This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

The collaboration will enable merchants to rely on a chargeback alert system that notifies them in the event of an impending chargeback. Notifications are made via the ChargebackZero dashboard, which combines a variety of alert types from card issuers with ChargebackZero’s dispute management tools. The alerts allow merchants to identify and revolve customer disputes with the customer’s issuing bank in near-real time. By preventing chargebacks, including chargebacks that occur post-authorization, the partnership will make it easier for merchants to accept more orders without increasing their exposure to potentially fraudulent activity.

Ethoca offers a suite of solutions to help merchants and issuers eliminate chargebacks, reduce card not present (CNP) fraud, recover lost revenue, and improve the customer experience with a better dispute resolution process. Ethoca’s Consumer Clarity solution connects issuers to merchant order and account history details in real time. This gives issuer call center agents with the data they need to manage real-time conversations with cardholders when disputes arise. Ethoca also offers its Ethoca Alerts technology, which provides issuers and card-not-present merchants with access to a global collaboration network that enables them to share fraud and customer dispute data in real time, rather than in weeks as is normally the case with chargebacks.

Headquartered in Toronto, Ontario, Canada, Ethoca made its Finovate debut at FinovateFall in 2015. In the years since then, the company has inked partnerships with fellow Finovate alum TSYS, as well as Pegasystems, BlueSnap, and Cartes Bancaires. Ethoca agreed to be acquired by Mastercard in the spring of 2019 for an undisclosed sum. Calling Mastercard “a natural home,” Ethoca CEO Andre Edelbrock said the acquisition would “bring our services to more places and more people, ultimately contributing to the beset possible online payment experience.”

Ethoca serves more than 5,400 merchants in 40+ countries and more than 4,000 card issuers in more than 20+ countries. Eight of the top ten North American ecommerce brands, 14 of the top 20 North American card issuers, and six of the top ten U.K. card issuers use Ethoca’s technology to eliminate chargebacks, prevent fraud, and recover lost revenue.

Uber is launching a new debit card with tandem checking account.

The Uber Pro debit card is made available via partnerships with Mastercard, Marqeta, and Branch.

Uber Pro cardholders can receive up to 7% cashback on fuel purchases.

Uber’s latest attempt to attract more drivers to its platform comes in the form of a debit card with a tandem checking account. Late last week, the rideshare company announced the Uber Pro debit card.

The new debit card comes courtesy of partnerships with Mastercard, Marqeta, and Branch, a workforce payments platform that caters to gig economy workers and contractors. The card offers Uber drivers up to 7% cash back on gas purchases when they achieve Diamond status as an Uber Pro driver.

The Uber Pro card comes with a checking account powered by Branch, which will automatically deposit cardholders’ earnings into their account after every trip. Branch offers a unique take on earned wage access by enabling workers to access their paycheck as they earn it. The card currently has a wait list and will launch in the coming weeks.

This latest announcement comes three years after Uber originally introducedUber Money, a debit card and mobile app powered by Green Dot, and five years after the company launched its Barclays-powered credit card.

The launch of the Uber Pro card comes alongside a handful of other driver-related announcements from the ridesharing company. The Uber app will now offer drivers a range of nearby trips to choose from, show drivers their exact earnings upfront before they accept a trip, and offer enhanced benefits to Uber Pro drivers.

These driver-focused benefits are in part an effort to smooth out the supply and demand issue that Uber is facing. The nationwide labor shortage, combined with high fuel prices, has historically made it difficult for Uber to attract drivers. In May, Uber CEO Dara Khosrowshahi said, “Our need to increase the number of drivers on the platform is nothing new nor is it a surprise … there’s a lot of work ahead of us, but this is a machine that is rolling.”

This week’s edition of Finovate Global takes a look at recent fintech developments in Germany where green banking, embedded finance, and open banking are the themes at the top of this week’s fintech headlines.

First up, Berlin-based Sustainability-as-a-Service innovator ecolytiqannounced that it was teaming up with Slovakian financial institution Tatra Banka. The climate engagement fintech will provide Tatra Banka with the technology the firm needs in order to launch new green banking functionality on its online banking brand, Blue Planet. The new feature, which will be made available to Tatra Banka’s more than 600,000 customers, will enable users to monitor the impact their transactions may have on the environment (for example, with CO2 emissions), provide users with ideas on how to reduce their environmental impact, and offer rewards for spending that is environmentally friendly.

Founded in 2020, ecolytiq demonstrated its technology at Finovate’s developer event, FinDEVr 2021, which was held as a part of FinovateSpring that year. Putting accurate data at the center of the ability to move toward greater environmental sustainability, ecolytiq demonstrated how its open knowledge graph and streaming technology keep its data relevant and current. More recently, the company announced a strategic partnership with exceet Card Group, makers of sustainable payment cards made from wood and, the following month, teamed up with French sustainable neobank Green-Got.

Peter Golha, a director at Tatra Banka said that the institution believed it had a a role to play in the transition toward a more environmentally sustainable economy. “Not only have we a chance to change our own trajectory, but also a chance to live the topic of sustainability alongside our clients,” Golha said.

Founded in 1990, Tatra Banka was the first private bank to be established in Slovakia. Winner of the TREND Bank of the Year award for two years in a row, Tatra Banka announced this spring that it had achieved its greatest profit to date, reporting $164 million (EUR 162.1) in consolidated profits for the financial year 2021.

Second, German financial management platform for businesses Airbank inked a deal with Klarna Kosma this week. Klarna Kosma is an open banking platform launched by Swedish e-commerce innovator Klarna this spring. Seen as a rival to fellow Finovate alum Tink and its open banking platform, Klarna Kosma offers financial institutions, fintechs, and merchants connectivity to more than 15,000 banks in 24 countries around the world via a single API. Kosma was made possible in many ways by Klarna’s acquisition of direct, bank-to-bank payments company SOFORT in 2014, and Klarna has been developing and expanding the service ever since.

“Over the past year, the demand for Open Banking services from financial institutions and fintech startups has reached a tipping point,” Klarna Kosma VP Wilko Klaassen said. “(This) is why we have built a dedicated business unit which brings together engineering, product management, sales and marketing all together in the same team to focus on this $15 billion, fast-growing market.”

Airbank will leverage its new relationship with Klarna Kosma to “accelerate” its expansion into European markets and beyond. Airbank enables businesses to consolidate their bank accounts in a single location, allowing them to more easily automate bill management, make payments, and manage their finances. Companies also can use Airbank’s platform to track their financial transactions and forecast future liquidity. The partnership with Klarna Kosma will make it possible for Airbank to securely access account information from thousands of banks around the world, expand more aggressively, and better serve its SME customers that have global requirements.

“By the end of this year, we will serve over 50 counties, making Airbank the most comprehensive global banking solution for SMEs in the industry, with the ability to connect bank accounts from almost anywhere in the world,” Airbank founder and CEO Christopher Zemina said. “We are delighted to have Klarna Kosma as an experienced and dynamic partner that shares our ambition to shape the future of B2B financial management.”

Lastly, early in the week we learned that Berlin-based embedded finance startup Monite had teamed up with Codat, a U.K. firm that offers a universal API to enable access to consented business data from banking, accounting, and ecommerce platforms. The partnership will enable both SaaS platforms and financial institutions to integrate invoicing and billing functionality into their apps. This will allow platforms and institutions to offer businesses a unified solution for managing their financial operations.

In a statement, the CEOs of both Monite and Codat praised the great variety of financial apps and platforms dedicated to serving SMEs. The challenge, according to both Monite CEO Ivan Maryasin and Codat CEO Pete Lord, is that the variety can be overwhelming for many small businesses. “What’s still missing are the ‘super apps’ that bring everything together,” Maryasin said. “It can be time-consuming to manage and get the most out of them all,” concurred Lord.

Founded in 2020, Monite has raised $7.8 million in funding for its technology that empowers financial institutions and platforms to offer financial services such as multi-banking, AP automation, invoicing, and more to their customers. London, U.K.-based Codat neared unicorn status last month upon raising $100 million in Series C funding. The investment took the company’s total funding to more than $176 million and gave Codat a valuation of $825 million. The round was led by JPMorgan Partners, and featured participation from Plaid and Shopify.

Specifically the partnership will seek to develop “quantum-hybrid” solutions to solve problems in consumer loyalty and rewards, cross-border settlement, and fraud management. The two companies will use D-Wave’s annealing quantum computers and quantum hybrid solvers through the Leap quantum cloud service to deliver real-time access to quantum applications powered by Mastercard’s network.

“People expect hyper-personalized experiences,” Mastercard Chief Innovation Officer Ken Moore said. “Quantum computing’s unique ability to analyze huge numbers of potential combinations can deliver optimal solutions that will improve efficiency and provide choice.” Moore said that the partnership will explore applications of quantum computing technology that offer “practical, real-world” solutions in financial services.

The world’s first commercial supplier of quantum computers, D-Wave is the only firm building both annealing quantum computers and gate-model quantum computers. D-Wave’s technology has been used to solve challenges in a wide range of fields including logistics, drug discovery, cybersecurity, and financial modeling. Founded in 1999 and headquartered in Burnaby, British Columbia, Canada, D-Wave has partnered with firms such as NEC Corporation, Volkswagen, Lockheed Martin, and the University of Southern California. PSP Investments, Goldman Sachs, and BDC Capital are among D-Wave’s investors.

“D-Wave and Mastercard have a shared vision of harnessing the power of technology to positively affect business and society,” D-Wave CEO Alan Baratz said. “This alliance supports that vision by delivering quantum innovation that will tackle increasingly complex problem sets across applications like loyalty programs, fraud management and anti-money laundering in financial services and, ultimately, unlock more value for customers.”

Courtesy of Tencent, Block (formerly known as Square), and existing investor Insight Partners, Indonesian consumer payments platform Flip has secured a $55 million addition to its Series B round. Also involved in the funding were a handful of individual investors including Checkout.com CEO Guillaume Pousaz, DoorDash executive Gokul Rajaram, and former Venmo COO Michael Vaughan.

No updated valuation information was included in the funding announcement. The company has raised a total of $120 million since inception three years ago. Flip raised $48 million in Series B funding in December 2021.

Flip enables millions of Indonesians to access P2P payments with interbank transfers to more than 100 Indonesian banks. The company also offers international remittances, e-wallet top-ups, and business solutions for employee payroll, customer refunds, invoice and supplier payments, as well as international transfers. More than $12 billion in transactions a year are processed on Flip’s platform.

“The growth opportunity of the Indonesian digital economy is vast with its massive population and favorable demographics, Flip co-founder and CEO Rafi Putra Arriyan said. “We are laser-focused on helping millions of Indonesians, both individuals and businesses, execute various money transactions at a low cost through our platform.”

Flip plans to use the new capital to increase headcount, especially with regard to engineering and product development. The company also will invest in new products and technology development to both enhance quality of service and power further expansion.

Crypto may be a fighting word in El Salvador these days, which has hitched its economy to the fate of digital assets like nowhere else. But the move to bring cryptocurrency-based solutions to Latin America is still going strong. Visa announced late this week that it is launching the first crypto cards in Latin America – targeting Brazil and Argentina for the debut of its new products.

As reported in Crypto News and other media outlets that picked up the story from Expansión, Visa has partnered with a number of fintech companies in the region to issue cards that will enable users to receive cashback in Bitcoin when they make payments. In Argentina, Visa’s partners include cryptocurrency exchange Lemon Cash, which will offer 2% Bitcoin cashback Visa cards. Visa also has teamed up with Argentinian cryptocurrency trading platform Satoshi Tango and Crypto.com. In Brazil, Visa is working with Alterbank and Zro Bank.

“The cryptocurrency ecosystem continues to gain momentum in the region with increased investment, more consumer adoption, and more crypto-enabled use cases,” Visa SVP of Products and Innovation for Latin America and the Caribbean Romina Seltzer said. “We will continue to build on our strong strategy to build the future of crypto and payments for our customers, clients, partners, and consumers.”

Here is our look at fintech innovation around the world.

Sub-Saharan Africa

Following up on its acquisition of U.S.-based Global Technology Partners, African digital payments network MFS Africa announced a $100 million equity and debt extension to its Series C round.

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

Mastercard takes the uncertainty out of digital payments with Smart Payment Decisioning Tools. Advanced data analytics and ML make payments faster, more convenient, and safe.

Features

Better onboarding experience

Reduce ACH returns, failure & fraud

NACHA Verification for WEB debit rule

Why it’s great

Mastercard’s Smart Payment Decisioning Tools reduce risk in ACH payments and optimize cost and speed through open banking.

Presenter

Serenie Gagon, VP Product Management Gagon is an experienced product evangelist with deep expertise in the payments space. Gagon is responsible for strategic vision and payment enablement roadmap through open banking. LinkedIn

While much of the financial world is united in its efforts to distance itself from Russia as the country’s leader, Vladimir Putin, orders his forces continue their invasion of neighboring Ukraine, many of those in the cryptocurrency world are decidedly more ambivalent.

Is this a function of the underlying libertarian spirit that powers much of the enthusiasm for digital assets? Or is this just a reflection of a relatively young industry that is not yet ready to take on the responsibilities that its growing role in the financial world will eventually demand?

First, the ask. At the beginning of the week, Ukrainian Vice Prime Minister and Minister for Digital Transformation Mykhailo Fedorov took to social media to ask cryptocurrency exchanges to block transactions from Russia. Federov’s request was not just directed at the Russian government, or the country’s notorious oligarchs, but for everyday Russian users of cryptocurrencies, as well.

“It’s crucial to freeze not only the addresses linked to Russian and Belarusian politicians,” Federov wrote on Twitter, “but also to sabotage ordinary users.”

In the same way that some people have criticized the international sanctions regime against Russia for allowing a loophole when it comes to energy – specifically banning oil and gas exports from Russia – Federov and others have warned that not restricting, if not outright eliminating, Russian access to cryptocurrencies is a critical flaw in the effort to financially squeeze the Russian economy.

In response to this request, many nations have taken action. France’s Finance Minister, Bruno le Maire, said that the EU would include cryptocurrencies in its sanctions. The Financial Conduct Authority in the U.K. has reminded its U.K.-based and regulated cryptocurrency companies of their obligations to respect the sanctions policy against Russia. Even those cryptocurrency firms that are not regulated have been encouraged to support the sanctions regime. “We would urge unregulated member(s) to take action to ensure your platforms do not become a loophole for sanctioned Russians,” U.K. cryptocurrency organization Crypto UK said in a statement.

In the U.S., while some lawmakers have encouraged the government to help ensure that Russians are not using cryptocurrencies to skirt sanctions, the Biden Administration appears less concerned about that threat – at least on the large scale. Carol House, director of cybersecurity for the National Security Council said this week that “the scale that the Russian state would need to successfully circumvent all U.S. and partners’ financial sanctions would almost certainly render cryptocurrency as an ineffective primary tool for the state.” If anything, it seems that U.S. authorities are somewhat more concerned about potential theft and cybersecurity issues surrounding cryptocurrency companies than they are of Russians using these firms and exchanges for what would otherwise be legitimate purposes.

The response from cryptocurrency companies – including some of the largest firms like Binance and Kraken – have suggested that while they are comfortable blocking the accounts of sanctioned Russians, banning all Russians from their platforms is, for these companies, a bridge too far. At least for now.

“We are not political, we are against war, but we are here to help the people,” Binance founder and CEO Changpeng Zhao said, explaining his company’s position. “There are a few hundred individuals that are on the international sanctions list in Russia, mostly politicians, and we follow that very, very strictly.” But Zhao added that Binance draws a line “between the Russian politicians who start wars and the normal people, many normal Russians do not agree with war.”

Similarly, Kraken CEO Jesse Powell tweeted, “I understand the rationale for this request (to block Russians from Kraken’s platform) but, despite my deep respect for the Ukrainian people, Kraken cannot freeze the accounts of our Russian clients without a legal requirement to do so.”

That said, Powell noted, “Russians should be aware that such a requirement could be imminent.”

Additionally, it should be added many cryptocurrency companies are not agnostic to the conflict in the Ukraine and have lent their support to the Ukrainian cause. Federov expressed his, and his country’s, appreciation for the efforts of firms like Polkadot, which donated $5 million, as well as Solana and Everstake, which have created a joint effort called Aid for Ukraine in partnership with the country’s Ministry of Digital Transformation.

“This will certainly contribute to the Ukrainian victory as well as support civil people,” Federov said on Twitter earlier this week. “We will win – the best people (are) with us.”

FinovateEurope 2022 is only a few weeks away. Register today to save your spot at our annual European fintech conference: March 15 digitally and live in London on March 22 and 23.

Here is our look at fintech innovation around the world.

Yesterday, Mastercardunveiled two new clients for its Mastercard Track Business Payment Service. The New York-based payments giant announced that BMO and Moneris Solutions Corporation have joined Mastercard Track.

Mastercard launched the new service for Canadian businesses earlier this year. Mastercard Track creates efficiencies for business users by simplifying and automating the exchange of payments data between buyers and suppliers. The service seeks to modernize the $135 trillion B2B payments market.

“Current business payment processes often require manual reconciliation work that can be very labour intensive,” said Sasha Krstic, President of Mastercard in Canada. “The availability of Mastercard Track through our new partnerships with BMO and Moneris will help Canadian businesses gain freedom from an inefficient process by simplifying and automating the exchange of payments to make B2B payments work harder, faster and smarter.”

Using Mastercard Track will help BMO and Moneris modernize the business payments process for their customers. Ultimately, the service will free up working capital for businesses by offering them more control of their payments and helping them to optimize cash flow management.

Derek Vernon, Head of Payments Modernization of BMO’s North American Commercial Deposits and Corporate Card division said that the service “enhances the digital experience by offering a universal solution to simplify and automate B2B payments.” Specifically, Vernon noted that Mastercard Track will help reduce supplier friction and facilitate quicker speed-to-spend.

Mastercard is a public company listed on the New York Stock Exchange under the ticker MA. It has a market capitalization of $364 billion. Michael Miebach took the helm of the company as CEO in January of last year.

The news is flying a bit under the radar. But from China to Bahrain to Jamaica, central banks are beginning 2022 having made major moves recently in support of digital assets.

We covered China’s CBDC announcement earlier this week. In short, the People’s Bank of China, the country’s central bank, made its digital yuan wallet available via both the Android and Apple app stores. Select Chinese citizens in a wide range of provinces – including Shenzhen, Shanghai, and Chengdu – will be able to download the e-CNY wallet. The Chinese government hopes that there will be significant use of the technology in the weeks leading up to the Winter Olympics in Beijing, which could represent a showcase for the digital currency.

Halfway around the world, the Central Bank of Bahrain (CBB) announced that it has successfully completed its test with Onyx by JPMorgan’s JPM Coin System. The test, the first of its kind in the MENA region, enabled Bank ABC to launch real-time payments for Aluminum Bahrain (ALBA) in the U.S. JPM Coin is a permissioned system that provides payment rail and deposit account ledger services that allow participants to transfer U.S. dollars that are held on deposit with JPMorgan.

“We at the Central Bank of Bahrain are extremely pleased to announce the success of this test which aligns with our vision and strategy to continually develop and enrich the capabilities extended to the stakeholders within our financial services sector in the Kingdom using advanced and leading emerging technologies,” Central Bank of Bahrain Governor Rasheed Al Maraj said in a statement.

JPM Coin is the inaugural product offering from JPMorgan’s Onyx, a blockchain-based platform that facilitates the exchange of value, data, and digital assets. Onyx was formed in 2020.

Several hundred miles to Bahrain’s west, the Bank of Jamaica (BOJ) announced that it also has completed a cryptocurrency pilot. Here, the digital asset is a central bank digital currency (CBDC), which has been undergoing testing in the island nation for the past eight months. The project was conducted in partnership with Irish fintech eCurrency Mint, a company with a 10+ year pedigree in innovation on CBDCs. The stated goal of the initiative was to determine “whether a central bank digital currency along with the attendant technology solution could be successfully implemented in Jamaica.”

Three specific tasks were part of the test: minting of the CBDC, issuing the CBDC to wallet providers, and distributing CBDCs to retail customers. This final component of the test involved wallet provider NCB, and the successful onboarding of 57 customers who conducted person-to-person, cash-in, and cash-out transactions with small businesses as part of an NCB-sponsored event in December called “Market on the Lawn.”

In the wake of the successful test, the Bank of Jamaica has planned a national roll-out of its new CBDC in the first quarter of 2022. The roll-out will feature the continued onboarding of new and existing customers by NCB, the introduction of two additional wallet providers, and a test of transactions between customers of different participating wallet providers to establish interoperability.

Note that Jamaica’s Caribbean neighbor, the Bahamas, launched its CBDC, the Sand Dollar, in October of 2020. The Sand Dollar is the the world’s first official central bank digital currency to reach full circulation.

FinovateEurope 2022 is right around the corner. If you are an innovative fintech company with new technology to show, then there’s no better time than now and no better forum than FinovateEurope. To learn more about how to demo your latest innovation at FinovateEurope 2022 in London, March 22-23, visit our FinovateEurope hub today!

Here is our look at fintech innovation around the world.

Among the country’s largest commercial banks, Taiwan’s Taipei Fubon Bank teamed up with Avaloq to build a wealth management platform for its private banking business in Hong Kong. Avaloq won Best of Show at FinovateAsia in 2018.

Indonesia’s central bank unveiled a new retail payments system, BI-Fast, that will reduce the cost of money transfers.

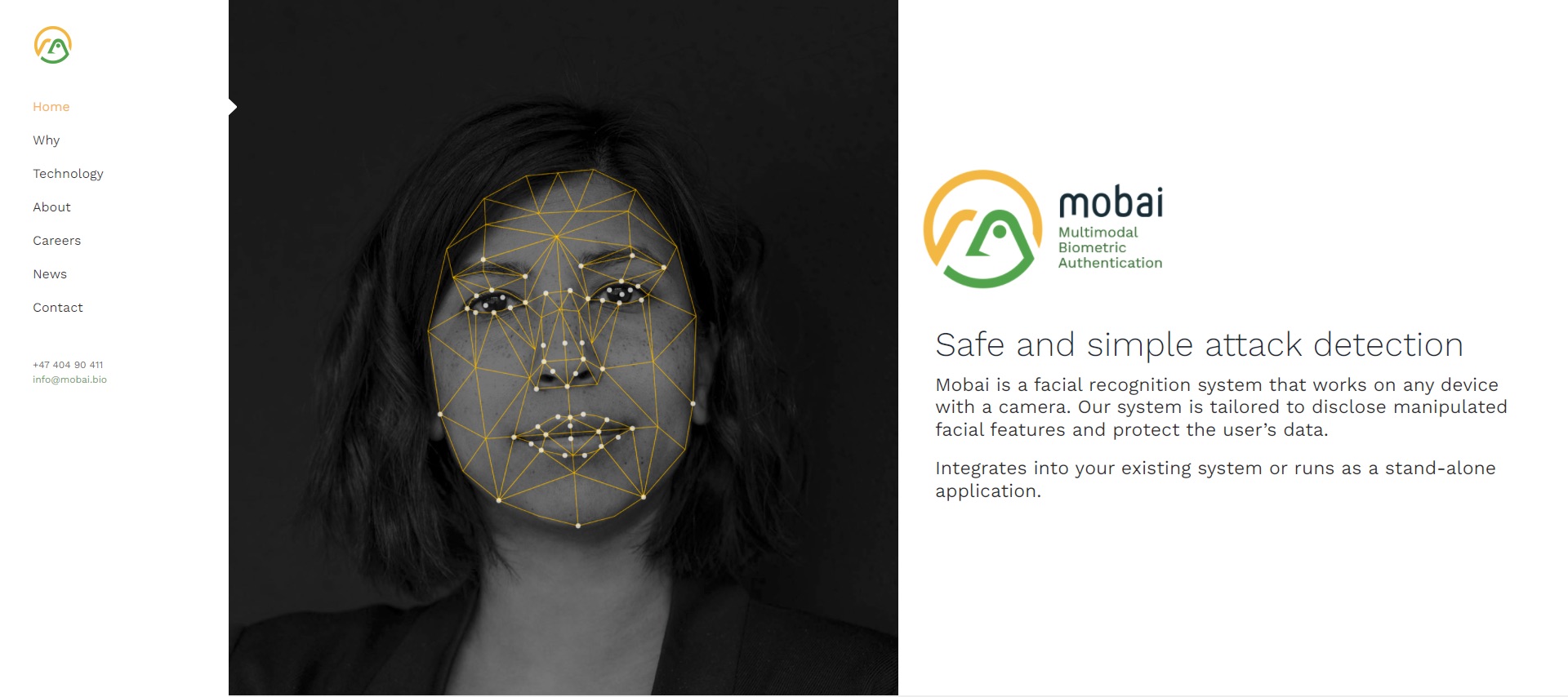

Norway-based biometric startup Mobaiwon $3.16 million (EUR 2.8 million) in funding to enhance the protection of personal biometric data in coalition with Vipps BankID, Sparebank1 Østlandet, KU Leuven, and NTNU. The project, named SALT for “Secure privacy preserving Authentication using faciaL biometrics to proTect your identity,” will bring new functionalities to Mobai’s facial recognition solution, and improve the quality of the technology to help firms meet eiDAS and AML regulations.

The project will drive innovation in the field of facial biometrics, particularly in the areas of biometric template protection, face quality assessment, and presentation attack detection. Mobai CEO Brage Strand noted in a statement that innovation in facial biometrics is especially urgent insofar as vulnerabilities in current authentication strategies such as passwords and even two-factor authentication increasingly have been exploited by fraudsters and cybercriminals.

“Our aim is to offer consumers a unique opportunity to prove who they are, as a way to combat the surge in phishing and identity theft we currently experience,” Strand said. He added the goal of the project was to move “beyond comparing a photo you store on a device with a selfie” to bring the same level of trust found in ePassports “into a digital domain.” Strand also emphasized the importance of leveraging “privacy-preserving technology” to ensure GDPR compliance and the integrity of personally identifiable information.

Mobai’s partners represent an interesting cross-section of the country’s financial services industry. Sparebank1 Østlandet is the fourth largest savings bank in Norway. Vipps is a payments and electronic ID provider with more than four million electronic ID users. NTNU is the Norwegian University of Science and Technology, the largest university in the country with more than 40,000 students; Mobai was spun out of NTNU’s Norwegian Biometrics Laboratory in 2019. Katholieke Universiteit Leuven is a research and educational institution, one of the oldest universities in Europe, with a reputation for pioneering scientific research.

“We see face recognition as a very promising and effective way to add an extra layer of security that will help combat identity theft, fraud, and money laundering,” Sparebank1 Østlandet EVP for Innovation and Business Development Dag Arne Hoberg said. “Imagine a situation where you may actually sign a mortgage electronically and use a ‘selfie’ as part of this process to confirm that your are the right person to sign.”

Meanwhile, in nearby Denmark, leading business automation software and services provider Visma announced its acquisition of expense management company Acubiz. Term of the transaction were not immediately available.

Visma will integrate Acubiz’s expense management solution into its Visma Enterprise HRM, but Acubiz will continue to function as an independent brand. The company, which has a 20% market share in Denmark and more than 200,000 users, offers solutions to help businesses better manage employee and travel expenses, as well as mileage reimbursement, invoice management, and time registration.

“I am excited to welcome another strong, Danish company into the Visma family,” Visma Enterprise A/S Managing Director Monika Juul Henriksen said. “There is no doubt that Acubiz is a perfect match not only businesswise but also in their culture and DNA. Acubiz wants to be the best – and so do we. Together, we will be even better.”

Founded in 1997 by Lars de Nully, Acubiz is based in Birkerød north of Copenhagen. This year, the company has forged partnerships with accounting firms Tal & Tanker and Tietotili, as well as with financial administration services provider Fiscales, HR software company Sympa, and Jutlander Bank.

In a year-end statement published on the Acubiz blog, the company noted that, in addition to its acquisition by Visma, it plans to unveil a new financial interface in 2022. The new UI will feature upgrades in performance, user-friendliness, and the ability to customize.

“By becoming a part of Visma, we do not only get a shortcut to new customers, markets, segments, and partners, we will also benefit from the knowledge and skills within legal, HR, marketing, and sales,” Acubiz Managing Director Henrik Malling said. “Being able to counsel with these experts is immensely valuable for us as a relatively small organization. So we honestly cannot wait to get started and to get to know all our new colleagues within Visma.”

FinovateEurope 2022 is right around the corner. If you are an innovative fintech company with new technology to show, then there’s no better time than now and no better forum than FinovateEurope. To learn more about how to demo your latest innovation at FinovateEurope 2022 in London, March 22-23, visit our FinovateEurope hub today!

Here is our look at fintech innovation around the world.

“Open banking empowers consumers and small businesses to use their financial data to expand access to financial services, such as demonstrating their financial wellness to increase access to credit, aggregating financial data to improve personal financial management, and to more seamlessly set up and manage payments,” Mastercard Chief Product Officer Craig Vosburg explained. “Together, we’ll continue to build up on our API connectivity and our multi-rail strategy to enable greater consumer access, control, and choice around the world.”

Aiia is the company known formerly as Nordic API Gateway, the leading open banking platform in Northern Europe. More than 40 financial institutions, as well as a number of enterprises, rely on the platform to integrate financial data and offer A2A (account-to-account) payments. Via a simple API, the solution supports a wide variety of payment services ranging from one-off, e-commerce payments to bulk payments for SMEs. The company demonstrated the technology at its Finovate debut at FinovateEurope earlier this year.

Founded in 2017, Aiia includes Danske Bank, OP Bank, Lunar, DNB, and Santander Consumer Bank among its partners. A licensed Payment Initiation Service Provider (PISP) and Account Information Service Provider (AISP), Aiia has raised more than $15 million (€13.5 million) in funding to date. This includes a $5 million investment from DNB and Danske Bank in April of last year.

“For the past decade, we have worked to build Aiia into a leading and quality-driven open banking platform, which has onboarded hundreds of banks and fintechs onto safe and secure open banking rails,” Aiia founder and CEO Rune Mai said when the acquisition news first broke in September. “We have worked closely alongside banks, customers, and local authorities to ensure that our APIs show the true effect of open banking. We’re excited to become a part of Mastercard and progress our journey of empowering people to bring their financial data and accounts into play – safely and transparently.”

Aiia is the latest fintech acquisition by Mastercard. The purchase comes a year after the completion of its acquisition of real-time financial data and insights company Finicity.

Three headlines in the cryptocurrency space this week show how seriously Big Tech, Big Fintech, and the world’s largest financial services companies are taking the rise of digital assets. And while each of the three companies listed below varies in the degree to which it is embracing our increasingly crypto-friendly future, their continued interest in the space suggests that the pace of adoption of digital assets – and the proliferation of use cases – is only likely to grow in the months and years to come.

The report is based largely on an interview that Apple CEO Tim Cook had with Aaron Ross Sorkin as part of the DealBook Online Summit sponsored by The New York Times. That said, those looking for a firm commitment from Apple in Cook’s conversation with Sorkin will be disappointed; while Cook expressed interest in cryptocurrencies from a “personal point of view … for awhile” and admitted that he believed that it was “reasonable to own (cryptocurrencies) as part of a diversified portfolio,” the idea of Apple accepting cryptocurrencies as payment for Apple products and services remains just that – an idea. Cook also expressed skepticism toward the notion of Apple investing in cryptocurrencies as part of a corporate investment strategy.

Apple’s relationship with cryptocurrencies has been cautious, to say the least. Back in 2014, Apple removed a number of Bitcoin wallets from its App Store, including one trading and storage app with 120,000 users, and another wallet app from Coinbase. More recently, there has been some softening of Apple’s stance, with Apple Pay VP Jennifer Bailey conceding the the company is “watching” the space and sees “interesting long-term potential” in digital currencies just a few years ago.

It’s worth noting that Apple’s reputation in technology is less as a first-mover and more that of a technology enhancer that often comes along and does a better job at innovations initiated by others. So the idea that Apple’s approach to embracing cryptocurrencies would be similarly slow-rolling is consistent with how the company has long operated. Nevertheless, Apple Pay’s fintech rivals – such as PayPal, Square, and Stripe – have been far more eager to pursue opportunities in crypto. Add to this the fact that Google Pay has teamed up with digital asset marketplace Bakkt in a deal that will enable users to spend Bakkt Card crypto funds directly from their Google Pay accounts. Together, it seems much more likely that a closer relationship between cryptocurrencies and Apple Pay is a question of “when” rather than “if.” As interest in digital currencies accelerate, and the solutions and services from these crypto-friendly fintechs become more widespread and even mainstream, it is hard to imagine Apple Pay remaining on the sidelines.

Revolut Takes Steps Toward Building a Cryptocurrency Exchange – The rumor that aspiring super app Revolut is looking to build a cryptocurrency exchange hinges largely on a job posting at LinkedIn. According to reports, Revolut wants to hire an individual with at least seven years experience in technology and in building order matching engines to lead a technical team to “architect and built Revolut Crypto Exchange.”

The crypto exchange would further establish Revolut as a leading player in the cryptocurrency space and potentially enable the company to diversify its services and create new cash flow, which could help Revolut establish another reliable revenue source going forward. The exchange news also follows reports that Revolut was looking into launching its own crypto token. And while Revolut has not commented on what it has referred to as a “mere rumor”, the report, first shared by Coindesk earlier this fall, does bolster the notion that Revolut is deepening its commitment to digital assets – a space the company has enjoined aggressively since introducing in-app cryptocurrency trading functionality in 2018.

In April of this year, Revolut added 11 new crypto tokens to its platform. The following month, the company launched its public beta for Bitcoin withdrawals. “I said before that 2021 would be the year of crypto and Revolut is here to deliver on that promise,” company Head of Crypto Edward Cooper announced in June when the company revealed that it would add Dogecoin to its current cryptocurrencies offerings for traders. “One of the most popular user requests over the past couple of months has been to add Dogecoin and we have answered the call!”

Revolut has more than 16 million customers around the world, and conducts more than 150 million transactions a month on its platform.

Mastercard Introduces Crypto-Linked Cards for the APAC Region – Also this week, Mastercard announced that it has secured partnerships with a trio of cryptocurrency companies – Amber, Bitkum, and Coinjar – who will issue crypto-funded Mastercard payment cards. The collaboration represents the first APAC-based cryptocurrency service providers (Amber and Bitkum are based in Thailand, Coinjar is headquartered in Australia) to join Mastercard’s Crypto Card Program, an initiative designed to enable companies to offer secure payment cards that meet regulatory requirements with regards to cryptocurrencies.

“Cryptocurrencies are many things to people – an investment, a disruptive technology, or a unique financial tool,” Mastercard EVP for Digital and Emerging Partnerships and New Payment Flows in the Asia Pacific region Rama Sridhar said. “As interest and attention surges from all quarters, their real-world applications are now emerging beyond the speculative. In collaboration with these partners that adhere to the same core principles that Mastercard does – that any digital currency must offer stability, regulatory compliance, and consumer protection – Mastercard is expanding what’s possible with cryptocurrencies to give people even greater choice and flexibility in how they pay.”

Mastercard’s APAC announcement comes on the heels of news that the company will enable the banks and merchants on its payment network to integrate cryptocurrency offerings into their products. The new arrangement comes courtesy of a partnership with Bakkt and will empower bitcoin wallet providers as well as issuers of credit and debit cards that offer rewards in crypto and enable digital assets to be spent. Also benefitting from Mastercard’s plan are those companies that offer loyalty programs that allow points from travel or hotel stays to be converted in to cryptocurrencies.

“Mastercard is committed to offering a wide range of payment solutions that deliver more choice, value, and impact every day,” Mastercard EVP for Digital Partnerships Sherri Haymond said. “Together with Bakkt and grounded by our principled approach to innovation, we’ll not only empower our partners to offer a dynamic mix of digital assets options, but also deliver differentiated and relevant consumer experiences.”