This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

May is Asian-American and Pacific Islander Heritage month. And with FinovateSpring less than a week away, we wanted to take a moment to celebrate the Asian-American fintech innovators who will be demonstrating their latest technologies on the Finovate stage live in San Francisco, California on May 21 through 23.

Tickets for FinovateSpring are still available. Visit our registration page today and save your spot. We look forward to seeing you in San Francisco!

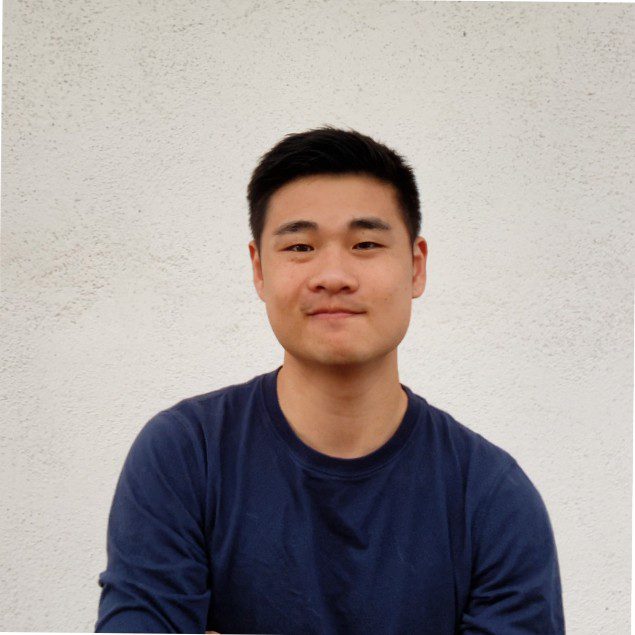

A former engineer at Dialpad, Dropbox, and Flexport, Ng is CEO and Co-Founder of Anvil. He is also a graduate of the University of Michigan and an alum of the Y Combinator Startup School Online.

Headquartered in San Francisco, California, Anvil was founded in 2018.

With experience in angel investments at 79 Studios, as a venture partner at Resolute, and a former I-banker at Chanin & CSFB, Saujin Yi is founder and CEO of LiquidTrust. Yi is a graduate of MIT and earned her MBA from UCLA Anderson, where she is a lecturer.

LiquidTrust was founded in 2019. The company is headquartered in Los Angeles, California.

A Venture Partner at JAZZ, Lin seeks to make everyone become “bionic” when it comes to investment research and analysis. Founder and CEO of Revelata, Lin is a graduate of Harvard University, earning his A.B. in Biochemical Sciences, as well as his S.M. and Ph.D. in Computer Science, at the institution.

Headquartered in Palo Alto, California, Revelata was founded in 2020.

Former Head of Operations for Juno Finance and Ownit, Chao is Co-Founder and Chief Operating Officer with Tennis Finance. Chao earned a B.A. in Economics and Psychology at University of California, Los Angeles.

San Francisco, California-based Tennis Finance was founded in 2022.

The stage is not the only place where Finovate celebrates the accomplishments of Black and African-American fintech and financial services professionals.

Since inception, Greg Palmer and the Finovate Podcast have showcased Black and African-American innovators, entrepreneurs, and thought leaders in the fintech and financial services space.

As part of our continued commemoration of Black and African-American History Month, today we highlight those conversations. Click the image to access the interview.

Nneka Ukpai – Better

Nate Gibbons – QuickFi

Jacqueline Baker – Author, The Unexpected Leader

Joseph Akintolayo – Deposits

Ariam Sium – FinGoal

William Crowder – Aperture Venture Capital

Sesie Bonsi – Bleu

Sharon Kimathi – Fintech Futures

Adrienne Harris – Superintendent NYS Department of Financial Services

To kick off Finovate’s commemoration of Black/African-American History Month this year, we’re highlighting some of the Black and African-American fintech professionals who represented their companies and their fintech innovations at our Finovate conferences in 2023.

Andre Llewellyn – Marketing Consultant/Advisory Board Member with AI Squared

Along with company CTO Michelle Bonat, Andre Llewellyn helped demonstrated the new Generative AI-based features on AI Squared’s platform at FinovateFall last year.

The company’s technology enables financial services companies to leverage Generative AI – and their own data – to maximize their enterprise assets.

A marketing consultant and AI Squared Advisory Board member, Llewellyn is a marketing veteran whose insights helped fuel new product and brand launches for Procter & Gamble, Instagram, Hashflow, and Candy Digital. He is a graduate of the NYU Stern School of Business.

Michael Duncan’s Bankjoy made its first Finovate appearance in 2016.

The company, which returned to the Finovate stage in 2022 and 2023 for FinovateFall, helps community banks and credit unions access modern banking technology. Bankjoy’s solutions help FIs better target specific market niches and deliver superior digital banking experiences.

Duncan (CEO) co-founded Bankjoy in 2015. Headquartered in Royal Oak, Michigan, Bankjoy has more than 60 clients, more than 120 integrations, and serves more than 1 million customers and members of banks and credit unions. This week, the company announced a new partner – Oregon State Credit Union – that will deploy Bankjoy’s online account opening and loan application.

Mountain View, California-based DataVisor made its Finovate debut last year at FinovateFall 2023.

Solutions Engineer Ryan Nichols (shown) joined company CRO Kevin McWey on stage as they demoed DataVisor’s Fraud & Risk Platform. The company’s solution supports the entire fraud workflow in a self-service solution that is single and flexible.

A software developer and solutions architect with experience at firms like CenturyLink and Internet publisher Giant Oak, Nichols joined DataVisor in 2021. As of the spring of 2023, he is both a Cryptocurrency Tracing Certified Examiner (CTCE) and a Certified Cryptocurrency Risk Specialist (CCRS).

Nate Gibbons – Chief Experience Officer with QuickFi

Nate Gibbons, QuickFi’s Chief Experience Officer, is no stranger to Finovate audience – nor to the Finovate Best of Show awards.

The company, an innovator in embedded financing for business equipment, has won Best of Show on two occasions: FinovateSpring 2022 and 2023. And Gibbons was part of the winning team both times (along with colleague Jillian Munson, VP of Process & Automation with QuickFi).

An alum of the University of Rochester Simon Business School, Gibbons is also a Certified Lease and Finance Professional (CLFP). Previous to his tenure at QuickFi, he was Project Manager and subsequently Vice President at First American Equipment Finance.

The company is an Equity, Diversity, & Inclusion firm that consists of The Urban Labs (services) and Lexicon (products). The Lazu Group made its Finovate debut last year at FinovateSpring, demoing its CULTURL Heritage Calendar that offers “content, ideas, and resources for creating timely communication to promote empathy and curiosity and encourage cross-cultural dialogue.”

Lazu is a speaker, a lecturer at the Massachusetts Institute of Technology, and an author. Her book, From Intention to Impact: A Practical Guide to Diversity, Equity, and Inclusion, was published this year. Lazu is also a former banking professional, having worked as EVP and Chief Experience and Culture Officer for Berkshire Bank in Boston.

ModernTax founder and CEO Matthew Parker introduced his company to Finovate audiences last year at FinovateSpring. ModernTax is a data company that makes tax and financial data on non-public entities more accessible. The company has created a verification platform that includes more than seven million businesses, and ModernTax has validated tax records for “hundreds of thousands” of them.

Before launching ModernTax, Parker was co-founder and CEO of Rapidly.co, a SaaS platform that connects accountants, enrolled agents, and tax professionals to their clients online. We caught up with him last fall to talk about the founding of ModernTax and what it means to have a more transparent financial ecosystem.

FinGoal first introduced itself to Finovate audiences at FinovateFall in 2021. But it was the company’s return to the Finovate stage the following spring that earned the Colorado-based fintech its first Best of Show award.

Led by Ariam Sium, VP of Product (shown) and Jenn Underwood, Product Analyst, FinGoal’s demo of its Aggregator Switch Kit showed how developers can readily transition from their current data aggregator to access the most enriched and reliable data available.

Finovate VP and host of the Finovate podcast Greg Palmer sat down with Sium in the wake of FinGoal’s Best of Show win last year. Check out their conversation from last summer.

AI Squared made its Finovate debut at FinovateSpring 2023. The company, founded in 2019 and headquartered in Washington, D.C., specializes in helping companies integrate AI and machine learning functionality into any web-based application. Leading the company’s demo was founder and CEO Benjamin Harvey.

With a Master’s degree and a Doctor of Science in Computer Science – as well as years spent as both a Research and Assistant Professor – Harvey brings a wealth of academic experience to the challenge of entrepreneurship and innovation in the fintech space.

We discussed this, and other aspects of his background and goals, in a Finovate blog interview back in August of last year.

To celebrate National Hispanic Heritage Month, we wanted to recognize some of the contributions Hispanic entrepreneurs have made in the fintech industry. From the start, Hispanic professionals have played a pivotal role in shaping fintech by using their creativity and unique perspective to build and improve solutions that truly make a difference for both retail and commercial users.

Below is a selection of Hispanic-founded fintech companies that continue to make a transformative impact in the worlds of banking and fintech. Join us in celebrating diversity, inclusion, and the achievements from these individuals during this month of recognition and reflection. Please note that this is simply a conversation starter and is not an all-inclusive list of Hispanic-founded fintechs.

Securitize

Securitize enables digital securities, which are easier to own, simpler to manage, and faster to trade. Founders: Carlos Domingo, Jamie H. Finn, Shay Finkelstein, and Tal Elyashiv

Payjoy

PayJoy is a consumer financing company that allows consumers to buy a smartphone on credit and pay it off in installments. Founders: Doug Ricket, Gib Lopez, Mark Heynen, and Tom Ricket

Finix

Finix develops a payment processing platform for businesses. Founders: Richie Serna and Sean Donovan

Petal

Petal offers three Visa credit card products for underserved consumers. Founders: Andrew Endicott, David Ehrich, Jack Arenas, and Jason Rosen

Flywire

Flywire is a global payments enablement and software company that simplifies complex payments for its clients and their customers. Founder: Iker Marcaide

Octane

Octane offers access to instant financing to fuel their customers lifestyles. Founders: Andre Gregori, Jason Guss, Mark Davidson, Mark Garro, and Michael Fanfant

Origin

Origin is a financial planning platform that manages compensation, benefits, and personal finances for employees. Founders: João de Paula and Matt Watson

Oportun

Oportun is a digital banking platform that puts its 1.9 million members’ financial goals within reach. Founders: Gabriel Manjarrez and James Gutierrez

Brex

Brex is a global spend platform with corporate cards, expense management, reimbursements, and billpay. Founders: Henrique Dubugras and Pedro Franceschi

Camino Financial

Camino Financial is an online finance company that offers business loans and wealth-building solutions to help small businesses grow. Founders: Kenneth Salas and Sean Salas

Ontop

Ontop offers streamlined payroll, onboarding, and smooth payments for international teams. Founders: Julian Torres and Santiago Aparicio

Papaya

Papaya develops technology designed to simplify bill payment for consumers. Founders: Jason Meltzer and Patrick Kann

Snowball Wealth

Snowball Wealth offers a mobile app designed to help users tackle debt and build generational wealth. Founders: Pamela Martinez, Pearl Chan, and Tanya Menendez

Paystand

Paystand is a cloud-based billing and payment platform for B2B companies. Founders: Jeremy Almond and Scott Campbell

Listo

Listo offers insurance and loans via retail and mobile experiences. Founders: Alan Chiu and Sam Ulloa

Ripio

Ripio is a bitcoin and digital payments company that provides electronic payment solutions for businesses in Latin America. Founders: Luciana Gruszeczka, Mugur Marculescu, and Sebastian Serrano

InvestCloud

InvestCloud is a global company specializing in digital platforms that enable the development of financial solutions. Founders: Colin Close, John Wise, Julian Bowden, Michael A. Smith, Vincent Sos, and Yaela Shamberg

Novel Capital

Novel Capital provides revenue-based financing to B2B companies. Founders: Carlos Antequera and Keith Harrington

Flow

Flow offers an open architecture that connects investment managers with their limited partners and service providers. Founders: Adrian Ortiz, Brendan Marshall

Milo

Milo is reimagining the way crypto and global consumers access credit and financial solutions. Founder: Josip Rupena

Traive

Traive is a lending platform that connects lenders to farmers to provide financial products and services for the agricultural supply chain. Founders: Aline Pezente and Fabricio Pezente

Finally

Finally helps small and medium-sized businesses automate their accounting and finances. Founders: Edwin Mejia, Felix Rodriguez, and Glennys Rodriguez

Alvva

Alvva offers credit-building loans to pay for immigration expenses. Founders: Jorge Gonzalez and Sergio Torres

Portabl

Portabl offers identity-powered user experiences via a single API. Founder: Nate Soffio

Onyx Private

Onyx offers a modern private bank for the new generation. Founders: Douglas Lopes, Tiago Passinato, and Victor Santos

SMBX

SMBX is a funding portal and public marketplace for issuing and buying U.S. small business bonds. Founders: Benjamin James Lozano, Bhavish Balhotra, Gabrielle Katsnelson, and Jackie Chan

Zoe Financial

Zoe Financial helps its clients find and hire their ideal financial advisor. Founder: Andres Garcia Amaya

OKY

OKY is building technologies that help immigrants to improve their lives by connecting families and sending value home efficiently. Founders: Alejandro Miron, Estuardo Figueroa, Santiago Rossi, and Victor Unda

Caplight

Caplight is a platform that enables institutional investors to buy and sell derivatives of private equity. Founders: Javier Avalos, Justin Moore

Aeropay

Aeropay enables businesses to accept compliant, digital payments. Founder: Daniel Muller

Flourish FI

Flourish FI is a financial wellness and engagement platform for financial institutions. Founders: Jessica Eting, Pedro Moura

Capchase

Capchase provides financial solutions to startups by allowing access to funds as they grow. Founders: Ignacio Moreno Pubul, Luis Basagoiti Marqués, Miguel Fernandez, and Przemek Gotfryd

Chargezoom

Chargezoom is a B2B integrated payments platform. Founders: Matt Dubois and Miguel Avellan

Chipper

Chipper is a student loan app that helps users lower payments, qualify for forgiveness, and chip away debt faster. Founder: Tony Aguilar

Ease

Ease is a corporate card and practice operations software for private practices. Founders: Mario Amaro and Miles Montes

How can greater transparency in financial services help improve underwriting, lower risks, and create more opportunities for banks and small businesses alike?

We caught up with Matthew Parker, founder and CEO of ModernTax, to discuss how bringing more transparency to areas of finance like taxation can help credit providers make better decisions.

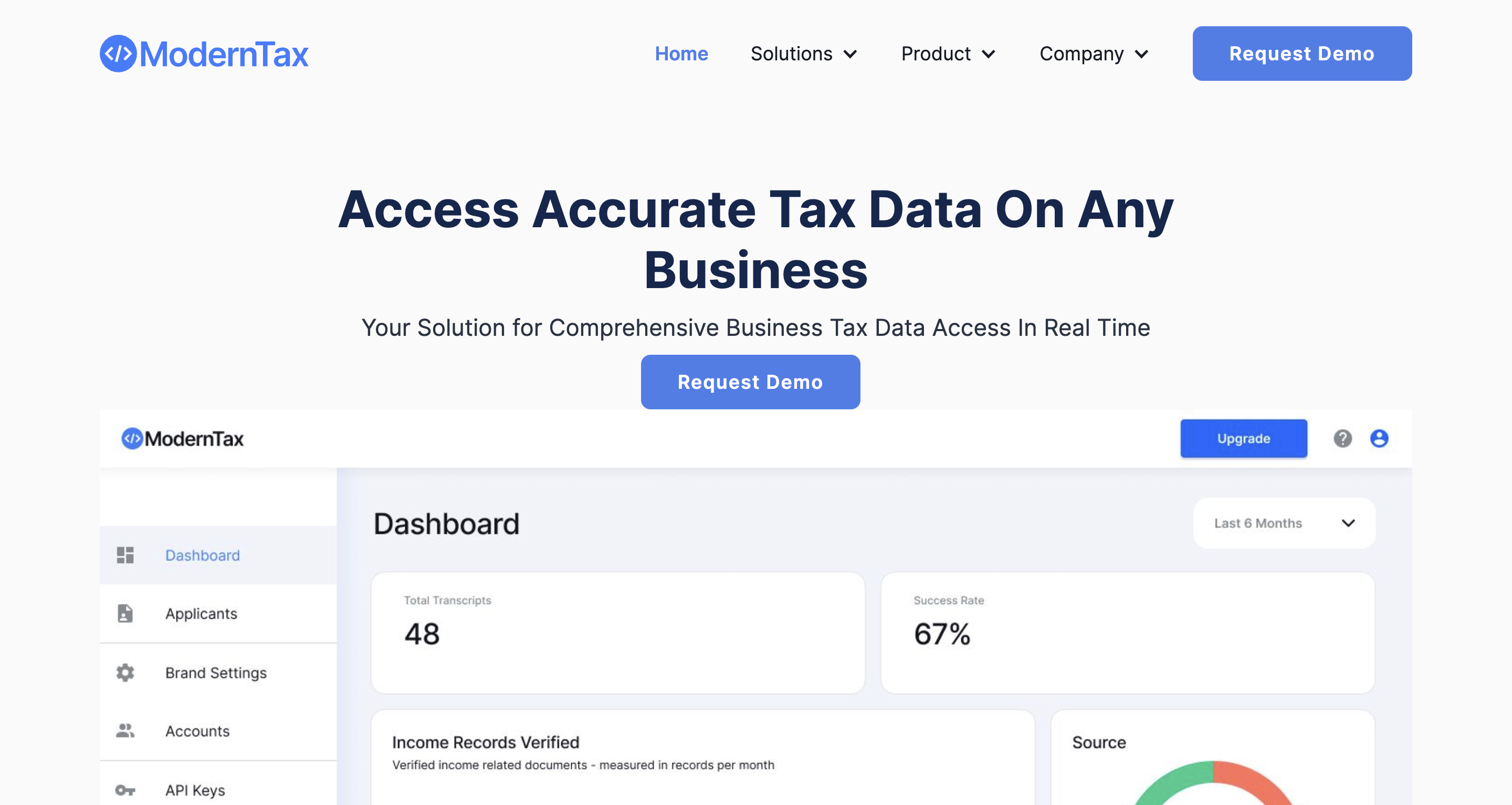

Founded in 2021 and headquartered in San Francisco, California, ModernTax made its Finovate debut earlier this year at FinovateSpring. At the conference, the company demoed its Business Verification Platform and Verifier API, a secure solution that enables fintechs and banks to verify tax records, business standing and KYC data.

Last month, ModernTax launched its Live Contributory Network for on-demand tax verification. The solution connects licensed tax professionals with ModernTax customers to provide on-demand, secure, and reliable tax verification services.

To start off, what is it about taxes that interests you? Of all the areas of finance, what’s special about taxes?

Matthew Parker: My first job out of college was in social services, specifically working in child support. My responsibilities included calculating the combined income of two people with misaligned incentives. This experience opened my eyes to how broken the world of tax, income, and finance can be at the ground level.

A few years later, I worked in consulting, helping banks understand what went wrong with the mortgage crisis. I then stumbled into my first entrepreneurial endeavor: a franchise tax preparation company. Over three years, I grew from one office to five and learned the ins and outs of the tax preparation business.

In 2017, I caught the technology bug and bought a one-way flight to San Francisco with the goal of starting a tax startup that utilized all of the tax data I had been accessing through my tax preparation business as alternative data to underwrite loans.

Six years later, I am building ModernTax to make use of this data to help underwrite, decrease risk, and create a more transparent financial ecosystem for U.S.-based small businesses.

Can you elaborate on that?

Parker: One thing that has consistently bothered me is the black box of tax information that lives outside of our bank feeds and accounting feeds. There is an entire business that helps accountants export accounting data into tax software (they are a customer), but that is a niche market.

The real problem we are solving is financial transparency. Many businesses that provide financial services are locked out of access to critical financial records, and 99% of U.S. businesses are not required to report any financials. This results in a massive transparency gap. Tax records are one way to fill this gap, with 15 million unique entities and 160 million individual tax returns filed annually in the U.S. alone.

How does ModernTax solve this problem better than other companies, or other solutions?

Parker: ModernTax aims to solve the problem of financial transparency by providing tax information on all U.S. small businesses, which can level the playing field and create a more transparent financial ecosystem. The commercial credit market in the U.S. alone is worth $8.8 trillion annually, and the average company in this industry generates approximately $7 billion in yearly revenue.

By utilizing tax records, which are filed by 15 million unique entities and 160 million individuals annually in the U.S. alone, ModernTax’s strategy revolves around transparency and eliminates the need for countless hours of back-and-forth communication and manual data entry to collect this information, saving commercial providers time and money, and making it easier to evaluate businesses.

What is your primary market? What has the response to your technology been like?

Parker: We primarily sell to commercial credit providers such as banks, online lenders, and other data providers that assist companies in underwriting, fraud prevention, and verifying financial documents for their customers.

We have received positive responses from data providers such as D&B, Experian, and Transunion, as well as from our first paying partner, Enigma Technologies. Moreover, ModernTax has been well-received by direct carrier insurance companies for both underwriting and claims processing on income-related products.

Are there any deployments or features of your technology that are especially noteworthy?

Parker: In the past month, we have added 14 new features. One notable observation is the need for a robust platform that allows our contributors to efficiently provide us with data. Unfortunately, the IRS does not provide adequate tools to help companies maintain transparency in their reporting. We are constantly learning from our contributors on how we can build tools to address this issue.

ModernTax is headquartered in San Francisco and was founded in 2021. What is it like to be a young startup in San Francisco today?

Parker: Personally, it feels surreal to me. I moved to San Francisco in 2017, lived through the pandemic, and experienced the boom of 2021 and the correction of 2022. Nevertheless, San Francisco is resilient. Although there are political and socioeconomic problems that come with being a high-stakes, high- reward city, founders can arrive here with nothing and become paper billionaires and liquid millionaires faster than anywhere else in the world.

This creates a tale of two cities. To be a young startup, you have a ton of resources right in your backyard, but you also realize how competitive it is. There was a new billion-dollar company born every day for a certain amount of time and now, with AI, we are seeing history repeat itself. It’s important to keep your momentum but also not get too distracted.

We also wanted to talk with you as a Black founder and entrepreneur. What advice would you give to other potential founders-of-color?

Parker: Starting a company is hard, full stop. I even joke with my wife that I don’t mind telling my 18-month-old son “no” a lot because it’s just the nature of life in general. As a black founder, I have experienced both ups and downs. George Floyd’s murder created a domino effect of predominantly white people at large institutions feeling guilty, which led to a lot of initiatives that were half-baked and more PR moves than anything. That sentiment wore off pretty quickly, especially as markets turned for the worst in 2022.

If you built your brand “how hard it is to be a black founder”, you are likely bitter right now because we learned that the market didn’t care about you being black or about what happened with George Floyd. We are now seeing pushback with the rollback of affirmative action, the lawsuit impacting Fearless Fund, and I think more challenges will come. So, I would say focus on your business, focus on your customers, and build products. If you play the victim in a game that is already hard, you decrease your chances of winning.

You demoed your technology at FinovateSpring earlier this year. What was that experience like for you and your team?

Parker: This demo helped us think about how our product helps financial institutions and we were able to demonstrate the capabilities that companies can experience by getting access to this information in real-time.

What are your goals for ModernTax? What can we expect from the company over the balance of 2023 and into next year?

Parker: ModernTax aims to provide near-instant access to verified tax and financial information through a network of licensed tax agents to create a more transparent verification process for their customers. Over the balance of 2023 and into next year, the company plans to add eight new customers, launch new features for its contributor portal and business user features, and attend various business development events and in-person client meetings.

Will 2023 be known as the year AI came of age? With the advent of Generative AI and tools like ChatGPT, the technology world got an unexpected boost this year as interest in the potential for artificial intelligence soared.

What does the surge in interest and activity in AI mean for financial services? How can fintechs leverage the technology to help banks, credit unions, and other financial services organizations and institutions better serve their customers with more choice, more security, and more efficiency?

We caught up with Dr. Benjamin Harvey, founder and CEO of AI Squared. Headquartered in Washington, D.C., AI Squared made its Finovate debut earlier this year at FinovateSpring and will return to the Finovate stage next month for FinovateFall. The company specializes in integrating artificial intelligence and machine learning into existing apps. We discussed the rise of AI, the impact AI might have on financial services, and the work of AI Squared in helping businesses take advantage of the emerging technology.

We also talked about the challenges Harvey has faced as an African American entrepreneur and founder in the technology industry. As we commemorate Black Business Month here in August, we are also happy to share his insights and advice on what African American founders and entrepreneurs need to keep in mind when starting out.

Let’s start with a big picture question: what is overhyped about AI, what’s underhyped, and what are we getting right?

Benjamin Harvey: There’s a lot of hype around AI, and some of it is warranted, but not all. One of the most overhyped ideas is that AI will replace humans in the workforce on a large scale. While AI can automate certain tasks, it can’t replicate the creativity, empathy, and critical thinking that humans bring to the table. On the flip side, what’s underhyped is the potential for AI to be simple while being useful. Many AI products have incredible potential but are too complicated for widespread adoption. Simplifying AI and making it more accessible can unlock its true potential and bring about transformative change across industries.

What most observers and commentators are getting right about AI is that it’s here to stay. AI is not just a passing trend; it’s a technological revolution that’s reshaping the way we live and work.

Now let’s turn to your company. What problem does AI Squared solve and who does it solve it for?

Harvey: AI Squared is a platform designed for product owners, data scientists, and enterprise leaders. We empower users to accelerate both predictive and generative AI projects, measure their benefits, and drive significant revenue growth and cost reduction. Our solution is industry-agnostic and loved by our users.

We address a critical issue in the AI industry: 90% of AI and ML models never make it into production or use, largely due to the time and cost involved. AI Squared tackles this problem head-on, reducing the time to production and use of AI and ML models from an average of 8 months to 8 hours or less. We provide a secure environment for accelerating AI projects, enabling users to measure benefits, use no/low code solutions, and deliver trustworthy AI results. By streamlining the AI deployment process, we help organizations harness their data to drive game-changing AI capabilities, driving innovation and growth.

How does AI Squared solve this problem better than other companies, other solutions?

Harvey: We understand that the key to successful AI adoption is seamless integration into existing workflows. Our solution is designed to fit effortlessly into the applications that our customers already use on a daily basis. By embedding AI capabilities directly into these familiar tools, we eliminate the need for users to switch between different platforms, thereby reducing friction and increasing efficiency. This approach not only enhances the user experience, but also drives greater AI adoption across the organization. Our technology is versatile and accessible, making it a valuable asset for teams at all levels, from operational staff to executive leadership. The result is a more informed, agile, and productive organization that can leverage AI to its full potential.

What is your primary market? What has their response to your technology been like?

Harvey: Our primary market is financial services and the response has been overwhelmingly positive! Financial services organizations are constantly seeking ways to improve efficiency, reduce costs, and enhance customer experiences. And our platform has been proven to address these needs by accelerating the deployment of AI and ML models, making it easier for these organizations to harness the power of their data.

When clients see how we can reduce AI implementation from 8 months to 8 hours they’re blown away. We’re proud to say that we’ve turned our clients into our biggest champions. The value we provide goes beyond just the technology; it’s about the tangible benefits that our platform brings to their operations. They appreciate the speed at which they can now bring AI projects to fruition, the ease of integration with their existing systems, and the measurable ROI that our platform delivers.

Are there any deployments or features of your technology that are especially noteworthy?

Harvey: First and foremost, we prioritize data security and privacy. Unlike many other AI platforms, we don’t store or copy our customers’ data. This is a crucial differentiator, especially for organizations in highly regulated industries like financial services, where data privacy and security are paramount.

We offer flexible deployment options to suit the specific needs of our customers. Our on-premises deployment ensures that all data remains within the customer’s own infrastructure, providing an added layer of security. For those who prefer a cloud-based solution, we offer a multi-tenant deployment that still maintains robust data privacy and security measures.

One of our standout features is our Human-in-the-Loop (HITL) capability. This feature allows human verification and corrections to be made to the data generated by Generative AI before it’s used in critical business applications. This ensures a high level of accuracy and reliability in the data, which is essential for making informed business decisions. Our HITL feature is particularly valuable for organizations that need to ensure the utmost accuracy in their AI-generated data, such as those in the financial services sector where even small errors can have significant consequences.

You and many of your team have significant backgrounds in academia and the government. How has the transition into a more entrepreneurial space been?

Harvey: The transition from academia and government to the entrepreneurial space has been both challenging and rewarding. Initially, it was a bit of a culture shock to shift from a focus on the technical aspects of AI to a more value-driven approach. In academia and government, the emphasis is often on the theoretical and technical aspects of AI, whereas in the entrepreneurial space, the focus is on delivering tangible value to customers.

But once we got past the initial adjustment, we found that our diverse backgrounds gave us a unique perspective and a competitive edge. While our experience in academia has equipped us with a deep understanding of the technical intricacies of AI, our government experience has given us insights into the importance of security and compliance, especially when dealing with sensitive data.

We’ve been able to leverage these insights to develop a platform that not only delivers powerful AI capabilities but also addresses the specific pain points and challenges faced by our customers. Our approach is rooted in a deep understanding of both the technical and practical aspects of AI, and we’re able to offer solutions that are tailored to the unique needs of each customer.

Left to right: AI Squared’s Benjamin Harvey, Alvin McClerkin (COO), and Michelle Bonat (CTO) at FinovateSpring.

We also want to showcase AI Squared as part of our Black Business Month commemoration. What challenges have you faced as a Black founder and entrepreneur? What advice would you give?

Harvey: Launching a company as a Black entrepreneur, particularly in the AI/technology space, comes with its own unique set of challenges. One of the most significant hurdles is the lack of resources and representation in the industry. As a Black founder, I often found myself navigating uncharted territory without the benefit of a robust network or role models to look up to. However, I believe that these challenges can be overcome with determination, persistence, and a strong support system.

My advice to aspiring Black tech founders is to build a solid network of mentors, advisors, and peers who can provide guidance and support along the way. Don’t be discouraged by setbacks or rejections; instead, use them as learning opportunities to refine your approach and strategy. Do your homework, stay informed about industry trends, and be prepared to articulate the value proposition of your technology clearly and convincingly. Most importantly, reach out to other Black founders and executives who have walked the path before you. Their insights and experiences can be invaluable as you navigate the complexities of the tech startup ecosystem.

Remember, you are not alone in this journey. There is a growing community of Black tech founders and professionals who are eager to support and uplift each other. By working together, we can break down barriers, create more inclusive opportunities, and pave the way for future generations of Black tech entrepreneurs.

Speaking of African-Americans, AI Squared is headquartered in Washington, D.C. What is the technology scene like there?

Harvey: D.C. is a hotbed of tech innovation, especially in security and intelligence. Being close to the Federal Government and defense agencies, we’re in a unique spot to work on projects that matter for national security. It’s a vibrant scene here, with big tech firms, cool startups, and research hubs all mixing it up. We’re a tight-knit community, always meeting up, sharing ideas, and pushing each other to innovate.

The best part is that if your tech is good enough for national security, it’s good enough for anything. We’re talking finance, healthcare, consumer goods – you name it. Being in D.C. gives us the credibility to branch out into these sectors. It’s an exciting place to be, and we’re happy to be part of it.

You demoed your technology at FinovateSpring earlier this year. What was that experience like for you?

Harvey: The experience of demoing our technology at FinovateSpring was exciting and valuable for us. It provided us with a unique platform to showcase our product to a large audience of stakeholders, and to connect with key decision-makers in the financial services industry. We got valuable feedback on our product.

But the demo wasn’t without its challenges. Some technical difficulties with signing in and that, combined with the strict time constraints of the event, impacted our demo. These are things that tend to happen when demo-ing in a new forum. But it’s in our DNA to adapt and we did – and received positive feedback from attendees and made valuable connections that have since led to fruitful discussions. Overall, the experience was a great opportunity for us to showcase our technology, connect with industry leaders, and learn from the challenges we faced.

What can we expect from AI Squared over the balance of 2023 and into next year?

Harvey: Our primary goal for AI Squared is to continue delivering exceptional value to our customers, with a focus on the financial services sector. We’re committed to optimizing our product to enhance the customer experience and build strong, lasting relationships. As we approach the end of 2023, we are on track to exceed our internal goals, thanks to the dedication of our team.

Looking ahead to next year, we have ambitious plans for growth. We’re preparing to raise our next round of funding with a strategic team of investors who share our vision. This funding will enable us to continue providing world-class service and products. We’re also planning to expand our product offerings and explore new markets. We are excited about the opportunities that lie ahead and look forward to sharing our progress with you!

Disability Pride Month is coming to a close. The annual July commemoration is an opportunity to honor the experience and achievement of those in the disability community. The month of July is special because President George H.W. Bush signed the Americans with Disabilities Act into law on July 26, 1990. The landmark legislation was the first comprehensive law enshrining the civil rights of people with disabilities.

Today we take a look at just a handful of ways financial technology and the financial services community is helping support people with disabilities, whether those challenges are physical or cognitive, transitive or enduring.

There are some who bristle at the euphemism “differently abled.” But the idea of leveraging one ability to make up for another is at the heart of inclusion when it comes to people with disabilities. This is true when we are talking about technologies that enhance the power of hearing or touch for those with visual challenges. It is also true when we talk about a digital banking world that ultimately makes banking services more accessible to all – including those who cannot easily travel.

At the same time, greater awareness of the challenges faced by those with physical and cognitive challenges also means understanding the limits of technology. A pilot project in 2010 that explored disability inclusion in microfinancing institutions in Africa produced what one observer called “several clear conclusions from this pilot worth repeating because they are likely to have near universal application for MFIs entering this market.” The recommendations?

Don’t develop special credit products. Don’t give special conditions. Don’t get disappointed too soon. Identity existing clients with disabilities. Learn from them and use them in promotional efforts and in reaching out to new clients. Join efforts with local disability organization. Improve the physical accessibility of the premises.

A sizable number of government organizations and non-profit entities exist to help support people with disabilities secure employment, housing opportunities, as well as economic and health benefits. In many instances, non-profits have benefited from partnerships with financial institutions. This includes the partnership between JP Morgan Chase and the National Disability Institute. The bank, for example, is backing the NDI’s effort to inform and educate low- and moderate-income individuals with disabilities about the resources available to them under the Community Reinvestment Act (CRA).

The partnership between NDI and JP Morgan has produced some interesting insights into the challenges of small business owners with disabilities, as well. The report, Small Business Ownership by People with Disabilities: Challenges and Opportunities, makes a number of important points – foremost among them that entrepreneurialism is often a major employment choice for people with disabilities. The reasons for this vary from preferring a more flexible work schedule to previous experiences with discrimination or a hostile work environment to a lack of advancement opportunities. Importantly for people in financial services and fintech, the report noted that smaller, disability-owned businesses often avoid traditional financial channels and struggle to secure financing.

The causes for this aversion include concerns about using personal assets as collateral, a lack of assets, or benefit-related issues – such as a fear of losing social security benefits if their countable assets climb too high. Helpfully, the report provides a number of recommendations to help banks and fintechs better serve disability-owned businesses. These suggestions include greater investment in CRA funds for small businesses to more support of policies that would boost business opportunities, access to capital, and better coordinate of public resources.

Sometimes helping people with disabilities means helping people who help those with disabilities. According to data from co-parenting solution provider SupportPay, 38 million people are taking care of loved ones in 2023. To this end we share news that SupportPay has unveiled a new app designed to make it easier for caretakers to share, manage, and track expenses. The solution also enables caretakers to coordinate schedules and streamline communication. It is expected to be available in the fall of 2023.

Sheri Atwood, SupportPay founder and CEO, highlighted the fintech component of the new offering compared to other solutions on the market. “While several caregiver solutions are entering the market, none are focused on reducing the stress of managing expenses between multiple caregivers,” Atwood explained. “Our solution is built to solve this pain point by simplifying and streamlining this process.”

More than 65,000 parents are using SupportPay to manage more than $450 million in expenses and payments. In addition to helping caregivers share, organize, and track expenses and schedules, the new offering also helps caregivers review and resolve disputes as well as maintain certified records of expenses and payment histories. These can be especially helpful for tax purposes or addressing legal issues that arise.

“We knew our platform could be of assistance to all family members, including the staggering number of caregivers,” Atwood said. “From our co-parenting solution, we know that when people share financial responsibilities – whether it’s with an ex, a sibling, or another family member – the process can be much more time-consuming, conflict-ridden, and stressful.”

Founded in 2018, SupportPay is headquartered in Charlotte, North Carolina. The company has raised $6.8 million in funding. SupportPay’s investors include LAUNCH and The Syndicate.

What are the biggest challenges, concerns, and factors that impact LGBTQ financial consumers in 2023?

A wide-ranging survey by the Center for American Progress (CAP) from the beginning of the year actually sheds some light on the relationship between financial services themselves and the LGBTQ community. This knowledge can help guide banks, fintechs, and financial services providers better tailor their products, services, and experiences for a more diverse customer base.

Here’s one interesting example. The LGBTQ respondents tended to have higher employment rates compared to the non-LGBTQ respondents. At the same time, members of the LGBTQ community were more likely than members of the non-LGBTQ community to be engaged in part-time, freelance, or gig economy work. In the latter category, LGBTQ respondents outnumbered non-LGBTQ respondents 5% to 1%. With regard to transgender respondents, they were twice as likely as non-transgender respondents to report working part time.

These survey results have significant implications for financial services companies. Among other things, the responses underscore the importance of mobile and remote access to financial services. This includes features like virtual assistants to ensure 24/7/365 service for workers with atypical or irregular working hours. Offerings like Earned Wage Access can help workers smooth out irregular cash flows for part-time workers. Additionally, LGBTQ respondents to the CAP survey reported incomes that were on average lower than those of non-LGBTQ respondents. Providing cash flow services can be a way of helping this community avoid the temptation of more costly and potentially predatory financing options.

These responses also suggest a new approach for financing and lending services companies. In order to compete, they may need to think differently about creditworthy potential borrowers who don’t have traditional employment histories. The trend toward an embrace of alternative data in credit scoring is a good development, and one that is likely to benefit LGBTQ communities. The same is true about initiatives to deal with the challenge of bias in AI.

Both as workers in the financial services industry and consumers of financial services, members of the LGBTQ community suffer from discrimination and harassment. This can range from verbal harassment to the denial of equal access to services. While many companies in the financial services industry have been commended for their LGBTQ-friendly policies and environments, ensuring that the financial services workplace is free from anti-LGBTQ behavior is important for both workers and customers alike.

Asian-American entrepreneurs, founders, and technologists have been demoing fintech innovations on the Finovate stage from the very start. In 2008, the first year Finovate hosted fintech conferences on the West coast as well as the East, we were thrilled to showcase Weiting Liu of SocialPicks, Peter Pham of BillShrink, and Kenneth Lin of Credit Karma.

Fifteen years later, Asian-Americans continue to play a major role in driving fintech innovation – and in demoing those innovations live on the Finovate stage. Here is a look back at those Asian-American fintech and financial services professionals who led live demos at our conferences in New York and San Francisco last year in 2022.

FinovateSpring 2022 – Coinme – Sung Choi, SVP Strategy & Business Development

FinovateSpring 2022 – HAWK:AI – Steve Liú, General Manager North America

FinovateSpring 2022 – JUDI.AI – Su Ning Strube, Chief Product Officer

FinovateSpring 2022 – Prelim – Heang Chan, CEO and Co-Founder

FinovateFall 2022 – PennyWorks – Ivan Zhang, CEO and Co-Founder

FinovateFall 2022 – Supply Wisdom – Shaun Wong, Head of Product

FinovateSpring 2023 is right around the corner – May 23 through 25 in San Francisco, California. Early-bird savings end on Friday, so register today and save your spot!

May is Asian-American/Pacific Islander Heritage Month. May is also the month that brings Finovate back to San Francisco for our annual spring fintech conference, FinovateSpring.

To this end – and to officially launch our Asian-American Month Commemoration – we’re highlighting the women and men of Asian-American heritage who will be taking the stage at FinovateSpring May 23 through May 25.

Today is the final day of Women’s History Month. At Finovate, we have spent the past 30+ days highlighting the accomplishments of women in our industry. We began our commemoration with a look at the women who would demo their companies’ latest technologies at FinovateEurope. We followed up on International Women’s Day, showcasing the women who would deliver mainstage keynote addresses at the conference. And just this week, we featured the winners of the “Female Founded/Owned” category of our Finovate Demo Scholarship program for fintech startups.

Today we share insights from Maggie O’Toole, Vice President of Strategic Partnerships at TabaPay. Headquartered in Mountain View, California, and founded in 2017, TabaPay is a specialist in real-time money movement. The company facilitates one million transactions every day, has more than 2,000 clients, and is the number seven ranked CNP (card-not-present) acquirer in the U.S.

We caught up with Ms. O’Toole to discuss her work at TabaPay, her experience as a female leader in fintech and financial services, and what needs to be done in order to enable more women to secure leadership roles in our industry.

Tell us about your background and current position at TabaPay.

Maggie O’Toole: When I graduated college and moved to the United States from Poland, I faced some of the biggest challenges of my life. Being an immigrant in a new country without speaking the language was a difficult experience, but it also ignited a fire in me to prove that I could succeed.

Over the past decade, I’ve dedicated myself to the payments industry, focusing on strategic partnerships that help businesses thrive. My time at Onbe was particularly impactful; I had the opportunity to lead the charge on launching new products and forging partnerships that enabled real-time payments. I’m proud to say that I played a pivotal role in helping Onbe grow from a startup to a scaled enterprise, while completing a successful M&A strategy.

Today, at TabaPay, I focus on maximizing value for our clients and positioning the company for long-term growth. Building solid relationships with clients, networks, and banks is at the heart of everything I do. I take pride in the fact that I’ve been able to establish a partner management department from scratch, which is set to quadruple in size by the end of the year.

My journey has been anything but easy, but it has shaped me into the leader I am today. I’m passionate about the payments industry and helping businesses succeed, and I’m excited to see where my journey will take me next.

What challenges have you faced as a woman in fintech, and how have you overcome them?

O’Toole: As a woman in fintech, I have faced various challenges throughout my career. I’m still amazed by the vast underrepresentation of women in leadership positions in the industry. This has made it more difficult to find role models or mentors who share similar experiences and can provide guidance and support.

Another challenge I have faced is the pervasive gender bias that exists in many aspects of the industry. This bias can manifest in subtle ways, such as being interrupted or talked over in meetings, or in more overt ways, such as being passed over for promotions or opportunities.

To overcome these challenges, I have sought out supportive networks of women in fintech and other industries. These networks have provided me with invaluable mentorship, advice, and opportunities for growth. I have also worked hard to advocate for myself and my accomplishments, and to challenge gender bias whenever I encounter it.

Furthermore, I have always prioritized my personal and professional development. I have sought training and education opportunities to improve my skills and knowledge, allowing me to excel in my role and advance my career despite these challenges.

How have these challenges shaped your leadership style?

O’Toole: My experiences as a woman in fintech have influenced my leadership style. I believe overcoming challenges and facing obstacles head-on has helped me become a stronger and more effective leader. By persevering through difficult times, I have developed a resilient and adaptable leadership style; I’m always ready to take on new challenges.

One way these challenges have shaped my leadership style is by making me a better communicator. I have learned the importance of clearly articulating the company’s vision and plan to my team, so everyone is on the same page and working towards the same goals. Additionally, I have become more empathetic and understanding of my team’s needs, providing them with the support and guidance they need to be successful. I truly believe that sound, repeatable, positive business results are a natural outcome of prioritizing our employees, clients, and partners through building trusted and safe relationships.

Finally, setbacks and failures have taught me to view them as learning opportunities and growth. I encourage my team to adopt a similar mindset and not to be afraid to take risks and make mistakes. I believe that taking pauses periodically and reflecting on where we are and where we’re headed as a team is essential for long-term success.

Overall, my experiences have made me a more effective and compassionate leader, and I am grateful for the lessons they have taught me.

What is your approach to building work environments and teams?

O’Toole: My approach to building work environments and teams is rooted in building strong relationships. As a leader, I believe it’s essential to take the time to understand the backgrounds, experiences, and perspectives of each team member to foster a culture of trust and mutual respect. By investing in these relationships, I aim to create an environment that empowers individuals to be their best selves and feel supported in their growth and development.

I strive to create a work environment that encourages collaboration, creativity, and innovation. This includes providing opportunities for open communication and feedback, as well as recognizing and celebrating individual and team achievements. Ultimately, I aim to build a team united by a common purpose and inspired to work towards a shared vision.

What are the most important qualities for women in leadership positions in fintech, and how can they develop these qualities?

O’Toole: As women in leadership positions in fintech, we have unique perspectives and valuable insights to bring to the table. We must have confidence in our abilities and not let anyone else define us or hold us back. We should proudly tell our stories, embrace our individuality, and be intentional with our time and energy.

To develop the necessary qualities for leadership, we should constantly be growing and learning, personally and professionally. We can bring new skills and lessons from our personal lives into our work and vice versa and remain open to new perspectives and opportunities for growth.

As leaders, we must be intentional about what we say “yes” to, knowing that every decision comes with trade-offs. We should prioritize our strengths and areas of expertise and allocate our time strategically to make the most significant impact on our teams and organizations. By doing so, we can create a more fulfilling and rewarding work environment for ourselves and those around us.

How do you see the role of women in fintech evolving over the next five years, and what are your thoughts on the industry’s progress toward gender parity?

O’Toole: The fintech industry has come a long way regarding gender parity, but much more work remains to be done. As a female leader in fintech, I’m confident that women will continue to play a pivotal role in shaping the industry over the next five years, and beyond.

Companies need to recognize the value of diversity and make a concerted effort to hire and promote female leaders. This is not about meeting quotas, but about creating a genuinely inclusive workforce that reflects the communities we serve. By empowering women to take risks, dream big, and believe in themselves, we can develop a culture of success that benefits everyone.

At TabaPay, I’m proud to be part of a team committed to diversity and inclusion. With 55% of our employees and 65% of our leadership identifying as women or non-binary, we’re setting a powerful example for the rest of the industry. In the years to come, I believe we’ll see even more significant progress as more companies recognize the critical importance of gender parity in fintech and beyond.

In 2022, Finovate launched its Demo Scholarship Program. The goal of the program is to highlight fintech founders from underrepresented communities, as well as fintech startups that are tackling issues of climate change, diversity, and financial inclusion. At each event, starting with FinovateFall in 2022, Finovate grants five scholarships in the categories of Environment, Social, Governance, Person of Color Founded/Owned, and Female Founded/Owned.

With Women’s History Month drawing to a close this week, we wanted to take a moment to highlight the scholarship winners in our Female Founded/Owned category since our scholarship program was launched last year.

Pave

FinovateSpring 2023 Scholarship Winner – Headquartered in Palo Alto, California, Pave enables credit risk teams to identify healthy borrowers, optimize credit limits, and improve collections outcomes. Pave’s technology provides access to a unified view of end customers’ cash flow and financial profile to help power a range of use cases including cash advances, credit building, overdraft protection, and more.

Pave was co-founded by Ema Rouf in 2020. Previously, Rouf co-founded Adazza – a company that built integrations with telecoms and mobile money operators in emerging markets including Africa and Central Asia in order to collect and analyze data for analytics and machine learning applications.

Quoroom

FinovateEurope 2023 Scholarship Winner – Headquartered in London, U.K., and founded in 2018, Quoroom offers an end-to-end fundraising and cap table management software solution for private companies. The firm’s technology enables users to raise capital up to four times faster thanks for Quoroom’s investment workflows. Quoroom supports a range of functions including building an investor pipeline and conducting investor matchmaking and outreach, as well as legal completion and cap table management.

Ulyana Shtybel is co-founder and CEO. Shtybel was named to the Inspiring Fifty Europe’s roster of the Top Fifty Women in European Tech for 2022.

TAZI AI

FinovateEurope 2023 Scholarship Winner – Based in San Francisco, California and founded in 2017, TAZI AI is a machine learning platform that enables businesses and data scientists to develop ML models for agile decision-making. The company earned recognition from Gartner as a Cool Vendor in Core AI Technologies for its continuous learning, explainable AI, and human-in-the-loop technology. TAZI AI won Best of Show in its Finovate debut at FinovateEurope this year.

Zehra Cataltepe is co-founder and CEO. A former professor of computer engineering for 17 years, Cataltepe is a member of the Forbes Technology Council, and an alum of the Alchemist Accelerator, Class 26.

Debbie

FinovateFall 2022 Scholarship Winner – Based in Miami, Florida and founded in 2021, Debbie is the Noom for debt loss. The company leverages behavioral psychology and rewards to help users pay off 3x more debt and enable lenders to recession-proof borrowers. Debbie won Best of Show at FinovateFall 2022 for its app that guides borrowers in a curriculum based on actionable financial assignments, offers rewards for successful goal achievement, and makes it easier for borrowers to connect and track all of their debt accounts.

Co-founder Frida Leibowitz is CEO. A member of the inaugural class of On Deck’s fellowship program in 2021, Leibowitz spent more than two and a half years working for Marcus by Goldman Sachs.