This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Digital lending platform Blend has agreed to acquire Mr. Cooper-owned Title365 for $422 million.

Blend will leverage Title365 for its title, escrow, and settlement services. Integrating this technology into Blend’s platform will allow the company to automate title commitment upon loan application submission, digitally reconcile settlement fees in real time, and streamline communication among parties. Ultimately, Blend anticipates that Title365’s industry expertise will help minimize costs by integrating title and settlement into the loan process.

Title365 was founded in 2009 and is headquartered in California. The company fits nicely with Blend’s approach of offering a modern experience with its mission “to be the most technologically advanced title insurance and settlement services provider.”

Title365 will be part of Blend’s title marketplace that allows lenders and consumers to choose their preferred title and escrow partner. The tool will be similar to Blend’s insurance marketplace that allows consumers to shop for competitive rates from more than 25 insurance carriers.

“We’re really excited about the agreement to add Title365 to our team as we continue our work to build the full consumer homebuying journey into our platform,” said CEO Nima Ghamsari. “With Title365, we will be able to expand our ability to put lenders at the center of a vastly improved homebuying journey that delivers new levels of efficiency, speed, convenience, and cost savings to everyone.”

Founded in 2012, Blend recently received $300 million in new funding, bringing its total funding to $665 million and boosting its valuation to $3.3 billion. The company facilitated $1.4 trillion in loans last year and counts 285+ lender partners, which together are responsible for around 30% of all mortgage volume in the U.S.

ESG investing is no longer the only environmentally conscious aspect of the financial services world. Recently, we’ve seen an explosion of fintechs– both new and incumbent players– going green.

Here’s a roundup of who’s who in sustainable fintech:

Ando Money

Ando Money is a California-based digital bank that uses client deposits to support green initiatives.

Ant Group

Ant Group, the fintech subsidiary of China-based Alibaba Group, has pledged to go carbon neutral by 2030.

Aspiration

Aspiration is a digital bank that won’t use consumer deposits to fund fossil fuel projects like pipelines, oil drilling, and coal mining. Additionally, the fintech plants trees in collaboration with reforestation partners when users round up their purchases.

Atmos Financial

California-based Atmos Financial offers a savings account that uses client deposits to exclusively finance climate-positive projects at scale.

Carbon Chain

Founded in 2019, CarbonChain offers organizations visibility into the emissions of their supply chains to identify the highest polluting transactions.

Carbon Collective

Carbon Collective offers roboadvisory services that help users divest from fossil fuels and invest in stock market funds that are low-carbon and don’t depend on fossil fuels for their core business.

Carbon Zero

Carbon Zero offers a credit card that rewards users’ purchases by using merchant-paid fees to buy carbon offsets.

Cloverly

Cloverly integrates with existing fintech apps, financial institutions, and payment processing services to assess their carbon impact and determine offsets needed.

Cooler Future

Still in beta, Cooler Future is a Finland-based startup that enables users to invest in a sustainable portfolio.

Doconomy

Doconomy is a Sweden-based digital bank that wants to inspire behavioral changes and reduce unsustainable consumption and carbon emissions.

Ecocart

Ecocart is a browser extension that works with merchants to help customers offset the environmental impact of their online purchase.

Helios

Founded in 2019, Helios is a France-based fintech that offers a digital bank account that helps users offset their carbon footprint.

Joro

Joro connects to users’ payment cards to analyze their carbon footprint and determine the biggest drivers of their carbon footprint.

Meniga

As part of its digital banking platform, Meniga provides a Carbon Insight tool that offers end users visibility into their carbon footprint based on their spending.

NetZero

NetZero connects to users’ bank accounts to determine the carbon footprint of their purchases. The fintech also helps users reduce their emissions and offset their footprint.

Nori

Headquartered in Seattle, Washington, Nori is developing a marketplace for carbon removals.

OpenInvest

OpenInvest helps advisors offer their clients ESG investing that align with their values.

Raise Green

Raise Green offers a marketplace where users can invest in local, impactful projects.

ReGal

Headquartered in the U.K., ReGal offers alternative financial services based on Green Blockchain.

Ripple

Payments network Ripple pledged to be carbon net-zero by 2030 and to decarbonize public blockchains.

Stripe

U.S.-based ecommerce and mobile payments company Stripe offers a tool called Stripe Climate. The offering enables businesses to direct a portion of their revenue to help scale emerging carbon removal technologies.

Tomorrow

Tomorrow offers a digital bank account that uses customer deposits to fund sustainable initiatives. The startup’s premium account, Tomorrow Zero, offers a payment card that is made of wood.

Treecard

Treecard offers a free payment card made of wood. The company donates 80% of its profits to reforestation.

Trine

Trine is a Sweden-based company that allows firms as well as private and professional investors to crowdfund solar energy products.

Tumelo

Tumelo helps investment platforms and pension providers engage investors by showing them the companies in their portfolio and empowering them to vote on ESG issues.

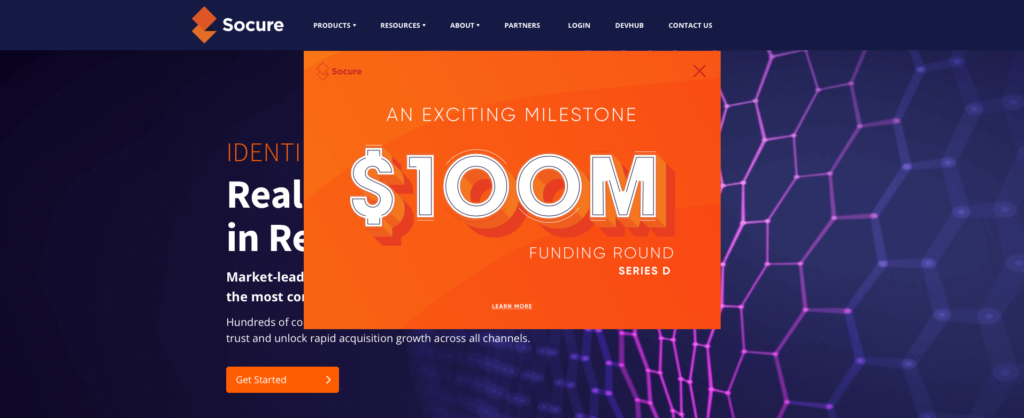

Digital identity verification company Socure announced that it has secured $100 million in Series D funding in a round led by Accel and featuring participation from the investment divisions of Citi and Wells Fargo. The investment brings the company’s total capital to more than $196 million.

“We are now more confident than ever that we will be the first company to eliminate identity fraud while unlocking complete and fully-automated coverage of every good ID,” Socure CEO Johnny Ayers said.

Also participating in the round were Commerce Ventures, Scale Venture Partners, Flint Capital, Strategic Capital, Synchrony, Sorenson, and Two Sigma Ventures. And while a specific new valuation was not included in the funding announcement, Socure’s Ayers hinted at the lofty level – and more – in congratulating his team on the company’s success.

“Reaching unicorn status is a testament to our dedicated and talented team which we are looking forward to rapidly scaling to meet demand,” Ayers said. “We are incredibly grateful for the chance to innovate and partner to solve this problem with some of the greatest companies in the world and are energized for the opportunities that lay ahead for Socure, especially as we make our march to a potential IPO.”

A Finovate alum since 2013, the company demonstrated its digital-to-physical identity verification technology at our fall conference in 2017. Socure’s predictive analytics platform marries AI and machine learning with trusted on- and offline data intelligence from a wide variety of sources to verify identities in real time. Operating in a number of verticals ranging from financial services and eCommerce to gaming and telecom, Socure has more than 350 customers including three of the top five banks, six of the top 10 card issuers, and more than 75 of the most innovative fintechs including Varo Money, Chime, and Stash.

More recently, Socure announced a partnership with advisory, tax, and assurance firm Baker Tilly that has since established that Socure’s Intelligent KYC product meets “and creates additional assurance” in providing USA PATRIOT Act compliance. Earlier in the year, Socure had announced that Intelligent KYC would be made available to digital gaming operators in eleven states.

Payments ecosystem giant PayPal announced a collaboration with Flutterwave, a leading payments technology company in Africa, this week. Through the collaboration, PayPal will enable its users to pay African merchants using Flutterwave’s platform.

The partnership will not only connect Flutterwave’s African merchant clients with PayPal’s 377 million accountholders, it will also help them work around the fragmented and complex payments infrastructure in Africa. To use the new functionality, online shoppers across the globe simply select the Pay with PayPal option while checking out at an African merchant’s page online.

Flutterwave launched to help businesses and individuals make payments across the continent flexibly and affordably. This comes at a crucial time for Africa. The ecommerce sector on the continent is expanding and is expected to grow from $16.5 billion in 2017 to $29 billion by next year.

“The collaboration reinforces our vision of creating a seamless digital payments system for Africa’s business communities that can now transact with international consumers,” said Flutterwave Founder and CEO Olugbenga Agboola. “By working with PayPal, we can further strengthen our commitment to our customers and service users as we will be enabling them to transact and expand their business operations to reach new markets.”

Flutterwave was founded in 2016 and has since processed over 140 million transactions worth over $9 billion. Today’s news comes just a couple of days after the company closed a $170 million round at a $1 billion valuation.

“International trade and foreign exchange can be a complex business for financial institutions of any size to manage successfully,” Finzly CEO and founder Booshan Rengachari said. “With one integration to the core, our FX STAR and EXIM STAR solutions help institutions like Fulton Bank to more efficiently, securely, and cost-effectively meet the needs of their customers.”

Finzly specializes in connecting banks and their customers via a real-time payment services hub and cloud-based bank operating system, BankOS, delivering a modern, digital banking experience. The company’s platform leverages open APIs and integrations into core technology to enable financial institutions to subscribe, try, and launch both Finzly’s and third-party fintech apps and solutions. With FX STAR, Finzly’s customers are able to execute foreign currency transactions, purchase foreign currencies in bulk using multi-currency accounts, as well as initiate payments. EXIM STAR serves as an international trade finance solution to help financial institutions manage the transaction lifecycle for commercial letters of credit, standby letters of credit, and documentary collections.

“We recognize Finzly as a proven provider that understands the unique business needs of regional financial institutions,” Fulton Bank International SVP and Manager Amy Sahm said. “Through the implementation of their user-friendly platform, our bank has been able to achieve better standard functionality across the board – from improved access to reports and confirming trades, to upgrades in investigation and reconciliation capabilities.”

Fulton Bank operates more than 223 financial centers in Pennsylvania and New Jersey, as well as in the mid-Atlantic states of Maryland, Delaware, and Virginia. The firm is a subsidiary of Fulton Financial Corporation, a financial holding company based in Lancaster, Pennsylvania, with $26 billion in assets.

Finzly made its Finovate debut in 2019. The Charlotte, North Carolina-based company most recently demonstrated its digital account opening solution at FinovateWest 2020, earning a Best of Show award from conference attendees. This year, in addition to its partnership with Fulton Bank, Finzly teamed up with Lead Bank, a Kansas City, Missouri-based “community-minded” commercial bank. Lead Bank implemented Finzly’s Payment Hub – part of Finzly’s Bank OS – to boost its own payment and digital capabilities.

“The ability to service our fintech and corporate clients with a Banking as a Service solution, as well as communicate messages to and from the core platform, is crucial to fulfilling and facilitating the requirements of Lead Bank and our channel partners,” Sheila Stratton, Director of Digital Strategy, Lead Bank said. “Finzly’s solution provides a modern technology platform in which our bank can expand payment capabilities while tapping a flexible and innovative solution to support our bank in delivering on the specialized needs of our clients.”

As well as partnerships, 2021 marked the launch of Finzly’s SWAP STAR solution. The new technology provides an end-to-end, sales, trading, and post-trade processing system for interest rate derivatives. SWAP STAR is available as an app within Finzly’s BankOS cloud-based bank operating system.

Social trading and investment marketplace eToroannounced today that it is making the leap to go public. In true 2021 style, however, the Israel-based company isn’t pursuing an IPO. Instead, eToro is merging with FinTech Acquisition Corp. V, a publicly-traded special purpose acquisition company (SPAC), in a deal worth $10 billion.

When the deal is finalized, the combined company will operate as eToro Group Ltd. and is expected to be listed on the NASDAQ.

The move to go public comes after a period of growth for the Israel-based company. Last year, eToro added more than five million new users and brought in $605 million in revenue, 147% higher than the revenue it saw in 2019. Additionally, average monthly registrations have grown from 192,000 in 2019 to 440,000 in 2020. In January 2021 alone, eToro added more than 1.2 million new registered users. Similarly, the number of trades executed on its platform has grown– from eight million average trades per month in 2019, to 27 million in 2020, and 75 million in January 2021 alone.

“We founded eToro with the vision of opening the global market for everyone to trade and invest in a simple and transparent way,” said eToro CEO Yoni Assia. “Today, eToro is the world’s leading social investment network. Our users come to eToro to invest, but also to communicate with each other; to see, follow, and automatically copy successful investors from all around the world. We created a new category of wealth management – social investing – and we are dominating the market as evidenced by our rapid expansion.”

eToro is the seventh fintech to use a SPAC to go public in the past few months, joining SoFi, BankMobile, Payoneer, MoneyLion, Apex, and OppFi.

eToro was founded in 2007 and has offices in Cyprus, the U.K., Australia, and the U.S. The company is among Finovate’s earliest alums, demoing at the very first FinovateEurope conference in 2011.

“As one of the fastest growing technology companies in the world, this cash injection – in addition to having the built-in option to expand the financing – will significantly accelerate the growth of our customer base, enhance SumUp’s technology leadership position, and drive the development of new services to support our merchants globally,” SumUp co-founder Marc-Alexander Christ said.

SumUp’s funding news comes at a time when the company is adding to its product portfolio in both Europe and the U.K. Much of this growth has come through acquisitions of POS software providers like London-based Goodtill, as well as Tiller, a digital service provider for gastronomy merchants. Separately, SumUp’s recent acquisition of Paysolut, a Lithuanian cure banking system provider will enable the company to fortify the banking services that it offers to its merchants.

SumUp supports more than three million merchants around the world. In addition to its expansion in Europe – going live in Romania to bring the total number of its European markets to 29 – the company has added to its interests in the Chilean market and launched operations in Columbia – the fourth largest economy in Latin America.

At the beginning of this year, SumUp announced that it was working with Shutterstock to give merchants the ability to add high-quality visual images to enhance their online storefronts.

“It’s important now more than ever that small businesses have the means to trade in the e-commerce space in order to take on larger competition,” SumUp European EVP Alex von Schirmeister said. “This partnership with Shutterstock will do just that, giving them more visibility to grow their customer bases.”

Founded in 2011, SumUp made its Finovate debut at FinovateEurope in 2013. Daniel Klein is CEO.

upSWOT, a fintech that helps bring business intel to small business owners, has raised $4.3 million in seed funding. Among Finovate’s newest alums, upSWOT offers a data aggregation and business finance management platform that leverages cash flow predictions and business insights to enable banks, insurance companies, and other institutions to better serve their small business and mid-market customers.

“Managing a portfolio of SMB clients is a challenge for every bank, lender, and servicer,” upSWOT CEO Dmitry Norenko said. “Amidst a global pandemic, the financial industry must find new and innovative ways to support this vital customer segment. Our white-label solution helps leading national and community banks gain granular insights into their SMB customers launched within six weeks, and with minimal strain on internal IT or overlap with legacy systems.”

upSWOT’s funding round was led by Common Ocean, a venture capital firm that specializes in early-stage fintechs that are innovating in the financial wellness space. Also participating in the round were CFV Ventures, ICBA, First Southern National Bank, and SpeedUp Venture Group, as well as previous investors. upSWOT said that it would use the funding to grow its business in the U.S., add talent to support “a growing list of deployments with Tier 1 and Tier 2 financial institutions,” as well as continue to add features and functionality to its data aggregation and BFM platform.

upSWOT leverages APIs to aggregate data from more than 120 widely-used business solutions such as Quickbooks, Salesforce, Amazon, and Shopify and provide business owners with predictive analysis and actionable insights. Via partnerships with financial institutions, upSWOT’s goal is to help SMEs that have been left to “fend for themselves” by giving them “modern day tools” to help support cash flow management, debt funding, financial planning and accurate cash reporting.

Founded in 2019, upSWOT demonstrated its white-label platform at FinovateWest Digital last year. A graduate of the Berkeley SkyDeck accelerator, the company includes Raiffeisen Bank International, Privat Bank, D&B, and Mastercard among its customers.

What happens after the newest cutting-edge banking technologies become table stakes? Banks move on to tackle another new technology.

In fact, in the past decade or so, banks have been constantly moving from one new technology to the next– from remote deposit capture to merchant-funded rewards, roboadvisory services, AI-informed marketing strategies, and finally on to complete digital transformation.

So now that 2020 served as the year of digital transformation, what’s next? How will banks use their limited resources to get ahead of the curve? Below are a few areas in which banks are focusing their attention to gain competitive advantage:

Communication

Last year we saw multiple financial services organizations update their communication technologies in tandem with digital transformation. But the game of facilitating customer communication is far from over. As Ron Shevlin pointed out in his piece, Every Bank Needs A Chatbot (Or Two) For Its Digital Transformation, chatbots are no longer simply a novelty. Instead, these tools offer fast turnaround for customer inquiries, provide additional data about consumers, and help firms hold personalized conversations with clients.

Another communication enhancement comes in the form of leveraging popular third party apps to communicate with customers. Axis Bank, for example, India’s third-largest private sector bank, recently announced a partnership with WhatsApp. Customers can now use WhatsApp to inquire about their account balance, recent transactions, credit card payments, deposit details, and block their credit or debit card.

Cryptocurrencies

Ready or not, crypto is here! In January, the U.S. Office of the Comptroller of the Currency (OCC) published an interpretive letter detailing that banks can transfer stablecoins to other banks. While banks haven’t been rushing to leverage this functionality, there have been a few moves that indicate financial services are slowly entering the cryptocurrency game.

First off, marketing services company Kasasaunveiled plans to help its bank and credit union clients provide bitcoin wallets to their consumers. Additionally, Mastercard recently announced it willallow merchants to accept payments in cryptocurrencies, and BNY Mellon agreed to begin custody of cryptocurrencies.

Payment tools

With so many payments moving online in the past year, banks need to be even more aware of their role in the online payments flow. In fact, the recent rise in embedded payments poses a risk to banks as third party apps such as Uber and DoorDash make the payment element of a transaction almost disappear.

There’s also been a lot of competition in the booming buy now, pay later (BNPL) space, and not just from third party fintechs like Klarna and Afterpay. Last year, Citi announced Citi Flex Pay, a product that enables cardholders to pay for select purchases over time at a lower interest rate than their card’s purchase rate. And in 2019, JPMorgan Chase launched My Chase Plan, an offering that allows cardholders to make equal monthly payments on purchases of $100 or more with no interest, just a fixed monthly fee.

Offering another tool to make payments more flexible, is U.K.-based fintech Curve. The fintech connects with consumers’ existing payment cards to offer rewards as well as a Go Back in Time feature that lets users switch payments from one card to another for up to 14 days after the purchase was made.

Sustainability

If you’re not green, you’re gone! O.K., maybe not quite, but in the past few months we’ve seen an increase in fintechs working toward a more sustainable future. In fact, just this month there have been multiple headlines that highlight fintech’s green future. First, U.K.-based digital bank Starling Bank launched recycled plastic debit cards. Second, Citi began restricting financing for companies expanding coal power. And finally, Menigapartnered with Iceland’s Íslandsbanki to integrate Meniga’s Carbon Insight into its digital banking solution.

Fintechs are also helping consumers do their part to minimize their impact on the environment. Aspiration, for example, ensures accountholders that their deposits won’t fund fossil fuel projects like pipelines, oil drilling and coal mines. The startup also works with reforestation partners to plant a tree when users roundup their purchase to the nearest dollar. And speaking of trees, Treecard offers a wooden Mastercard and donates 80% of its profits to reforestation efforts.

Ecommerce technology company Stripe announced over the weekend that it recently raised $600 million in funding. The Series H round brings the company’s total funding to $2.2 billion and boosts its valuation to $95 billion.

Investors in this month’s funding round include Allianz X, Axa, Baillie Gifford, Fidelity Management & Research Company, Sequoia Capital, and Ireland’s National Treasury Management Agency.

Stripe will use the funds to expand its Global Payments and Treasury Network and invest in its European operations to support increasing demand in the region. Specifically, the California-based company aims to boost its Dublin headquarters.

“We’re investing a ton more in Europe this year, particularly in Ireland,” said Stripe President and Cofounder, John Collison. “Whether in fintech, mobility, retail, or SaaS, the growth opportunity for the European digital economy is immense.”

Stripe has clients in 42 countries, 31 of which are in Europe. Among the company’s European clients are Deliveroo, Doctolib, Glofox, Klarna, ManoMano, N26, UiPath, and Vinted.

As Stripe pointed out in a blog post, only 14% of commerce happens online. That’s why, as the company’s CFO Dhivya Suryadevara notes, Stripe is “investing in the infrastructure that will power internet commerce in 2030 and beyond.” More specifically, the company is expanding its software and services and is making its technology available to millions more businesses in Brazil, India, Indonesia, Thailand, and the UAE.

“While Stripe already processes hundreds of billions of dollars per year for millions of businesses worldwide, the opportunity ahead is much larger for Stripe than it was when the company was started 10 years ago,” added Suryadevara.

This week for our Finovate Global Lists feature we congratulate the graduates of Startupbootcamp FinTech Dubai. Eleven startups successfully completed the MENA-based accelerator program in late February, wrapping up the three-month experience with a pitch opportunity before an audience of investors, corporate partners, mentors, and industry analysts.

“As the Demo Day has passed and the 11 startups of our third cohort continue their growth journeys – we are incredibly proud to welcome the 23 amazing founders of these startups as part of our global @sbcFinTech family!” Startupboootcamp Dubai announced via Twitter.

The graduates are:

Finllect: a UAE-based financial wellness app for Gen Zs.

Flaist: a digital transformation platform for banks.

Singular Capital: a digital asset mobile wallet based in Malaysia.

Open CBS: a Hong Kong-based, open and scalable, cloud-based core banking system for smaller FIs.

Absolute Collateral: a digital B2B capital markets trading platform based in the U.K.

Tajjir: a Jordanian startup that offers a stock trading software solution for retail investors.

Aura Technologies: an insurtech firm that enables non-insurance businesses to sell insurance to their customers.

CaaS (Compliance-as-a-Service): a regulatory reporting platform based in the U.K.

Stornest: a UAE-based digital legacy planner to support end of life planning.

Raseed: an investment platform that enables users in the UAE and Saudi Arabia to buy and sell U.S. stocks.

Kilde: a global private debt marketplace headquartered in Singapore.

Startupbootcamp FinTech is conducted in partnership with Dubai International Financial Centre (DIFC), Visa, HSBC, and Mashreq Bank. The program is open to fintech startups throughout the MENA region, as well as around the world, and offers expert-led Master Classes, tailored mentorships, as well as coworking space and living expense support for the duration of the program. Participants also benefit from access to corporate partners and an alumni growth program that helps startups remain networked after the program ends.

Since its launch in 2018, more than 30 fintech startups innovating in payments, lending, and Islamic digital banking count themselves as alumni of the accelerator. Startupbootcamp FinTech Dubai is part of an international network with more than 20 industry-focused programs for technology startups. The network boasts 950 startups accelerated – 41% of which were female-led – that have raised a combined $869 million (€ 727 million) in total funding.

Here is our look at fintech innovation around the world.

Supply chain financing expert Taulia is making a $6 billion credit facility available to its supplier clients this week. The funds were secured through a JPMorgan-led consortium that also includes UniCredit, UBS, and BBVA.

The news comes after Taulia partner Greensill Finance filed for insolvency earlier this week due to its largest client, GFG Alliance, defaulting on its debts. Taulia expects that the credit facility will help its clients that relied on Greensill Finance by offering them access to a different source of liquidity.

To be clear, the financing is not funding for Taulia itself; it is funding to help suppliers on its platform that are linked to Greensill Capital clients.

“Taulia’s priority, first and foremost, has been to enable businesses both large and small to unlock liquidity trapped in their supply chain in order to invest, operate and thrive,” said Taulia CEO Cedric Bru. “In the current environment, with the potential loss of a funder, our commitment to providing choice has become even more paramount.”

Today’s financing is the continuation of Taulia’s strategic partnership with JPMorgan that began in April of last year. Last July, the financier participated in Taulia’s $60 million financing round that boosted the San Francisco-based company’s total funding to $177 million.