This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

A look at the companies demoing at FinovateEurope on March 15 digitally and on March 22 and 23, 2022, in London. Register today and save your spot.

TeamViewerEngage is a next-gen digital customer engagement platform for providing digital customer service, holding online consultations, and creating online sales opportunities.

Features

Digital customer service

Consultation and advisory engagement

Digital sales engagement

Why it’s great

With TeamViewer Engage, banks turn their digital banking portal and app into an online bank branch experience. It is fully web-based and requires no downloads or installations.

Presenters

Mathias Holzinger, General Manager, Austria Holzinger is the General Manager for TeamViewer Engage. Mathias joined TeamViewer as a result of the company’s acquisition of customer engagement specialist Xaleon. LinkedIn

Horst-Georg Fuchs, Director, Solution Sales Engage As Co-Founder, and more importantly a passionate entrepreneur, marketer, and salesman, Horst-Georg has supported a large number of customers in their digital transformation of customer engagement! LinkedIn

From the very first FinovateEurope, women have led and helped lead live demonstrations of how companies were using new technologies to tackle the financial challenges faced by businesses, families, and communities. As part of that inaugural event in 2012, women from Cardlytics, ETRONIKA, Figlo, Ixaris Systems, Kabbage, Liqpay, Mootwin, Striata, and ValidSoft were on stage delivering the message of fintech innovation.

As Women’s History Month gets underway – and with International Women’s Day, March 8, right around the corner – we wanted to highlight some of the women who will be demoing their company’s latest fintech innovations this month at FinovateEurope 2022. Catch all of our FinovateEurope demoes during our Digital Kickoff on March 15, and on March 22 and March 23 for the live event in London.

Liron Diamant

Fintech Executive, Anodot. A payments expert with more than ten years’ experience in fintech startups, Diamant has a focus on building payments platforms and managing relationships with international banks and payments companies.

Daria Dubinina

CEO and Co-founder, Crassula. A strategist and entrepreneur as well as a CEO and founder, Dubinina has spent more than ten years specializing in payments, e-commerce, and business development.

Patrycja Karwat

IT Security Specialist, BNP Paribas Poland. Presenting in partnership with Secfense, Karwat has more than five years of experience in cybersecurity and banking. Previously, she spent more than four years in various technical roles with Deloitte including as Senior Analyst and Quality Assurance Tester.

Katalin Kauzli

Co-founder, Business Development Director, Partner HUB. With experience on both the principal and advisor side of business operations, Kauzli has 10+ years experience in a variety of roles, including assisting startups seeking equity in Hungary and managing corporate finance assignments.

Mariam Malwand

Product Owner, Topicus.Finance. Educated at Amsterdam’s Hotelschool Den Haag, Malwand brings founding and managing director experience to her work as Product Owner at Topicus Finance.

Yasmina Siadatan

Sales and Marketing Director, Dynamic Planner. With knowledge and experience across core marketing areas from analysis and communication to digital content and sales, Siadatan has helped drive awareness of Dynamic Planner and its brand throughout the retail investment industry.

Ana Luísa Silva

Head of Marketing, ebankIT. Silva brings more than seven years of experience in marketing and communications to her role at Finovate Best of Show winner ebankIT. She holds advanced degrees from the EAE Business School and the Universitat Politècnica de Catalunya.

FinovateEurope 2022 is only a few weeks away. If you are an innovative fintech company with new technology to show, then there’s no better time than now and no better forum than FinovateEurope. To learn more about how to demo your latest innovation at FinovateEurope 2022 in London, March 22 and 23, visit our FinovateEurope hub today!

A look at the companies demoing at FinovateEurope on March 15 digitally and on March 22 and 23, 2022, in London. Register today and save your spot.

PaxFamilia is an end-to-end wealth planning platform that helps financial advisors serve their clients with a structured and holistic approach to their wealth.

Features

Getting a 360° overview of the client thanks to the collection of data in structured inventories

Detecting and reporting opportunities through planning tools

Providing holistic services

Why it’s great

PaxFamilia provides financial advisors with all the tools and resources they need to turn their punctual services into continuous ones and thus become the trusted advisor of their clients.

Presenter

Guillaume Desclée, CEO Guillaume was product manager at Danone until 2009. Before PaxFamilia, he (co-)founded two other platforms, both dedicated to crowdfunding (Impulso in Brazil in 2009 and Spreds in Belgium in 2010). LinkedIn

A look at the companies demoing at FinovateEurope on March 15 digitally and on March 22 and 23, 2022, in London. Register today and save your spot.

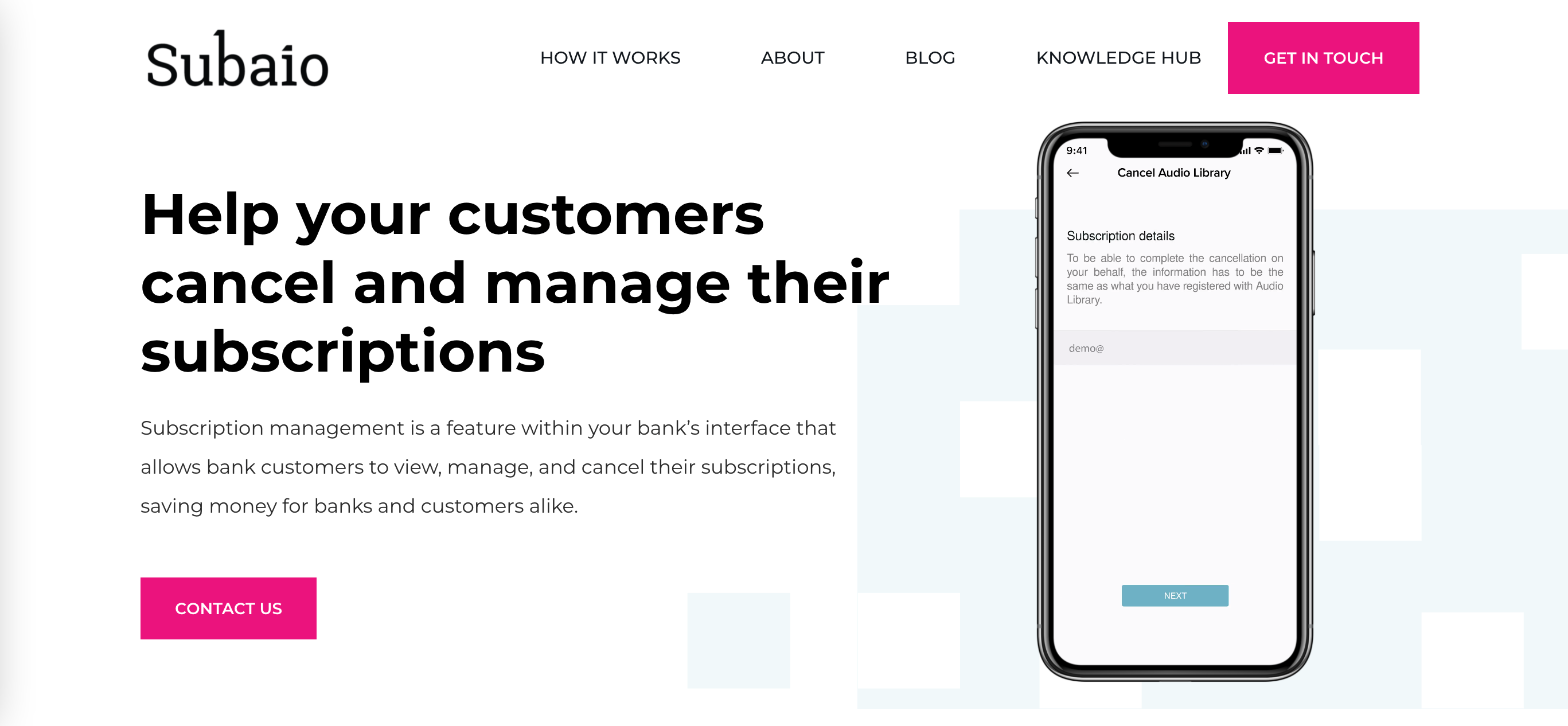

Subaio generates new revenue streams for financial companies by delivering insights on recurring payments.

Features

New revenue streams

Insights on recurring payments

Personalized selling

Why it’s great

Financial companies can generate more revenue, lower their costs, and live up to new EU legislation by using Subaio’s creditworthiness assessment solution that uses PSD2 Open Banking data.

Presenter

Søren Nielson, Chief Commercial Officer Nielsen is a seasoned fintech entrepreneur. He has raised millions of euros with different companies, written books on innovation, and sold solutions to some of the world’s biggest banks. LinkedIn

A look at the companies demoing at FinovateEurope on March 15 digitally and on March 22 and 23, 2022, in London. Register today and save your spot.

Finshape’sMoney Stories is a ready-made solution for banks, highlighting key events in customers’ financial lives through 7 to 10-second snapshots that are swipeable and easy to digest.

Features

Help customers understand their finances better.

Give personalized tips with the help of data science-based predictions.

Get customers engaged and ready to take action.

Why it’s great

Money Stories can be easily integrated into any bank application within a few days and deliver results in weeks.

Presenters

Tamás Braun, International Sales Director Braun has worked in the retail banking technology industry for the past 20 years at technology vendors such as IND and Misys before joining W.UP (now Finshape), as an International Sales Director. LinkedIn

József Nyíri, CEO Nyíri is a hands-on innovator and growth leader with more than 15 years of fintech experience. He successfully built up digital innovation based technologies at IND and W.UP. Nyíri is now Co-CEO of Finshape. LinkedIn

You’ve no doubt heard of the three largest buy now, pay later (BNPL) players, Klarna, Afterpay, and Affirm. The oldest of these, Klarna, has been around since 2005. But after the BNPL boom exploded in 2020, dozens of new players (and even some consolidation) emerged in the BNPL arena.

With so much competition– especially competition from large incumbents such as Chase–it can be difficult for BNPL companies to stand out and attract frequent customer spend. That is why some firms have found it advantageous to tailor their offering to a more specific audience. By targeting niche consumer groups, companies can provide a better user experience by tailoring each aspect of their offering to the specific group.

We’ve identified four niche players, each of which uses specificity to its advantage.

Study now, pay later

Australia-based ZeeFi recently launched its platform that helps education providers maintain cashflow and offers students a flexible, interest-free payment solution. The education provider receives payment upfront, while students can spread out the cost of their course for up to 36 months. ZeeFi was founded in 2016 under the name Study Loans. The company has raised $88.5 million.

Travel now, pay later

Uplift was founded in 2014 to allow users to pay for their travel experiences over time. The San Francisco-based company partners with travel brands, including hotel, airline, cruise, travel agencies, and more, and offers a point-of-sale financing option that lets customers spread their purchase out over time. Depending on factors such as purchase details and the traveler’s credit history, Uplift offers no-interest and simple interest loans that users can pay back over time, even after their trip.

Healthcare now, pay later

medZero‘s tool allows businesses to offer their employees a way to spread out the cost of their out-of-pocket healthcare expenses. The company provides users on-demand access to funds to pay up-front for the fraction of their healthcare bill that their insurance doesn’t cover, and pay the balance back over time. medZero doesn’t run credit checks, is fee-free, and charges no interest. The Missouri-based company has raised $5.7 million since it was founded in 2015.

Housing now, pay later

New York-based Flex helps renters pay their landlord on a schedule that works with their cashflow. Flex automatically connects to major rent payment companies and sends rent money on the user’s behalf to their landlord on the first of the month. As an added bonus, the company can help users build their credit scores, too. Flex, not to be confused with challenger bank Chime’s in-house BNPL tool with the same name, was founded in 2019 and has raised $5.8 million.

Canadian financial institution Innovation Credit Union (ICU) teamed up with digital banking solutions provider VeriPark to launch a new digital banking experience.

VeriPark made its Finovate debut in 2019 at our Dubai conference, FinovateMiddleEast.

With more than 57,000 members, ICU is the third largest credit union in the province of Sasakatchewan.

“Innovation has grown to become one of the leading credit unions of Canada,” Innovation Credit Union CEO Daniel Johnson said. “With this enhanced simplified look, our goal was to modernize our visual identity and further align to our purpose of simplifying banking for our current and future members.”

ICU will deploy VeriPark’s VeriChannel internet banking and mobile banking solutions, enabling the Saskatchewan-based credit union’s 57,000+ members to enjoy omni-channel banking experiences with seamless, multi-device functionality. The new platform provides a more convenient digital banking experience along with a new and improved website and a mobile app that is both faster and more intuitive. Savings and mortgage calculators are among the tools available with the new offering, along with other features to help members open and manage their accounts, transfer money, and track requests.

The partnership with VeriPark is no small matter for ICU, which described the collaboration as part of its goal of becoming Canada’s first fully digital credit union. Founded in 2007 by way of a merger between Southwest Credit Union and BCU Financial, ICU is the third largest credit union in the province and the 21st largest credit union in the country with more than $2.4 billion in assets. The institution began its journey to became the third, federally-regulated credit union in Canada after 82% of its members voted in favor of a special resolution in 2017 promoting federalization. This move will enable the credit union to operate nationwide and fulfill its goal of bringing “responsible banking to all of Canada.”

Founded in 1998, VeriPark maintains offices in the U.K., the U.S., Europe, Asia, Africa, and the Middle East. The company’s technology helps businesses improve customer acquisition, retention, and cross-selling capacities with the goal of guiding financial institutions on their digital transformation journeys. With secure and scalable solutions for customer engagement, omni-channel delivery, branch automation, loan origination, and more, VeriPark leverages Microsoft’s cloud platforms and Microsoft Dynamics 365 to serve customers in more than 30 countries around the world.

VeriPark began the year earning recognition from Gartner in its 2022 Market Guide for Digital Banking Multichannel Solutions. Last fall, the company leveraged the Microsoft Cloud for Financial Services to create three new apps: a complaints and service requests solution, a financial transactions app, and a Customer 360 app that provides insights into customer balances, transactions, utilized solutions, and more. Özkan Erener is CEO.

Mobile payments company Boku has sold its Mobile Identity unit to cloud communications firm Twilio.

Twilio will leverage the technology to create new packages in its Lookup API and Verify API offerings.

Terms of the deal were not disclosed.

Mobile payments company Bokuannounced it has sold its Mobile Identity unit to cloud communication company Twilio. Financial terms of the deal were not disclosed.

Twilio says the purchase is a reflection of its commitment to accelerate its vision for seamless mobile identity and digital intelligence. “Twilio and Boku Mobile Identity share a common goal– building a seamless consumer identity solution that doesn’t sacrifice user experience for security,” said Twilio’s General Manager of Account Security Aaron Goldsmid.

Boku’s Mobile Identity unit verifies customer data in real time using its database of mobile network operator identity connections. Ultimately, the tool helps business customers verify client data in real time, providing a smooth onboarding experience for their end users while mitigating fraud.

San Francisco-based Twilio said it will leverage Boku’s mobile identity technology to create new packages in its Lookup API and Verify API products. The company also plans to build on Boku Mobile Identity’s comprehensive mobile identity network to improve its existing security offerings.

Founded in 2008, Twilio seeks to reinvent how companies engage with their customers by digitizing communication channels via its APIs. The companies tools– which target voice, text, chat, video, and email– do everything from helping companies connect IoT devices to cellular networks to building real-time video applications.

Boku, which offers solutions that help deliver mobile payments, was founded in 2008. Last summer, the company launchedM1ST, also known as Mobile First. The new offering features 330+ mobile payment methods, including mobile wallets, direct carrier billing, and real-time payments schemes. M1ST reaches 5.7 billion mobile payment accounts across 90 countries.

This is a sponsored post by Carol Hamilton, Senior Vice President, Global Solutions at Provenir.

New survey data reveals uncertainty in the accuracy in credit risk modeling, underscoring the need for AI, machine learning, and alternative data.

Consumer credit markets have changed dramatically over the past two years during the Covid-19 pandemic, translating into economic uncertainty for millions across the globe, and it seems for the fintechs and financial services organizations that serve them.

After all the disruption we’ve seen over the past 24 months, how sound are credit risk models? This was the question we sought out to find the answer for with a global research study that surveyed 400 decision makers in the industry. The results were more than a little unsettling — only 18 percent of fintechs and financial services organizations believe their credit risk models are accurate at least 75 percent of the time.

That’s pretty astonishing — especially given the fact that the rest of the respondents indicated they believed their credit risk models were accurate less than 75 percent of the time.

Credit risk modelling is at the heart of every fintech and financial services company and this financial fault line in credit risk decisioning should send chills down the spine of the entire sector.

This “risky business” uncertainty in credit risk modelling accuracy may be why real-time credit risk decisioning was respondents’ No. 1 planned investment area in 2022, as organization’s work to resolve this financial fault line in credit risk decisioning. The survey underscored the growing appetite for AI predictive analytics and machine learning, data integration, and use of alternative data as the means to improve credit risk decisioning.

Aside from improving credit risk modelling accuracy, organizations are also employing credit risk decisioning platforms to help address the key priorities of fraud detection/prevention and financial inclusion. And increasingly these credit risk analysis strategies employ the use of alternative data.

Fraud continues to grow for financial services and lending firms, both before and during the pandemic, with identity fraud being a key factor.

Sixty-five percent of decision makers in our survey indicated they recognize the importance of alternative data in credit risk analysis for improved fraud detection. Additionally, 51 percent recognize its importance in supporting financial inclusion. Alternative data is a more varied way for lenders to evaluate those individuals with a thin (or no) credit file put together a more holistic, comprehensive view of an individual’s risk. This vastly benefits those who can’t be easily scored via traditional methods, while also benefitting financial institutions, by expanding their total addressable market.

To level-up credit risk decisioning, organizations need more data, more automation, more sophisticated processes, and more forward-looking predictions. And to do that, businesses need AI that can provide immediate impact to the decisioning process. AI-enabled risk decisioning is seen as key to usher in improvements in many areas, including fraud prevention (78%), automating decisions across the credit lifecycle (58%), improving cost savings and efficiency (57%), more competitive pricing (51%), and improving accuracy of credit risk profiles (47%).

For unbanked and underbanked consumers, AI gives organizations the opportunity to support those consumers’ financial journeys. Financial services organizations typically struggle to support these consumers because they don’t come with a history of data that is understandable by traditional decisioning methods. However, because AI can identify patterns in a wide variety of alternative, traditional, linear, and non-linear data, it can power highly accurate decisioning, even for no-file or thin-file consumers.

While AI and machine learning, and alternative data may have been on the credit risk decisioning “nice to have” list a few years ago, fintechs and financial services organizations are quickly realizing legacy technology and methods simply are not up to today’s task of credit-risk decisioning. By deploying new technology such as AI and machine learning, and embracing alternative data, organizations are on their way to improved confidence in the accuracy of their credit risk models – moving to remediate their credit risk “risky business.” In doing so, they will be more prepared to react to changes moving forward, while supporting inclusive finance.

Carol Hamilton is Senior Vice President, Global Solutions at Provenir, which helps fintechs and financial services providers make smarter decisions faster with its AI-Powered Risk Decisioning Platform. Provenir works with disruptive financial services organizations in more than 50 countries and processes more than 3 billion transactions annually.

Bulgaria-based Payhawk extended its Series B funding round by $100 million to $215 million.

The investment values Payhawk at over $1 billion and brings its total funding to $239 million.

The company currently serves businesses in 30 countries and will use the recent funding to pursue further global expansion.

Bulgaria may be known more for its beaches and opera singers than it is for its fintech. Business spend management platform Payhawk may soon change that, however. The Bulgarian-based fintech just extended its recent Series B round by $100 million and is now valued at over $1 billion. This new valuation makes Payhawk Bulgaria’s first unicorn.

The fresh funding brings its Series B round to $215 million and boosts its total funding to $239 million. Today’s round was led by Lightspeed Venture Partners and saw participation from Sprints Capital, Endeavor Catalyst, HubSpot Ventures, and Jigsaw VC.

Payhawk’s $1 billion valuation is a huge leap forward for the fintech. Just three months ago when the company first announced its Series B round, Payhawk was valued at $570 million. It now sits 75% higher.

Payhawk, which currently serves businesses in 30 countries, will use the investment to expand its presence in the mid-size enterprise market and pursue global expansion. The company will open offices in Paris and Amsterdam this month and will add one in New York in September.

To support this growth, Payhawk plans to ramp up its workforce by 3x. The company plans to grow from 100 to 300 employees by the end of this year. As part of this expansion, Payhawk will increase the size of its product team by adding 60 additional senior software engineers to meet customer demand for new features.

Payhawk was founded in 2018 to offer businesses a way to control company spending. In addition to payment cards, the startup offers invoicing, employee reimbursement, and billpay tools along with accounting software integration, built-in spending policies, and analytics.

“Every employee that deals with company payments feels that there should be a better way to do it, but this huge problem was never tackled by a strong product team with a hardcore engineering background,” said Payhawk Founder and CEO Hristo Borisov. “This is what Payhawk brings to the market.”

The collaboration, announced late last month, will provide access to Rize’s banking infrastructure and compliance program. Both current and new clients also will be able to securely link bank accounts from 16,000+ financial institutions and fintechs by way of MX’s data connectivity network, which leverages machine learning to clean and enrich transaction data.

“Our partnership with Rize is all about developing new financial products and services through one API,” MX EVP of Partnerships Don Parker said. “By cutting the associated time and costs of development, we’ll open up MX functionality to a wider range of fintech companies and organizations already working to improve financial strength and access to quality financial tools.”

Powering 85% of digital banking providers and thousands of banks, credit unions, and fintechs, MX most recently demonstrated its technology on the Finovate stage last fall in New York for FinovateFall. At the conference, the multiple-time Best of Show winner showed its Open Finance portal that improves the data sharing experience between providers and recipients for the benefit of the customer. The technology relies on modern, token-based connectivity to give financial institutions the ability to monitor and manage how customer data is shared.

In the months since its appearance at FinovateFall, MX has forged partnerships with Deposits.com to promote financial inclusion in underbanked communities, and with H&R Block, where the Lehi, Utah-based fintech will help the tax preparer provide customers of its Spruce mobile banking platform with greater transparency. In February, MX teamed up with Cadence Bank, a regional financial institution based in Tupelo, Mississippi with more than $50 billion in assets and 400+ branches in the American South, Midwest and in Texas. MX began the year with the appointment of Shane Evans as Interim Chief Executive Officer. Evans took over the top spot from MX founder Ryan Caldwell, who transitioned to the role of Executive Chair.

Open banking platform Tink partnered with Irish postal services provider An Post.

Tink will provide data and analytics that fuel An Post’s Money Manager app.

The new partnership serves as an inroad for Tink into the Irish market.

Visa-owned open banking platform Tink formed a new partnership this week that will bring its open banking capabilities to users of Irish postal services provider An Post.

An Post, which offers not only parcel and mail logistics but also financial services, operates a network of 920 post offices for its 1.5 million weekly customers. An Post offers many of the major services typical of high street banks, including current accounts, savings accounts, credit cards, loans, and a currency card that allows users to purchase and top up 16 currencies.

Leveraging Tink for data and analytics, An Post now delivers a Money Manager app that helps users track their income and spending, set budgets, and receive insights about how they can better manage their funds.

“The partnership with Tink is the next step in our transformation journey, to firmly position ourselves as a challenger to the banks in Ireland, and to give customers access to simple money management tools that will enable them to build their financial confidence,” said An Post Financial Services Director John Rice. “As the leading open banking platform in Europe, Tink was a clear choice of partner for us to provide the data and analytics that sit at the core of our Money Manager app.”

For Sweden-based Tink, the partnership with An Post serves as an important inroad into the Irish market. “An Post is in the perfect position to help simplify money management for its customers through the power of open banking technology,” said Tink UK & IE Banking Lead Tasha Chouhan.

More than 10,000 developers use Tink’s tools to help financial services firms leverage the power of open banking via a suite of open banking tools including income verification, payment tools, risk insights, and more. Tink currently serves 18 markets from its 13 offices and integrates with more than 3,400 banks and financial institutions reaching over 250 million end customers across Europe.

Founded in 2012, Tink is a two-time Finovate Best of Show Award winner, and most recently demoed at FinovateEurope 2019. The company acquired FinTecSystems earlier this year, a move that expanded Tink’s reach into the DACH region with a range of new customers including N26, DKB, Santander, Solarisbank, and Check24.