This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

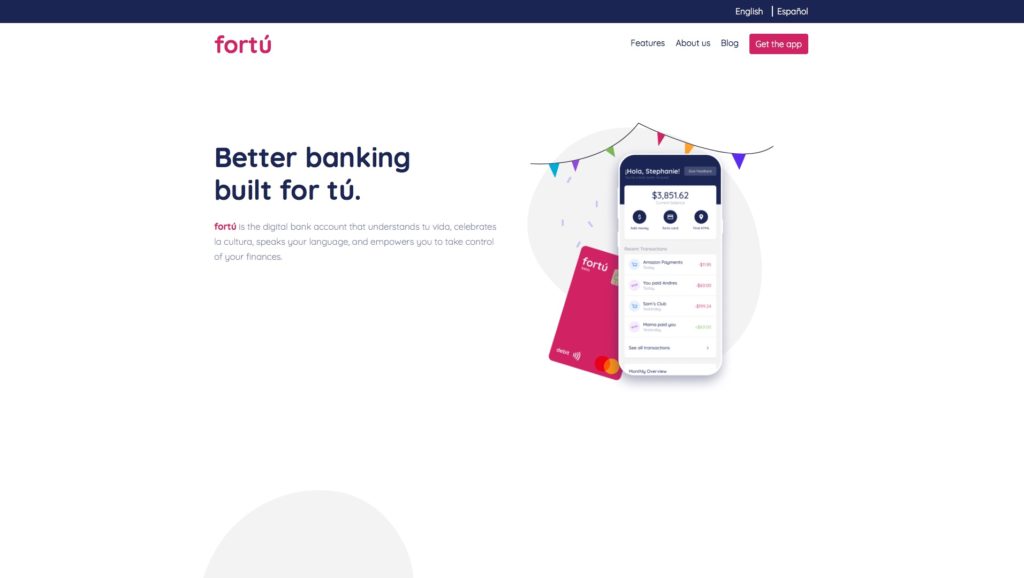

A new challenger bank launched this week with the goal of serving the needs of Latin American consumers in the U.S. Built on Galileo’s payment processing platform, Miami, Florida-based Fortú is dedicated to providing culturally-contextual financial and banking services to the country’s growing Latino and Hispanic populations.

Fortú co-founders Charles Yim and Apoio Doca bring a combination of Big Tech savvy and global neobanking experience to the task of better serving the 22% of Hispanic adults who, according to the Federal Reserve, are underbanked. Yim is a former Amazon Web Services and Google executive with a background in business development and partnerships. Doca helped build a pre-smartphone era digital bank based in Brazil called Lemon Bank that was acquired by Banco do Brasil.

The Fortú team features both first and second generation immigrants with family ties to many of the largest Spanish-speaking countries in Latin America. Together they bring this experience to the cause of helping others negotiate the unique challenges many Latinos and Hispanics face when banking in the U.S.

“Compared to other demographics, Latinos in the U.S. are more likely to live in multigenerational and multilingual households, with a significant percentage needing to send regular cross-border remittances, leading to an over-reliance on non-bank financial services,” Doca said. He added that financial barriers for Latinos and Hispanics can range broadly from a lack of non-English language services to more mundane annoyances like the tendency to randomly truncate Latino names – many of which do not fit within the 24-character embossing standard used by most financial institutions.

Fortú offers a digital bank account that can be opened without needing a social security number; a Mastercard debit card; fast, no-hidden-fee international transfers (courtesy of a partnership with Finovate alum Wise), as well as the ability to deposit cash at more than 100,000 retail locations like CVS and Walmart, and make free cash withdrawals at more than 55,000 Allpoint ATM locations.

“By creating products to answer the needs of Latinos, who are more likely than the general population to be under- and unbanked, Fortú has set itself apart from other neobanks, while transforming financial wellness for the Latino community,” Galileo CEO Clay Wilkes said.

Fortú has raised $5 million in funding from Valar Ventures and other investors. The fintech’s banking services are provided by LendingClub Bank.

Julie Muhn chats with Rita Martins, FinTech Partnerships Lead – Innovation Finance and Risk at HSBC about her experience as a woman in fintech, trends she’s seeing across the industry, and what can be done to encourage more female founders.

Tell us about yourself and your career path to your current role.

RitaMartins: My career started with an internship at Santander in Asset Management managing mixed portfolios. After a few months, a great opportunity came up to join the consulting world. Working at Ernst and Young and later at Accenture, I travelled the world driving large scale transformation projects and advising C-Suite on the applicability of new technologies in finance. During this time, I started diving into the fintech world and noticing first-hand how fintechs were making a difference in developing countries (despite challenging conditions, everyone had a phone and used it for payments).

In 2018 I moved to HSBC, where I currently Lead FinTech Partnerships for Finance and Risk. I am responsible for managing relationships with third parties and driving collaboration between fintechs and traditional financial services SMEs.

What trends are you seeing driving fintech this year? Are they different to previous years, or when you first started in the industry?

Martins: Nowadays, fintech companies are much more mature than when I started in the industry. Fintechs discovered where they can have an impact and when to partner with others in the market.

This year we continue to see fintechs emerging in the Artificial Intelligence (AI) and Cloud spaces. Additionally, there is a new trend in ESG (Environment Social and Governance), with many new fintechs researching and developing solutions in this space.

In your opinion, what is the secret to a successful partnership between bank and fintech?

Martins: There isn’t one factor but a combination of factors that lead to a successful collaboration. Before a partnership is created, both parties need to understand if their culture, goals, and strategy are aligned. An ideal partner will be someone who complements the other and brings new ideas to the table to ensure continued innovation.

After papers are signed, there needs to be an open and frequent dialogue to ensure issues are quickly solved, targets are met, and any changes needed are settled.

What is important to you to see from a fintech leader/ founder of a new start-up you’re looking to work with?

Martins: A fintech-bank partnership is much more than finding great technology; human interaction is vital. When looking for new partners, the fintech leader or founder is often the one representing the company, so in the initial discussions, we would be looking at a combination of factors:

1. Their knowledge of the technology and industry

2. Their values and how they connect with our team

3. How innovative they are and what new ideas they bring to the table

4. What their goals for the partnership are, and how flexible they are

Do you see many women leading fintechs or in senior positions? Is there enough diversity across the board in these roles?

Martins: No, there is still a noticeable lack of women and minorities in senior positions and even fewer women founders.

Typically, women who work in fintech will have roles in sales, communications, or marketing with a noticeable gap in the technology and senior roles.

So, what can the industry do to better encourage women to get involved with fintech?

Martins: I would challenge the industry to do more at the senior level. Those changes will empower young women to join the industry, retain existing leaders, and decrease the pay gap.

Two key areas that need immediate change are:

More investment needs to go into female-founded fintechs. In 2020, only 2.3% of VC capital went to female-only founded start-ups (according to Crunchbase)

Banks and fintechs boards and leadership need to be more diverse. In 2020 women represented only 14% of fintech boards (according to Oliver Wyman)

Listen to more from Rita as she looks back on her experience at FinovateEurope 2021 below

When we think of global corporations and business in general, do we feel pride in how we do things? Beyond Good, a new book by Unconventional Ventures co-founders Theodora Lau and Bradley Leimer, is a call to arms for business leaders to recognize how they can do well by doing good.

Beyond Good showcases how fintech is changing business models and what every industry can learn from it. The leaders in financial services are fostering a thriving ecosystem of incumbents and startups, unlocking new possibilities to make broader financial inclusion a reality.

With a foreword from the Aspen Institute, exclusive interviews with leading B-Corps, policy makers, executives, and case studies from companies like Sunrise Banks, Ant Group, Village Capital, Microsoft, and PayPal, Beyond Good shows how everyone can contribute to a more common good. Finovate readers can also get 20% off their copy of the book, using code Inspire20.

Below are a few excerpts from our conversation with Theo and Brad on the new book and their upcoming appearance at FinovateSpring next month. For the full interview, check out the video above.

On the importance of financial inclusion

Theo Lau: “If we talk about the onset of the so-called fintech revolution, if you will, a lot of the new startups seemed to regurgitate old ideas that have already been around. They make it prettier, they create this bamboo credit card … But it that really changing our behavior, is it really changing how we work? In the West, are we really including more demographics and doing things better for them? I would argue a lot of the time we are not.”

Bradley Leimer: “Inclusivity goes much broader than just a credit card or just lending or just credit. And that’s a lot of what we discuss. There’s more to a financial relationship than one side of the balance sheet. There’s more to the financial services model than just profitability. There are longer term implications in everything we do every single day and every decision that we make.”

Why fintechs and financial services need to move “beyond good.”

Leimer: “We’ve seen a lot of stakeholder capitalism lately and examples of companies that have tried to mean more for their business model and their communities. That’s what we celebrate in the book, the shift that we can include more people in our communities in society. Especially in financial services and technology, companies we really need to focus how we can serve these larger groups. Everybody in society should be able to be a part of our business models. And that’s why we go “beyond good.”

Lau: “We want to reinforce that this is not a zero-sum game. Just because we are including more demographics and more considerations on how we conduct business doesn’t mean you’re losing. Case in point, one of the things lately we’ve been talking about is student loan debt, $1.7 trillion dollars of debt. Obviously the burden is shared across all demographics, but particularly in communities of color, among first generation college students, and among those in other less advantaged groups.

So our question is: how do we go about solving it? There are a lot of different moving parts. But for financial services, the role isn’t just to offer another loan on top of the pile of deb because that’s not solving the problem. We need to go back further to ask how we create a more equal society, more equal products, and create services to help people rethink their finances and get to a healthier financial situation.”

Join Theo Lau and Bradley Leimer at FinovateSpring May 10 through 13. For more information about our upcoming, all digital, spring fintech conference, visit our FinovateSpring hub today.

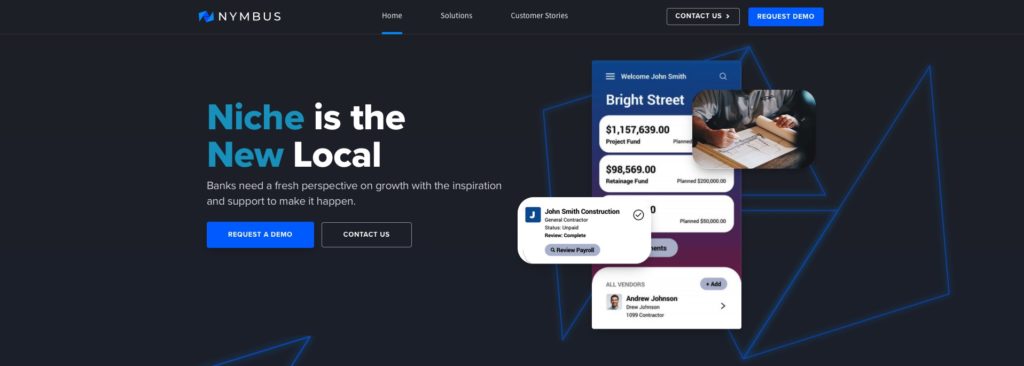

News of NYMBUS’$15 million fundraising this week – and the company’s recent appointment of three women to key leadership positions – serves as a fitting bookend to a first quarter that began with big investment and big C-suite hires, as well.

In January, the Miami, Florida-based banking technology provider expanded its leadership team with the addition of Chief Alliance Officer Sarah Howell and Chief Product Officer Larry McClanahan. A month later, Nymbus secured a Series C investment of $53 million in a round led by Insight Partners.

“As the pandemic has pushed digital to the forefront, more banks and credit unions have turned to Nymbus as their partner for growth,” Nymbus CEO and Chairman Jeffery Kendall said when the funding was announced in February. “This new and significant investment validates a confidence in Nymbus to continue transforming the financial services industry with a banking strategy that buys back decades of lost time to speed digital innovation.”

Little did we know how quickly further valuation would arrive. This week’s investment by European private equity firm Financial Services Capital doubles its investment in Nymbus to more than $31 million. The funding gives Nymbus a total capital raised of more than $98 million.

“We look forward to continue working with Nymbus as they build out a best-in-class, cloud-native offering that is well positioned to be a leader in the industry and will transform our portfolio companies,” Financial Services Capital Managing Partner Miroslav Boublik said. He and fellow Managing Partner Matthew Hansen will join the Nymbus Board of Directors as part of the investment.

Also joining “Team Nymbus” is Veeva Systems co-founder Matt Wallach, who will serve as a Strategic Advisor. Nymbus will benefit from Wallach’s experience in co-founding one of the leading cloud software companies in life sciences. Founded in 2007 and, 14 years later, the first publicly traded company to transition into a public benefit corporation, Veeva now has a market capitalization of more than $40 billion and 975+ customers in the pharmaceutical industry, as well as in emerging biotech.

As mentioned, Nymbus’ funding announcement comes on the heels of the company further bolstering its leadership ranks with a trio of new, C-suite hires. The women – Trish North as Chief Customer Officer, Michelle Prohaska as Chief Compliance Officer, and Crina Pupaza as Chief People Officer – bring years of customer success, risk management, and people-centered programming experience to a company that has seen significant growth as banks turn increasingly toward digital transformation of their outdated legacy systems.

“In order to help our partner institutions serve the unique financial needs of niche audiences, success begins with diversity in our own Nymbus leadership,” Kendall said last week when the appointments were announced. “I’m incredibly proud of the impactful effort we are making to recruit a balanced male to female representation into our C-suite, and beyond confident of the value that Trish, Michelle, and Crina will each uniquely provide to both our team and partner clients.”

Not letting any grass grow beneath its feet in the wake of the U.S. Justice department’s decision to block its acquisition by Visa, fintech infrastucture company Plaid has since launched its FinRise incubator to support early-stage founders who are members of ethnic minority groups.

“While technology has come a long way to level the playing field, the reality is that many minority-owned businesses are still frequently denied access to some of the most basic resources needed to start and grow their businesses,” Nell Malone and Bhargavi Kamakshivalli wrote on the Plaid blog when the program was announced in January. Highlighting in particular the plight of African-American owned businesses as noted in a report from the Small Business Administration, Malone and Kamakshivalli wrote: “It is a shared responsibility to help power a financial system that works for everyone, and we recognize that one way to achieve that is to support and promote a diverse ecosystem of entrepreneurs.”

All this makes today’s announcement that FinRise has chosen the first companies to participate in its accelerator program that much more exciting for supporters of financial inclusion and diversity. Out of more than 100 applications, five early-stage fintechs were selected, offering solutions in everything from identity verification and authentication to financial wellness and lending.

The qualifications for consideration were startups with at least one founder who is African-American, indigenous, or a “person of color,” has two or more employees, and is post-seed, pre-Series B in its funding status. The members of the incoming class are below:

Global Data Consortium: a global identity verification API that provides KYC and eKYC services for businesses

Guidefi: a financial wellness marketplace to help members of ethnic minority groups connect with “vetted, culturally-attuned” financial advisors

OfColor: a financial wellness program that offers personalized PFM and loans to help ethnic minority employees maximize their 401(k) contributions

Walnut: a point-of-sale lending platform that works with healthcare providers to make it easier for patients to pay for their medical bills

Zeta: a financial wellness company that specializes in PFM solutions for couples and families

FinRise begins with a three-day bootcamp of workshops covering issues ranging from regulatory and policy concerns to marketing and communications strategy. After the bootcamp, startups will be paired with Plaid mentors to help them further develop and scale their products. The nine-month program consists of workshops and networking opportunities with accelerator partners, as well as discounts on services offered by Plaid network partners. Even those startups not selected for the accelerator this session will be eligible for discounts and credits from companies supporting the program.

FinRise’s network partners include: Alloy, AWS Activate, Brex, Fintrail, FS Vector, Hummingbird, Very Good Security, and Zendesk.

The launch of Cheese, a digital banking platform dedicated to serving Asian American communities, is the latest instance of entrepreneurs seeking to translate a renewed sense of ethnic identity among many Americans into greater financial wellness, if not empowerment, for those in their communities.

“I have always envisioned launching a digital banking platform that someone like me could easily access but also serves a deeper purpose, with the power to positively impact Asian communities,” Cheese CEO Ken Lian said. “Cheese is that banking platform.”

Cheese includes Ifly.vc and Amplify among its chief investors, having raised $3.6 million in seed funding from the two firms in a round that also featured participation from former Wealthfront CEO Adam Nash and Zillow co-founder Spencer Rascoff. As part of the company’s offering, Cheese accountholders get a debit card (issued by Coastal Community Bank), two-day early advance pay with direct deposit, a 3% deposit bonus for referrals, a 0.3% annual percentage yield, and as much as 10% cash back on purchases at more than 10,000 participating merchants.

And as part of its pledge to support Asian American communities, Cheese will donate $100,000 to nonprofit organizations and community service programs that support Asian neighborhoods and small businesses – especially those impacted by COVID-19. Communities in San Francisco, Los Angeles, and New York City are among the first areas of focus.

The Asian American community is characterized by its diversity and its rapid growth; there are nearly 21 million Asian Americans in the United States. The relatively high income and education levels common in this community compared to other minority communities in the United States makes them an attractive opportunity for providers in financial services – from digital banking to wealth management.

At the same time, the rising number of incidents of violence against Asian Americans in 2021 are reminders that discrimination and racism against Asian Americans continues to be a challenge in a rapidly-diversifying country. In financial services, this issue often manifests itself most acutely with new Asian immigrants who may have language barriers or lack a credit history and struggle to even secure a bank account. Lian, who immigrated to the U.S. from China in 2008, knows this problem well.

“I had been declined multiple times for basic bank accounts,” Lian said, “even with an 800+ FICO score.”

Cheese is headquartered in Pasadena, California. The company was founded in 2019.

As our recent conversation featuring Boss Insights founder and CEO Keren Moynihan, reminds us, the fintechs (and “TechFins”) of the Great White North are engaged in some of the most forward-looking innovation on the continent.

This week brings an above average volume of news from Canada’s ambitious real-time payments industry. For one, the Vancouver Bullion & Currency Exchange (VBCE) announced a partnership with EMQ to bring “near real-time” cross-border payments to businesses and consumers across Canada. A PSP as well as a foreign currency exchange, VBCE hopes that its partnership with the global financial settlement network will give its customers the ability to move money faster and more efficiently. The firm also anticipates being able to use EMQ’s network to bring new services to market and scale existing ones.

“The speed and reach of EMQ’s global network allows us to pilot new services in one market and scale them rapidly across others to meet the evolving customer needs,” VBCE VP of Business Development Kevin Ma said. “This is especially important for our business with a diverse product portfolio.”

Elsewhere on the Canadian real-time payments beat, Payments Canada announced a collaboration with debit network Interac to support real-time payments in the country. Interac will serve as the exchange solution provider for Real-Time Rail, the real-time payments systems operated by Payments Canada and regulated by the Bank of Canada. RTR, scheduled to go live in 2022, will enable Canadians to initiate payments and receive funds in seconds.

Payments Canada President and CEO Tracey Black said that RTR will be the “foundation for faster, data-rich payments” and will serve as a “platform for innovation.” Black also praised Interac as a “well-suited partner” with the requisite infrastructure and connectivity to support “the rapid adoption of real-time payments in Canada.”

Last, some developments on the Canadian neobank front. Toronto, Ontario-based challenger bank KOHO added a no-fee savings account to its offerings this week. KOHO Save gives account holders 1.2% interest on their entire balance. There are no teaser rates and no minimum balance is required to acquire an account, which is available on the KOHO app.

“We’re excited to add KOHO Save to our product line as a simple and valuable money earning tool for Canadians,” KOHO CEO and founder Daniel Eberhard said. “We’ve been able to build a savings tool that doesn’t follow the same restrictions of most other savings products on the market. People just want to access their money freely and earn a great interest rate. We think Save is a wonderful step in that direction.”

KOHO also offers a savings and checking account and gives users a minimum of 0.5% (up to 10%) cash back on all purchases. KOHO Premium account holders get an additional 2% cash back on three major spending categories. The company, founded in 2014 and headquartered in Toronto, Ontario, has raised $57.5 million in funding from investors including Drive Capital and Portag3 Ventures.

Here is our look at fintech innovation around the world.

Israel-based Rewire, a cross-border digital banking firm that serves migrant workers, announced $20 million Series B round led by Finovate alum OurCrowd.

With Black History Month drawing to a close and Women’s History Month just underway, now is an excellent opportunity to look at some of the ways that fintechs and financial services companies are responding to the needs of women- and ethnic minority-owned small businesses and their employees.

This is a story about how three companies – a Canadian fintech and Finovate alum named Boss Insights, a diversity-focused neobank called Paybby, and one of the biggest African-American banks Carver Federal Savings Bank – came together to help struggling small business owners survive in a world made even more unequal by the global pandemic.

Can you tell us how the collaboration began?

Richard Muskus, SVP and CRO Carver Federal Savings Bank: The collaboration began as Carver was in the late stages of assessing and negotiating a technology solution for our PPP platform with a large well- known national firm and there was a great deal of urgency to have this platform in place to meet the upcoming government program launch.

Facing a delay in setting up an all-hands call to finalize planning, we were introduced to Boss Insights and Paybby who engaged Carver within hours and moved to demo and agreement within 48 hours. As impressed as we were with the tech, we were as equally impressed with the speed by which Carver was up and running.

Hassan Miah, founder and CEO, Paybby: When PPP came out, the first round, people of color were underrepresented. Either they didn’t know (about the program) or they had issues getting their data. We went around and looked at what platform would be the best that would help these communities do better in this next round.

We did a deep dive on multiple platforms, including Boss Insights’ platform, and we saw they they had an architecture and a product that would best serve the community we are focused on.

Why is it important for you to be involved in this round of the PPP?

Keren Moynihan, founder and CEO, Boss Insights: We were having meeting after meeting and reading article after article about the program and someone said to me at one point: “You’re a female founder. Can you tell me what you’re doing to help diverse and minority companies survive?”

When someone says something like that it resonates in your head and you just don’t stop thinking about it. In the first round of PPP only 14% of participants reported their demographic information. But in that 14%, 16% were female-owned companies and 18% visible minorities. If you look at that and compare it to the actual number of businesses run by females or by visible minorities there is a large difference. “Boss” in Boss Insights stands for “back office software systems” and insights on those. We are a data-driven company and so when you look at those numbers it’s clear that something had to be done.

Muskus: Serving the needs of our communities is foundational to the organization since 1948 and not only being involved, but being a leader in the PPP is representative of our mission.

What is gained when fintechs and neobanks and community banks collaborate?

Muskus: Partnering with firms such as a Boss Insights and Paybby allows small community banks such as Carver to provide customers with the highest quality of service and is incredibly important in our growth and impact in the market.

Miah: When we first got involved, Carver and some of banks we talked with told us that in the Black community many people don’t even have a bank account. We saw this as an opportunity to provide that account and then support them on their loan efforts.

Many of these small businesses are small Mom and Pop businesses, many of them work out of their back pockets: they use their regular personal checking account, make no distinction between their social security number and EIN, and those kinds of things. So we saw that they needed these services – and wanted them. There’s a lot of opportunity there.

Moynihan: The piece that has become much clearer to me is that we have been focusing so much to make sure that this technology works seamlessly, that it can get onboarded in one hour – meaning any lender who wants to support businesses and measure them on their merit, they’re one hour away from doing it.

You can sometimes get so into that rabbit hole that you forget about the reason you started to begin with. Business owners, they are people, with families and children, and what we want is to give them the ability to go to a lender and say: this is me, this is my package of information, please evaluate me. Don’t look at extraneous details – look at me and tell me if I am a good bet.

How will you measure success and what insights have you gained from the partnership?

Muskus: Our success is measured primarily by how successful our customers view Carver being. The successful delivery of our products and services leveraging these types of partnerships is representative of the choices we make in partnering to begin with.

Miah: Part of our goal is to bring data science to the community in a way that is usable. One reason we bought banking app Wicket is that it categorizes your spending. Our vision is you go from having a bank account where you just spend money and your account starts at $500 and it goes down to $50 to where you start saying, “hey I spent $100 on Starbucks . Did I really need to do that when I can’t even feed my family.” The idea is to marry the data with the use case, and now we have the technology and the know how to not just tell people “oh you ought to learn how to do better and think about managing (your finances)”, but the tools and technologies and everything are there and available.

Moynihan: When you’re a business and you’re asking for money from a bank, the first thing they do is they send you a laundry list of information they need to get from you. (But) if you have a connection to where they are collecting it, and it’s on the cloud, you can get it in real-time. So whether it’s accounting information for businesses that have made it that far, banking information for ones who are just starting out, or credit scores which will continue to get better, you can have access to the information in real time. The industry is called the “financial services industry”. (Now) lenders can focus on the services part of that, not on the data administration part. That’s what we’re all doing here together, that’s the real crux of the collaboration.

Founded in 2017 and headquartered in Toronto, Ontario, Canada, Boss Insights made its Finovate debut two years ago at FinovateFall. At the event, company founder and CEO Keren Moynihan demonstrated Boss Insights’ Smart Capital platform, which leverages data-driven insights to accelerate the lending process.

A public benefit challenger bank dedicated to bringing financial empowerment to African-American and Latino communities, Paybby offers a financial wellness and PFM app – Wicket – courtesy of its recent acquisition of the eponymous Overland Park, Kansas-based neobank. Wicket provides a Mastercard debit card and FDIC-insured savings and checking accounts, as well as early direct deposit and automatic savings solutions.

Founded in 1948, Carver Federal Savings Bank is one of the largest African-American banks in the U.S. Headquartered in Harlem, New York, the bank has been designated as a Community Development Financial Institution (CDFI) by the U.S. Treasury Department for its community-based banking operations. Carver Federal Savings Bank is committed to reinvesting 80 cents of every dollar deposited back into the African American community.

With International Womens’ Day just around the corner, we continue our #WomeninFintech series and speak with Kim Snyder, CEO & Founder, KlariVis about her journey through fintech and advice to the next generation of women coming through.

Tell us about yourself and your career path to your current role.

Snyder: Personally, I am a very family-oriented person and prior to the Pandemic we had started some new traditions, like “Sunday Brunch-day”; it truly is my favorite thing to do and I cannot wait until we are able to restart those activities!

My career path to KlariVis is probably not what you would expect. I started my career with KPMG and then moved into an accounting/finance role for a small private liberal arts college. My next step was where the entrepreneurial bug hit me: I joined a local start-up company focused on creating new innovations in a variety of industries and it was here I saw what it was like to build something from scratch and it was invigorating, exciting and scary all at the same time. I then spent 10 years at a community bank, and it was my passion for this industry that fueled my drive to take the chance and start my own consulting business. During those course of 4+ years, I hired many previous team members to help me build a premier, boutique consulting firm focused on helping community banks solve the prevalent issues they are faced with in this rapidly changing industry.

The one challenge that resonated more than any other, though, is the data conundrum that exists in the banking industry. Regardless of size, core system, talent level or management team experience, our clients were paralyzed with the mass volume of data generated by the various siloed processing systems and the bank’s inability to access that data in an efficient manner, thus making it virtually useless to the institution. We knew that there had to be a better way and thus the idea of KlariVis was born. We spent about a year incubating our solution and our consulting clients became our focus group – by the end of that year, they were using phrases like “game-changer” related to our solution. So, I started a second company in February 2019 and hired a technology firm to take our proof of concept and turn it into reality. We launched KlariVis in January 2020 and the response was incredible from our prospect banks. We issued a press release last week – FVCBank has now invested in KlariVis due to the value and impact our platform is having on their bank. I’m not sure what better testament there can be than for a client to say, I want to be more than a client, I want to invest in your success and become your long-term strategic partner.

There seems to be a big push towards knowing your customer and providing a personalized and exceptional service in recent years. How should banks go about this?

Snyder: Community banks are known for their exceptional customer service – they typically have a very loyal customer base who value the personal touch. The PPP program highlighted this very fact – it was the community banks who stepped up and were the heroes by helping the small businesses in their communities.

How do they take that exceptional customer service and turn it into a more personalized experience? I believe it all starts with treating data as an enterprise-wide asset – making sure it is in the hands of the relationship managers who interact with and serve bank customers every day. The banking customer is communicating to its bank every day through transactions, whether they be transacted in person or digitally.

Unfortunately banks and credit unions are hampered by the numerous disparate systems that exist in the banking ecosystem, most of all which have critical data points about their customer base. As such, they have no choice but to leverage solution providers to enable them to aggregate this information, cut out the noise and focus on the high-value actionable data points that will allow them to offer that more personalized touch.

Allowing easy and efficient access to customer data at the front-line is paramount to improving and personalizing the customer experience.

Are there other trends you see driving innovation within banking/ fintech?

Snyder: Digital transformation is the primary focus for financial institutions of all sizes and I don’t see that changing for quite some time. We’ve been talking in the industry for years about this wave coming, and due to the Pandemic, it’s here. In a recent survey by the Digital Banking Report, the top three strategic priorities for 2021 were consistent for big and small institutions: 1) improve digital experience for consumers; 2) enhance data and analytic capabilities; and 3) reduce operating costs.

Fortunately for KlariVis, we hit 2 of the top 3 strategic priorities – enhancing data and analytic capabilities and reducing operating costs. Our solution accomplishes both and enables financial institutions to improve the overall customer experience.

What is important to you as a leader of a fintech? Does KlariVis have any initiatives that support diversity/ women in fintech?

Snyder: I strive to build a diverse and talented team. KlariVis was born out of an identified need in the banking industry but it was conceptualized through creativity and innovation. Diversity provides our team with expanded creativity stemming from different perspectives based upon life and work experiences. Absent of diversity of thought, skills and unique perspectives, our concept would not be what it is today.

My goal is to hire the best talent for the Company’s open positions, but as a female leader, I am passionate about ensuring that opportunities for women continue to grow in fintech and would like to see the same trend at KlariVis. Many tech industry roles are often filled by men. At KlariVis we have three females at the C-Suite level and each of us is equally passionate about hiring, promoting, and compensating talented deserving women. We would like to see more female applicants for technical positions particularly software engineers and have recently begun participation with a university’s internship program which may yield diverse candidates for future open positions.

What advice would you give to women looking to begin a career in banking/fintech?

Snyder: For women looking to begin a career in banking, fintech or another field, it is critical to learn the industry. Evaluating positions typical to the industry and matching that with individual skills, likes and dislikes is key to finding a position that is a good match. Passion is critical particularly in the rapidly growing fintech arena.

In addition to pursing an applicable degree and identifying a mentor, take the time to listen and learn from that person who can provide a frame of reference that you would not have otherwise. There are many different aspects of banking and financial technology is moving quickly with new innovations. Banks are trying to keep up with the latest and greatest technology advancements as well as their competitors with the goal of enhancing the customer experience. I recommend that anyone with an interest in banking or fintech read everything they can to stay current with the industry.

First Boulevard, a challenger bank dedicated to serving the African American community, announced a $5 million seed funding round this week. Participating in the investment were Barclays, Anthemis, and a number of angel investors including actress Gabrielle Union and AutoZone CFO Jamere Jackson. Donald Hawkins, CEO and co-founder of the Overland, Kansas-based neobank, said that the funding would help First Boulevard build out its business marketplace of black-owned SMEs for its Cash Back for Buying Black program.

The capital will also enable the company to grow its team, its customer base, and its platform. Co-founded last August by Hawkins and COO Asya Bradley during the George Floyd/anti-racism protests of 2020, First Boulevard anticipates launching in Q3 of 2021. Among the neobank’s initial offerings will be a no-fee debit card, solutions to automate savings and wealth-building, as well as financial education resources.

As we noted last month in our Black History Month look at African-American based digital banks, the fledgling challenger bank already has forged an innovative partnership with Visa. First Boulevard will pilot a new suite of Visa’s crypto APIs that enable the trading and custody of digital assets.

“The First Boulevard mission is to help Black America build wealth,” Hawkins said last month when the initiative was announced. “We are thrilled to partner with the leader in digital payments, Visa, and leverage their crypto APIs to provide another channel for the Black community to access crypto as a new asset class that can help build Black wealth.”

First Boulevard’s participation in the cryptocurrency project is a reminder of the growing intersection between the African American community and digital assets. A growing number of black observers of and participants in the cryptocurrency space have advocated Bitcoin and other digital assets as a way for African Americans to achieve independence from a financial structure many believe is systemically stacked against them.

It may not be the return of Black Wall Street. But from veteran bankers leading their institutions into the digital future to celebrities and athletes, who are leveraging their fame to encourage African Americans to take advantage of digital financial tools, the challenger banking revolution that is sweeping the globe is also creating new opportunities for banking in African American communities.

As part of our Black History Month commemoration, we’re taking a look at three, digital-first neobanks – and another that was a digital pioneer ahead of its peers – that were founded and are run by African Americans. It is especially interesting to see how all of these financial institutions both respond to the financial wellness needs of the individual while also working support African American small businesses.

It should be noted that digital banking customers who want to support black-owned banks also have the option of signing up for the online offerings of the more than 40 brick and mortar black-owned banks in the U.S. that provide digital banking services.

First Boulevard – Headquartered in Overland Park, Kansas, First Boulevard offers “Unapologetic Banking Built for Black America.” In addition to a contactless Visa debit card and P2P payments, First Boulevard also includes programs such as Early Payday, which enables account holders to get paid up to two days early, and rewards program called “Cash Back for Buying Black.” This program gives First Boulevard accountholders up to 5% cash back at participating African-American businesses.

First Boulevard charges no overdraft or monthly fees, and has no minimum balance requirements. The bank’s app features PFM tools that enable users to round up purchases to store away extra savings, as well as provie spending recommendations and real-time insights based on the user’s purchases.

“(First Boulevard’s) mission is to help Black America build wealth,” said CEO Donald Hawkins. Hawkins co-founded First Boulevard along with COO Asya Bradley, who was recently recognized as an “Inspiring FinTech Female” by NYC FinTech Women. “We are thrilled to partner with the leader in digital payments, Visa, and leverage their crypto APIs to provide another channel for the Black community to access crypto as a new asset class that can help build Black wealth,” he said.

Greenwood Financial – Founded by a host of African American notables including Civil Rights leader Andrew J. Young, rapper and activist Michael “Killer Mike” Render, and Bounce TV Network founder Ryan Glover, Greenwood Financial blends “best-in-class” online banking services with innovative strategies to support black and Latino-oriented causes and SMEs.

Greenwood borrows its name from the Greenwood District of Tulsa, Oklahoma, which featured what was called “Black Wall Street” of early 20th century black-owned financial institutions established in the wake of the Reconstruction Era.

The firm’s C-suite includes Aparicio Giddins, President and Chief Technology Officer, a former executive at both Bank of America and TD with years of work in mobile product and emerging platform management – experience that will prove critical in helping Greenwood grow.

“I wanted to start a bank out of college,” Giddens told ABC News in an interview earlier this year, adding that he was motivated in part by the fact that he observed so few African Americans in banking. In Greenwood, he recognizes the opportunity not just to increase African American representation in the industry, but to bolster the community by using black-owned banks to “recirculate dollars” back into the community.

Greenwood Financial raised $3 million in seed funding back in October. Last month, the platform announced that it has topped 500,000 sign-ups for its virtual banking solutions in its first 100 days. Greenwood’s offering includes savings and spending accounts, virtual debit cards, P2P transfers, mobile check deposit, and no-hidden-fee ATMs in more than 30,000 locations.

OneUnited Bank – In addition to being the largest African-American owned, FDIC-insured bank, OneUnited Bank also has the distinction of being a pioneer in Internet banking among black-owned banks. Founded in 1968 as Unity Bank and Trust Company with $1.2 million in capital, OneUnited Bank has grown into a multi-branch bank and community development financial institution (CDFI) with more than $680 million in total assets. And with offices in Los Angeles, Boston, and Miami, OneUnited Bank has financed more than $100 million in loans over the past two years.

This month, the institution announced its OneTransaction Campaign. In partnership with Visa, and including a free virtual financial conference on Junetheenth of this year (June 19), the initiative is geared toward convincing African Americans to choose one transaction in 2021 to improve their financial net worth. Ideas range from getting life insurance to starting an automatic savings plan to get rid of high-interest debt.

“The reality is the racial wealth gap for each family can be closed by one strategic transaction,” OneUnited Bank Chairman and CEO Kevin Cohee explained. “By encouraging our community to accomplish One Transaction in 2021, we can make financial literacy a core value of the Black community and create generational wealth.”

Last fall, OneUnited Bank announced a $10 million deposit from international biotech company Biogen. “This deposit is one of many ways we are delivering on our enhanced Diversity, Equity, and Inclusion strategy,” Biogen EVP for Global Product Strategy and Commercialization Chirfi Guindo said. “But for OneUnited’s customers, this deposit could mean allowing them to pursue their dreams or strengthening underrepresented minority businesses.”

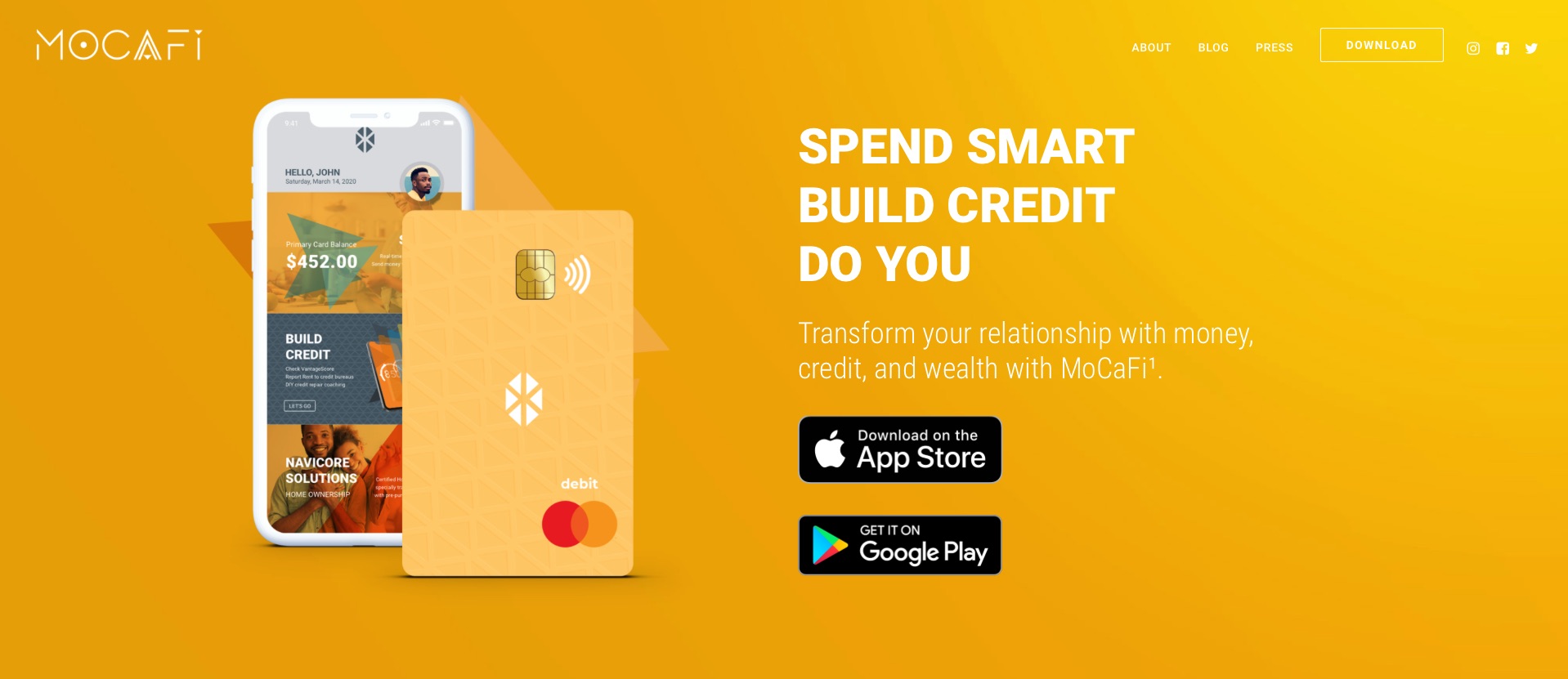

MoCaFi – Headquartered in New York, MoCaFi (which stands for Mobility Capital Finance) is a black-owned mobile banking platform that specializes in helping members of underserved communities benefit from digital financial services. Founded in 2015 by CEO Wole Coaxum, MoCaFi combines 21st century financial wellness solutions with an equally contemporary awareness that – in many communities – both physical money and physical banking locations are a major part of the financial ecosystem. The company partners with retail stores to enable MoCaFi account holders to deposit and withdraw money from their accounts without fee.

Last fall, MoCaFi announced a partnership with Finovate alum InComm that will give members of the black-owned neobank the ability to load their MoCaFi Mobility Debit Mastercard cash at physical retail locations around the country. InComm Payments SVP of Sales Tim Richardson praised MoCaFi as “one of the fastest growing mobile banking platforms in the country” and highlighted the company’s ability to close the “cashless” payments gap for many underbanked consumers that do not have a traditional credit or debit card.

“We already know that Blacks and Hispanics spend at least 50% more on banking services than their white counterparts,” Coaxum said last summer as the company launched its upgraded banking platform. “This is not acceptable. MoCaFi is addressing structural failures in our financial system by reimagining services that ensure that all Americans have access to safe, secure, affordable, and convenient products and services.”

MoCaFi has raised $5.3 million in funding. The firm’s investors include Radicle Impact and Partnership Fund for New York City.

Can cryptocurrencies play a role in bringing the benefits of modern – or even post-modern – finance to underserved African American communities? Is it possible that bitcoin could be the key to enabling black Americans to close with wealth gap with their non-black fellow citizens?

Provocative as it sounds, this is the thesis of Isaiah Jackson, co-founder of KRBE Digital Assets Group. Jackson’s book Bitcoin & Black America makes the case that a cryptocurrency like Bitcoin has a number of features that make it an important ingredient in the kind of economic independence he believes would benefit black Americans. In an interview with Forbes’ Jason Brett last summer, Jackson noted that during the golden era of black-owned banking in the United States – the Reconstruction Period after the Civil War – the existence of multiple currencies played a significant part in supporting the development of community-based financial institutions. This, in turn, helped build the first black middle class in the U.S.

Jackson sees Bitcoin playing a similar role today. He approves of both Bitcoin’s deflationary nature, which he says encourages savings over spending, and its “circular economy” which – not unlike the economy of 19th century black banking – exists significantly outside of a traditional banking system Jackson decries as racist.

With a background as a computer scientist, as well as a Bitcoin consultant and trader, Jackson is nevertheless wary about a future in which Bitcoin and other cryptocurrencies are common. To the extent that human nature endures, discriminatory practices like redlining, in his opinion, are likely to follow us into our digital future – with the moral (or immoral) panic of the day incentivizing regulators to monitor and restrict certain digital currency transactions from certain people or communities. And if history is any guide, the negative impacts of these restrictions are most likely to fall on those least able to manage them.

Nevertheless, when it comes to the potential for Bitcoin to make a difference for black Americans, Washington is a believer. “For the first time in history,” Washington told CNBC in an interview last month, “we have a Plan B option to the current financial system which has seen years of redlining, racial discrimination, and other egregious acts by retail banks to the Black community.”

The second edition of Bitcoin and Black America is currently available via pre-order. The new edition features seven additional chapters including information on Bitcoin specifically for small business owners, as well as a roster of more than 200+ black professionals working in the Bitcoin industry.