This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

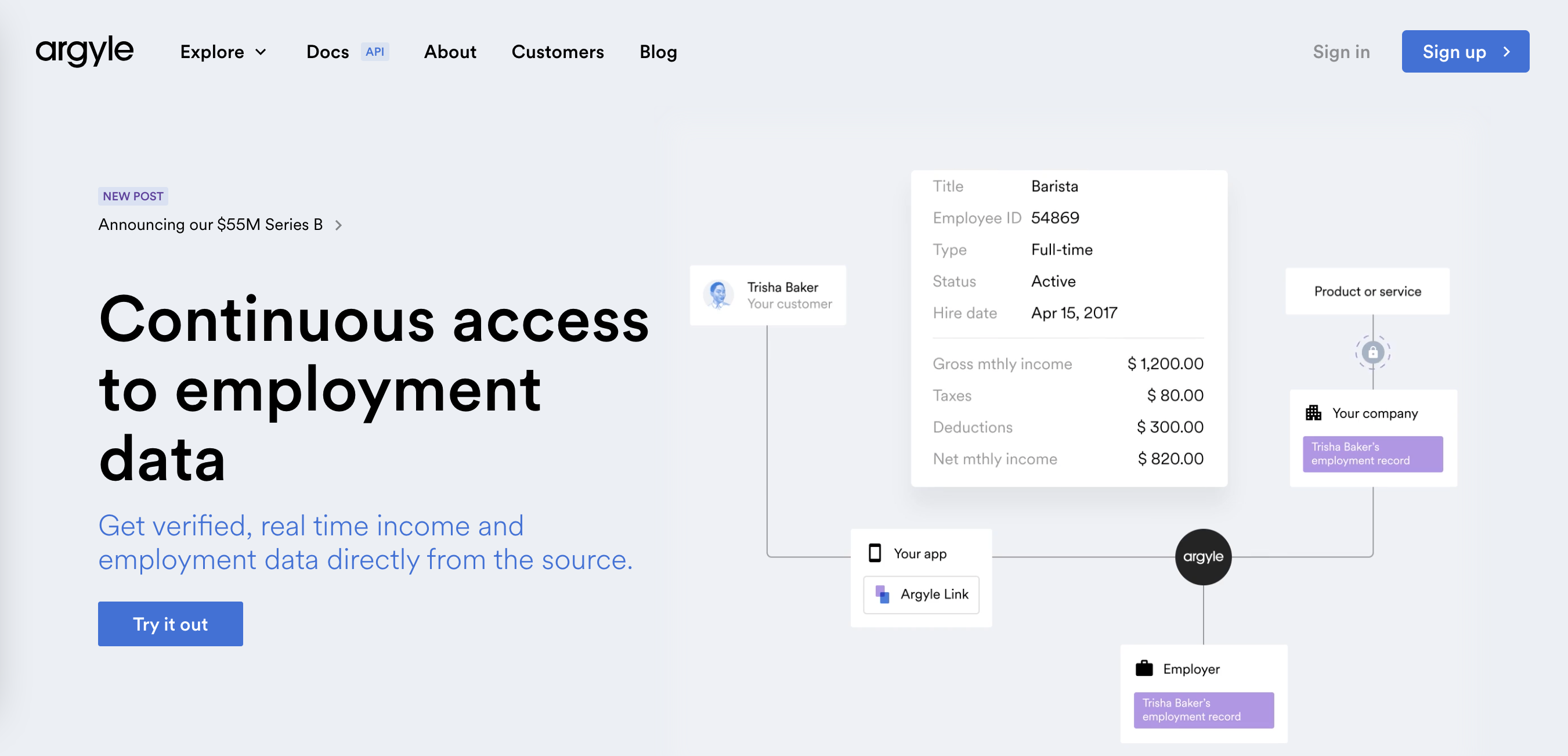

Argyle provides streaming, user-permissioned, read-and-write access to employment records. Link 4.0 provides an updated look and feel for a more integrated and delightful end user experience.

Features

Customizable experience

Modern, simple, breathable search screen layout

Simplified multi-factor authentication

Clear error messaging

Why it’s great

The redesign provides a more transparent and trustworthy experience for end users to successfully connect their accounts, decrease drop-off rates, and evolve visual style.

Presenter

Billy Marsden, COO & Co-Founder Marsden is a Co-Founder and COO of Argyle. Prior, he was an Investor Associate with F-Prime Capital, VP of Business Operations with STRATIM, and Senior Associate Consultant with Bain & Company. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

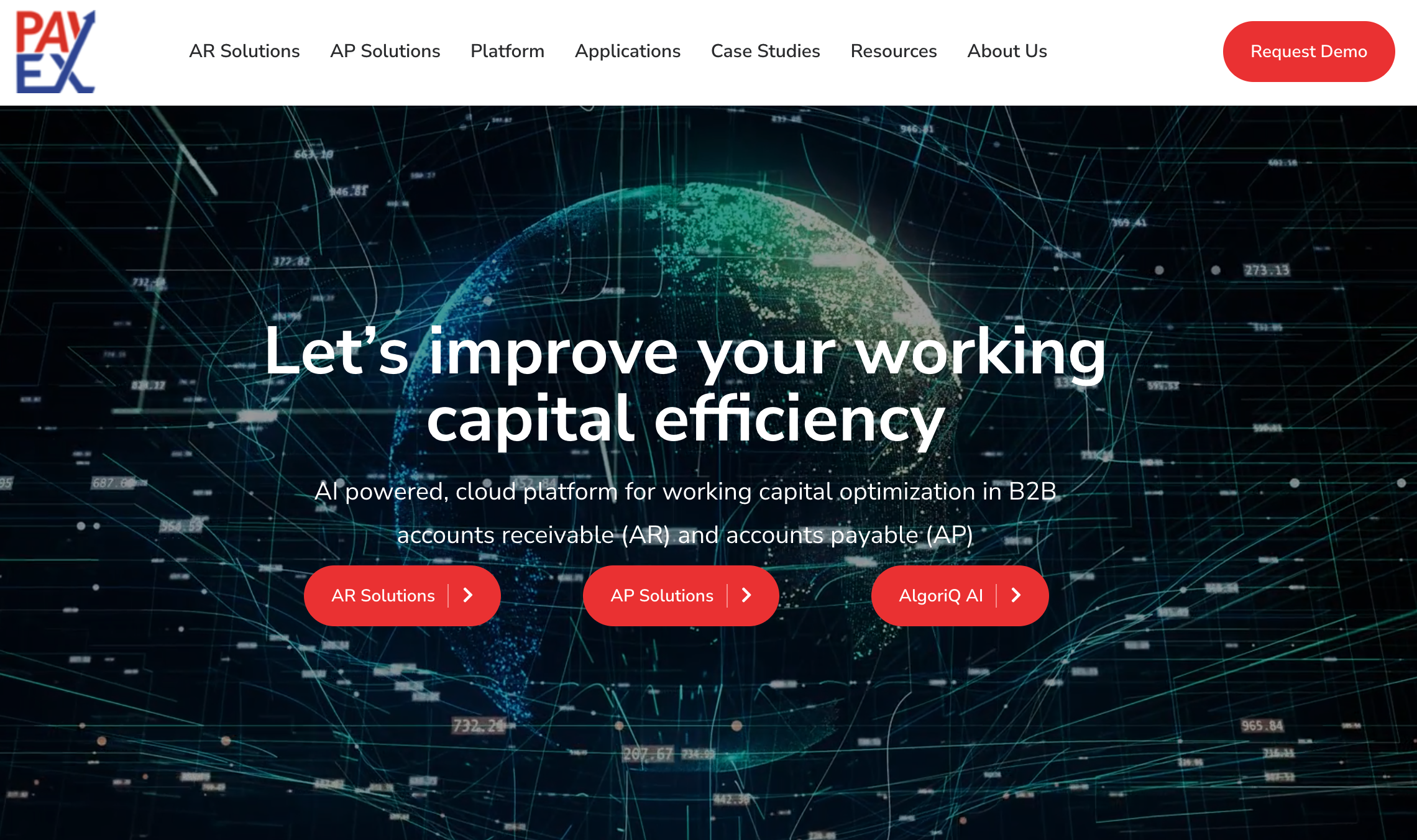

Global PayEx’s AI-powered, cloud platform targets working capital optimization in B2B accounts receivable (AR) and accounts payable (AP).

Features

95% straight-through reconciliation

20%+ reduction in DSO

1-4% enhancement in revenue

Why it’s great

It’s an AI-based reconciliation solution that’s customizable to every company’s accounts processes through core, ML-based modules.

Presenters

Naru Ramamoorthy, CRO Ramamoorthy specializes in growing P&Ls, leveraging technology, process, operations, and market needs. He’s held leadership roles in industries including payments, banking and financial services, and retail. LinkedIn

Anu Agrawal, Executive VP & Head, North America Agrawal has worked with tech start-ups and global giants and specializes in setting up new regions and taking them to scale. He has over two decades of leadership experience in banking and payment and tech. LinkedIn

Three credit unions – VyStar CU, BCU, and Reseda Group – have invested in credit risk management specialist AKUVO.

Terms of the funding were not disclosed.

The new capital will help AKUVO further develop its credit risk and delinquency management platform, Aperture.

Credit risk and delinquency management specialist AKUVOannounced a new investment not from the world of venture capital, but from the land of membership-powered credit unions. The amount of the investment was not disclosed, but the names of the credit unions involved in the funding have been: VyStar Credit Union, BCU, and Reseda Group, a wholly-owned CUSO (credit union service organization) of Michigan State University Federal Credit Union (MSUFCU).

The funding will enable AKUVO to further develop its collection and credit risk platform, Aperture. The cloud-based, API-enabled portfolio risk and delinquency management solution provides streamlined information for quick and easy research and leverages robotic processing to offer businesses a 20% improvement in collector efficiency, a 15% reduction of effort for speciality processes, a 10% reduction in collection workload, and a 10% increase in manager efficiency.

“Our goal is to empower members to discover financial freedom, and I am optimistic AKUVO’s data science solutions will help us accelerate our ability to do just that,” BCU EVP and COO Jim Block said. “We anticipate rapid growth over the next decade, and the Aperture platform has the promise to scale with our membership.”

With $5.5 billion in assets, BCU is based in Vernon Hills, Illinois, in the greater Chicago area. BCU is the smallest (by assets) of the three credit unions involved in AKUVO’s funding this week. Reseda Group is part of $6.8 billion MSUFCU and this investment represents the second time the institution has invested in AKUVO (the first being in January of this year).

“AKUVO’s Aperture platform will change the way we provide members with individual credit solutions that maximize recoveries,” MSUFCU Chief Risk Officer Jim Hunsanger said. “Aperture’s data-based decisioning also ensures we meet regulatory and legal requirements. We’re excited to be an AKUVO client and early investor.”

VyStar Credit Union, based in Jacksonville, Florida, has $12 billion in assets, and is one of the 15 largest credit unions in the country. Speaking on behalf of the firm, VyStar’s SVP of Loan Administration Eric Weatherly said that the investment in AKUVO will “allow us to be a greater force for change for our members and the credit union community.”

Courtesy of the investment, each of the three credit unions involved will have a representative on AKUVO’s board of directors. Headquartered in Pennsylvania, AKUVO was founded in 2019.

Deserve received a $250 million credit facility from Goldman Sachs, Cross River, and Waterfall Asset Management.

Last year, Deserve experienced a 650% growth in transactions volume and an 800% growth in receivables.

The company will use the credit facility to meet the growing demand from financial institutions, fintechs, and consumers.

Payment-card-as-a-service startup Deserveannounced a new $250 million credit facility from Goldman Sachs, Cross River, and Waterfall Asset Management.

Deserve (formerly Self-Score) has re-imagined traditional credit cards by transforming the application and onboarding processes, as well as the credit card itself by bringing them into the digital-first era. The company enables businesses to provide a white-labeled or co-branded card program made possible via a set of configurable APIs and SDKs.

Among Deserve’s clients are BlockFi, M1 Finance, OppFi, Seneca Women, Notre Dame Global Partnerships, and KrowdFit. The company will use today’s funds to meet the growing demand from financial institutions, fintechs, and consumers. Last year, Deserve experienced a 650% growth in transactions volume and an 800% growth in receivables. The company expects the new credit facility will boost its growth even further.

“At Deserve, we’re committed to helping organizations quickly and securely launch any type of credit card product in the cloud, customized to their specific audience – a valuable touchpoint with customers and a must-have in today’s landscape of competitive brand loyalties,” said Deserve CEO and Co-founder Kalpesh Kapadia. “Because our platform is digital-first and mobile-centric, customers can, in turn, begin using their Deserve-powered credit card minutes after application, no plastic required. We’re excited about what this new financing will enable us to do as we amplify our reach and help more fintechs, financial institutions, SMB lenders, and brands connect with and grow their customer base.”

In the coming years, Deserve plans to launch card programs to help consumers manage subscriptions, augment BNPL, and unlock their home equity. The California-based company also plans to build card programs for SMBs and commercial customers.

The $250 million credit facility comes six months after Deserve’s $50 million Series D equity round in October 2021 which boosted the company’s total funding to over $294 million.

FinovateSpring 2022 goes live next week. From Wednesday, May 18 through Friday, May 20, FinovateSpring returns to San Francisco, California for three days of innovative fintech demonstrations, insightful mainstage presentations, and lively debates and panel discussions on the most critical topics in fintech today.

To help get you ready for next week’s event, here’s an opportunity to get to know some of the companies that will be making their first-ever appearance at a Finovate conference. From innovators in credit decisioning and data management to specialists in cybersecurity and financial wellness, this year’s cohort of FinovateSpring newbees promises something for everyone.

Click on the buttons below to learn more about each of the companies making its Finovate debut next week at FinovateSpring. Then visit our FinovateSpring 2022 hub to pick up your ticket today!

Be sure to catch our Finovate first-timers next week at FinovateSpring 2022 in San Francisco, California, May 18 through May 20. Tickets are still available, so visit our registration page today and save your spot.

Business expense management firm Expensify is in the process of beta testing a unique new feature. Though, it’s more of a perk than a feature. The Expensify Lounge is a chic new space in the entrance to Expensify’s San Francisco office located in the heart of the financial district.

The idea for the Expensify Lounge came about pre-COVID. Much of the company’s workforce was already working remotely, and the Expensify Lounge was slowly becoming a ghost town. To maintain the vibrancy of the office, the team decided to turn the office into “best co-working cafe in the city” by launching the Expensify Lounge, a cafe-like working environment that includes great coffee, great cocktails, and great company. Now that the pandemic is waning in the U.S., the Expensify Lounge is in beta testing this spring.

“We added a ridiculously over-the-top cocktail bar like you’d find tucked away in a Tokyo high rise, and put in an espresso bar even us Portland coffee snobs can respect,” described Expensify CEO David Barrett. “Then we paired it with our integrated chat Concierge to offer to-your-seat delivery, and then turned the overall furnishings of everything else up to 11.”

The newly-renovated space functions like a high-touch version of a co-working space. Expensify customers can work from the space as often as they like, as long as they like, with wifi, complimentary drinks, and snacks. During the beta test period, there’s no membership required. The company is especially encouraging early stage companies and VCs to come in and check it out and kick the tires.

If you’re in the area and interested in visiting the Expensify Lounge during the beta period, go to https://use.expensify.com/lounges and use the password “Finovate” when you arrive. If you’re attending FinovateSpring on May 18 through May 20, you’re in luck. The Expensify Lounge is just a 10 minute walk from the event venue, the Hilton San Francisco Union Square.

The lounge is open Monday through Friday from 8 a.m. to 5p.m. and is located at:

88 Kearny St., 16th Floor San Francisco, CA 94108

After the beta period, Expensify clients can enjoy lounge access as part of their $9 per month Expensify membership. ” I guarantee it’s better than your office, or any office, and it’s designed to be a better place to work than any cafe in the city, too,” Barrett added.

A public company as of last November, Expensify is part of the fast-growing business financial management segment. The company’s flagship service is expense reporting, but it has since grown to add billpay, a travel concierge, and a corporate payment card.

Current launched its platform API today and introduced Plaid as its first partner.

The collaboration between Current and Plaid will enable Current members to access digital financial services from more than 6,000 apps and services on the Plaid network.

Current earned a valuation of $2.2 billion after securing $220 million in Series D funding last spring.

Fintech platform Currentlaunched its platform API today. The new offering is designed to bring seamless integrations and embedded banking experiences to fintechs and financial services companies. The product launch is being accompanied by news that Current has secured its first partner, API-first data network Plaid. The partnership will enable Current members (totaling nearly four million) to access an even wider range of innovative digital financial solutions to help them better manage their finances. These solutions, available via the Plaid network, range from digital payments to financial planning to investment tools.

“Our new platform API gives open banking partners the capability to embed our core banking technology,” Current CTO Trevor Marshall said. “We’re thrilled to be working with Plaid, the industry leader in open banking, as our first partner. We enabled this integration in response to feedback from our members. With Plaid, our members can access experiences that can help improve their financial lives with control and security.”

In working with Plaid, Current will provide its members with a credential-less open finance experience, leveraging both Current’s API as well as phone number and device authentication to reduce friction.

“We’re thrilled to enable a simple, secure on-ramp to digital financial services for Current members, who are often banking for the first time in their lives,” Plaid Partnerships Lead for Universal Access Raja Chakravorti said. “The integration ensures that consumers are in control of where and how their financial data is permissioned and shared, information that is essential to setting up a healthy financial life.”

Founded in 2015 and headquartered in New York, Current offers a variety of solutions to help its members change their lives by creating better financial outcomes. The company offers up to 4.00% APY via its Savings Pods solution, provides overdraft protection of up to $200, enables early wage access for members who use direct deposit, and gives consumers up to 15x the points on qualifying transactions made via the Current debit card.

Current secured $220 million in Series D funding last spring in a round led by Andreessen Horowitz. The investment gave the company a valuation of $2.2 billion. Stuart Sopp is CEO.

Banco Santander is launching a new tool to help retail customers track the carbon footprints of their transactions.

The bank is partnering with ClimateTrade and the Mastercard donation platform to enable users to offset their impact.

The app is currently available to customers in Spain and will soon go live in Poland, Portugal, and the U.K.

Banco Santander is out with a new ESG initiative today. The Spain-based bank unveiled a new feature that enables its retail banking customers in Spain and Chile to track and offset their carbon footprints.

Developed in-house and available on Santander’s website and app, the tool will help customers measure the carbon footprint of the purchases they make with their Santander accounts and payment cards. Customers can see their monthly carbon footprint reported in kg CO2-eq in a range of categories, including supermarkets, transport, health, and education.

To help users take action against their carbon output, Santander’s tool will show eco-friendly tips for each category, as well as facts on how users can reduce their footprint and transition to a more sustainable economy.

Santander is partnering with ClimateTrade to enable customers to voluntarily use the tracker to offset their carbon footprint. ClimateTrade connects sustainable project developers with users looking to offset their carbon footprint. Because the company’s marketplace leverages the blockchain, all transactions, which are processed through the Mastercard donation platform, are traceable.

Santander has been fighting climate change since 2011 by measuring and reporting on its own carbon footprint. The bank became carbon neutral in 2020 and pledges to reach net zero emissions by 2025 in its financing, advisory, and investment services, as well as across all operations.

The app will go live in Poland, Portugal, and the U.K. in the coming months.

Earlier this year, PwC’s Vicki Huff Eckert published a report that looked at the impact of VC investment on the technology industry. Eckert is Vice Chair for Technology, Media, and Communications – and the global leader of New Ventures and Innovation – for PwC. She will be featured at FinovateSpring next week in San Francisco as part of our Fireside Chat series.

Eckert’s report, Living in a World of Unicorns, examines the role that venture capital has played in not just funding, but in actually helping transform a variety of industries – including fintech and financial services. Some of her key takeaways as they relate to fintech specifically include:

“Tech is now influencing so many verticals that the investments and business processes in those verticals are evolving and beginning to blur industry lines.”

“In the U.S., companies are mostly using AI to improve performance, gain greater insights from their data, or automate business operations. In China, AI companies are primarily focused on facial recognition and computer vision. Alarmingly, investment in cybersecurity hasn’t kept pace …”

“The growth of the platform economy and e-commerce created an unprecedented need for seamless, cross-border, highly scalable digital payments.”

“The digitization of the economy is also establishing the foundation and infrastructure for digital currencies to eventually go mainstream.”

“Today’s unicorns aren’t just shaping capital markets and investment strategies, they are shaping and redefining the industries in which they operate – by developing new products and services, expanding rapidly into new geographic markets, and using their cash (and valuable stock) to attract talent.”

Check out the report from PwC’s Vicki Huff Eckert, and then be sure to join us next week for our Fireside Chat at FinovateSpring in San Francisco, Friday morning, May 20th at 9:30am.

Apple is using CNote’s platform to invest $25 million in underserved communities.

Oakland-based CNote facilitates investments in economic equality, racial justice, gender equity and climate change initiatives.

Apple joins other companies using CNote to invest, including Mastercard, Patagonia, PayPal, and Netflix.

CNote, a company that facilitates investments in fixed income and time deposit products that advance the social good, revealed its newest investor today. Apple is using the California-based company’s platform to invest $25 million in underserved communities.

“We’re committed to helping ensure that everyone has access to the opportunity to pursue their dreams and create our shared future,” said Apple VP of Environment, Policy, and Social Initiatives Lisa Jackson. “By working with CNote to get funds directly to historically under-resourced communities through their local financial institutions, we can support equity, entrepreneurship and access.”

Apple’s $25 million contribution is part of the company’s Racial Equity and Justice initiative, an effort to address systemic racism and expand opportunities for people of color.

CNote has already deployed some of the funds to an initial round of financial institutions, including:

ANECA Federal Credit Union in Louisiana

Bank of Cherokee County in Oklahoma

Carver State Bank in Georgia

Education Credit Union in Texas

First Southwest Bank in Colorado

Hope Credit Union, which serves Alabama, Arkansas, Louisiana, Mississippi, and Tennessee

Kaua‘i Federal Credit Union in Hawai‘i

Latino Community Credit Union in North Carolina

Legacy Bank in Missouri

Optus Bank in South Carolina

Self-Help Federal Credit Union, with locations in California, Illinois, Washington, and Wisconsin

VCC Bank in Virginia

As Bank of Cherokee County EVP Susannah Plumb Scott explained, the funds invested via the CNote platform can make a real difference in underserved communities. “Partnerships like the one we have with CNote and Apple are essential to our efforts to expand access to capital, as well as to financial products and services, in a historically underserved market,” said Scott, whose institution invests 95% of deposits back into Cherokee County.

Echoing those thoughts is Education Credit Union President and CEO Eric Jenkins, who said deposits like Apple’s “allow ECU to serve more consumers and meet a broader range of needs.”

Founded in 2016, CNote’s platform provides insured deposits to a group of vetted, mission-driven financial institutions, including community development financial institutions (CDFIs), low-income designated (LID) credit unions, and minority depository institutions (MDIs). These financial institutions use the deposits to help promote economic equality, racial justice, gender equity, and climate change initiatives.

CNote investors, a list that includes Mastercard, Patagonia, PayPal, Netflix, and now Apple, receive quarterly impact reports with details on which institutions received deposits and the populations that are benefiting.

CNote was a B Lab “Best for the World” honoree in 2019 and was named “Best Women-Owned Business” by the U.N. Women’s Empowerment Principles program in 2020. The company has raised $43 million.

Minna Technologies has launched a new solution to help merchants recover revenue and re-engage customers who recently canceled subscriptions.

The new offering, Merchant Solutions, helps solve a pain point in which bank cards are often blocked during a subscription cancellation.

Merchant Solutions tackles the new reality of subscription management in which customers are more proactive toward both signing up for and cancelling subscription-based services.

Sweden-based subscription management infrastructure company Minna Technologiesunveiled its new Merchant Solutions late last week. The solution will enable subscription-based businesses to recover revenue from customers who have recently canceled their service and who manage their subscriptions via their retail bank app.

“We are thrilled to allow the 20% of consumers who cancel with Minna to more easily return to the subscription service when it suits them; and to enable subscription businesses to more personally retarget these consumers with suitable offers,” Minna Technologies Chief Product Officer Tiama Hanson-Drury said. “Not every cancellation is a desire to sever ties with the merchant – often it is a call for increased flexibility or personalization. By keeping the channel open, merchants have the chance to evolve the customer relationship and reacquire the consumer.”

Minna Technologies’ new solution also helps merchants deal with an unintended consequence of consumer protection efforts that require banks to support subscription payment management, especially with regard to unidentified or unintended payments. Sometimes, the subscription cancellation process results in the customer’s bank card being blocked to prevent future wrongful payments. Minna Technologies cited a study by Experian Insights that indicated that almost 80% of those who try to re-establish their subscriptions within three months after canceling have found that their bank cards have been blocked. This friction can be enough to cause the customer to abandon the attempt to resubscribe to the service.

To this end, Minna will offer a new “unblock” feature that facilitates communication between banks and subscription businesses to unblock bank cards in instances when banks have confidence that no wrongful payments will be reattempted by the business. This block removal service will help alleviate operational issues and the potential for poor customer service when payments are automatically blocked during subscription cancellation. Minna noted that the Unblock feature is one example of the kind of assistance the company is developing for subscription-based merchants with other solutions, including a way to prevent cancellations in the first place, to be offered in the near future.

Minna Technologies’ new offering also responds to the challenge of what Minna Technologies’ VP of Sales, Partnerships and Solutions Erica Katsambis referred to as the “rise of new subscription personas”. These personas reflect a growing assertiveness on the part of consumers who are more likely to be proactive in expressing their digital preferences than consumers of even a few years ago.

“From the ‘lost, confused, and angry’ who are disengaged and canceling via their bank, to the ‘savvy’ consumers switching subscriptions regularly or those consumers happy to try out many new subscriptions, they all demand more from their subscriptions,” Katsambis explained. “It is more important than ever to diversify and bolster digital channels and functionality to retain users, grow your customer base, and prevent unwanted churn.”

Minna Technologies made its Finovate debut at FinovateEurope 2019. In the time since then, the company has forged partnerships with ING Belgium, Lloyds Bank, and Danske Bank; earned recognition as an Inclusive Fintech 50 member; and raised more than $23 million in funding. Late last year, Minna launched its “1-click” subscription management solution. Early this year, the company announced the appointment of new board chairwoman, Amanda Mesler.

Payment and transaction services company Worldline and credit decisioning firm Algoan are joining forces.

The two are developing a credit assessment tool that will help lenders make better, faster, and more efficient lending decisions.

The credit assessment solution will leverage Worldline’s open banking experience as well as Algoan’s credit decisioning expertise.

Payment and transaction services company Worldlineannounced a partnership with credit decisioning firm Algoan. As part of the agreement, the two firms will work together to develop a credit assessment solution to help lenders and services providers make better credit decisions.

Specifically, the partnership will leverage Worldline’s open banking experience. “At Worldline we look for innovative partners who share our vision and enable us to enrich and expand our open banking services,” said Worldline Managing Director Financial Services Michael Steinbach. “As a lead and one of the largest Open Banking providers in Europe, we are committed to unlocking the full potential of Open Banking. With Algoan, we will be able to offer our customers an end-to-end and cost-efficient white-label solution to assess credit worthiness.”

According to Alogan CEO Michael Diguet, it is an ideal time to launch this solution. “Open Banking credit scoring is experiencing momentum that big players should embrace,” said Diguet.

Another key resource behind the credit assessment solution is Alogen’s four years of credit scoring expertise. Financial institutions can use the new tool to receive more accurate credit scoring and increased processing efficiency. Underwriting use cases include personal finance, consumer lending, auto finance and leasing, retail lending, BNPL, insurance, and utility providers.

The credit assessment solution will also bring benefits to borrowers. The enhanced data means that more borrowers may be approved and will receive their approval faster.

Having won its first contract to facilitate card transactions in 1973, Worldline currently has 20,000 employees in more than 50 countries and counts annual revenue of almost $4 billion. Gilles Grapinet is CEO.