

Here’s some funding news that slipped beneath our radar this summer: AI-powered customer analytics platform unitQ has secured an investment from Zendesk Ventures. The amount of the funding was not disclosed, but it turns Zendesk from a unitQ customer into a strategic investor, as well.

“We chose unitQ after evaluating and trying different solutions in the market,” Zendesk VP of Global CX Operations Shawn Slipy said. “The granularity and speed at which unitQ is able to deliver actionable customer insights is above and beyond what others could offer, and we’re grateful for our continued partnership.”

unitQ had raised $41 million in capital ahead of the June investment, according to Crunchbase. The current investment comes amid Zendesk Ventures’ determination to back companies that are leveraging AI to enhance both customer and employee experience. The venture fund will provide unitQ with access to CX and AI experts to help drive innovation and assist the company in recruiting talent, growing unitQ’s customer base, and building its brand.

“We’ve experienced the power of Zendesk’s community first-hand and are excited to explore joint go-to-market efforts with Zendesk’s ecosystem of customers, technology partners, and evangelists,” unitQ CEO and Co-Founder Christian Wiklund said. “Partnering with Zendesk means joining forces with a leader that opens doors to top-tier talent and industry networks. We’ve gained more than just funding – we’re now connected to a community and receive tailored mentorship to help our company’s growth.”

Customer service platform Zendesk leverages AI agents, workflow automation, and human agents to help businesses provide better service to customers and make workplaces more efficient for employees. The company has more than 100,000 customers in 160 countries and territories and 5,450 employees. Zendesk launched its Zendesk Ventures global venture fund in June with a mission to provide emerging companies with capital, CX and AI expertise, as well as strategic partnership opportunities – especially for AI-first companies.

“Every organization is on a path to becoming AI-driven, and we’re eager to form partnerships with companies leading this new era,” Ben Barclay, SVP of Strategy, Corporate Development, & Transformation at Zendesk, said.

unitQ made its Finovate debut at FinovateFall 2021, and returned to the Finovate stage the following year for FinovateSpring in San Francisco. In the time since then, the company has launched a range of new solutions, including its Impact Analysis Tool and its generative AI engine for measuring product quality, unitQ GPT. This spring, unitQ added Product Analytics to its User Feedback Platform to enable institutions to view and analyze real-time user feedback along with behavioral analytics data.

In recent months, the company has also forged partnerships with Chess.com, streaming media platform Plex, and most recently with product analytics platform Amplitude.

Founded in 2018, unitQ is headquartered in Burlingame, California.

The partnership will enable Varo Bank to offer a range of new products including digital wallet tokenization via Apple and Google Wallets for its cardholders.

Headquartered in Oakland, California, Marqeta was founded in 2010.

Card issuing platform Marqetahas signed a five-year deal with Varo Bank to serve as the financial institution’s issuer processor. Marqeta’s ability to blend virtual, tokenized, and physical card-issuing technology with faster speed-to-market was among the factors cited by Varo Bank in teaming up with the fintech.

“We sought an issuer partner that complements our unique position as both a technology company and a regulated financial institution,” Varo Bank CEO Colin Walsh explained. “This partnership with Marqeta enables us to offer cutting-edge card issuing technology, giving our customers enhanced ability to view and manage their transactions efficiently. This advancement aligns perfectly with our mission of financial empowerment.”

Widely recognized as one of the first nationally-chartered consumer-based techbanks in the U.S., Varo Bank offers fee-free checking accounts, high-yield savings accounts, secured credit-building credit cards, instant payment solutions, and free ATM access at more than 40,000 locations. Varo Bank’s mobile app enables customers to review and improve their financial health, and now, courtesy of the institution’s partnership with Marqeta, the bank will enable digital wallet tokenization with Apple and Google Wallets for its cardholders.

“Marqeta is proud to announce this deal with Varo Bank, which relies on the latest payments and banking technologies to help Americans who are striving to get ahead,” Marqeta CEO Simon Khalaf said. “Varo’s mission is aligned with ours and we can’t wait to start innovating with the Varo team, enabling their customers to see transactions in real-time thanks to Marqeta’s APIs.”

Marqeta is an alumnus of our developers conference series, FinDEVr. The company presented its technology at our event in Silicon Valley in 2016. In the years since then, the Oakland, California-based fintech has grown into a major, modern card issuing platform operating in 40 countries and processing more than $160 billion in volume in 2022. The company’s partnership news with Varo Bank comes less than a month after Marqeta announced that it had become the first issuer processor in the U.S. that was certified to enableVisa Flexible Credential, a product that provides access to multiple funding sources from a single payment card.

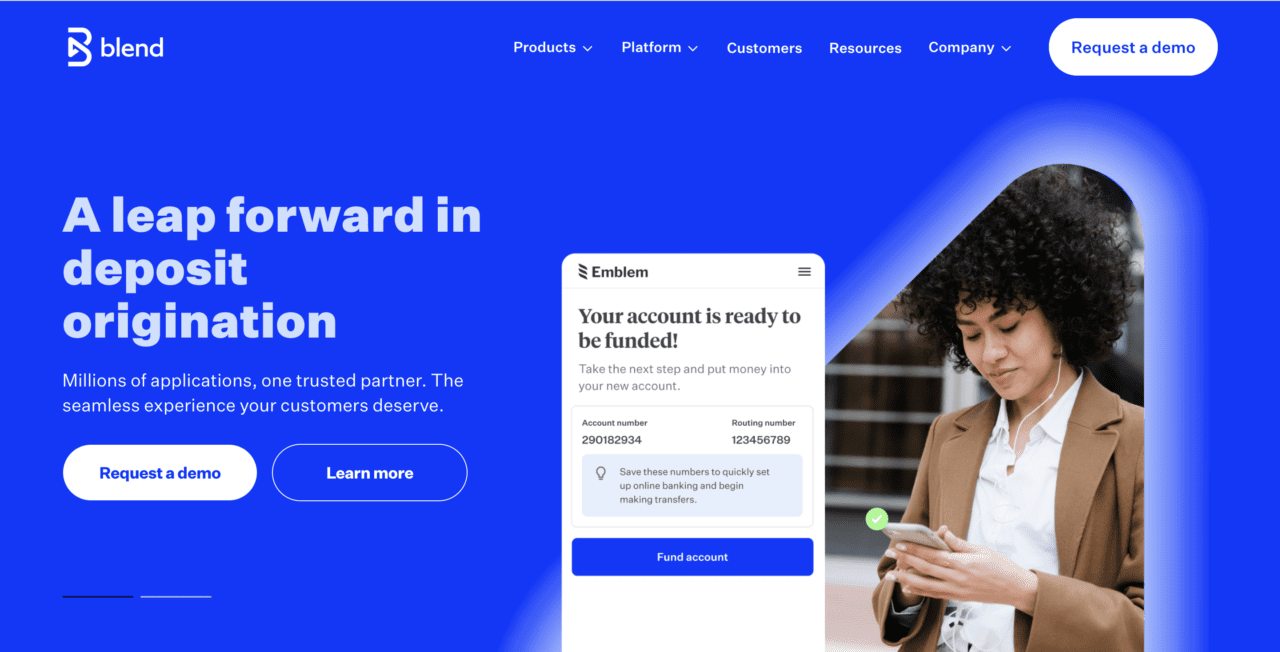

Digital banking solutions provider Blend has forged a partnership with instant payments-as-a-service company Astra. The partnership will integrate Astra’s Card to Account payment solution directly within Blend’s Deposit Account application flow. This will enable Blend customers to drive digital engagement beyond the initial application capture, lowering abandonment rates and helping consumers complete applications faster.

“Today consumers expect a frictionless, real-time product experience, and that starts at account opening,” Astra CEO and Co-Founder Gil Akos said. “Financial institutions and fintechs need to deliver a best-in-class onboarding flow to win new customers – instant account funding is the perfect solution, leading to improved activation rates of 30% or better on day one. We’re proud to partner with Blend to offer this experience to their customers.”

Funding by card is an increasingly popular option given the relative inconvenience of other methods, such as ACH transfers. By comparison, funding new accounts via debit cards is a faster and more seamless process (no routing or account numbers to remember). And because cards only enable transactions up to the available balance, card funding also helps avoid potential overdrafts when using ACH transfers, a risk for consumers who may have limited funds or irregular cash flow.

Further advantages include accelerated onboarding, more activated accounts, reduced abandonment, a smoother application experience, and less manual intervention.

Blend noted in a statement that card funding is also one of the more popular ways for consumers to fund new accounts. The company pointed to one of its customers, a major credit union, that reported that 82% of their new deposit accounts were funded using Astra card funding. Another credit union customer of Blend said that 66% of its consumers preferred funding via Astra card compared to other methods. Card funding for Blend Deposit Accounts is now generally available for all customers.

Astra offers a platform for instant payments that enables product teams to embed payments into their solutions. The company’s API facilitates seamless fund transfers between bank accounts and cards, providing a fast, secure, and built-for-scale alternative to traditional fund transfer methods such as ACH.

Astra launched its first, end-to-end instant payment solution with FedNow in the fall of 2023. In December, the company announced a partnership with merchant connectivity platform Knot to enable seamless card switching with instant funding. Founded in 2016, Astra is headquartered in Menlo Park, California.

Blend demoed its technology at FinovateSpring 2016. At the conference, the company demoed its Data-Driven Mortgage solution which leverages high-fidelity data sources to drive down origination costs, maintain digital compliance, and provide a positive user experience for borrowers.

Last month, Blend announced its acquisition of applied AI company nuvu, and expanded its partnership with DataIQ. In May, Blend secured an investment of $150 million from technology-focused private equity firm Haveli Investments.

Headquartered in San Francisco, California, and founded in 2012, Blend is a publicly-traded company on the NYSE. Trading under the ticker BLND, the company has a market capitalization of $678 million. Nima Ghamsari is CEO and Co-Founder.

In partnership with financial literacy platform Doshi, Yorkshire Building Society is offering online financial education to first-time prospective homebuyers.

The new free tool, available on the YBS website to customers and non-customers alike, walks new homebuyers through the entire home-buying process.

Doshi made its Finovate debut earlier this year at FinovateEurope in London.

Yorkshire Building Society (YBS) has teamed up with gamified financial literacy platform Doshi to launch an online educational program for first-time prospective homeowners. The new tool is available in the mortgage section of Yorkshire Building Society’s website, and guides borrowers through the process of applying for a mortgage and buying their first home.

The program walks prospective homeowners through the entire home-buying journey, including how to prepare for buying a home, how to secure financing, understanding the various steps of the home-buying process, and the importance of maintaining their home once they’ve made their purchase. The program explains important concepts and potentially unfamiliar terms, and provides a timeline of the overall process. The tool is available free of charge to both YBS customers and non-customers.

“Partnering with Yorkshire Building Society to empower aspiring homeowners is a significant step toward making homeownership more accessible,” Doshi CEO Daniel Rose said. “Our program demystifies the mortgage process, providing engaging, bite-sized guidance every step of the way. We are excited to see the positive impact on first-time buyers.”

The new offering comes in the wake of research conducted by YBS that indicated that a lack of knowledge about the home-buying process was a major barrier for would-be homeowners. YBS noted that only 18% of those surveyed felt knowledgeable about the mortgage process, with even fewer respondents – 14% – saying that they knew what financial factors were key when applying for a mortgage. The survey further indicated that only 45% of respondents believed that a good credit score was an important factor in securing a mortgage. Only 34% stated that the ability to repay debts was important when it comes to obtaining the financing necessary to buy a home.

“We know from customer research that people feel more confident in their decision making when they are informed and know what to expect, which is why we are trialing this new learning tool, aimed at helping first-time buyers understand more about the home-buying process,” YBS senior manager for digital mortgage and enabling services Geddy Meguyer said.

The third-largest building society in the U.K., Yorkshire Building Society is a financial services mutual organization that offers savings, investing, insurance, and mortgage products. Headquartered in Bradford, West Yorkshire, YBS had total assets of more than £60 billion as of December 2023. Along with its assets – the Chelsea Building Society, the Norwich and Peterborough Building Society, Accord Mortgages, and savings business Egg – known as the Yorkshire Building Society Group, the group employs more than 3,000 and serves a membership of three million.

YBS’s partnership with Doshi is the latest effort by the building society to support first-time homeowners. This spring, YBS launched its £5k Deposit Mortgage product, which enabled first-time homebuyers to buy a property worth up to £500,000 with a deposit of only £5k, rather than the typical 5% down payment. The idea behind the £5k Deposit Mortgage was to deal with the biggest obstacle prospective homebuyers tend to face – raising the funds for a down payment.

Doshi made its Finovate debut at FinovateEurope 2024 in February. At the conference, the company demoed its white-label app, which leverages personalized learning journeys and community rewards to turn complex topics into engaging experiences. Doshi’s AI-powered financial assistant technology is built for banks, credit unions, and fintechs, and is available as an app, a plug-and-play web module, as well as via API.

Doshi was founded in 2021. The company is headquartered in London.

A major sell-off in the stock market is giving investors jitters as August begins in earnest. Funding news for companies in lending and wealth management leads the fintech news this week. Be sure to check back over the next few days for the latest updates and announcements.

Lending

U.K.-based SME lender Shawbrook partners with nCino to automate loan origination.

Alternative financing company for mid-sized SMEs, ThinCats, secures a £75 million mezzanine facility.

This week’s edition of Finovate Global highlights recent fintech news from India.

A strategic partnership between financial software applications and marketplace company Finastra and Tech Mahindra, announced today, will help corporate banks accelerate their digital transformation journeys. Specifically, the partnership will make Tech Mahindra the exclusive global implementation partner for Finastra’s Cash Management platform. Tech Mahindra will also become the preferred partner for Finastra’s Trade Innovation and Corporate Channels solutions in the U.S., Canada, and Europe.

“This is an important partnership that aligns closely with our commitment to helping our customers navigate today’s challenges and embrace much needed digitalization,” Finastra CEO Simon Paris said. “The broad portfolio of services and deep experience offered by Tech Mahindra are a valuable complement to our modern and open software. With this combination, we look forward to propelling the digital transformation of even more banks and financial institutions around the world.”

The partnership will enable the two companies to offer a variety of cross-functional solutions across digital advisory, system integration, integrated infrastructure, and cloud services. These solutions will help corporate and institutional banks streamline and digitalize their operations. Financial institutions will further benefit from faster time to value for customers courtesy of faster implementations and upgrades.

“This partnership brings together two global leaders in digital transformation and financial services applications to help corporate banks scale at speed,” said Tech Mahindra CEO and Managing Director Mohit Joshi. “We believe our joint efforts will redefine the way banks digitize to improve their profit margins.”

Founded in 1986, Tech Mahindra is an international IT services and consulting company, headquartered in Pune, India. Part of the Mahindra Group, Tech Mahindra has more than 147,000 employees in 90+ countries serving 1,100+ clients. The firm offers solutions and expertise in verticals ranging from banking, insurance, and telecommunications, to media, entertainment, and retail. The first Indian company to earn the Sustainable Markets Initiative’s Terra Carta Seal, Tech Mahindra is publicly traded on India’s National Stock Exchange (NSE) and has a market capitalization of $17.8 billion (₹1.5 trillion).

The product of a union between Finovate alum Misys and D+H in 2017, Finastra offers software and solutions for financial institutions across lending, payments, treasury and capital markets, as well as retail, digital, and commercial banking. The company’s technology for banks helps them develop their direct banking relationships and to grow through new channels such as Banking-as-a-Service and embedded finance. More than 8,000 institutions – including 45 of the world’s top 50 banks – rely on Finastra’s technology.

The Reserve Bank of India (RBI) has been making fintech, financial, and economic news of late. On the fintech side, the RBI has granted cross-border payment licenses to three fintechs: BillDesk, Amazon Pay, and Adyen. These licenses will enable these companies to operate as cross-border payment aggregators and, ultimately, to offer their customers payment services for both imports and exports.

The RBI has been actively encouraging many fintechs to secure payment aggregator licenses; more than 20 companies have been granted PA licenses to date. In many of these instances, the RBI has suggested that companies interested in cross-border payments in particular apply for these licenses. Another firm that recently secured its PA license for cross-border payments for import and export from the RBI is Cashfree Payments.

In order to secure PA licenses, fintechs must register under the Financial Intelligence Unit-India (FIU-IND) in order to become authorized to process transactions. Fintechs must also maintain a minimum net worth of Rs 15 Cr ($1.8 million) during application, a sum that will increase to Rs 25 Cr ($2.9 million) after March 2026.

Speaking of payments, the RBI is now a part of Project Nexus. The first project from the payments sector of the Bank for International Settlements (BIS), the project seeks to connect the Faster Payment Systems of four Association of Southeast Asian Nations (ASEAN) countries – Malaysia, the Philippines, Singapore, and Thailand – and India. While India’s RBI has collaborated with a number of other countries via its Unified Payments Interface (UPI) to support bilateral payments, RBI’s participation in Project Nexus is the first time the bank has officially joined a multilateral project of this scope.

Additional countries are expected to be added over time. The project will help small and medium-sized businesses in India make faster, less expensive, and more reliable cross-border payments. To this end, the project will also make it easier for Indian banks to offer cross-border payment services to a broader range of countries. Speed and greater transparency are also among the benefits highlighted by observers.

Are you a fan of CBDCs? This week, the RBI reported that its central bank digital currency (CBDC) pilot has five million users and 420,000 participating merchants as of June 30. According to Reuters, transactions in the digital rupee are running at a pace of 100,000 a day, significantly below lofty expectations and hopes of one million transactions a day by 2023. It has also been pointed out that the digital rupee may suffer from competition with the country’s popular faster payments system, UPI.

Nevertheless, the digital rupee may be getting a bit of a boost courtesy of cryptocurrency exchange Bybit, which launched digital rupee payments on its platform this week. According to Cointelegraph, the digital rupee will be available as a wallet-based payment option, along with the exchange’s payment options in rupees via bank transfer, third-parties such as Paytm, and India’s Unified Payments Interface (UPI).

“By incorporating the eRupee payment, Bybit aims to elevate the payment experience for INR (Indian rupee) users, fostering trust and reliability in every transaction,” said Bybit sales and marketing director Joan Han. “Furthermore, this initiative is expected to attract a wider pool of merchants to the platform, driving business growth and expanding the reach of Bybit’s services within the market.”

Founded in 2018, Bybit is the second-largest cryptocurrency exchange by trading volume in the world, with more than 37 million users.

Here is our look at fintech innovation around the world.

Middle East and Northern Africa

Faye, an insurtech startup based in Israel, raised $31 million in Series B funding.

Egyptian B2B platform Cartona secured $8.1 million in a Series A extension round led by Algebra Ventures.

Israel-based financial crime detection company ThetaRayacquired screening company Screena.

Central and Southern Asia

Bangladesh-based fintech Nagad teamed up with Huawei Technologies.

The Reserve Bank of India approved cross-border payment licenses for BillDesk, Amazon Pay, and Adyen.

Texas-based migration fintech Vesti announced an expansion to Bangladesh, India, and Pakistan.

Latin America and the Caribbean

Caribbean-based PROVEN Bank partnered with Ireland’s Fenergo to enhance its transaction monitoring and AML operations.

Mexican fintech platform for the underbanked and microbusinesses Aviva raised $5.5 million in funding.

Rippleteamed up with the National Federation of Associations of Central Bank Servers (Fenasbac) to promote fintech innovation in Brazil.

Asia-Pacific

ADVANCE.AI launched its KYB business intelligence service to enhance its operations in Singapore and Malaysia.

Polish IT solutions provider Comarch announced a strategic partnership with DSK Bank.

The partnership will help accelerate a strategic digitization program the bank launched in 2021.

Comarch has been a Finovate alum for more than a decade, making its Finovate debut at FinovateEurope 2013 in London.

Comarch, an IT solutions provider and systems integrator based in Poland, has forged a strategic partnership with DSK Bank. The partnership will accelerate the Bulgaria-based financial institution’s ongoing strategic digitalization efforts, which began in earnest in 2021.

“We are delighted to support DSK Bank in achieving its digitalization goals with our cutting-edge IT solutions,” Comarch Group CEE Director Piotr Kusek said. “This partnership underscores our mutual commitment to introducing innovative strategies that will transform the banking landscape and elevate financial services to a new level.”

An international IT business solution provider, Comarch employs 6,400 engineers, business consultants, marketing specialists, and other professionals who help optimize operations and business processes for companies in a wide variety of verticals including telecommunications and financial services. Comarch’s clients include BP Global, Telefónica Global, and Vodafone Germany.

Part of the OTP Banking Group, DSK Bank is Bulgaria’s largest bank. The institution was founded in 1951, and has total assets of more than $15.8 million (€14.74 million). In the spring of 2022, DSK Bank teamed up with another Finovate alum, Backbase, to support its digital transformation efforts.

Founded in 1993 and headquartered in Kraków, Poland, Comarch made its Finovate debut at FinovateEurope 2013. Within a few years, the company reported revenues in excess of PLN 1 billion, hired its 5,000th employee, and opened its 90th worldwide office. Comarch launched its modern financial platform for business, Apfino, in 2021, and unveiled Poland’s first commission-free shopping platform, Wszystko.pl, in 2023.

This year, the IT solutions provider has extended its partnership with Dutch telecommunications operator KPN, teamed up with insurance company P&V Group – which will adopt Comarch’s Employee Benefits solution – and announced a collaboration with UAE-based telecommunications company and ICT player du. Last month, Comarch joined the European Loyalty Association, partnered with charitable organization The Blind Loyalty Trust, and secured accreditation as a Peppol Service Provider in Malaysia.

Loan intelligence system company Parlay will join Mastercard’s Start Path Small Business program. Parlay is one of eight companies selected.

Parlay’s technology complements a bank’s or credit union’s loan origination system to streamline and enhance small business loan processing.

Parlay made its Finovate debut at FinovateSpring 2024 in May as part of our Sustainability & Inclusion Scholarship program.

Parlay, which offers an AI-powered Loan Intelligence System (LIS) to help community banks and credit unions boost small business loan volume, is one of eight startups selected to participate in Mastercard’sStart Path Small Business program.

The incoming cohort consists of startups that have shown “dedication to democratizing financial tools and providing cutting-edge services for SMEs,” Mastercard noted in a statement. The statement underscored specific functions – such as spend management, onboarding, risk monitoring, loan approvals, and embedded finance solutions – that innovative fintech startups are helping digitize for small businesses.

Joining Parlay in the upcoming cohort of the program are Ballerine, Boost, CredibleX, Digi, Merge, Prime Dash, and RedOwl. The four-month program will give these startups the opportunity to leverage Mastercard’s network and subject matter expertise to forge product partnerships that help small businesses digitize their operations.

Parlay’s embedded fintech software helps lenders achieve a 64% increase in approved loans and an 87% reduction in manual underwriting workload. A white-label solution that complements loan origination systems, Parlay’s technology enables lenders to generate high-quality loan packets and maximize the eligible applicant pool. The company’s LIS also offers readiness insights to help businesses improve their creditworthiness; pre-screening to identify prime, marginal, and ineligible candidate pools; and pipeline analytics to enable loan officers to monitor applicant progress and underwriting eligibility.

“After a decade of work in economic development, our team realized that 77% of small businesses still struggle to access affordable capital and lack the insights need to navigate the lending process,” Parlay founder and CEO Alex McLeod said in a statement announcing the final eight startups invited to join the program. “We envision a future where community lenders, powered by Parlay’s AI-driven loan intelligence system, can get millions more small businesses approved for loans using unique, personalized insights that help both lenders and borrowers.”

Parlay made its Finovate debut at FinovateSpring in May as part of our Sustainability & Inclusion Scholarship program. The program is designed to spotlight underrepresented founders, as well as startups that are tackling issues such as climate change, diversity, and financial inclusion. Scholarships provide startups with complimentary demo participation, as well as the ability to network with our 2,000+ senior-level fintech attendees, fellow demoing companies, and more.

Past scholarship winners include Best of Show winning companies like Debbie, which won Best of Show at FinovateFall 2023, as well as Kobalt Labs and Remynt, both of which won Best of Show at FinovateSpring 2024.

Founded in 2022, Parlay is headquartered in Alexandria, Virginia.