This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Courtesy of a partnership with a pair of current customers, card issuing platform Marqeta is open for business in Australia. The company announced today that its arrival in the Asia-Pacific market will also help support fellow Finovate alum Klarna and customer Doordash as they expand in the country.

“Card issuing is on its way to being an $80 trillion global opportunity by 2030, and Marqeta is perfectly positioned to take advantage of this over the coming years,” Marqeta founder and CEO Jason Gardner said. “The Australian market relies heavily on card spending and is digitizing rapidly. It is a market that was important to our customers and where we saw a lot of potential for Marqeta technology to help revolutionize customer experience in payments.”

Marqeta’s announcement comes in the wake of news that the company – in partnership with Visa – had earned certification to process payments in 10 countries in the Asia-Pacific region. In Australia, the first market in the APAC where Marqeta’s services will be available, the company hopes to take advantage of both the high penetration of traditional bank accounts compared to the rest of the region, as well as a boom in digital payments.

With the first transactions facilitated by Marqeta in late January, partner Klarna is already appreciating the results. “Our close collaboration in bringing an entirely new product offering and shopping experience to the Australian market in record time has been a big success,” Koen Koppen, Klarna CTO, said. “The positive reaction of Australian consumers is evident in just how many are downloading and using the app and virtual card each day.”

An alum of our developers conference, Marqeta delivered a presentation on Democratizing Issuer Payment Processing with Just-in-Time Funding at FinDEVr Silicon Valley in 2016. The Oakland, California-based company was last valued at nearly $2 billion, following a May 2019 Series E round that added $260 million to Marqeta’s coffers.

When it comes to defending your data, Enveil’s speciality is helping prevent you from losing it while you’re using it. The company, which picked up $10 million in funding last month and made its Finovate debut at FinovateFall in 2017, enables businesses to securely perform analysis on encrypted data at scale.

“Over the past three years, we’ve successfully created a market, solidified customer use cases, executed enterprise deployments, and expanded our capabilities, for protecting data in use where it is and as it is today,” company CEO and founder Ellison Anne Williams explained when the company’s Series A round was announced. She added that the funding will help the company market its ZeroReveal product suite on a “global scale” and, indeed, the company announced just a few days later that it was opening a new office in London.

Enveil VP of Sales Craig Trautman referred to the London opening as “an important first step toward expanding our footprint in the regions most directly affected by evolving global regulatory standards.”

Founded in 2016, Williams launched Enveil after years of working with institutions like the National Security Agency – where she was a Senior Researcher for more than ten years – and Johns Hopkins Applied Physics Lab. She has leveraged this experience – and advanced degrees in mathematics (algebraic combinatorics and set theoretic topology) and computer science (machine learning) – into building one of the more innovative companies in the secure data collaboration / privacy enhancing technologies industry.

In a commentary for Dark Reading last month, Williams explained how a focus on securing data itself is one of the best ways for companies to negotiate an ever-shifting regulatory environment. To avoid the “hamster wheel of compliance,” she argued, businesses should learn how to secure data rather than the “networks, applications, and endpoints” that data uses.

The biggest challenge with securing data is that one of its most critical states – the state of being used – is also the most challenging state to secure. Compared to data that is not being used – data either at rest or in transit – data in use, according to Williams, represents the “point of least resistance” for the latest generation of cybercriminals. This is in large part because many of the technologies to secure data in use have historically not been “practical enough for commercial use.”

And this is where Enveil comes in. By discovering a way to apply technologies like homomorphic encryption, that are effective defenses for data in use, in a commercial context, Enveil offers businesses in verticals ranging from financial services and supply chain finance to cloud security and healthcare a way to securely work with secure data without having to decrypt it.

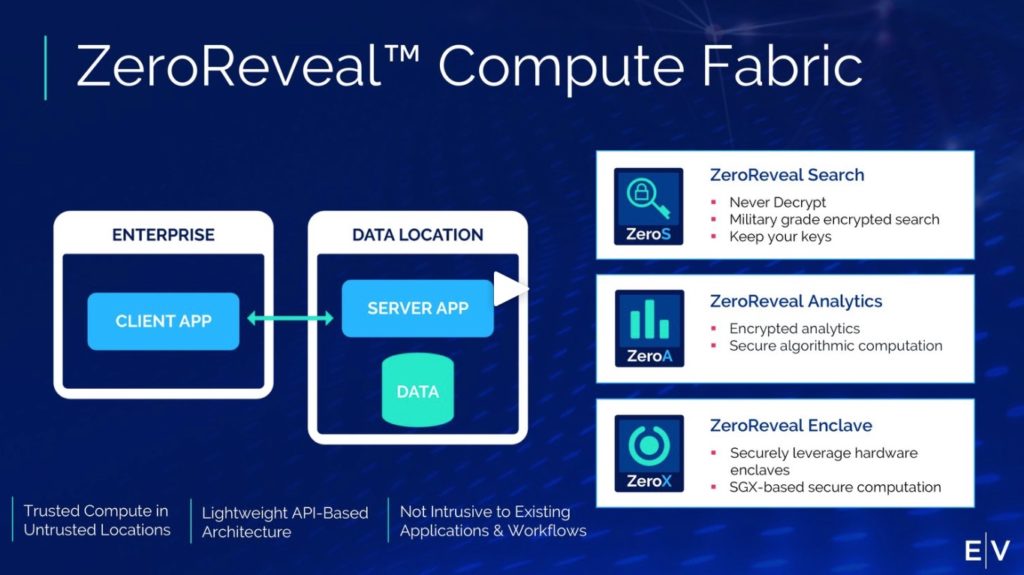

Enveil’s flagship solution, its ZeroReveal Compute Fabric, is a two-party platform of a ZeroReveal Client application which resides within the enterprise, and the ZeroReveal Server application, which is located where the data is kept. Via standard APIs, the technology works alongside the business’s current protections to provide security during the data processing lifecycle. Within this solution, Enveil offers functionality to power searches of secure data (ZeroReveal Search), conduct analytic investigations on encrypted data (ZeroReveal Analytics), and support the use of secured enclaves like Intel’s SGX (ZeroReveal Enclave).

In addition to expanding geographically, Enveil is also looking to add to its team. The company is specifically looking to bring on engineering talent to support new products, as well as additional sales and marketing team members to help drive Enveil’s efforts overseas.

“Enveil is stepping up to solve a fundamental security challenge: preserve privacy while ensuring that data remains usable,” C5 Capital Managing Partner Zulfe Ali said. “By empowering organizations to secure data throughout its lifecycle, Enveil’s contributions go beyond adding business value and ensuring compliance.”

A new partnership between intelligence-driven security operations platform ThreatConnect and account takeover prevention solution provider SpyCloud will help individuals take action during the critical time between credential exposure and account breach.

Two of ThreatConnect’s solutions – its Security Orchestration, Automation, and Response (SOAR) and Threat Intelligence Platform (TIP) work jointly to help spot and respond to potential cyber threats. Adding Spycloud’s database of exposed credentials will enable ThreatConnect to more comprehensively scan for personally-identifiable information – email addresses, usernames, passwords, and more – that may be exposed and available for exploitation by cybercriminals and fraudsters shopping for credentials on the dark web.

“Our customers know that poor user password habits put accounts at risk,” ThreatConnect Integrations Product Manager Richard Cody said. “Having access to SpyCloud’s dataset through our platform means they can detect and remediate credential compromises before account takeover attacks begin.”

Austin, Texas-based SpyCloud earned a Best of Show award for its FinovateFall demonstration of its Exposed Credential Monitoring and Alert service. SpyCloud uses human intelligence-gathering strategies to identify and recover stolen assets from threat actors and private sources before they are traded on the dark web. As a result of this approach of going beyond automated solutions and webcrawlers, the company’s technology has resulted in the capture of 40 million exposed assets every week. In addition, SpyCloud also helps protect company employees from future account takeover attacks via its integration into their current authentication system.

“The data we provide to ThreatConnect customers through this partnership will not only allow them to prevent damaging account takeover attacks, but should also give them a better understanding of credential management habits among their employee and customer bases,” SpyCloud Chief Strategy Officer Chris LaConte explained. He added that making password remediation automatic and relying on NIST (National Institute of Standards and Technology) guidelines for strong, secure passwords are key components of robust cybersecurity and reducing the risk of data breaches.

Last fall, SpyCloud introduced a new suite of automated solutions to support password security maintenance in Microsoft Active Directory. The company has raised more than $28 million in funding, most recently securing $21 million in a round led by Microsoft venture fund, M12. Ted Ross is CEO and co-founder.

Kyndi, Featurespace, Onfido Recognized as AI Innovators in Fintech – A trio of Finovate alums are among the 100 companies highlighted by CB Insights in its newly-available report, AI 100: The Artificial Intelligence Startups Redefining Industries. The report, CB Insights’ 4th edition, focuses on companies that are innovating in the fields of “synthetic voice, quantum machine learning, protein modeling, and more.”

Top level takeaways from the report include the fact that 10% of the companies in the 2020 AI 100 are unicorns with a valuation of more than $1 billion. Most of the companies (65%) are U.S.-based, with Canada and the U.K. coming in second with eight startups each. China has six companies represented in CB Insights’ AI roster.

Kyndi demonstrated its Explainable AI platform at FinovateSpring 2018. The technology leverages machine learning to streamline regulated business operations and provide auditable AI systems. The company was founded in 2014, and is headquartered in San Mateo, California. An alum of FinovateFall, U.K.-based Featurespacedemonstrated its ARIC Fraud Manager at FinovateFall 2016. This solution uses machine learning and adaptive behavioral analytics to identify potential fraud based on anomalous behavior.

Demonstrating its Facial Check with Video solution at FinovateFall 2018, Onfido showed how its technology used machine learning to compare images on identity documents with facial biometric data and digitally verify people’s identities.

Agora Scores $2 Million in Funding – Digital platform banking solution provider Agora is in the process of securing $2 million in funding. News of the investment comes as the company announces opening a new headquarters in Atlanta, Georgia.

“We selected Atlanta because the region provides us the best combination of access to business development and talent, while also being a part of the growing fintech community,” Agora Services founder and CEO Arcady Lapiro said. Agora made its Finovate debut last year at FinovateSpring, demonstrating its mobile banking solution for teenagers.

Regional banks and credit unions leverage Agora’s technology to provide a digital experience for their customers without having to replace their core banking systems. Agora enables institutions to offer their customers popular digital banking and financial management solutions such as shared accounts, PFM, card controls, money pools, and children’s account management.

“In order for financial institutions to remain competitive,” Lapiro said, “they must have the latest and most robust digital offerings. Banks have to move beyond a website, a standard app, or mobile check deposit. They must compete with the latest fintech technology.”

Here is our weekly look at the latest news from our Finovate alums.

ECOMMPAY becomes the first PSP to integrate with the new PayPal commerce platform.

Singapore Exchange acceptsAyondo’s application to extend submission deadline for its proposal to resume trading.

MYHSM partners with ACI Worldwide to integrate its Hardware Service Module into ACI’s UP platform.

TransferWisegoes live in Portugal in partnership with Activo Bank.

Fiservacquires merchant services company MerchantPro Express.

Leading Vietnamese commercial bank, MSB, will deployMambu’s cloud-native banking platform by the end of this year.

Vantage Bank Texas to deploy digital banking technology from Backbase.

Forte Payment Systemslaunches its new BillPay solution.

TurnKey Lenderpartners with Cambodia-based Sambat to bring real-tie decisioning to their loan application processing.

DemystData to provide contextual data for SparkBeyond.

Roostifyexpands deal with TD Bank to include home equity loans and lines of credit.

HousingWire namesLoan Scorecard a 2020 HW Tech100 Mortgage Winner.

Larkyjoins Visa’s Fintech Fast Track program to integrate Larky’s nudge engagement platform with VisaNet’s global payment network.

New Hampshire Mutual Bancorp migrates to Jack Henry & AssociatesSilverLake System core platform

Finovate Alum Features and Profiles

PayPal Takes to the Google Cloud – Google Cloud has unveiled its latest data center and announced that PayPal will be among the first to move key components of its payments infrastructure to Google’s cloud region.

Conversational AI Innovator Clinc Inks Partnership with Visa – Courtesy of a newly-announced partnership between Visa and the conversational AI innovator, customers of participating banks and credit unions will be able conduct a wide variety of banking operations by communicating directly with their bank accounts using natural, conversational language.

How a Banking License Evolved Neo’s Vision – Neo was founded in 2017 with a vision, as described by CEO Laurent Descout, “to create a platform that can replace the old fashioned banking platform. A true ‘one-stop shop’ that offers all the financial products a corporate client needs to operate in a global environment.”

New Investment Gives Ant Financial a Minority Stake in Klarna – Chinese conglomerate Ant Financial has purchased a minority stake in Sweden’s e-commerce payments innovator Klarna. The terms of the investment were not disclosed, but the company said that the funding amounts to a 1% stake.

Equifax Adds Rental Payment History to Credit Insights – Consumer insights company Equifax is partnering with U.K.-based Credit Ladder, a rent reporting service. Under the partnership, Equifax will leverage data from Credit Ladder to help tenants who pay their rent on time access fairer credit rates.

Thought Machine Locks in $83 Million in Growth Funding – U.K.-based, cloud native, core banking technology provider Thought Machine has just secured Series B funding that will help the U.K.-based company expand into the Asia-Pacific.

The ruling is subject to appeal. But for now, advocates for cryptocurrency trading in India have won the day: the Supreme Court of India has overturned a ban on cryptocurrencies that was issued by the Reserve Bank of India in 2018.

Specifically, the Reserve Bank forbade Indian banks from working with cryptocurrency exchanges out of concerns ranging from “consumer protection” to “market integrity.” And while India’s participation in the worldwide cryptocurrency market is modest (less than 5% when the ban was instituted), the reaction to the ruling was strong, with a number of cryptocurrency exchanges challenging the Reserve Bank in court. This week, the court sided with the exchanges, observing that no bank regulated by the Reserve Bank had been negatively affected by cryptocurrency trading before the ban, and that a complete ban was thus a disproportionate response.

That said, the ban is not yet a settled matter. The RBI plans to file a review petition with the Supreme Court, again citing systemic risk concerns for the country’s banking system should trading in cryptocurrencies be permitted. As of now, however, cryptocurrency exchanges and platforms in the country are free to operate, legal experts say.

FinovateAsia alum TurnKey Lender will help leading Cambodian financial services institution Sambat improve its loan application processing courtesy of a newly-announced partnership. Sambat, which serves both retail customers as well as micro, small, and medium-sized businesses, will use TurnKey Lender’s Unified Lending Solution to accelerate loan decisioning, increase portfolio profitability, and boost customer lifetime value.

TurnKey Lender CEO Dmitry Voronenko praised Sambat as one of Cambodia’s “early adopters of the fully digital approach to banking.” Managing Director for Sambat Harvey Poh called the deployment a “major milestone” and “a testament to our commitment to deliver digital financial services to our customers.”

Founded in 2014, TurnKey Lender has a U.S. headquarters in Austin, Texas, and maintains offices in Singapore; Kuala Lumpur, Malaysia; and the Philippines. The company was recognized by Frost & Sullivan’s Asia-Pacific Best Practices Awards at the beginning of the year, taking home top honors in the Singapore Fintech Industry New Product Innovation category.

Here is our weekly look at fintech around the world.

Latin America and the Caribbean

Brazilian challenger bank Nubank launches its Nu credit card in Mexico.

Chilean venture capital fund Magma Partners closes its $50 million fund, the largest ever raised by the firm.

Peruvian fintech Ayllu announces project to map out of all the fintech startups in the country.

Asia-Pacific

Turnkey Lenderforges partnership with leading Cambodian financial institution, Sambat Finance.

Mastercard to play leading role in Series B investment for Indonesian fintech Digiasia.

Sub-Saharan Africa

Cointelegraph takes a deep dive into the emerging fintech economies of Kenya, Ethiopia, and Ghana.

A new payment license requirement may complicate life for Nigerian fintechs.

FLASH International, based in the Democratic Republic of the Congo, announces an initiative to fund fintech startups in the country.

Central and Eastern Europe

Wirecard partners with Estonia-based Xolo to serve the gig economy.

Finovate’s sister publication, Fintech Futures, profiles Polish digital banking provider and Finovate alum Efigence.

Polish asset manager Skarbiec TFI teams up with fintech solution provider NeoXam to enhance its portfolio management.

Middle East and Northern Africa

The UAE’s National Bank of Fujairah to leverage the RippleNet network to provide real-time, cross-border fund transfers to India.

Dubai International Financial Center announces a tripling of the size of its Fintech Hive.

Monoco’s Privatam, which offers structured investment products, goes live in Dubai.

Central and Southern Asia

Indian SME lender SMEcorner raises $30 million in Series B funding.

Supreme Court of India overturns Central Bank’s ban on cryptocurrency trading.

Leap Financial, a fintech platform that specializes in providing financing to Indian students studying abroad, secures $5.5 million in round led by Sequoia India.

U.K.-based, cloud native, core banking technology provider Thought Machine has just secured Series B funding that will help the U.K.-based company expand into the Asia-Pacific. The $83 million raised this week, courtesy of a round featuring all of the company’s existing investors, takes the firm’s total capital to more than $106 million.

Valued at $143 million at the time of its Series A round in 2014, Thought Machine is currently believed to be worth between $220 million and $320 million.

Thought Machine founder and CEO Paul Taylor said that the funding had arrived at a “pivotal stage” in the company’s development, citing both “healthy” revenues and “huge” customer demand. “As well as international expansion we will put further investment into our core technology,” Taylor said, “ensuring that banks will always have the best possible cloud native platform, and allow them to keep up with technology breakthroughs in the future which bring agility, security, resilience, and good economics.”

An alum of European fintech conference, the company demonstrated its core banking solution, Vault, at FinovateEurope 2018 . With this technology, Thought Machine enables both incumbent and challenger banks to operate and compete with a cloud-based offering of their own. Vault offers institutions checking and savings accounts, well as credit cards, loans, and mortgage financing.

Last fall Thought Machine announced a partnership with Standard Chartered’s new digital bank in Hong Kong, and unveiled a new collaboration with Swedish financial group, SEB. Both deals will feature deployment of Thought Machine’s Vault platform.

After expansion to Australia and Japan, Thought Machine plans to go live in the United States later this year.

The news that Jassby, a PFM app for kids, has raised $5 million in new funding is one small step for savings solutions and one giant leap for financial education.

The Family Finance App, which has more than 100,000 users, enables kids to receive money from parents and grandparents, which they can then save, spend, or donate in a safe, supervised “Walled Garden”-style, digital platform. Jassby notes that the combination of a digital wallet and a shopping tool – along with parental participation – will help kids learn responsible financial habits by connecting what they have to what they want. This can be a more effective way of learning than simply studying lessons on smart financial habits and then taking tests and quizzes to see if the material is truly understood and absorbed.

Benjamin Nachman, Jassby CEO, called the promotion of financial literacy “one of our core values.” He added “we have built a cutting-edge system that allows us to partner with schools, sports clubs, and businesses to create a full ecosystem for our users.”

“Jassby has created a holistic digital financial ecosystem for kids, teens and their parents,” Moneta Managing Partner Adoram Gaash said. “(Jassby) deals with the real issue of financial illiteracy, and lets kids use financial services in a very smart way.” The app is currently available as a downloadable iOS solution, as well as a web app.

The round, which takes Jassby’s total capital to $10 million, featured participation from Needham Bank and Moneta Capital, as well as Blumberg Capital, Correlation VC and PnP Ventures. The company said the funding will help speed development and take the app to one million users within a year. Nachman added that the company also plans on raising an additional $20 million later this year to help reach that goal.

Jassby is headquartered in Waltham, Massachusetts, and was founded in 2018. Last fall, the company announced a partnership with Needham Bank to enable banking services for users of its family financial app. The fintech has also teamed up with Boston Siege Football club, signing on the semi-pro soccer club as a corporate sponsor. Boston Siege began wearing Jassby’s logo on its kits and training gear last year. The two organizations are planning on a project involving the club’s payment and revenue infrastructure in 2020.

Chinese conglomerate Ant Financial has purchased a minority stake in Sweden’s e-commerce payments innovator Klarna. The terms of the investment were not disclosed, but the company said that the funding amounts to a 1% stake in Klarna. The most recent assessment of Klarna, based on a $460 million funding round in 2019, puts the company’s valuation at $5.5 billion.

“Alipay, and the wider Alibaba Group, have truly set the global pace on retail innovation and the app economy,” Klarna CEO Sebastian Siemiatkowski said. “We are delighted in this confidence shown in Klarna in defining the future of payments and shopping and are very much looking forward to working together further in the future.”

The investment comes as a tonic in the wake of Klarna’s first annual loss of $113 million in 2019. It also represents a deepening of the partnership between the two firms that will make more of Klarna’s buy now pay later solutions available to consumers and merchants in the Alibaba ecosystem. This includes more integration between Klarna and Alibaba’s Alipay which, via AliExpress, Alibaba’s retail online marketplace, leverages Klarna’s e-commerce solution.

“At the heart of this cooperation between Klarna and Alipay is a shared ambition of innovating truly superior shopping experiences and creating destinations of inspiration for consumers across the world,” Siemiatkowski said.

More than 200,000 merchants and e-commerce platforms around the world are powered by Klarna technology. The company’s partners include IKEA, Adidas, Spotify, and Expedia Group, among many others, and in 2019 alone, Klarna added more than 75,000 new merchants to its platform. Founded in 2005 and a Finovate alum since its debut at FinovateSpring in 2012, Klarna has 2,700+ employees and is live in 17 countries. Late last month, the company announced that Klarna had reached the seven million customer milestone and 1.6 million app downloads.

The number of women in technology in general, and fintech in specific, is growing. That’s the good news.

As Julie Bort and Rachel Sandler wrote in their 2018 feature on female engineers for Business Insider, “for all the arm waving about the lack of women in STEM professions, the truth is, there are some powerful role-model female engineers having fabulous careers and creating tech used by millions, if not billions of people everyday.”

A report from consulting firm Korn Ferry supports this. The study, conducted last year and looking at the top 1,000 U.S. companies by revenue, noted an increase of 2% in the number of women who held the role of CIO or CTO last year. “The industry with the highest percentage of women CIOs/CTOs,” the report noted “is financial at 25%.”

By comparison, the number of women fulfilling the role of Chief Technology Officer within the tech industry remains fewer, maybe even far fewer, than you might suspect. By industry, Korn Ferry ranked technology behind financial, healthcare, retail, and consumer, besting only the services industry.

Women like Padmasree Warrior, who served as Cisco Systems’ CTO between 2007 and 2015 and, before that, as CTO for Motorola for four years, have been among the relatively few women at the top tier of technology leadership – especially at the largest tech companies. Elissa Murphy, at GoDaddy, Selina Tobaccowala at SurveyMonkey, and Raji Arasu at StubHub are just a few of the female CTOs in charge of technology at some of our economy’s newer, most innovative companies.

Pamela Rice, former SVP of Technology at OnDeck and current CTO of Earnest, during her presentation at FinDEVr Silicon Valley.

Turning to fintech – and our own experience at Finovate – a woman like Pamela Rice comes to mind. The former Senior Vice President of Technology at OnDeck who represented the company at our developers conference FinDEVr, Rice is currently Chief Technology Officer for Earnest. The San Francisco, California-based company she joined in 2019 provides consumer financing options for underbanked populations including recent college graduates. Last summer, she participated in a company-hosted, Tech Meet-Up on Diversity and Inclusion, sharing her thoughts on the value of making diversity “part of the DNA of everything you do.”

We took a look at how the fintech industry was faring in terms of female representation at the CTO level. There is still a great deal of progress to be made. Here is a sample of the women who are increasingly providing technical leadership for fintechs large and small.

Marianna Tessel – Intuit – With more than 20 years experience as a VP of Engineering for companies like Ariba, Docker, and VMWare, Tessel took the helm as Intuit’s Chief Technology Officer in January 2019.

Educated at Technion – Israel Institute of Technology and the Weizmann Institute of Science – and having served as a captain in the Israeli Army – Tessel was praised by new Intuit CEO Sasan Goodarzi as a “transformational change agent” who has created “an engineering culture that has accelerated innovation.”

At Intuit, Tessel is responsible for leading the company’s product engineering, data science, information technology, and information security teams around the world. She first joined Intuit in 2017, leading product development for the firm’s Small Business and Self-Employed Group, including the company’s QuickBooks product family.

Rija Javed – MarketFinance (formerly MarketInvoice) – After more than four years as an engineer for Wealthfront, including roles as Director and Senior Director, Javed joined U.K.-based MarketFinance as the company’s Chief Technology Officer in 2018. This made her one of the first female fintech CTOs in the country.

“Having Rija on board underlines our focus on hiring the best talent and building innovative technology to deliver business finance solutions,” MarketFinance CEO and Co-founder Anil Stocker said. “It’s the foundation we’ll use to help thousands of business(es) access funding quickly and easily.”

While at the Wealthfront, Javed built the company’s first mobile app. Transitioning to the company’s investment products platform, she helped scale Wealthfront’s offerings including the development of a new brokerage and banking platform. With degrees in Electrical and Computer Engineering from the University of Toronto, Javed is also a mentor for the New York Academy of Sciences.

Ekate Kuznetsova – Token Transit – Sometimes the only way for a woman to make sure that there’s a woman’s place at the tech table is to build the table herself. That’s the approach of Kuznetsova, who parlayed her experience in software engineering at Akamai and Google into launching a fintech startup of her own. Token Transit, for which Kuznetsova is founder, CEO, and Chief Technology Officer, provides mobile ticketing and payment verification solutions for public transportation.

Launched in 2016 and available in more than 75 cities in the U.S. and Canada, Token Transit enables people to pay for fares and passes with their credit, debit, or commuter benefits card and provides them with a digital ticket that is stored on their smartphone.

Kuznetsova earned her Bachelor of Science degree from Massachusetts Institute of Technology, where she studied Mathematics and Computer Science.

While the ranks of female CTOs in fintech remains modest, it should be mentioned that there are women – from VPs of Engineering to Chief Scientists – who are not only currently leading tech teams, but also are likely among the CTOs of tomorrow. For a peek at one shortlist, check out Angie Chang’s spotlight on 21 female executives who could become one of the Fortune 100’s next CTOs.

Know a woman who’s driving technology innovation at one of your favorite fintechs? Send us a note at [email protected]!

Financial institutions leveraging Visa APIs can now enable voice-first digital banking technology from Clinc. Courtesy of a newly-announced partnership between Visa and the conversational AI innovator, customers of participating banks and credit unions will be able conduct a wide variety of banking operations by communicating directly with their bank accounts using natural, conversational language. No special keywords, phrases, or scripted questions.

“Our goal has always remained the same – to create technology that makes people’s lives easier,” Clinc co-founder and interim co-CEO Lingjia Tang explained. “Partnering with a leader like Visa is a milestone for Clinc, and this API integration is going to offer small and mid-size banks a similar experience that some of the largest banks in the world are using.”

The collaboration will allow digital banking customers to check balances, transactions, and spending history; pay bills and transfer money; as well as perform financial management functions such as creating payment plans, checking rewards programs, and disputing transactions. Customers will also be able to conduct a wide variety of card management operations ranging from turning cards on and off, reporting and reissuing lost or stolen cards, and activating new cards – all using their natural voice in a conversational way.

“This is the kind of capability and cutting-edge AI wouldn’t be otherwise be accessible without Visa, ” Tang added.

Clinc’s partnership with Visa is the latest example of how the Ann Arbor, Michigan-based company is helping banks enhance the customer experience. Founded in 2015 and making its Best of Show-winning Finovate debut a year later at FinovateFall, Clinc teamed up with Singapore’s OCBC Bank last year, helping the bank launch its voice-enabled mobile banking assistant. The company has also partnered with Turkish bank Isbank, powering one of the most widely-deployed mobile banking voice assistants, with more than six million users.

Clinc has raised $60 million in funding. The company picked up the lion’s share of that amount last spring in a $52 million Series B round.

Google Cloud has unveiled its latest data center and announced that PayPal will be among the first to move key components of its payments infrastructure to Google’s cloud region. The news is the latest example of a partnership between the two technology giants that extends back at least as far as 2017, when PayPal became an authorized payment method for Android Pay (which later became Google Pay).

The new cloud region, Google’s 22nd globally, will be based in Salt Lake City and is designed to provide customers in the western U.S. with better, more reliable cloud services.

“When it comes to processing a financial transaction, security and speed count,” PayPal VP for Employee Technology & Experiences and Data Centers Dan Torunian said. He added that Google Cloud will provide PayPal with the “security, quality, and velocity” it needs, particularly when it comes to managing seasonal payment transaction volume surges and keeping regional expansion costs low.

In fact, PayPal reportedly chose Salt Lake City in part for low-latency access to its own data center, which will make it easier for PayPal to commit additional resources to the cloud over time. The partnership will also allow PayPal to establish a migration pattern that can be used to convert more on-premises infrastructure to the Google Cloud – at the Salt Lake City data center or to any other Google Cloud platform region.

More than 300 million consumers and merchants in 200 markets use PayPal’s payments technology for financial services and commerce. The San Jose, California-headquartered company began the year forging a strategic partnership with UnionPay International that will boost its merchant and consumer business in the Chinese market. PayPal reported adding more than 37 million net new active accounts last year, processing “nearly $200 billion” in total payment volume in the fourth quarter alone.

Two of the biggest themes in fintech – digital identity and the rise of fintech in Central and Eastern Europe – meet in the latest announcement from biometric authentication specialist and Finovate Best of Show winner iProov. The company’s facial recognition technology now makes it easier for users of SK ID Solutions’ Smart-ID Service in countries like Estonia, Latvia, and Lithuania to renew their accounts without having to visit a physical bank branch.

“This is a major development for all digital identity providers,” iProov CEO Andrew Bud said. “Estonia has proved, for the first time, that a remote, automated, biometric ID verification service can deliver the highest possible levels of security.”

Recognized as equal to a handwritten signature throughout Europe, Smart-IDs enable users to authenticate themselves and provide permissions online using a smartphone app. iProov’s facial recognition technology adds a three-second scan to compare the image of the user to the image on their presented ID document to help defend against fraud and identity theft.

Smart-ID also leverages NFC-based ReadID document verification technology from InnoValor.

Financial crime risk management innovator Featurespace will be helping Enfuce combat fraud and money laundering courtesy of a newly announced partnership. Enfuce, a financial services firm based in Finland, will use Featurespace’s ARIC Risk Hub to enhance its ability to protect its customers from fraud and financial crime.

“Our clients deserve industry-leading services that allow them to freely and fully concentrate on the success of their core business, without worrying about ever-evolving fraud,” Enfuce co-founder and chair Monika Liikamaa said.

ARIC Risk Hub offers real-time transaction monitoring for fraud and financial crime, enabling institutions to identify and act against anomalous and potentially dangerous behavior as it occurs. The technology also reduces the number of false positives by as much as 70%, keeping anti-fraud processes efficient. Featurespace introduced its fraud-fighting technology to Finovate audiences at FinovateEurope 2016.

Here is a round up of recent news from our Finovate alumni.

Sezzleunveils new logo along with its first annual report.

Flybitsexpands its executive team in New York, Toronto, the U.K., and Dubai.

Yseop and Automation Anywhere join forces to scale intelligent automation.

Lighter Capitalappoints Kevin Fink at CTO and Patricia Elliott as CSO.

InCommlaunches Roblox gift cards in France and Germany.

Finovate Alum Features and Profiles

Revolut’s $500 Million Round Boosts Valuation to $5.5 Billion – Global financial platform Revolut has secured its place as the U.K.’s most valuable fintech.

Dealing with Deepfakes in Fintech – The fintech industry is ripe with security firms, such as iProov, that use AI to combat both video and audio deepfakes with anti-spoofing technologies.

Envestnet | Yodlee Acquires Indian Data Aggregator FinBit.io – Envestnet | Yodlee has acquired another asset in its strategy to further grow and develop its data aggregation and analytics business.

Meet Sonect: Cash Network Builder, Finovate Newcomer, Best of Show Winner – What’s better than having a large pizza with all your favorite toppings delivered to your front door? How about a side order of cash, saving you a trip to the ATM or bank branch?

Azimo Taps Ripple for Cross-Border Payments to the Philippines – Fueling these payment transfers is Ripple’s On-Demand Liquidity (ODL) solution that uses XRP to source liquidity and complete money transfers within three seconds.

Lendio Lands $55 Million to Match Small Businesses with Lenders – The investment more than doubles the company’s previous funding, bringing its total to $108.5 million.

SheerID Expands Identity Marketing Platform – The move enables brands to identify and acquire new customers across the globe.