This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Moneyhub raised an additional $18.2 million (£15 million) from savings and retirement business Phoenix Group.

The investment is the second part of a 48.6 million (£40 million) Moneyhub received in October, and brings the company’s total funds to $81.6 million.

Phoenix Group’s Standard Life is a long-standing client of Moneyhub.

Open finance solutions company Moneyhubannounced it received an additional $18.2 million (£15 million) investment. Today’s funds come from savings and retirement business Phoenix Group.

The funding round is a follow-on to the recent $48.6 million (£40 million) Moneyhub received in October. Legal & General and Lloyds Banking Group led that round, contributing $42.4 million (£35 million), and Shawbrook Bank provided an additional $6 million (£5 million) in debt funding. Moneyhub’s total funding now adds up to $81.6 million.

Moneyhub was founded in 2014 and creates software for open banking, open finance, and open data applications. Organizations leverage these tools to add data aggregation, insights, and payment systems to their applications in order to create a more personalized digital experience for their end users. U.K.-based Moneyhub plans to use the investment to develop its solutions and expand globally. The company currently counts more than 100 organizations, including more than 30 high-profile enterprise firms, as clients.

Phoenix Group’s Standard Life is a long-standing client of Moneyhub. The firm leverages Moneyhub’s Open Finance platform to create Money Mindset, a financial wellness proposition for workplace pension customers.

“We are delighted that Phoenix Group has chosen to go even further by investing in the business,” said Moneyhub CEO Samantha Seaton. “With Consumer Duty and Pensions Dashboard driving the need to focus on consumer outcomes, the only answer is to work in a trusted data sharing approach with your customers.”

Multi-currency payment services company Conotoxia launched multi-currency card 2.0.

The update enables cardholders to add users to their card.

The multi-currency card 2.0 enables cardholders to hold accounts in 20 currencies and pay in more than 160 currencies.

Multi-currency payment services company Conotoxia is making it easier for users to share payment cards with friends, family, and employees. The new capabilities come as part of the company’s new launch, multi-currency card 2.0.

“We have been observing very strong interest in our multi-currency cards. Customers recognize their advantages and their superiority over bank debit cards,” said Conotoxia Vice President Pitor Kicinski. “The multi-currency card 2.0 and its new functionality can mean significant savings for families and businesses, as well as, for example, an interesting gift for those traveling abroad or shopping in international shops.”

Existing cardholders can share their card with new users after they register with Conotoxia. Once the new user is registered, they can begin making transactions using both physical and virtual cards. Meanwhile, the primary cardholder can view the card balance, control expenses, and set spending limits.

With the multi-currency card 2.0, cardholders can hold accounts in 20 currencies and can pay in more than 160 currencies. The tandem Conotoxia mobile app for iOS and Android enable users to view their transaction history, manage cards, and more. At the start of 2022, Conotoxia added Apple Pay as a payment option for cardholders, and contactless payments are also available with Google Pay, Fitbit Pay, and Garmin Pay.

Launched in 2014, Conotoxia offers foreign exchange and cryptocurrency trading, online payments, and online currency exchange in addition to its multi-currency cards. The company employs more than 250 people in its offices based in Poland, Illinois, and The Republic of Cyprus.

London-based regtech Sumsub has partnered with Paris-based money transfer company Tempo.

The partnership will help Tempo enhance its user identity verification operations and reduce fraud in line with French regulations.

Sumsub made its Finovate debut at FinovateEurope 2020 in Berlin, Germany.

London-based regtech Sumsub – which stands for Sum & Substance – has teamed up with Paris-based money transfer company Tempo. The partnership will enable the French fintech to leverage Sumsub’s technology to verify user identities and secure customer data in line with KYC and AML regulations. Tempo will benefit from access to a range of KYC services and the partnership already has enabled Tempo to meet AML compliance requirements as established by French regulators.

“We are glad to offer our all-in-one verification platform to global digital payments providers like Tempo, making money transfers more accessible to people worldwide,” Sumsub CEO and co-founder Andrew Sever said. “With Sumsub’s KYC. KYB, transaction monitoring and AML solutions, it’s easier for businesses to expand to international markets and increase their client base while staying fully compliant with regulations and ensuring bulletproof fraud protection.”

Sumsub made its Finovate debut two years ago at FinovateEurope 2020 in Berlin, Germany. At the conference, the company demoed its KYC/AML Checks and Risk Management Toolkit, which enables businesses to accelerate verification, and lower costs by as much as 6x, as well as detect and eliminate digital fraud. The company offers global coverage of more than 200 markets and combines best-in-class technology with human legal expertise to enable Sumsub to help companies in diverse regulatory regimes.

In a statement, Tempo France CEO Alla Zhedik highlighted the fact that Tempo is licensed by the Bank of France. “This imposes strict compliance obligations,” Zhedik said. “And that is where KYC plays a great role and is also why the joint project with Sumsub is so important for us.” Zhedik added that the partnership not only helped minimize fraud and money laundering risks, but also gives Tempo “access to the most advanced customer data processing solutions.”

With more than 2,000 customers in verticals ranging from fintech and digital assets to transportation and gaming, Sumsub claims to have achieved some of the highest conversion rates in the industry, reaching more than 91% in the U.S., and more than 95% in the U.K. The company said that is is able to verify users in less than 50 seconds on average.

Sumsub’s partnership news comes one month after the company announced that it was joining Brazilian fintech association, ABFintechs. Also in November, Sumsub reported that Markor Technology, provider of B2B and B2C technology solutions for iGaming operators, had selected Sumsub to provide enhanced verification and fraud protection.

Glia and Jack Henry announced a partnership this week that will integrate Glia’s Digital Customer Service into Jack Henry’s Banno digital banking platform.

The integration will enable a wider number of banks and credit unions to interact with their customers via digital channels such as voice and video banking.

Glia and Jack Henry are both Finovate alums. Jack Henry made its Finovate debut in 2010. Glia has won Best of Show at Finovate conferences six times.

A newly announced partnership between a pair Finovate alums will bring some of the latest innovations in digital customer service to more bank and credit union customers. Digital Customer Service specialist Glia announced this week that its technology is now available via Jack Henry’sBanno Digital Platform.

The integration will give financial institutions using the platform the ability to engage customers across all digital channels – from SMS and chat to voice and video banking. Glia’s acquisition of fellow Finovate alum Finn AI in June adds innovative virtual assistance technology to Glia’s offering – technology that will now be available to banks and credit unions on Jack Henry’s platform. The integration was facilitated by the Banno Digital Toolkit, which uses the same set of APIs upon which the Banno Digital Platform is built.

“Glia is making Digital Customer Service accessible to a growing number of banks and credit unions, empowering them with powerful tools to digitalize and transform customer service,” Glia SVP of Alliances Steve Kaish said. “Our integration with Jack Henry accelerates that mission, allowing more institutions to facilitate digital-first engagements within the digital domain.”

A six-time Finovate Best of Show winner, Glia most recently demoed its Digital Customer Service technology at FinovateSpring last year. At the conference, Glia showed how its latest innovation automatically connects customer inbound calls to the customer’s associated online browsing sessions to give customer service representatives context when handling the customer query. This helps improve the quality of the session, making it easy for the representative to collaborate online with the caller via features like co-browsing, screensharing, and one- or two-way video. This, according to Kaish, will help “community institutions create competitive advantage” versus their national and international rivals.

Founded in 2012, Glia is headquartered in New York City. Daniel Michaeli is CEO and co-founder.

With more than 9,000 customers in the U.S., Jack Henry offers banks and credit unions an ecosystem of innovative financial services solutions, as well as the ability to integrate with leading fintechs. Headquartered in Monett, Missouri, and founded in 1976, the company made its Finovate debut in 2010 and has since grown into a major technology and payment services company with $1.7 billion in revenue for the fiscal year ended June 30, 2021. Jack Henry is a publicly traded entity on the Nasdaq under the ticker “JKHY,” and has a market capitalization of $13 billion.

A Finovate alum since 2010, Jack Henry & Associates was featured in Computerworld’s “Best Places to Work in IT” list for 2023. This week, the company announced that it was adding automated policy management technology to its Governance, Risk, and Compliance (GRC) Suite. David Foss is President and CEO.

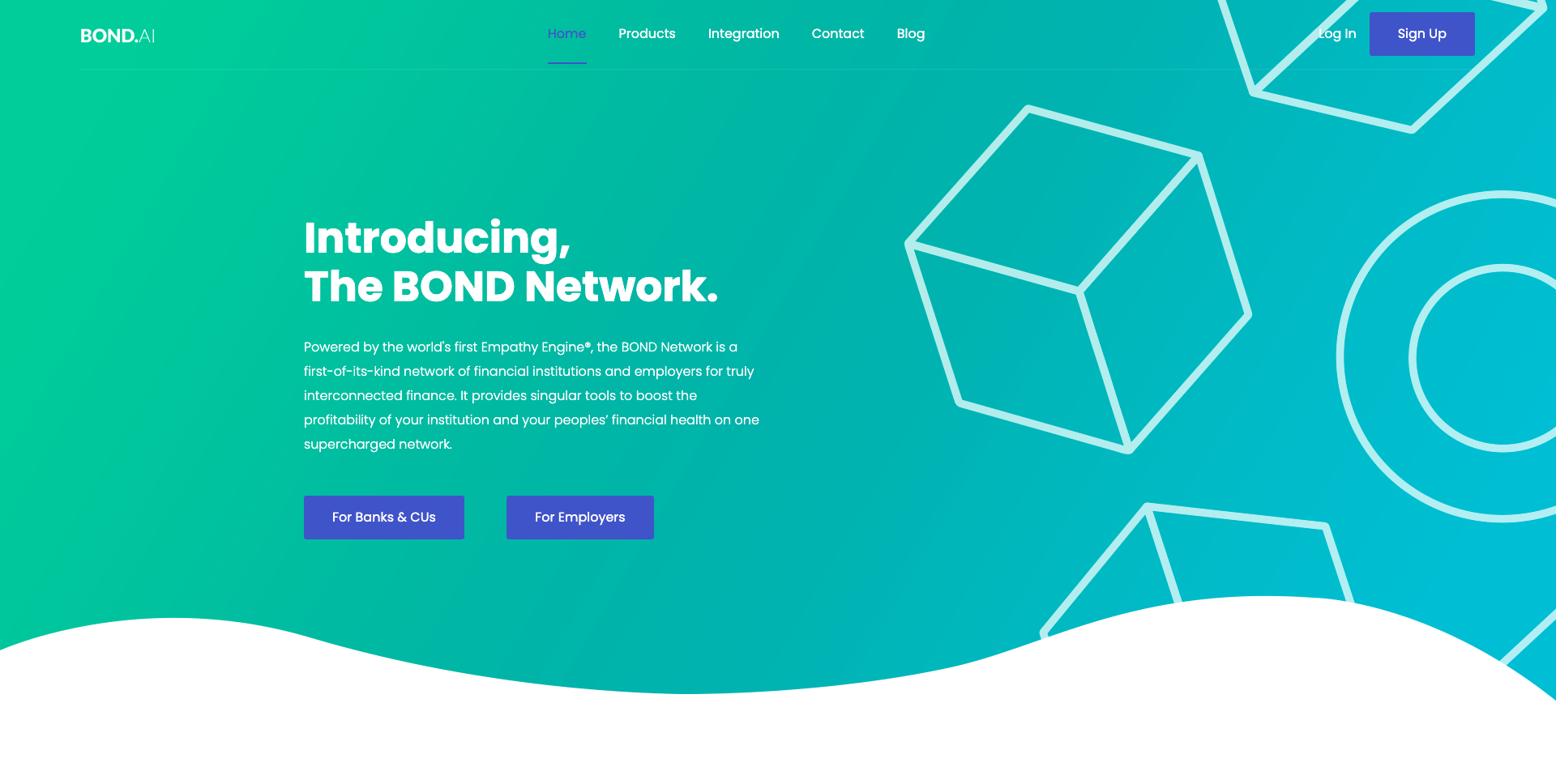

One of the more compelling presentations at FinovateFall this year was the keynote address from BOND.AI CEO Uday Akkaraju. Titled “Why the Future of Finance is Beyond Finance, And How to Get There,” Akkaraju’s discussion looked at the wave of digital transformation in financial services and asked “is there a radically smarter path to profitability while staying relevant to customer expectations?”

We pick up on this conversation in today’s extended interview with the BOND.AI CEO. Akkaraju has leveraged his background in interaction design and cognitive science to help make machine intelligence more empathetic and human-oriented. The result is the world’s first Empathy Engine for finance – a technology that helps bridge the gap between consumers struggling to meet their financial needs and banks that are eager to engage these consumers with new technologies that offer greater personalization and effectiveness.

Founded in 2016 and headquartered in Little Rock, Arkansas, BOND.AI won Best of Show in its Finovate debut at FinovateFall 2018. We talked with the company’s CEO about the how the company is helping financial institutions better serve their customers, as well as what to expect from BOND.AI in 2023.

You recently spoke at FinovateFall on Why the Future of Finance is Beyond Finance. Can you tell us a little bit about what you shared with our audience in that keynote?

Uday Akkaraju: It was my pleasure to be asked to speak again at FinovateFall this year. A lot has changed since I spoke last time in 2018! And a lot has changed for the better in terms of banking.

The pandemic spurred investments in technology and digital channels to reach customers—a benefit for the banking and fintech industry. However, we must now utilize opportunities accelerated by the pandemic to create a future of better financial health for everyone.

I wanted to use my keynote speech to highlight the “Empathy Gap” between what customers need and what banks can offer today, especially given the fast-changing economic environment. For me, it’s essential we discuss how fintech can help bridge the communication gap between banks and customers. Banks need to strategically implement discourse analysis tools with measurable KPIs to ensure they don’t return to past mistakes.

That’s where human-centered AI comes in. In this case, AI is our chatbot-powered Empathy Engine that can converse with customers via an app to get a deeper understanding of their needs. Through conversation, banks can grow their revenue using customers’ contextual information. With more customer data, individual banks can meet and even predict an individual’s needs, improving financial health as they tailor their products and services as a result. Of course, conversational data is only a part of it. You still need the bank data – otherwise, you only get half the truth.

BOND.AI won Best of Show at FinovateFall 2018 with a live demo of its Empathy Engine. You’ve also talked about something you call the “Empathy Gap.” For the uninitiated, what does the “empathy gap” mean?

Akkaraju: The Empathy Engine is our main vehicle for closing the gap between customer needs and a bank’s inability to meet those needs, which we’ve labeled the “Empathy Gap.” We quantify this gap between what banks offer and what individuals need to be worth roughly $34.2 trillion. I like to say the only thing that changes faster than technology is consumer expectations. Unfortunately, banks’ inability to keep up with those expectations leaves them with a lot of money left on the table for them and a lot of lost opportunities for consumers.

The Empathy Engine helps banks to better communicate with and service consumers to close this “Empathy Gap.” We use its ability to talk directly to customers and deliver personalized service at scale. This aids banks in seeing a holistic picture of each individual and better meeting their financial needs.

The main point of my presentation, though, was to make it clear it’s not going to be possible for one fintech or financial institution to close that gap alone. That’s why we created The BOND Network, to connect banks, employers, and fintechs and make it a true network—not just a marketplace—to balance the needs of all three stakeholders.

How does BOND.AI’s Empathy Engine flow from this?

Akkaraju: We launched the world’s first Empathy Engine for finance in 2018. It’s designed to bridge what the consumer needs against what the bank can offer to give a holistic view of customers, including their needs, strengths, weaknesses, and potential.

Right now, for customer segmentation, banks only consider financial data, and that information remains too broad. It fails to keep up with fast-changing consumer expectations or recognize an individual’s circumstantial information. Segmentation should consider both financial and non-financial data to be effective and offer a hyper-personalized approach that talks directly to the customer.

The BOND.AI Empathy Engine was developed in response to this insight. Instead of considering massive amounts of data with lots of noise, the engine moves to a small-data approach, where segmentation happens based on actual and observed behavior rather than traditional correlations and predictors.

Who is BOND.AI’s primary market and how do those customers use your technology?

Akkaraju: Our primary market is currently made up of financial institutions to whom we provide a white-label solution for insights, analytics, and customer communication. These are our core customers, and they are also members and contributors to The BOND Network.

We also have employers on the network who provide our mobile app to their employees as a financial benefit. At this point, we have 28 employers bringing about 300,000 employees into the network, which is set to grow next year.

What makes BOND.AI’s technology unique in the way it solves problems for your customers?

Akkaraju: Our Empathy Engine is the first-of-our-kind, human-centered technology focused on increasing the financial health of institutions and individual consumers. It also powers The BOND Network, which nurtures an ecosystem of financial institutions, fintechs, employers, and employees that all benefit. The engine identifies stakeholder needs and connects the dots to fulfill those needs, thus making this a network rather than a marketplace.

This is how our efforts move ‘beyond finance’. We believe to bridge the Empathy Gap it will take collaborative action to understand people as more than just transactional data and talk to them instead to establish their needs and situational context. With AI tools, we can speak directly to customers from the comfort of their own home or on the go with our mobile app. This intimacy builds trust and strengthens the customer’s relationship with their bank, so people feel able to share their problems.

The best part? Insights are there for everyone across the network to see how they can further close the Empathy Gap.

I think some would be surprised to learn that BOND.AI has headquarters in Little Rock, Arkansas. What does Little Rock offer a company like BOND.AI?

Akkaraju: There’s a lot we feel Little Rock can offer us, which is why we moved here! We were previously based in New York but chose Little Rock strategically for both the company and our employees. The work-life balance is good here. There’s also barely any commute considering most places can be reached in 20 minutes. That’s ideal for a fast-growing start-up where time is money.

There has been a move away from the coast, but tier-two cities are also getting a little cramped. People are happy to explore other options at this point, and Little Rock is an interesting place where both company and employee dollars stretch further.

There are also a lot of possibilities here for us as a start-up looking to connect with employers and their workers. Walmart’s headquarters is here, and many of its vendors are nearby. You don’t need to move to the city to find talent and opportunity. The next thing we’d like to do is start consciously investing in the local talent we think is out there to really prove that to people.

What can we expect from BOND.AI in 2023?

Akkaraju: In 2023 we’re excited for our app to be going direct-to-consumer via employers and expanding our partnerships for The BOND Network. We’ll be using these acquisitions to grow the company organically. These developments will also aid us in our mission to give the power of data back to the consumer and show banks what types of data they can leverage more effectively.

We want to focus on alternative wealth building, giving more people the tools they need to take control of their finances confidently. Budgeting is good, but it doesn’t fix the bottom line and, in many cases, more support is needed. We want to extend the possibilities of financial inclusion by giving everyone access to the tools used by high-net-worth individuals and sharing guidance on how to use them.

If you plan on binge watching holiday movies in the next few weeks (or if you have been since October), here’s something to think about. Did you know that many of these films come with lessons for the fintech industry?

Here are some films you may want to watch over your winter break, along with some of the wisdom they hold.

Home Alone (1990)

In this movie, Kevin McCallister finds himself left at home without any adults to help him carry out daily tasks and defend himself against burglars. In the same way, many customers are conducting their banking activities from home on their own devices. The only tools they have to successfully conduct banking activities are a strong password and your bank’s user-friendly design.

Lesson: Don’t make your customers feel at home alone. Provide them with tools they need to successfully conduct everyday banking tasks from your app.

It’s a Wonderful Life (1946)

After George Bailey contemplates suicide during a time of financial instability, his guardian angel comes to show him all the ways in which he has made a difference in the lives of others. In the end, he begs his angel to give him his life back. After he does, his community rallies around him to help him regain financial stability. The current economy is impacting firms across banking and fintech differently. Every organization has a storm to weather.

Lesson: Pay attention to what’s truly important in life and maintain a focus on community, especially in the midst of economic turmoil.

Family Stone (2005)

When a woman from the big city, Meredith, accompanies Everett, her boyfriend, to his childhood home for Christmas, they both discover that they aren’t right for one another. As the story progresses, it becomes apparent that Everett and Meredith’s sister Julie are falling for each other. Keep your bank or fintech partners in mind while watching this one.

Lesson: Finding the right bank or fintech partners can be a struggle. However, it is worth conducting proper due diligence to find the right partner before committing.

The Santa Clause (1994)

Toy salesman Scott Calvin is unexpectedly forced to become Santa Clause after the original Santa Clause falls off his roof. After spending much of the movie in denial and resisting his new role as Saint Nick, Scott Calvin ultimately accepts his new role, and everyone is better off because of it. Has your organization ever had to make a similarly drastic pivot?

Lesson: When the needs of the customer evolve, so should your business. Being able to pivot to meet customer expectation not only benefits end users, it will also be good for your bottom line.

Die Hard (1988)

When New York City Policeman John McClane visits his ex-wife at a holiday party on Christmas Eve, terrorists attempt to take over the building and John realizes that he is the only one who can save everyone. Whether you can see the fraudsters or not, everyone deals with them on a daily basis.

Lesson: You are responsible for creating the first line of defense between your customers and cybercriminals.

Jingle All the Way (1996)

In this holiday movie, Howard Langston tries to impress his son by giving him the season’s hottest toy, the Turbo-Man, for Christmas. The toy is almost sold out, however, and Howard goes to great lengths to compete with another father to get the toy. Ultimately– and only after proving himself a hero– Howard gets the Turbo-Man toy to give to his son in time for Christmas. While the customer acquisition race isn’t as competitive as a war over the Turbo-Man toy, it may seem like a battle at times.

Lesson: There will always be competition between and among banks and fintechs. And just like Howard’s fight for Turbo-Man, fighting to gain customers takes sacrifices and ultimately may require your organization to prove itself a hero to the customer before winning them over.

How the Grinch Stole Christmas (1966)

The Grinch, who hates Christmas, tries to take the joy away from the townspeople of Whoville by stealing their presents and other Christmas paraphernalia. Even after he does so, however, he hears the townsfolk joyfully celebrating Christmas, despite the lack of presents, food, and decorations. In the end, the Grinch realizes that Christmas is more than presents, tinsel, and bows. Just as the Grinch discovered there is more to Christmas than the money-making aspects of it, perhaps we can all look beyond our bottom lines this season to discover how we can better serve our target market.

Lesson: Perhaps there is more to fintech than just pandering to populations that seem the most profitable. Look for ways to benefit to others, even if they may be a net-zero opportunity.

Any Hallmark Christmas special

Many Hallmark holiday movies seem to share a similar premise. A big-city girl inherits a vineyard or a bed and breakfast in a small town. During her visit to the country, she meets a charming man and falls in love with both him and the small town lifestyle. You don’t have to watch a Hallmark movie to realize that expanding your horizons can be beneficial.

Lesson: It may profitable to serve the underserved populations found in rural locations. They could have more in common with your existing target audience than you think.

National Lampoon’s Christmas Vacation (1989)

Clark Griswold tries to create the perfect Christmas for his family, but when the Christmas bonus he expected for the year fails to come through, Clark’s cousin Eddie takes the issue up with Clark’s boss. Though Clark ends up receiving his bonus after all, the movie serves as a reminder not to financially overcommit before funds are guaranteed.

Lesson: Even when times are good, don’t count on extra cash to get your company through. Watch your burn rate.

Frozen (2013)

The main characters, sisters Anna and Elsa, illustrate the ups and downs of the crypto market. After Elsa freezes the town, the damage seems permanent, and residents wonder if they will have to live in wintertime conditions forever. At the end of the film, Elsa figures out how to control her magic and returns the town to its regular climate.

Lesson: Crypto will one day exit the crypto winter and will once again level out. The key to achieving this stasis may be the arrival of regulation in the cryptocurrency space, which is already be on its way. Today, U.S. Senator Elizabeth Warren unveiled a bill to enforce against crypto money laundering.

The financial services industry has seen a breathtaking amount of innovation over the last decade thanks to fintech applications that streamline user experiences and improve operational efficiencies. Many of these solutions incorporate third-party viewing integrations that allow people to view and manage documents, eliminating the need to switch back and forth between different software.

Implementing specialized viewing technology saves time and resources during the development process so fintechs can get their products to market faster. By selecting the right integration partner from the beginning, they can put themselves in a position to scale capabilities in the future without suffering unexpected costs or compromising performance.

Viewing Integrations and the Problem of Scale

Fintech developers often turn to API-based viewing integrations like Accusoft’s PrizmDoc because they provide the tremendous power and flexibility that modern financial services applications require. Whether it’s file conversion, robust annotation, document assembly, or redaction, fintech software must be able to provide extensive document processing features to meet customer expectations.

In order to implement those advanced viewing capabilities, the developer usually needs to set up a dedicated server as part of their on-premises infrastructure or in a cloud deployment. One of the biggest advantages of API-based integrations is that customers only have to pay for the processing resources they use, but this can also pose some challenges when it comes to scaling application capacity.

As fintech companies expand their services, they need to be able to deliver document viewing capabilities to a larger number of users. If each viewing session requires the server to prepare and render documents for viewing, costs can quickly escalate. As server workloads increase, viewing responsiveness may be affected, resulting in delays and slower performance.

While some users may still need to use server-based viewing to access more powerful imaging and conversion features, many customers simply need a quick and easy way to view and make minor document alterations. Fintech developers need a versatile solution that can meet both requirements if they want to scale their services smoothly.

Introducing PrizmDoc Hybrid Viewing

PrizmDoc’s new Hybrid Viewing feature provides fintech applications the best of both worlds by offloading the document processing workloads required for viewing to client-side devices. Rather than using server resources to convert files into SVG format and render them for display, Hybrid Viewing instead converts files into PDF format and then delivers that document to the end user’s browser for viewing.

Shifting the bulk of document processing work to client-side devices significantly reduces server workloads, which translates into lower costs for fintech applications.

For documents not already in PDF format, the PrizmDoc Hybrid Viewing feature offers new PDF viewing packages that pre-convert documents into PDF for fast, responsive local viewing. By reducing the server requirements for rendering files, fintech providers can easily scale their applications without worrying about additional users increasing their document processing costs. PrizmDoc Hybrid Viewing also eliminates the need for separate viewing solutions implemented to work around server-based viewing, which allows developers to streamline their tech stack and further optimize customer experiences.

PrizmDoc’s Hybrid Viewing feature provides FinTech developers with several important benefits that improve application flexibility and deliver greater value to their customers.

Resource Savings Hybrid Viewing minimizes server loads by offloading the bulk of the processing required to view a document to client-side devices. Reducing server requirements translates into lower costs and frees up valuable processing resources for other critical fintech workloads.

Scalable Viewing Shifting the processing work required for viewing to local devices allows fintech applications to scale their user base with minimal cost.

Enhanced Performance Offloading document preparation to the end user’s device improves viewing speed and responsiveness, especially for large documents.

Increased Productivity Diverting workloads to client-side devices allows application users to process, view, and manage multiple documents faster. Fintech developers can leverage Hybrid Viewing to provide a better user experience that helps their customers to be more efficient and productive.

Improved Storage Management For documents not already in PDF format, Hybrid Viewing can utilize PDF-based viewing packages that are significantly smaller than conventional SVG viewing files. Files can be pre-converted for fast, easy viewing without taking up extra storage space.

Enhance FinTech Applications with PrizmDoc Hybrid Viewing

PrizmDoc’s new Hybrid Viewing feature allows fintech developers to seamlessly scale their application’s viewing capabilities without having to deploy new servers or rethink their cost structure. Shifting document processing to local devices provides end-users with faster, more responsive performance, especially when viewing lengthy documents. By keeping viewing-related costs low, fintech developers can focus their resources on developing new application features that help their products stand out in an increasingly competitive market.

ING Germany has tapped Paysafe’s cash arm, viafintech, to offer its users cash deposit and withdrawal services.

Using ING Germany’s Banking to Go app, customers can deposit and withdrawal cash at more than 12,500 participating brick-and-mortar stores.

Withdrawals are free, but customers will be charged a 1.5% fee on the total amount they deposit.

Global payments platform Paysafeannounced today that its cash arm, viafintech, has partnered with ING Germany. Under the agreement, ING Germany will leverage viafintech for its cash deposit and withdrawal features.

viafintech’s technology will enable ING Germany to offer its nine-plus million customers to access a new feature, ING Cash, in its Banking to Go app. The tool will empower users to make cash deposits or withdrawals from their current account at participating brick-and-mortar retailers.

Here’s how it works: a customer decides how much they want to withdraw or deposit, and the app generates a barcode that they can scan at a participating brick-and-mortar store. Currently, ING Germany has more than 12,500 participating stores in Germany, including Rewe, Penny, Rossmann, and dm drogerie Markt.

Users are not required to make a minimum purchase at the retail locations. And while it is free for them to withdrawal funds, ING Germany charges a 1.5% fee on the total amount they deposit.

viafintech was founded in 2011 and was acquired by Paysafe in 2021. The company’s API offers organizations access to its payment infrastructure that enables cash withdrawals and deposits, bill payments, credit payouts, cashless payment methods, prepaid solutions, and gift cards.

Paysafe is a legacy player in the fintech space, having launched in 1996. The U.K.-based company offers payment processing, digital wallet, and online cash solutions connecting businesses and consumers across 100 payment types in over 40 currencies around the world. Last year, Paysafe processed $120 billion in transactions. The company is publicly listed on the New York Stock Exchange under the ticker PSFE and has a market capitalization of $824 million.

Alumni Alley is the latest addition to our upcoming FinovateEurope conference in March. This new feature is exclusively for FinovateEurope alums, and will give these companies a unique opportunity to share their latest innovations in a special showcase at the event. Learn more about FinovateEurope’s Alumni Alley and see if it’s a fit for you!

This week we continue our commemoration of FinovateEurope’s earliest alums with a look at SaaS accounting platform innovator Xero, digital communications provider Striata, and digital identity pioneer miiCard – now DirectID.

Your Cloud Accounting Platform Hero, Xero

Believe it or not, there was once a debate about whether or not accounting technology truly qualified as fintech. Helping make the case were companies like Xero, a Wellington, New Zealand-based startup, founded in 2006, that was bringing its SaaS accounting solution to small businesses and their accountants around the world. When the company made its Finovate debut at FinovateEurope in 2011, the five-year old firm had raised $35 million and had 27,000 customers in 50 countries. Today, Xero is a cloud-based accounting powerhouse with more than $680 million in equity capital raised, and more than 3.5 million subscribers to its technology around the world.

Xero’s new CEO Sukhinder Singh Cassidy

Founded by Rod Drury, who was CEO of Xero until 2018, Xero offers small businesses the tools they need to manage many critical financial operations including accepting payments, billpay, inventory and project tracking, expense claim and invoice management, and more. A partnership with fellow Finovate alum Gusto enables Xero users to calculate pay and deductions, as well as make payroll payments to employees.

Earlier this month, Xero announced that Sukhinder Singh Cassidy had been appointed as the company’s new CEO. Cassidy will take the reins from Steve Vamos, who has served in the position for almost five years. Xero Chair David Thodey praised his new CEO as a “purpose-driven and human-centered leader who is passionate about supporting our customers and is committed to growing and nurturing Xero’s unique and vibrant culture.”

Striata Becomes Tilte: Beyond the Business of eDoc Delivery

The business of edocument delivery has changed significantly over the decade-plus since FinovateEurope 2011. But New York-based customer communications specialist Striata, which made its Finovate debut at our European event that year, has continued to innovate in this space, transforming complex customer communications systems and leveraging multi-factor authentication and encryption key management to ensure both security and compliance.

This helps explain why the company caught the eye of customer communications management (CCM) software and services company Doxim who, in 2020, acquired Striata for an undisclosed sum. The acquisition integrated Striata’s technology into Doxim’s CCM Platform, helping move the solution closer to Doxim’s goal of offering an “integrated SaaS CCM platform” that supports the entire omni-channel customer communications lifecycle.

Striata CEO Michael Wright introducing his company to audiences at FinovateEurope 2011.

“For over 20 years, Striata has been innovating in the CCM space by delivering digital-first solutions across multiple industries, channels, and devices,” Striata CEO Michael Wright said when the acquisition was announced. “As the world evolves into a digital community, a platform approach to scalable and secure yet personalized communications will be critical.”

In October, Striata underwent another transition as the firm’s South Africa team, under the leadership of Wright, launchedTilte.cx. The new venture is an IT services and consulting company that helps businesses enhance customer engagement via solutions ranging from digital communications and chat commerce to customer journey orchestration and data analysis.

Innovations in Digital Identity: from miiCard to DirectID

The FinovateEurope 2011 demo from Edinburgh-based miiCard (now DirectID) helped introduce many fintech observers to the challenges – and opportunities – in the field of trusted online identity.

Founded in 2010, miiCard appeared on the FinovateEurope stage with an identity-as-a-service solution that enabled users to prove that they “were who they said they were” online in minutes. The verification was as authentic as a physical passport or photo ID, establishing identity to level of assurance 3+, as well as meeting both KYC and AML compliance requirements.

Company founder and CEO James Varga introducing miiCard – now DirectID – at FinovateEurope 2011.

Founded by James Varga, who continues to serve as the company’s CEO, miiCard rebranded to The ID Co. in 2016. The move reflected the growth of the company’s B2B DirectID service, which, launched in 2014, provided an “all-in-one” embedded, integrated verification solution that was especially valuable for financial institutions processing high value transactions online.

“Our mission is to create a layer of trust online, a digital world where you can trust that people really are who they say they are,” Varga said when the rebrand was announced. “Our new company name represents who we are, and better reflects our mission to help solve one of the greatest challenges of our time.”

Four years later and the impact of DirectID on the company’s business was so profound that another rebrand was launched, this time naming the company after what had clearly been demonstrated to be the firm’s most accomplished solution. “The market has changed so much, and data has become such an important part of our offering, that this change in focus was required,” Varga explained in a blog post.

Since the latest rebrand, DirectID has forged partnerships with a wide range of companies including authentication company Trust Stamp and credit hire organization AX. More recently, DirectID teamed up with U.K. payments company ShieldPay and secured $3 million in new funding.

Insurtech company Oyster received $3.6 million in seed funding.

The round was led by New Stack Ventures.

Oyster was founded in 2021 by Blend, Stripe, and Strategy& alumni Vic Yeh, Jon Patel, and Nikhil Kansal.

Insurtech company Oysterreceived $3.6 million in funding this week. The Seed Round was led by New Stack Ventures with contributions from Global Founders Capital, Conversion Capital, Cambrian Ventures, SNR VC, Kearny Jackson, Valia Ventures, Interlace Ventures, V1 VC, and a group of angel investors.

Oyster a new take on insurance. It provides merchants an embedded insurance tool to integrate into their point-of-sale that offers customers insurance for a good or service they are about to purchase. Oyster will use today’s investment to fuel its point-of-sale insurance platform and add more merchant partners. The company’s list of merchant partners currently includes Bulls Bikes, Jewels by Grace, Zooz Bikes, Bario Neal, Area 13 Ebikes, and The New Wheel.

“You can buy a $5,000 ebike or engagement ring online in just a few clicks and get it delivered the next day. Want to get insurance for that purchase? Good luck! It’s an offline process that can take many days and lots of paperwork,” said Cambrian Ventures Founding Partner Rex Salisbury. “Oyster is offering embedded insurance for high growth ecommerce categories to allow consumers to seamlessly insure some of their most important possessions at point of sale in a few minutes. It’s a huge opportunity to move personal insurance into the digital age.”

Oyster differentiates itself by offering affordable insurance rates for products including bikes, ebikes, jewelry, phones, collectibles, and electronics. The company provides full coverage from theft, loss, and accidental damage– and many policies offer a zero dollar deductible.

The company was founded in 2021 by Blend, Stripe, and Strategy& alumni Vic Yeh, Jon Patel, and Nikhil Kansal. The team recognized the insurance market as one of the last financial sectors to be disrupted by the technological innovations of the past two decades. “The insurance industry is still in the early innings of digital transformation,” the company said in a blog post announcement. “As such, we’re accelerating the speed of innovation in order to provide the best-in-class products and services to our customers and partners.”

A pair of Finovate alums — Salt Edge and ebankIT – have teamed up to help financial institutions leverage open banking to provide more services to customers.

The partnership will enable ebankIT’s bank and credit union clients to access accounts from more than 5,000 financial institutions.

Salt Edge is headquartered in Toronto, Ontario, Canada. ebankIT is based in Porto, Portugal.

A newly announced partnership between Finovate alums ebankIT and Salt Edge will help financial services companies in Canada, Europe, and elsewhere to maximize the opportunity of open banking. The partnership will enable ebankIT to empower banks and credit unions to access accounts from more than 5,000 banks. At the same time, working with Salt Edge – an ISO 27001 certified company licensed as an AISP under PSD2 – will ensure that open banking compliance requirements across regions will be fulfilled.

“At ebankIT, we understand that Open Banking is the way forward when it comes to humanizing the digital banking experience for millions of end-users worldwide,” ebankIT Head of Sales HQ and Partnerships Pedro Leite said. “That’s why we believe that this partnership with Salt Edge will bring great benefits to our ecosystem of financial institutions.”

With its Omnichannel Digital Banking Platform, ebankIT helps financial institutions to make digital transformations, regardless of their size. Currently licensed to FIs in 11 countries, ebankIT’s platform enables banks and credit unions to offer customer experiences across all modern digital channels, from online and mobile to wearables and the metaverse. A Best of Show winner at FinovateFall in 2019, the Portugal-based company most recently demonstrated its technology this spring at FinovateEurope.

In addition to its partnership with Salt Edge, ebankIT has teamed up with other Finovate alums in 2022. In October, the company announced that it was working with multiple-time Finovate Best of Show winner MX to integrate MX’s Insights and Personal Financial Management (PFM) tools into its digital banking platform. Earlier this year, ebankIT announced a collaboration with another multiple-time Finovate Best of Show winner, Horizn. This pact is designed to help financial institutions smoothly launch new ebankIT platform deployments for both front-line employees and customers.

Salt Edge, which demoed its technology at a part of FinovateEurope in 2018 and 2019, was founded in 2013 and is headquartered in Toronto, Ontario, Canada. The company offers both an open banking gateway – to help companies access account information, conduct payment initiation, and leverage data enrichment to turn raw data into actionable insights – as well as a PSD2 compliance hub. Salt Edge’s compliance hub provides a full-stack compliance solution for banks and electronic money institutions, strong, mobile customer authentication, and TPP verification.

“As two cutting-edge tech players pursuing to revolutionize the financial world, we strive to create innovative solutions that will improve financial services for both institutions and consumers,” Salt Edge Chief Growth Officer Alina Beleuta said. “By teaming up, we can double our forces to bring innovations to the financial landscape through seamless open banking solutions.”

What does it take to be a fintech analyst? You have to be willing to get things wrong on occasion. Along with that, you need to be able to admit when you’re wrong. This becomes most apparent every December, when it comes time to share predictions on what the fintech industry can expect in the coming year.

Many of my predictions for 2023, which you can find published in this month’s eMagazine, were shaped from looking back at the trends I predicted for the latter half of 2022. Here’s a look at some of those trends, along with an assessment of how I did and a prediction for how the trend will fare in 2023.

Prediction #1: Beginning the era of “neo super apps”

How I did: Wrong. With every other fintech company claiming to be a super app these days, this prediction is slightly subjective. In my opinion, however, we haven’t entered an era of neo-super apps.

What to expect: A year ago, I would have identified the first potential U.S. super app as PayPal. However, Walmart has been making strides in this area and is getting ready to compete in the fintech arena. As a bottomline, we are still a ways out from super apps taking over fintech.

Prediction #2: Accelerating M&A activity

How I did: Somewhat correct. In comparing M&A activity to pre-pandemic 2019 levels, M&A activity has indeed increased. Though year-end data for 2022 hasn’t been published yet, according to FT Partners’ Q3 2022 Fintech Insights Report, there have been 998 deals so far in 2022. While this represents a slight increase over the 986 M&A deals conducted in 2019, it is a large slide from the 1,486 deals closed last year.

What to expect: The recent economic decline is causing companies to watch their pockets closely and mitigate risk where they can. Many large fintechs have already made major layoffs in order to maintain their bottomline or reduce their burn rate. These factors will contribute to both lower deal numbers and deal volume in 2023.

Prediction #3: Dwindling conversation around digital transformation

How I did: Correct. While the need for digital transformation across verticals has not subsided, the continuous pulse of conversation around digital transformation has eased up.

What to expect: This does not mean that digital transformation is over. In fact, many of the conversations we can expect to have in 2023– such as embedded finance, banking-as-a-service, and personalization– are built on the foundation of digital transformation.

Prediction #4: More discussion around Central Bank Digital Currencies (CBDCs)

How I did: Correct. In the U.S., the Federal Reserve has not taken much action toward creating a CBDC other than issuing a discussion paper on the topic. However, there has been a flurry of activity around CBDCs across the globe. In December of 2021, nine countries had launched a CBDC, while today, 11 have launched their own CBDC. Similarly, CBDC development has increased. In December of 2021, 14 companies had a CBDC in development, while today there are 26 countries with a CBDC in development.

What to expect: In the U.S. the discussion around CBDCs will progress, especially now that the FTX scandal has brought to light the need for more governmental intervention and oversight.

Prediction #5: BNPL takes a backseat

How I did: Wrong. Though there have been many publications warning consumers about the dangers of misusing BNPL tools, we are still seeing a regular pulse of new BNPL launches throughout the industry. And while the CFPB published a study on the growth of BNPL and its impact on consumers, the organization has not implemented any formal regulation restricting BNPL players’ movements in the market.

What to expect: I’m refreshing this prediction for 2023. Consumers have over-leveraged themselves when it comes to BNPL, and it is not only starting to catch up with them, but it is also catching up with the BNPL companies themselves. According to the CFPB’s study, “Lenders’ profit margins are shrinking: Margins in 2021 were 1.01% of the total amount of loan originated, down from 1.27% in 2020.”

Additionally, though the CFPB has been vague on the timing, there is looming regulation facing BNPL tools. “Buy Now, Pay Later is a rapidly growing type of loan that serves as a close substitute for credit cards,” said CFPB Director Rohit Chopra. “We will be working to ensure that borrowers have similar protections, regardless of whether they use a credit card or a Buy Now, Pay Later loan.”

Subsiding talent acquisition

How I did: Correct. Though companies will always face difficulties trying to secure quality employees, we are no longer seeing the tech talent war that we experienced in 2021. In fact, in the latter half of 2022, we saw the opposite. A handful of fintech companies, including Plaid, Autobooks, MX, Klarna, Brex, Stripe, Chime, and more, have laid off sizable portions of their staff.

What to expect: The painful reality is that the layoffs will likely continue into 2023 as the economy continues to contract.