This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Conversational AI technology company Gridspace announced new emotional intelligence capabilities for its virtual voice agent Grace.

The update enables Grace to respond more swiftly and empathetically, and enhances the agent’s ability to express its own emotional states.

Gridspace made its Finovate debut at FinovateFall 2022 in New York.

Voice technology and AI software innovator Gridspaceunveiled new emotional intelligence capabilities for its virtual voice agent Grace. The new capabilities enable Gridspace’s voice agent for business to respond faster and more empathetically to the speaker’s emotions. The enhancements also improve Grace’s ability to express its emotional states.

“Grace’s new emotional intelligence capabilities make voice calls with Grace even more natural,” Gridspace CEO Evan Macmillan said. “We are excited to further advance customer satisfaction with voice agents and make it even easier for businesses to deploy them.”

Bringing emotional intelligence capabilities to voice agents is a major advance in spoken dialog systems, according to Gridspace. Because so many contact center interactions involve customers experiencing frustration, being able to respond appropriately is paramount. Grace’s enhancements will enable the voice agent to manage more complex interactions with greater nuance, and also act as a buffer for high-volume contact centers. To this point, human agents working with Grace have reported not only being able to spend more time on complex calls, but also are experiencing less stress, lower burnout rates, greater productivity, and higher job satisfaction.

Founded in 2012, Gridspace made its Finovate debut at FinovateFall 2022. The California-based company was created through a collaboration between SRI Speech Labs – the entity behind Siri – and a diverse team of designers and engineers. Gridspace has been innovating in fields such as high-performance voice telephony, automated speech recognition (ASR), hyper-realistic TTS (text-to-speech), low-latency spoken dialog systems, as well as tools and solutions to help institutions deploy and manage conversational AI.

Gridspace has raised more than $27 million in funding and includes Private Investors and USAA among its investors.

A look at the companies demoing at FinovateFall in New York on September 9 and 10. Register today using this link and save 20%.

BankShift

BankShift is a brand-on-banking ecosystem for digital banking platforms, crafted by humans with experience in digital-first and data-driven innovations from leading financial institutions and brands.

Features

Leverage free API gateway for real-time vendor monitoring

Elevate operations and engagement with intuitive web admin portal

Scale platform with patent-pending branding technology

Who’s it for?

BankShift harmonizes brands with banking technology, enabling community banks and credit unions to seamlessly embed their digital banking ecosystems within a brand’s app to create new revenue streams.

Carrington Labs

Carrington Labs empowers financial institutions with explainable AI solutions to enhance credit risk scoring and loan limit recommendations, driving more informed and inclusive lending decisions.

Banks, credit unions, payment providers, and financial institutions focused on unsecured consumer lending.

Delfi Labs

Delfi Labs is a financial technology company that provides an AI-enabled SaaS copilot to help enterprises of all sizes protect themselves from financial market volatility.

Features

Non-generative AI, Oracle: provides actionable strategies in minutes

Risk analytics, Overwatch: offers advanced simulations for markets, balance sheets, and securities

Delivers powerful yet intuitive dashboard

Who’s it for?

Delfi’s initial focus is to serve community banks, credit unions, and financial asset managers in optimizing their balance sheets and structuring risk management strategies in real-time.

Odynn

Odynn is an embedded fintech, AI/ML, loyalty optimization program management platform for travel tech. Odynn has re-imagined customer loyalty while generating significant revenues for its partners.

Features

Delivers next-gen program management platform (holistic travel portal)

Offers live pricing in points, miles, and cash, for every major travel loyalty program

Generates personalized redemption recommendations for end users

PointChain is an intelligent risk management platform designed to bring proactive compliance and risk controls to the forefront. They are focused on delivering real-time transaction monitoring and regulation filings.

Features

Illustrates real-time transaction monitoring

Highlights how a bank can deal with a flagged transaction (Request for Information)

Includes intelligent SAR/CTR Filings

Who’s it for?

Banks, credit unions, credit card companies, and financial service providers who are required to implement and adhere to stringent BSA and AML policies.

Speakeasy

Speakeasy enables fintechs and financial institutions to grow API user adoption and streamline integrations with auto-updated robust SDKs, Terraform providers, and documentation.

Features

Accelerates integrations with SDKs

Prevents breaking changes with testing

Guarantees consistency with governance

Who’s it for?

Any company working in the financial space that has an API — whether available to the public or for private, internal company use only.

Zingly.ai

Zingly.ai empowers businesses to deliver value across the entire customer journey by seamlessly blending data, GenAI, and humans in persistent digital spaces for personalized, lasting relationships.

Features

Creates persistent digital spaces for ongoing, personalized customer interactions

Delivers seamless integration of data, GenAI, and human touch

Offers goal-oriented GenAI for acquisition through support and upsell

Who’s it for?

Zingly.ai serves businesses from Fortune 500-scale to SMBs in banking and financial services.

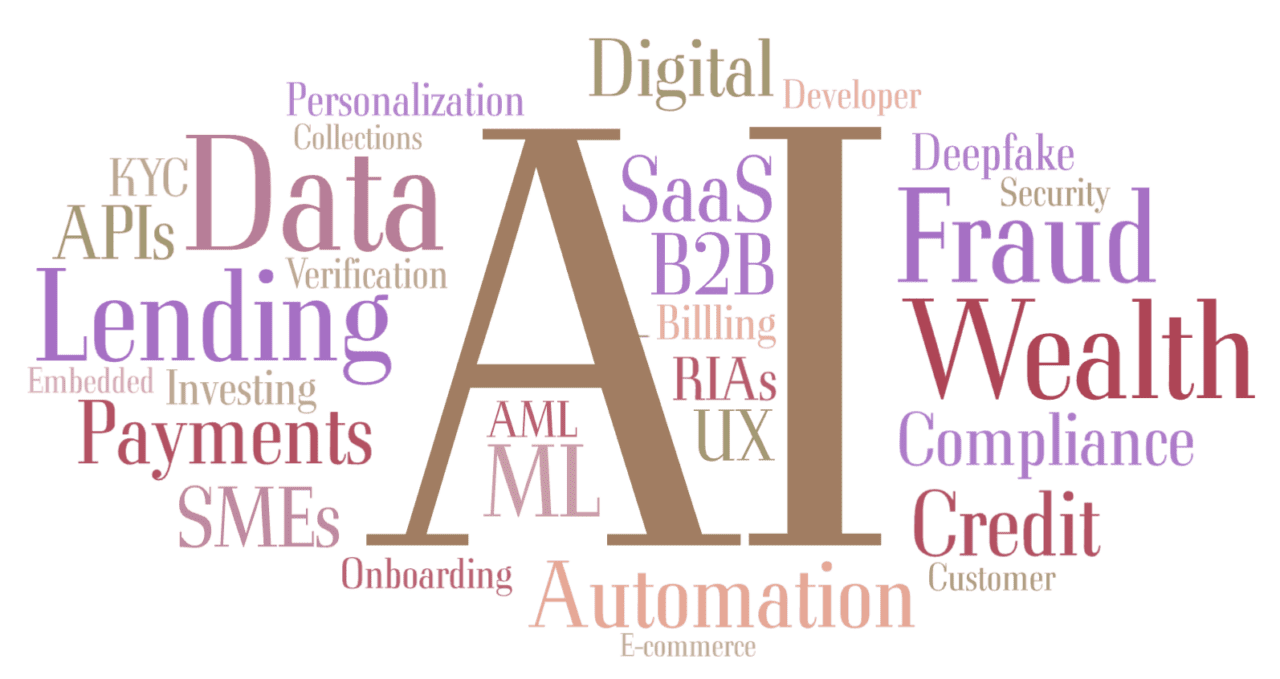

What themes will dominate the conversation at FinovateFall next month in New York (September 9-11)?

Many of the popular themes in recent years still endure. The customer is still king. Data and personalization matter. And payments, in the words of one clever panelist many Finovates ago, continues to be the “gift that keeps on giving.”

But in some ways these issues have been, if not eclipsed, then perhaps subsumed by enabling technologies like AI, machine learning, and what I call “Automation 2.0” – the leveraging of AI technology to automate a growing range of business operations and manual tasks.

These technologies have brought new energy to sectors such as lending and payments. They have raised the stakes on what it means to provide truly personalized financial services. And when it comes to the customer, these enabling technologies promise new and exciting ways to engage them and deliver digital experiences that would have been hard to imagine even a few years ago.

In fact, I’d argue that some of the themes we see in the word cloud above, such as “compliance,” “security,” and “fraud,” are more prominent than before not simply because of the growing impact of financial crime or fresh concerns over regulatory priorities, but also because of the way that enabling technologies such as AI, machine learning, and automation have given fraud fighters and compliance teams new tools to keep consumers safe and company operations compliant.

If these themes resonate with you, then remember that at Finovate, what you see is what you get. Each of these themes has at least one, if not two or three, innovative companies who will be demoing their response to these challenges and opportunities live on stage next month at FinovateFall in New York. Check out our Finovate Sneak Peek series, as well as our evolving FinovateFall agenda, to learn more.

Wealth management solutions and technology company SigFig has added a number of new capabilities to its financial advisor collaboration platform, Engage.

The new capabilities include a range of AI-powered tools and solutions to enhance client engagement and boost efficiency for advisors and their teams.

San Francisco-based SigFig has been a Finovate alum since its FinovateFall debut in 2011.

Digital wealth management solutions and technology provider SigFigannounced a range of new capabilities for its financial advisor collaboration platform, Engage. These new capabilities include AI-powered tools and solutions that boost the effectiveness of advisors and their teams. SigFig also has added enhanced core integrations with leading industry systems to promote greater efficiency. Together, the new functionalities enhance the digital experiences available via the platform and deepen client engagement.

“AI has the ability to dramatically increase financial advisor productivity and effectiveness,” SigFig founder and CEO Mike Sha said. “We know that advisors need to be able to focus on fostering impactful relationships with their clients, truly understanding their pain points and goals. Engage acts as a hub to drive richer, more personalized client experiences, taking care of those time-consuming, but necessary, administrative tasks, so advisors can do exactly that.”

The new AI capabilities include AI-powered smart tips, including in-meeting prompts and customized recommendations based on real-time conversation analysis. Engage will now also feature proactive surfacing of the right content, tools, paperwork, and workflows, all based on an analysis of real-time discussions. Other new AI-driven additions include automated transcripts, meeting summaries, and post-meeting notes.

Streamlining integration with systems from Salesforce, Docusign, Microsoft, and Google is another major platform enhancement announced by the company late last week. The CRM integration, for example, creates a bi-directional data synch that enables advisors to view client data on the Engage platform as well as sync meeting notes, client details, meetings, and other tasks into Salesforce. This not only helps advisors provide more personalized advice, but also helps advisors accelerate the sales process as well as client conversions.

SigFig made its Finovate debut at FinovateFall 2011. In the years since then, the company has grown into a comprehensive digital wealth solutions business with nearly 1.5 million customers and 6,000+ advisors on its platform. The firm, founded in 2006 and headquartered in San Francisco, counts financial institutions such as UBS, Wells Fargo, and Scotiabank among its partners.

Are you an innovative fintech with new technology that’s ready for prime time? Join us in New York next month for FinovateFall and take advantage of the opportunity to showcase your solution before an audience of 2,000+ decision-makers.

Finovate’s Fintech Rundown is here with a look at some of the top fintech headlines. From startups emerging from stealth flush with capital to the launch of new AI-powered fraud fighting technologies, we’ve got you covered. Be sure to check back all week long for the latest updates.

E-commerce

E-commerce payments solution provider Klarnaacquires New Zealand’s Laybuy.

This week’s edition of Finovate Globalhighlights recent fintech headlines from Ireland.

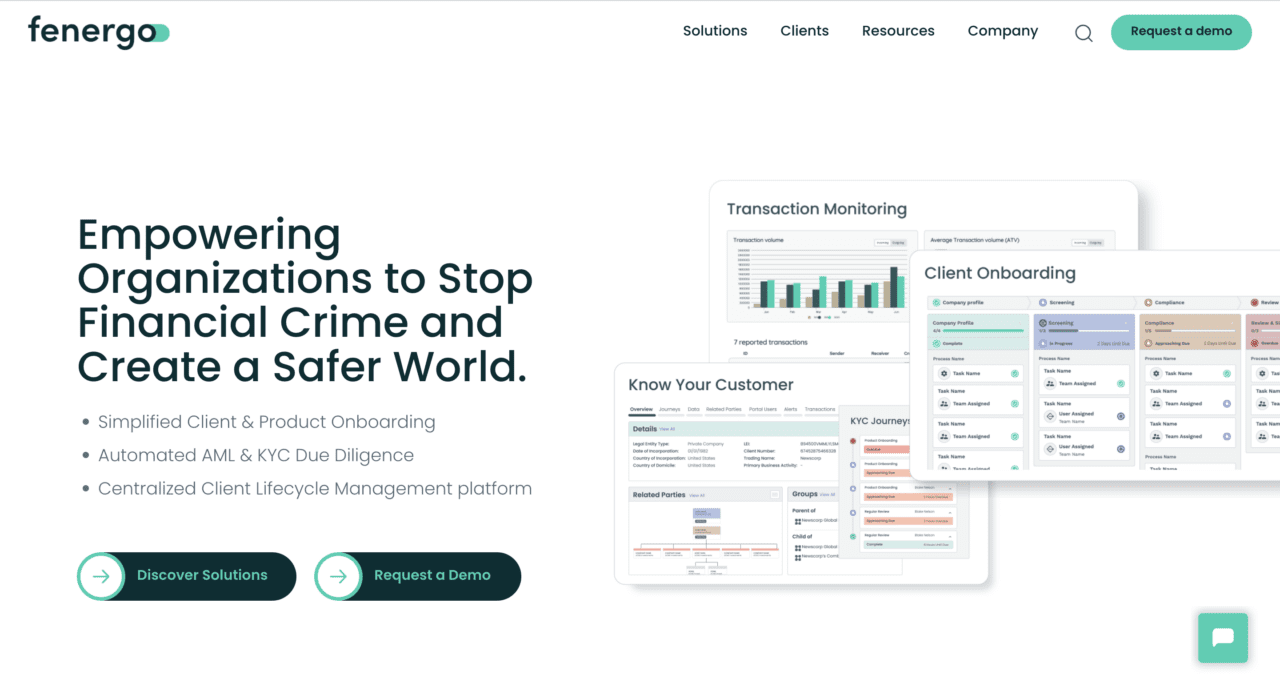

Dublin-based regtech Fenergo has inked a partnership with Caribbean-based PROVEN Bank. The financial institution will leverage Fenergo’s transaction monitoring solution to enhance and streamline its anti-money laundering (AML) compliance operations.

PROVEN Bank Deputy Chief Executive Officer Nikita Kissoon underscored increasing regulatory pressure on financial institutions as one of the reasons the bank sought the partnership with Fenergo. Kissoon praised the company’s “excellent reputation for expertise in both AML regulations and cutting-edge compliance technology,” and said that enhanced AML compliance “aligns with our commitment to combat financial crime and remain future-proofed against fast-evolving regulatory changes across our offshore locations.”

Fenergo’s technology will help boost operational efficiency for the Caribbean-based financial institution. PROVEN Bank will benefit from the automation of multiple manual AML processes, which will reduce the number of false positives and free up compliance resources to focus on more complex situations and higher-risk customers. The bank will begin deploying the technology at its Cayman Islands location and subsequently expand the solution to its offices in St. Lucia and its affiliate company, PROVEN Wealth, based in Jamaica.

The partnership is especially timely. The Cayman Islands, where PROVEN Bank is based, was only recently removed from the Financial Action Task force’s AML grey list and the European Union’s black list earlier this year.

Fenergo Chief Strategy Officer Stella Clarke pointed out that banks like PROVEN that operate in multiple jurisdictions often struggle to keep up with local regulations with regards to AML. “Our transaction monitoring solutions offers PROVEN Bank the flexibility to seamlessly adapt to fast-evolving regulatory environments, while empowering it to more effectively cross-sell services to existing customers based on rich data insights,” Clarke said.

Fenergo made its Finovate debut 12 years ago at FinovateEurope in London. The company has raised more than $760 million in funding, and includes TLG Capital and Bridgepoint among its investors. Fenergo’s partnership news comes at the same time that the firm announced that it had formed an alliance with Deloitte Ireland to help deliver Fenergo’s CLM solutions to financial institutions throughout EMEA.

The Bank of Ireland wants you!

If you are a technology specialist looking to drive fintech innovation in the Republic, that is.

The Bank of Ireland just announced that it is recruiting for 100 technology roles in a variety of digital projects, including fighting fraud and advanced data analytics. The Bank is specifically looking for talent with experience in data, delivery management, engineering, resilience and cybersecurity. Open banking, cloud computing, APIs, and AI are also among the areas of emphasis.

“We continue to invest in our talent, technology, and infrastructure to ensure customers have the very best banking services,” Bank of Ireland Group Chief Operating Officer Ciarán Coyle said, “We’re currently progressing a range of innovative digital projects across the Group and we want to recruit talented specialists who can enhance the banking experience for our customers.”

The bank’s search for tech talent comes as the institution has increased its investment in financial technology. After making more than 60 enhancements to its mobile banking app, including biometrics and fraud monitoring, the bank saw an 18% year-on-year increase in active digital users. The bank announced the largest single investment in ATMs in the last decade earlier this year, as well as an investment of €15 million on new fraud prevention technology.

“We are looking for the very best talent to join our technology team as we continue to deliver improvements for customers and colleagues across the organization,” Coyle said.

Ireland’s PTSB has extended its agreement with Worldpay, giving the bank’s customers access to an additional range of services from the company, including e-commerce and ePOS. PTSB will also gain access to Worldpay DCC, a dynamic currency conversion solution that allows cardholders to pay in the currency of their choice.

PTSB Head of Personal Banking at PTSB Jeff Harbourne said that the ability to offer “a best-in-class merchant services solution” was key to the bank’s “ambition of becoming Ireland’s best personal and business bank.” Harbourne added, “By partnering with Worldpay, we’re offering a competitive advanced payments solution to our existing and new customers that enables them to grow their businesses and accept payment across all channels.”

With more than 1.2 million customers, PTSB has a presence in 98 locations throughout Ireland. Founded in 1816, the financial institution rebranded from Permanent TSB last fall following its acquisition of a sizable portion of Ulster Bank, including the firm’s Retail, SME, and Asset Finance businesses.

A Finovate alum since 2015, WorldPay today is a major payments technology and solutions company that processes more than 40 billion transactions across 146 countries and 135 currencies. Headquartered in Cincinnati, Ohio, and founded in 1971, WorldPay announced an extension of its strategic partnership with fellow Finovate alum ACI Worldwide in July, and inked a new partnership with another Finovate alum, American Express, in May.

Here is our look at fintech innovation around the world.

Latin America and the Caribbean

Colombian payment orchestration platform Yuno teamed up with Medellin-based financial services app Nequi.

Mexico City-based cryptocurrency exchange Bitso partnered with blockchain company Coincover for its non-custodial disaster recovery service.

Peruvian investment and asset management arm of Credicorp, Credicorp Capital, went live with Temenos’Multifonds accounting and investor servicing solution.

Financial Times profiled Kim Beom-su, founder of Kakao and one of the richest men in South Korea, who was recently arrested on stock manipulation charges.

Digital identity verification provider ADVANCE.AI signed an agreement with the Credit Information Corporation (CIC) to become the newest credit bureau in the Philippines. Read more about fintech in the Philippines in last week’s edition of Finovate Global.

Estonian payments and e-commerce solution provider Montonio introduced its new CEO Johan Nord.

Payments infrastructure company Kevin has been blocked from serving new clients by the Bank of Lithuania, which has also appointed a “temporary representative to oversee” the firm’s activities.

Middle East and Northern Africa

Singapore’s Prytek bought a controlling stake in Israeli fintech Tip Ranks, giving the company a valuation of $200 million.

For the first time, FinovateFall 2024 (September 9-11) will showcase innovations in wealthtech. From AI-powered analysis and decision-making to embedded technologies that are democratizing the world of investing, now is a great time for asset managers, RIAs, and others looking to leverage technology to boost their wealth management businesses.

“Finovate spotlights cutting-edge technology and finserv themes dominating industry news,” Finovate VP and Demo Director Heather Stowell said. “The Great Wealth Transfer has been at the forefront of conversations, and we’re excited to showcase several startups innovating within wealth management and investing.”

Indeed. In its annual survey of wealth managers, Acuity Knowledge Partners noted that the intergenerational wealth transfer was a major opportunity and challenge facing asset managers. Additionally, survey respondents also expressed a desire for comprehensive solutions for estate, tax, and retirement planning. Growing revenues via customized research offerings was also mentioned as a goal, along with managing costs while embracing digitalization and new, enabling technologies like AI.

Offers investments to all clients starting from $10, and not just the top 1% via a financial advisor. Headquartered in New York. Founded in 2021. LinkedIn.

GPTadvisor

Empowers financial institutions with AI tools for optimized decision-making, streamlined workflows, and improved client advisory, driving business growth and operational excellence. Headquartered in Madrid, Spain. Founded in 2023. LinkedIn.

illuminote

Enables financial institutions and advisors to authenticate registered client legal estate records with confidence, providing access to authenticated data without expensive tech integrations. Headquartered in Santa Rosa, California. Founded in 2022. LinkedIn.

QuAIL Technologies

Automates processes and increases productivity so organizations can spend less time managing and more time growing. Headquartered in Pittsburgh, Pennsylvania. Founded in 2022. LinkedIn.

TIFIN AG

Uses AI and ML to deliver actionable insights, helping financial advisors make data-driven decisions that boost client acquisition, expansion, and retention, achieving organic growth. Headquartered in Charlotte, N.C. Founded in 2023. LinkedIn.

TradingValley

Empowers companies that adopt its AI investing model that reduces the investing research time for both individual and institutional investors. Headquartered in Taiwan. Founded in 2015. LinkedIn.

Are you an innovative fintech with new technology that’s ready for prime time? Join us in New York next month for FinovateFall and take advantage of the opportunity to showcase your solution before an audience of 2,000+ decision-makers.

A look at the companies demoing at FinovateFall in New York on September 9 and 10. Register today using this link and save 20%.

APIMatic

APIMatic’s developer experience platform adds a layer of technology between fintech APIs and developers to make integrations faster through automation and AI.

Features

Automates the creation of SDKs

Includes dynamic use case guides

Delivers AI-generated integration code

Who’s it for?

Payment providers, banks, and fintech startups.

Corsound AI

Corsound AI enhances security against voice fraud with patented voice-to-face technology and deepfake detection, backed by over 200 autonomous AI patents.

Features

Offers revolutionary security – the future of verification technology

Delivers unique voice-to-face matching that matches a face to a voice without a database

Provides deepfake detection: No enrollment needed, agnostic to new tools

Who’s it for?

Banks, credit unions, identity verification companies, and more.

CSS

CSS introduces IMPACT 3.0, an innovative debt collections platform with AI Copilot Assistants, enhancing compliance, efficiency, and debtor communication.

Features

AI Collector Copilot: Real-time collections advice for agents

AI Automation: Design processes by chat

AI Executive Insights: Instant financial and performance data by chatting

GPTadvisor is the assistant for wealth managers. Their advanced generative AI, in a powerful SaaS platform, enhances productivity for wealth managers across day-to-day activities.

Commercial banks with a private banking arm along with purely wealth management and advisory firms. GPTadvisor’s product also fits the needs of IFAs and includes a licensed SaaS version, as well.

QuAIL Technologies

Q(Fin) by QuAIL Technologies allows financial advisors to elevate productivity and grow their business with powerful AI that is safe, secure, and compliant.

Features

Elevates productivity through automated workflows

Enhances customer engagement with highly personalized content

Improves investment outcomes with deeply integrated AI

Who’s it for?

Registered Investment Advisors and wealth managers.

Synctera

The Synctera Platform equips banks with the tools, infrastructure, and data insights they need to scale a compliant sponsor banking program.

Features

Efficiently manages compliance with a complete set of tools and workflows

Centralizes data and streamlines reconciliation with the Synctera Ledger

Maintains complete data visibility

Who’s it for?

Banks and companies launching fintech or embedded banking products.

TIFIN AG

Through advanced artificial intelligence and machine learning, rich data partnerships, and data science expertise, TIFIN AG provides personalized and actionable insights to drive organic growth.

Features

Unifies data and delivers AI-driven insights and recommendations

Empowers advisors to make data-driven decisions

Enhances client growth and retention

Integrates seamlessly with existing technology

Who’s it for?

RIAs, broker-dealers, wealth managers, banks, credit unions, and insurance platforms.

The battle against fraud is a never-ending one. And recent fintech news headlines have helped remind us all of how broad the frontlines are. From the challenge of AI-powered deepfakes to the sad fact that many of our own bad habits continue to keep fraudsters in business, fintechs are busy developing solutions to help us get and stay at least one step ahead of the bad guys. Here are a trio of stories highlighting the latest efforts by fintechs to combat financial crime.

Digital identity verification innovator Socure has unveiled its Selfie Reverification solution. The new capability provides a way to validate return consumers online in less than two seconds with just a selfie. The technology matches incoming selfies with previously verified ID headshots, and features a true match rate of 99.9%. Built on the company’s Document Verification (DocV) solution, Selfie Reverification also detects signs of deepfaking, and readily identifies age discrepancies between the photo and the credential.

“Identity verification isn’t a one-time event. As consumers interact with an online service over time, their risk profile can change. That’s why it’s important to determine you are still who you say you are, without going through the full verification process again,” explained Socure Chief Product and Analytics Officer Pablo Abreu.

Selfie Reverification prompts the user to take a selfie, and sends real-time feedback on positioning, angle, and lighting. Once taken, the selfie undergoes a Level 2 NIST PAD compliant liveness check to prevent spoofing, as well as Socure’s injection attack detection process which makes sure that a fraudster has not injected a false or altered credential into the session. Lastly, the selfie is compared against a set of hundreds of thousands of curated deepfake samples created by more than 20 different AI generators.

The technology leverages biometric analytics to evaluate more than 80 facial features, from eye distance and nose width to jawline contours and emotional expression, to create a facial map and ensure an accurate match. Use cases for Selfie Reverification include preventing account takeover, securing high-risk transactions, streamlining account recovery and re-verification/re-validation, and more.

Founded in 2012 and headquartered in Incline Village, Nevada, Socure most recently demoed its technology on the Finovate stage at FinovateFall 2017. Today, the company has more than 2,500 customers, including four of the top five banks, the top credit bureau, and 400+ fintechs. Businesses ranging from Capital One and SoFi to DraftKings and the State of California rely on Socure’s technology for accurate identity verification and fraud prevention. Johnny Ayers is Socure’s founder and CEO.

Digital banking solution provider Alkami has added credential stuffing protection to the challenge-response authentication process for its digital banking platform. The new functionality automatically checks for human behavior in the background, but does not require visual puzzles or any additional time spent by the user.

“This enhancement in Alkami’s platform has given us the ability to provide an additional layer of security for our account holders,” Quontic Bank SVP of Digital Banking Grace Pace said. “The secure and seamless login experience has contributed to reducing potential fraudulent activities, offering our customers greater peace of mind without added complexity.”

Credential stuffing refers to a type of cyberattack in which a hacker uses credentials obtained through data breaches or purchased from the dark web in order to attempt to access another service. A typical case of credential stuffing, for example, could involve a hacker using the credentials from a breach at a retail store to attempt to log into a bank’s website.

Credential stuffing is a common attack in part because it takes advantage of the tendency of individuals to reuse usernames and passwords. But its commonality takes nothing away from the damage these attacks do. One estimate determined that credential stuffing costs businesses $6 million a year on average, to say nothing of the negative reputational impact that often accompanies it.

The addition of credential stuffing protection is the latest example of Alkami’s layered approach to fraud detection and prevention in digital banking. “Alkami continues to evolve its platform as the security threats change for our customers, and we’re proud to integrate credential stuffing as part of our standard solution for everyone,” Alkami Director of Product Management Brad Cranford said. “Our goal is to help our customers manage security while providing the best experiences for their account holders.”

Headquartered in Plano, Texas, Alkami made its Finovate debut in 2009 as “IThryv.” Alex Shootman is CEO.

Data and technology company Experian is adding behavioral analytics to its fraud detection capabilities courtesy of a newly announced acquisition of NeuroID.

More specifically, Experian is looking to bolster its defenses against AI-generated fraud threats. With their ability to apply fraud detection strategies to key vulnerabilities such as origination and account management, insights from behavioral analytics can help mitigate fraud in real time and defend users against a range of malevolent actions including identity theft, account takeover, bot attacks, and fraud rings.

“Our acquisition of NeuroID highlights our commitment to provide our clients with world-class data, analytics, and insights to prevent fraud,” said President of Experian’s North American Identity & Fraud business, Robert Boxberger. “Together with NeuroID, we’re excited to build new blended offerings that detect risk but also empower businesses to confidently navigate the online landscape and trust in their transactions.” He added, “In today’s highly competitive and digital-first world, the use of behavioral analytics is now vital for innovating for the future of fighting fraud.”

NeuroID’s solutions are now available via CrossCore on the Experian Ascend Technology platform. The integration will enable platform users to use a single service provider to monitor and analyze real-time digital activity.

“NeuroID unlocks a new view into a user’s riskiness based on behavioral interactions,” NeuroID CEO Jack Alton said. “This view arms companies with a proactive, first line of defense to detect sophisticated fraud rings and bot attacks. By joining forces with Experian, we’re looking forward to helping companies confidently navigate this new era with solutions that enable more secure and frictionless experiences.”

A Finovate alum since 2011, Experian most recently demoed its technology at FinovateFall in New York in 2018. Headquartered in Dublin, Ireland, the company employs more than 22,000 people, including more than 9,000 technologists and product developers, working in 32 countries.

Are you an innovative fintech with new technology that’s ready for prime time? Join us in New York next month for FinovateFall and take advantage of the opportunity to showcase your solution before an audience of 2,000+ decision-makers.

Streamly Fintech Insights offers unique opportunities to hear from some of the most innovative personalities in fintech and financial services.

Streamly’s interviewees range from entrepreneurs and investors who are helping build and fund tomorrow’s fintech solutions today to analysts and regulators whose job it is to ensure that the interests of consumers are heard and the rights of citizens are protected.

This week, we’re sharing six new conversations from Streamly’s Fintech Insights series.

Financial crime compliance platform Lucinity announced a strategic partnership with AI data management company Knights Analytics.

The partnership will bring advanced AI-powered data management capabilities to bear to fight financial crime.

Lucinity made its Finovate debut at FinovateSpring 2023 in San Francisco.

Lucinity has forged a strategic partnership with Knights Analytics, bringing advanced AI data management capabilities to its financial crime compliance platform.

The integration will enable Lucinity customers to consolidate, standardize, and reconcile their data within Lucinity’s unified Case Management system. The strategic partnership will also introduce additional ways to deploy Generative AI capabilities, including entity resolution, network analysis, and automated data extraction from documents. Users can also engage with their data via Lucinity’s AI copilot Luci, which offers actionable insights that are both intuitive and fully explainable.

“We are thrilled to simplify the ability to integrate more data within Lucinity’s platform,” Knights Analytics CEO Alex Ridden said. “Combining our data matching and entity resolution solutions with Lucinity ensures financial institutions make the most of their data. Financial institutions these days are sitting on a wealth of information that they don’t utilize effectively.”

Knights Analytics helps companies extract insights from large and siloed datasets. The firm specializes in combining graph analytics and AI, transforming structured and unstructured data into a high-quality, unified data layer. Leveraging innovations in data linkage and entity resolution technologies, Knights Analytics enables businesses to build a solid data foundation from which they can accelerate business processes and derive actionable insights.

“Partnering with Knights Analytics will take the Luci AI copilot to the next level by enhancing data accuracy, reducing manual analysis, and increasing the reliability of financial crime investigations through advanced data linkage and profile analysis,” Lucinity CEO Guðmundur Kristjánsson said. “This integration will unlock new use cases like on-demand entity resolution, enabling AI-driven automations and insights to streamline case investigations.”

Lucinity made its Finovate debut last year at FinovateSpring 2023. At the conference, the Reykjavik, Iceland-based company demonstrated its AI-powered copilot, Luci. Luci can conduct internet searches, background checks, fraud detection, sanctions screening, and more. This ability to manage and streamline tedious and time-consuming tasks enables compliance professionals to focus their decision-making on more complex issues.

Lucinity was founded in 2018. The company has raised more than $25 million in funding, according to Crunchbase. Keen Venture Partners and Experian are among the firm’s investors. Last month, Lucinity won the 2024 ICA Award for Innovation in Financial Crime Prevention for its Luci copilot. The company has also received accolades in recent months from Chartis Research and Microsoft, which named Lucinity one of its partners of the year for both its technological innovation and its commitment to “significant social impact and growth.”

Read our profile of Lucinity from earlier this year.

FORUM Credit Union has selected Apiture’s Business Banking solution to enhance its commercial digital banking experience.

FORUM Credit Union anticipates the move will expand its commercial member base.

“The comprehensive functionality available in Apiture’s Business Banking solution coupled with the company’s commitment to innovation made Apiture the right choice for our members and employees,” said FORUM Credit Union Chief Technology and Risk Officer Cameron Piercefield.

Digital banking solutions provider Apitureannounced today that FORUM Credit Union will use the fintech’s digital banking capabilities to power its commercial digital banking suite.

FORUM, a $2.1 billion, not-for-profit cooperative based in central Indiana, selected Apiture’s Business Banking solution to enhance the online and mobile banking experience for its commercial members. The credit union is also hoping to expand its commercial member base. FORUM was interested in Apiture’s ability to create a customized tool that integrates with its existing retail banking solution.

“As a member-owned organization with the mission of ‘helping members live their financial dreams,’ FORUM is committed to providing technology solutions that optimize our members’ banking experience,” said FORUM Credit Union Chief Technology and Risk Officer Cameron Piercefield. “The comprehensive functionality available in Apiture’s Business Banking solution coupled with the company’s commitment to innovation made Apiture the right choice for our members and employees.”

Apiture was founded in 2017 to help credit unions compete with larger banks and credit unions when it comes to digital banking experiences. The company’s solutions, which work with more than 40 cores, offer both consumer and commercial banking experiences, along with account opening, embedded banking, and data intelligence tools. Powering these capabilities are Apiture’s network of more than 200 pre-vetted fintech partners, including Glia, Deluxe, MX, Mambu, and DefenseStorm.

“We are proud to partner with FORUM Credit Union to support its growth objectives and drive member satisfaction,” said Apiture CEO Chris Babcock. “With integrations to more than 200 best-of-breed fintech partners and an API-first approach that enables rapid innovation, our Business Banking solution will empower FORUM to deliver a fully featured banking experience that supports businesses of all sizes.”

Headquartered in Wilmington, North Carolina, Apiture also has offices in Austin, Texas. The fintech has raised $69 million from investors including T. Rowe Price, Live Oak Bank, and others.