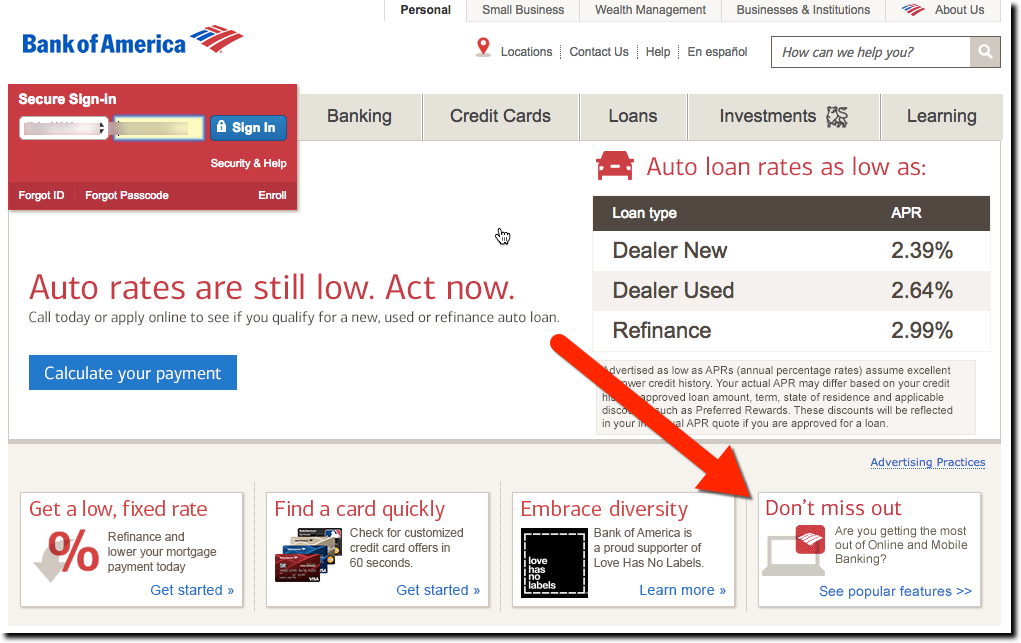

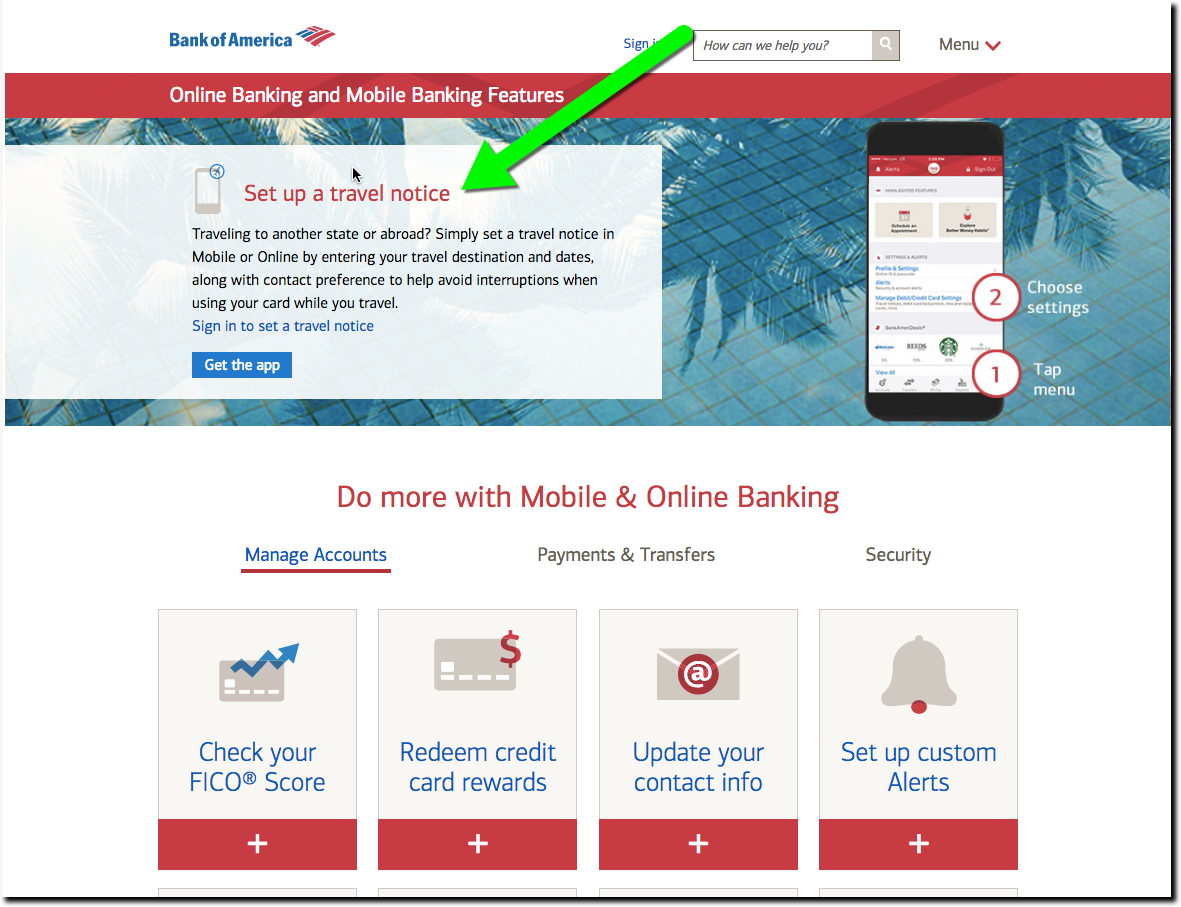

Recently, BofA has been promoting its online/mobile features with a homepage promotion (see screenshot #1 below). I first noticed it while paying my BofA card Friday, but I don’t know how long it’s been running. Clicking the See popular features link delivers you to a page touting features across three categories: Manage Accounts, Payments and Transfers, and Security. The first five are visible on screenshot #2 below:

- Set up a travel notice (currently the featured feature across top-half of screen)

- Check your FICO score

- Redeem credit card rewards

- Update your contact info

- Set up custom alerts

The other 11 (not shown in screenshot):

- Replace card

- Go paperless

- Direct Deposit

- Reorder Checks

- Bill pay

- Transfer and send money

- Pay with a digital wallet

- Mobile Check Deposit

- Lock or unlock your debit card

- Fingerprint sign-in

- Security Center

Note: I’m surprised Bank of America’s “deals” aren’t one of the 16 features highlighted. Even though you can’t really make it out, the mobile phone at the top of the landing page (screenshot 2) has the BankAmeriDeals section open along the bottom (note the Starbucks logo).

Bottom line: A good explanation of digital features and benefits should be easy to find on your website and mobile app. Even though the features seem straightforward to power users like yourself, it’s all a big mystery to 95+% of your customers who just want to spend as little time as possible banking.

{kind=link}