This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

PayPal launched a small business credit card this week.

The PayPal Business Cashback Mastercard is PayPal’s first business credit card.

PayPal also offers a range of other tools for small businesses, including working capital tools, business loans, risk management support, and more.

Small businesses in the U.S. have gained yet another credit card option this week with PayPal’slaunch of its its first commercial credit card.

The PayPal Business Cashback Mastercard, which is issued by WebBank, has no annual fee and offers cardholders 2% cashback on all purchases. The rewards are not subject to earning caps nor do they expire. Additionally, the card comes with free employee cards, does not charge a foreign transaction fee, and integrates with PayPal’s merchant platform to facilitate access to transactions, balances, available credit, and rewards.

Once a business is approved for the card, it can immediately begin spending via a virtual card that is automatically integrated into their PayPal account. Businesses can view their account and spending details via their PayPal Business account.

“As small business owners continue to recover from the challenges of the past two years, having multiple financing options to address their capital needs is more important than ever,” said PayPal Vice President of Global Merchant Lending Bernardo Martinez. “The PayPal Business Cashback Mastercard provides merchants greater value, more choice, and the increased flexibility they need to manage their business finances, offering among the best value available on no annual fee business credit cards today. This new solution continues PayPal’s commitment to supporting small businesses and offering options to help manage the day-to-day costs of operating their business.”

Founded in 1998, PayPal has long been an ally to small businesses. In addition to the business credit card, the California-based company also offers a working capital solution that has distributed more than $20 billion, as well as payout capabilities, business loans, payment acceptance tools, risk management support, and more. These products have helped PayPal amass 20 million small business customers in the U.S. And this is no small feat, given the fact that there are only 33 million small businesses in the U.S.

The launch of the The PayPal Business Cashback Mastercard comes five years after PayPal launched its credit card for individual users in 2017.

PayPal is boosting its humanitarian efforts in Ukraine.

The payments company is expanding upon its P2P money transfer services, waiving fees, and facilitating funds transfers to payments cards.

These efforts are being made in addition to the company’s Cash Pick-Up and Mobile Phone Reload tools.

Citizens across the globe have donated millions of dollars in aid to the people living in Ukraine since the Russia invasion last month. And financial services provider PayPal is paying attention. The San Francisco-based company announced three new moves yesterday that will help people living in the region access humanitarian funds.

Peer-to-peer payments expansion

PayPal is expanding upon its existing money transfer services. The company is enabling Ukrainian PayPal accountholders to send and receive peer-to-peer (P2P) payments in four currencies– USD, CAD, GBP, and EUR.

Waiving fees

PayPal is waiving its own fees until June 30 for customers sending funds to Ukrainian PayPal accounts or receiving funds into Ukrainian PayPal accounts. Additionally, PayPal’s international remittance service, Xoom, is waiving transaction fees sent to recipients in Ukraine.

Funds transfers

PayPal will allow Ukrainian accountholders to transfer funds from their Ukrainian PayPal Wallet to an eligible Mastercard or Visa debit or credit card. Once the transfer has taken place, the money will be available in the currency associated with the payment card.

In addition to these new efforts, PayPal also offers Cash Pick-Up, a feature that enables digital money transfers to be sent to be picked up at physical locations throughout Ukraine such as Oschadbank, Privatbank, and Ukrgasbank; and Mobile Phone Reload, a tool to reload mobile phone airtime at five telco carriers.

PayPal is among many other fintechs making technological efforts to stem the violence in Ukraine and bring aid the country’s citizens. And as Russia’s war crimes continue and the situation worsens, we expect to see more fintechs rise to the occasion.

PayPal has confirmed recent rumors regarding plans to launch its own stablecoin. According to Bloomberg, which broke the news last week, a developer found evidence of PayPal’s future stablecoin in the form of the below logo inside the fintech’s iPhone app.

Photo credit: Bloomberg

SVP of Crypto and Digital Currencies at PayPal Jose Fernandez da Ponte later confirmed the suspicion. “We are exploring a stablecoin; if and when we seek to move forward, we will of course, work closely with relevant regulators,” Fernandez da Ponte told Bloomberg.

Developer Steve Moser made the discovery by looking at hidden code inside the PayPal app. The code unveils work on PayPal Coin, a PayPal-specific stablecoin that would be backed by the U.S. dollar. After PayPal was made aware of the discovery, the company confirmed that the code was part of a recent internal hackathon and that details surrounding the project will likely change.

If the project comes to fruition, the stablecoin would be just one initiative among a host of other cryptocurrency efforts. In October of 2020 the company partnered with cryptocurrency company Paxos to allow PayPal users in the U.S. to buy, hold, and sell cryptocurrencies. And last March, PayPal launchedCheckout with Crypto, a tool that enables users with cryptocurrency holdings to transact using crypto at the online point of sale.

When it comes to working on a stablecoin launch, PayPal is in good company. Meta (formerly Facebook) was developing its own stablecoin, Diem, until it experienced regulatory hurdles and pivoted to work with the Pax dollar instead. On top of that, Visa is looking to leverage a stablecoin to settle transactions.

In addition to its stablecoin ambitions, PayPal is also hoping to gain a reputation as the first super app in the U.S. The company revamped its mobile app last September and now offers a range of features including direct deposit, billpay management, rewards, and more. Founded in 1998, PayPal is now listed on the NASDAQ under the ticker PYPL. The company’s market capitalization currently sits at $213 billion.

PayPalannounced this week it is partnering with online retail giant Amazon. Under the agreement, PayPal’s Venmo will be listed as a payment option for U.S. Amazon shoppers online and in the Amazon mobile app. Venmo’s 80 million users will have the option to pay with their Venmo balance or their Venmo-linked bank account.

Venmo SVP and GM Darrell Esch explained that the new integration enhances the versatility of users’ Venmo accounts. “Over the last year, we have focused on giving our Venmo community more ways to use Venmo in their daily lives, including the ability to pay with QR Codes and providing more shopping features like purchase protections,” he said.

The new payment capability will come at a good time for Venmo users. According to the press release, 65% of Venmo users increased their online purchasing behaviors during the pandemic and 47% are interested in paying with Venmo at checkout.

Amazon will also benefit from providing an additional payment option for its customers. “We understand our customers want options and flexibility in how they make purchases on Amazon,” said Amazon’s Director of Global Payment Acceptance Ben Volk. “We’re excited to team-up with Venmo and give our customers the ability to pay by using their Venmo accounts, providing new ways to pay on Amazon.”

The move likely won’t help Venmo win any new users from Amazon’s 300 million active user base, however. That’s because most Amazon shoppers have already entered their preferred payment method into their Amazon Wallet, which currently allows for credit cards, debit cards, store cards, checking accounts, HSAs, FSAs, and EBT. And because Amazon is an expert at making payments disappear into the background of the user experience, most users don’t think about adding a new payment method unless their is an issue with their current one.

There is no exact date as to when Venmo will be integrated into Amazon’s checkout flow, however PayPal said it “will be available in 2022.”

Venmo has been around since 2009 and is known for its popularity among Millennials as a peer-to-peer payment app. Over the past couple of years, however, the New York-based company has proven that it does more than just help 20-year-olds exchange $15 and pizza emojis. Earlier this year, Venmo launched a check cashing feature that enables users to cash paper checks in the Venmo app. The company also offers debit and credit cards, as well as a crypto offering that allows users to buy, sell, and hold cryptocurrencies.

The Buy Now Pay Later (BNPL) revolution shows no signs of abating any time soon. A combination of newcomers, Buy Now Pay Later pioneers, and even credit card companies like Visa and Mastercard are figuring out new ways to integrate themselves into the biggest consumer commerce phenomenon since shopping by smartphone.

According to CNBC, which bases its analysis on data from FIS Worldpay, the Buy Now Pay Later market has an estimated value of $60 billion globally as of 2019 – though there are even higher estimates. Excluding China, this sum represents 2.6% of all e-commerce. And while BNPL represents less than 2% of sales in North America, the overall BNPL market, CNBC believes, could reach $166 billion by 2023.

Here is just a smattering of this week’s headlines from the Buy Now Pay Later beat that only underscores the velocity of the flight from credit cards and traditional consumer financing.

Stripe teams up with Klarna as BNPL competition from Square, PayPal intensifies

Klarna, a company with a long pedigree in providing consumers with alternative payment options, announced this week that it was partnering with ecommerce innovator and payments platform Stripe. The deal will enable Stripe customers in 20 countries to offer Klarna as a payment option to their customers. As part of the partnership, Klarna will use Stripe to accept payments from consumers in both the U.S. and Canada.

“Over the past years, Klarna and Stripe redefined the e-commerce experience for millions of consumers and global retailers,” Klarna Chief Technology Officer Koen Köppen said. “Together with Stripe, we will be a true growth partner for retailers of all sizes, allowing them to maximize their entrepreneurial success through our joint services. By offering convenience, flexibility, and control to even more shoppers, we create a win-win situation for both retailers and consumers alike.”

The partnership is widely seen as a way for Stripe to compete with payments rivals PayPal and Square, which have deepened their commitment to BNPL in recent months. Square agreed to acquire Australia’s Afterpay for $29 million in August. A month later, PayPalannounced its $2.7 billion acquisition of Japanese Buy Now Pay Later company Paidy.

Affirm partners with American Airlines to ease cost of holiday travel

In a move well-timed to take advantage of end-of-year travel trends, American Airlines has announced a partnership with Buy Now Pay Later innovator Affirm. The collaboration will enable eligible travelers to pay for the costs of airfare over time on an installment basis, providing them with “flexibility, transparency, and control,” according to Affirm Chief Commercial Officer Silvija Martincevic. Using Affirm, travelers can pay for flights costing at least $50 with monthly installments without having to pay late fees or worry about hidden charges.

“While consumers are as eager as ever to get away,” Martincevic said, “they remain conscious of fitting travel into their budget.” Martincevic cited a survey conducted by the company that indicated that 74% of Americans queried said they would spend more on holiday travel this year “than ever before,” but that 60% were worried that they would not be able to “afford to travel as they would like to.”

The offering is currently available only to select customers, but will be expanded to include more U.S. consumers in the weeks to come. The collaboration marks the first time that American Airlines has integrated BNPL options into its website.

Marqeta and Amount announce collaboration to help banks offer BNPL

The partnership announced this week between card issuing platform Marqeta and bank technology provider Amount will make it easier for financial institutions to get into the Buy Now Pay Later business. Marqeta and Amount have forged a virtual card and loan origination partnership that will enable banks to go to market with their own BNPL/virtual card offering in months. This will help them boost revenues, grow market share, and promote loyalty.

Echoing the challenge that banks and other financial institutions face from Big Tech and fintech alike, Amount CEO Adam Hughes pointed to the partnership with Marqeta as a way for banks to close the consumer expectations gap between themselves and more tech-savvy, tech-native enterprises entering the financial services space. “Banks must compete or continue to lose market share to digital challengers who offer a more flexible way for their customers to pay,” Hughes said.

Part of what makes the Marqeta/Amount partnership interesting is how it takes advantage of research that suggests that a significant number of consumers who have used BNPL would prefer it if the service came from their bank or credit card provider. Amount’s modular approach to BNPL is configurable, easy to deploy, and integrates readily with banks’ legacy platforms, giving FIs the ability to introduce BNPL offerings over a variety of different channels and payment methods.

Berlin-based Billie banks $100 million in funding

The latest reminder of the international growth of Buy Now Pay Later comes from the $100 million investment secured by Berlin, Germany-based, B2B Buy Now Pay Later startup, Billie. The Series C round was led by U.K.-based Dawn Capital and featured participation from Tencent and, interestingly enough, Klarna. In fact, Klarna’s investment comes in the wake of a strategic partnership with Billie in which the two companies will integrate their service to better leverage their core competencies, with Billie serving business customers and Klarna handling retail consumers.

“BNPL for B2B is still in its infancy phase,” Klarna CEO and co-founder Sebastian Siemiatkowski explained, “even though the demand has never been higher. We are here to solve problems and by being able to offer this service to our merchant partners together with Billie, we are doing just that.”

The Series C round gives Billie a valuation of $640 million, and is believed to be the largest B2B Buy Now Pay Later funding round to-date. Co-founder and co-CEO of Billie, Dr. Matthias Knecht noted that those companies buying from larger businesses and individual retailers are increasingly embracing a “digital-first” approach that includes not just “modern user interfaces, high limits for shopping carts, as well as real-time decisions for B2B” but options like BNPL, as well. “There is nearly no provider of a BNPL product (for these companies) like what Klarna offers for B2C,” Knecht said. “We aim to close this gap.”

Visa expands BNPL offerings in Canada via partnership with Moneris

International card company and financial services provider Visa has been making inroads of its own into the Buy Now Pay Later market. This week, the company made headlines in the Canadian fintech news space via a new collaboration with unified commerce company Moneris.

“We’re happy to be working with a trusted brand like Visa Canada on providing a buy now pay later option to Canadians,” Moneris Chief Product and Partnership Officer Patrick Diab said. “Bringing flexible payment methods like buy now pay later to our merchants helps them offer their customers more options when it comes time to pay.”

Courtesy of the new collaboration, merchants partnered with Moneris will be able to leverage Visa’s BNPL solution – Visa Installments – to give eligible Canadian credit cardholders access to installment payments on qualifying purchases. Cardholders can use the existing credit on their cards to pay for purchases in smaller, equal payments over a defined time period, with no additional, new service sign ups or requirement to apply for a new line of credit.

Moneris is set to begin offering Visa Installments to its customers by the spring of 2022.

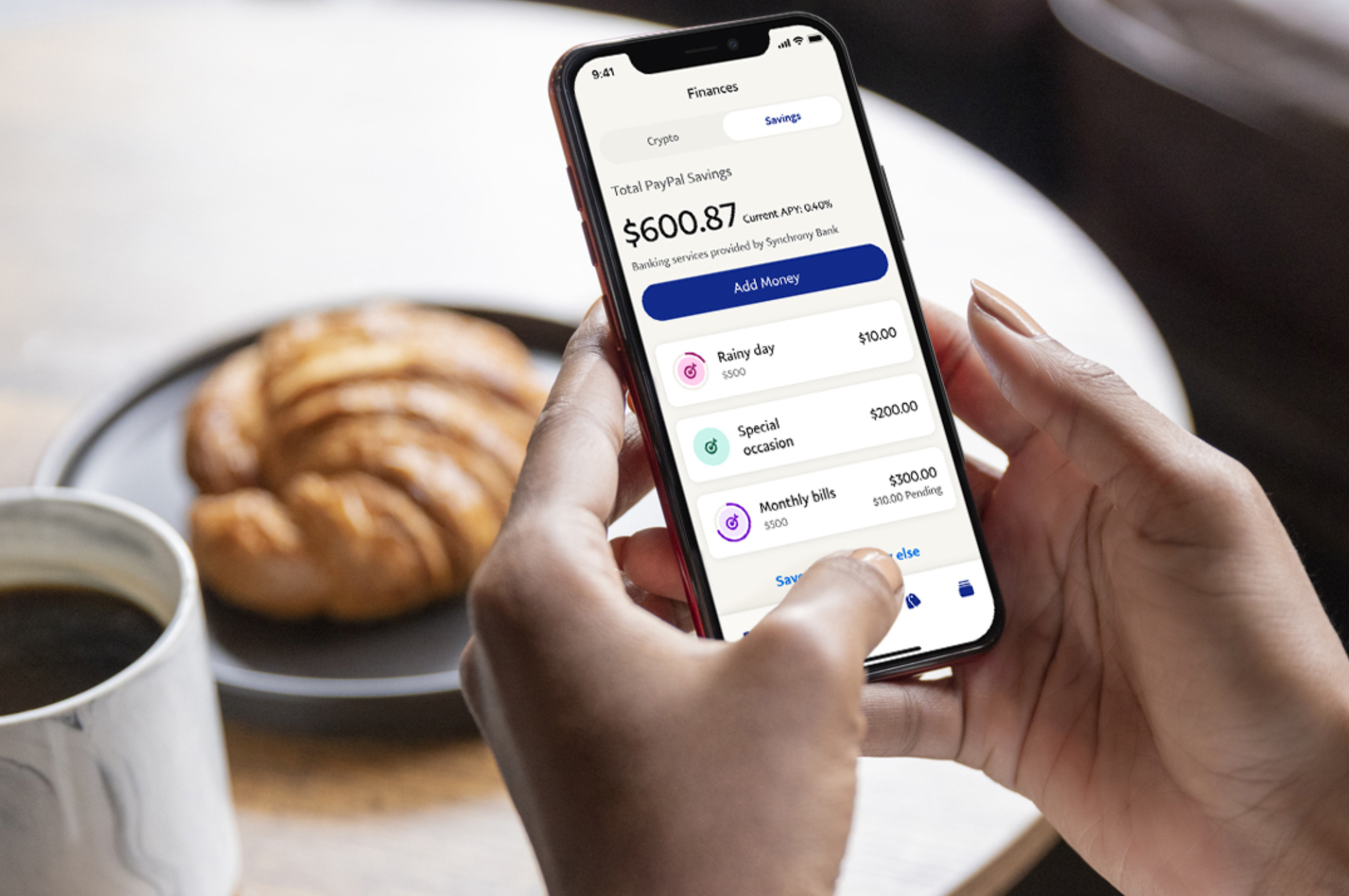

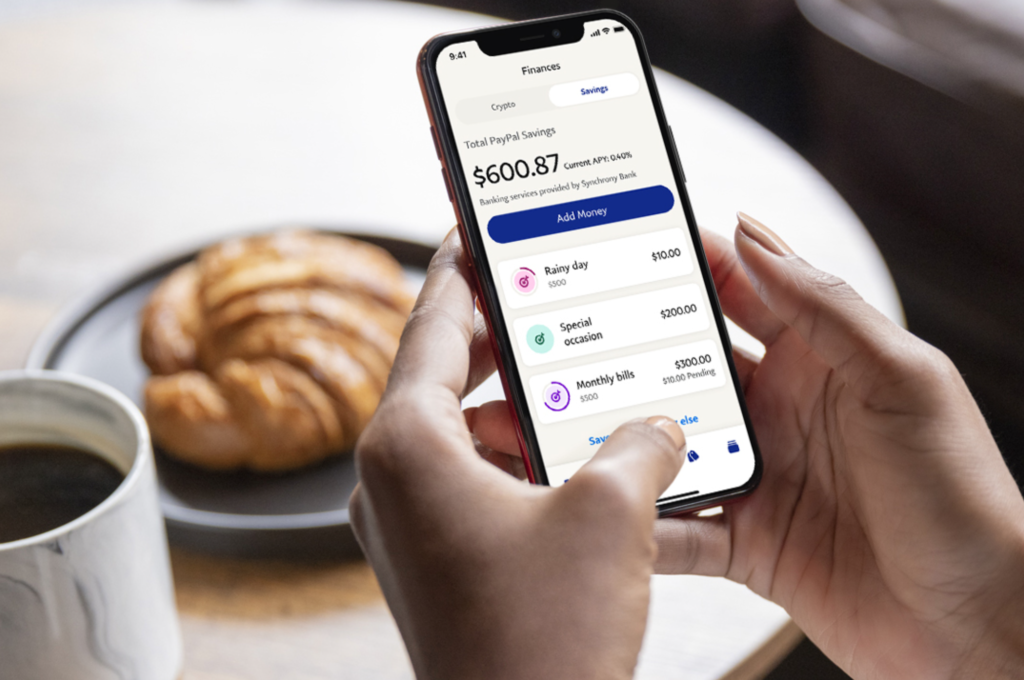

The company is adding a handful of features that bring it into “super app” territory, competing with the likes of WeChat, Alipay, and Paytm. PayPal’s app already offers a peer-to-peer payment tool, a mobile wallet, and a charity donation feature.

The new release, however, will offer more features and new banking capabilities. Here’s a rundown of what to expect:

PayPal Savings, a new, high-yield savings account provided in partnership with Synchrony Bank that pays 0.40% APY

In-app shopping tools that allow customers to discover and earn loyalty rewards

Billpay management tools that help users track, view, and pay their bills

A new Direct Deposit feature that fronts users their paycheck up to two days early

Rewards capabilities

Gift card management

Credit access

Buy Now, Pay Later services

Crypto purchasing, holding, and selling abilities

The app will show users a personalized dashboard of their account; a wallet tab to manage payments and direct deposits; a finance tab to access savings and crypto accounts; a payments tab that enables users to send and receive money, make a donation, and manage billpay; and a messaging feature built around peer-to-peer payments.

“We’re excited to introduce the first version of the new PayPal app, a one-stop destination for our customers to take charge of their everyday financial lives, with new features like access to high yield savings, in-app shopping tools for customers to find deals and earn cash back rewards, early access Direct Deposit, and bill pay,” said PayPal CEO Dan Schulman. “Our new app offers customers a simplified, secure and personalized experience that builds on our platform of trust and security and removes the complexity of having to manage multiple financial or shopping apps, remember different passwords and track loyalty rewards.”

What’s next for PayPal’s Super App? The company will add investment tools, offline QR code payments, and new shopping and deals capabilities.

PayPal is currently the closest thing the U.S. has to a super app. However, the new app is still missing some key elements that Asia’s successful super apps have, including food delivery, transportation, travel, health, insurance, government, and public services.

The Road to Greater Financial Inclusion in Latin America

This week’s Finovate Global Reports takes a look at the drive for financial inclusion in Latin America. BN Americas this week featured a research survey conducted by Peruvian financial services company Credicorp and research firm Ipsos. The study queried approximately 8,400 households in seven Latin American countries: Bolivia, Chile, Colombia, Ecuador, Mexico, Panama, and Peru.

The key takeaways from the study underscored both the need for more aggressive efforts to boost financial inclusion, as well as the concern that those most in need of financial services are also those who are the most marginalized in society overall. The survey highlighted special challenges when it comes to better engaging women, seniors (people over the age of 60), as well as people living in rural locations and those with “limited education and income” in the mainstream financial ecosystem.

Credicorp Head of Corporate Affairs Enrique Pasquel said that promoting financial inclusion was a critical component of improving the business climate in Latin America. “If Latin America continues to have societies where not all enjoy the same benefits,” Pasquel said, “it’s difficult to see how a business can be viable in the long term.”

Education is one of the tools Pasquel sees as especially valuable in driving greater financial inclusion in the region. Many of the study’s respondents who had low levels of engagement with their country’s financial system pointed to a number of issues – from a lack of interest to an inability to see the benefits to a sense that the services available were not necessary to them – as chief obstacles.

Nevertheless, Pasquel believes that the benefits of financial inclusion – such as the increased safety in enabling individuals to reduce their use of cash – are significant enough to overcome many of these reservations. He called on the private sector to play a greater role in financial inclusion efforts.

Checking In on Fintech Innovation in the Middle East

IBS Intelligence took a look at the fintech industry in Egypt and highlighted a quartet of companies – Fawry, MoneyFellows, Paymob, and Yomken – that it believes represent the pinnacle of fintech in North Africa’s most populous country.

The article noted that recent changes in the financial services industry in Egypt are likely responsible for what has made fintech one of the fastest-growing sectors in the country. The Arab republic passed major new banking legislation in 2020 that, in addition to mandating new minimum capital requirements for Egyptian banks, also provided new guidance for both the Egyptian banking sector, as well as for the country’s growing population of e-payments startups, fintech companies, and cryptocurrency firms.

With a tip of the hat to the four major Egyptian fintechs noted by IBS Intelligence, this week’s Finovate Global Lists is sharing eight other fintechs from the country that have made recent Finovate Global headlines. While not as well known as the quartet highlighted above, we think the eight Egypt-based fintechs below are worth keeping an eye on in the months and years to come.

Cassbana: Helps underserved communities obtain financial identities via micro-lending and an AI-powered, behavior-based scoring system.

Dayra: Provides financial services to un- and underbanked gig economy workers and micro-businesses.

Digital Finance Holding: Supports and promotes fintech innovation in Egypt’s non-banking financial services industry

Flextock: Offers technology-enabled, fast, and affordable fulfillment solutions for businesses.

Hollydesk: Provides a SaaS platform for SMEs that supports daily expense and accounts payable management.

Khazna: Serves underbanked communities in Egypt with a solution that provides convenient and secure smartphone-based financial services.

MoneyHash: Offers a single platform to enable access to payment and financial services across the Middle East and Africa.

Telda: Provides a P2P payment service designed for Egypt’s Millennial and GenZ population.

Here is our look at fintech innovation around the world.

PayPalannounced plans today to acquire Japan-based Paidy, a payments company with a buy now, pay later (BNPL) offering that facilitates transactions for both merchants and consumers. The deal is expected to close for $27 billion (¥300 billion) in the fourth quarter of this year.

PayPal’s purchase will work alongside its existing ecommerce business in Japan, which is the third largest ecommerce market in the world. Paidy will also expand PayPal’s capabilities, relevancy, and distribution in Japan’s domestic payments market.

“Paidy pioneered buy now, pay later solutions tailored to the Japanese market and quickly grew to become the leading service, developing a sizable two-sided platform of consumers and merchants,” said VP and Head of Japan at PayPal, Peter Kenevan. “Combining Paidy’s brand, capabilities, and talented team with PayPal’s expertise, resources, and global scale will create a strong foundation to accelerate our momentum in this strategically important market.”

Paidy was founded in 2008 and enables its six million registered users to make purchases online without the use of a debit or credit card. Instead, Paidy operates on a BNPL model by billing customers for all purchases at the end of each month. Payments can be made via bank transfer or in-person using cash at a convenience store.

This model works not only for ecommerce purchases, but also for brick-and-mortar transactions. The company’s Paidy Link tool was launched earlier this year and allows customers to link digital wallets, including PayPal, to make purchases using the digital wallet but make payment via Paidy. For PayPal, Paidy’s model that circumvents credit and debit card rails is a good thing. It enables PayPal to own the payment flow (and the revenue that comes with it).

“Paidy is just at the beginning of our journey and joining PayPal will accelerate our plans to expand beyond ecommerce and build unique services as the new shopping standard,” said Paidy President and CEO Riku Sugie. “PayPal was a founding partner for Paidy Link and we look forward to working together to create even more value.”

Sugie, along with Paidy Founder and Executive Chairman Russell Cummer, will continue to lead Paidy, which will continue to operate and maintain the brand.

Paidy marks PayPal’s 23rd acquisition, following Honey in 2019 and Curv and Happy Returns in 2021. The purchase of Paidy, with its BNPL capabilities, hints at PayPal’s evolution into becoming more of a holistic shopping platform.

U.S. payments platform PayPal has been slowly inching toward becoming a super app in the past few years. Today’s news that the California-based company has acquired Happy Returns indicates a step further toward that goal.

Terms of the deal are undisclosed.

“The post-purchase experience is something we’ve been looking into, since it’s such a pain point — people want to shop online and return in store, and vice versa,” PayPal SVP of Consumer In-Store and Digital Commerce Frank Keller told CNBC in an interview. “For retailers, we’re providing more comprehensive services beyond payments.”

Happy Returns launched in 2015 to provide box-free, in-person returns for online orders. The company sees the benefits as three-fold– it makes for a better customer experience, it is less expensive for the merchant, and is less wasteful and therefore better for the environment.

Consumers making purchases at one of Happy Returns’ hundreds of brand partners can use the company’s software to make returns at 2,600+ drop-off locations in 1,200+ cities across every U.S. state.

What started as PayPal’s flagship payments platform expanded to encompass the pre-purchase shopping experience when the company acquired Honey in 2019. Today, with the addition of Happy Returns, PayPal adds another element to serve the post-shopping experience to its already robust platform.

This holistic shopping experience is in line with PayPal CEO Dan Schulman’s plan for the company. Schulman recently announced PayPal will roll out a “next-generation” digital wallet that will offer a personalized shopping, financial services, and payments experience.

PayPallaunchedCheckout with Crypto today. The new development enables users with cryptocurrency holdings to seamlessly transact using crypto at the online point of sale. Starting today, U.S. shoppers can make purchases using crypto at millions of online businesses.

The new Checkout with Crypto payment option will automatically appear in U.S. users’ PayPal wallets at checkout when they have a cryptocurrency balance of Bitcoin, Litecoin, Ethereum, or Bitcoin Cash that will cover an eligible purchase. Because PayPal makes money when users buy and sell cryptocurrencies on its platform, it is not charging additional transaction fees.

“As the use of digital payments and digital currencies accelerates, the introduction of Checkout with Crypto continues our focus on driving mainstream adoption of cryptocurrencies, while continuing to offer PayPal customers choice and flexibility in the ways they can pay using the PayPal wallet,” said PayPal President and CEO Dan Schulman. “Enabling cryptocurrencies to make purchases at businesses around the world is the next chapter in driving the ubiquity and mass acceptance of digital currencies.”

Essentially, Checkout with Crypto works behind-the-scenes of a transaction to help customers sell cryptocurrency through the PayPal platform. PayPal then uses it to pay a merchant, who receives U.S. dollars in exchange. Because of the embedded nature of the tool, the process happens in one seamless flow at checkout.

There are a few restrictions around Checkout with Crypto. First, the tool is only available to U.S. users. Second, purchases must be eligible. Finally, users can’t split the payment among currency types. In other words, in order to make a purchase in cryptocurrency, they must have a sufficient balance of a single cryptocurrency.

In the coming months, PayPal plans to expand the service to its full list of 29 million online merchant clients across the globe.

This move expands PayPal’s previous cryptocurrency capabilities. In partnership with Paxos, PayPal began enabling users to buying, selling, and holding crypto last October.

Payments ecosystem giant PayPal announced a collaboration with Flutterwave, a leading payments technology company in Africa, this week. Through the collaboration, PayPal will enable its users to pay African merchants using Flutterwave’s platform.

The partnership will not only connect Flutterwave’s African merchant clients with PayPal’s 377 million accountholders, it will also help them work around the fragmented and complex payments infrastructure in Africa. To use the new functionality, online shoppers across the globe simply select the Pay with PayPal option while checking out at an African merchant’s page online.

Flutterwave launched to help businesses and individuals make payments across the continent flexibly and affordably. This comes at a crucial time for Africa. The ecommerce sector on the continent is expanding and is expected to grow from $16.5 billion in 2017 to $29 billion by next year.

“The collaboration reinforces our vision of creating a seamless digital payments system for Africa’s business communities that can now transact with international consumers,” said Flutterwave Founder and CEO Olugbenga Agboola. “By working with PayPal, we can further strengthen our commitment to our customers and service users as we will be enabling them to transact and expand their business operations to reach new markets.”

Flutterwave was founded in 2016 and has since processed over 140 million transactions worth over $9 billion. Today’s news comes just a couple of days after the company closed a $170 million round at a $1 billion valuation.

With a Democratic administration only weeks away from taking office, some are wondering about the prospects for a revitalized Consumer Financial Protection Bureau (CFPB). Created during the last Democratic administration – and largely sidelined during the now-ending Trump administration – the CFPB has found itself back in the fintech headlines in recent days.

PayPal Takes On CFPB Over Card Rules

A federal judge brought resolution to a lawsuit PayPal filed against the Consumer Financial Protection Bureau in December 2019. U.S. District Court Judge Richard Leon agreed with PayPal that the CFPB had overstepped its authority in its effort to regulate prepaid cards and digital wallets. PayPal had asserted that in forcing them to include “short form” fee disclosures that included categories that were not relevant, the CFPB’s rule was confusing customers. What’s worse, customers were being led to believe, PayPal claimed, that they were exposed to a wide variety of potential fees – which was not the case.

The situation seems almost to be one of mistaken identity. The rules being applied by the CFPB with regard to expenses like ATM balance inquiries make sense for providers of reloadable prepaid cards, but not for PayPal, which does not subject its customers to these fees. That said, it was the CFPB’s rule-making authority itself that was the target of what Reuters described as a judicial “decision studded with exclamation points.”

PayActiv Wins Earned Wages Access Approval

Meanwhile, the Consumer Financial Protection Bureau’s aim seems to be more true in the case of of earned wage access. PayActiv, Finovate alum and innovator in the earned wage access space, announced last week that its program is exempt from Federal lending laws per new regulations established by the CFPB.

The key issue was whether or not PayActiv’s Earned Wages Access (EWA) program, which enables workers to get access to their already-earned wages in advance of scheduled paydays, involves credit. If it did, the program would be subject to the Federal Truth in Lending Act, as well as Regulation Z.

Fortunately, the CFPB ruled that “the accrued cash value of an employee’s earned but unpaid wages is the employee’s own money” and, as such, does not create a debt obligation. PayActiv added that the approval was both the first of its kind from the CFPB and specific to PayActiv’s EWA program. The CFPB added that the company’s initiative was an “innovative mechanism for allowing consumers to bridge the gap between paychecks (and) differs in kind from products the Bureau would generally consider to be credit.”

PayActiv co-founder and CEO Safwan Shah called the approval a “watershed moment” for his company. “We are very proud that the CFPB has recognized this important innovation and validated PayActiv’s pioneering work in creating low or no-cost employer-sponsored access to earned wages. Employers can take comfort in knowing that PayActiv continues to be the leader in responsible EWA for employees.”

Synchrony Gets Nod for Secured/Unsecured Credit Card

The new dual feature credit cards (DFCC) from Synchrony Bank are designed to provide financing opportunities for consumers who do not have strong credit profiles. Cardholders provide a security deposit in order to use the credit cards in their secured mode and, if certain eligibility criteria are met after a minimum of one year, the cardholder becomes eligible to use the card in its unsecured mode. And last week, the CFPB gave the wholly-owned subsidiary of Synchrony Financial the green light to go forward with its DFCC solution.

In large part, the CFPB’s ruling for Synchrony represented a broader embrace of bringing financing to consumers with lower credit scores. The Bureau referred to these efforts as “represent(ing) a potentially significant point of access to credit for certain consumers” and favorably compared Synchrony’s dual feature card to other secured card offerings.

Critically, Synchrony will provide complete transparency with regard to the cost differences between the secured and unsecured features, including the lower rate on the secured card. Cardholders that graduate to the unsecured Synchrony credit card are not eligible to return to the secured card.