This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

German trading and investing platform NAGA has announced a strategic partnership with stock research company TipRanks.

The partnership will bring advanced stock analysis and institutional-grade research tools to retail investors.

Founded in 2012, TipRanks won Best of Show in its Finovate debut at FinovateSpring 2013. The company took home Best of Show honors again at FinovateFall later that year.

Germany-based fintech NAGA has teamed up with stock research firm TipRanks. The strategic partnership will bring advanced stock analysis and institutional-grade research tools to retail investors.

“We are delighted to partner with NAGA. Both our companies are laser-focused on making data and information more readily available to all investors,” TipRanks CEO Uri Gruenbaum said. “We believe technology has an important role to play in improving outcomes for every investor, giving individuals access to the tools and insights that were once only the domain of large-scale institutions.”

The partnership will enable NAGA users to access detailed forecasts from industry analysts. This includes specific price targets for stocks, as well as recommendations for stocks over varying time periods. The partnership will also allow users to better see how hedge funds are investing in different markets, and how well the managers of those funds are performing.

Users will also benefit from TipRanks’ enhanced Smart Score solution. Smart Score ranks stocks from one to 10 based on eight key factors, including how the stock is viewed by top-performing stock analysts, whether or not hedge funds are in the process of accumulating or distributing the stock, and more. Enhancements have made the tool faster and easier to use when evaluating stocks and making buy and sell decisions.

“Our collaboration with TipRanks will yield significant benefits for our users,” NAGA CMO Valentin Ilioi said. “These enhancements represent our commitment to providing innovative tools that give our traders a competitive edge. By continually improving our platform with TipRanks’ insights, we’re ensuring NAGA remains at the forefront of social trading innovation.”

All-in-one trading platform NAGA facilitates trading and investing in more than 4,000 assets including CFDs on stocks, Forex, indicies, commodities, exchange-traded funds (ETFs), bonds, and cryptocurrencies. NAGA also offers social trading which includes an Autocopy tool that enables traders and investors to benefit from the experience of other traders and investors by following and copying their market moves. With more than 1.5 million users on its platform, NAGA is headquartered in Hamburg, Germany, and was founded in 2015.

Founded in 2012, TipRanks won Best of Show in its Finovate debut at FinovateSpring 2013 in San Francisco. The startup scored a second Best of Show award when the company returned to the Finovate stage for FinovateFall later that same year. Most recently, the Tel Aviv-based firm launched Spark AI, a comprehensive AI-powered stock analyst solution that provides data-driven insights on penny stocks and blue chip equities alike. The technology generates reports that detail strengths, risks, financials, and peer comparisons to give traders and investors the information they need in order to make better buy and sell decisions in the market.

Yesterday, Donald Trump signed an Executive Order (EO) to modernize the U.S. payments system by phasing out paper checks. The EO mandates that the Federal government will stop issuing paper checks for all disbursements starting September 30, 2025.

The EO, which is targeting waste, fraud, and abuse, will offer both banks and fintechs opportunities and challenges as they seek to bring digital banking to underbanked consumers who need to send payments to and receive payments from the federal government.

So as you begin your second quarter planning initiatives, here are a few things you’ll need to know about this week’s Executive Order.

Real time payments become solidified

Banks’ adoption of FedNow and The Clearing House’s RTP is increasing, and so are consumer expectations for faster fund transfers. This week’s EO stipulates the move to “fast, electronic payments,” which will change the expectations of even underbanked and elderly populations that rely on government monetary benefits.

Heightened emphasis on payment security and fraud prevention

The Fact Sheet detailing the EO specifically cites security and fraud prevention as major reasons for modernizing US payments. “President Trump is cracking down on waste, fraud, and abuse in government by modernizing outdated paper-based payment systems that impose unnecessary costs, delays, and security risks,” the Fact Sheet said. The move will ultimately bring stricter standards to government payments and will help foster consumer trust.

A shift toward digital identity verification

As payments digitize, reliable identity verification methods will become increasingly crucial. While bringing payments into the digital space will help boost KYC and AML verifications, it will also offer opportunities for fraudsters to create new scams. As an example, non-digitally native consumers may be more likely to fall victim to phishing attacks that they perceive to be payments from the federal government.

Not everyone is required to make the change

The EO states that exceptions will be made for people without banking or electronic payment access, in specific emergency payments cases, for certain law enforcement activities, and for other special cases that qualify for an exception.

Consumer awareness is key

The EO explains that, prior to the September 30 deadline, the government will initiate a comprehensive public awareness campaign to inform federal payment recipients of the shift to electronic payments. Banks should work alongside these campaigns with public awareness initiatives of their own to offer guidance on setting up digital payments and mitigating fraud.

Overall, this new EO represents a significant opportunity for banks and fintechs. By accelerating the shift to digital payments, the EO underscores the value of digital-first strategies and positions banks in a great place to attract new customers who previously relied on paper checks.

Banks and fintech companies that proactively support consumers during this transition—through seamless onboarding, education, fraud prevention, and robust digital identity verification—can strengthen their market position, deepen customer relationships, and foster long-term trust. Ultimately, the shift away from paper checks will reinforce existing efforts toward financial inclusion, drive consumer adoption of digital tools, and encourage innovation across the payments landscape.

Mercury raised $300 million in Series C funding, bringing its total investment to $452 million and boosting its valuation to $3.5 billion.

The round, which was led by Sequoia Capital, includes both primary (growth) and secondary (stakeholder liquidity) funding.

Mercury differentiates itself by offering integrated digital banking solutions for startups and SMBs, positioning it as a direct competitor to Brex and Ramp.

Business banking fintech Mercuryunveiled today that it closed a $300 million funding round, rocketing the company’s total raised to $452 million. The Series C investment round was led by new investor Sequoia Capital and saw participation from other new investors Spark Capital and Marathon, as well as existing investors Coatue, CRV, and Andreessen Horowitz.

The round includes both primary and secondary funding. This means that not only will the company have funds to use for growth, but it will allow early stakeholders the opportunity to cash out part of their investments. The investment also boosts Mercury’s valuation. The California-based company is now valued at $3.5 billion, which is more than double its 2021 valuation of $1.6 billion.

Mercury was founded in 2017 and has since focused on serving small businesses and investors. In 2022, the company launched its corporate card. Two years later, Mercury expanded once again to launch financial tools to help companies pay bills, send invoices, automate accounting, and manage employee expenses.

Today, the company helps more than 200K businesses and entrepreneurs access banking tools, credit cards, and software they need to manage their financial workflows. Among Mercury’s customers are startups like Linear, Phantom, and ElevenLabs, as well as venture capital firms and e-commerce companies like Cocolab and Bogey Bros.

When Silicon Valley Bank (SVB) collapsed in 2023, Mercury saw $2 billion in client deposits from entrepreneurs seeking an alternative banking option. Today, the digital bank retains 95% of those funds. In fact, Mercury’s handling of the SVB collapse was what gained it the attention of Sequoia, the lead new investor of today’s round.

“Mercury began with the vision that banking should do more than safely hold money – it should bring all the ways people and businesses use money into a single product that feels extraordinary to use,” said company CEO and Co-Founder Immad Akhund.

Along with its funding announcement, Mercury also unveiled key financial growth milestones, including:

Ten consecutive quarters of profitability based on both EBITDA and GAAP net-income

$500 millionin revenue in 2024

40% growth in customers year-over-year

$156 billionin annual transaction volume, up 64% year-over-year

Last year, Mercury introducedMercury Personal, a digital bank account that offers a personal bank account for users who want self-serve banking and a high-quality product experience to optimize their personal finances. Mercury Personal is slated to launch later this year.

“Mercury is a disruptive company with a bold vision for the future of banking,” said Sequoia Capital Partner Sonya Huang. “It has been synonymous with banking for startups, but Mercury is built for nearly every business and is a real competitor to legacy banks. With its track record of profitability, innovation, operational excellence, and clear vision for what banking can become, I believe that Mercury has a chance to be a generational company at the intersection of financial services and software.”

Mercury sits in the same arena as competitors Brex and Ramp. However, Brex and Ramp have carved out niches through corporate credit cards and expense management solutions aimed at high-growth startups and larger enterprises, while Mercury differentiates itself by delivering more of a comprehensive digital banking solution with integrated financial management software tailored to early-stage startups and entrepreneurs.

Credit card-linked installment payments solutions company Splitit launched its embedded Shopify app.

The new app, Splitit Card Installments, gives merchants a one-click installment payment experience without redirects or applications.

Splitit made its Finovate debut in 2014 (as PayItSimple USA). The company rebranded as Splitit in 2015.

Card-linked installment payment solutions company Splitit has unveiled its embedded Shopify app: Splitit Card Installments. The new offering gives merchants an all-in-one service that includes credit card processing along with a seamless one-click installment payment experience for consumers that doesn’t require redirects or applications.

“Our Embedded Shopify App marks a transformative leap in the installment payment landscape,” Splitit CTO Ran Landau said. “By seamlessly integrating into the Shopify checkout, we’ve eliminated the friction typically associated with pay-over-time solutions, a key factor in cart abandonment. This white-label approach empowers merchants to offer branded, one-click installment options while maintaining full control over their customer journey and data. For shoppers, it provides unparalleled convenience, allowing them to easily manage their finances without leaving the merchant’s ecosystem.”

The new app is embedded into the Shopify checkout flow, and gives consumers the option to pay in full or by installments directly within the credit card section. A white-label solution, Splitit Card Installments gives merchants control over both their brand identity and customer relationships. There is no distracting third-party branding and all first-party consumer data remains with the merchant. The app is available to shoppers in more than 100 countries who will benefit from access to localized payment options. Merchants benefit from accessing a more diverse, global customer base, as well as new markets and revenue streams.

“This innovation not only enhances the customer experience but also presents a significant opportunity for merchants to acquire and retain customers in an increasingly competitive e-commerce landscape,” Landau added.

Splitit made its Finovate debut (as PayItSimple USA) at FinovateFall 2014. The company rebranded as Splitit the following year in an effort to “better align the Company’s brand with its overall strategy and product offering.” Since then, the company has grown into a major Installments-as-a-Service provider serving many of Internet Retailer’s top 500 merchants. Additionally, Splitit’s solutions are accepted by more than 1,500 ecommerce merchants in 30+ countries and by shoppers in 100+ countries.

Splitit’s new app launch news comes just days after the company announced a partnership with modern card issuance company and fellow Finovate alum Highnote. Courtesy of the partnership, Splitit will leverage Highnote’s tokenized virtual cards to pay merchants and provide real-time functionality that enables Splitit to offer consumers a new option for paying over time. This allows consumers to use their digital wallets to access Splitit’s card-linked, embedded, installment payment options. The process features a low-friction, pay-later approval flow that eliminates the need for a credit check by referencing the consumer’s existing available credit.

Splitit CEO Nandan Sheth praised Highnote’s platform for its “flexibility, scalability, and security.” He added, “This partnership allows us to offer shoppers a seamless and efficient way to make payments over time, directly within their digital wallets or at merchant checkout, further simplifying the shopper journey.”

Headquartered in Atlanta, Georgia, Splitit also maintains an R&D center in Israel and offices in London. The company was founded in 2012.

LoanPro and NovoPayment have teamed up to help expand access to credit for consumers in Latin America.

The partnership integrates LoanPro’s credit ledger and origination, servicing, and collections technology with NovoPayment’s API-based issuing processing.

Utah-based LoanPro made its Finovate debut at FinovateSpring in 2021.

Modern credit platform LoanPro and financial infrastructure provider NovoPayment have announced a partnership to help boost access to credit in Latin America. The two companies will give financial institutions and fintechs throughout the region an integrated, end-to-end infrastructure that can support credit and lending products of virtually any class.

The integration will give FIs and fintechs access to a suite of solutions to boost their own credit offerings. These solutions include LoanPro’s Transaction Level Credit product, which facilitates the assignment of unique repayment terms, fee structures, and interest rates to individual transactions. This helps institutions offer customers personalized credit solutions, and enables different categories of transactions to feature different interest rates and financial terms.

FIs and fintechs will also benefit from NovoPayment’s cloud-native platform that puts real-time processing, robust security, event-driven architecture, and an API-first approach to work to deliver low-latency transactions and automated failover. This further supports the ability of companies to offer customized credit solutions.

“Access to credit is a cornerstone of true financial inclusion,” NovoPayment CEO Rodrigo Rodas said. “NovoPayment’s trajectory has been defined by our commitment to bridging financial gaps through innovative infrastructure solutions. Partnering with LoanPro enables us to empower financial institutions and fintechs across Latin America, providing them with the tools to offer diverse credit products and foster economic growth in the region.”

The partnership between LoanPro and NovoPayment comes at a time when modernization in banking and financial services infrastructure in Latin America is increasingly lagging behind the expansion of the financial services market as a whole. In a statement, the companies noted that while financial inclusion in Latin America has made significant gains from 2021 to 2024, with 28% of adults reaching an “advanced level of financial inclusion,” millions still lack access to modern credit and lending solutions. This issue is all the more acute due to the inability to scale those products financial institutions do offer. The integration of NovoPayment’s issuing processing with LoanPro’s credit ledger and origination, servicing, and collections solutions directly addresses these challenges.

“NovoPayment has been at the forefront of enabling financial innovation across Latin America, and their work aligns perfectly with LoanPro’s mission to modernize credit,” LoanPro CEO and Co-Founder Rhett Roberts said. “By bringing LoanPro’s lending technology into NovoPayment’s ecosystem in Latin America, we’re giving financial institutions and fintechs the tools they need to offer credit with confidence and compliance at the core.”

A leading payment processor for markets throughout Latin America, NovoPayment enables businesses and financial institutions to launch and scale their digital banking and payment offerings. The company processed more than 310 million transactions in 2024 and operates in 15 markets. Founded in 2007, NovoPayment is headquartered in Miami, Florida, and has offices in Mexico, Colombia, Peru, and Ecuador.

LoanPro made its Finovate debut as part of our all-digital FinovateSpring conference in 2021. That same year, the company also participated in our developers conference, FinDEVr 2021. Headquartered in Farmington, Utah, and founded in 2016, LoanPro serves more than 600 financial organizations, providing them with a modern credit platform that gives financial institutions and fintechs the infrastructure to manage lending and credit programs at scale, including loan origination, servicing, and collections.

FinovateSpring 2025 comes to sunny San Diego, May 7 through 9 at the Sheraton San Diego Hotel and Marina. Pick up your ticket today and take advantage of early-bird savings!

Trek partnered with Gr4vy to power an online-to-offline payment experience, offering consumers accurate inventory checks and simplified checkout.

Gr4vy’s payment orchestration dynamically routes transactions, which reduces friction, increases authorization rates, and allows Trek to manage multiple merchants efficiently.

Gr4vy provides Trek with a no-code, cloud-native platform to quickly implement diverse payment methods, comply with data laws, and enhance fraud prevention.

When it comes to buying bicycles and cycling accessories, consumers often prefer a shopping experience that takes place in multiple channels. To better accommodate these changing preferences, bicycle manufacturing company Trek has selected payments infrastructure-as-a-service (IaaS) company Gr4vy to power an online-to-offline payment experience that enables consumers to Buy-Online-Pickup-In-Store (BOPIS).

BOPIS has grown with the surge in ecommerce, along with heightened expectations of consumers, who prefer to order online and pick up in-store. In fact, 50% of shoppers select online stores based on in-store pickup availability. These changes in preferences, however, come at the same time that retailers and manufacturers are facing payment processing and inventory management challenges that pose checkout issues and stock shortages. To successfully execute BOPIS, retailers must ensure accurate inventory updates and a reliable payment system.

Gr4vy is partnered with online-to-offline shopping API solution Locally to enable Trek to show real-time inventory data from its network of retailers. This visibility allows shoppers to check stock availability on Trek’s website and complete the transaction online, while picking the item up in-store.

“Our goal is to give enterprises full control over their payment processes while removing unnecessary complexity,” said Gr4vy Founder and CEO John Lunn. “Ultimately, simplifying payments, so merchants can focus on what truly matters—growth.”

With its payment orchestration system, Gr4vy dynamically routes transactions to the optimal payment service provider to help reduce friction and increase authorization rates. When a customer completes their purchase, Trek and the local retailer receive the transaction details, and the customer can pick up their item in the store. Gr4vy’s dynamic payment routing helps Trek manage online and in-store transactions across multiple merchants of record.

Gr4vy also gives Trek a no-code method of adding multiple payment options, including digital wallets, Buy Now, Pay Later (BNPL), and alternative payment methods. “Partnering with Gr4vy has transformed how we approach payments, enabling us to seamlessly integrate options like BNPL and local shop inventory in a single checkout experience,”explained Trek Vice President of IT and Digital Steve Novoselac.

Gr4vy is cloud-native, PCI Level 1-compliant, and enables merchants to set up dedicated instances in specific regions to improve transaction speed and comply with data localization laws. Additionally, the API is set up to allow Trek to quickly implement new payment methods, currencies, and fraud prevention tools.

Founded in 2020, Gr4vy offers a platform that allows businesses to gain access to over 400 payment methods with a single integration. The platform also offers anti-fraud tools, and helps payment service providers optimize their payment stack without the need for IT expertise. In 2022, the California-based company was awarded Top Emerging Fintech Company at the Finovate Awards. Earlier this month, Gr4vy partnered with Australia-based New Payments Platform (NPP) Azupay to bring account-to-account payment solutions to Australian e-Commerce businesses.

Truework Intelligence, a new offering from income and employment verification technology company Truework, will provide mortgage lenders and property managers with a fully automated and comprehensive verification platform. The solution provides automatic orchestration, data standardization, and insights to provide an end-to-end verification experience that leverages new data methods, predictive modeling, and more.

“We started Truework to reinvent the way consumer data was collected and processed for maximum security and accuracy,” Truework CEO and Co-Founder Ryan Sandler explained. “From the early days, machine learning was a core part of our product. It has continued to evolve over time, both through internal modeling efforts and the latest external technologies. The Intelligence Platform is the result of this evolution to truly serve as a single solution for customers.”

Truework Intelligence replaces homegrown vendor “waterfalls” and related internal processes, removing guesswork and giving customers a plug-and-play verification solution. Among the platform’s features are the addition of bank income and tax transcripts to its current data methods, and predictive modeling for report turnaround times and the likelihood of report completion. This second feature of Truework Intelligence helps provide transparency and insights into the verification process and adds to the platform’s existing machine learning models that extract and parse data for accuracy and estimate the accuracy of income based on employment information.

“It’s not about returning the first data set we find,” Sandler added. “That’s what everyone else does. And it doesn’t work. It makes organizations leverage subpar vendors to fill data gaps. We are looking at the bigger picture by providing an accurate and complete picture of every consumer, using technology to handle data with trust and attention to detail.”

Truework’s product news comes just a few weeks after the company announced that it was working with TransUnion. The collaboration is designed to give mortgage lenders better and more reliable access to the verification of income and employment data they need to accelerate and enhance underwriting while keeping costs low. As part of the partnership, Truework’s TruVision Income and Employment Verification solution is now available via the TransUnion API. TruVision gives lenders access to instant data from more than 48 million active employee records, consumer-permissioned payroll (which covers 90% of employers in the US), as well as automated outreach to HR departments and third-party providers.

Also this year, Truework teamed up with another fellow Finovate alum—BlendLabs—to make income and employment verification technology available across both home lending and consumer banking. Blend Labs integrated Truework’s intelligent verification of income and employment technology directly into its consumer banking and home lending products in order to provide faster borrower approvals and much broader income and employment data coverage.

“Building a best-in-class lending experience means bringing together the right technology partners to streamline every step of the process,” Blend Co-Founder Nima Ghamsari said. “Partnering with Truework strengthens this commitment by delivering more seamless and comprehensive verifications, helping lenders drive efficiency and provide faster, more reliable approvals for their customers.”

Truework made its Finovate debut at FinovateFall 2021 in New York. At the conference, the San Francisco, California-based company demonstrated how its API enables developers to automatically verify income and employment data for any US employee. The company showed how its front-end widget, Truework.js, powered by the Truework API, allows users to log in to their payroll accounts and share source-of-truth data for those instances when their records are outside of Truework’s network of 35 million employees.

Users of Truework’s technology include eight of the top ten lenders in the US by origination volume. The company noted that its solutions have helped mortgage lenders across the country lower costs by 50% and achieve average completion rates of 75%. The company was founded in 2017.

Chime has launched Instant Loans, a micro-lending product offering up to $500 instantly with a fixed interest rate of 29.76%, without credit checks.

When members repay these loans on time, it can help boost their credit scores by 10 to 30 points, as Chime reports on-time payments to credit bureaus.

The Instant Loans product complements Chime’s existing suite of financial tools targeted toward middle-income users, including MyPay (paycheck advances) and SpotMe (fee-free overdrafts).

Neobank mega-competitor Chimeannounced that it has launched Instant Loans, a new product that allows users to access to up to $500 in funds instantly with a fixed interest rate.

The Instant Loans are three-month installment loans of up to $500 available to Chime members who receive direct deposits to their Chime Checking Account and are pre-approved, with no credit check required. To underwrite the loans, Chime uses its own technology combined with its own unique data sources.

Chime will notify members who are pre-approved within the Chime app and if a customer chooses to access the funds, they pay a fixed interest rate of $5 for every $100 borrowed and repay the funds in three monthly payments of $35 per $100 borrowed. This equates to an interest rate of 29.76%.

When consumers repay on time, they can potentially build up their credit, as Chime reports each on-time payment to credit reporting agencies. According to Chime, customers who pay on time may see their credit score increase by 10 to 30 points.

“We are relentlessly focused on helping everyday people achieve financial progress,” said Chime Chief Product Officer Madhu Muthukumar. “Our members have told us that they want simple and transparent tools to access money when they need it, and to help them build credit — and we’re excited Instant Loans provides both to our members.”

Chime was founded in 2012 and is well known in fintech for offering tools and services that cater to lower-to-middle income consumers. The challenger bank is best known for its earned wage access tool that allows users to receive their paycheck up to two days earlier when they set up direct deposit, but Chime also offers a credit-building tool and a feature that will spot users up to $200 to avoid account overdrafts.

Today’s launch of high interest micro-loans is a perfect fit for Chime, which aims to create transparency in lending with the fixed interest rate. The new Instant Loans product sits in Chime’s portfolio of other micro-loans, including MyPay, which is a paycheck advance product that allows members to access up to $500 of their check before payday with no interest; and SpotMe, which allows members to overdraft without fees.

The rage over regtech is real. In response to growing customer demands, emerging financial crime threats, and attempts by regulatory bodies to manage both of these developments, the field of regulatory compliance has never been more topical in financial services.

To this end, we interviewed banking and financial services compliance veteran Tracy Moore. Director of Thought Leadership & Regulatory Affairs at Fenergo, Moore joins the Finovate blog to provide her perspective on the regulatory environment for banks, fintechs, and financial services companies in 2025.

As part of Finovate’s commemoration of Women’s History Month, we also discuss issues of gender diversity in banking and financial services, and the role of mentorship in helping foster future leaders in the industry.

Can you tell us a little about yourself and the work you do at Fenergo?

Tracy Moore: I began my career in corporate legal training, specializing in finance and treasury transactions. My journey took me to Europe, where I transitioned into banking, spending much of my career in legal and compliance roles at global financial institutions. Upon returning to the U.S., I continued this path at a super-regional bank, gaining extensive experience in regulatory compliance and financial crime risk management.

Today, I serve as the Director of Thought Leadership & Regulatory Affairs at Fenergo, the global leader in Client Lifecycle Management (CLM) technology for financial institutions. In this role, I focus on financial crime risk management, regulatory change, and digital transformation, helping institutions solve for complex regulatory environments while enhancing operational efficiency.

I am deeply passionate about influencing industry change and driving technological advancements that make the financial sector safer and more resilient. My work involves collaborating with global regulators, financial institutions, and technology providers to develop innovative solutions that protect the industry against financial crime. I help connect regulation and technology to shape the future of compliance and risk management in today’s financial landscape.

What is it about the field of banking compliance that you find most interesting professionally?

Moore: I find it fascinating how geopolitical events shape the global financial industry, influencing not just regulatory frameworks but also presenting new challenges, such as financial crime and evolving risk landscapes. Today’s economy is so interconnected, and this means that financial institutions must constantly shift to address challenges such as sanctions, emerging threats, and evolving compliance requirements.

What truly interests me is the delicate balance financial institutions must strike meeting regulatory expectations, staying ahead of increasingly sophisticated bad actors, driving revenue growth, and ensuring safe financial services for their clients. Achieving this balance requires a combination of strategic foresight, innovation, and collaboration across the industry. Everyday has a new perspective and new challenges.

How has banking compliance changed over the course of your career in the industry?

Moore: Looking back over the past 25 years, the evolution of banking compliance has been nothing short of dramatic. When I started my career, compliance was often seen as a back-office function, more about checking boxes than driving change. Fast forward to today, and compliance has become a core pillar of financial institutions, shaping everything from risk management to customer experience.

One of the biggest shifts of course has been technology advancements. Alongside this, the sheer pace and complexity of regulatory change. Events like 9/11, the 2008 financial crisis, and major geopolitical shifts have completely reshaped the regulatory landscape. We’ve moved from more localized, paper-based processes to a hyper-digital, data-driven, and globally interconnected approach to compliance.

As a woman in this industry, I’ve also witnessed the growing role of diverse leadership in compliance and risk management. The field has evolved beyond traditional legal and audit backgrounds to welcome technologists, data analysts, and strategic thinkers, many of whom are women bringing fresh perspectives to a historically male-dominated space.

Issues (and innovation) in banking compliance have never been more top of mind. How have we arrived at this point, and is it a good thing for banks and their customers?

Moore: We’re here because the stakes have never been higher. Over the past two decades, a mix of financial crises, evolving threats, digital disruption, and geopolitical shifts has pushed compliance to the forefront. Regulators have responded with increasingly complex expectations, bringing the role of compliance into strategic planning for financial institutions.

This pressure has fuelled innovation.

AI, automation, and data analytics are transforming compliance, reducing manual processes, improving risk detection, and enhancing the customer experiences. Banks are now able to onboard clients faster, monitor activity in real time, and anticipate threats before they escalate.

For banks, it’s both a challenge and an opportunity. Compliance is tougher than ever, but those who embrace technology can gain a competitive edge. And for customers stronger compliance means better security, smoother transactions, and more trust in the system.

Seeing this shift firsthand is what lead me to make the decision to leave the traditional compliance role in banking and join Fenergo because I knew technology would be the driving force behind the future of compliance, and I wanted to be part of this transformation.

How do AI and automation create new compliance challenges for banks? In what ways can firms use these technologies to address compliance issues?

Moore: AI and automation can streamline compliance, but they also raise concerns both from regulators and banks themselves. Many institutions are skeptical, worrying about black-box decision-making, regulatory scrutiny, and potential biases.

The key challenge is explainability. Regulators need to understand how AI-driven decisions are made, so firms must prioritize transparency, clear documentation, and strong oversight.

That said, when used responsibly, AI can enhance risk detection, automate manual tasks, and improve compliance efficiency. The solution lies in communication by working with regulators to ensure AI models are interpretable, auditable, and aligned with compliance standards.

What areas of banking compliance do you think deserve more attention than they are getting?

Moore: Emerging digital assets and global regulatory alignment are two areas that need far more attention in banking compliance. The rapid rise of crypto, tokenization, and digital payments has outpaced regulatory frameworks, leaving financial institutions in a tough spot. How do you innovate while staying compliant in an environment where the rules are still being written? Without clear, consistent guidelines, banks are hesitant to fully engage, creating uncertainty for the entire industry.

At the same time, jurisdictional differences make compliance incredibly burdensome in today’s global economy. Financial crime doesn’t stop at borders, but regulations do, forcing banks to navigate a patchwork of requirements that slow down operations and increase costs. More global alignment and collaboration between regulators could ease this burden, ensuring that compliance is both effective and practical in a world where money moves faster than ever.

And lastly, the evolving nature of financial crime. Criminals are getting more sophisticated, using everything from deepfake identities to crypto mixing services to evade detection. Compliance programs need to move beyond traditional rule-based approaches and embrace real-time, predictive intelligence to stay ahead.

What are your thoughts on the progress made—or not made—toward greater gender diversity in banking in recent years? Are you optimistic about the future of women in banking, particularly in areas like compliance?

Moore: Women in banking, especially in compliance, have made progress, but not nearly enough. Too often, diversity is overlooked as a business advantage instead of recognized for the value it brings. In today’s geopolitical and financial environment, organizations need diverse perspectives to navigate risk and drive innovation, yet those perspectives are still dismissed.

Despite this, I am optimistic. Women are smart, resilient, and persistent. We continue to prove our expertise in ways that cannot be ignored. Compliance is an area where women thrive because it demands strategic thinking, problem-solving, and leadership under pressure.

Real change will happen when companies move beyond surface-level efforts and embrace diversity as a competitive advantage. Women will keep breaking barriers, whether the industry is ready or not.

Mentorship can play a key role in helping women entering financial services or launching fintechs. Did mentorship play a significant role in your early career? What message would you give to banking and financial services professionals when it comes to sharing their insights and experience as mentors?

Moore: Mentorship has been invaluable in my career. I have always sought out mentors and sponsors—both men and women—who could guide my development and challenge me to grow. Beyond that, I have chosen a personal board of directors: female professional leaders across various industries who have provided insight, support, and perspective at every stage of my journey.

For those in banking and financial services, mentorship is more than just giving advice or sharing a coffee. It is about opening doors, advocating for talent, and sharing real, honest experiences. The next generation of female leaders is watching and learning. It is up to us to make sure they feel supported, empowered, and ready to step forward.

It’s been nearly a year since we celebrated the innovators crowned Best of Show winners at FinovateSpring 2024. As we gear up for our upcoming FinovateSpring 2025 event in sunny San Diego, taking place May 7 through 9, we’re taking a moment to reflect on the impressive achievements of last year’s standout demo companies. These fintechs have continued their momentum from FinovateSpring by making waves in the fintech industry.

Business Insider listed Cascading AI as one of 15 Most Promising AI-Powered Fintech Startups to Watch in 2025.

Gartner identifies Casca as a key vendor for GenAI in lending.

Prosperity Now announces Lukas Haffer, CEO and Co-founder of Casca, as second place award winner of the RISE Challenge Award for its solution to improve loan assistance and identification.

Cascading AI featured in AI in Business Lending Report fro Datos Insights.

Finopotamus features how Remynt rethinks debt collection.

Fox 26 interviews Remynt Founder and CEO Gwyneth Borden on the state of debt in Texas.

Badcredit.org highlights how Remynt brings empathy to collection practices.

FinovateSpring 2025 kicks off May 7 through 9 in San Diego, California. Visit our FinovateSpring hub today to learn more about our emerging speaker lineup, demoing companies, and how to plan your visit to Finovate’s first conference in SoCal!

The first full week of spring is bringing news of partnerships in fraud prevention, lending, and insurtech as well as new product launches in regtech and payments. Be sure to check Finovate’s Fintech Rundown all week long for the latest in updates and announcements in fintech.

Fraud prevention and identity verification

Wisconsin-based community bank IncredibleBank partners with Alloy to enhance its account opening process.

Income and employment verification technology company Trueworkannounces enhancements to its Truework Intelligence platform.

Regtech

Financial services compliance company Thistle Initiativeslaunches its integrated Risk Management as a Service (RMaaS) solution.

Vanquis Banking Group choosesFinScan to help optimize AML processes and strengthen financial crime risk management.

Encryption and tokenization technology payments company Bluefinteams up with Printec Group to bring its PCI-validated, point-to-point encryption solution to retailers in Europe.

Somalia launches its first national instant payment system powered by BPC.

Blackhawk Network and Exchange Solutions partner to offer robust data-driven consumer loyalty program capabilities.

AstroPayexpands access to multicurrency wallet across Latin America.

Splititunveils first fully embedded white-label installment solution for Shopify merchants.

Grazzy teams up with U.S. Bank’s debit card program simplifies the way tipped employees earn and receive digital tips.

Digital banking

Canada’s largest federal credit union, Coast Capital, launches its new digital commercial banking platform courtesy of its partnership with ebankIT.

Credit Union 1 selectsnCinoto power omnichannel experiences for members.

This week’s edition of Finovate Global looks at recent fintech headlines from the South American countries of Argentina, Brazil, and Uruguay.

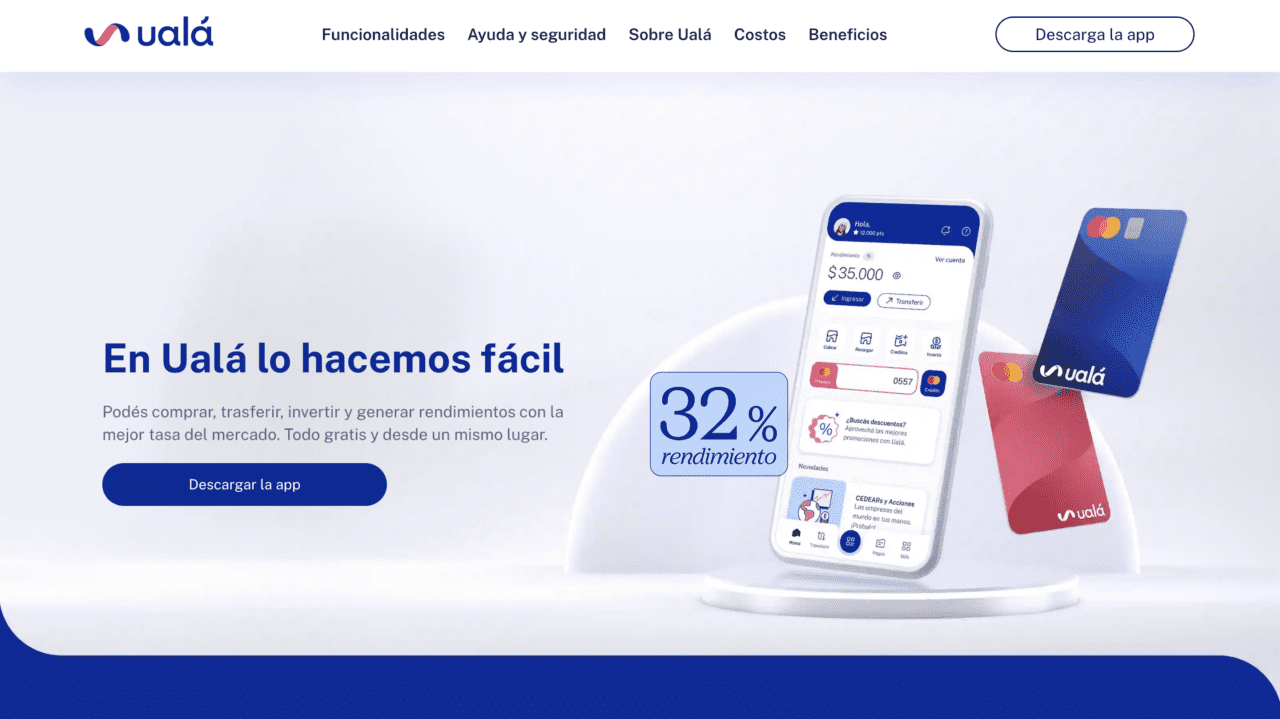

Ualá Raises $66 Million at $2.75 Billion Valuation

In a funding round that featured participation from Mexican media titan TelevisaUnivision, Argentina-based fintech Ualá has added $66 million in funding to its Series E round. The additional funding brings the round’s total to $366 million and gives the company a valuation of $2.75 billion.

The capital comes via an equity sale and will be used to fuel Ualá’s growth throughout Latin America—with a particular emphasis on expansion in Mexico. Ualá Founder and Chief Executive Officer Pierpaolo Barbieri praised the participation of TelevisaUnivision, which he called a “very relevant and influential outlet, across Spanish-speaking markets but especially in Mexico.” Barbieri added, “It will help us create confidence and closeness with a lot of Mexicans that still don’t know us.”

The first close of the Series E round was led by Allianz X, German insurance company Allianz SE’s venture capital arm. Also participating in the first close were Stone Ridge Holdings Group and Pershing Square Foundation. Additional investors in the extension round were not named.

Founded in 2017 in Argentina, Ualá offers financial services including payment accounts connected to an international Mastercard prepaid card, as well as savings accounts, loans, investments, business collection solutions, and more. The company has nine million users in the region, including in countries such as Argentina, Colombia, and Mexico.

Ualá began the year by announcing the availability of six new mutual funds in its ecosystem, including one fund denominated in dollars. In February, the company integrated an advanced artificial intelligence platform, powered by OpenAI’s GPT-4, into its customer service process.

dLocal partners with Temu, Belmoney

Uruguayan fintech and cross-border payments company dLocal announced a pair of partnerships in recent days. First, dLocal launched a new collaboration with Europe-based, remittance-as-a-service (RaaS) provider Belmoney. The goal of the partnership is to facilitate cross-border payouts, leveraging the integration of more than 900 local and alternative payment methods (APMs) such as credit and debit cards, bank transfers, and instant transactions. The collaboration is also designed to boost service reliability and efficiency for those making cross-border transactions in countries including Bangladesh, Ecuador, Peru, and Pakistan.

“Our partnership with dLocal is a game-changer in the remittance space,” Belmoney CEO and Founder Bruno Pedras said. “By integrating with dLocal’s comprehensive network, we can significantly lower costs, improve transaction speeds, and provide a better cross-border payments experience for both senders and recipients.”

Second, dLocal announced that it has formed a strategic partnership with Temu, the international e-commerce platform of China’s PDD Holdings. Together, the two companies seek to provide shoppers in Africa, Asia, and Latin America with new seamless and secure payment options that are suited to local preferences. Millions of customers in 15 emerging markets in these regions stand to benefit from the collaboration.

“By partnering with dLocal, we’re excited to extend these benefits to millions of customers in emerging markets, ensuring that more people can enjoy accessible, convenient shopping experiences,” a Temu spokesperson said in a statement.

Launched in 2022, Temu is an online marketplace that offers consumer goods at significantly discounted prices. Shipping goods directly from the People’s Republic of China, Temu reportedly has more than 292 million monthly active users of its app worldwide. The app was among the most popular in US app stores for both iOS and Android in 2024.

Founded in 2016, dLocal is headquartered in Montevideo, Uruguay. The country’s first unicorn, dLocal offers an all-in-one payment platform that enables companies to accept and disburse a wide range of local payment methods and currencies. In 2024, the company processed more than $25 billion worth of payments. dLocal works with 700+ merchants, supports 900 payment methods, and operates in more than 40 countries. A publicly traded company on the Nasdaq exchange under the ticker DLO, dLocal has a market capitalization of $2.7 billion. Sebastián Kanovich is CEO.

Ant International’s Bettr brings embedded finances services to ecommerce merchants in Brazil

Speaking of partnerships between businesses in Asia and Latin America, we learned this week that Bettr, Ant International’s AI-driven lending business, has gone live in Brazil. Bettr will help expand lending opportunities for small and medium-sized enterprises (SMEs) by working with local partners such as AliExpress. Through this partnership, Bettr will introduce a new financing solution, Bettr Working Capital, for local merchants working on AliExpress’s platform.

“This collaboration reinforces our commitment to helping small and medium-sized businesses thrive by providing accessible and efficient financial tools that can take their operations to the next level,” LatAm director of AliExpress Briza Bueno said. “In this way, we are not only supporting the individual growth of these entrepreneurs but also contributing to the advancement of e-commerce in the country.”

Bettr Working Capital will be introduced gradually; the first round of disbursements began this week. The technology analyzes merchant sales records and other unstructured business data from AliExpress to make smarter, tailored, more affordable loan solutions. This will help small and medium-sized businesses better manage cash flow and expand into new markets.

Headquartered in Singapore, Ant International is an international digital payments and financial technology provider. Bettr is the company’s digital lending business, which specializes in serving micro, small, and medium-sized enterprises (MSMEs). The firm combines emerging technologies like AI and data-driven credit modeling to offer secure financial solutions that better fit borrower needs.

Here is our look at fintech innovation around the world.

Latin America and the Caribbean

Argentina-based fintech Uala raised $66 million at a valuation of $2.75 billion in an extended Series E round.

Remittance company Pomelo integrated with Visa clearing house in Mexico.

Asia-Pacific

Indonesian ride-hailing service InDrive teamed up with Singapore’s Fingular and Indonesia’s Sharia-compliant P2P lending platform Ammana to launch its new inDrive.Money app.

Malaysian wealth management platform Versa raised $6.8 million in Series A funding.

Japan’s international payment brand JCB partnered with integrated payment provider First Cash Solution, expanding JCB Card acceptance in Germany.

Sub-Saharan Africa

African payments technology giant Flutterwave integrated with Pay With Bank Transfer to support businesses in Ghana.

Mastercardextended its collaboration with London-based Paymentology to boost financial inclusion in South Africa.

Compliance and fraud prevention platform Sumsubannounced a partnership with the Association of Fintechs in Kenya.

Central and Eastern Europe

Lithuanian identity verification provider iDenfy announced a collaboration with mobility provider Evemo.

Estonian fintech Hoovi raised €8 million in funding via a structured bond issue from Finland’s Multitude International Bank.

Moldova-based digital wallet and electronic money institution (EMI) Paynet partnered with open banking services provider Salt Edge.

Middle East and Northern Africa

Israeli fintech FINQ became the first Israeli company to secure a US Securities and Exchange Commission (SEC) Registered Investor Advisor (RIA) license without relocating to the US.

Egyptian fintech Fawry inked a strategic agreement with Contact Financial Holding to expand access to Buy Now, Pay Later (BNPL) services.